※ This article series covers the DeFerence 2024 event, sponsored by Four Pillars, and will be published in three parts. This article is the second part of the series, and all attached presentation images were captured from the YouTube recording.

Part I - [Recap of Deference 2024] #1: Contribute to the Blockchain Ecosystem

Part II - This Article

Part III - [Recap of DeFerence 2024] #3: Discussing the Present and Future of Blockchain Infrastructure

In the previous article, "[2024 Difference Review] #1: Contributing to the Blockchain Ecosystem]," we briefly introduced the first part of the DeFerence event. It featured a keynote speech on the social, economic, and industrial values expected from blockchain technology and case studies from Decipher members who have made direct contributions to the ecosystem.

After a 50-minute break, the second part of the event, "Blockchain, Reaching the Masses," took place. This part featured a keynote speech on developing products based on an understanding of crypto culture, presentations by Decipher members on how to integrate blockchain into everyday life from RWA and data analysis perspectives, and a panel discussion with industry professionals on whether infrastructure or applications will lead the way for blockchain mass adoption.

Overview

Gideok Jang from the ATIV team explained why understanding the cultural phenomena of crypto is essential from a product-building perspective. He shared the context and vision behind the formation of the ATIV team and their future goals. The ATIV team aims to reshape the music industry's culture through IP Acceleration, with three main objectives: first, to widely publicize the concept and value of neighboring rights through the $ATIV token; second, to make artists' IP easily accessible to the public and fairly evaluated; and third, to support the conversion of these evaluated IPs into revenue-generating assets for various financial activities.

Comments

As Steve mentioned in the previous keynote speech - no matter how advanced the technology is, it has no value if it is not adopted. Since much of the blockchain industry remains undefined, it is crucial to understand the characteristics of the crypto industry to envision new use cases for blockchain technology in addition to efforts to improve technical usability.

In this regard, the experiences of the ATIV team provide valuable insights for teams with the potential to use blockchain to solve problems and contribute to existing industries. Their approach illustrates how blockchain can address specific issues and thereby enhance various existing sectors.

Below is a summary Gideok Jang’s presentation.

The term 'cult' can have various interpretations, but in the Western context, it is often used to describe fringe, fanatical groups or followers. In its early days, the crypto industry also progressed significantly through such cult-like communities - the crypto industry has had a religious aspect, where a small group of fanatical followers forms around a new technology promoted by a specific opinion leader, leading to various community-driven activities.

However, as of 2024, the crypto industry's atmosphere has changed significantly. It has evolved from small communities blindly following specific projects to being driven by initiatives involving the broader public - examples of crypto assets being integrated into the mainstream economic system are increasing, including JP Morgan's ONYX chain launch, ETF approvals, Pudge Penguin merchandise sales at Walmart, Azuki's animation production, Coinbase's NASDAQ listing, and etc.

This shift indicates that crypto is no longer just a cult but has the potential to become a mainstream culture. As online contexts occupy an increasing part of our lives and the need for digital currencies (e.g., stablecoins) grows, crypto is expected to play a more significant role in our daily lives. In this regard, we can envision a future where crypto significantly reshapes the cultural industry as well.

The current music market is rapidly shifting from offline to online streaming, with various streaming services like Tencent Music and Amazon Music emerging. It is anticipated that by 2030, the online streaming market will account for 80% of the music industry.

However, existing industry players often face failures despite spending significant amounts on content creation and marketing. While there could be multiple reasons for this, the key issue is the rapid change in how people discover and consume music - the success of the streaming industry now heavily depends on how frequently the content is exposed through algorithms and how effectively viral marketing is executed.

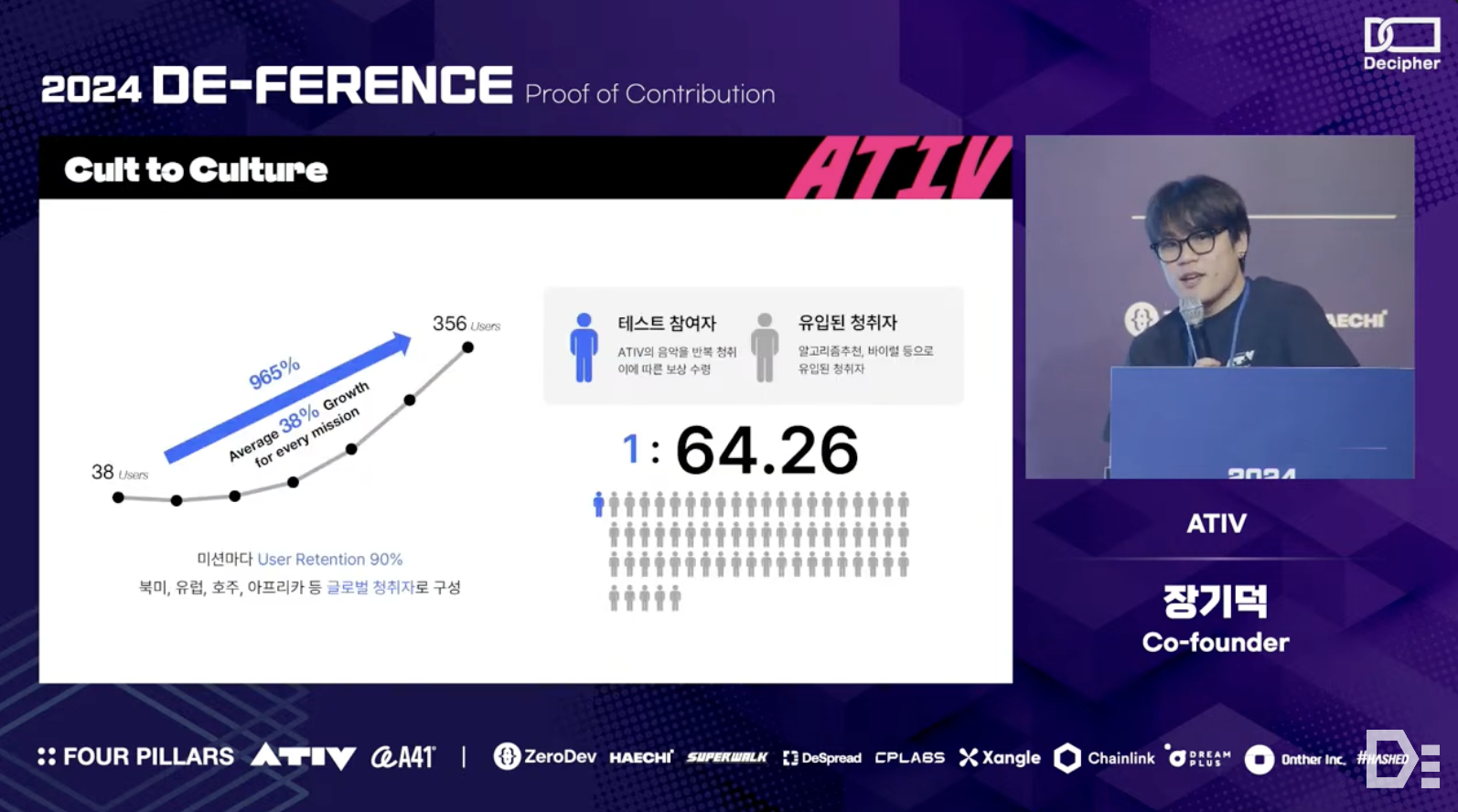

In response, the ATIV team conducted an intriguing experiment by applying the viral capabilities of crypto cults to the music industry. They implemented a simple system that rewards listeners with coins for listening to songs by artists partnered with ATIV. This system is integrated with a Discord bot connected to Spotify, which tracks the listening and sharing records of these artists' music. Based on their performance, listeners are rewarded with blockchain tokens.

Through this experiment, the ATIV team discovered that one listener could bring in approximately 64 new listeners, and retention rates were also high—listeners were motivated to listen more to earn additional rewards. Some artists experienced exposure on Spotify billboards or official playlists, and some experienced an increase in their listener numbers by 10 to 30 times.

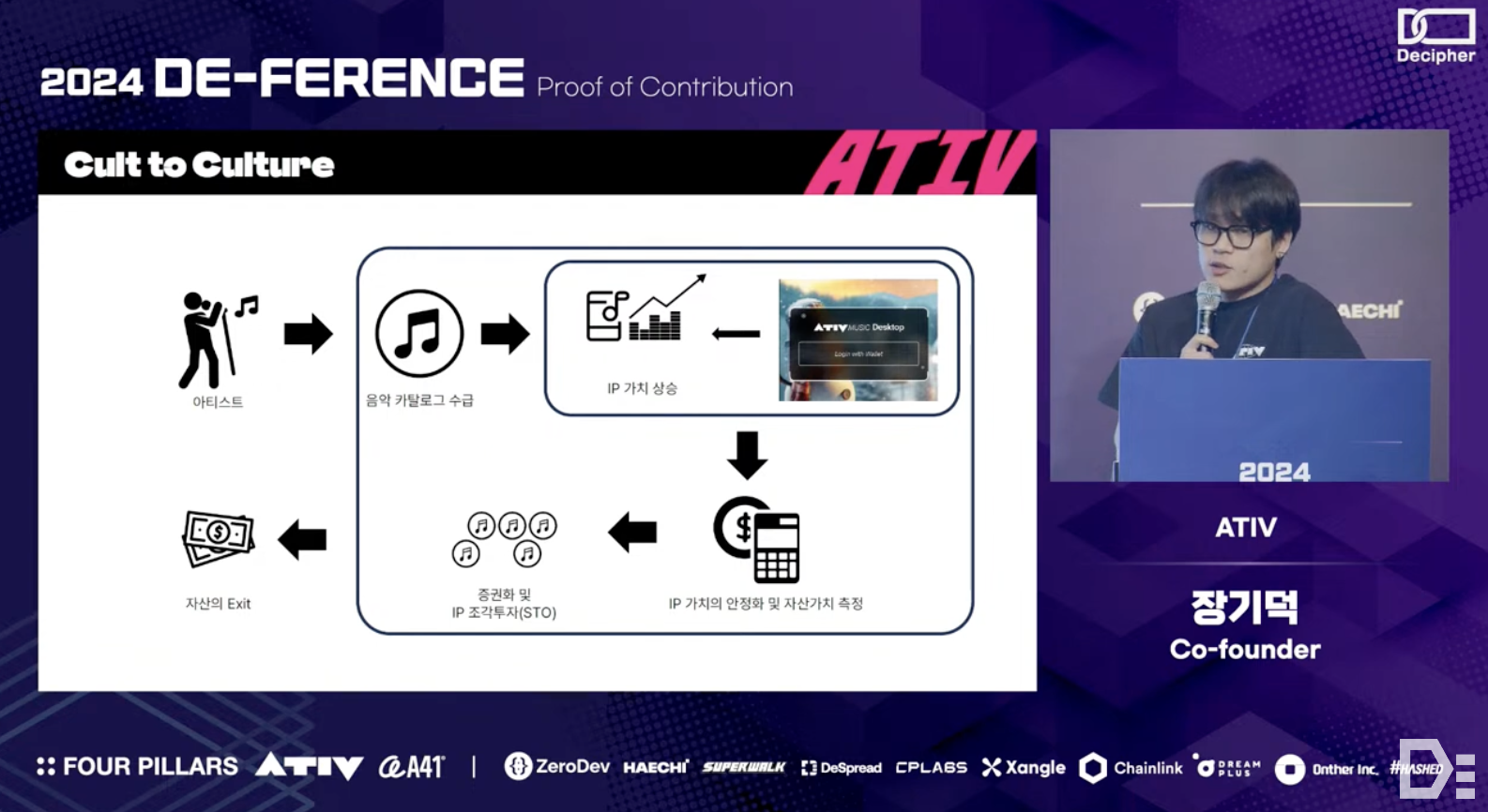

Based on these initiatives, the ATIV team envisioned using the crypto cult community to accelerate IP. Instead of promoting the work of famous artists, they aimed to support talented but under-recognized artists by obtaining neighboring rights from them. The goal is to help these artists gain exposure and grow together with the ATIV platform.

The vision and ecosystem ATIV is building also extend to listeners - by rewarding listeners with coins for engaging with music, ATIV aims to increase the value of IP while creating a platform that enables the secondary financial activities with the IP rights.

*Neighboring rights are similar to copyrights but are granted to individuals who contribute to making a work accessible to the public without directly creating the work. For example, performers, producers, and broadcasters can hold neighboring rights.

ATIV is a startup associated with the high-barrier blockchain industry, which could pose significant risks for artists. Despite this, ATIV has tested and secured approximately 60 songs from various artists, continuing to move forward. ATIV's goal is to further refine their vision of IP Acceleration, strengthening the ATIV platform to the point where all artists will want to participate voluntarily, thus building a sustainable IP ecosystem.

The lesson the ATIV team has learned through their journey is that while technical research is crucial for the development of the crypto industry, understanding the phenomena of crypto is essential for its practical adoption. Just as BTS successfully used viral marketing from Southeast Asia to target the Western market, reshaping culture requires new approaches that differ from traditional methods. ATIV aims to closely observe crypto trends and lead the ‘Cult to Culture’ initiative, positioning themselves as a key player in guiding crypto cults to drive internet culture.

Q: When the time comes for mass adoption of crypto through ATIV, what do you envision for the future of crypto?

A: The ATIV team sees themselves creating a social currency similar to Farcaster's $FRAME in the music industry context. And when that time comes, these sorts of attempts will likely become more widespread across various industries. After the market undergoes a period of overheating, the 'Cult (of Crypto) to Culture' era we envision will truly begin to take shape.

Overview

Minyoung Kang from the RWA Frontier team discussed the definition, rapid growth in market, and inherent value of the Real-World Asset (RWA) in her presentation. The team conducted interviews with various groups to clearly define RWA based on three criteria and analyzed the main revenue sources of RWA platforms, which are 'cost reduction' and 'additional revenue generation opportunity,' using real-world examples. Additionally, they compared regulatory environments across different countries to emphasize the importance of technical implementation and flexible regulations for the successful adoption of blockchain technology, and concluded the presentation by providing insights into how blockchain technology can be well integrated into the existing financial system.

Comments

With the advent of the IT era, where many processes are handled by computers and the internet, numerous new technologies have emerged explosively. However, despite the rapid emergence of new technologies, the adoption rate for them is inevitably slower in this complex and diverse society, especially when the impact of the technology is significant. This has been the case with many innovative technologies such as the sharing economy, fintech, autonomous vehicles, and drones.

However, hastily implementing regulations is not the answer for successfully integrating these innovative technologies into existing societies. As the RWA Frontier team presented, the widespread adoption of RWA using blockchain technology is a highly impactful initiative, especially in economic terms across nations. Therefore, it is essential to thoroughly identify uncertain areas and propose various regulatory initiatives to establish a flexible framework through international cooperation.

Additionally, for researchers and developers, it is crucial to closely understand the current regulatory landscape as well. This understanding helps bridge the communication gap between blockchain developers and regulatory bodies, ensuring that technology development is not hindered by regulations. Ultimately, this approach enhances the practical applicability of technology and accelerates the adoption of blockchain technology in the global market.

Below is a summary of Minyoung Kang’s presentation.

As of September 2023, the RWA market has rapidly grown to achieve a market capitalization of approximately $2.4 billion. This accounts for 6.5% of the entire DeFi market, and considering that this percentage has doubled in just about eight months, further growth seems highly probable. To understand the positive outlook behind this trend, the RWA Frontier team conducted interviews with teams experienced in the RWA business, such as Avalanche, Elysia, Creder, and Lambda256, to grasp the definition and intrinsic values of RWA.

