*Asia Stablecoin Alliance is launched by Heechang Kang and Jinsol Bok from Four Pillars, along with Alex Lim (Jongkyu Lim), the Korea lead at LayerZero, to accelerate stablecoin adoption across Asia and to serve as a research and community hub for establishing clear stablecoin strategy and technical infrastructure. (X Link, Substack Link)

Stablecoins is the most ideal form of asset, as its programmability expands the functional limits of traditional money.

Major Asian IT platforms, or “super apps,” has a wide range of services and are central to daily life and national competitiveness; stablecoins can enhance these platforms by streamlining financial interactions and being the financial rail for these platforms.

For stablecoins to serve as foundational financial infrastructure, collaboration among IT platforms, banks, and non-bank institutions is essential, enabling cross-platform integration, secure collateral management, and the creation of seamless experience.

Successful adoption of stablecoins in Asia requires clear legal frameworks supporting capital market-based models, the formation of consortiums to avoid ecosystem fragmentation, and strategic partnerships between platforms and financial institutions to maximize user benefits and market reach.

The question of why Asian countries need their own stablecoins is similar to asking why we need local currencies like the Korean won when the dollar already exists. As our societies continue to digitize, stablecoins emerge as the most ideal form of currency, expanding the functional limits of traditional money.

In Asia, where digital adoption is already widespread, introducing stablecoins specific to each country opens vast potential across numerous sectors. Beyond simply serving as digital points like Naver Points or Wechat Points, stablecoins could facilitate scenarios previously imagined in blockchain’s optimistic future - such as streamlined trade settlements between businesses, automated tax deductions for charitable donations, and automatic discounts across affiliated platforms.

