It is time for the RWA market to move beyond the issuance phase and focus on how tokenized assets are traded, settled, and monetized. In the long run, the players that capture the largest value flows in the RWA space will not be those with the highest TVL, but those that generate meaningful trading volume. The key variable is not the total supply of tokenized assets, but how efficiently those assets can be traded as capital.

The RWA market is already prepared in terms of regulatory frameworks, onchain compatibility of RWAs, and issuance infrastructure. However, its expansion remains constrained by low liquidity and inefficient trading environments. Structural limitations such as NAV-based pricing, low trading frequency, and the absence of effective hedging tools make it difficult for market makers to participate.

Theo proposes a full-stack RWA platform with liquidity at the core of its design. Its first milestone, thBILL, is an onchain money market fund backed by short-term U.S. Treasuries. Through an optimistic minting structure, where market makers mint tokenized assets instantly based on per-block quotes and settlements are processed on the backend, thBILL creates a favorable environment for liquidity provision.

Theo is founded by former market makers and backed by active market-making firms. The team includes professionals with experience at HFT firms and traditional financial institutions such as Optiver, IMC Trading, and Bain Capital. Leveraging direct experience in liquidity provisioning algorithms, position risk management, and market infrastructure operations, the team aims to build an RWA platform truly optimized for the onchain.

When evaluating a protocol’s growth, TVL without capital efficiency is a vanity metric. From an accounting perspective, TVL is a liability, representing assets that must be redeemable to users at any time. What matters more is how those deposited assets are managed and how efficiently they are used as capital.

This principle holds true in traditional finance as well. Even BlackRock, with over $12T in AUM, generates only about $5.5B in annual net income. In contrast, high-frequency trading (HFT) firms such as Citadel, Jane Street, and HRT manage just a few billion dollars but consistently deliver significantly higher returns and double-digit annual growth rates. While risk profiles and business models differ, it is clear that trading volume has always been a more decisive factor for profitability than AUM or TVL.

Crypto is now entering the same volume-driven paradigm. The evolution from Uniswap v2 to v3, and from GMX’s GLP to Hyperliquid, signals a broader industry shift away from TVL and toward capital efficiency and turnover. Uniswap v3 improved capital productivity by concentrating liquidity within narrow price ranges, enabling more trades with the same amount of capital. Hyperliquid, with ultra-fast execution, generated greater fee-based revenue from trading activity than GLP.

These examples illustrate a core truth: the value capture of any protocol depends on how many transactions occur on the same capital base and how much fee income is generated from that activity. The shift from TVL-focused metrics to volume-based metrics in crypto is becoming increasingly visible.

This brings us to the central point of this thesis: the same transition is inevitable for the RWA market. To date, the RWA narrative has largely focused on the technical and legal complexities of bringing real-world assets onchain, given regulatory uncertainty and a lack of precedent. As a result, early movers such as Securitize, Ondo, and Superstate have dominated the space, collectively accounting for approximately 88% of tokenized U.S. Treasuries. So far, growth in the RWA sector has been driven almost entirely by issuance.

However, issuance alone is not enough for RWAs to become a foundational asset class in onchain finance. The time has come to focus on how tokenized assets are distributed, traded, and monetized. This will mark a new phase for RWAs, where success is no longer defined by the volume of issuance, but by the trading activity and velocity surrounding these assets.

This naturally leads to the next critical question: just as Uniswap v3 and Hyperliquid redefined capital efficiency and liquidity in DeFi, which RWA platform is best positioned to capture value through volume-centric design? One strong candidate is Theo. Theo firmly believes that the success of RWAs lies beyond issuance and is building a liquidity‑centric tokenization platform that integrates the full lifecycle from issuance to trading. As we will explore in the following sections, this approach positions Theo as a leading contender in the emerging RWA volume game.

To understand how far RWAs have progressed in the onchain ecosystem, we must begin with the current state of the issuance phase. A few years ago, the concept of RWAs was still abstract and poorly defined. Today, the issuance process has become increasingly structured. However, bringing real-world assets onchain remains a complex task. To assess the maturity of this space more clearly, we can examine three critical components:

2.1.1 Regulatory Framework

Recent examples such as BUIDL (Securitize) and thBILL (Theo & Libeara), both tokenized money market funds (MMFs), indicate that a significant portion of the institutional groundwork for bringing real-world assets onchain has already been established. BUIDL, for example, is a tokenized security registered with the U.S. SEC. It is issued through a licensed broker-dealer structure (Securitize Markets LLC), complying with private placement regulations under Reg D, Rule 506(c), for accredited U.S. investors.

