Neutrl’s core play is built on three main sources: buying locked tokens at steep discounts via OTC deals and hedging them with perp shorts, earning funding premiums from basis trades, and staking yield on hedged locked collateral when possible.

Together, these package hedgefund grade strategies into a synthetic dollar so ordinary users can access real trading yield.

The product is already drawing capital, with about $50 million in private beta deposits earning around 29% APR, and the opportunity set is vast: $55 billion in token unlocks over the next two years and $200~400m in monthly OTC volume.

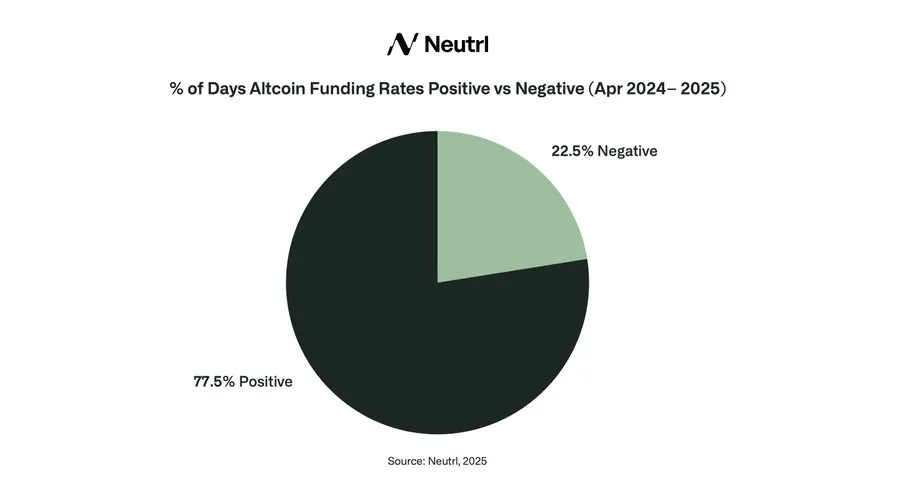

Altcoin funding rates reward shorts roughly three quarters of the time (funding was positive on about 77.5 % of days between April 2004 and April 2005), so basis trades tend to pay shorts rather than cost them.

To harvest these spreads safely, Neutrl uses KYC, escrow and legal checks with counterparties, hedges price exposure and keeps reserve buffers to ride out negative funding or market shocks.

In tradfi, market neutral strategies (e.g. arbitraging price differences while hedging away directional risk) are the domain of hedge funds and trading desks. They require capital, access and expertise, so retail investors rarely benefit.

Neutrl aims to change that. It issues a synthetic dollar, NUSD, that behaves like a dollar but accrues yield from real trading profits. The core idea of Neutrl’s NUSD is a simple one. Proven strategies, such as buying discounted locked tokens with hedges and earning futures funding premiums, are packed into a product anyone can hold. This neutralizes directional risk, meaning that the yield accrued by NUSD doesn’t depend on crypto price swings. Rather, it depends on capturing structural mispricings that exist in all markets.

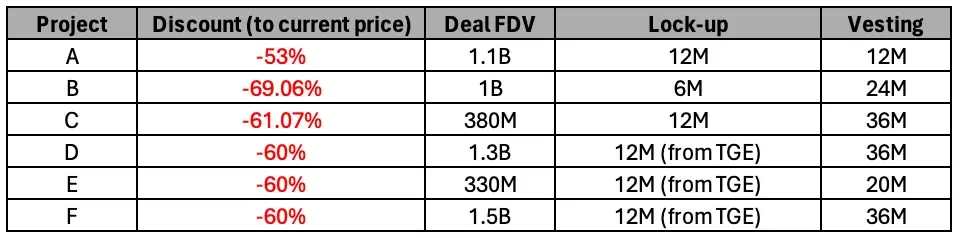

Crypto projects often release tokens on long vesting schedules. When sentiment cools or investors need liquidity, these locked allocations trade at steep discounts in the secondary market. Presto Labs reports that in 2024 many top 20 tokens changed hands at about a 50% discount, and lesser known projects sold at 70% or more. Buyers effectively pay pennies on the dollar for assets that will unlock later. Such spreads exist because sellers need liquidity before tokens unlock, while buyers are scarce.