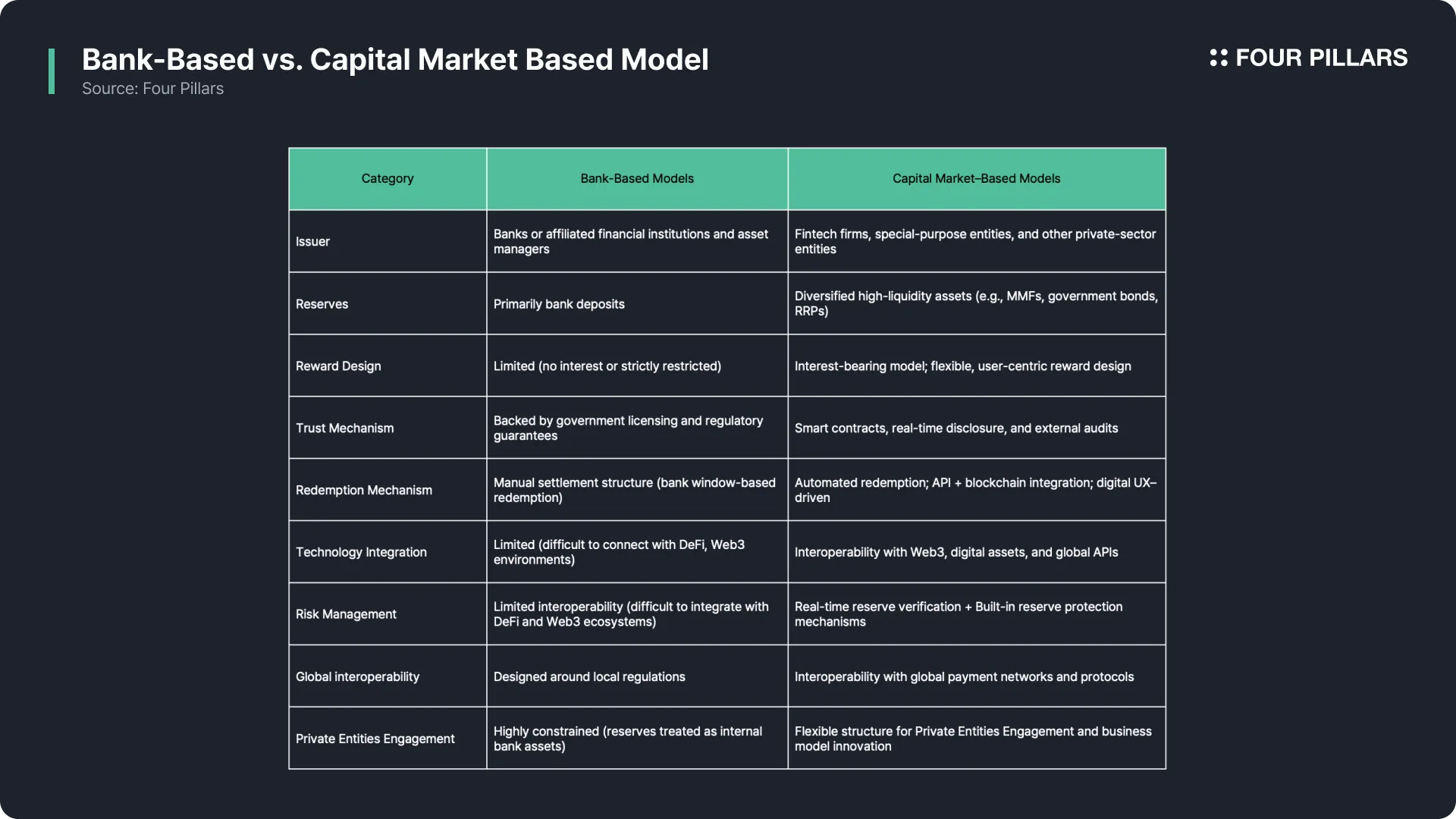

Stablecoins have the potential to alter public perception, challenging existing skepticism toward “cryptocurrencies” whose underlying value is often unclear. To effectively leverage this potential, adopting “capital market-based stablecoins” is essential. Such stablecoins move beyond merely tokenizing bank deposits; they involve diverse non-bank institutions, fintech companies, and other entities issuing stablecoins backed by highly liquid cash-equivalent assets exceeding 100% reserve ratios.

Given the significant reliance on a few dominant IT platforms, or “super apps,” across Asian countries, creating an interconnected financial ecosystem through stablecoins could deliver the ideal digital financial experience.

Ultimately, the usability and success of stablecoins depend heavily on the strategies adopted by their issuers and operators. Limiting issuance and operation solely to banks constrains the strategic opportunities available to stablecoins. However, this does not diminish the critical role of banks; rather, banks become foundational institutions ensuring stability through collateral asset management and reserve oversight. To maximize market penetration, banks must strategically partner with leading platforms and enterprises like Grab, Naver, and SK Telecom, which would act as operators.

This article highlights why stablecoins are destined to proliferate, emphasizing the particular importance and suitability of capital market-based stablecoins within the Asian context.

