Yield-bearing stablecoin yields converge around three sources: treasury interest, crypto funding rates, and private credit. Each carries a distinct tradeoff: rate dependency, market sentiment dependency, and counterparty risk, respectively. thUSD uses all three as auxiliary components, but places roughly 80% of its yield on an independent source tied to none of them: gold futures roll yield.

thUSD's yield consists of gold futures roll yield (about 80%) and thGOLD gold lending yield (about 20%). The two are linked to different variables: interest rates and storage costs for the former, retailer inventory demand for the latter. Their low correlation means that when one compresses, the other provides a yield floor.

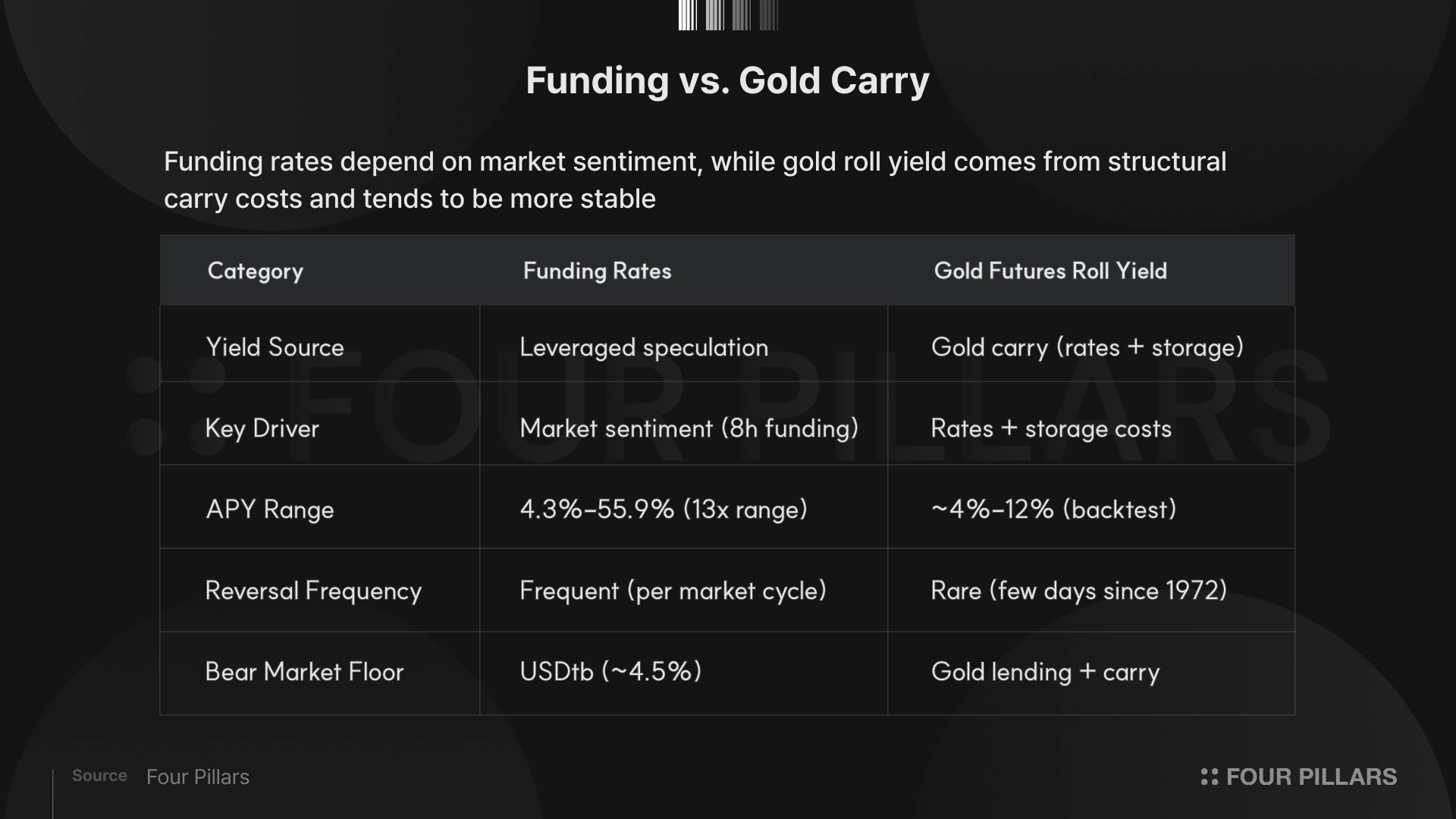

If crypto funding rates are a function of market sentiment that shifts every eight hours, gold roll yield is an economic constant derived from a contango structure sustained for over 50 years. CME gold futures OI of $210B is 33x that of BTC's total OI, offering a structurally wider runway for position scaling.

