Ethena manages a multibillion-dollar collateral mix (ETH, BTC, SOL, USDtb, etc.) with automated short positions across major derivatives venues, maintaining a flawless peg under extreme market volatility.

While a traditional hedge fund might need an entire floor of risk specialists to handle similar swings, Ethena’s lean 26-person team executes seamless rebalancing 24/7, avoiding any margin blowouts or depegs.

Institutional credit lines, multi-venue analytics, and a reserve fund for negative funding episodes create a near-impossible barrier for newcomers seeking to replicate Ethena’s $5 billion scale.

By introducing iUSDe for institutional compliance and leveraging interest-rate arbitrage, Ethena aims to bridge crypto yields and TradFi capital, driving USDe supply toward $25 billion.

Have you ever tried eating hot noodles while riding a rollercoaster? It might sound absurd, but it’s the best analogy for what Ethena accomplishes daily: it maintains a $5B market-cap stablecoin (USDe) that stays at $1 despite the nonstop chaos of crypto volatility. And it does all this with just 26 people on the team. This memo dives into Ethena’s secret sauce, shows why it’s so hard to replicate, and explains how Ethena plans to push USDe toward $25B in circulation.

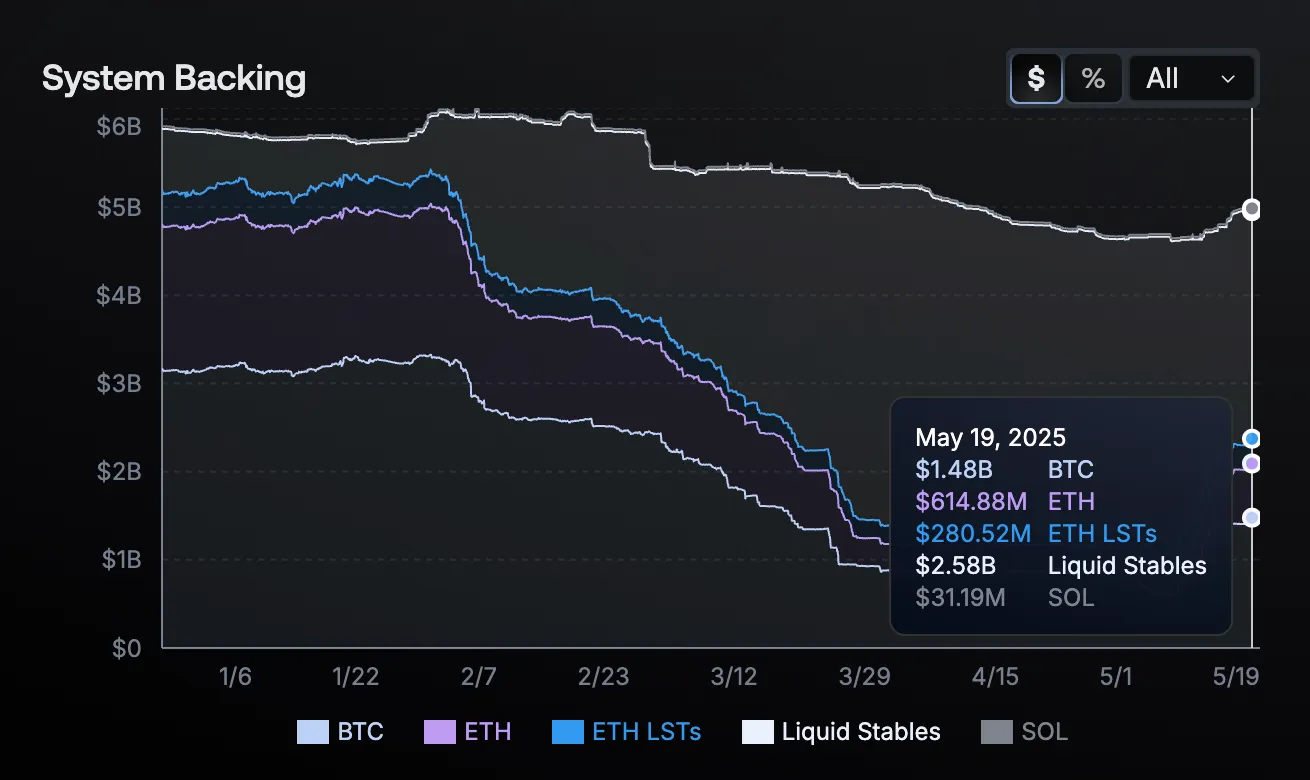

A stablecoin typically looks boring: $1 is $1, right? But if you look under the hood at Ethena, it’s anything but simple. Rather than backing its stablecoin with dollars in a bank, Ethena employs a robust mixture of ETH, BTC, SOL, ETH LSTs, and liquid stables, and even $1.44 billion worth of USDtb (a T-bill-backed stable asset). These assets are continuously shorted on major derivatives markets so that any fluctuation in the collateral’s price is offset by a corresponding gain or loss in the short position.

Source: Ethena Transparency Dashboard

If ETH pumps 5% and your hedge ratio slips, that could be tens of millions in unprotected exposure. If markets tank at 3am, your risk engine must instantly rebalance collateral or close positions. The margin for error is minuscule. Yet Ethena has run billions in daily hedging without a single meltdown (no depegs, no margin blowouts, no shortfalls) all through 2023–2024’s rollercoaster markets.

This stability also held firm during the Bybit hack, where Ethena remained solvent and emerged without any collateral losses. A traditional hedge fund might need an entire floor of analysts and traders just to handle this level of volatility, yet Ethena does it with a lean crew and zero drama.