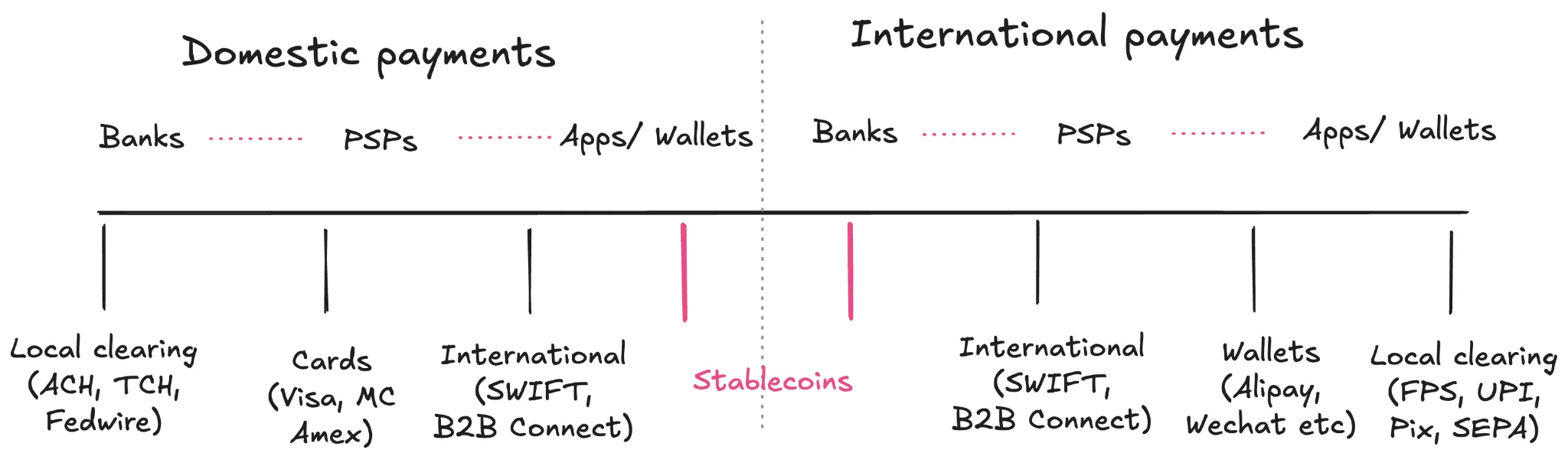

Stablecoins are blockchain-based assets accessible globally, 24/7, without geographical or temporal constraints. They offer two essential programmable characteristics: programmable functions and programmable collateral.

Programmable functions enable smart contracts to automatically incentivize or automate specific user behaviors under predefined conditions. Meanwhile, programmable collateral means stablecoins can be issued against both off-chain assets like bank deposits and government bonds, and on-chain assets such as USDC and ETH. This collateral can be transparently managed and verified on the blockchain. Therefore, stablecoins bridge the gap between traditional and digital financial assets, significantly enhancing automation and transparency within the financial sector.

This versatility positions stablecoins as foundational infrastructure for various services, including fast and inexpensive remittances, programmable payments, DeFi lending and deposits, and cross-border settlements. Stablecoins democratize access to financial services even for users without traditional bank accounts, allowing developers to innovate and create new financial products and applications. Hence, stablecoins transcend being mere payment methods, evolving instead into critical infrastructure within the digital economy - platforms themselves.

A platform, by definition, is an environment or system facilitating value exchange among diverse participants. Stablecoins fit this definition perfectly, extending beyond merely stable digital currencies to enabling a broad range of financial services and applications.

For example, PayPal's PYUSD is a stablecoin pegged 1:1 to the US dollar and operates across various blockchains, including Ethereum, Solana, and Stellar. PYUSD supports global payments, instant transfers, and business-to-business transactions. It is integrated into global corporations such as PayPal, SAP, and Coinbase, supporting practical use cases like transfers, payments, invoicing, and real-time funding. Developers and businesses can easily build new applications and services on the PYUSD infrastructure, demonstrating stablecoins' role as platforms connecting users and services and offering innovative value beyond traditional payment systems.

Ultimately, stablecoins represent not just currencies but expansive digital financial platforms connecting diverse financial and non-financial services, powering the future digital economy.

Source: Stablecoins are a new platform

Asia’s major IT platforms are expanding, with both global giants and regional leaders actively competing to establish dominant positions. Unlike the West, Asian platforms have evolved into "super apps," integrating diverse services such as news, shopping, payments, social media, and mobility into single, unified apps. Users rely on these platforms to address almost every aspect of daily life.

These platforms go beyond mere economic activity, significantly influencing social interactions, information dissemination, and even political discourse. In Korea, platforms like Naver and Kakao reflect local cultural preferences and integrate various services such as messaging, shopping, search, and donations, continuously broadening their scope.

Asian countries also regard these platforms as critical to national competitiveness and digital sovereignty, strategically nurturing local platforms to counter foreign dominance.

Korea, China, and Japan leverage domestic platforms to protect cultural, linguistic, and economic ecosystems, positioning themselves competitively on a global scale. Consequently, these platforms are central hubs of innovation and critical drivers of new economic ecosystems.

Stablecoins can significantly enhance these ecosystems by facilitating more efficient economic interactions within or across each platform’s environment.

Source: Super App Strategy: How To Make A Profit From Super Apps

Asian super apps like KakaoTalk, Naver, and WeChat already provide comprehensive services encompassing messaging, payments, shopping, investments, insurance, and donations, thereby creating extensive digital economic ecosystems. KakaoTalk, for instance, enables convenient money transfers through KakaoPay, shopping via KakaoShopping, donations via KakaoTogether, and financial investments through Kakao Securities.