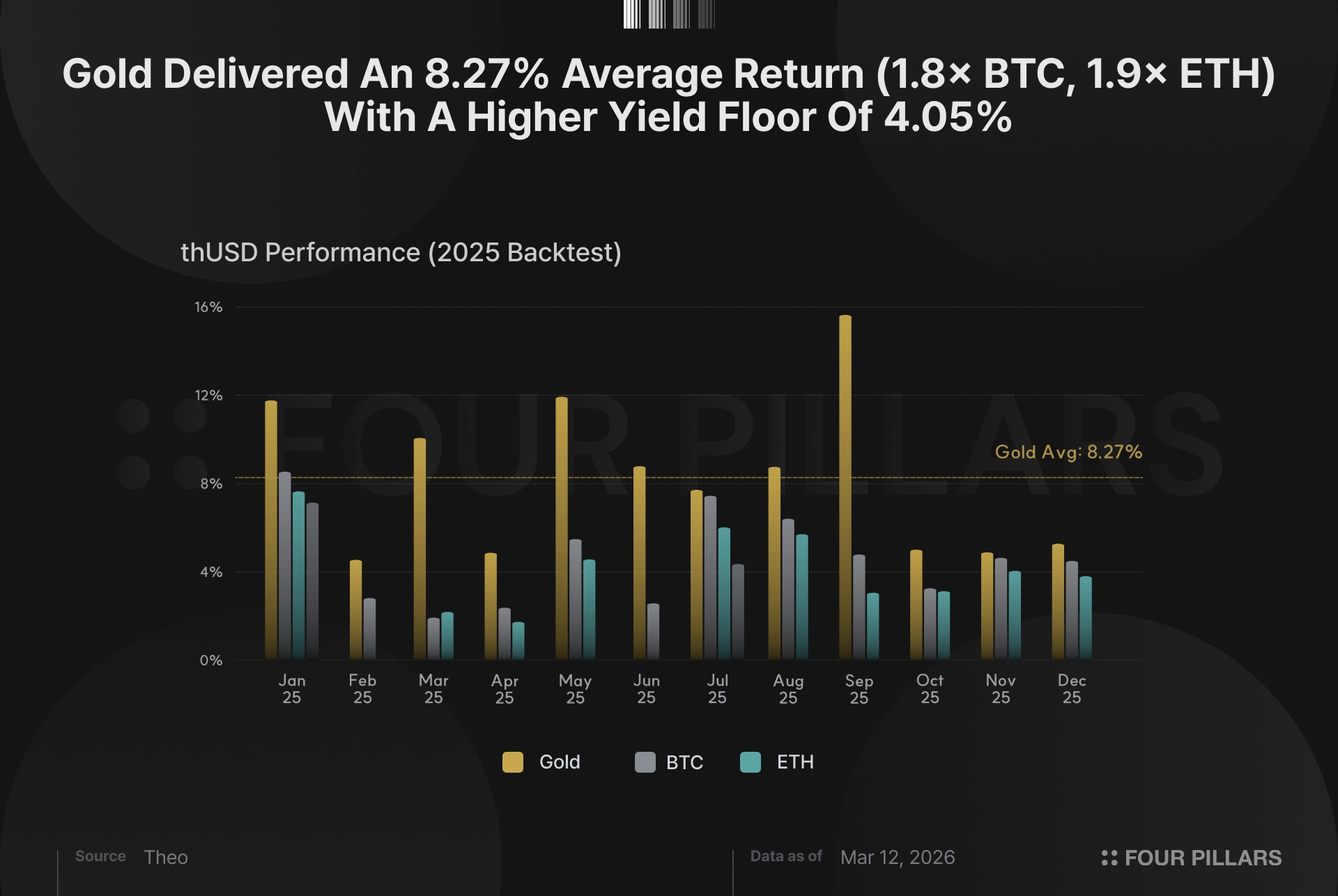

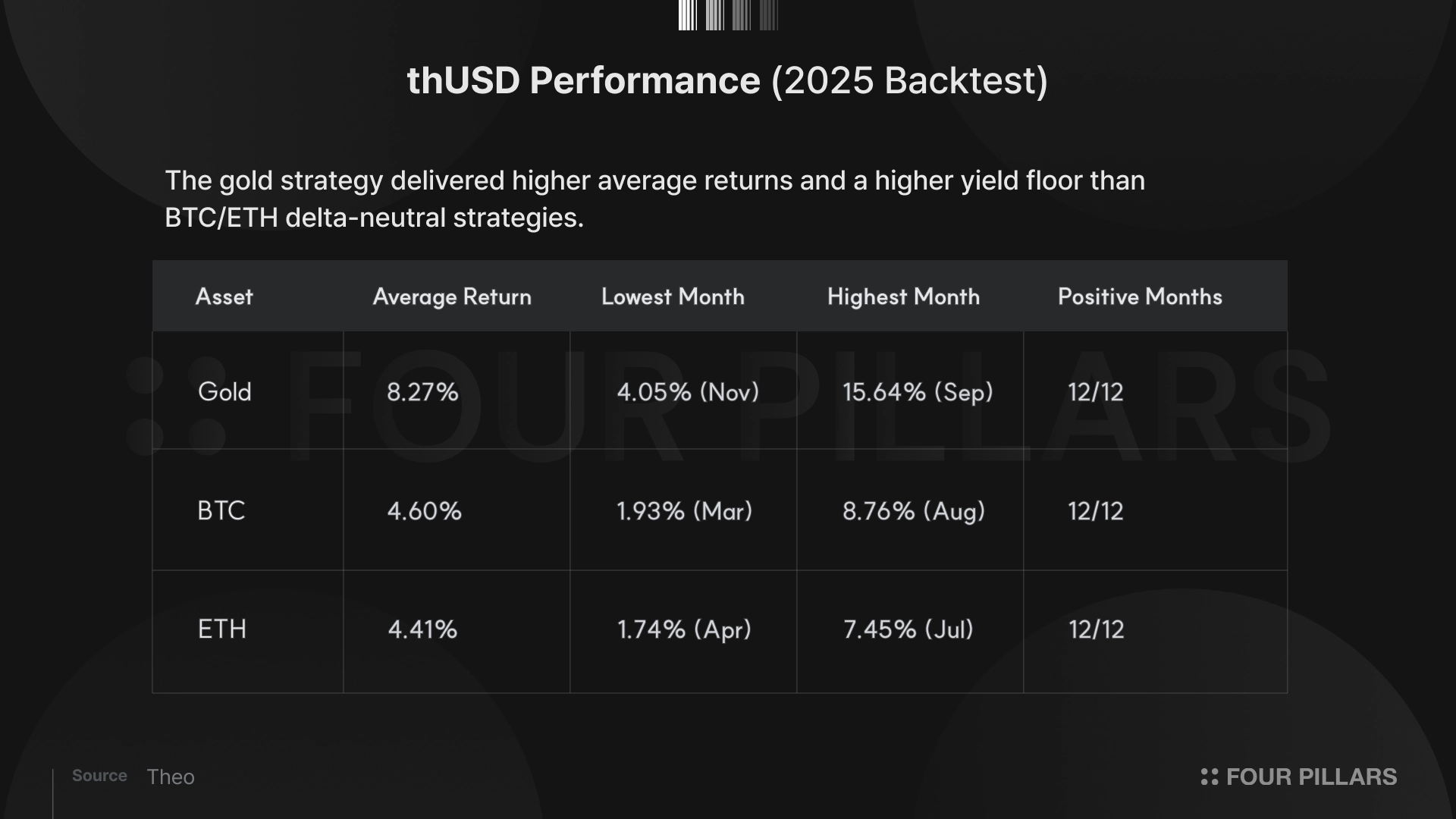

In a 2025 backtest, the gold delta-neutral strategy recorded an average APR of 8.27% with positive returns in all 12 months. Even in its weakest month, the floor was 4.05%, more than double that of BTC (1.93%) and ETH (1.74%). Whether this figure holds in live operation is the key question for thUSD.

The yield-bearing stablecoin market is growing fast. Total market cap has reached roughly $22B, up over 300% year-over-year.

However, prolonged crypto bear market conditions are applying pressure across the sector. sUSDe, which once exceeded 55% APY, has dropped to the mid-single digits. USDe's TVL has fallen from a peak of $14.8B to the $6B range. That is a nearly 13x swing in just five months.

This is not unique to Ethena. Every yield-bearing stablecoin carries advantages tied to its yield source, along with corresponding tradeoffs. Tracing where these yields come from, the sources converge into three categories: treasury interest, crypto funding rates, and private credit.

Treasury yield: USDY (Ondo), USTB (Superstate), and others. Reserves are invested in U.S. Treasuries, short-duration bonds, or MMFs, and coupon income is passed through. Yield is capped at the federal funds rate. Credit risk is effectively zero, but the model is 100% dependent on the rate cycle. Currently stable at around 4-5% on short-term Treasuries, but yields decline as the Fed enters a cutting cycle. Had this model existed during the 2020-2021 zero-rate environment, its yield would have converged to 0%.