In other words, these products are operated under full regulatory compliance without relying on regulatory sandboxes. Tokenized assets are not bypassing existing securities law. Instead, they are being issued within the regulatory framework of traditional capital markets.

2.1.2 Onchain Mapping of Real-World Assets

The cornerstone of tokenizing real-world assets is ensuring a precise 1:1 correspondence between the offchain collateral and the onchain token. This requires transparent custodial systems and mechanisms for real-time verification. Backed Finance, for example, issues tokenized versions of equities and ETFs fully backed by offchain assets, using Chainlink’s Proof of Reserve (PoR) oracle to automatically verify collateral levels onchain. This creates an onchain audit system where users can verify token circulation and backing at any time.

In addition, accurate onchain pricing for tokenized assets depends on robust oracle infrastructure. Chainlink supports data feeds for NAVs, interest rates, and credit ratings, while Redstone provides RWA-specific oracles and collaborates with firms like Apollo and BlackRock to deliver real-time pricing for institutional tokens such as BUIDL and ACRED in Solana-based DeFi. Through this infrastructure, tokenized assets are increasingly used as DeFi collateral and are becoming programmable financial instruments.

2.1.3 Issuance and Operational Infrastructure

For tokenized assets to circulate meaningfully, they require institutional and technical infrastructure that spans issuance, management, redemption, and settlement. This includes legal ownership records, investor onboarding (KYC/AML), revenue distribution logic, onchain accounting, and secure custody. Most importantly, the infrastructure must ensure full compliance with securities regulations to prevent unlawful offerings.

Several integrated frameworks have already been deployed in the market. Securitize has onboarded assets from institutional managers such as Apollo and BlackRock. Ondo Finance and Franklin Templeton are operating tokenized MMFs with daily rebasing, token-based yield distribution, and real-time redemption models. These platforms are setting new standards for end-to-end RWA operations.

Taken together, the regulatory structure, onchain mapping capability, and operational infrastructure show that many of the prerequisites for RWA issuance have already been met. Yet despite this progress, the RWA market has not demonstrated substantial growth. Most media coverage still focuses on which regulatory framework a token used, or which protocol onboarded a token, rather than any meaningful trading volume or fee generation. This suggests that while issuance is evolving, the post-issuance phase remains underdeveloped, and the gap toward becoming a mainstream asset class is still significant.

What is preventing the RWA market from scaling? The key bottleneck is liquidity. In particular, delayed redemptions and shallow secondary markets make tokenized assets difficult to trade efficiently.