Stablecoins could further strengthen these interconnections by introducing robust incentive structures across these services. For example, users might receive discounts or rewards points for using services within the platform, increasing service usage frequency and user loyalty.

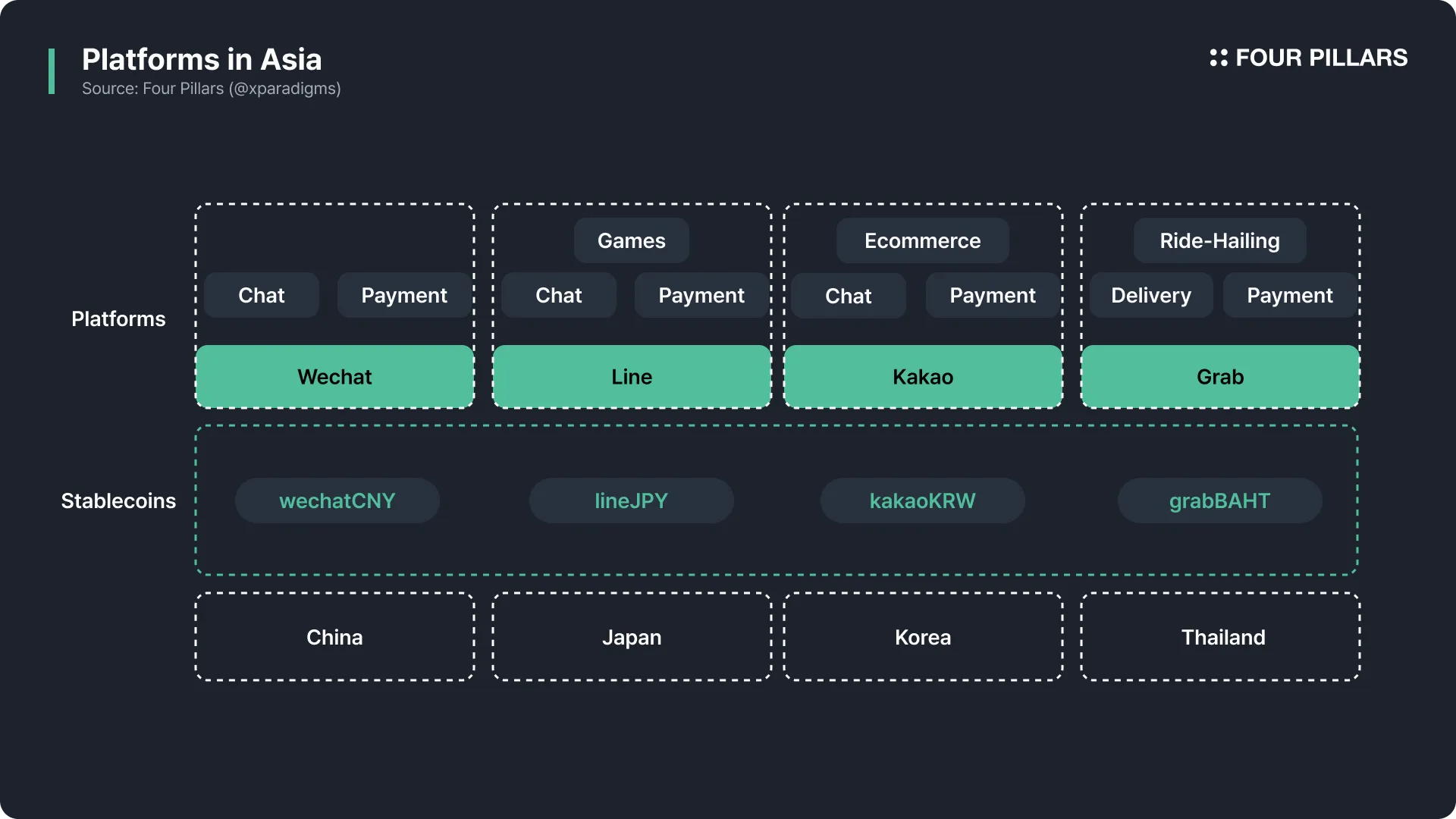

Moreover, interoperability between stablecoins issued by different platforms, such as kakaoKRW, naverKRW, rakutenYEN, and tencentCNY, could create a seamless financial ecosystem across platforms. This integration would facilitate cross-platform financial transactions and asset management across national and corporate boundaries, enhancing user convenience and establishing a robust digital economy.