Funding rate: Ethena's USDe is the representative example. It takes a delta-neutral position with spot long ETH/BTC and perpetual futures short, collecting the funding rate generated by the crypto market's structural long bias. In bull markets where the funding rate stays positive, it delivers the highest yield of any source. In bear markets, when funding flips to 0% or negative, the yield structure breaks down entirely. Ethena has introduced USDtb (backed by BUIDL) as a treasury-backed backstop, but this brings yields down to roughly 4% during bear phases.

Credit yield: Maple's syrupUSDC is the representative example. Deposits are lent to institutional borrowers, who pay interest in return. Borrowers are primarily crypto market makers and trading firms, taking overcollateralized loans against digital assets like BTC. Average APY is around 8%, the highest of the three paths. The tradeoff is borrower counterparty risk. TrueFi saw $4.4M in defaults after a borrower lost the ability to repay. On Goldfinch, $7M out of a $20M loan was exposed to loss risk. Overcollateralization and due diligence processes mitigate the risk, but as long as money is being lent to someone, counterparty risk is an inherent variable in this model.

All three paths present clear yield-risk tradeoffs. Treasury models are stable but capped by rates. Funding rate models have a high ceiling but a deep floor. Credit models offer high yield but require accepting counterparty exposure.

Theo's thUSD includes funding rates, thBILL (treasuries), and private credit in its reserves. However, it places roughly 80% of its yield on an independent source that is not dependent on any of these three paths: gold futures roll yield.