Source: Presto Labs

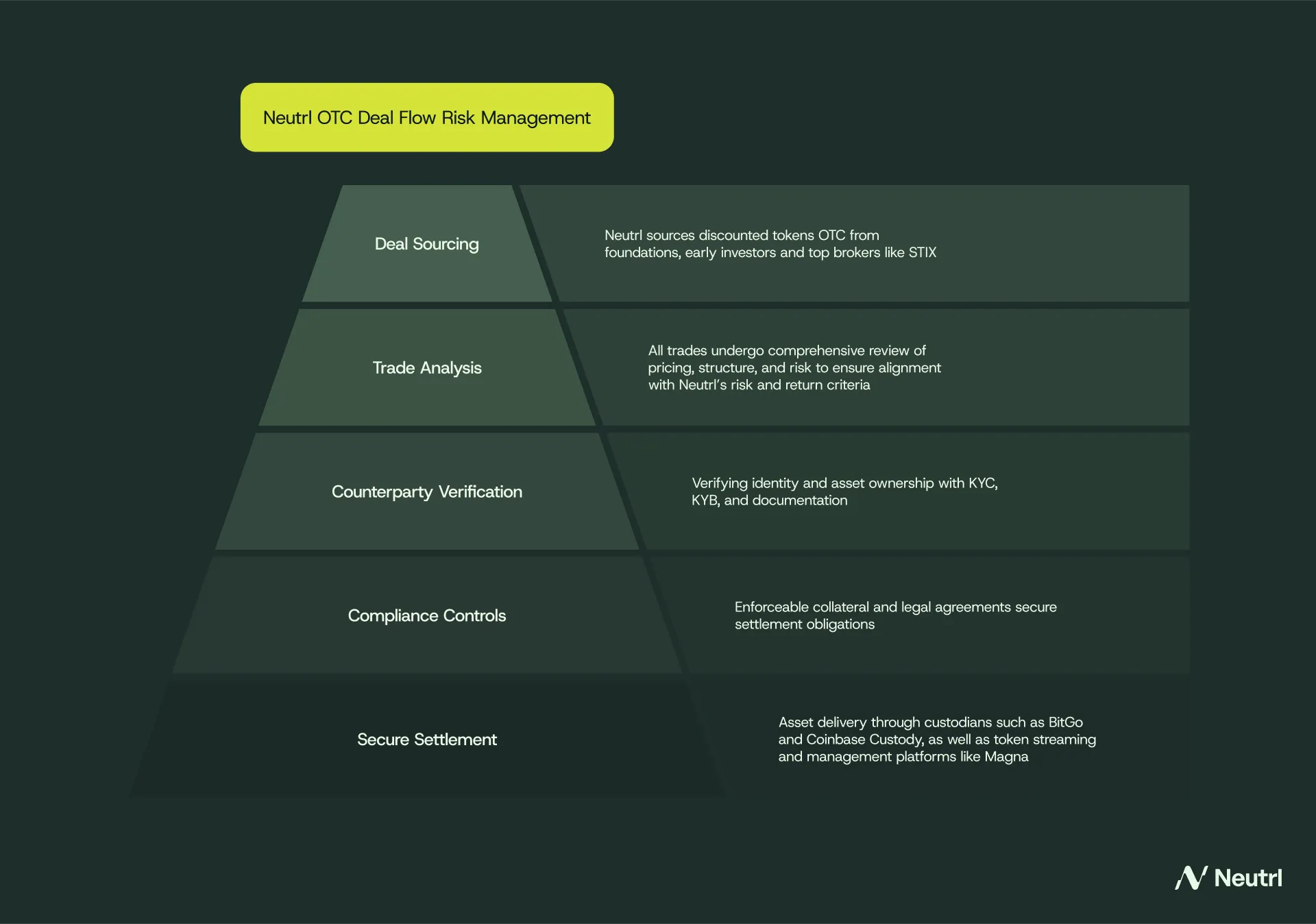

Neutrl sources these deals through foundations, VCs, private funds, and institutional platforms like STIX, where sellers are KYC/KYB checked, prove ownership of their allocation and settle via custodians or smart contracts. Once Neutrl buys the tokens, it shorts an equivalent futures or perpetual contract. This hedge neutralizes price movements. When the token unlocks, Neutrl unwinds the hedge and captures the discount as profit. Because the return comes from the spread between private and public prices, it is independent of whether crypto markets rise or fall.

