With the Pectra upgrade, Ethereum is moving toward expanding the Max Effective Balance to 2,048 ETH through EIP-7251, thereby reducing the number of validators and easing bandwidth pressure on the consensus layer. This is not simply an adjustment of the upper bound; rather, its significance lies in structurally securing network scalability through validator consolidation.

Such a transition presupposes execution-layer–based compounding withdrawal credentials, and in doing so, further reinforces an operational model in which a validator’s ETH balance remains within the protocol for extended periods of time.

However, in a structure where automatic sweeps effectively depend on a fixed threshold(i.e., 2,048 ETH), rewards may not be transmitted externally for a considerable duration. This can introduce rigidity for validators, particularly in terms of capital turnover and reward visibility. EIP-8148 is a proposal that seeks to transition this structure into a more flexible, policy-based framework.

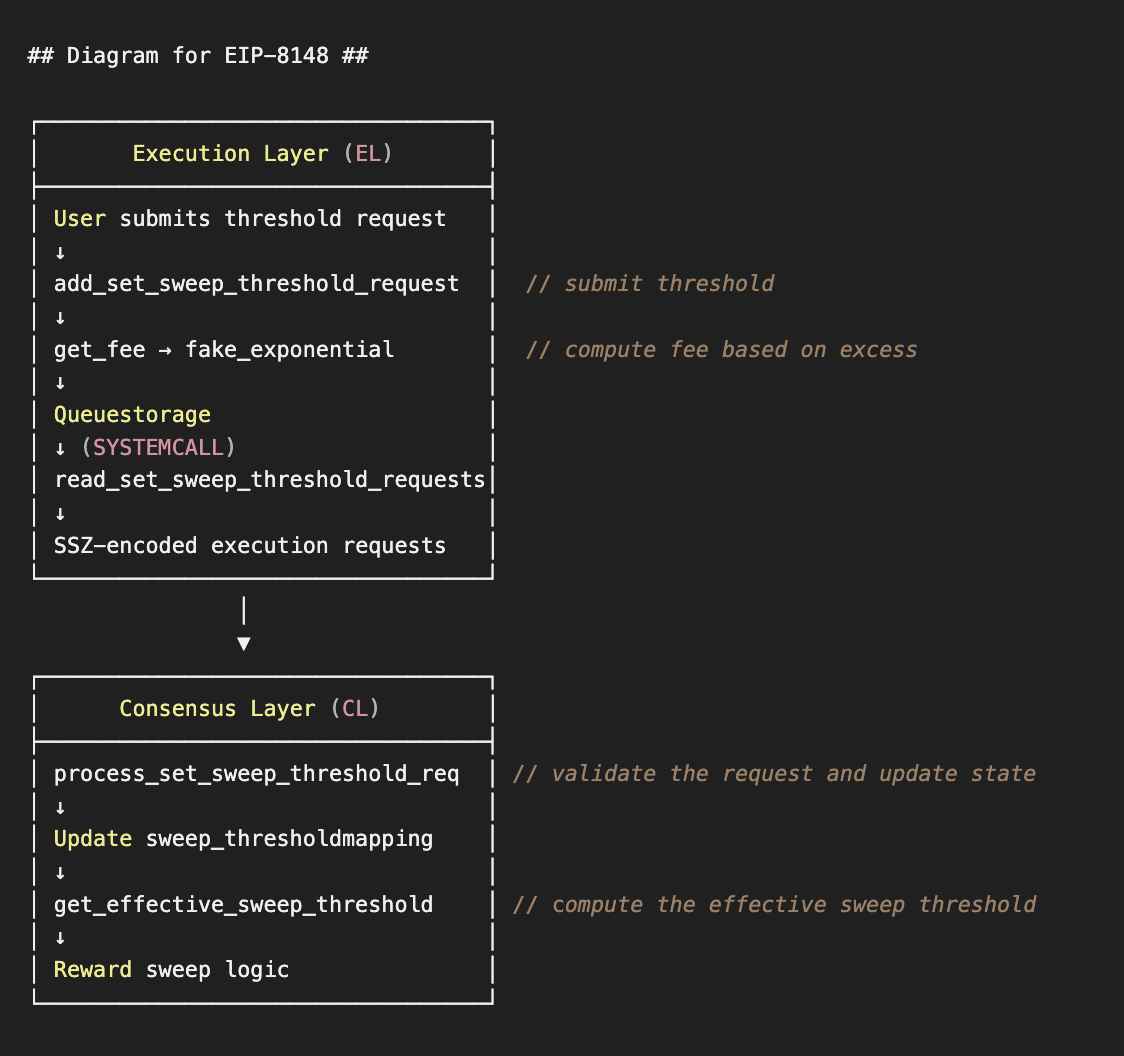

At its core, EIP-8148 allows validators to directly configure the automatic sweep threshold (; sweep_threshold) - in other words, a validator’s balance may compound up to the specified limit, and only the portion exceeding that threshold would be automatically transferred to the withdrawal destination.

This design constitutes a relatively small change—a minimal state extension—that adjusts only the timing of reward routing without compromising consensus safety - it does not modify slashing conditions or effective balance calculations; instead, it introduces a policy variable into the flow of capital.

From a more strategic perspective, this proposal can shift staking toward a more “policy-designable yield infrastructure.” For example, large LST protocols such as Lido Finance pursue operational efficiency through validator consolidation, while also seeking to fine-tune the timing of yield distribution within strategic vault structures like stVaults.

If the sweep threshold can be set dynamically, validators may allow rewards to compound up to a certain level in order to maximize capital efficiency, and thereafter deploy the excess at the execution layer—whether through redepositing, restaking, or allocating into DeFi strategies. In this sense, staking rewards are no longer confined to being merely accrued yield, but can instead be redefined as “routable liquidity.” Ultimately, while EIP-8148 may appear, on the surface, to be a UX-oriented refinement, its implications are structurally significant across stakeholders.

For the macro-level design of MaxEB expansion and validator consolidation to remain sustainable, the micro-level dynamics of capital rotation and reward visibility must also be carefully calibrated. In this regard, the proposal can be understood as a micro-adjustment that bridges this gap, and as part of the broader transition toward making staking rewards a more programmable yield primitive.