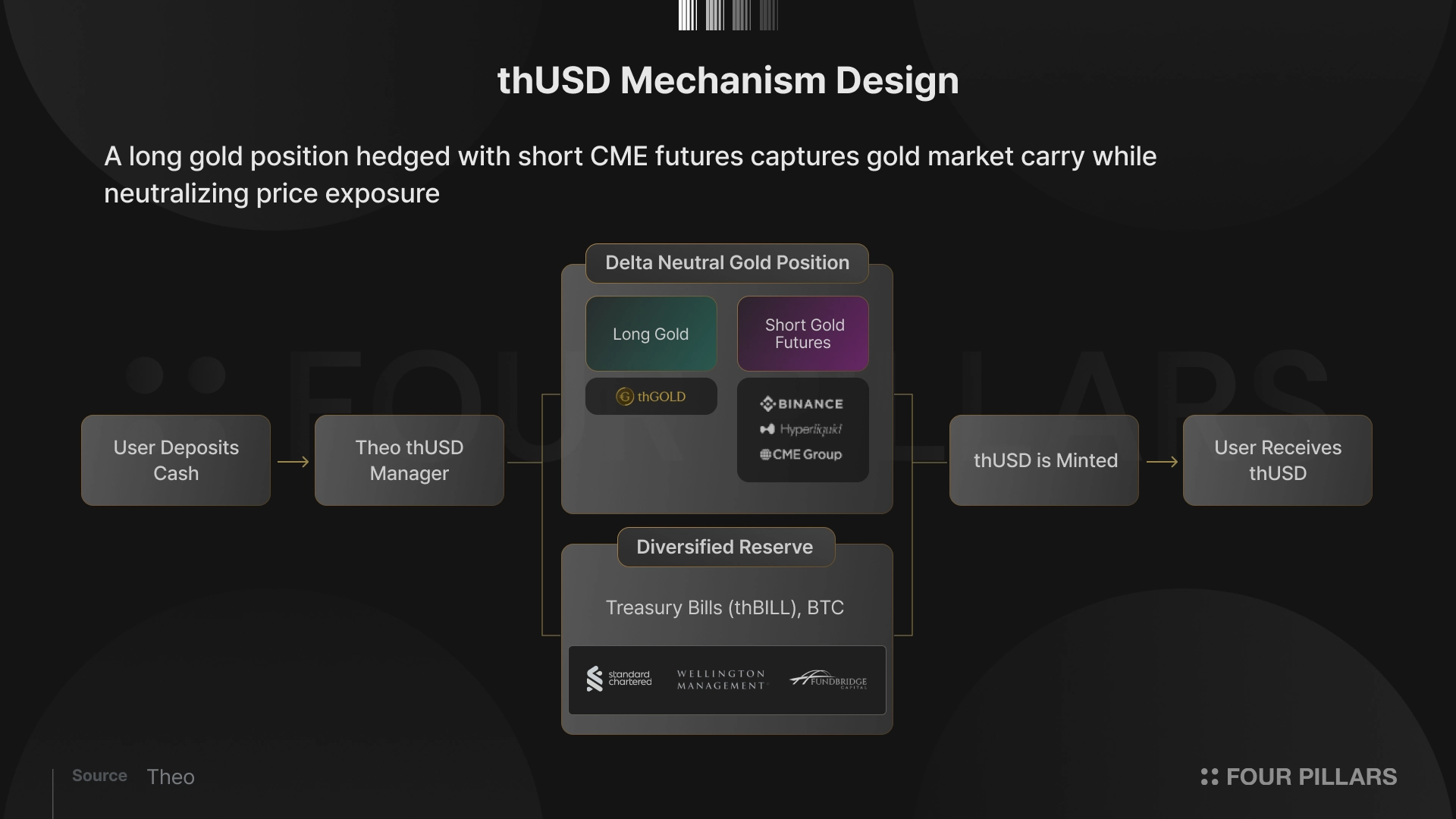

In one sentence, thUSD is a delta-neutral synthetic dollar that holds yield-bearing tokenized gold (thGOLD) as spot long and shorts gold futures on regulated exchanges like CME to eliminate gold price exposure. Based on an internal 2025 backtest, it recorded an average APR of 8.27%. The yield breaks down into roughly 6.69% from gold futures roll yield and roughly 2.50% from thGOLD gold lending yield.

Delta-neutral itself is already a familiar mechanism through Ethena's USDe. However, the underlying asset (thGOLD) and the yield source (roll yield) are new. The following sections break down each yield component.

2.1.1 Why Gold Futures Are Almost Always More Expensive Than Spot

Spot long + futures short, and roll yield. Roughly 80% of thUSD's yield comes from here.

thUSD's strategy is straightforward. It goes long spot gold (thGOLD) and shorts the same amount in gold futures. If gold rises, the spot side profits and the futures side loses. If gold falls, the opposite happens. The two sides cancel out, bringing net gold price exposure to zero. Up to this point, the structure is identical to USDe's delta-neutral using ETH/BTC, a model that has been sufficiently validated.

The difference is the yield source. USDe collects funding rates on perpetual futures. thUSD shorts gold futures with expiration dates on regulated exchanges like CME, and captures the roll yield generated during the contract rollover process. Understanding how this roll yield is generated on a recurring basis requires a look at a few mechanics of the gold futures market.

Unlike perpetual futures, standard futures contracts have expiration dates. As expiry approaches, the current contract is closed and replaced with the next contract. This is called a rollover.

