Today, the NYSE announced its plan to launch a tokenization platform. The exchange stated that it will offer tokenized stock trading with features such as 24/7 trading, instant settlement, and stablecoin funding.

The sequence is becoming clearer. Stablecoins came first, then U.S. Treasuries, and tokenized stocks are emerging as the next key asset class. While the tokenized stock market is still at an early stage, its long-term growth potential is substantial.

Tokenized Treasury issuance: $9.3B

Tokenized stock issuance: $900M

At present, cumulative issuance of tokenized Treasuries exceeds that of tokenized stocks by more than 10x. However, when viewed through the lens of traditional financial markets, the relative size is reversed.

U.S. Treasuries: $30T

U.S. stock market capitalization: $69T

On a global basis, stock markets are roughly twice the size of government bond markets. Given this structure, the potential market size of tokenized stocks is likely far larger than that of tokenized Treasuries.

When technical primitives change, the businesses built on top of them change as well. Stablecoins demonstrated this first. Tether and Circle now circulate a combined $250B in stablecoins, and Tether has grown into a company that holds more U.S. Treasuries than most G20 countries.

Beyond issuance, the stablecoin business landscape has already expanded into orchestration (i.e., BVNK, Stripe), onchain neobanks (i.e., Ether.Fi, UR), and POS terminals (i.e., Ingenico x WalletConnect). These are no longer experiments but products in active commercial use.