Within months of launching, Ethena was the largest counterparty on multiple centralized exchanges. Its hedging flows even influenced liquidity and order book depth, yet few people noticed because the stablecoin just “worked.”

*About that high yield: Ethena has offered double-digit APYs when market conditions are bullish. Observers initially recalled Terra/LUNA and its 20% Anchor fiasco. The difference is that Ethena’s yields come from real market inefficiencies (staking rewards plus positive perp funding rates, etc.) rather than minted tokens or unsustainable subsidies.

When a user deposits $1k ETH, they can mint ~$1k USDe. The protocol automatically opens a short futures position. If ETH’s price goes down, the short makes money that offsets collateral losses; if ETH goes up, the short loses but the collateral gains. The result is net dollar value stays stable. Meanwhile, when perpetual markets get overleveraged on the long side, Ethena (holding the short) can collect funding fees, enabling USDe to offer double-digit APYs under bullish conditions, all without treasury subsidies.

Ethena spreads these hedges across Binance, Bybit, OKX, and even some decentralized perp protocols to avoid single-exchange risk and margin limits. A recent governance proposal reveals plans to add Hyperliquid to this mix, letting Ethena short perps wherever it finds the deepest liquidity. By diversifying short positions, Ethena reduces reliance on any one venue, further shoring up stability.

Source: Ethena Transparency Dashboard

To handle the nonstop adjustments, Ethena deploys automated bots in conjuncture with the trading team (similar to high-frequency trading systems) that constantly rebalance the entire multi-venue book. This is how USDe stays pegged regardless of the market’s wild swings.

Finally, the protocol is over-collateralized to handle extreme drops and can pause minting if conditions become unsafe. Custodial integrations (Copper, Fireblocks) let Ethena keep real-time control of its assets rather than leaving them in an exchange’s hot wallet. If an exchange goes bust, Ethena can undelegate collateral quickly, insulating users from single-point-of-failure disasters.

Ethena’s approach might look replicable in paper (delta-hedge some crypto, collect funding, profit), but in reality, the protocol has built formidable moats that deter copycats.

One key hurdle is trust and credit lines: Ethena hedges billions off-exchange through institutional deals with custodians and major venues (Binance Ceffu, OKX). Most smaller projects cannot just waltz into these institutions and negotiate minimal on-exchange collateralization for multi-million-dollar short positions; that access requires legal, compliance, and operational rigor at an institutional level.