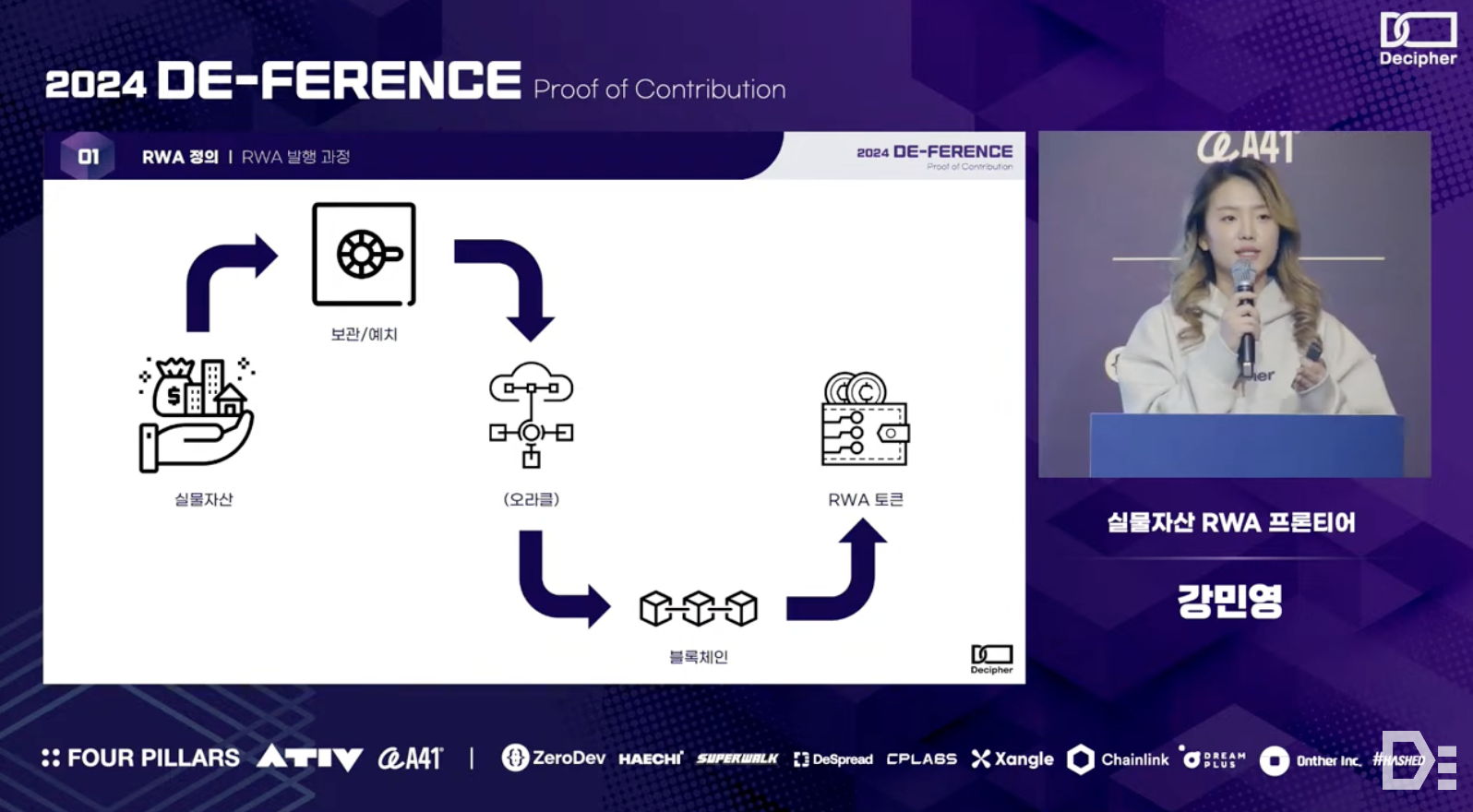

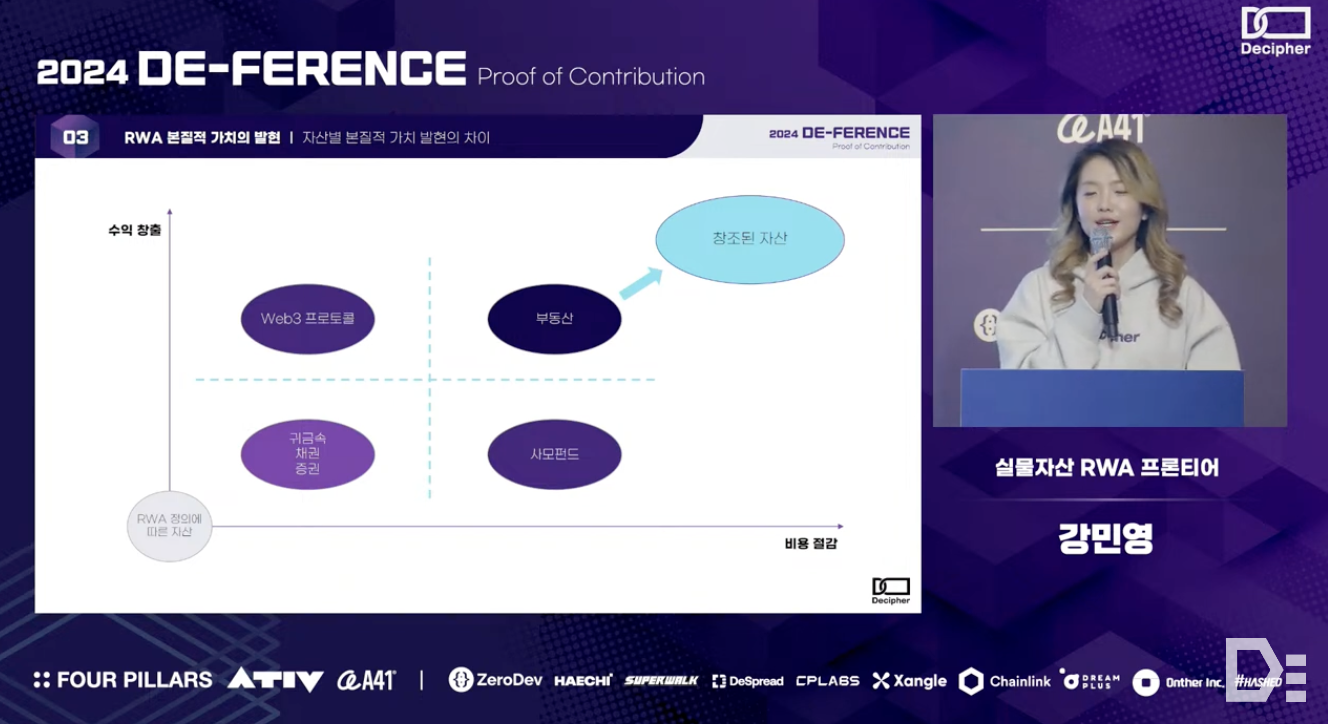

First off, the RWA Frontier team defines RWAs based on three criteria: price (market existence), ownership (the ability for an individual to store or entrust their asset), and value transfer (the equivalence of the asset's value in its tokenized form on the blockchain and its real-world form). They explained that for these assets to be traded in the RWA market, there must be entities or institutions that can deposit or store the real assets, and oracles that can reflect the asset's value on the blockchain.

The significant attention RWA has garnered is primarily due to two major benefits: 'cost reduction' in the asset issuance process and 'additional revenue generation opportunities' in the asset distribution process.

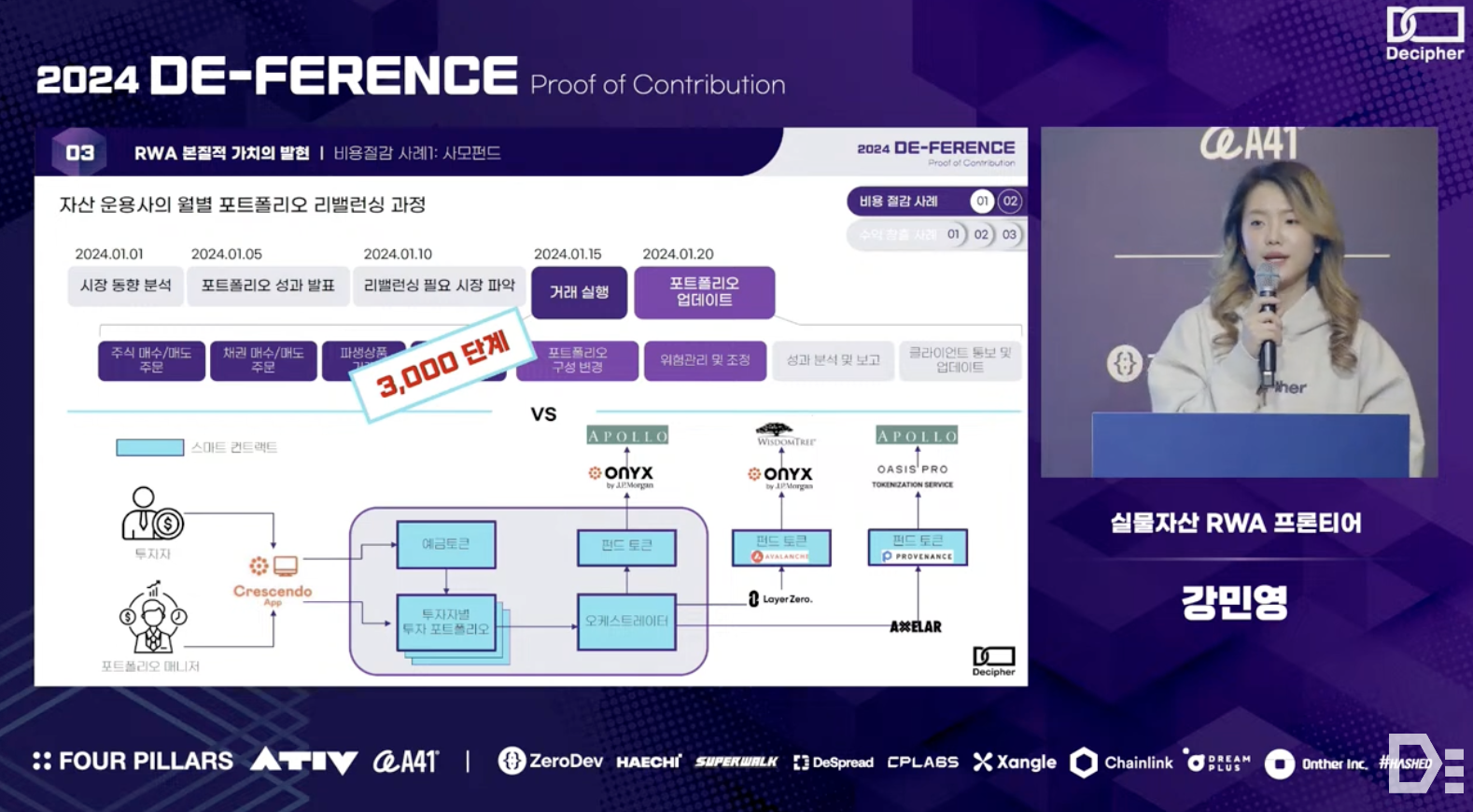

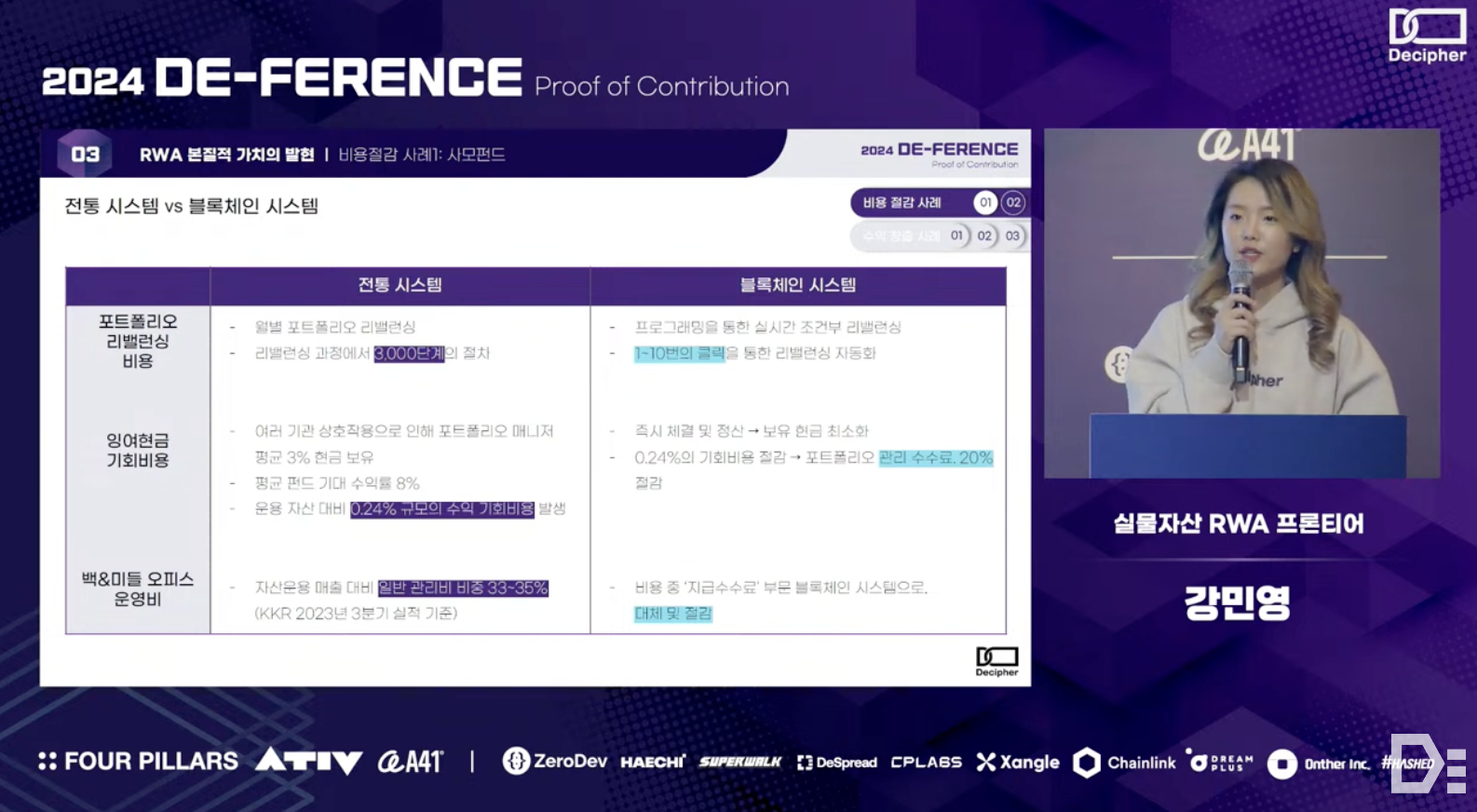

Firstly, examining the aspect of cost reduction, the first tokenization case is the operation of private equity funds - Apollo Global Management and JP Morgan's Onyx token issuance protocol have been conducting Proof of Concept (PoC) with the Avalanche mainnet for private equity fund management. The operation of private equity funds involves particularly complex middle and back-office operations and the periodic portfolio rebalancing process, which includes adjusting investment allocations and reporting. However, by utilizing smart contracts implemented on the blockchain, the entire series of processes, such as deposit management, asset transfer and distribution for investor-specific portfolio management, and investment execution, can be significantly simplified to just a few clicks.

The second case, tokenized securities, also achieves cost reduction in a similar manner. Procedures such as IPOs, and listings require extensive time and numerous steps, including due diligence and reviews. While many aspects still need careful human evaluation, formal paperwork, inter-channel communication, and regulatory compliance can be streamlined through the adoption of smart contracts - smart contracts facilitate the simplification of portfolio rebalancing operations, maximize the use of surplus cash to reduce opportunity costs, and lower operating costs in the middle and back-office.

The opportunity for additional revenue generation is related to the potential market size increase or the creation of new markets, which is made possible by increased investment accessibility to alternative assets (e.g., commodities, private debt) or previously illiquid assets.

