Aave v4 replaces pool-based lending with a chain-level unified liquidity (Hub) and modular credit markets (Spokes).

Liquidity is centralized, while collateralization and liquidation risk remain isolated at the Spoke level.

Hub-level base rates position Aave as an on-chain reference rate for funding costs, with early market adoption.

Scalability depends less on architecture and more on governance throughput, incentives, and user understanding.

Aave is one of the oldest and most relied-on pieces of plumbing in DeFi. When Aave changes something, the flow of liquidity, collateral, and yield across the ecosystem shifts with it. v4 is no trivial update, and it is well worth examining. It's a redesign of how liquidity, collateral, and credit flow across the protocol.

This piece breaks down how v4 works, why the architecture matters, and where the tradeoffs lie. If you’ve ever supplied assets to Aave or borrowed against collateral, the differences should be immediately apparent.

DeFi lending protocols, including Aave v2 and v3, were built around an early assumption that each lending market must operate as its own isolated liquidity pool. This design, while easy to bootstrap, fails to scale efficiently. The architectural limitations is as follows:

Liquidity fragmentation: Capital is trapped across dozens of deployments—per chain, per asset type, or per use case.

Inefficient utilization curves: Because each pool has its own supply/demand dynamics, most markets never operate near optimal utilization. The protocol as a whole runs cold even when individual pools run hot.

Redundant configuration: Each market replicates oracles, collateral types, and rate curves. This adds governance overhead and friction for new market types.

Poor composability: Strategies involving multiple pools require bridging, manual rebalancing, and disjointed user experience.

Poor composability: Strategies that span multiple collateral types or market styles require bridging and juggling between pools, breaking UX and creating friction for product builders.

No rate standardization: With dozens of yield curves, Aave cannot offer a unified rate usable as a funding benchmark.