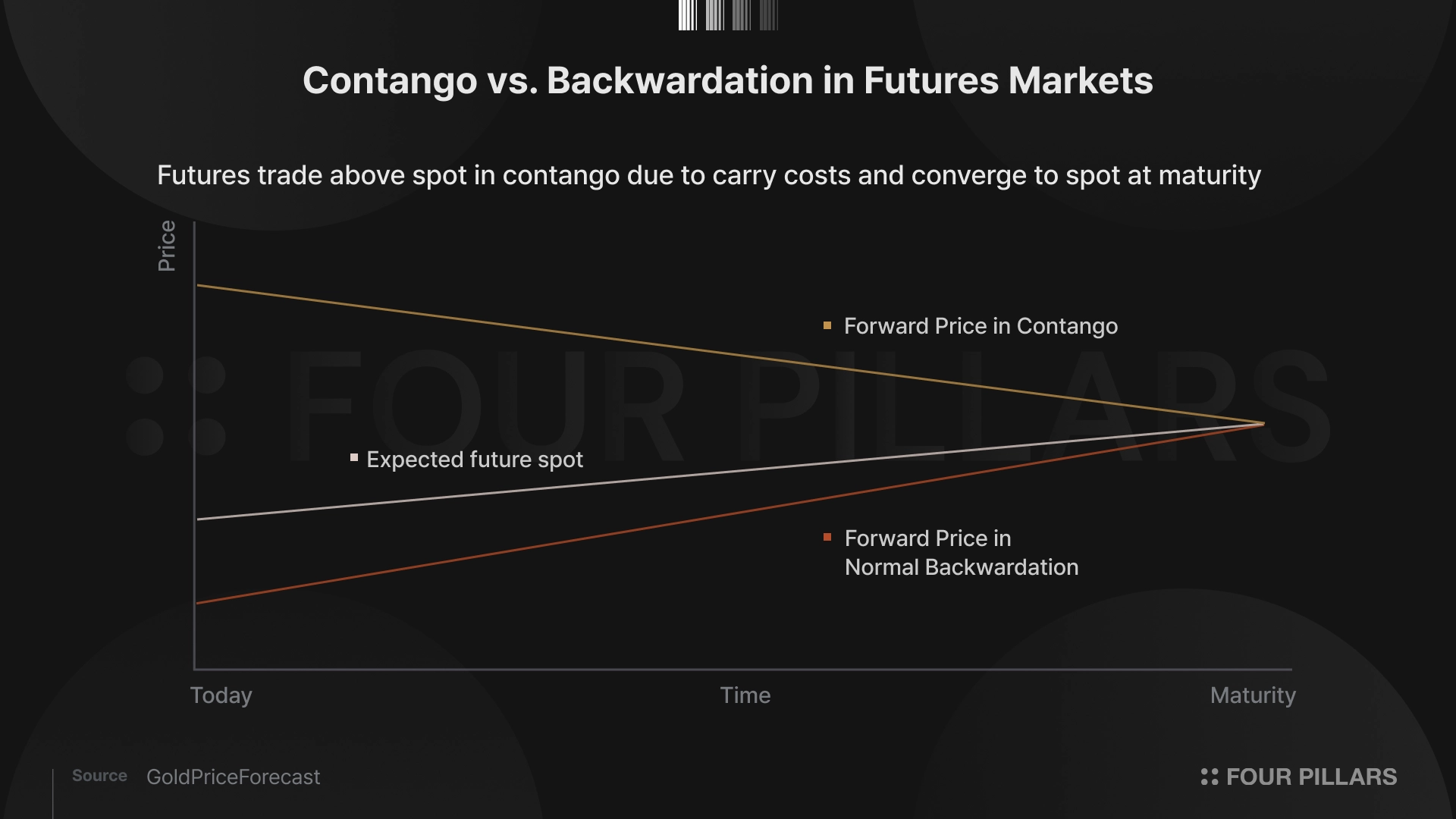

As discussed below, thUSD captures roll yield through this rollover process. The reason yield is generated here is that gold futures are almost always priced above spot gold. This state, where futures trade above spot, is called contango.

\Why does contango persist in the gold futures market?

Contango is fundamentally driven by storage costs. Buying and holding physical gold requires vault rental (storage), insurance, and the opportunity cost of capital. Buying a futures contract, on the other hand, secures the same gold exposure without bearing these costs upfront. The futures buyer pays a price premium as the cost of not bearing the carry cost (cost of carry) today.

As a result, gold futures prices are determined by "spot price + carry cost." As long as interest rates and storage costs remain positive, futures prices almost always trade above spot. Roll yield is derived not from speculative sentiment, but from the structural cost of physical storage.

2.1.2 thUSD's Roll Yield Strategy

thUSD converts this contango into roll yield. As noted, thUSD goes long spot gold and shorts futures. The process of replacing this short position at each expiry is the primary point where yield is generated. As the futures price converges to spot at expiry, the short position's profit is locked in. The specific mechanism, illustrated with an example:

Spot gold at $5,000, 6-month futures at $5,100 (contango premium of $100). The futures are shorted.

As expiry approaches, the futures price converges to spot. The contract sold at $5,100 is closed at $5,000, locking in $100 of profit.

The next futures contract (another 6 months out) is shorted. The next contract also carries a contango premium, so the same process repeats.

The roll yield accumulated through this repetition is included in the interest returned to holders. It is independent of whether gold prices rise or fall. Yield is generated solely from the price difference between futures and spot. Based on the internal backtest, roughly 81%, or 6.69%, of the average 8.27% APR came from roll yield.