The second pillar is the basis trade. In crypto futures markets, perps frequently trade at a premium to spot because levered traders are willing to pay for long exposure. Short sellers receive a funding payment from longs.

Ethena’s analysis shows that over the past 3 years BTC and ETH funding rates have averaged 7.8~9% annualized and negative funding days have been rare. The trade is straightforward: buy spot, short the perp, and collect funding from the longs. Neutrl doesn’t restrict itself to BTC and ETH; STIX notes that the same premium exists across hundreds of altcoin perps. Diversifying across many assets reduces concentration risk and increases the likelihood of earning positive funding even when majors briefly pay little.

Together, discounted token trades and basis trades form a delta‑neutral engine. Returns come from structural spreads instead of betting on price. These strategies are standard fare for hedge funds; Neutrl simply tokenizes them and shares the yield.

In some OTC deals, the locked tokens held as collateral can be staked on-chain — for example, delegated to validators or put into liquid staking protocols. Neutrl takes advantage of this when possible, staking the hedged collateral to earn additional rewards during the lock period. Since the tokens are already delta-hedged via perps, the staking income adds to returns without introducing directional risk. The level of staking yield depends on the underlying asset and network conditions, but it can provide a meaningful boost to overall performance and help smooth the APY when other yield sources tighten.

Skeptics worry about two things: 1) getting burned in an OTC deal 2) having positions frontrunned if trades are public. Both concerns are valid, but they are also manageable.

Source: Neutrl

Avoiding bad counterparties: The worst OTC losses happen when you trade with strangers in private chats. A report on CryptoRobotics recounts an “astonishing $50 million fraud linked to a Telegram OTC scam.” By sourcing deals through trusted platforms like STIX, Neutrl minimizes counterparty risk. Sellers pass identity checks, prove token ownership, and settle via regulated custodians or smart contract escrows rather than p2p transfers. Legal contracts govern the transaction, and sellers may be required to post collateral. These steps drastically reduce the risk of defaults.

Balancing transparency and secrecy. Investors need to know that NUSD is fully backed; traders need secrecy until a deal settles. Neutrl therefore reports aggregate exposures and risk metrics on‑chain. For example, it can publish total value in OTC deals, the size of basis positions, daily value at risk and collateral buffers without revealing the exact token or exchange. Proof of reserve attestations verify that the assets exist. Once a trade is settled, more detail can be disclosed. This approach provides confidence that the backing is real while limiting information that traders could use to frontrun or manipulate markets.

Hedging and diversification reduce the payoff for attackers. Neutrl’s positions are hedged. Pumping the spot price of a hedged token will have limited effect on a short perp hedge. By diversifying across many small positions, Neutrl avoids creating a single juicy target. It also maintains liquidity buffers and can adjust or close positions if a market becomes prone to manipulation. Assets are held off-exchange, so exchange failures or extreme wicks do not trap the collateral.

Careful process design makes opaque, risky OTC trading safe and auditable without sacrificing trade economics.

Critics point out that in a bear market perpetual contracts can go into backwardation, meaning shorts receive funding from longs. In that environment, a long spot/short perp position loses money. The risk is real, but Neutrl is well positioned to respond to such an outcome

Source: X (@behrin_n)

Consider several points:

The data favour positive funding.

Altcoin funding rates have been positive far more often than not. Over the past year (Apr 2024 – Apr 2025), they were positive on 77.5% of days and negative on just 22.5%, with an average annualised daily funding rate of 4.7%, despite this being one of the toughest funding environments in recent history. This positive bias reflects the mean reverting nature of spot–future basis: extreme conditions tend to self correct as traders step in to capture the other side of the trade.

Ethena’s funding analysis shows a similar bias for BTC and ETH: negative less than 1/5 of the time, with healthy positive averages. Negative streaks have historically been short (the longest lasting 13 days), implying that positive funding is the norm, not the exception.

