The word tokenization is overused. It sounds like a magic formula that can upgrade any asset, attract new users, increase liquidity, and make everything feel like the future of finance. But beyond the buzz, few truly understand what makes tokenization actually valuable.

Tokenization, by itself, doesn’t make a bad asset good. It won’t turn an illiquid or unattractive investment into something people suddenly want to buy.

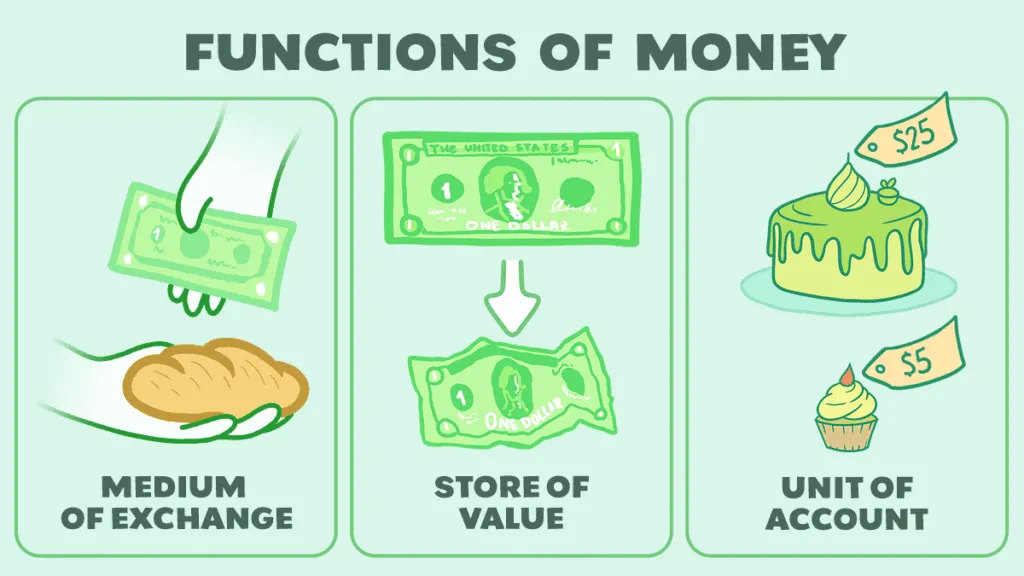

However, there’s one killer feature that makes tokenization feel like magic: it makes everything behave like “Money.” Money serves three essential purposes: It can be spent, saved, and valued.

Traditionally, assets like funds, equities, bonds, or venture capital shares are not money. You can’t easily spend them. They’re slow to convert into cash. And you can’t use them to compare value in real-time against other assets.

Tokenization is changing that, and lets look into this each functions with the market leader Securitize’s offerings.

The word tokenization is overused. It sounds like a magic formula that can upgrade any asset, attract new users, increase liquidity, and make everything feel like the future of finance. But beyond the buzz, few truly understand what makes tokenization actually valuable.

Tokenization, by itself, doesn’t make a bad asset good. It won’t turn an illiquid or unattractive investment into something people suddenly want to buy. In fact, if the liquidity and infrastructure around the tokenized asset are insufficient, the costs of maintaining it - custody, compliance, monitoring - can outweigh the benefits.

However, there’s one killer feature that makes tokenization feel like magic: it makes everything behave like “Money.” Money serves three essential purposes:

It can be spent or traded - as a medium of exchange.

It can be saved - as a store of value.

It can be valued - as a unit of account.

Traditionally, assets like funds, equities, bonds, or venture capital shares are not money. You can’t easily spend them. They’re slow to convert into cash. And you can’t use them to compare value in real-time against other assets.

Tokenization is changing that, and lets look into this each functions with the market leader Securitize’s offerings.

Source: What is Money? (History + Function) - WhiteboardCrypto

The first step toward making assets spendable is enabling them to move instantly, globally, and without friction.

In traditional finance, assets such as private equity shares, venture fund interests, or money market funds exist within fragmented silos. Their transfer requires custodians, transfer agents, and clearinghouses, operating only during market hours and often constrained by jurisdictional and regulatory barriers. The result is an ecosystem where ownership is static and liquidity is conditional.

Blockchain introduces a new foundation: a shared, programmable settlement layer. It allows regulated institutions to issue compliant tokens that preserve investor protections while gaining the fluidity and composability of digital assets. Instead of being confined to closed systems, tokenized instruments can now interact seamlessly across markets, protocols, and geographies.