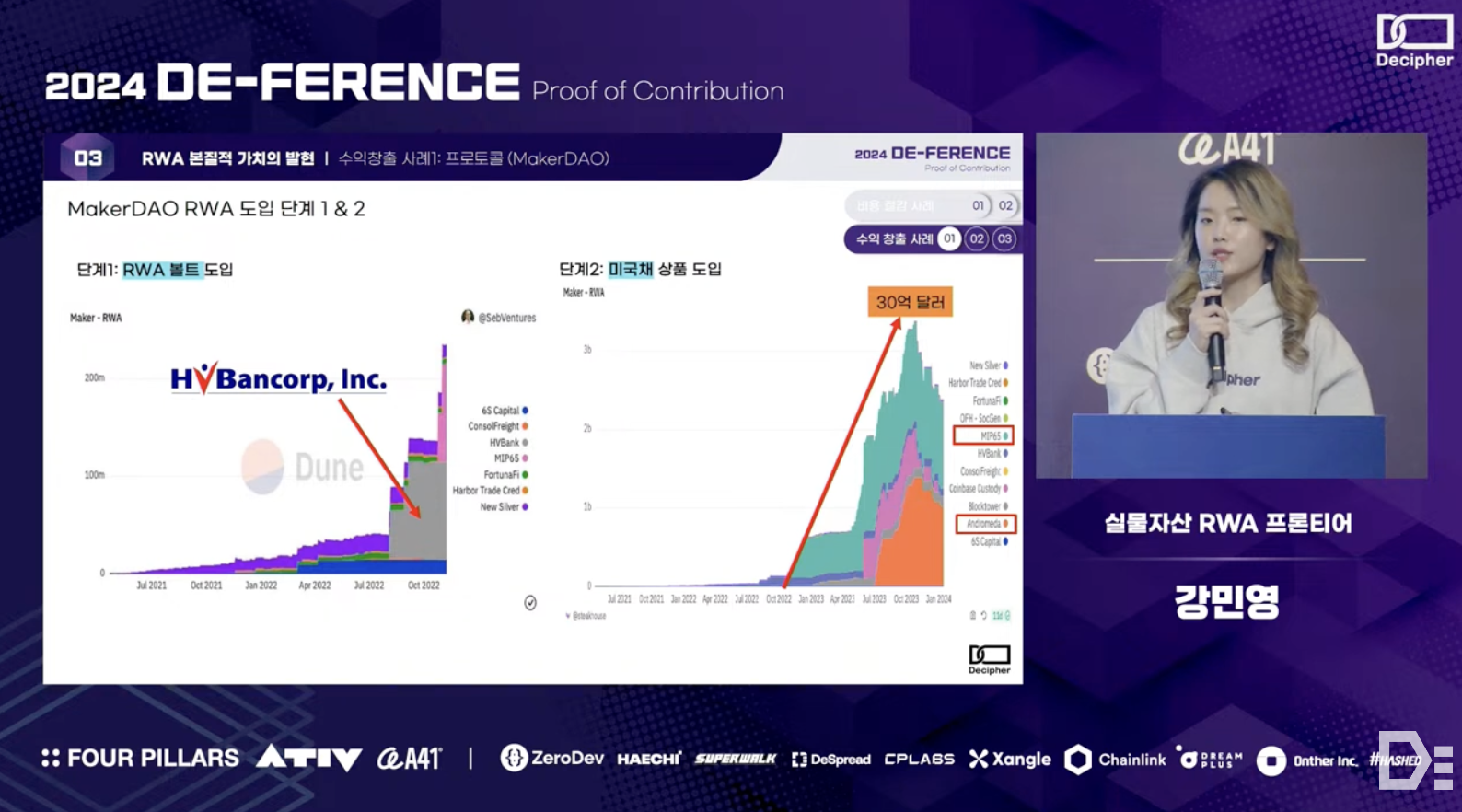

The first case is the collateralized lending protocol, MakerDAO. MakerDAO is a prominent DeFi protocol that introduced RWA operations in the blockchain space, attracting significant liquidity through various RWA vaults. It expanded liquidity by attempting to collateralize commercial real estate development projects, freight bills of lading, or HVBank loan products to issue DAI. In October 2022, they introduced the MIP65 vaults, which use U.S. Treasury bonds and corporate bonds as financial products, and in July 2023, they launched the BlockTower Andromeda vaults, which use U.S. short-term Treasury products, securing liquidity in a rising interest rate market.

To reduce macroeconomic dependence and enhance overall vault stability in MakerDAO, the proportions of RWA and DSR are organically adjusted, and their effects are tested at the moment. These cases demonstrate that RWA product adoption can bring traditional market funds onto the blockchain.

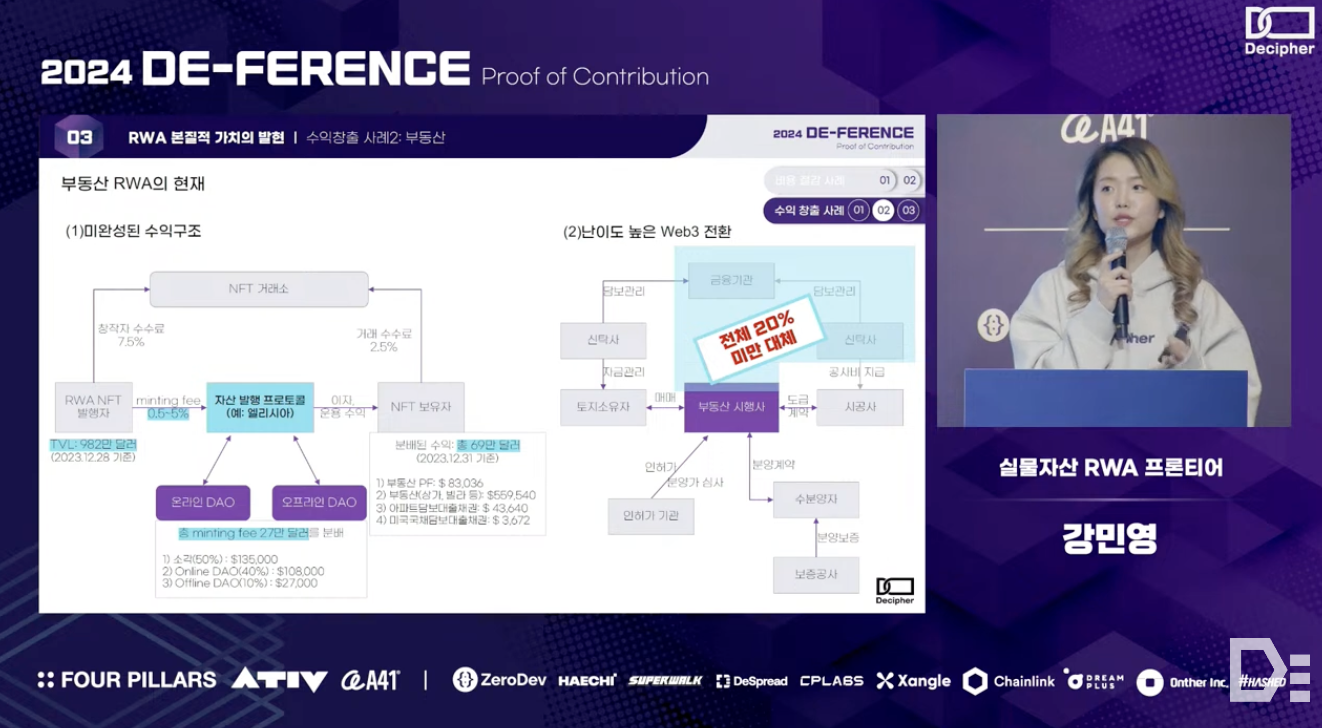

The second case is the real estate RWA project, Elysia. Elysia issues RWA NFTs to real estate holders, allowing them to engage in secondary financial activities. Such real estate RWA projects offer clear advantages in investment accessibility, enabling cross-border real estate investments or fractional investments in real estate assets. However, while similar to traditional REITs, Elysia differentiates itself by allowing DAOs and smart contracts to handle middle and back-office operations typically managed by traditional asset management companies or custodians.

But there might be some challenges in practically implementing real estate RWA projects - first, the minting fees for real estate asset NFTs are low, ranging from 0.5% to 5%, and must be shared among multiple parties, limiting the platform's revenue generation. Thus, achieving sustainable growth in this business is challenging. Second, the most profitable segment of real estate is the development sector, and considering the overall structure and ecosystem of this business, blockchain can improve less than 20% of this segment.

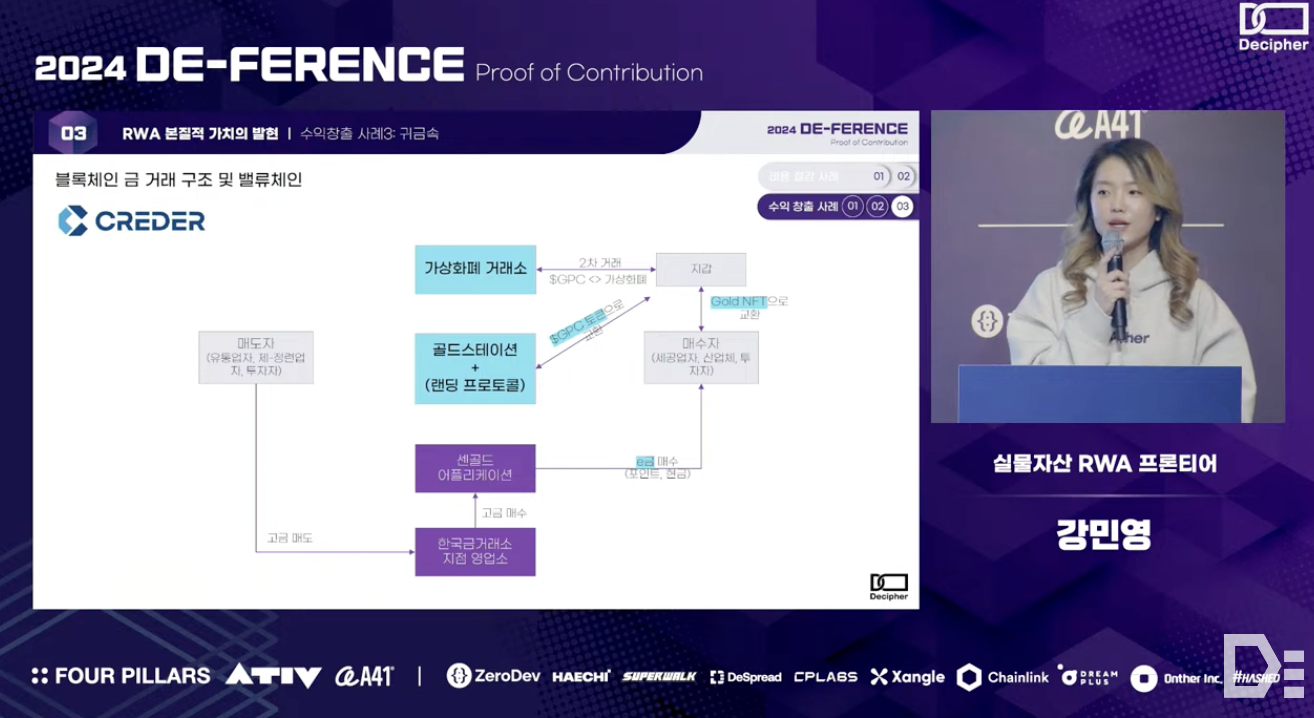

The final case of additional revenue generation opportunities involves precious metals RWA. General gold trading is freely available on the Korea Exchange, but a team called Creder connects this trading logic with DeFi protocols, converting physical gold into digital gold and supporting secondary financial transactions on the blockchain.