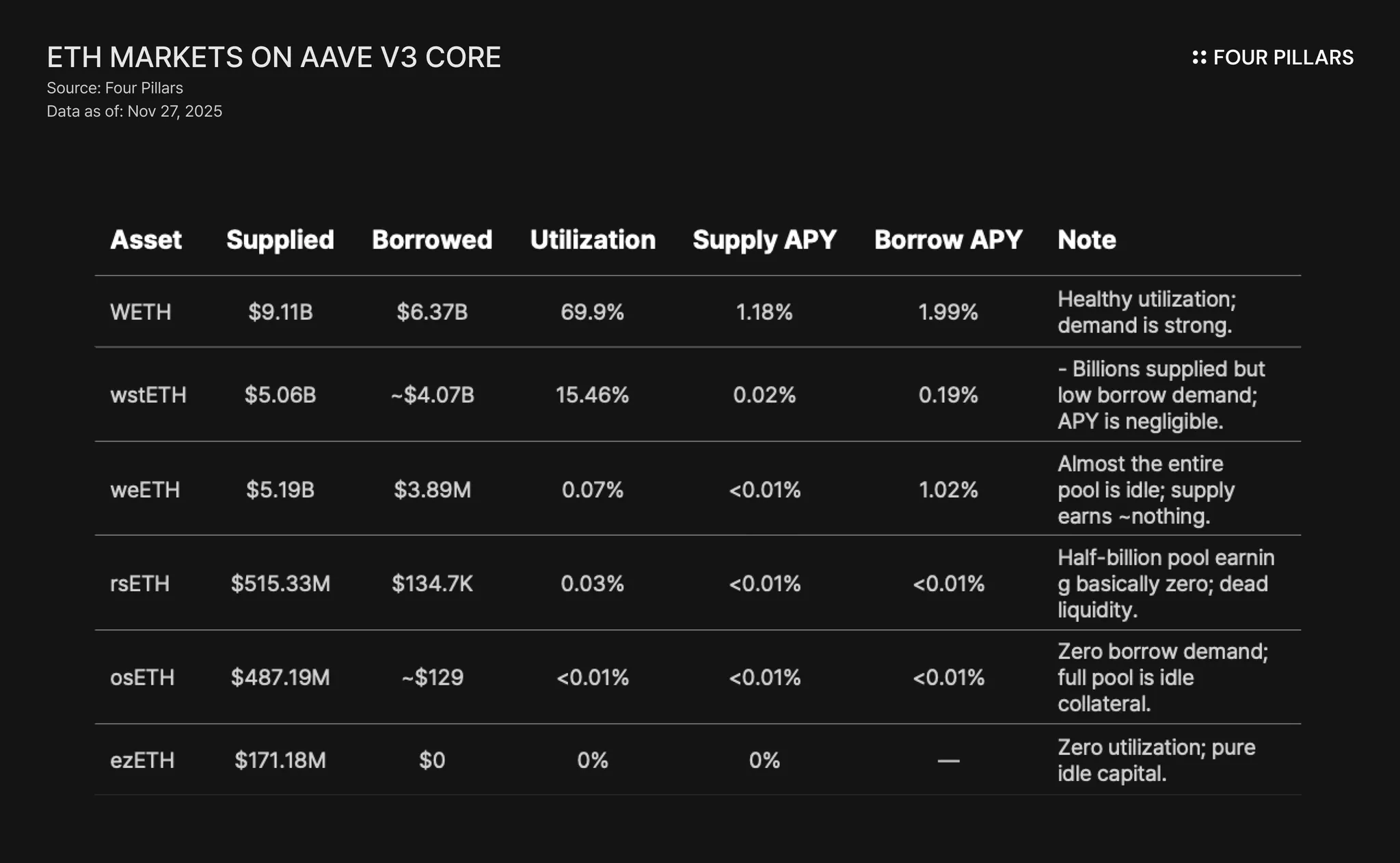

For example, the assets included in the table above are all ETH-based collateral with nearly identical economic properties, yet v3 splits them into separate markets with radically different utilization. WETH operates at ~70% utilization while more than $6B of LST collateral earns near-zero APY simply because liquidity is siloed.

Lending protocols like Morpho and Euler arose specifically to exploit these inefficiencies, by reshaping how liquidity is matched (Morpho Blue) or how markets isolate risk (Euler), but both work around the constraints of the pool model rather than eliminating it.

Aave v4 addresses this by decoupling liquidity from markets. It reframes Aave not as a set of standalone lending pools, but as a shared balance sheet powering many market types. Liquidity becomes unified; risk remains modular; utilization becomes chain-wide rather than pool-level.

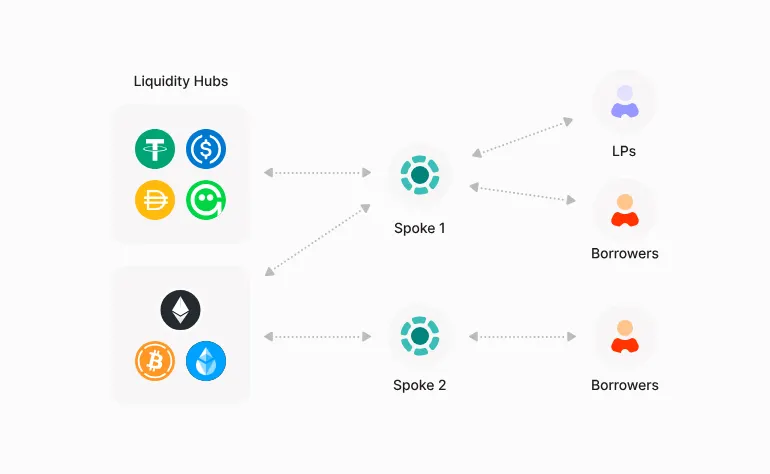

Aave v4 discards the fragmented pool model and introduces a two-tier architecture: one liquidity base (the Hub), and many modular lending environments (the Spokes).

Source: Aave docs

The Hub: Each chain has a single Hub that holds all supplied assets (ETH, USDT, USDC, GHO, etc.), tracks system-wide supply and borrow totals, accrues interest per asset, and enforces utilization-based rate curves. Users do not deposit to the Hub directly. Assets flow into the Hub after being supplied through Spokes. The Hub issues credit and debit limits to Spokes, defining how much liquidity each Spoke can draw or return.

Spokes: Spokes are isolated lending environments with their own collateral lists, liquidation rules, and risk parameters. They do not hold liquidity themselves; instead, they access the Hub’s pooled assets subject to supply and borrow caps. Spokes can represent LST leverage markets, RWA credit modules, permissioned institutional markets, or advanced multi-Hub Spokes that draw liquidity from more than one Hub.

Supply and Borrow Caps: These caps define how much liquidity from the Hub a Spoke can use. They contain risk (Spokes cannot exceed their credit line) while allowing unified liquidity across the chain.

