Last week, the markup of the Crypto Market Structure Bill that had been scheduled in the US Senate was canceled.

One of the main points of contention was the debate over whether stablecoins should be allowed to pay interest, but the withdrawal of support by Coinbase CEO @brian_armstrong also had a meaningful impact.

Why did Brian Armstrong oppose the bill? There are several reasons, but he viewed the bill as effectively banning tokenized equities.

Source: Toungvy Le

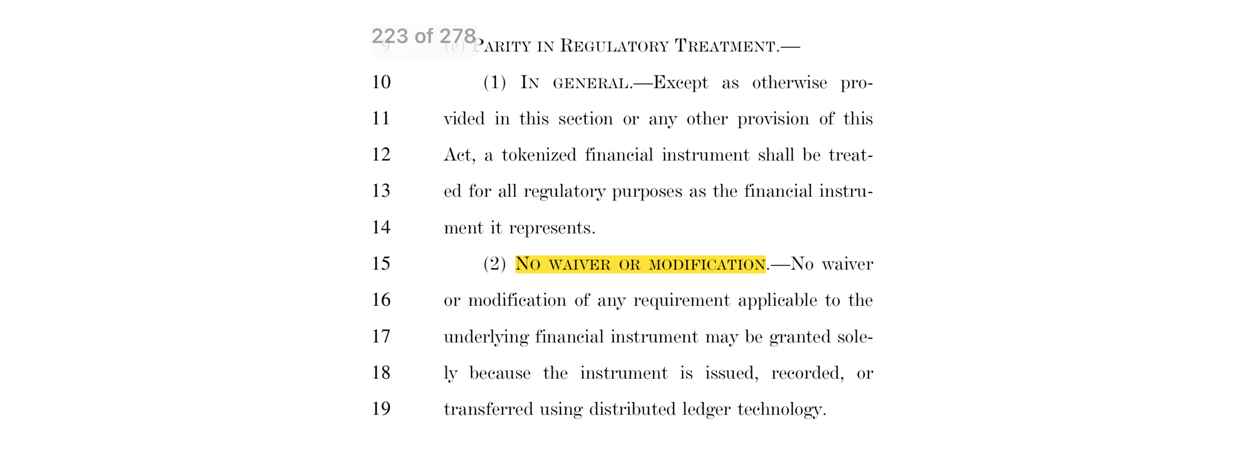

The basis for this argument can be found in Section 505(e)(2) of the Market Structure Bill.

This provision states that even if a financial instrument is tokenized using DLT or blockchain technology, the applicable financial regulations do not change. In other words, even when equities are tokenized, they are still required to comply with existing securities laws.

If Brian Armstrong believes that, in the future, a better form of equity could emerge, not traditional shares but instruments that incorporate governance tokens and more advanced voting structures, then the current draft of the bill could be interpreted as prohibiting such an idealized version of tokenized equities.

However, tokenizing equities today is merely a change in form factor. Naturally, they must continue to comply with securities laws.

In reality, platforms such as @Securitize are already tokenizing equities in full compliance with US securities regulations. Is Securitize breaking the law? Not at all. Tokenized equities are already possible today, and the Market Structure Bill does not prohibit them.

Fiat currency in the form of stablecoins and US Treasury money market funds each have a single, standardized way to be tokenized. Equity tokenization, however, is still at an early stage. Because there are many different stocks and a wide range of associated rights, the methods of tokenization are highly fragmented.