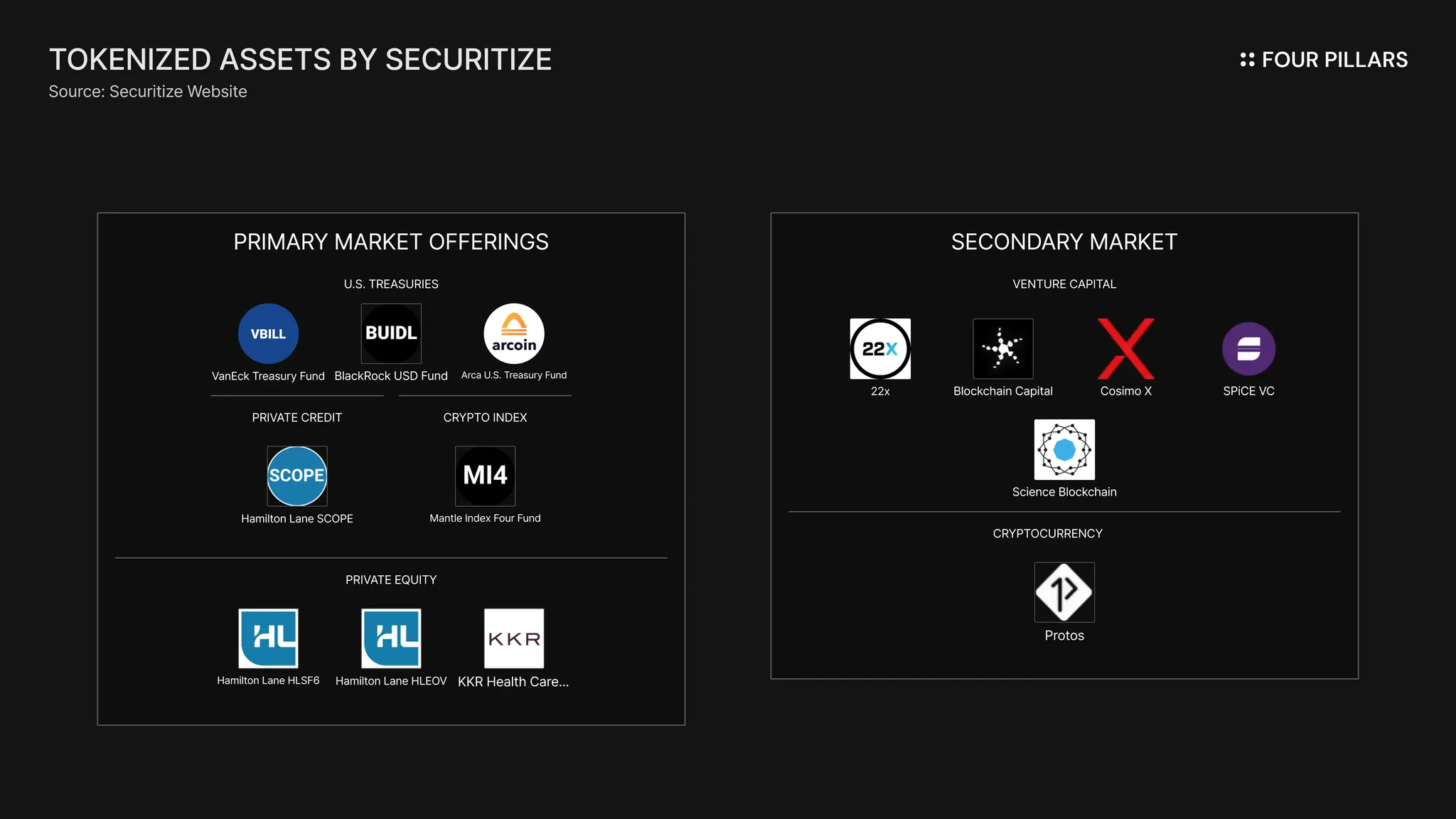

In this new architecture, tokenized assets behave like universal trading primitives. Whether it’s a stock, bond, fund, or other real-world asset, every token can move, trade, and settle on the same infrastructure. A single investor can now:

Exchange a tokenized Treasury fund (e.g., BlackRock’s BUIDL) for tokenized private equity shares (e.g., Hamilton Lane’s PE fund) or stablecoins (e.g., USDC) - all within the same onchain wallet.

Swap tokenized corporate bonds for crypto assets like ETH, BTC.