Achieving this vision requires collaboration among IT platforms, banks, and non-bank financial institutions to secure and manage collateral assets, issue and redeem stablecoins, and ensure transparency and trust through monitoring systems. A cooperative infrastructure, possibly involving cross-national partnerships and global entities, is crucial for stablecoins to become essential financial infrastructure in Asian digital economies.

Asian countries are increasingly developing specific regulatory frameworks for stablecoins. Hong Kong has enacted the Stablecoin Act, Japan has clarified its legal framework through the Payment Services Act (PSA), and Korea is progressively establishing regulations under its Digital Asset Basic Act. Successful adoption requires several key considerations:

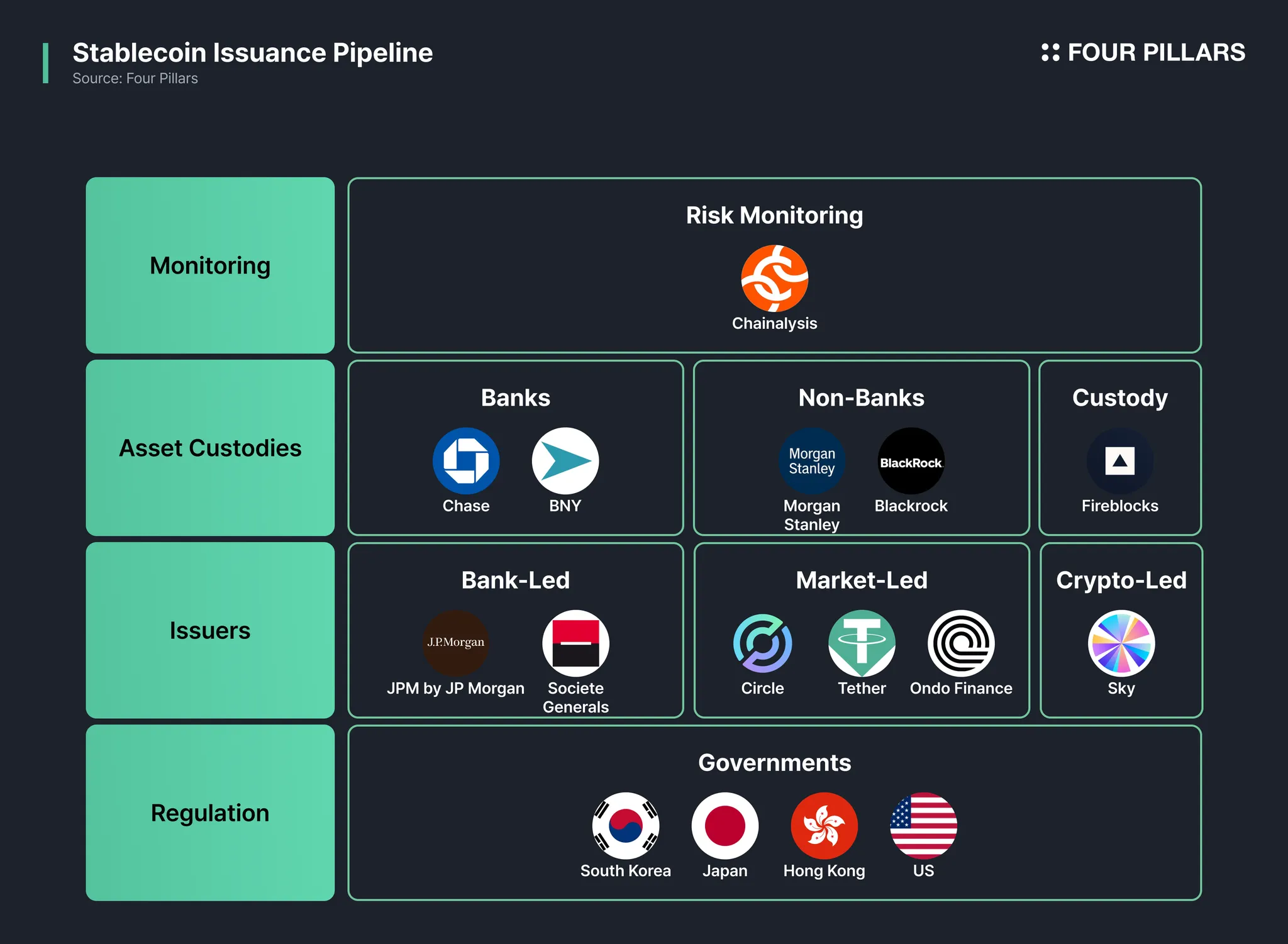

Future market growth in stablecoins will likely be driven by capital market-based issuance models. Unlike traditional bank-issued stablecoins backed by bank deposits, capital market-based models utilize a diverse range of collateral assets, such as government and corporate bonds, managed by fintech firms and non-bank financial institutions.

Although bank-issued stablecoins excel in financial stability and regulatory compliance, they face scalability and innovation constraints. Comprehensive growth depends on strategic partnerships with various enterprises. Therefore, Asian countries should enact clear legislation, referencing initiatives like the U.S. Genius Act and Hong Kong’s Stablecoin Act, to support capital market-based stablecoins, providing market clarity and fostering innovation alongside financial stability.

The future growth of the stablecoin market will ultimately be driven by a capital market-based issuance model. The main methods of issuing stablecoins are traditionally either direct issuance by banks using bank deposits as collateral, or capital market-based issuance by non-bank financial institutions or fintech companies using various collateral assets (e.g., government bonds, corporate bonds, deposits, etc.).

The bank-centric issuance model has strengths in terms of financial stability and regulatory compliance, but it has clear limitations in terms of scalability and innovation. Banks alone cannot meet the diverse needs of customers and services, so they must rely on collaborations and partnerships with various companies to grow.

As a result, not only Korea but also various countries in Asia should actively reference the U.S. Genius Act or Hong Kong's Stablecoin Act to legislate and secure a clear legal status for capital market-based stablecoins backed by various assets. This is essential for providing clear guidelines to market participants and creating an environment that supports both innovation and stability.