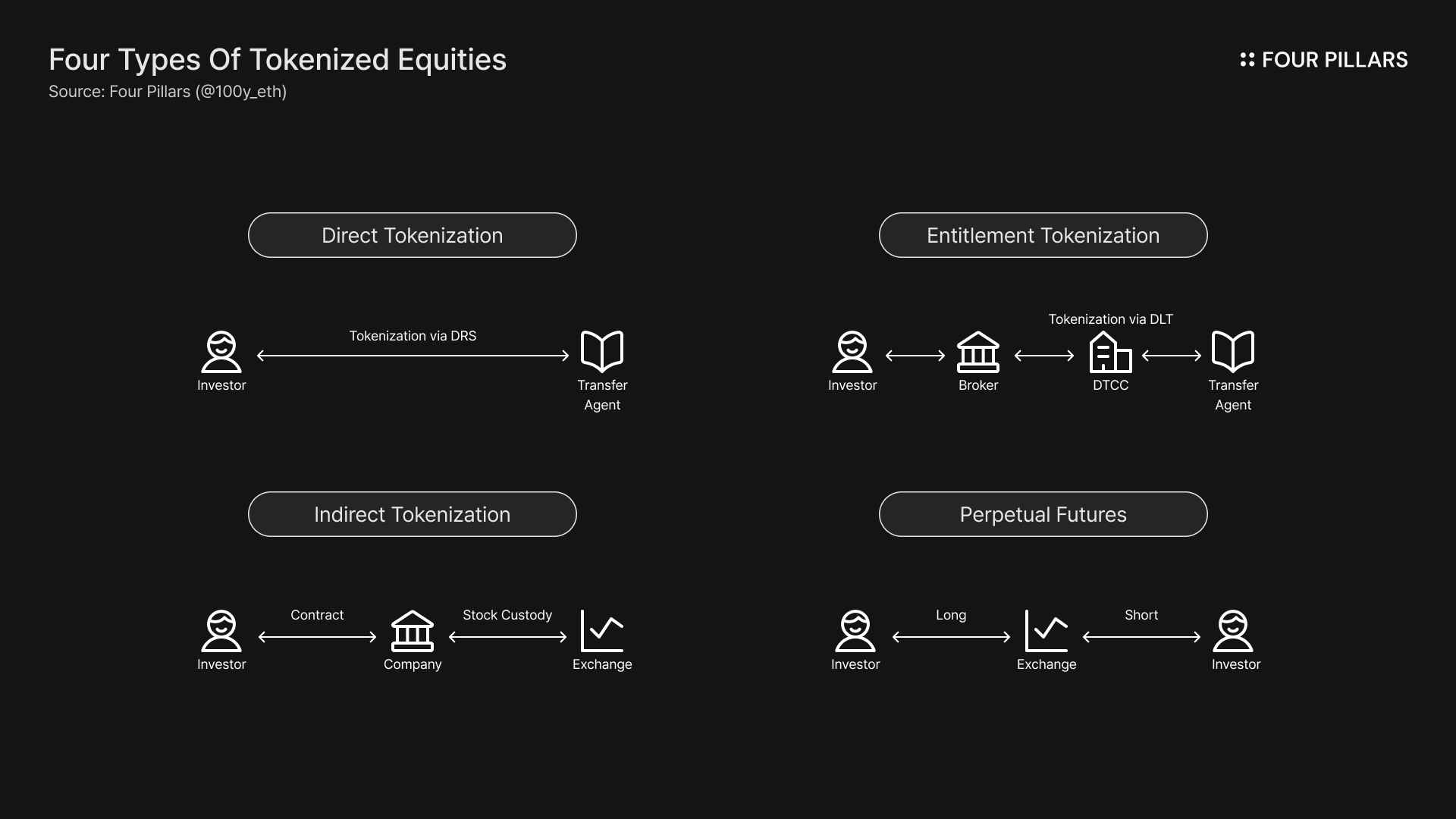

Today, equity tokenization broadly falls into four categories.

Direct Tokenization

Entitlement Tokenization

Indirect Tokenization

Perptual Futures

The first is direct tokenization. Platforms such as @Securitize and @SuperstateInc fall into this category. This approach does not rely on the existing DTCC infrastructure for custody or recordkeeping. Instead, investors register their shares directly with a transfer agent that maintains the official shareholder registry, and those shares are then tokenized.

This method fully complies with existing securities laws. Compared to traditional finance, it involves very few intermediaries, making it highly efficient, and all rights associated with ownership, including voting rights, are fully retained by the investor.

The second approach is entitlement tokenization. @The_DTCC falls into this category. In this model, the existing DTCC infrastructure remains intact, but instead of recording entitlements on an internal ledger, DTCC uses a blockchain.

This approach does not materially violate existing securities laws, and DTCC has recently received a no action letter from the SEC. It is highly efficient from the perspective of regulatory continuity and liquidity concentration, but because it preserves the existing infrastructure, the potential efficiency gains are limited.

The third approach is indirect tokenization. Platforms such as @RobinhoodApp, @BackedFi, @OndoFinance, and @DinariGlobal fall into this category. When an investor places a buy order, the platform purchases and custodies the underlying shares and issues a stock token to the investor that represents a 1 to 1 claim, conceptually similar to a bond.

This approach requires careful compliance depending on jurisdiction and service region and is subject to significant regulatory constraints. Because the tokenization is indirect, a major drawback is that investors do not receive rights such as voting rights.

The fourth approach is perpetual futures. Platforms such as @HyperliquidX, @QFEX, and @OstiumLabs fall into this category. These platforms use funding rates to keep futures prices aligned with spot prices. Rather than tokenizing equities directly, they provide exchanges where users can trade products that track equity prices. This makes them fundamentally different from the first three approaches, with clearly distinct advantages and disadvantages.

Perpetual futures also require careful consideration of jurisdictional regulations. If issues such as oracle reliability during off market hours and liquidity constraints can be addressed, this approach offers the highest level of accessibility and general usability.

Recently, Citron Research shared a particularly interesting view. They argued that when Coinbase stated it did not support the Market Structure Bill on the grounds that it would effectively ban tokenized equities, the real motivation may have been to push back against already licensed platforms like Securitize, which operate as transfer agents, broker dealers, and ATSs.

As discussed above, Securitize has already completed both the regulatory and technical preparations needed to tokenize equities in full compliance with existing securities laws. The Market Structure Bill does not ban tokenized equities. If anything, it provides greater regulatory clarity, which benefits Securitize.

2026 will be the year of tokenized equities. How competition unfolds and how the industry grows within the equity tokenization sector will be the key dynamics to watch.