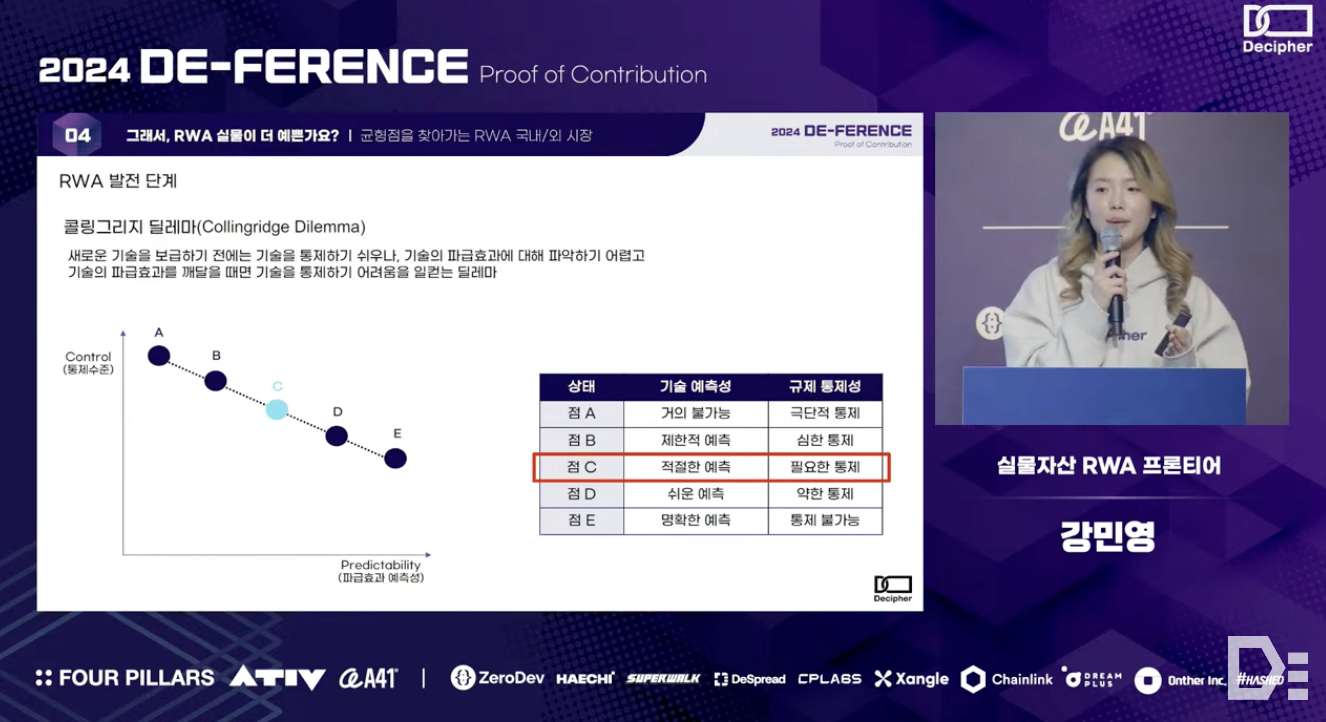

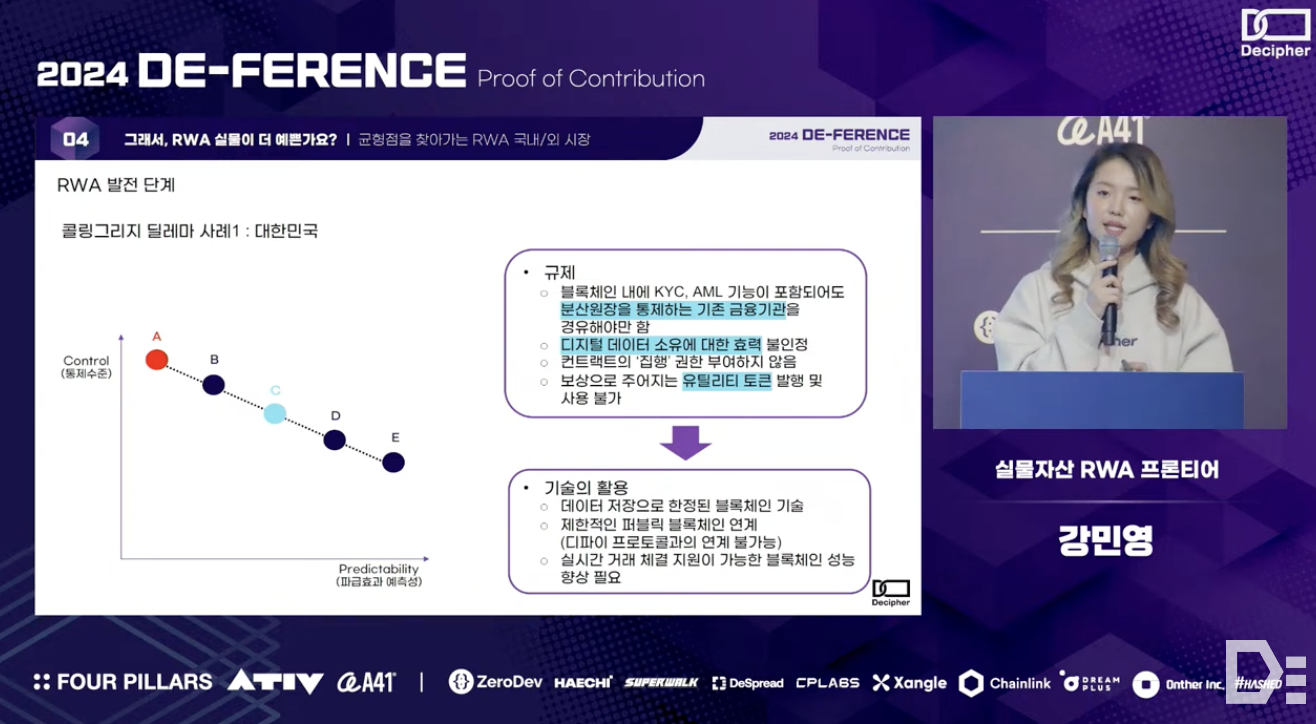

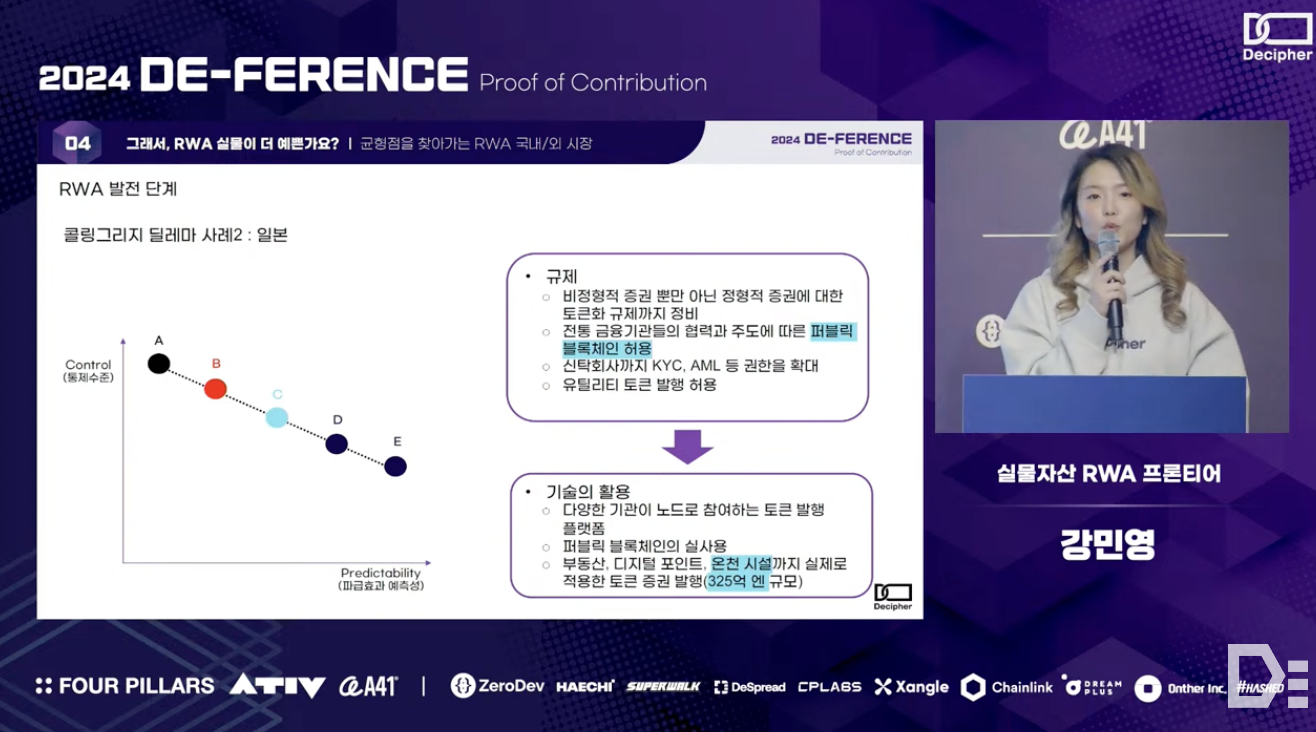

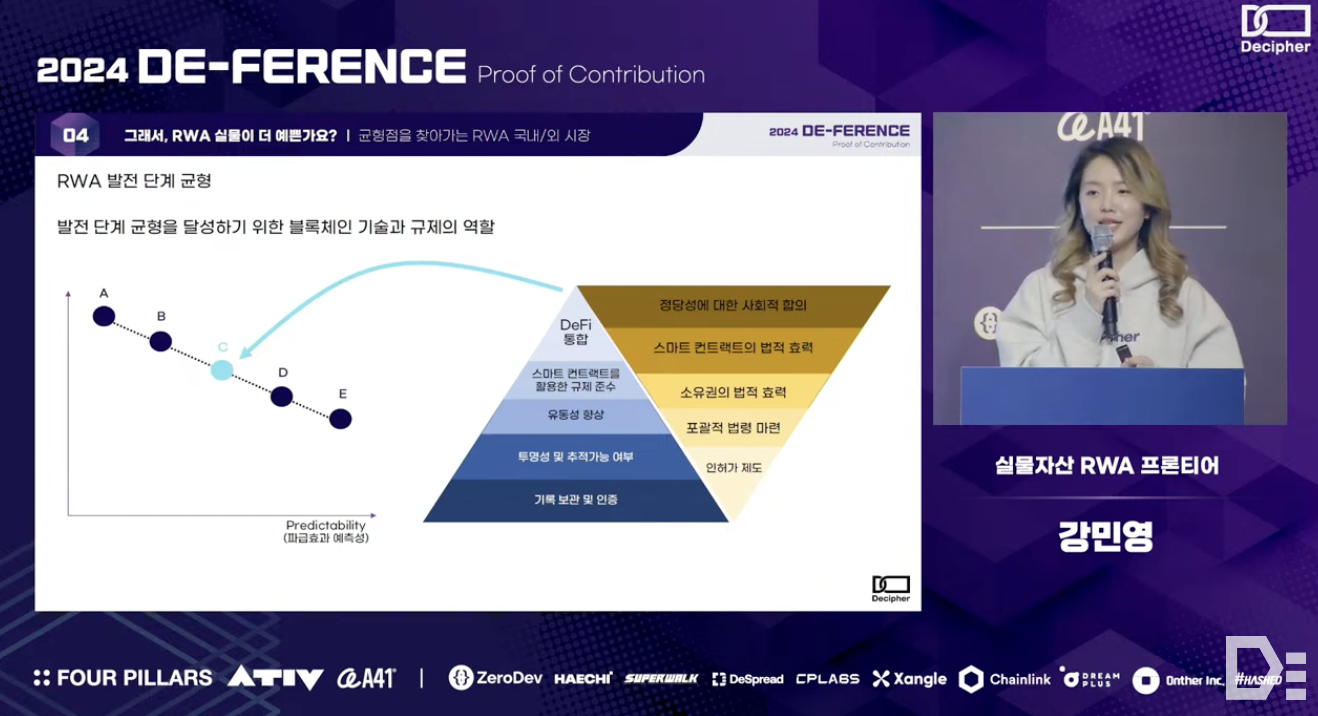

Finally, the RWA Frontier team analyzed the regulatory landscape for RWAs in different countries using the Collingridge Dilemma framework - the Collingridge Dilemma helps diagnose how to balance and address regulatory uncertainties that arise from the difficulty in predicting the innovation and impact of new technologies.

First, the regulatory control level in Korea is considered very high. Even if KYC and AML functions are inherently present on the blockchain, the market will not open unless existing financial license holders control the distributed ledger. Additionally, government regulations do not recognize the ownership of digital data, limit the use of blockchain to merely storing ledger data, and do not permit the issuance or use of utility tokens as transaction rewards on the blockchain.

In Japan, the regulatory environment is more advanced compared to Korea - Japan has established regulations not only for fractional investments and new asset areas but also for efficient markets such as bonds and securities. Additionally, the ecosystem allows traditional financial institutions to participate as nodes in public blockchains and issue tokens. Trust companies also have expanded authority to perform KYC and AML functions. Furthermore, the issuance of utility tokens is relatively unrestricted, leading to attempts to tokenize regional specialties or hot spring facilities. There are also active efforts to link RWA assets with DeFi protocols.

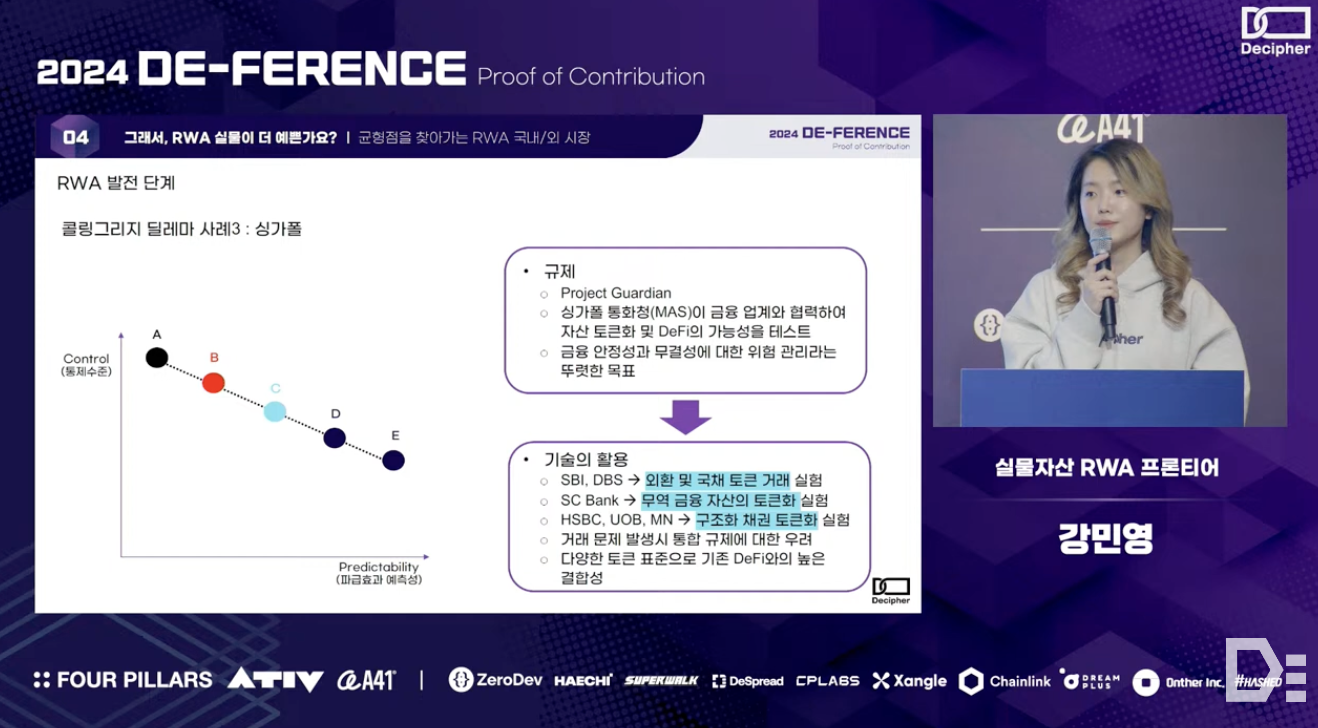

Lastly, although Singapore's approach is somewhat different, it is seen as having a regulatory level similar to Japan. The Monetary Authority of Singapore is working with financial institutions to promote asset tokenization through 'Project Guardian' and is relatively lenient regarding the issuance of utility tokens. This has led to various technological applications, including foreign exchange and government bond tokenization by SBI & DBS, trade finance asset tokenization by SC Bank, and structured bond tokenization by HSBC, UOB, and MN. Additionally, there are active efforts to adopt mainnet token standards like ERC-20, aiming to support integration with the existing DeFi market.

In summary, for blockchain to support various initiatives at a national level, appropriate technical implementation must be accompanied by flexible regulations - blockchain should evolve beyond merely serving as a record-keeping database to flexibly support secondary financial activities through integration with DeFi protocols. Regulations should initially begin with limited permissions but gradually recognize new concepts or rights introduced by blockchain. Ultimately, they should aim to achieve public consensus on the legitimacy of the blockchain financial system.

Q: Could you explain more about why stablecoins are not considered dollar RWAs?

A: Firstly, the RWA Frontier team believes that RWAs should directly reflect the value of physical assets. For example, when precious metals are tokenized, the token should always maintain the same value as the physical asset and be exchangeable at a 1:1 ratio. In the case of stablecoins, they are pegged to 1 dollar. However, Tether operates at an institutional level and runs its business through the profits from its operations. In other words, while an individual stablecoin holds the value of a dollar, we do not believe that all stablecoins circulating on the blockchain are equivalent in value to all the assets managed by Tether.

Q: I understand that there have been many attempts related to STO in Korea, but it seems there aren't many cases that have been successfully implemented. Could you share specific details about the progress of regulations related to RWA in Korea?

A: There is currently a guideline called the "Framework for the Regulation of Token Securities Issuance and Distribution," which was released in February last year. It is expected that more detailed guidelines will be issued in the future, focusing separately on issuance and distribution. As for real cases of STO, many are anticipated to emerge around the second half of this year.

Q: The STO being promoted in Korea can also be considered a part of RWA. I am curious about your outlook on the domestic STO market for this year.

A: This topic was briefly touched upon in the previous question by another team member, but personally, I think it is difficult to expect explosive growth at this early stage. However, it is noteworthy that in January this year, the Korea Exchange applied for an innovative financial service (financial regulatory sandbox) that allows for the trading of digital assets. For the token securities market to be activated, both the issuance and distribution markets are crucial. In this context, a state-approved sandbox will be an important driving force for the STO market to achieve significant results in its early stages.

Overview

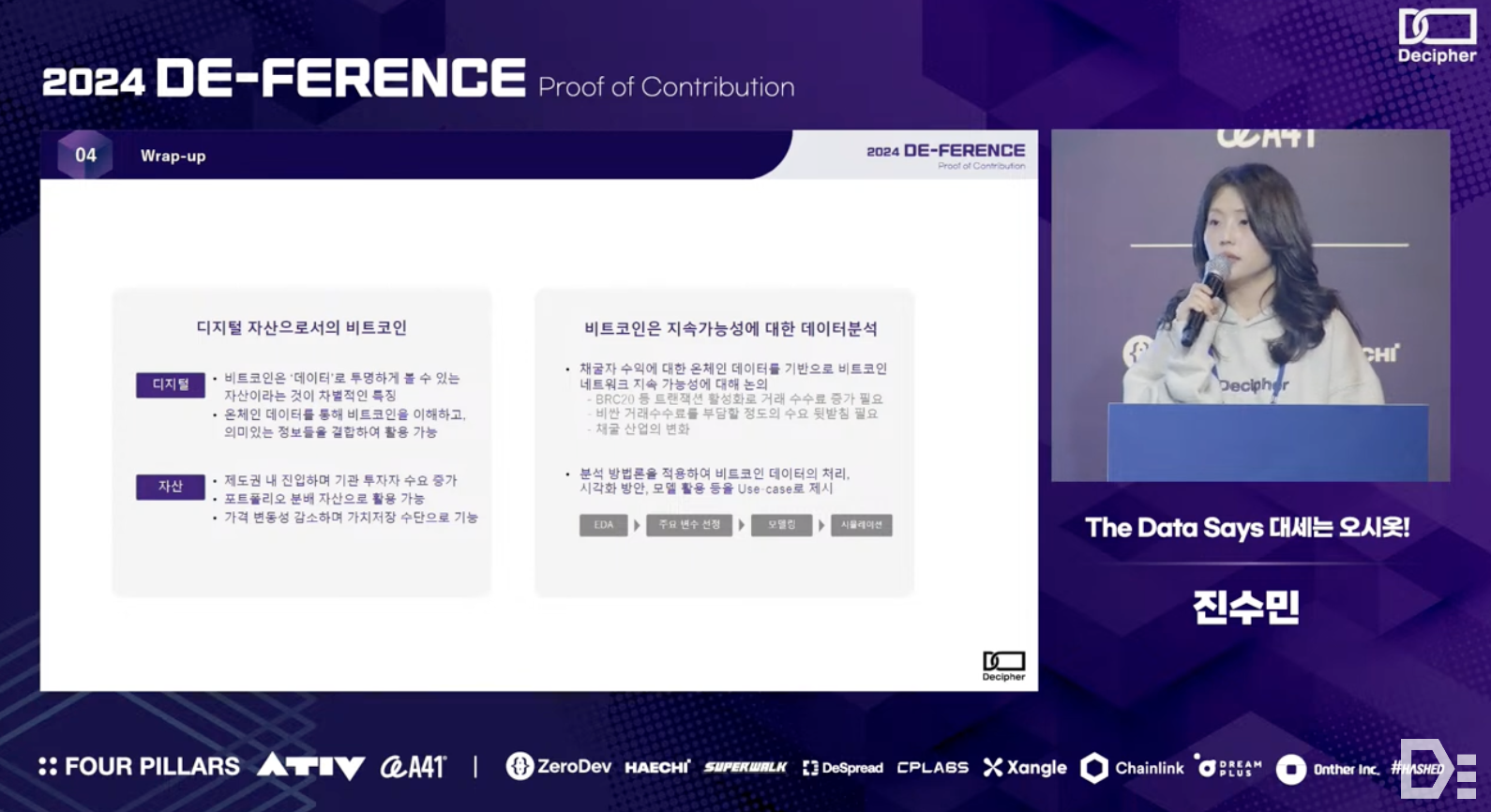

Sumin Jin from the O-siot team shared the results of an analysis that combined on-chain data with various off-chain data to explore the sustainability of Bitcoin, which is gaining attention as a digital asset or store of value. More specifically - the team observed patterns in Bitcoin's price, hash rate, and miner pool dynamics during past halving cycles. Through simulation modeling, they quantitatively revealed how transaction fees and Bitcoin prices need to be complementarily structured to maintain the network's sustainability at or above the current level.