Source: Stablecoin Issuance Pipeline [Part 2] | Four Pillars

If various companies issue stablecoins individually, there is a risk that incompatible stablecoins such as kakaoKRW, wechatCNY, jdHKD, and rakutenJPY will proliferate. Such fragmentation could lead to conversion costs and complexity for users, ultimately hindering the growth of the entire stablecoin ecosystem.

Similar fragmentation exists within the current banking system, but users do not perceive it because each bank manages funds internally and operates an interbank settlement system based on the central bank's currency. In essence, this is akin to having shinhanKRW, hanaKRW, hsbcHKD, and mufjJPY. Therefore, a similar approach should be applied to stablecoins among consortium.

If capital market-based stablecoins become active, various factors such as the type of blockchain network, the form of collateral assets, and token standards could reduce the interoperability of stablecoins. To address this, major companies, including IT platforms and financial institutions, should form a consortium. Through the consortium, joint standardization efforts and interoperability can be enhanced, and a unified management and settlement system can be established to minimize fragmentation.

Such a consortium will serve as a core strategy to provide a better user experience and accelerate the growth of a platform and service ecosystem based on stablecoins.

Source: Stablecoin Issuance Pipeline [Part 2] | Four Pillars

Despite slow progress in monitoring and managing systems, stablecoins clearly represent the ideal monetary form. Platforms central to everyday life and business activities are crucial for widespread stablecoin adoption. Regardless of issuance decisions, all platforms should strategize for future financial systems integrating stablecoins.

Asian super apps, with their extensive user bases and transaction volumes, represent strategic leverage points for stablecoin integration. Adopting or partnering on stablecoin initiatives could provide foundational infrastructure extending beyond simple payments into asset management, credit assessments, and reward systems. Given the platform-centric nature of Asian markets, strategies incorporating stablecoins are particularly essential.

Korea, Japan, and China, characterized by centralized platform ecosystems, can leverage stablecoins to integrate internal payments and settlements, establishing a future-proof financial platforms. Collaborating with regulatory bodies and integrating traditional financial systems can further enhance the global scalability and adoption of Asian stablecoins.

Dive into 'Narratives' that will be important in the next year