2.2.1 Redemption Delays

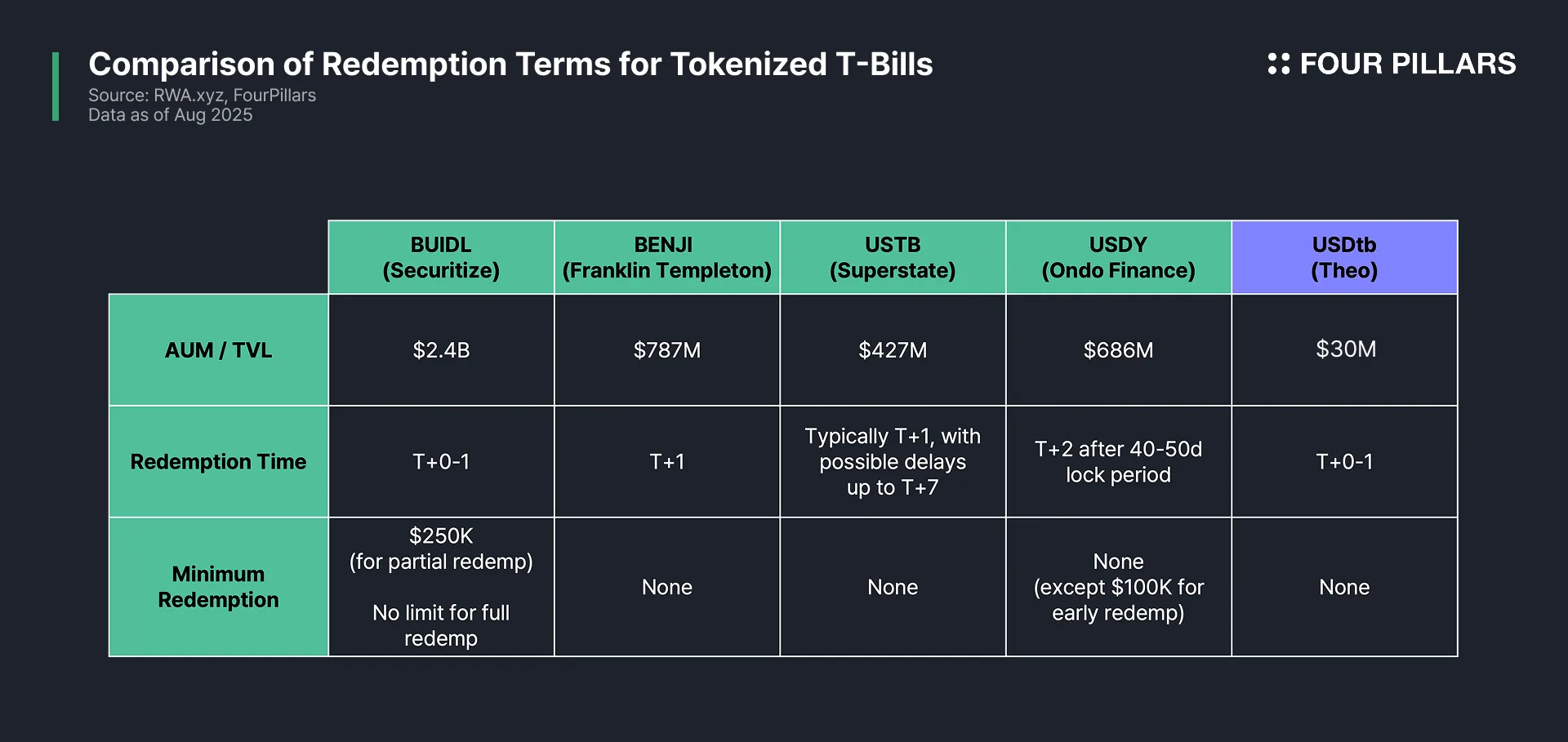

Even when looking only at tokenized U.S. Treasury products, there are multiple limitations that restrict investors from using their capital flexibly. Although 24/7 trading is often cited as an advantage of tokenized assets, actual redemption processes often fail to meet that expectation.

BUIDL offers T+0 or T+1 redemption but requires a minimum of $250,000 for partial redemptions. Full redemptions may take T+2 or T+3. BENJI and USTB provide T+1 redemptions, which are relatively quick, but still resemble traditional finance settlement cycles. Even in cases of T+0 redemption, strict cut-off times like 9 a.m. submission on business days apply. USDY imposes a 40–50 day transfer restriction after issuance, followed by a T+2 redemption cycle.

These products are constrained by the same timeframes and rigidities as traditional financial instruments. They fail to offer the real-time liquidity and programmability expected from onchain assets, leading to psychological and operational barriers for capital deployment.

2.2.2 Secondary Market Liquidity

In practice, most investors prefer to trade tokenized assets on secondary markets rather than redeeming them directly through the issuer. However, the lack of deep liquidity in secondary markets presents another bottleneck. This problem is frequently observed in the tokenized stock market, where even assets that are securely mapped and traded through order books suffer from poor execution, high slippage, and insufficient order depth.

The root cause lies in the difficulty of market-making for tokenized real-world assets. Compared to crypto-native assets, RWAs present structural challenges for liquidity provision, which can be broken down as follows:

Limited Liquidity Supply for Market Makers

Market makers in crypto usually borrow or receive tokens directly from the project. For RWAs, however, the liquidity is mapped to offchain collateral, and issuers rarely pre-mint large circulating supplies. Since pre-minting requires upfront acquisition of real-world assets, most issuers mint tokens only in response to demand. As a result, market makers are forced to either mint tokens themselves or operate with limited supplied liquidity, constraining their ability to maintain deep markets.