Comments

No matter how public and transparent it is, interpreting raw, anonymous on-chain data with countless transactions and deriving actionable plans from it is not an easy task. The presentation by the O-siot team effectively conveyed to the public the dynamics of the Bitcoin mining market, which holds significant influence over the crypto industry due to its substantial share of market liquidity, through easily understandable infographics.

Moreover, attempts to model using specific papers for simulation are particularly significant in analyzing trends in the crypto industry and, further, the sustainability of individual platforms in the future. This presentation provided an opportunity not only to understand the history and trends of the Bitcoin mining market but also to think about sustainability of various other platforms.

Below is a summary of Sumin Jin's presentation.

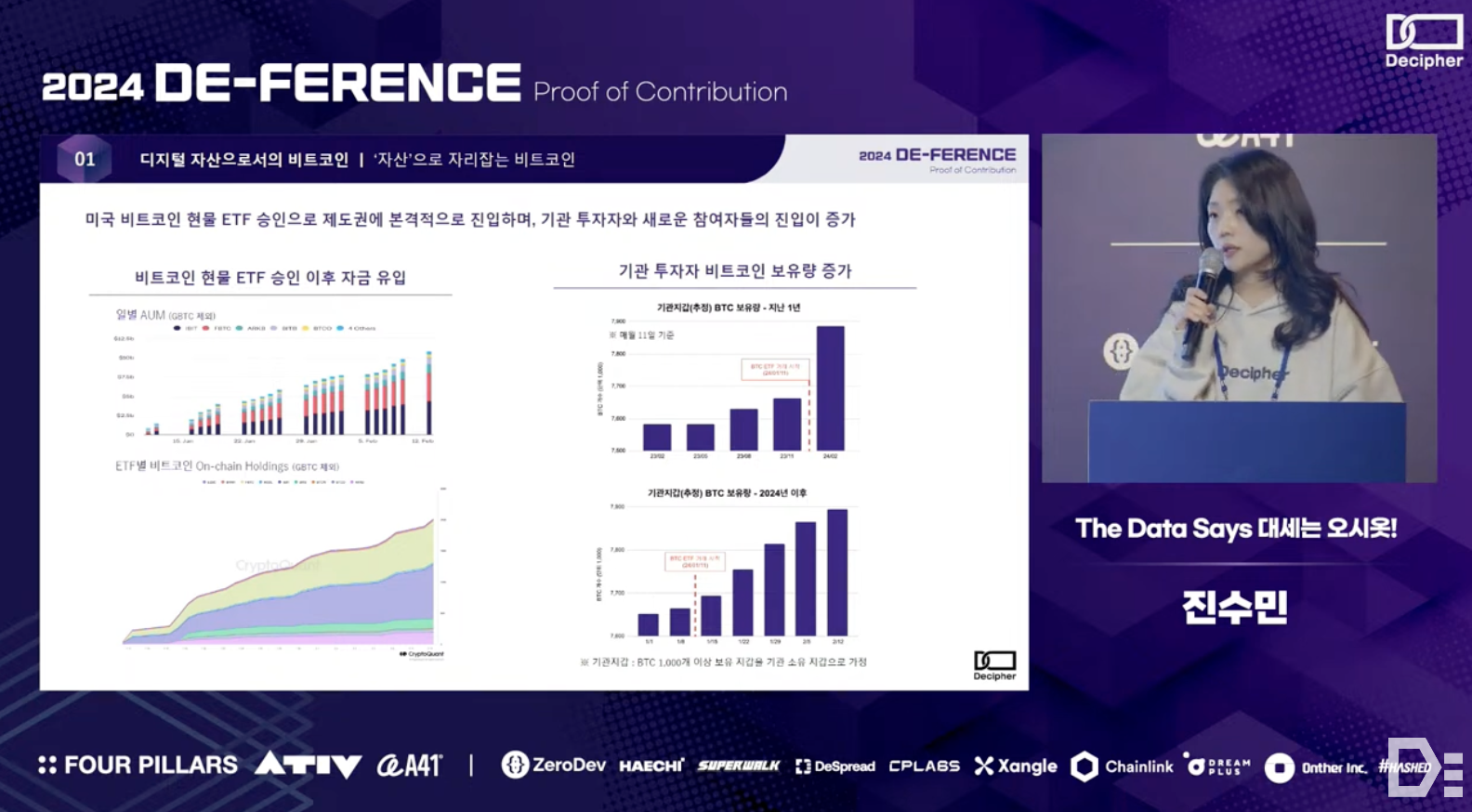

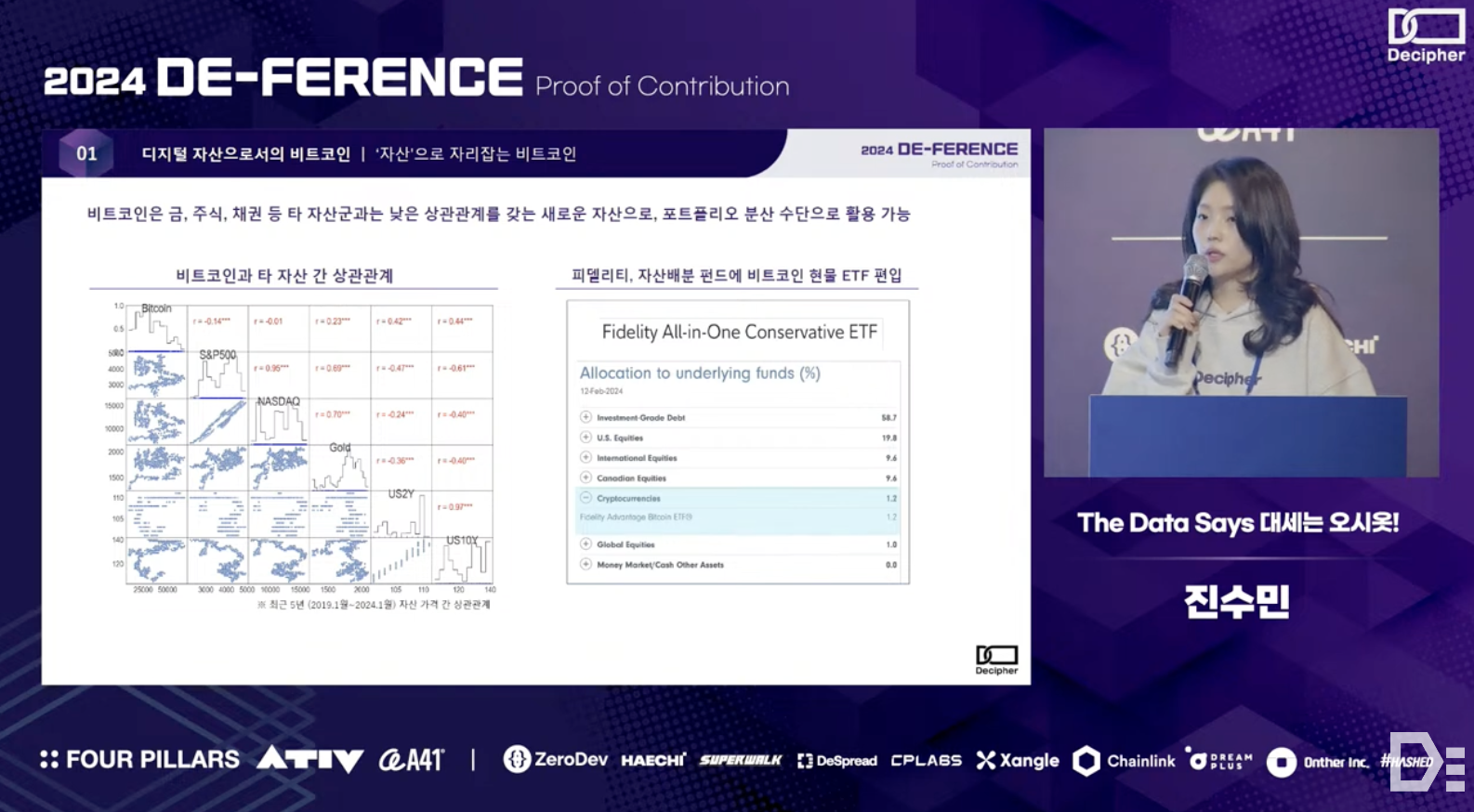

Bitcoin is an asset created on a digital network, distinguished by its ability to transparently and in real-time display all supply, transactions, and ownership statuses as data. Recently, Bitcoin has been solidifying its position as an asset, especially with the approval of Bitcoin spot ETFs, which marked its formal entry into the mainstream financial system. This has led to a sharp increase in participation not only from institutional investors but also from new retails.

Bitcoin is considered a new asset with low correlation to other assets like gold, stocks, and bonds over the past five years. Therefore, it is also attractive as a means of portfolio diversification - in fact, Fidelity has included Bitcoin spot ETFs at a ratio of about 1% in their asset allocation funds. Bitcoin, often compared to digital gold, is also showing its potential as a store of value as its price volatility gradually decreases.

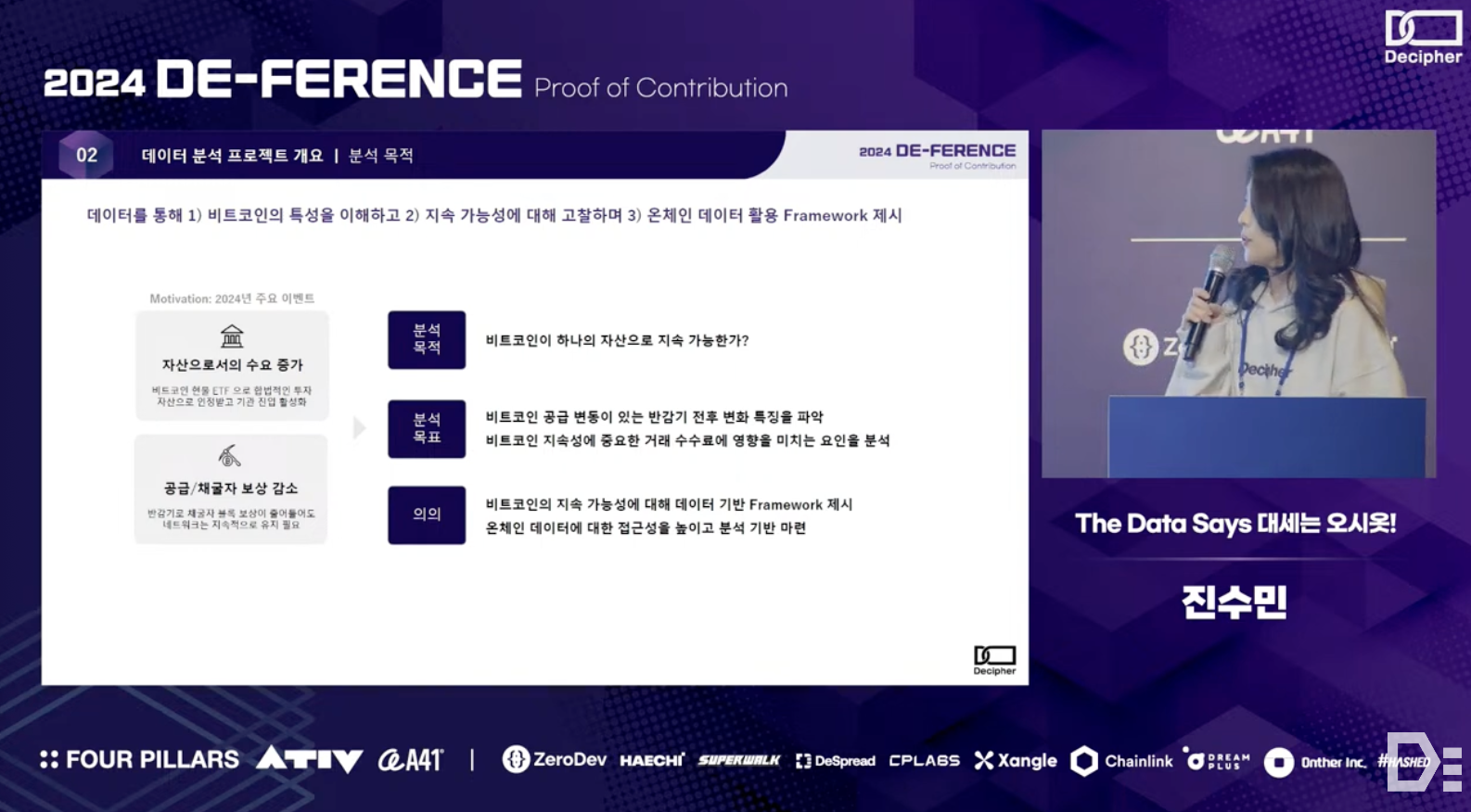

The demand for Bitcoin as an asset is increasing, and there is a significant event scheduled for the first half of the year (i.e., April) - the Bitcoin halving. Therefore, it is time to consider whether Bitcoin is sustainable as an asset. In response, the O-siot team aimed to create a data analysis framework that anyone can easily understand to examine the sustainability of Bitcoin.

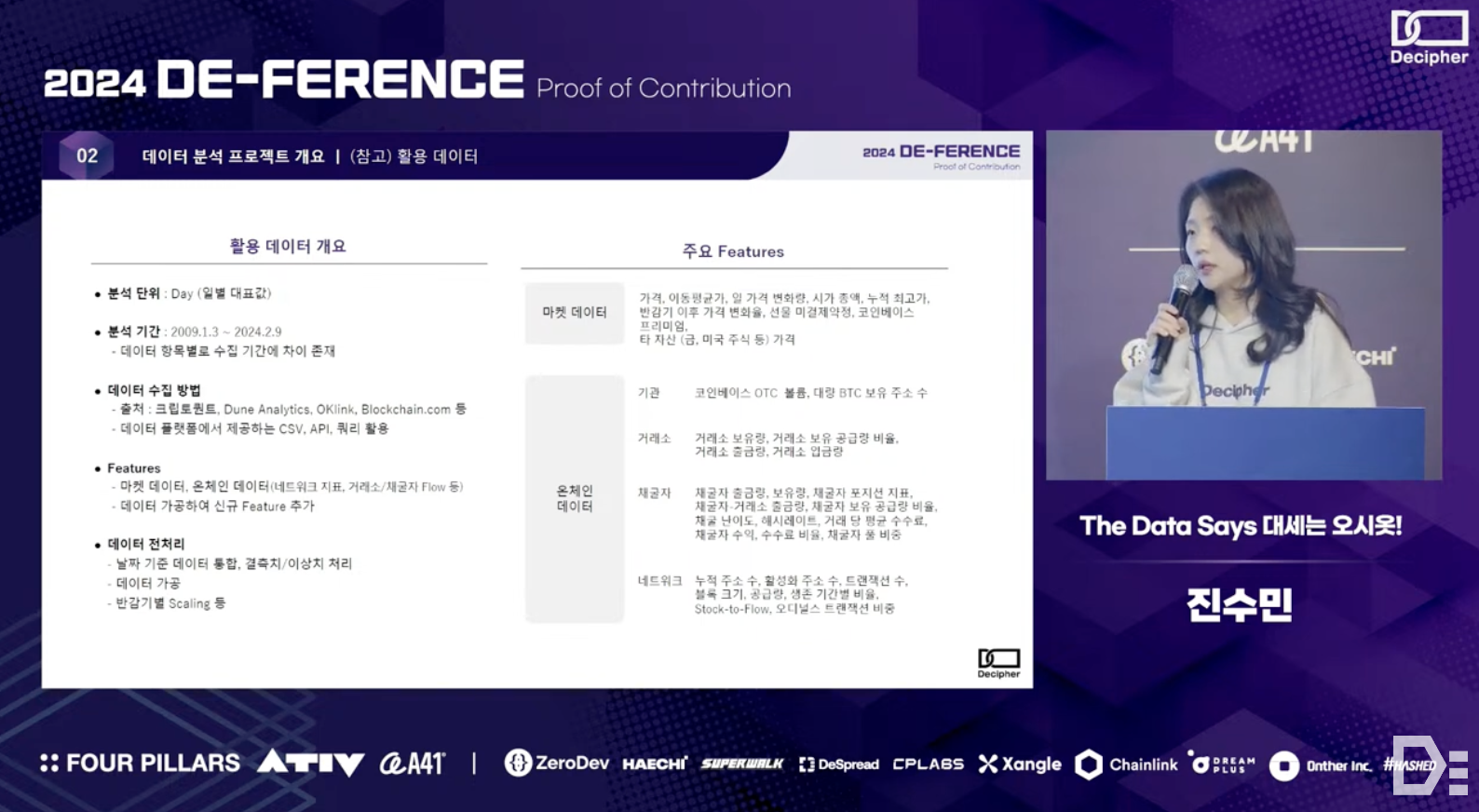

For reference, although anyone can view raw blockchain data, utilizing or interpreting it is not easy. Therefore, it is necessary to preprocess the data for better analysis or integrate off-chain data for labeling. In this regard, the O-siot team worked on collecting market data and on-chain data from various sources such as CryptoQuant, Dune Analytics, Oklink, and Blockchain.com, and preprocessing it for analysis.