Bear markets create deeper OTC discounts. When sentiment sours, more sellers need liquidity and fewer buyers exist. As mentioned above top tokens were trading at ~50% discounts and smaller ones at 70%. Taran (founder of STIX) observed investors dumping alts at 70~80% discounts as markets turned risk off. Those discounts more than offset a few percent of negative funding. For a delta‑neutral arbitrageur, bear markets can increase opportunity by widening spreads.

Dynamic allocation protects capital. A well run delta neutral protocol doesn’t blindly keep all assets in perps. Ethena maintains a reserve fund and can move backing assets into liquid stables (earning treasury yields) when funding is low or negative. Ethena’s treasury backed product (USDtb) provides a lower risk yield floor when crypto funding underperforms. Neutrl can do the same: if funding drops, park more collateral in tokenized T‑bills or money market tokens and rely more on OTC arbitrage.

Diversify across assets. Funding may be negative on majors but positive on long tail tokens. Taran highlights that the funding/OTC arbitrage remains open on hundreds of alts. Rotating into those markets when majors pay poorly smooths returns.

Accept variability. Yield will fluctuate. It might be high in bull markets and lower in prolonged bears. The principal remains hedged and backed. For example, Ethena’s USDe supply grew to roughly $2.39b within two months of launch due to high funding, then growth stalled when yields compressed. The system didn’t implode; it just paid a lower APY and cut fees. Investors in delta‑neutral stablecoins should expect variable returns, not fixed yields.

With proper risk management, negative funding becomes a factor to monitor and hedge around, not a fatal flaw.

The other major worry is capacity: will there be enough OTC deals to deploy billions of dollars? The evidence suggests probably yes.