Equally critical is multi-venue risk management. Splitting large hedges among multiple exchanges demands real-time analytics on par with a major Wall Street quant operation. Yes, anyone can replicate delta-hedging at a small scale, but scaling to $5 billion (and rebalancing enormous collateral across multiple platforms around the clock) is on another level. The scope of analytics, automation, and credit relationships required increases exponentially with size, making it nearly impossible for a new entrant to match Ethena’s scale overnight.

Meanwhile, Ethena does not rely on perpetual free yield. If perp funding turns negative, it dials back short positions and leans on staking or stablecoin yields. A reserve fund buffers extended negative-funding episodes, whereas countless high-yield DeFi protocols collapsed when the music stopped.

Counterparty risk is further minimized by never holding the entire collateral pool directly on any single exchange; instead, Ethena stores assets with custodians. If one venue becomes unstable, Ethena can quickly unwind positions and secure its collateral off-exchange, ensuring minimal risk of a catastrophic failure.

Finally, Ethena’s track record under extreme volatility cements its moat. USDe has survived months of severe market swings without a single peg break or meltdown. That reliability spurs new adoption, listings, and prime brokerage deals (from Securitize to BlackRock and Franklin Templeton), generating a snowball effect of trust no fork can copy-paste. The difference between talking about delta-hedging and delivering it at multi-billion scale 24/7 is precisely what separates Ethena from the crowd.

Ethena’s growth strategy hinges on a self-reinforcing ecosystem in which money (USDe), network (the “Converge” chain), and exchange/liquidity aggregation evolve simultaneously. USDe arrived first, propelled by crypto-native demand in DeFi (Aave, Pendle, Morpho) and CeFi (Bybit, OKX). The next phase involves iUSDe, a regulated version suited for banks, funds, and corporate treasuries that need compliance wrappers. Even a modest slice of TradFi’s enormous bond market, if drawn into USDe, could multiply the stablecoin’s float to $25B or more.

Driving this growth is arbitrage between on-chain funding rates and traditional interest rates. As soon as there is a meaningful yield gap, money will flow from low-rate markets to high-rate markets until equilibrium is reached. USDe thus becomes the pivot point that aligns crypto yields with macro benchmarks.

Source: Ethena 2025: Convergence

Meanwhile, Ethena is developing a Telegram-based app that introduces high-yield dollar saving to everyday users, bridging hundreds of millions into sUSDe through a user-friendly interface. On the infrastructure side, the Converge chain will weave DeFi and CeFi rails together, so each new integration amplifies liquidity and utility for USDe in a continuous cycle of growth.

Notably, sUSDe’s returns are negatively correlated to real rates, as evidenced in Q4 2024 when the Fed’s 75bps rate cuts coincided with a jump in funding yields from ~8% to beyond 20%, underscoring how declining macro rates can turbocharge Ethena’s yield potential.

This is no slow, phase-by-phase grind but a circular expansion: broader adoption reinforces USDe’s liquidity and yield potential, which then draws larger institutions, fueling further supply growth and a stronger peg.

Ethena is not the first stablecoin to promise strong yields or position itself as an innovative approach. The difference is that it has delivered, holding USDe firmly at $1 through some of the market’s worst shocks. Behind the scenes, it operates like a high calibre institutional outfit, shorting perpetual futures and managing staked collateral. The average holder, however, experiences a stable, yield-bearing dollar that just works.

Scaling from $5B to $25B will be no trivial step. Heightened scrutiny from regulators, larger counterparty exposures, and potential liquidity crunches could pose new risks. Yet Ethena’s multi-asset collateral (including $1.44B in USDtb), strong automation, and robust risk management suggest it is better equipped than most.

Ultimately, Ethena is rewriting stablecoin standards, demonstrating how to harness crypto’s volatility under a disciplined, delta-neutral strategy at mind-boggling size. It’s a vision of a future where USDe stands at the heart of every financial domain, from DeFi’s permissionless frontiers and CeFi’s trading desks to TradFi’s colossal bond market.

Dive into 'Narratives' that will be important in the next year