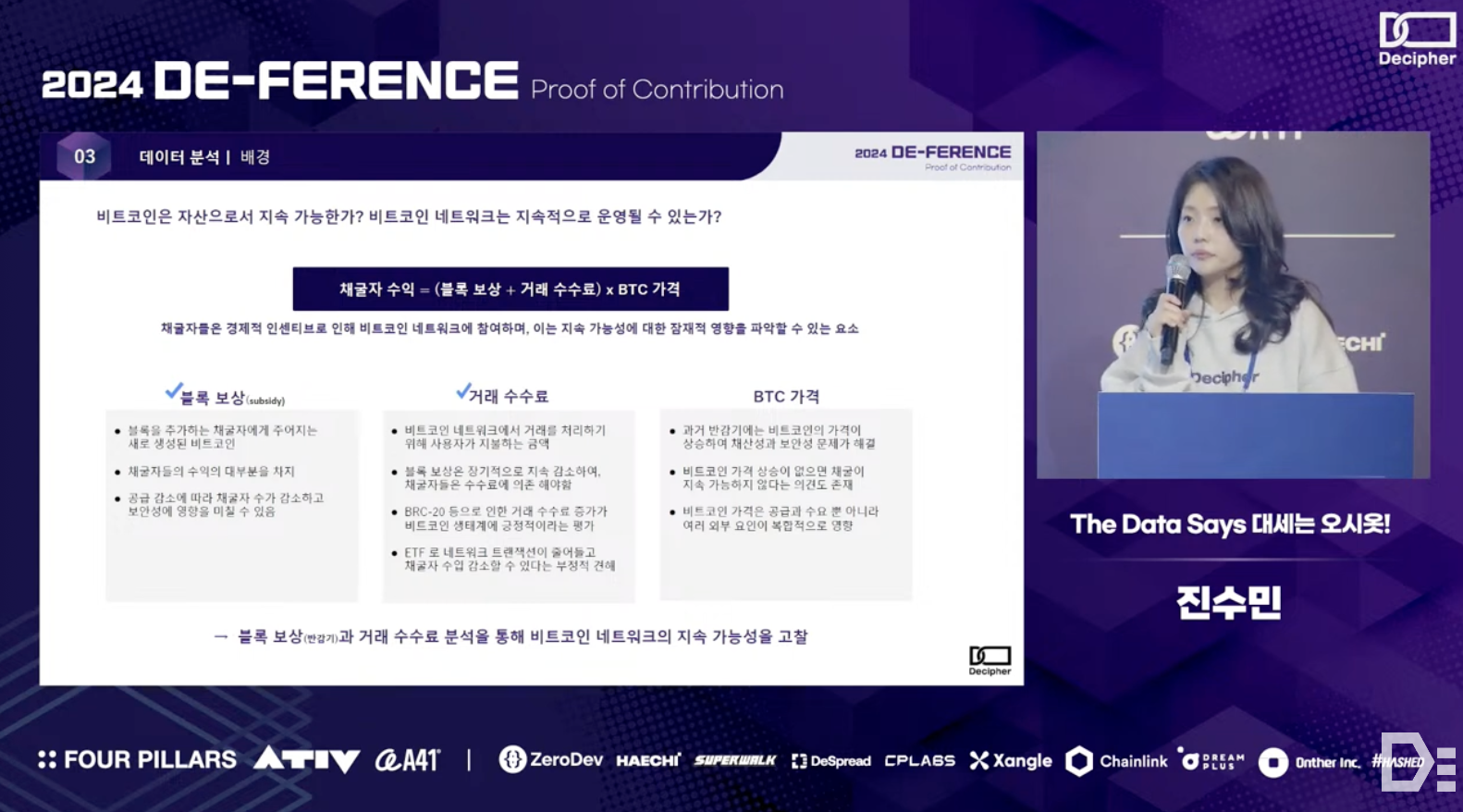

To evaluate the sustainability of Bitcoin as an asset, we need to determine whether the network can continue to operate. The Bitcoin network can operate by providing economic incentives to Bitcoin miners, whose revenues are related to block rewards, transaction fees, and the price of Bitcoin. However, since block rewards decrease over time due to halving events, miners will increasingly rely on transaction fees. Therefore, it is argued that more use cases with transactions, like Ordinals, need to be created and that the price of Bitcoin needs to rise. In this context, the O-siot team conducted an on-chain analysis of block rewards and transaction fees to assess the sustainability of the Bitcoin network.

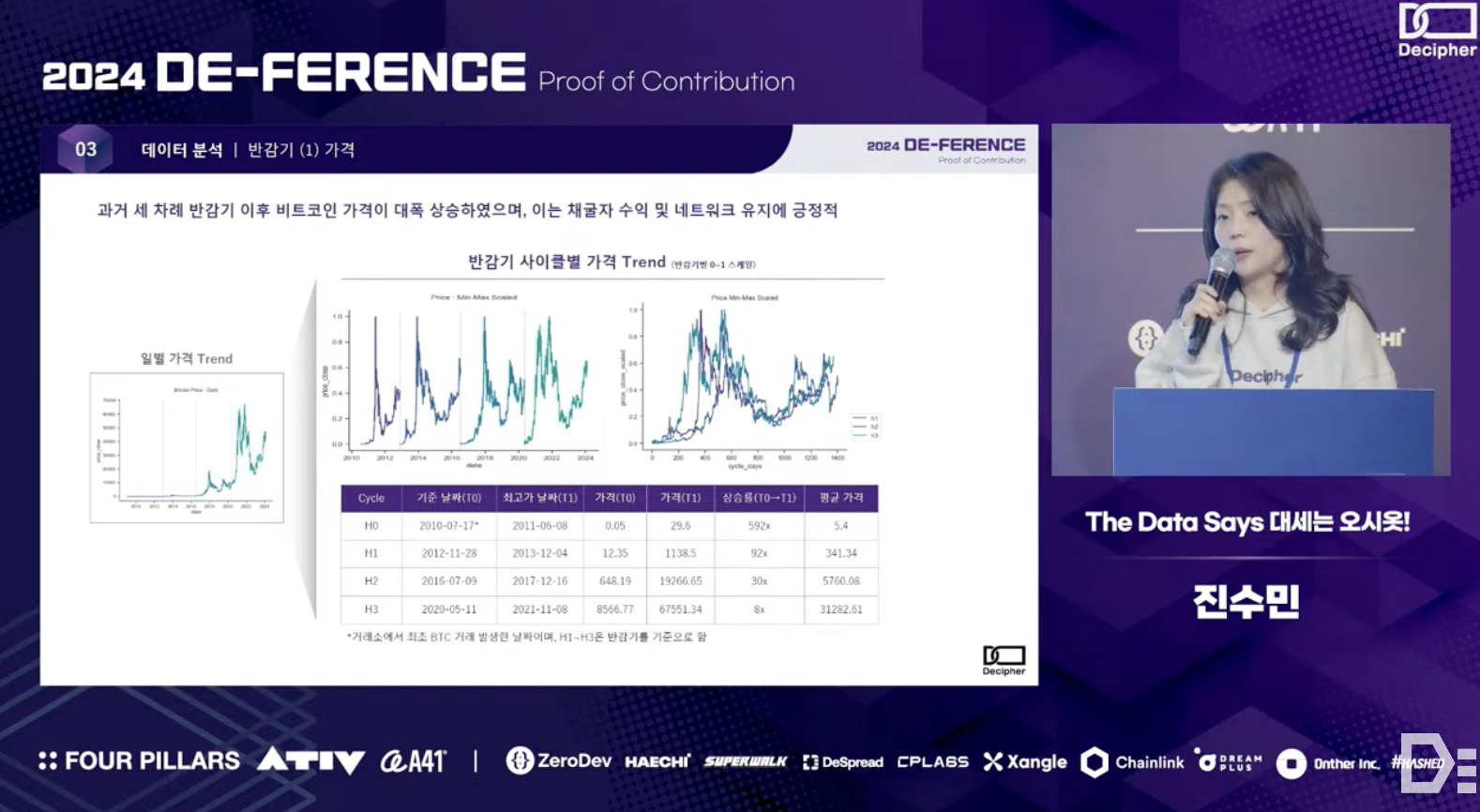

When the scheduled Bitcoin halving takes place in April, the block reward will decrease to 3.125 Bitcoins. In the past three halvings, Bitcoin's price has significantly increased due to the rise in scarcity. By separating Bitcoin's daily price trends by halving cycle and visualizing them using Min-Max scaling, it was observed that each cycle's pattern is very similar. Bitcoin's price tends to reach its peak approximately one to one and a half years after the halving, followed by cycles of decline and rise.

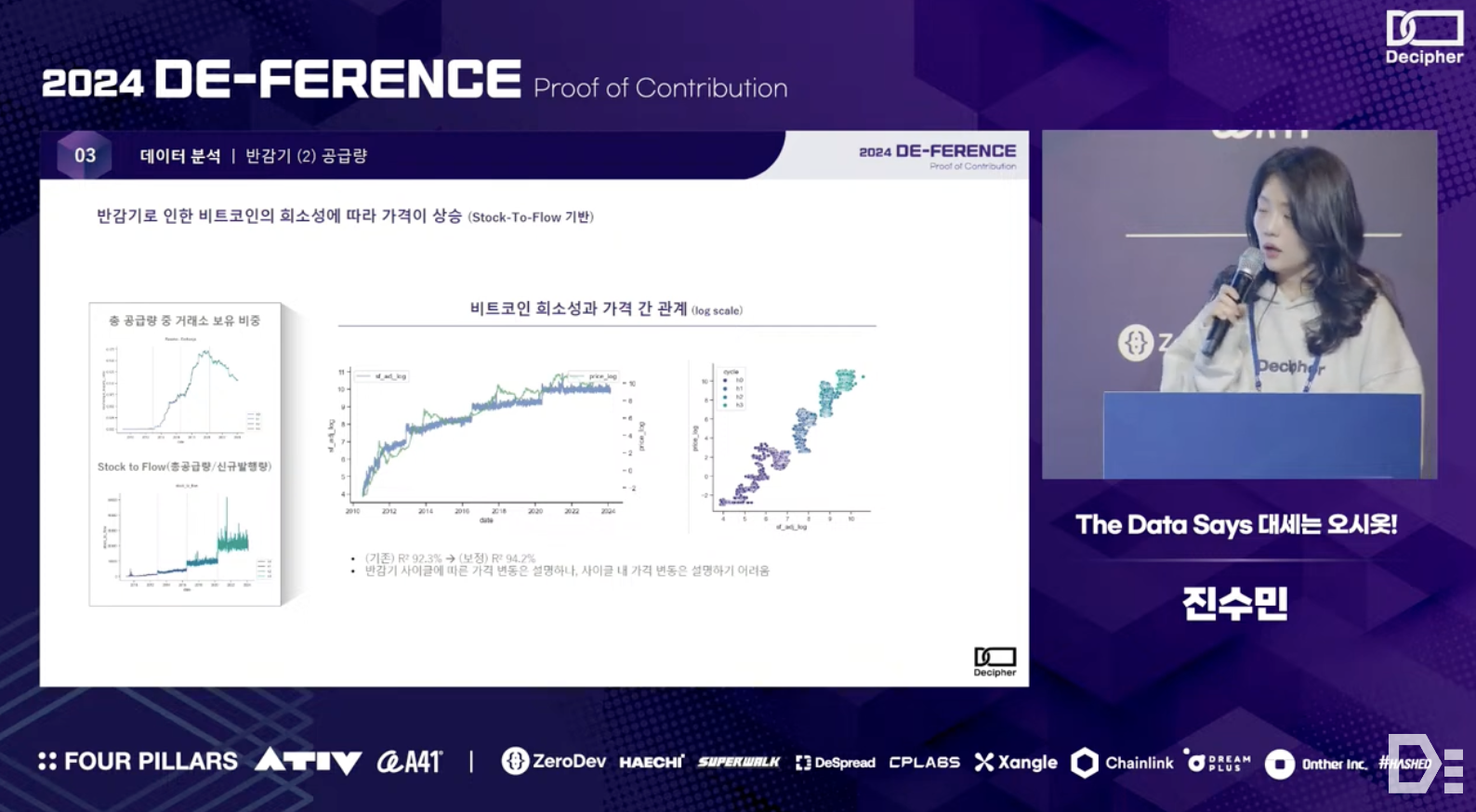

There are many factors that determine the price of Bitcoin, with scarcity due to supply reduction being a notable one. Analysis using the Stock to Flow (total supply/new issuance) model revealed a high correlation between this value and price fluctuations following halving cycles - however, the price variations within each cycle are not easily explained.

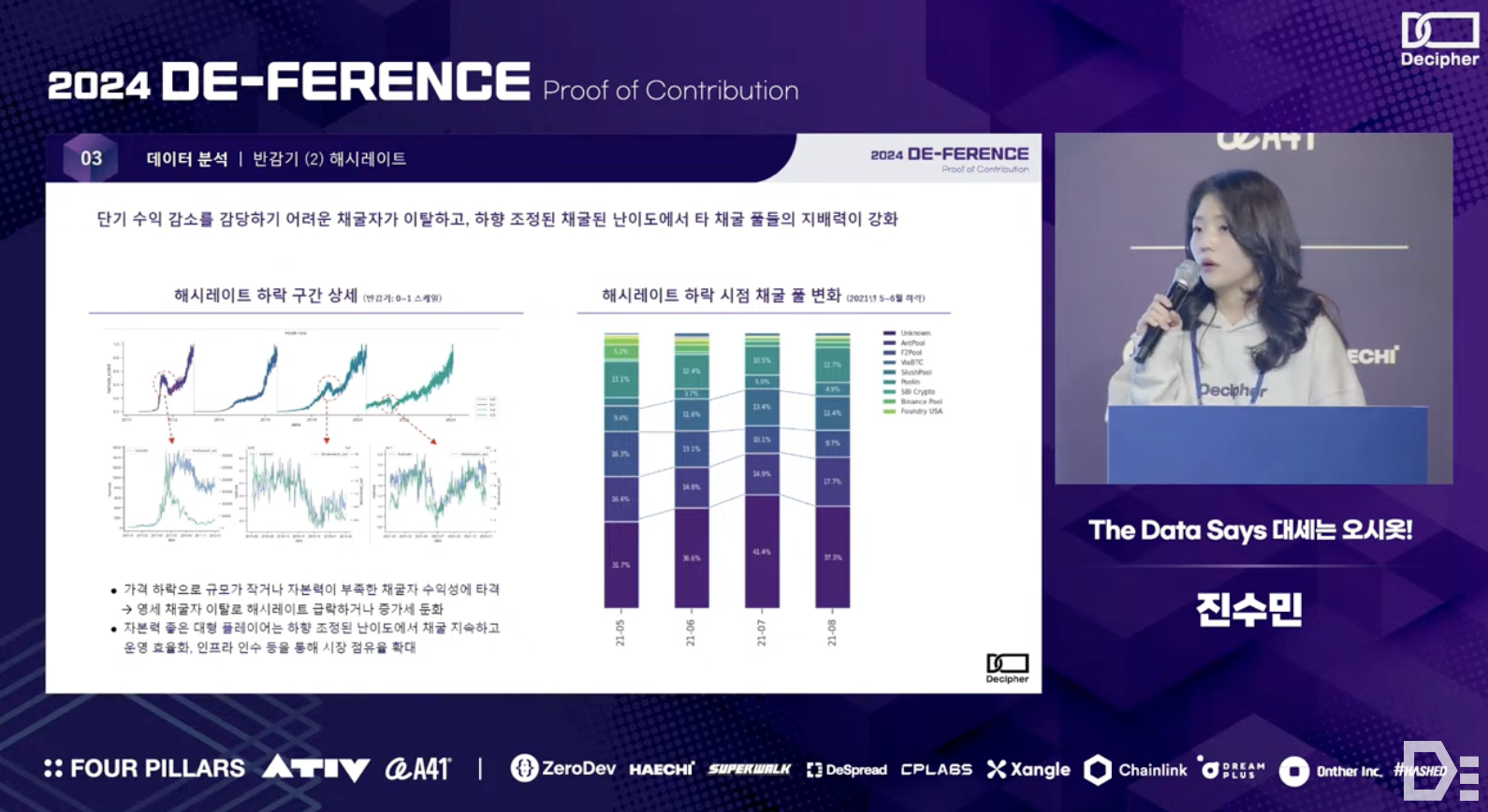

After the halving, if mining costs (hash rate) increase, some miners may not be able to bear the costs and will exit the market, which could lead to a decline in Bitcoin prices and create a vicious cycle. As shown in the left graph, there are times when the increase in hash rate slows down or drops sharply due to miners exiting the market. During these periods, smaller or less capitalized miners suffer losses in profitability. On the other hand, large and well-capitalized miners can acquire these smaller miners, gaining market dominance - this shift in miner dynamics towards larger players is evident in the bar plot on the right.