Swap tokenized real-estate to a tokenized VC fund (e.g. Blockchain Capital’s VC fund).

By turning static assets into programmable, composable units of value, tokenization platform like Securitize is turning private markets into public infrastructure - bridging the divide between institutional capital and onchain liquidity, into the world.

Ultimately, this interoperability extends beyond asset classes. It is beginning to connect entire financial systems, laying the groundwork for a world where every compliant asset can flow like “money.”

Source: The Leading Tokenization Platform

Source: X (@stablewatchHQ)

The second function of money is its ability to store value over time, to preserve purchasing power while potentially generating returns. Tokenization extends this idea by making traditionally static, illiquid holdings into onchain as self-custodial, yield-bearing assets that can be owned, tracked, and rewarded in real time.

Through tokenization, assets such as U.S. Treasury bills, corporate bonds, and money-market funds are not merely recorded on a blockchain; they become programmable stores of value that can distribute yield automatically to investors’ wallets. This fundamentally changes how value is saved - from passive holding to active, composable saving.

For example, BlackRock’s BUIDL Fund, issued and distributed by Securitize, represents tokenized shares of a U.S. Treasury money market fund. It automatically distributes yield daily to token holders, who can see their balance grow directly in their onchain wallet. This eliminates the friction of traditional fund accounting, dividend processing, and settlement delays - turning a conservative, institutional product into an always-on, blockchain-native savings vehicle.