Inventory Risk from Lack of Hedging Instruments

To provide liquidity, market makers must hold spot inventory, which exposes them to price risk. In crypto, this risk is typically hedged via derivatives. In the RWA market, such instruments either do not exist or remain underdeveloped. As a result, market makers bear full exposure to real-world price volatility, especially for assets like equities or commodities, where fluctuations are more pronounced. This makes inventory holding less attractive.

Low Volatility and Lack of Spread Opportunities

Market makers generate revenue from bid-ask spreads by capturing small price differentials. However, many tokenized MMFs and Treasury products update their NAV only once per day, making it difficult for market makers to adjust quotes dynamically and extract profits. With limited opportunities for spread capture, the incentive to participate weakens.

Source: Theo

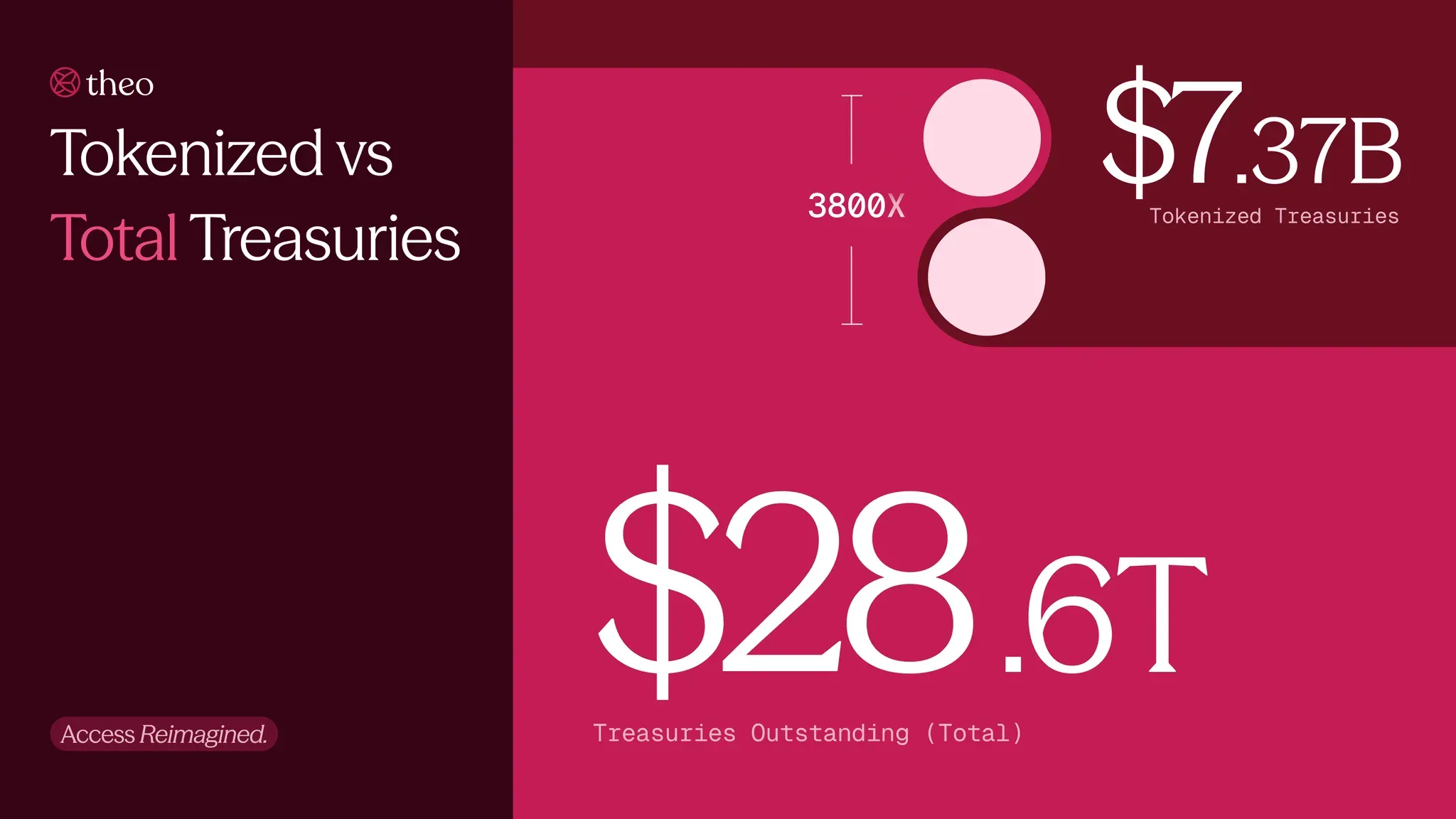

Due to these liquidity constraints, the growth of the RWA market remains limited in practice. While BlackRock manages over 100 times more capital than the entire onchain ecosystem, only around $7B in tokenized Treasuries exist. This represents just 0.03% of the $28T U.S. Treasury market.