Interest Rates: All Spokes inherit the Hub’s base rate for each asset. Borrowers then pay a risk premium based on their collateral mix inside that Spoke. For instance, a user borrowing WETH collateral might pay the base rate, whereas borrowing with USDe incurs a higher premium. This yields more granular pricing and aligns rates with collateral risk. Unified funding curve; Spoke-level pricing.

User Positions: A user’s position is per Spoke. Supplies, borrows, HF (health factor), liquidation conditions, and risk premiums are all isolated to that Spoke. Collateral in one Spoke cannot support borrowing in another. The health factor is computed from total collateral value, borrow value and collateral factors; HF must stay above 1 to avoid liquidation.

Position Managers: They automate cross-Spoke workflows (e.g., rebalancing or refinancing) but do not merge collateral or HF across Spokes. Risk isolation remains intact.

Not fully permissionless: Each Spoke must be approved by governance, including its caps and collateral rules, because every Spoke consumes shared Hub liquidity.

This design unifies liquidity at the Hub while keeping collateralization and risk siloed inside each Spoke.

To understand how Aave v4 changes the user experience, it’s useful to walk through a simplified supplier/borrower flow in both versions. Even though the core interactions remain familiar, liquidity behavior and borrowing experience shift in meaningful ways.

v3

Supplier: Alice deposits 100k USDC into Aave v3’s Ethereum Main Market. Her deposit earns yield based on utilization and borrowing activity within that specific pool.

Borrower: Bob wants to borrow USDC against wstETH, but the LST market is a separate deployment with limited liquidity. If Bob deposits wstETH into the LST market, he may face worse interest rates or limited borrow capacity due to its smaller TVL base.

Launching a new market (e.g., a permissioned RWA pool) requires bootstrapping its own supply and demand. Without liquidity incentives or initial deposits, suppliers like Alice have little reason to move funds, slowing down adoption.

v4

Supplier: Alice deposits 100k USDC into a v4 Spoke. She no longer chooses a specific market. Her liquidity is pooled in the Hub behind the scenes and earns the chain-level USDC rate.

Borrower: Bob opens a position in a Spoke designed for LSTs. He deposits wstETH and borrows USDC. This Spoke draws liquidity directly from the Hub, so Bob benefits from deeper capital and potentially better rates even though the LST logic is isolated in the Spoke.

Now consider a new Spoke—say, for tokenized treasuries. Once governance sets supply and borrow caps for the Spoke, it gains immediate access to USDC liquidity. Alice’s deposit services that market automatically, without any new action required from her.

Beyond efficiency gains, v4 meaningfully expands Aave’s design surface. Because Spokes inherit liquidity, liquidation systems, and governance frameworks from the Hub, developers can build markets that weren’t viable in v3. For example:

Pendle PT collateral markets can let users borrow USDC or GHO against Principal Tokens without fragmenting liquidity.

Uniswap or Curve LP Spokes can price collateralization based on pool composition and volatility, enabling credit against AMM positions that dynamically adjusts LTV as the pool shifts.

Ethena-style sUSDe or RWA-specific Spokes can isolate novel collateral types without forking Aave or bootstrapping deposits.

Fixed-tenor credit markets can match lenders and borrowers by duration, while letting unmatched liquidity continue earning yield from the Hub.

Secondary debt markets become feasible when Spokes can define custom reserve behavior or collateral flows.

The key shift is that developers focus on market logic, not liquidity sourcing. New markets expand Aave rather than competing with it, creating a positive-sum flywheel: every useful Spoke reinforces the Hub, and every stronger Hub increases the viability of the next Spoke.

Essentially, v4 shifts Aave’s role in the credit stack. Once liquidity is centralized into a Hub and market logic is modularized into Spokes, Aave stops functioning like a collection of lending venues and starts behaving like a unified funding market, where a shared source of collateralized liquidity that multiple credit environments draw from.

TradFi sees this pattern everywhere: repo markets, tri-party collateral systems, prime-brokerage funding lines, money-market funds, and dealer financing desks. In those systems, capital sits in a consolidated base while different desks originate loans or leverage positions under defined limits and collateral rules. Aave v4 adopts the same organizational logic but in a crypto-native, programmatic form.

v3’s architecture forced every market to bootstrap its own liquidity. Tokenized-treasury markets, LST leverage markets, RWAs, fintech lending rails, permissioned credit pools — all required separate deployments, governance cycles, incentives, and duplicated risk config. Liquidity fragmented across dozens of pools, each with its own collateral lists, oracles, and yield curves.

v4 removes this bottleneck. Because liquidity supplied into Spokes ultimately pools in the Hub, deposits function as a shared funding resource. Every Spoke draws liquidity from the same balance sheet within governance-defined supply and borrow caps.