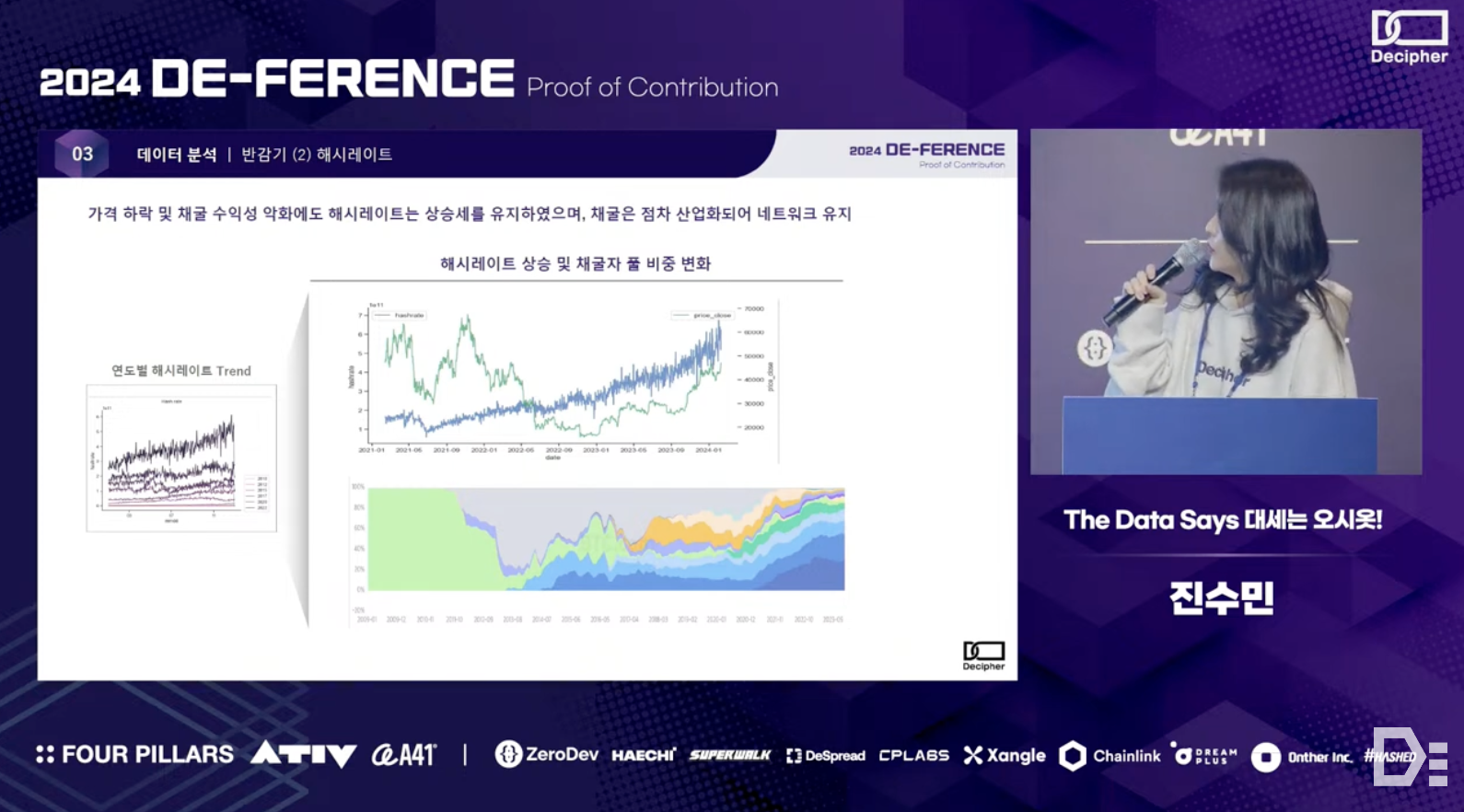

Looking at the hash rate trend during the Bitcoin price drop in 2022, we can see that the hash rate, which had plummeted along with the price, quickly recovered due to changes in the dynamics of mining pools market and maintained an upward trend in the long term. This could be seen as an indication that the industry is gradually becoming more industrialized, focusing on competitive mining pools.

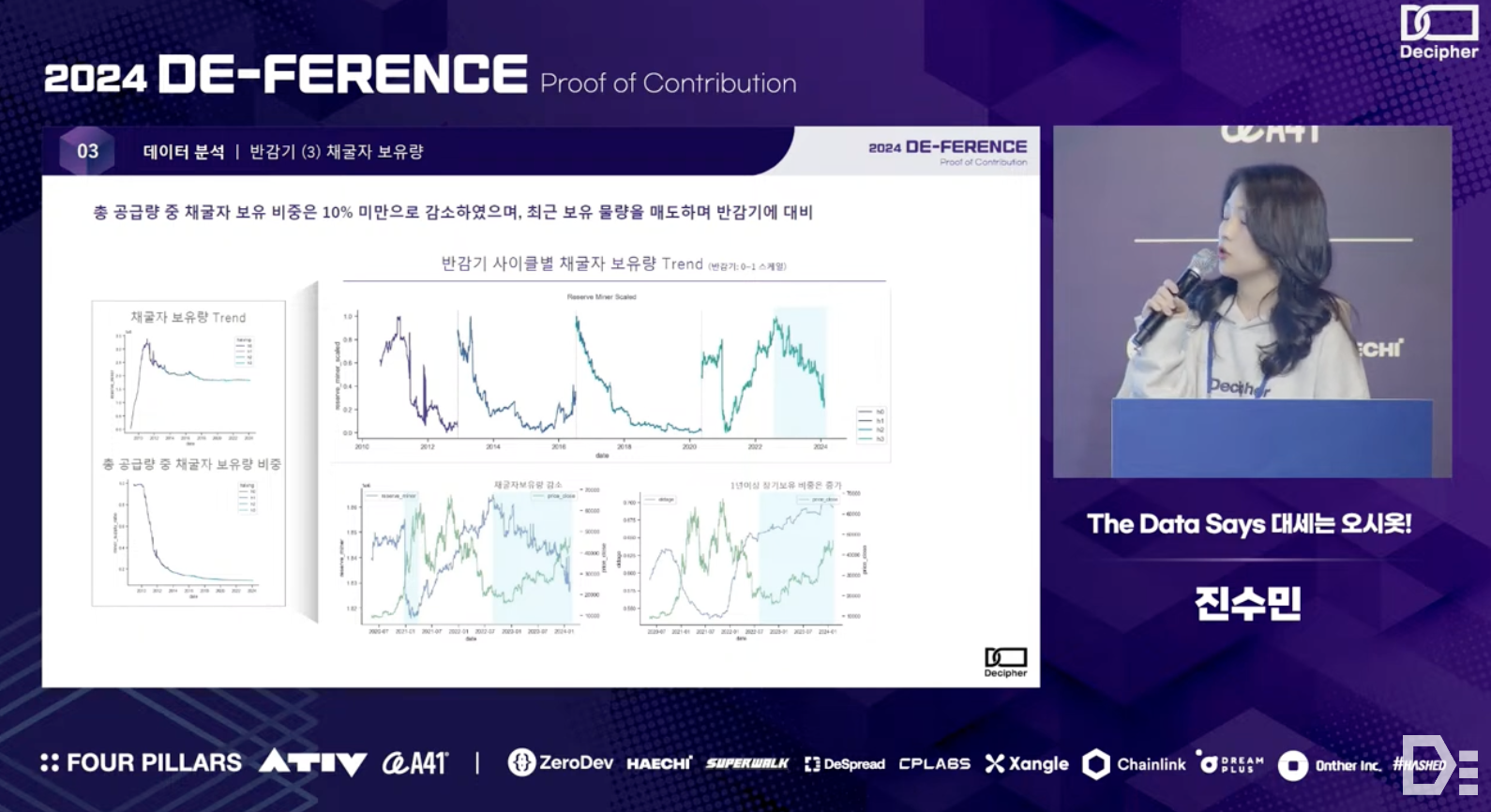

Currently, the proportion of Bitcoin held by miners is less than 10% of the total supply, and this percentage has been steadily decreasing compared to the past. As this proportion decreases, we can expect less price volatility due to miners' selling. Before the halving, miners often sell their Bitcoin holdings in advance to prepare for the reduction in block rewards. As shown in the graph, while miners' Bitcoin holdings have consistently decreased in each cycle, the recent cycle shows a slightly different pattern - after partially cashing out during the bull market in 2021, miners increased their Bitcoin holdings and then gradually started selling from the second half of 2022.

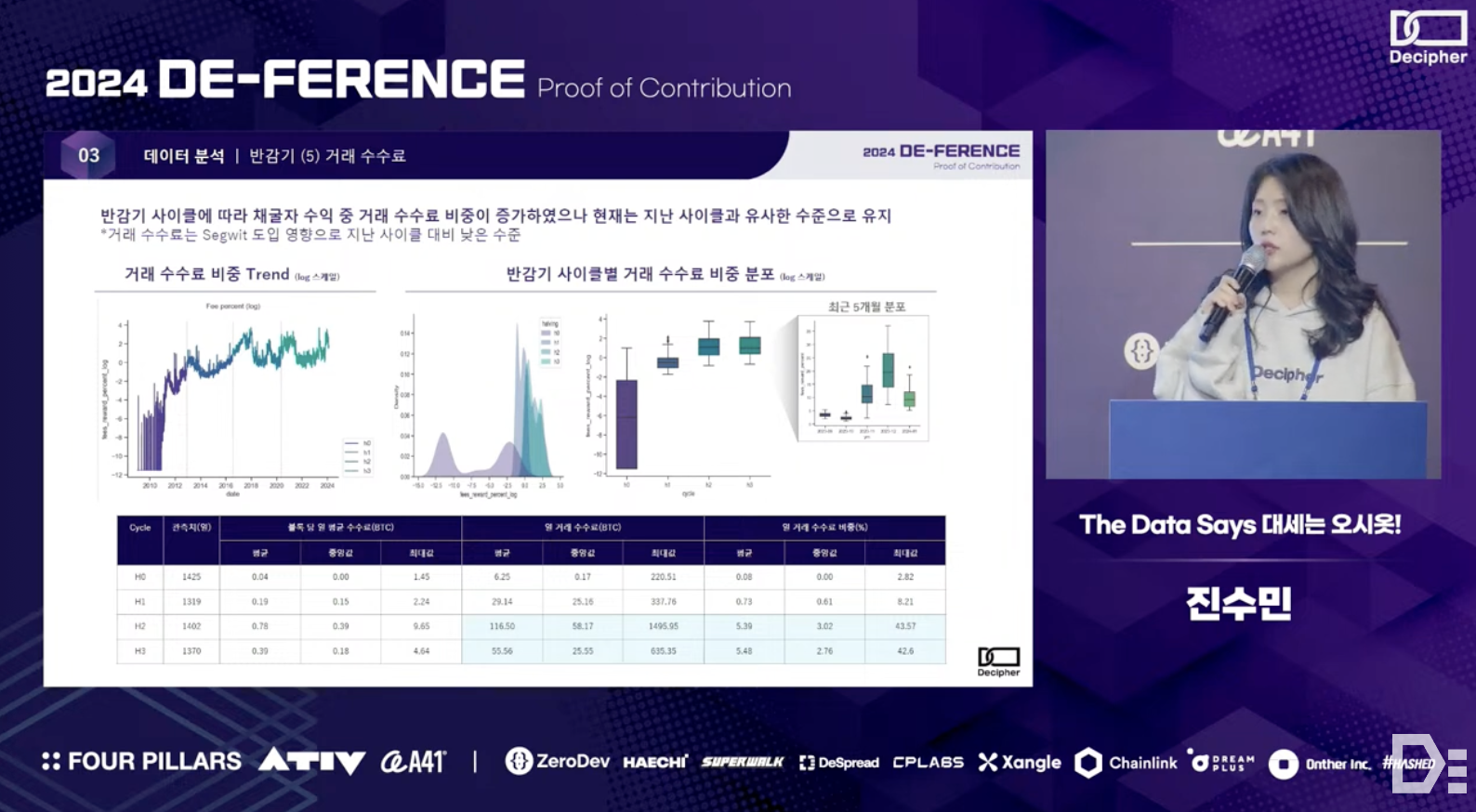

As previously mentioned, while miners adjust dynamics to maintain profitability due to price fluctuations and competition among themselves, their revenue is increasingly dependent on transaction fees in the long term. Historically, transaction fees have only accounted for about 5% of total miner revenue on average. However, since last year, due to increased transaction demand from Ordinals and other factors, this proportion has recently risen to around 30%. This is a positive indication that the Bitcoin network is becoming more active and miner revenues are stabilizing.

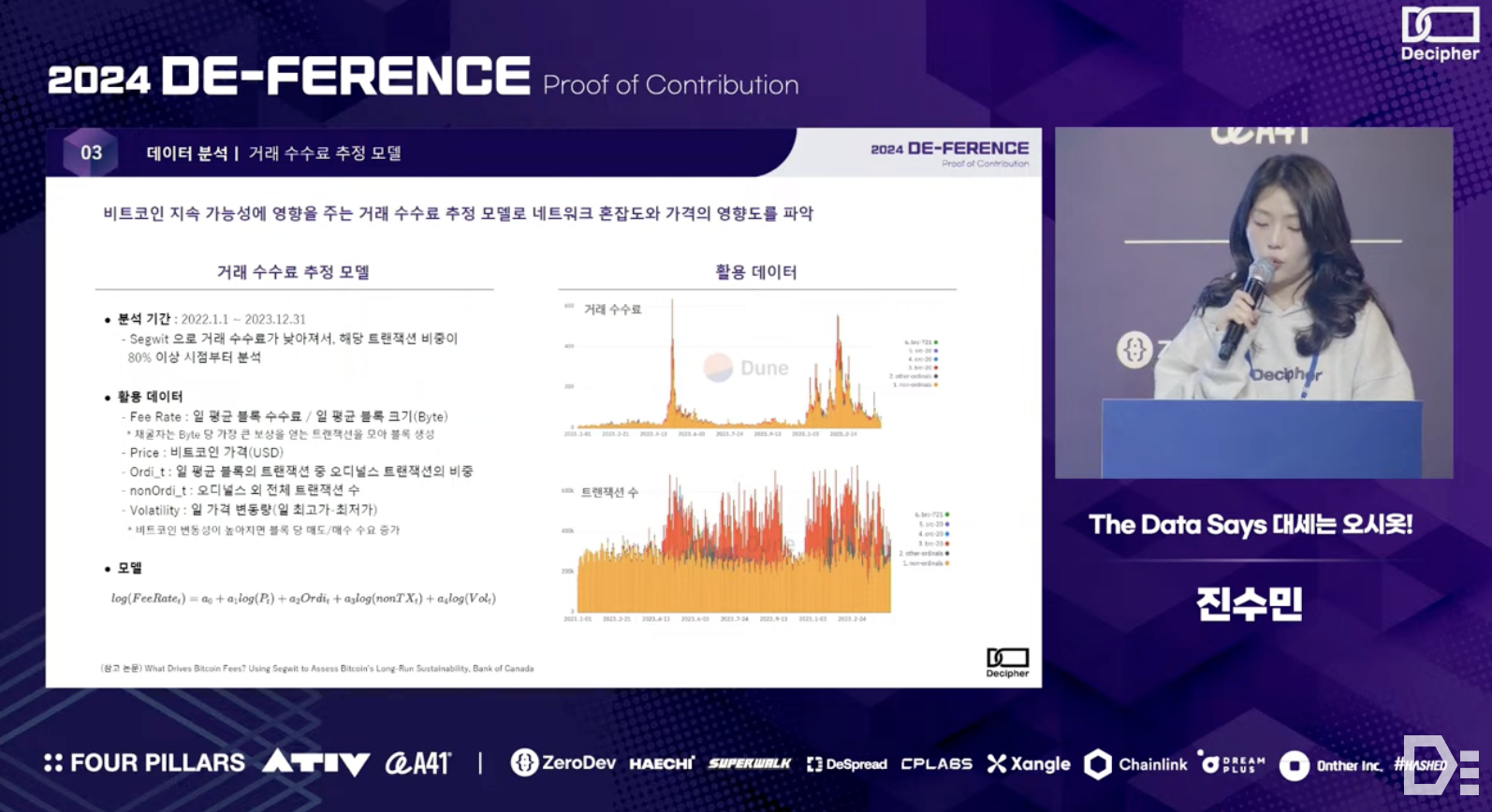

네트워크 혼잡도와 가격의 영향을 파악하기 위해 오시옷 팀은 Segwit 도입 이후 2022년 1월 1일부터 2023년 12월 31일까지 약 2년간의 트랜잭션 데이터를 분석하여 거래 수수료(Fee Rate) 추정 모델을 만들었다 - 이 모델은 비트코인의 가격, 일 평균 오디널스 트랜잭션 비중, 오디널스 외 전체 트랜잭션 수, 일 가격 변동량 등을 변수로 삼았다.