2.1.3 Yield Stability: Historical Persistence of Contango and Short Position Diversification

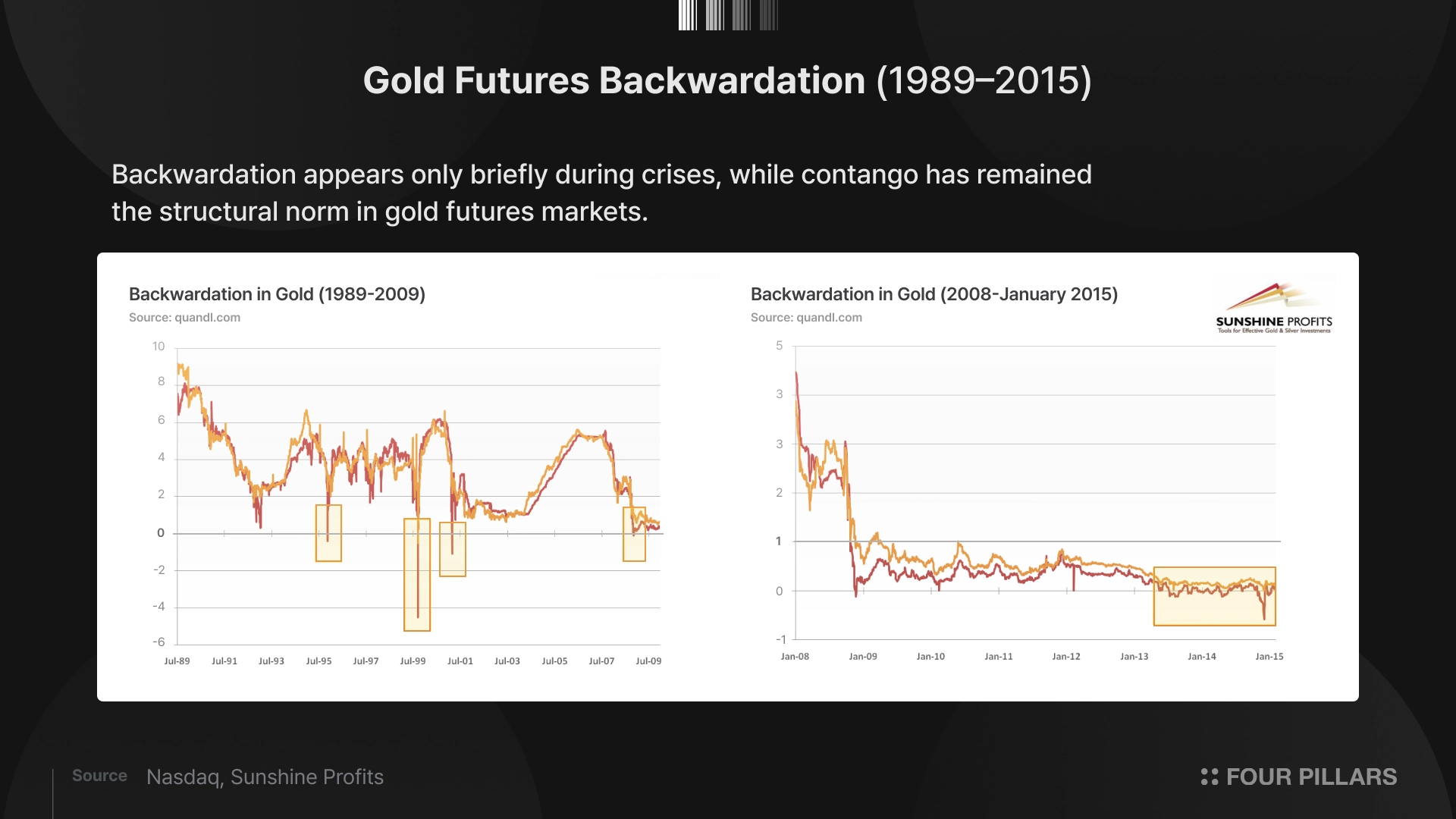

How stable is this contango historically? Since gold futures began trading on the Winnipeg Commodity Exchange in 1972, gold has maintained contango almost without exception. Through 2009, gold entered backwardation (spot > futures) on a total of just eight days. Brief backwardation episodes were observed during the December 2008 Lehman crisis, in 2015, and in early March 2020 during the pandemic, but all were temporary phenomena during extreme liquidity crises, resolved within days. The fact that backwardation totaled just a few days across more than 50 years supports the sustainability of roll yield.

The short position execution path is not limited to CME expiry futures. thUSD also uses gold perpetual futures on crypto exchanges like Binance and Hyperliquid. On perpetual futures, funding rates replace roll yield as the yield source. In an environment where gold, like crypto assets, exhibits structural long bias, the short position can continuously collect funding rates.

thUSD combines CME expiry futures roll yield with crypto exchange perpetual funding rates. The purpose is to diversify single-point risk and allocate capital to whichever path is more favorable given market conditions, securing yield stability.

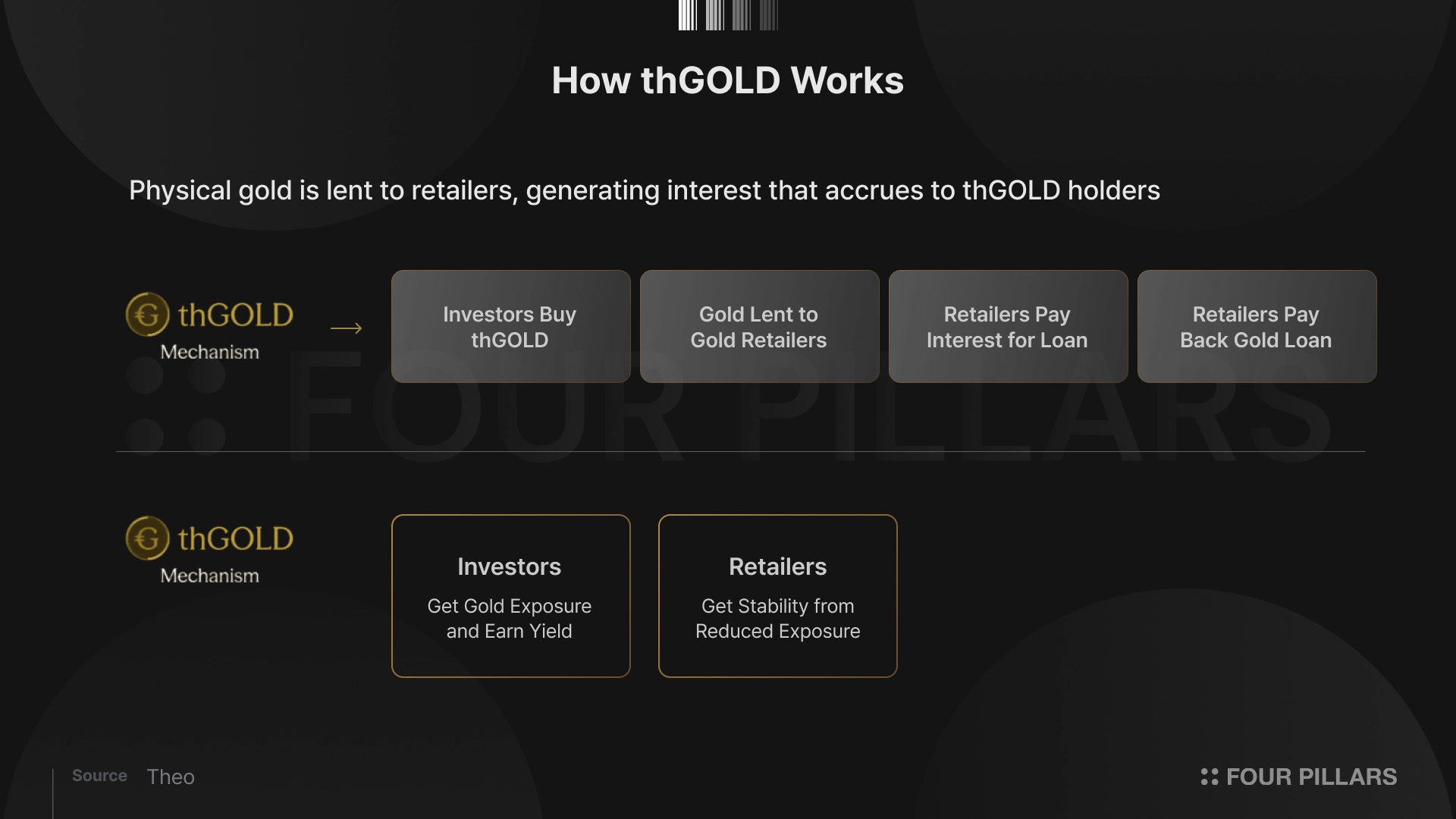

The remaining roughly 20% comes from thGOLD. thGOLD is a tokenized gold product that tracks the MG999 On-Chain Gold Fund, operated by FundBridge Capital with tokenization infrastructure provided by Libeara (a Standard Chartered subsidiary).