This unlocks immediate benefits:

No deposit bootstrapping: new markets can launch without TVL incentives.

No duplicated configuration: risk logic lives at the Spoke level; liquidity logic stays standardized.

Faster market velocity: builders iterate on underwriting, not infrastructure.

Institutional pathways: permissioned Spokes can embed KYC, risk filters, and compliance rules while borrowing from the shared pool.

Governance acts as a risk allocator, setting supply and borrow caps, configuring collateral rules, and metering how much liquidity each Spoke can access. These caps behave like internal credit lines, letting each market operate independently without endangering the funding base. The outcome is that Aave’s balance sheet becomes the wholesale cost of capital for anything plugged into the system.

In v3, each market produced its own yield curve. A token like USDC could have multiple funding rates across pools, each distorted by its own supply-demand mix or incentives. This fragmentation made it difficult for institutions and fintech platforms to treat Aave as a predictable cost of capital.

In v4, interest accrues at the Hub. Each asset inherits a single funding curve per chain, driven by system-wide utilization and collateral-specific risk premiums. New markets no longer create fragmented rate environments but inherit the same base cost of capital. This gives DeFi a credible funding benchmark that other protocols can reference:

RWAs can price stablecoin funding off the Hub rate.

Structured-credit vaults can define spreads over the benchmark curve.

Perps and trading engines can incorporate it into funding models.

Fintech consumer credit rails can adopt it as their base borrowing rate.

This is already happening today:

CoinDesk Overnight Rates (CDOR) launched in 2025 as DeFi’s first institutional-grade benchmark index, built directly from Aave’s USDC and USDT lending rates. CDOR treats Aave the same way SOFR anchors TradFi.

Cap uses Aave’s rate as the base market rate in its hurdle-rate formula and routes idle assets into Aave for yield.

Level USD publicly calls Aave its “core liquidity layer” and “DeFi’s reference point for trust, liquidity, and yield”, anchoring capital allocation around Aave’s rates.

Plasma deposited pre-launch funds directly into Aave, regarding it as the most reliable source of institutional-scale passive yield on-chain.