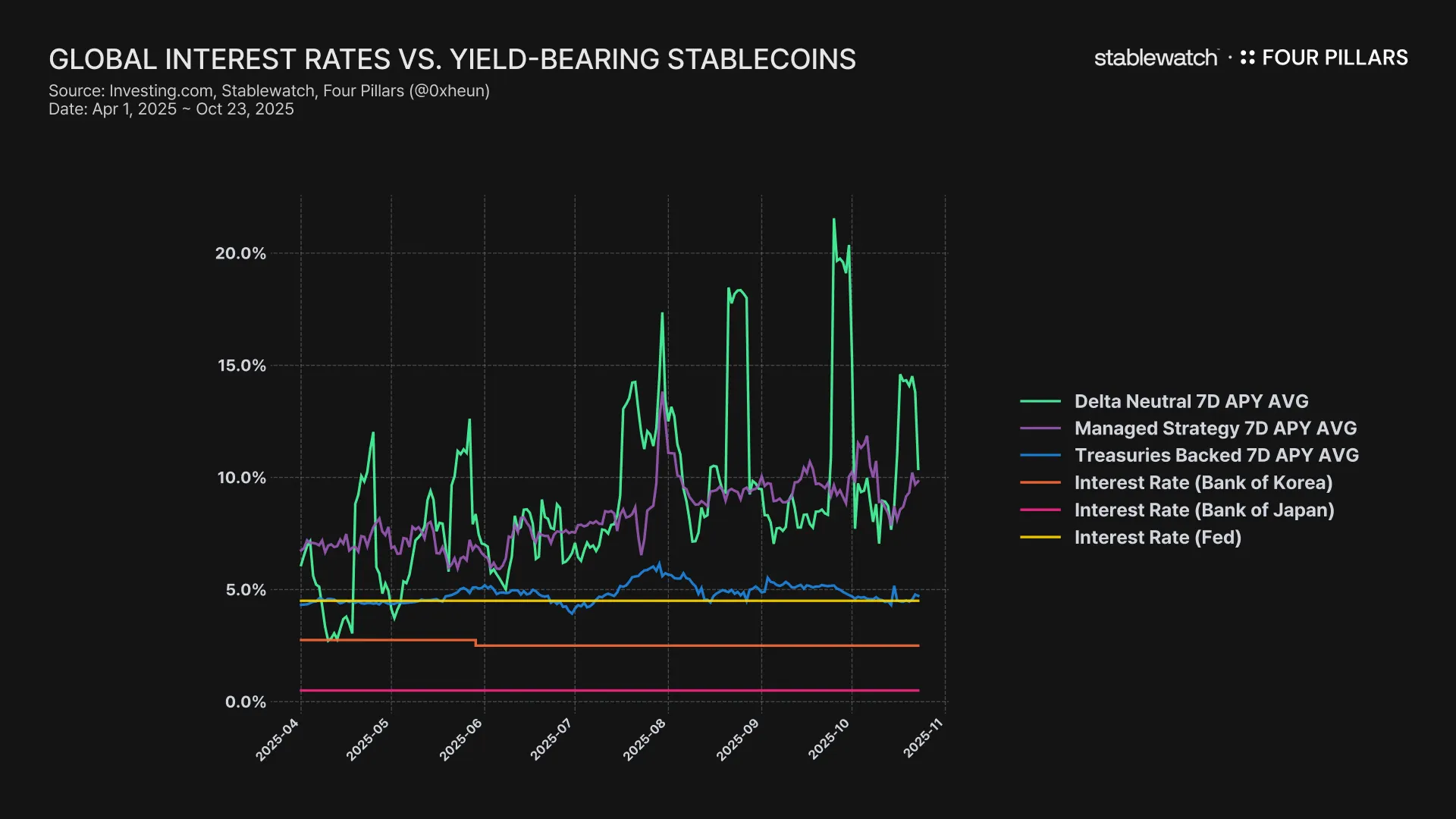

Onchain yields go beyond just replicating traditional interest rates. Once these assets are tokenized, they can be integrated into the broader onchain financial ecosystem - used as collateral in lending protocols, liquidity in automated market makers, or settlement reserves in payment rails. For instance, Institutions can programmatically allocate between multiple yield sources - for example, depositing BUIDL tokens into a repo-like onchain vault to earn extra basis-point spreads, similar to how banks manage liquidity portfolios.

This creates a new kind of “onchain yield curve,” where capital can flow frictionlessly between risk-free yields (like tokenized Treasuries) and higher-risk DeFi yields (like lending pools or structured vaults). In time, these onchain yields could serve as a benchmark for global digital interest rates, replacing traditional overnight indexes in tokenized markets.

As more tokenized funds emerge, these instruments will become the “savings accounts of the digital economy.” They combine the stability and trust of regulated securities with the efficiency, composability, and transparency of blockchain. This convergence allows both institutions and individuals to hold money that earns, moves, and compounds - seamlessly, across borders, and without intermediaries.

Source: Historical Yield Performance

The third function of money is to serve as a unit of account - a universal measure of value that enables consistent pricing, comparison, and settlement across markets. In traditional finance, this role is fulfilled by national currencies such as the dollar or yen. In the digital economy, this function is increasingly performed by “any tokenized assets.” Every pair could be made, and if mispriced, arbitraged.

In the on-chain world, each tokenized asset issued under the same contract is fungible and standardized. For example, shares of the tokenized Blockchain Capital VC Fund are identical regardless of where they are traded, and as cross-chain token standards like LayerZero’s OFT (Omnichain Fungible Token) become widely adopted, these tokens can also move seamlessly across different blockchains while preserving their identity and value. This cross-chain fungibility ensures that assets can be recognized and priced consistently throughout the on-chain ecosystem.