Source: BCG

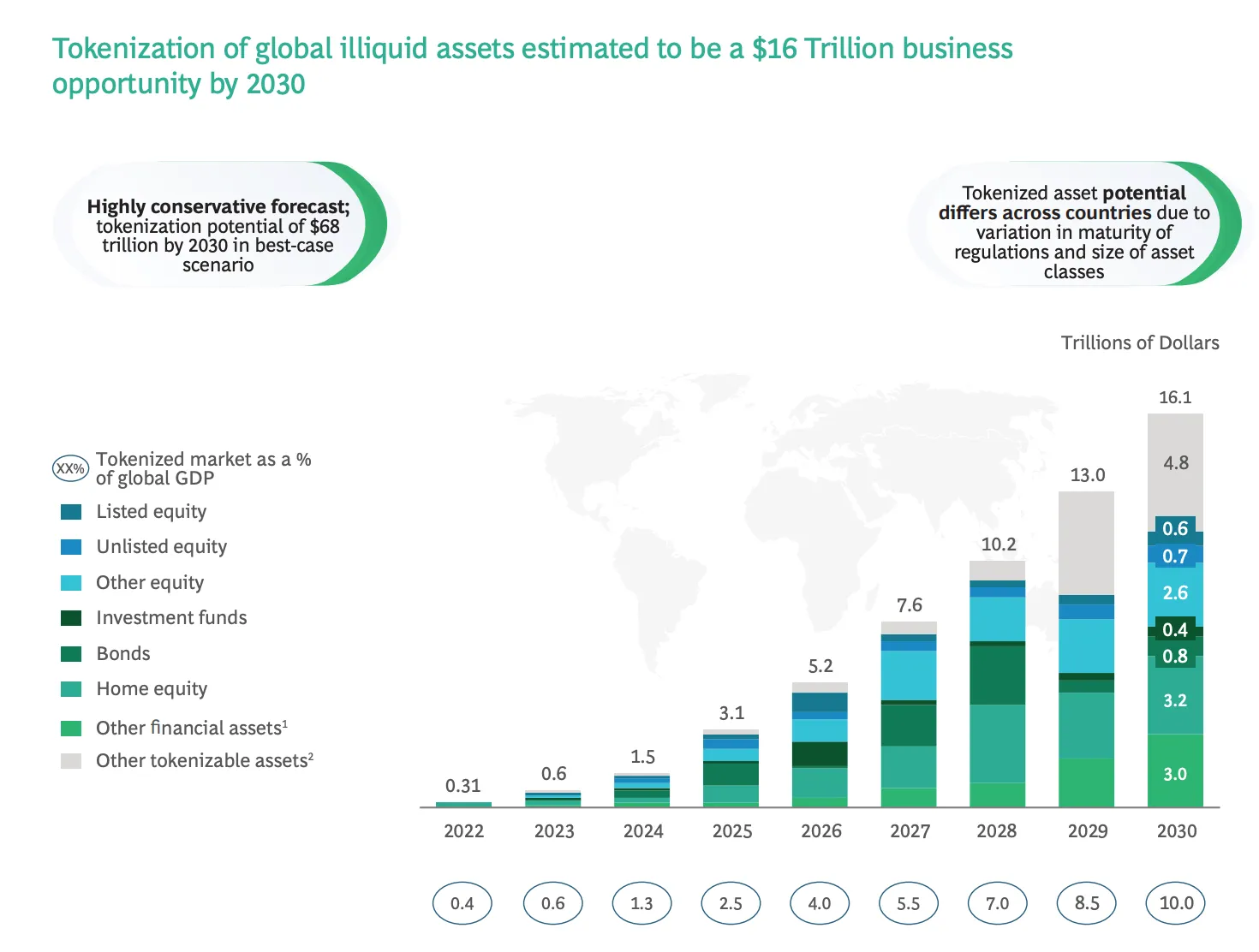

This gap is both a constraint and an opportunity. It reflects the early stage of the RWA market but also highlights the massive potential for expansion. According to BCG, approximately $16T in existing assets may be tokenized by 2030, representing roughly 10% of global GDP.

In conclusion, although regulatory and technical foundations are in place, friction in distribution and trading continues to hold back adoption. If liquidity infrastructure improves, a meaningful portion of traditional capital markets could migrate onchain. To unlock this future, the path forward is clear: the RWA market must evolve from an issuance-centric model to one centered on post-issuance liquidity and capital efficiency.

Source: Theo

As liquidity constraints continue to hinder the growth of the RWA market, Theo’s vision is clear. The protocol views issuance as merely the first step. True success in RWA is defined by what happens after, particularly in distribution, trading, and liquidity. At a time when various real-world assets such as U.S. Treasuries, private credit, and equities are being tokenized, and institutional interest in onchain exposure is growing, the most critical factor is the infrastructure that enables real trading activity and capital mobility.

To meet this demand, Theo presents an RWA infrastructure designed with liquidity at its core. It aims to establish a full-stack RWA platform that supports deep trading liquidity, efficient leverage, and high composability with onchain protocols, ultimately bridging the gap between traditional finance and the blockchain.

Theo is led by a team with extensive experience in global trading and market making. The founders come from firms like Optiver and IMC Trading, where they built expertise in high-frequency trading, liquidity provisioning, and position risk management. Their first-hand experience in traditional market microstructure gives them a deep understanding of capital efficiency and the capabilities to execute on it.

Source: X(@Theo_Network)

“Most people today are excluded from the most powerful engine of wealth creation, which is the U.S. financial markets. At Theo, we are building a new kind of financial institution from the ground up to bring these markets onchain and make them accessible to everyone."