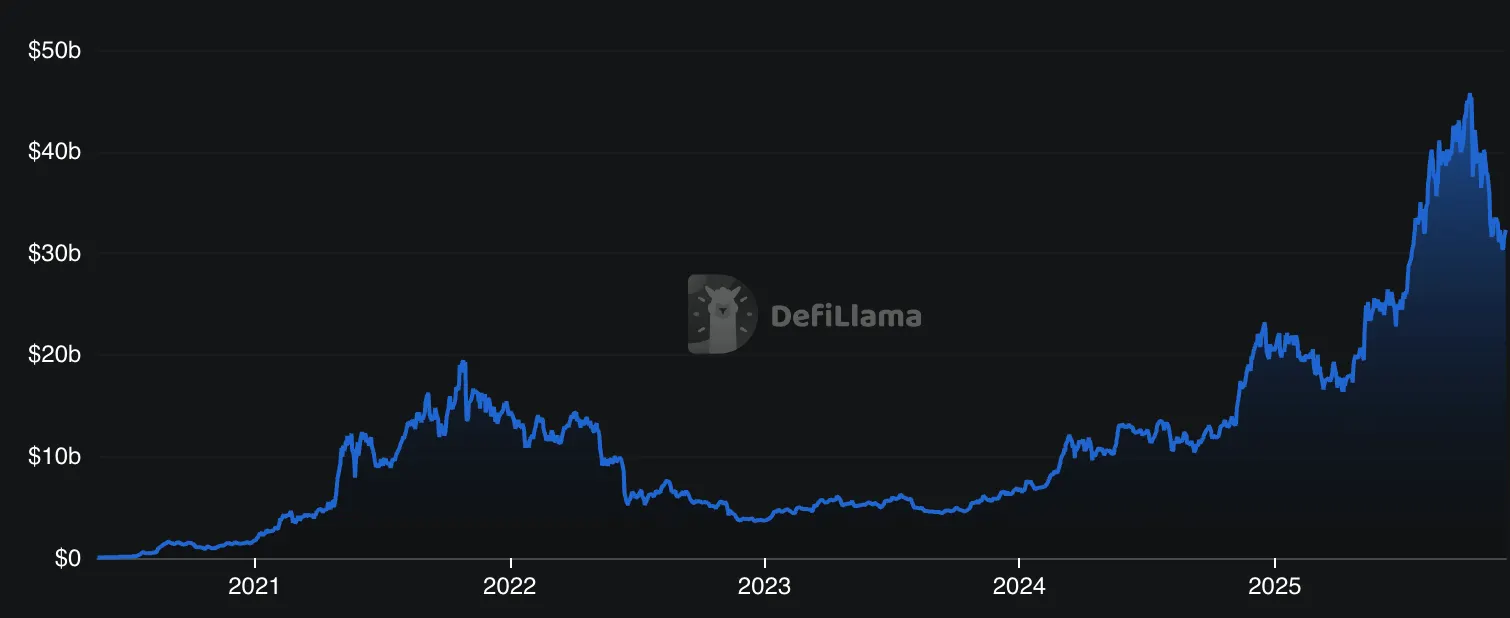

With v4’s unified Hub-per-chain model, this benchmark effect strengthens further. Moreover, Aave’s current ~$32B TVL gives it enough gravitational mass for this benchmark to matter.

Source: Defillama

That said, because each chain has its own Hub, “unified” means per-chain, not global — an important nuance for understanding how liquidity aggregates.

The real significance of v4 is not any single feature but the system-level behavior that emerges when funding and credit are separated.

Aave becomes:

a shared liquidity substrate,

a standardized funding source,

a platform for specialized credit markets,

a piece of financial infrastructure rather than a lending product.

Credit markets compete on underwriting, UX, and collateral design, not their ability to attract deposits. Funding becomes a shared public good, just like how prime brokerage abstracted funding from hedge-fund strategies, repo markets centralized dealer liquidity, and tri-party systems standardized collateral financing.

In every case, once funding is unified, the markets built on top accelerate. Aave v4 positions itself to be the unified funding market where liquidity is priced, where credit lines originate, and where new financial primitives connect to capital.