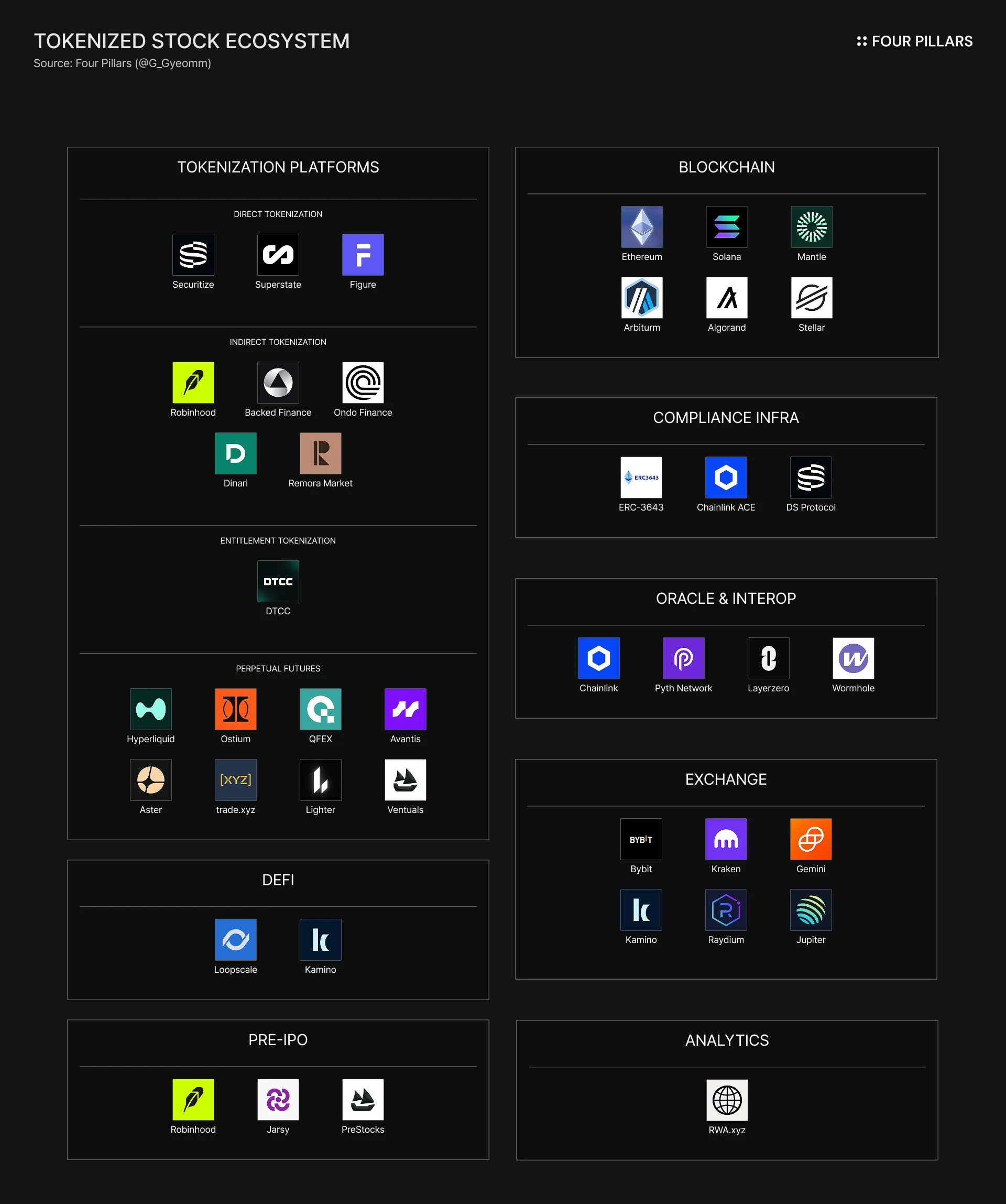

New technologies consistently create new economic activity and, in turn, new business opportunities. So, what kinds of opportunities does stock tokenization unlock?

Tokenization platforms

Depending on the tokenization model, stock tokens differ in legal ownership structure, permitted trading scope, and dividend distribution. Each model targets different investor segments and addressable markets. How will tokenization platforms evolve from here?

Securitize: A direct tokenization model that updates shareholder registries via blockchain-based DRS (Direct Registration System). Designed with regulatory compliance as the priority, trading is limited to ATS for accredited investors.

Backed Finance: An indirect tokenization model where stocks are purchased and held on behalf of users, and claims on those assets are tokenized. Major stocks such as TSLAx and NVDAx can be flexibly issued and traded, and are also used as collateral in DeFi.

Ostium: Implements stock tokens as perps that track stock prices without holding the underlying asset. While ownership is not guaranteed, it enables leveraged, long and short, high-frequency trading for any stock with sufficient price discovery.

Compliance infrastructure

Onchain stock token trading requires verification of KYC and AML, investor eligibility, and jurisdictional restrictions. As a result, infrastructure that enforces compliance policies at the token and contract level is emerging.

ERC-3643: Controls transactions using an onchain investor registry that represents eligible investors on Ethereum.

Chainlink ACE: Provides an identity framework called CCID to represent investor identity and credentials, along with compliance token extensions that connect CCIDs to tokens and policy enforcement logic.

Oracles

Nasdaq generated more than $600M in U.S. market data revenue in 2023. ICE, the owner of NYSE, generated $1.4B in revenue from market data and connectivity services in the same year. Price data has long been a core business in traditional stock markets.

In crypto, oracles have become key players in the price data business. As stock tokens expand, oracle providers are extending their role to deliver traditional stock market data onchain.

Chainlink: Chainlink Data Streams source offchain stock prices from consolidated tapes and data vendors such as Bloomberg, and deliver them onchain in real time.

Pyth Network: Pyth receives high-precision market data from major banks, exchanges, and financial institutions including Revolut, AMINA Bank, Cboe Global Markets, and LMAX.

Exchanges

If tokenization platforms act as the primary market by structuring stocks and defining compliance conditions, exchanges such as Bybit and Kraken function as secondary markets, similar to NYSE, Nasdaq, and CBOE.

Bybit: Supports 24/7 spot trading for xStocks across 10 assets, including COINx, NVDAx, and AAPLx.

Kraken: Offers zero-fee trading for xStocks. In December 2025, Kraken acquired Backed Finance.

DeFi

Tokenized Treasuries already function as reliable, composable collateral assets in DeFi. Aave Horizon, launched in August 2025, reached $600M in deposits and $200M in loans in less than six months.

Stock tokens are now gaining attention as collateral assets in onchain money markets. This shift democratizes stock-backed lending, previously limited to private banking, and is expected to drive meaningful borrowing demand from institutions.

Kamino: Provides isolated pools that separate money markets by token type, supporting stablecoin borrowing against stock tokens such as SPYx, AAPLx, and TSLAx.

Loopscale: An orderbook-based onchain lending protocol offering fixed-rate, fixed-maturity loans, operating xStocks collateral markets on Solana.

The expansion of tokenized stock markets faces many challenges, including off-hours trading, market maker inventory risk, liquidity gaps, and weekend price gaps. Nearly all of these frictions arise from the process of bringing traditional offchain stock markets onchain.

However, developments such as the launch of NYSE’s tokenized stock exchange, DTCC’s efforts to tokenize securities entitlements, and onchain IPO (dual stock / token issuance) point toward a near future where tokenized stock markets function as base markets themselves.

A 24/7 stock market with extreme capital efficiency may be closer than it seems.