"Tokenization has been discussed since at least 2018, starting with STOs. Many projects made flashy announcements and put assets onchain, but nothing happened. The benefits of onchain finance never materialized. That is why Theo focuses on what comes after issuance. We enable liquidity and connect tokenized RWAs to the places where real demand exists.”

— Iggy Ioppe, CIO, Theo Network

Theo deals with regulated real-world assets such as U.S. Treasuries, MMFs, equities, and commodities. Tokenizing and handling these assets onchain requires not only regulatory alignment but also trusted partnerships with asset managers and custodians. Theo’s CIO, Iggy Loppe, plays a central role in this bridge. He brings experience from Bain Capital, Credit Suisse, and hedge funds, and was also a co-founder of Location Labs, which was acquired for $220M in 2014. At Theo, he leads the initiative to connect traditional finance with onchain markets.

Theo does not stop at bringing assets onchain. Its entire infrastructure is focused on what happens after issuance, building liquidity-first architecture to overcome the structural limitations of the RWA market.

Theo’s full-stack RWA platform is still evolving, but its design clearly extends beyond simple tokenization. It integrates issuance, distribution, settlement, and composability. At the core of the platform is thBILL, an onchain MMF backed by short-term U.S. Treasuries. thBILL is fully compatible with traditional regulatory frameworks and reflects the yield of U.S. government debt.

It is issued using Theo’s proprietary iToken standard, which explicitly encodes asset states such as minting, settlement, and redemption directly onchain. The initial composition of thBILL consists entirely of tULTRA, a wrapped tokenized representation of a U.S. Treasury fund. Future deployments are expected across Ethereum, Hyperliquid, HyperEVM, Base, and Arbitrum.

thBILL combines the benefits of regulatory compliance with the unique capabilities of onchain finance, including real-time settlement, 24/7 availability, and composability with DeFi protocols. Key institutional partners enabling this structure include:

Wellington Management: One of the world’s largest independent investment managers with over $1.5T in AUM. It constructs and manages the underlying U.S. Treasury portfolio for thBILL.