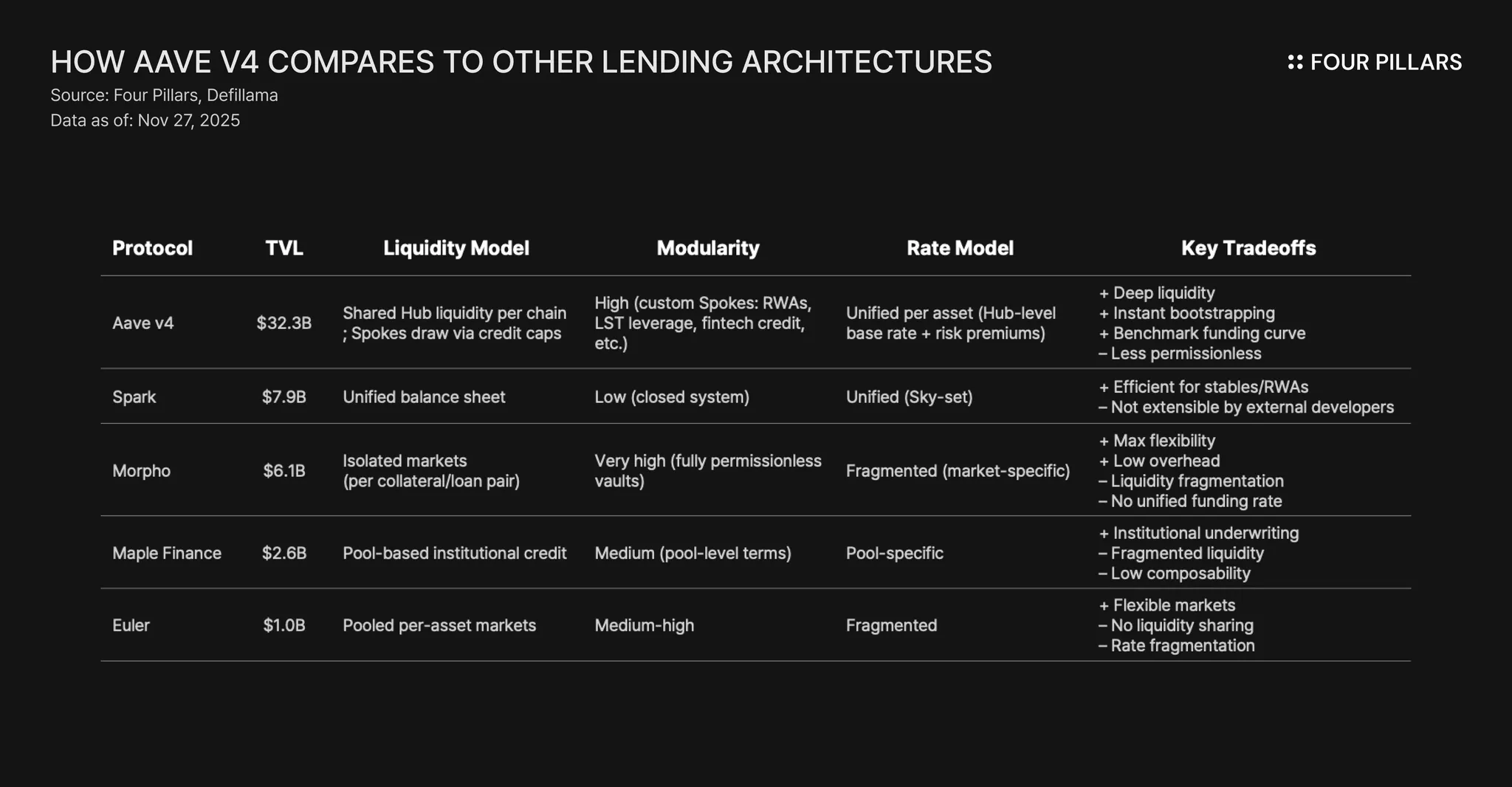

Aave v4 addresses liquidity fragmentation differently from other protocols. It is distinctive because it provides a shared liquidity base per chain while allowing modular lending logic through Spokes. Rather than maximizing permissionlessness or aiming for extreme simplicity, v4 combines capital efficiency with controlled extensibility. This positions Aave uniquely: it is currently the only architecture in DeFi that unifies liquidity, modular credit markets, and chain-wide benchmark rates. The table below outlines the key differences:

For all the upside, the Hub–Spoke design introduces its own constraints and operational choke points.

Governance bottlenecks remain the ultimate throughput limiter. Even with modular Spokes, every new market must still clear governance: collateral onboarding, supply/borrow caps, risk premiums, interest-rate parameters, and oracle configuration. This is weeks to months of process. If DeFi wants 50 Spokes, 100 Spokes, institutional Spokes, RWA Spokes, fixed-rate Spokes, exotic-asset Spokes, the bottleneck becomes governance throughput. Aave governance is slow, conservative, and intentionally cautious — which is good for safety, but bad for product velocity.

User positions remain fragmented at the Spoke level. Even though funding is unified, collateralization remains local. Supplies, borrows, HF, and liquidations stay Spoke-specific, collateral in one Spoke cannot support borrowing in another, and users must select the Spoke that matches their collateral and use case. For users, this means the system still behaves as multiple discrete credit environments, even though the liquidity behind them is shared.

Advanced features (multi-Hub Spokes) will be niche in practice. v4 introduces powerful capabilities like multi-Hub Spokes, but these require complex collateral logic, cross-Hub liquidation semantics, sophisticated risk modeling, extensive auditing, and careful governance calibration. Realistically, such Spokes will be built only by the core Aave team or high-trust partners. The feature is valuable, but may not broadly accessible for most builders.

Liquidity centralization increases the blast radius of mispriced incentives. For example, if a Spoke starts offering strong incentives (like yield or points), even if caps are conservative, liquidity behavior changes. Lenders pile into the high-APY Spoke, usage of other Spokes drops, funding curves distort, and user APYs jump or collapse chain-wide.

Aave v4 represents a shift in how DeFi funding markets are structured. By pooling liquidity at the Hub and pushing risk logic into modular Spokes, Aave moves from a collection of independent lending pools to a unified funding layer for on-chain credit. That opens the door to new markets, institutional credit rails, RWA integrations, and more consistent rate formation across an entire chain.

The result is a protocol that is more scalable, more expressive, and more aligned with how real funding systems behave, without abandoning the isolation and risk discipline that kept Aave alive through every market cycle so far. If DeFi continues to evolve toward modular credit, shared liquidity, and benchmark-grade yields, v4 is likely the model that will anchor that future.

Dive into 'Narratives' that will be important in the next year