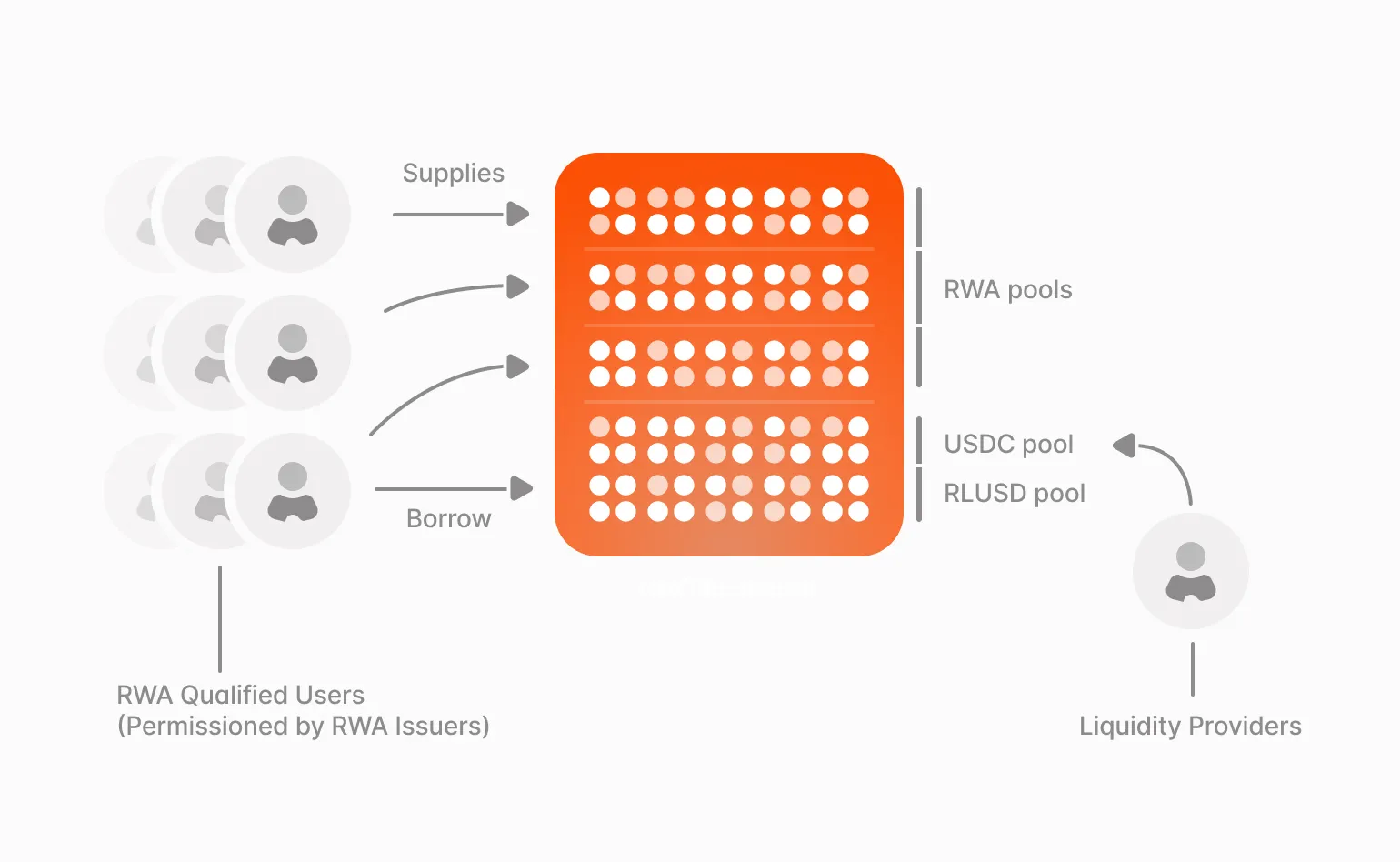

A unique innovation in this system is the emergence of receipt position tokens from on-chain lending protocols such as AAVE. When a user deposits assets - say, USDC or a tokenized fund - into AAVE’s liquidity pool, they receive an aToken, a receipt token that represents their lending position. The value of this token automatically increases as interest accrues from borrowers, effectively turning the deposit into a yield-bearing position.

These receipt tokens function as real-time accounting units, transparently reflecting both ownership and the accumulated yield of the underlying asset. Moreover, because they are fully composable, these tokens can be used as collateral across other protocols or even wrapped into new financial instruments. This enables recursive strategies such as lending, borrowing, and re-depositing, mirroring the layered leverage and re-hypothecation structures of traditional finance - only now executed programmatically, on-chain, and with full transparency.

Source: Horizon | Aave Protocol Documentation

As more assets are tokenized, assets that were once static are now circulating financial units. An investor might deposit tokenized Treasuries as collateral, borrow USDC, and reinvest in another yield-bearing fund - earning yield from both positions simultaneously. Conversely, they could pledge tokenized equities to borrow stablecoins for real-world spending. In both cases, assets continuously flow, reinforcing their role as interoperable units of value within a programmable financial system.

Ultimately, tokenization is making “everything” priced, with any pairs.