Libeara: A tokenization platform incubated by Standard Chartered’s SC Ventures. Libeara wraps FundBridge-managed fund shares into the tULTRA token, enabling onchain representation.

FundBridge Capital: A licensed entity under the Monetary Authority of Singapore (MAS). It serves as the legal fund administrator for the structure and ensures investor protections through a Delta Master Trust that isolates fund assets from operator risk.

LayerZero: Supports omnichain functionality for thBILL, allowing it to operate as an OFT (Omnichain Fungible Token) and be natively transferred across multiple public chains for greater DeFi integration.

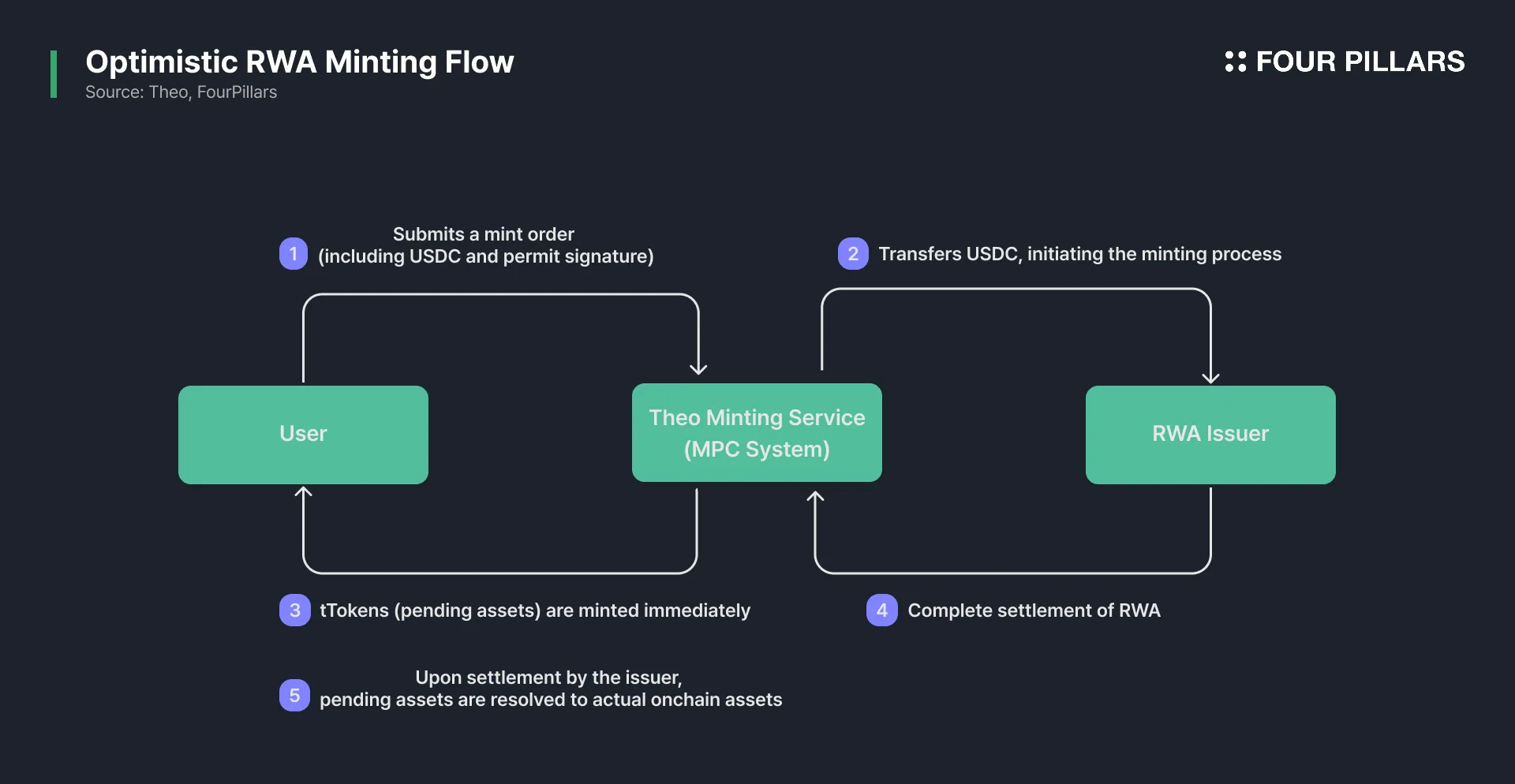

If thBILL were merely another tokenized asset, it would offer limited differentiation. What sets it apart is Theo’s Optimistic RWA Minting, a mechanism that allows real-time asset minting at block-level quotes, with backend settlement deferred. This design reduces friction and improves capital efficiency for market makers. The process works as follows:

User Submission: A user submits a minting request to Theo’s minting service, including USDC and a permit signature. This signature grants token allowance without requiring an onchain approval transaction.

Fund Transfer: Theo’s MPC (Multi-Party Computation) backend validates the permit and transfers USDC to the RWA issuer, initiating the purchase of real-world assets.

tToken Issuance: Upon USDC receipt, a tToken is minted immediately and recorded onchain as a pending asset. The user receives immediate liquidity, although settlement is not yet finalized.

Final Settlement: Once the RWA issuer completes settlement, the pending asset is converted into a fully-backed onchain position, completing the minting process.

This method draws inspiration from T+0 liquidity processing and pre-settlement models in traditional finance. It is especially well suited to low-volatility RWAs such as MMFs, but can also extend to equities and commodities. From a market-making perspective, optimistic minting addresses two key pain points:

Liquidity Constraints for Market Makers:

Since RWAs require real collateral, market makers cannot freely mint or borrow tokens in advance. Optimistic minting allows them to quote real-time block-level prices, fulfill trades immediately, and settle only the required quantity afterward. This decouples inventory risk from liquidity provisioning, enabling more flexible and scalable operations.

NAV-Based Pricing Limits Spread Opportunities:

Most RWA products are priced off a static NAV updated once per day. This limits price discovery and makes spread-based arbitrage difficult. Optimistic minting solves this by introducing real-time quoting at every block. Onchain users can mint or redeem tokens instantly at block prices, enabling more frequent price discovery and potential arbitrage opportunities.

While this model introduces backend dependencies and requires secure reconciliation of pending assets, it reflects Theo’s core philosophy: designing a liquidity-first RWA architecture from the asset layer upward. Starting with thBILL, Theo plans to expand into other categories such as equities, commodities, and fixed income.

To conclude, it is useful to reference the playbooks of leading players in the crypto market when clarifying the position Theo seeks to occupy in the RWA market. In fact, part of the renewed attention to RWAs in this cycle reflects a base effect arising from disappointment with many crypto-native projects. Put differently, although we are surrounded by countless projects and altcoins, truly competitive products on the strength of the product itself remain exceedingly rare.

Among the few exceptions, Hyperliquid stands out as a project that achieved meaningful product‑market fit. What gave it its edge? If its competitive advantages were to be distilled into two points, they would be:

Liquidity: Delivered superior execution through a deep order book and an ultra‑fast matching engine.

Trading Volume: Generated a stable revenue stream underpinned by large‑scale trading activity.

These advantages are simple to state yet difficult to replicate, creating a durable moat and setting a new benchmark for the perpetual futures DEX sector. Theo’s playbook in the RWA market follows a similar pattern:

Make RWA trading more accessible through deep liquidity and issuance/settlement infrastructure optimized for RWAs.

Build a stable value accrual structure on the foundation of active RWA trading.

In essence, Theo aims to satisfy both pillars of strong market competitiveness demonstrated by prior success stories: robust infrastructure and the ability to capture sustained trading volume. In this light, Theo’s strategy in RWAs can be compared to a Hyperliquid moment in the perpetual futures DEX.

In meeting the requirements for successfully realizing such a turning point, Theo is clearly well‑positioned. The company was founded by former market makers, has secured funding from leading market‑making firms, and is led by executives with extensive experience in tradfi. Whether its “Beyond the Issuance” vision will prove to be the key that bridges tradfi and onchain remains to be seen, but it will be worth watching how it unfolds.

Theo Docs - https://docs.theo.xyz/

Dive into 'Narratives' that will be important in the next year