thGOLD is different in nature from tokens like XAUT or PAXG that simply track the gold price. thGOLD is a private credit product based on a gold lending fund, generating interest income while tracking gold. The fund holds physical gold and lends it to Mustafa Gold, one of Singapore's largest gold dealers.

The reason gold retailers borrow gold is straightforward. Purchasing inventory outright ties up large amounts of capital, whereas borrowing allows them to secure stock without that capital burden. The retailer sells the borrowed gold, then repurchases the same amount on the market and returns it with interest.

Gold lending itself is not a new mechanism. Central banks lending their gold reserves to bullion banks and collecting interest has been standard practice in the London gold market for decades. thGOLD is closer to an on-chain translation of this structure. The lending interest generated through this process returns to thGOLD holders as roughly 2% annual yield.

In summary, thUSD's yield is generated from two independent paths. Gold futures roll yield accounts for roughly 80%, and thGOLD gold lending yield for roughly 20%. Roll yield is linked to interest rates and storage costs. Gold lending yield is linked to retailer inventory funding demand. The low correlation between these two variables means that when one compresses, the other provides a yield floor.

In addition, thUSD's reserves include thBILL (tokenized treasuries) and BTC delta-neutral positions as supplementary yield sources. The structure is designed to keep the gold carry trade at the center while diversifying yield sources, so that compression in a single path does not collapse overall returns.

thUSD's delta-neutral strategy is a model already validated by USDe. The difference, put simply, is one thing: the underlying asset changed from ETH/BTC to gold. However, this single change produces a structurally different profile across yield stability, market depth, and exchange risk. The following examines why Theo chose gold across three dimensions.

As discussed, USDe and thUSD use the same strategy (spot long + futures short), but the mechanisms generating yield are fundamentally different. USDe delivers the highest ceiling in bull markets, with annualized rates exceeding 30-50%. However, as long as yield is tied to the crypto cycle, yield compression in bear markets is unavoidable. If extreme outperformance in bull markets is this model's strength, yield compression in bear markets is its clear flipside.

thUSD's roll yield depends on different variables. It is derived from the economic factor of gold's carry cost (interest rates + storage + insurance) and operates independently of the crypto market cycle. Where crypto funding rates can change direction every eight hours, gold contango is closer to a structural constant sustained for over 50 years.

The most practical reason thUSD chose gold as its underlying is market depth. In a delta-neutral strategy, the liquidity of the derivatives market that can absorb the short position is the ceiling for scalability. As OI (Open Interest) share rises, the protocol's own short position compresses funding rates and basis, entering a self-cannibalization structure where yield itself erodes.

When USDe was at $420M in early 2024, it already accounted for roughly 5% of global ETH perpetual OI. Guy Young stated at the time that "occupying 30-40% of OI leads to serious capacity constraints." Ethena subsequently diversified collateral into BTC and SOL, scaling to a peak of $14.8B, but the size constraint of crypto derivatives OI remains a variable to consider.

thUSD approaches the same scalability problem differently. CME COMEX gold futures OI stands at roughly 409,789 contracts as of March 2026, with a notional value of roughly $210B at current gold prices. This means that even if thUSD grows to several billion dollars, it would represent just 1-2% of gold futures OI. Volatility differences matter as well. Gold's annualized volatility of 14.4% is less than half of BTC (33.5%) and a quarter of ETH (60.8%), which directly translates to lower margin requirements and reduced forced liquidation risk.

Delta-neutral entrusts short positions to exchanges. As the 2022 FTX collapse demonstrated, exchange counterparty risk is the tail risk of this model. USDe distributing positions across multiple exchanges including Binance, Bybit, and OKX is a response to this risk.

thUSD is not free from the same risk, given that it uses crypto exchanges as short execution paths. However, thUSD has the option of CME. When trading on CME, the exchange itself acts as a central counterparty (CCP) to every trade. Even if the counterparty on the other side of a short defaults, CME guarantees performance. CME has never failed on this guarantee since its founding in 1848, backed by a guaranty fund of roughly $8B.

thUSD can allocate to CME the short positions that account for roughly 80% of its yield. This is an option that does not exist in models that construct delta-neutral positions using only crypto assets.

Theo's published 2025 backtest compares three strategies across gold, BTC, and ETH under identical conditions (90% LTV) over 12 months.

The gold strategy outperformed BTC and ETH in 10 of 12 months. The average return of 8.27% is roughly 1.8x BTC (4.60%) and 1.9x ETH (4.41%).

However, what matters more than the average is the height of the floor. BTC's worst month was 1.93%. ETH's was 1.74%. In periods where funding rates compressed, yields dropped below 2%. When funding rates flip negative in bear markets, yields disappear or turn into losses. This is a structural weakness laid bare in the results.

The gold strategy's worst month was November at 4.05%. Even in its weakest month, it stayed above 4%. The ceiling is higher in crypto bull markets. In periods where funding rates exceed 30% annualized, the gold strategy cannot compete. However, the floor is where gold holds a clear advantage. If yield-bearing stablecoins are not instruments for aperiodic outperformance but foundational blocks of money legos, collateralized and earning predictable interest through DeFi, then thUSD's narrow yield band is a meaningful strength.