Source: Neutrl

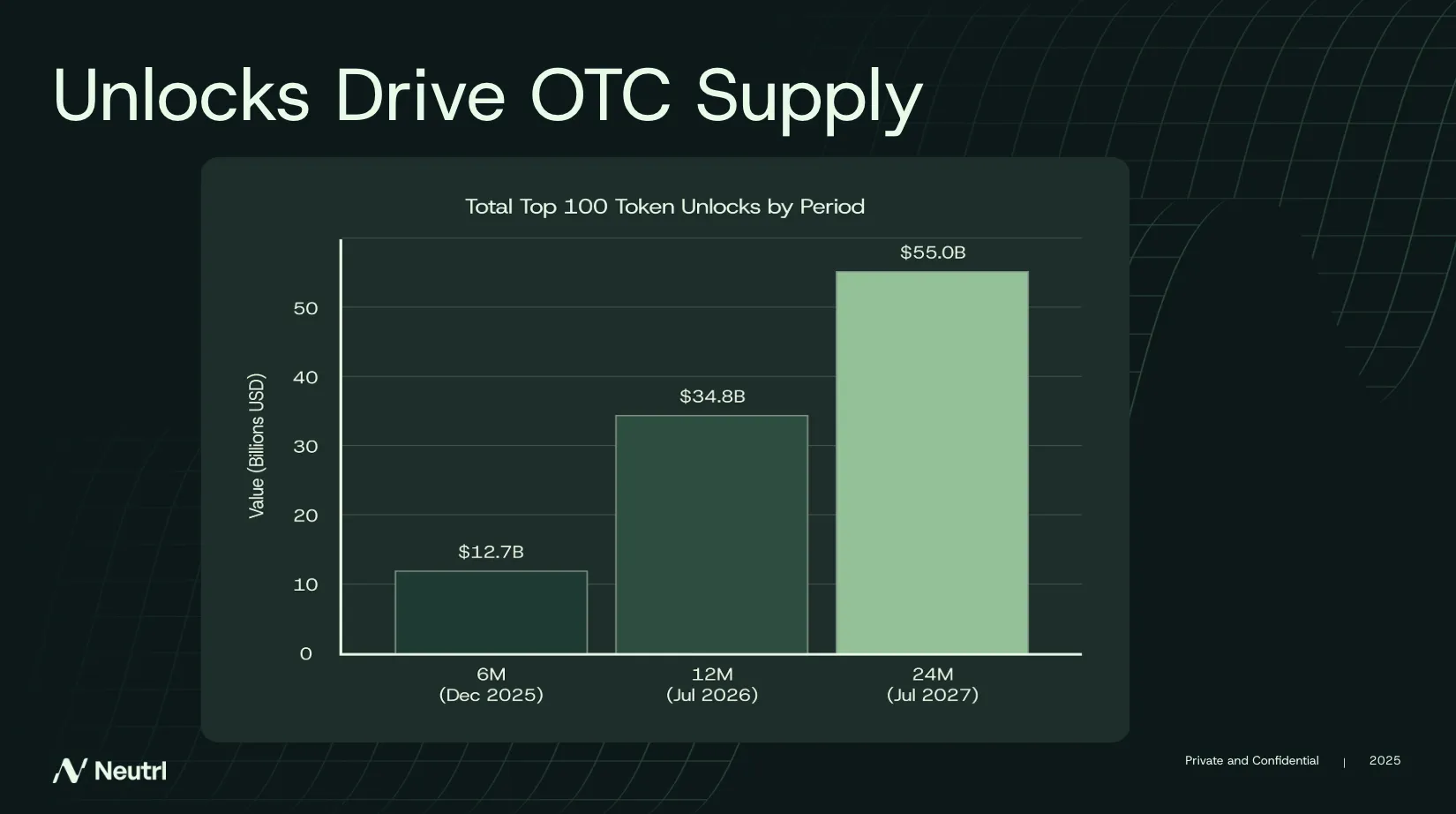

Massive and steady unlock pipeline. Over the next two years, more than $55 billion worth of tokens from the top 100 altcoins will unlock and enter circulation, ensuring a constant stream of potential discounted deals. In past cycles, STIX’s flow has shifted from prelaunch tokens to locked blocks of newly launched tokens, with continuous monthly unlocks and new project cliffs keeping inventory high.

Active trading volumes. The monthly trading volume in OTC secondary markets is already estimated at $200~400m, with activity spread across hundreds of assets.

Dual strategies provide flexibility. Neutrl is not locked into OTC trades. When deals are scarce (such as in a euphoric bull market where nobody wants to sell cheaply) funding premiums are usually high, so basis trades can absorb capital. When funding premiums compress (a sign of cooling markets), more sellers typically offer discounted tokens. The practice of early investors block trading altcoins at steep discounts to de‑risk isn’t going away and spans hundreds of assets. Block trades at heavy discounts are common in downturns. The two strategies naturally balance each other.

Demand for real yield is enormous. Ethena’s rapid growth shows that if you offer a double digit return backed by real trading revenues, billions of dollars will flow in. Neutrl does not need to corner the entire OTC market; capturing a small share could still support billions in assets.

For these reasons, deal flow should be sufficient for Neutrl’s early years. Over time, success may attract competition and compress spreads, but the crypto ecosystem continually mints new tokens and new inefficiencies. The question is not whether there is enough supply, but whether Neutrl can choose the right opportunities and manage risk prudently.

Neutrl is a disciplined attempt to make three proven, market neutral strategies (buying discounted locked tokens, capturing perp funding premiums, and staking yield on hedged collateral) accessible to everybody. These mispricings are real and substantial, though they will shift over time. Yield will ebb and flow with market conditions, and execution discipline will be just as important as the strategies themselves.

The early traction suggests there’s strong demand for this approach—about $50 million in private beta deposits are currently earning around 29% APR. This isn’t yield from token incentives or unsecured lending. It comes from real, tradable market inefficiencies.

By systematizing and tokenizing these trades, Neutrl could change the very OTC market it relies on, making it more transparent and liquid, which benefits the broader ecosystem even as it may compress spreads over time.

If executed with discipline, Neutrl has the potential to become one of the most robust yield generating synthetic dollar in DeFi: Fully backed, delta-neutral, and driven by institutional grade trading strategies that were once inaccessible to ordinary users. That’s the core of its USP, and the reason its approach can stand out even as the synthetic dollar space grows more competitive.

Dive into 'Narratives' that will be important in the next year