To understand the impact of network congestion and price, the O-siot team analyzed transaction data over approximately two years, from January 1, 2022, to December 31, 2023, following the introduction of Segwit - the team developed a fee rate estimation model using variables such as Bitcoin's price, the daily average proportion of Ordinals transactions, the total number of non-Ordinals transactions, daily price volatility, etc.

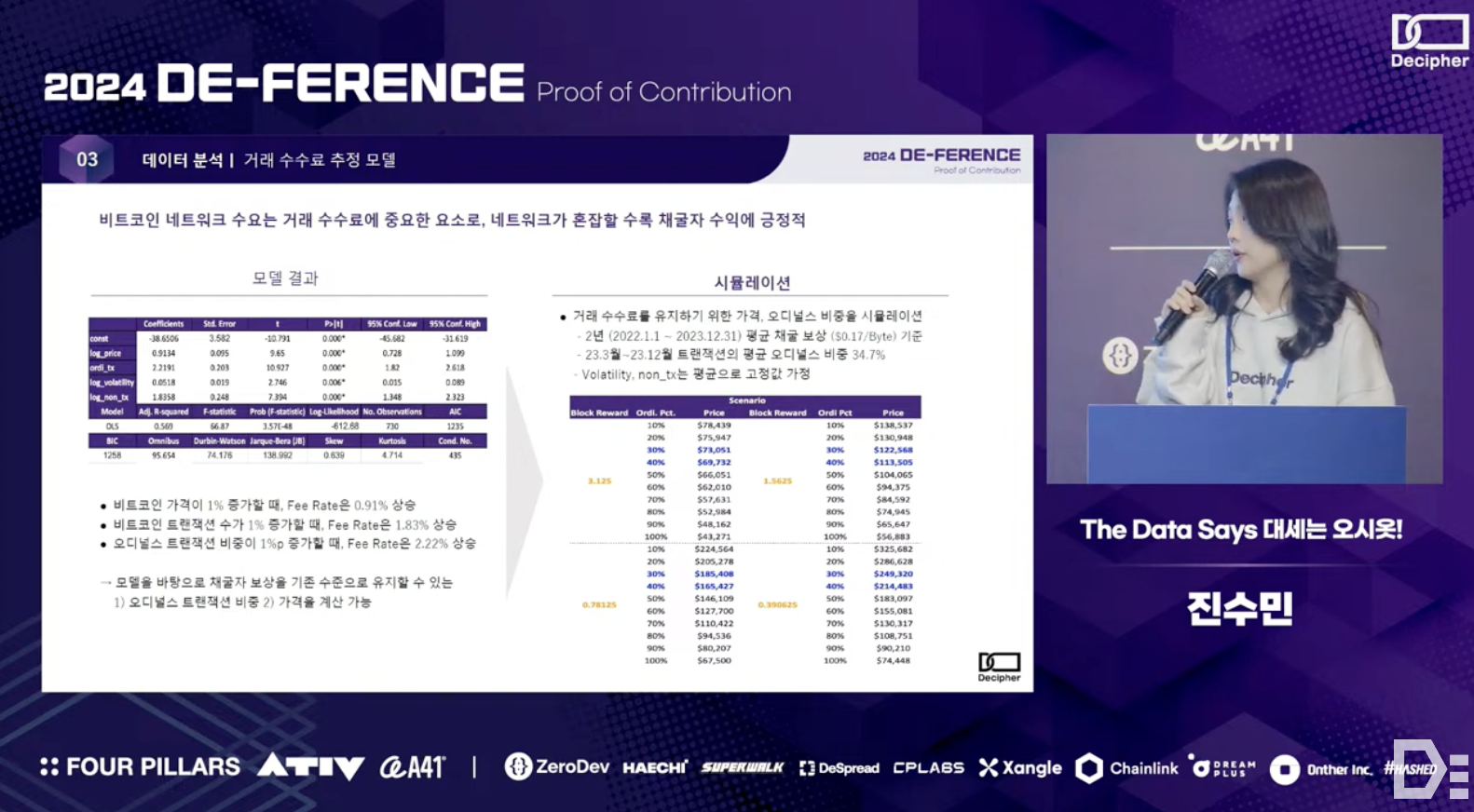

The analysis showed that when the price of Bitcoin increases by 1%, the fee rate rises by 0.91%. Additionally, when the proportion of Ordinals transactions increases by 1%p, the fee rate rises by 2.22%.

Using this model, the team simulated the proportion between Bitcoin's price and the fee of Ordinals transactions that would maintain a similar level of miner revenue as seen in the past two years, with an average mining reward of $0.17 per Byte. As summarized in the table on the right, the team found that a higher proportion of Ordinals transactions generates more transaction fees, allowing miners to sustain their revenue even if Bitcoin's price is not high. In other words, the demand for Bitcoin transactions complements the price through the effect of rising transaction fees, thereby contributing to network maintenance.

In summary, this presentation discussed the current state of Bitcoin as a digital asset and its sustainability from the perspective of miners through data analysis. The demand for Bitcoin as an asset has been steadily increasing, and its scarcity is heightened by the halving events that reduce block rewards. However, in the long term, transaction fees may become even more crucial for network security and maintanence. As seen in cases like Ordinals, it is important for transaction demand to continue, ensuring active network usage. Simulation results indicate that to maintain or exceed current revenue levels, Bitcoin prices must significantly rise with each halving, or Bitcoin transaction volumes—and thus transaction fees—must increase due to growing transaction demand.

In the long term, a balance might be found in the price of Bitcoin that considers both users' demand and the reasonable transaction fees they are willing to pay, as well as the costs that miners can sustain. Additionally, it will be worth closely observing how the dynamics of the mining industry mature, particularly in terms of energy savings and efficiency improvements.

There were no questions regarding this presentation.

Overview

The final session of Part 2 was a panel discussion on the topic ‘Who is leading the way for mass adoption (Infra vs. Application)’. The panel featured leaders from companies driving mass adoption of blockchain in both application and infrastructure sectors: Taewan Kim, CEO of SuperWalk (A), Byeongheon Lee, Engineer at CPLabs (B), Seunghwa Lee, Research Lead at DeSpread (C), and Geonki Moon, CEO of Haechi Labs (D). The discussion was moderated by Bohyun Park, Operations Lead at Decipher (M).

Comments

The debate sparked by the numerous emerging infrastructure solutions—’Which comes first, infrastructure or applications?’—is a long-standing topic in the blockchain scene, akin to the ‘chicken or egg’ dilemma. Unlike in the past when this debate began, we now see a surge in consumer applications (especially after Friend.Tech), with many attempts being made on the application side as well. Therefore, as panelist Byungheon Lee mentioned in this panel discussion, it would be more productive to focus not on the ‘Infra vs. Application’ dichotomy but on improving various elements together to discuss mass adoption effectively.

Separately, this panel discussion was very meaningful as it provided a platform for panelists who have long been active in the industry as infrastructure builders, application developers, and researchers to discuss the practical challenges of achieving mass adoption. While many aspects of the industry are still undefined, the standards within the industry have significantly improved over the past decade. It is hoped that the voices of these industry professionals will be effectively communicated within the industry and to the public, accelerating the adoption of blockchain.

Discussions

M. Many people agree that, in a broader context, the mass adoption of blockchain is related to the idea that everyone, regardless of age or gender, should be able to easily use blockchain services. What are the current difficulties that the general public faces when using blockchain?

B. First of all, I believe builders share some of the blame. Many services do not approach users with a "User-First" mindset, but rather take a high-handed stance of "You need to understand and use our service this way." Additionally, instead of integrating technologies with practical use cases, they try to approach from a systemic perspective that can change the entire paradigm. This results in many small but critical details being overlooked, making the entry barrier high for users. Finally, the onboarding process, such as on-ramps, is essential for using many services, but the process of going from CEX to on-chain services is too complicated.

C. Of course, accessibility and regulatory aspects are important factors, but I believe that blockchain technology has inherent limitations from its origin. Blockchain is fundamentally a financial technology, and financial technologies are inherently difficult for the general public to use. Additionally, characteristics of blockchain such as decentralization, transparency, and immutability are values that are not easily appealing to the public in an intuitive way. Therefore, the services created by blockchain technology are inevitably going to have a gap with existing services.

M. Those are definitely points that users can clearly feel. However, from a builder's perspective, creating products with mass adoption in mind seems challenging as well. What are some of the difficulties involved?

A. The Superwalk service has grown to achieve 200,000 MAU, primarily from domestic users, based on user feedback. Now, the goal is to expand this service globally. Currently, there are several challenges we face. Firstly, there are difficulties from a technical perspective. For instance, the service is currently operating on the Klaytn chain, but we need to provide multi-chain interoperability to enhance user accessibility. This presents a challenge because building blockchain services involves considering fragmented infrastructures, unlike Web2 service development, leading to technical concerns and hurdles for builders. Secondly, there are difficulties in business development. Implementing the custody or ownership experiences expected by Web3 users presents inevitable obstacles. It is challenging to address these issues for mainstream users, making it hard to achieve network effects and economies of scale. Lastly, there are regulatory issues. Due to some projects with malicious intent, there is a negative perception of the entire crypto industry. We expect that the industry will grow more rapidly if regulatory authorities provide clear guidelines.

D. I agree with B's earlier point that the lack of mass adoption is partly due to the builders' shortcomings. The fundamental reasons for this include, firstly, the market's speculative structure. Blockchain emerged as a financial technology accessible to everyone, but the current market is driven by repeated speculative activities creating liquidity. Builders focus more on generating hype rather than considering the value or problem-solving potential that coins and tokens offer to users. As a result, builders who genuinely try to solve user problems struggle to gain market attention. Secondly, despite the high accessibility of mobile applications, current app store policies present significant barriers to blockchain services that incorporate tokens. Therefore, most services are operated on the web. Lastly, we need to rethink the definition of mass adoption itself. Does mass adoption mean that blockchain must become a universally used technology like mobile or the internet? Considering that blockchain is a financial technology with inherently high entry barriers, and that a significant amount of liquidity already flows in crypto, which is about 2% of the global stock market, it can be argued that blockchain has already been adopted in many areas.

B. Firstly, the infrastructure for development is still immature - for example, nodes that have opened RPC endpoints often fail when there is a slight increase in requests. Therefore, rather than seeing many chains emerging rapidly, I would prefer to see a few but well-established infrastructures. Secondly, there are challenges due to the need to use various modules for development, as the interoperability between these modules is not well established.

M. What do you think mass adoption will look like in the future?

A. Having operated the service for just over two years, I have realized that the business that can best utilize this technology is one that designs rewards well to sustainably operate the platform. Therefore, I hope for a future where crypto assets are not seen as speculative tools but are effectively used as appropriate rewards for sustainable platform operation.

B. I believe that in the future, human life will become entirely digital. In such a world, the only way to own and transfer assets in a trustless manner is through blockchain. Therefore, as many aspects of our lives become digitized, I think blockchain technology will naturally become an integral part of that world.

C. Blockchain is a financial technology and a representative technology of decentralization at the same time. Therefore, in a world where blockchain technology is refined and its characteristics are maximized, financial activities using blockchain will likely integrate with many services we encounter in our daily lives. Just like the Farcaster application, which is currently booming, various use cases will emerge through utility assets representing services. Another powerful feature of blockchain from the supply side is the ability to design incentive structures in a decentralized manner. Hence, rather than companies launching products in a top-down manner, we will likely see more individuals completing applications and services in a bottom-up approach.

D. The most remarkable aspect of crypto is that it allows people to handle money freely - blockchain enables the infinite division of value and the ability to transfer it across borders. As people spend more time in digital worlds, similar to the scenario in the movie Ready Player One, blockchain will play a significant role as the infrastructure that allows the free use of money. For this to happen, it is essential for blockchain to integrate with real-world finance, and exchanges must effectively serve as gateways for on/off ramps.

Q. I would like to hear the panelists' opinions on whether the lack of infrastructure or the lack of applications is the main obstacle to effectively onboarding the general public.

A. From a user perspective, when considering the use of blockchain services, there are many obstacles in terms of UX and regulations in fully leveraging blockchain technologies. Despite many efforts to address these issues, there still seems to be a lack of advanced infrastructure technologies that support each service in focusing on its core value. In other words, the infrastructure sector needs further development.

B. Additionally, I think the title of the panel discussion is somewhat inappropriate. Infrastructure and applications are inseparable. A more appropriate comparison with such technologies might be with content. For mass adoption, the service must either provide exceptional value or convince the public of its necessity or legitimacy. From this perspective, I believe that the advancement of blockchain technology and the supply of high-quality content should occur simultaneously.

D. If we define all areas other than those for creating services as infrastructure, it seems that the development of infrastructure will be more important for mass adoption in the long term. However, improving infrastructure involves numerous and complex factors, including technical elements and regulations. Therefore, for the time being, I believe that only users who can navigate these complexities and appreciate the value of blockchain will adopt the technology.

Q. There are so many unused infrastructures. On the other hand, this could mean that people are already making full use of the available infrastructures. What do the panelists think about this?

D. As mentioned earlier, I believe that the main reason for the emergence of numerous L1 and L2 solutions is ultimately driven by the speculative desires of many participants. Therefore, I don't see a significant lack of infrastructure needed to create Web3 applications at the moment (though, of course, there is always room for improvement).

A. On a positive note, the bar for projects to get funded has been raised a lot compared to five years ago, which means that even the projects that are getting a lot of hype have a problem they are trying to solve, and the level of detail is increasing. Therefore, I believe that once a significant success story emerges from among these projects with well-resolved issues, public participation will greatly increase.

D. I agree with A's point. It's true that there are researchers and investors who contemplate the essence of blockchain technology, which is gradually raising the industry's standards. Therefore, it might be necessary to have figures like Steve Jobs who can create products with polished UX, rather than focusing solely on the maturity of the technology.

C. Blockchain's ability to allow individuals to create something quickly and freely according to their desired vision has led to the emergence of numerous solutions. In the evolution of every technology, there naturally comes a process of divergence and convergence. In this regard, I believe that as the industry gradually advances, there will come a time when a significant influx of new users occurs within the blockchain technology sphere.

※ This article series covers the DeFerence 2024 event, sponsored by Four Pillars. This article is the second part of the series. You can check the article for the first part in this link and the next part will be published soon - the topic of the next part is ‘Talk about the Present and Future of Blockchain Infrastructure.’

Dive into 'Narratives' that will be important in the next year