Source: Theo

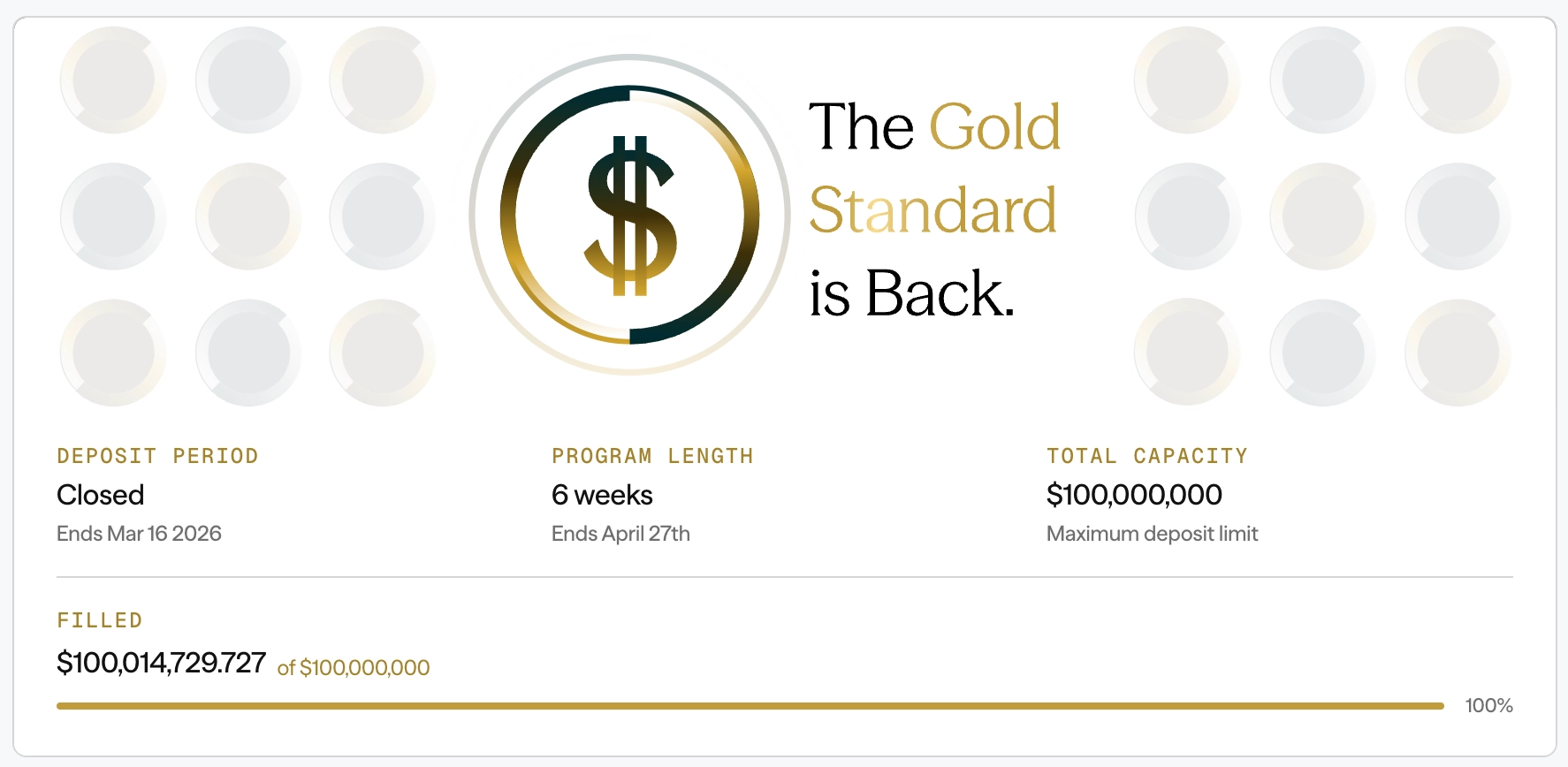

The $100M Genesis Vault that marked thUSD's launch opened pre-deposits on March 10 and drew enough interest to approach its cap.

The $100M Genesis Vault that marked the launch of thUSD opened for pre-deposits on March 10, and the cap filled quickly, drawing strong market interest.

Several factors contributed to the smooth start. Theo's previously launched thBILL validated DeFi integration paths for RWA tokens through integrations with protocols like Morpho and Pendle, surpassing $160M in issuance. thGOLD then expanded the asset class to gold. thUSD is the third step, layering delta-neutral on top.

As a result, Theo has internalized a diversified set of yield sources, from treasury backing (thBILL) to gold lending yield (thGOLD) to futures roll yield, all within a single stablecoin. In a yield-bearing stablecoin market where competition intensifies alongside market growth, this presents a profile that overlaps with none of the existing three pillars.

First, roll yield is linked to interest rates. Yield is ample in the current 4-5% rate environment, but if global rates decline sharply, carry costs compress and roll yield shrinks. While gold contango has been sustained for over 50 years, that track record belongs to an environment where rates were positive. During the 2008-2015 zero-rate era, GOFO fell near the zero line with increasingly frequent negative entries.

Second, gold's low volatility is a historical average, not a guarantee. In early 2026, spot gold broke through $5,600 before dropping sharply, recording its largest single-day decline on record. Silver fell over 25% in a single day.

Even so, the demand base for thUSD is relatively clear. Looping demand using yield-bearing stablecoins as collateral, and demand for stable yield independent of market direction during crypto bear markets, both support it. Theo plans to integrate thUSD as collateral, base pair, and yield layer across major DeFi protocols including Hyperliquid, Morpho, and Pendle. On the premise that the roughly 8% backtest yield is replicated in live operation, thUSD's positioning is more unique than that of any other yield-bearing stablecoin.

Dive into 'Narratives' that will be important in the next year