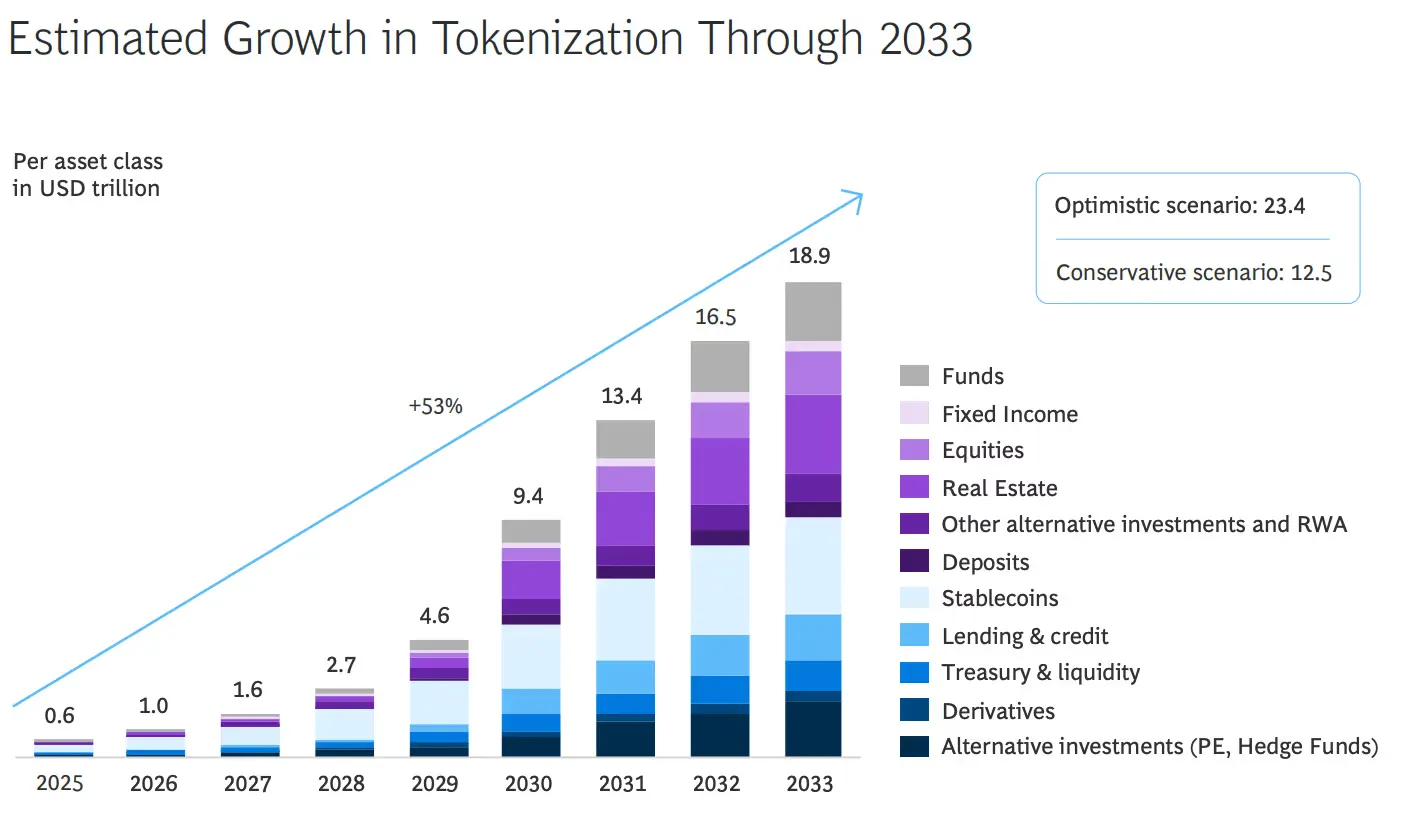

Source: RWA News: Tokenized Real-World Assets Could Reach $18.9T by 2033, Ripple and BCG Report Says

At its core, tokenization is not merely about putting assets on the blockchain — it's about redefining how assets behave. It fuses the traditionally separate worlds of money (e.g., dollar, euro) and assets (e.g., bonds, equities, real estate). Treasury bills, venture funds, real estate, or even intellectual property all can now exist as programmable, composable, and transferable tokens into money. Once tokenized, they can be spent, saved, or valued in real time. This convergence collapses the distinction between "what we own" and "what we can use," blurring the historical line between financial products and liquidity itself.

In this world, tokenization turns ownership into participation. It enables anyone, not just institutions, to move value across systems and strategies. As a result, every tokenized asset becomes part of an always-on financial network where value flows continuously, without needing to be "converted" into cash. A piece of tokenized real estate might generate rental yield distributed directly in stablecoins; a fund share might be borrowed against to finance another investment; or a yield-bearing token might itself serve as collateral to earn additional yield. Each interaction deepens the liquidity fabric of the system, transforming the static notion of holding assets into an active, dynamic state of capital utilization.

Ultimately, the potential of tokenization lies in its ability to make everything behave like money and by doing so, it will change not only how we spend, save, and value, but also how we think about finance itself.

Our mental model of money has always been linear: earn, save, invest, spend. In an onchain economy, those boundaries dissolve.

Tokenization pushes us toward a new mental state where financial activity is continuous, composable, and borderless. At the end of this road, tokenization is making the concept of "money" as something separate from "assets" disappear.

Everything we own becomes a fluid expression of value - always moving, always earning, always connected.

Tokenize the World.

Source: X (@Securitize)

Dive into 'Narratives' that will be important in the next year