With the passage of the GENIUS Act, stablecoins can now be regarded as a form of money equivalent to M1 payment instruments such as cash and demand deposits. Frax Finance implements M1-level financial infrastructure onchain, centered around the GENIUS Act–compliant stablecoin frxUSD.

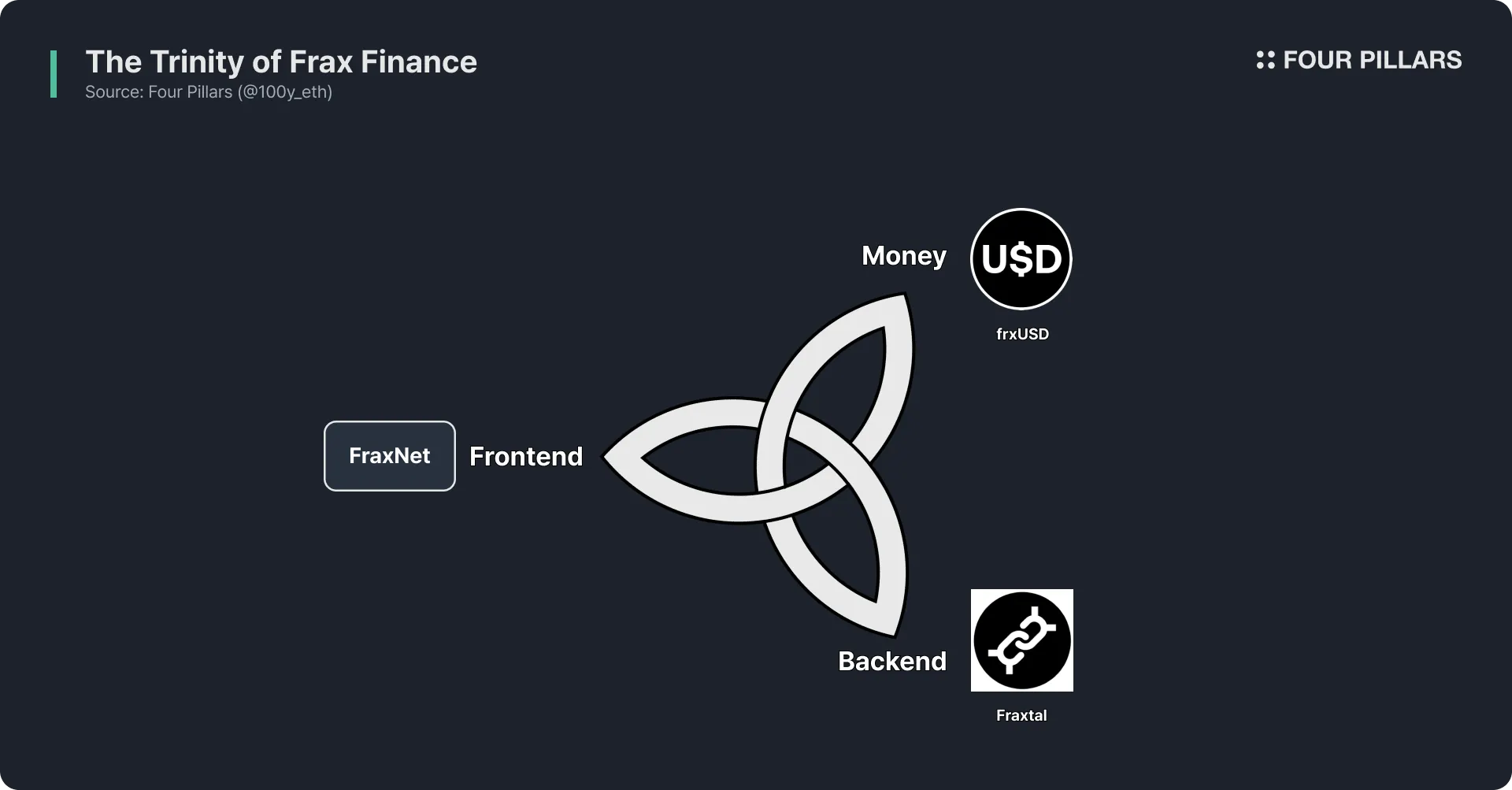

Just as traditional finance consists of money, frontends, and backends, Frax Finance builds the same three components of a financial system onchain through frxUSD, FraxNet, and Fraxtal. On this basis, it presents the vision of a Stablecoin Operating System that integrates the entire lifecycle of stablecoin distribution.

Frax Finance was the first to propose a vertically integrated model centered on stablecoins. Its own DeFi protocols (such as Fraxswap and Frax Ether) and multi-layered asset suite (including sfrxUSD and frxBTC) are designed to internalize long-term revenue streams and adapt flexibly to regulatory changes.

Stablecoin adoption will expand progressively in three stages: 1) crypto trading, 2) onchain capital markets, and 3) international remittances and payments. Frax Finance has already built the financial infrastructure to support each stage and continues to refine it.

Source: FOX

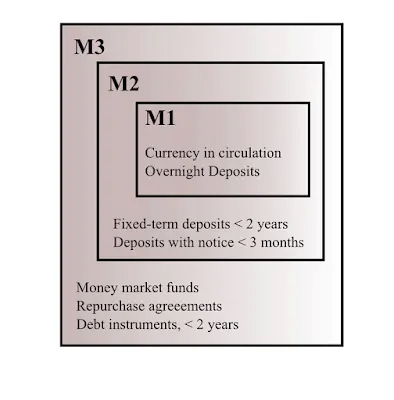

M1 represents the most liquid money supply that can be spent immediately in an economy. With the recent enactment of the GENIUS Act, stablecoins that meet specific criteria have gained a legal foundation to be recognized as payment instruments on par with cash and demand deposits.

Three provisions in particular define the conditions under which stablecoins can be included in the M1 category:

Full collateralization and immediate redemption: Issued stablecoins must always be backed 1:1 by ultra-low-risk assets such as U.S. dollar cash, short-term U.S. Treasuries, or reverse repos, and must be redeemable for the same amount of cash at any time.

→ This gives stablecoins the same legal character as cash and demand deposits, which are immediately exchangeable for fixed-value assets.

Bank-level supervision: Issuers must be officially licensed and continuously supervised by federal (OCC or Federal Reserve) or state regulators, with regular audits.

→ This ensures that stablecoins can achieve the same level of trust as public payment instruments issued by regulated financial institutions.

Priority claims for holders: If an issuing institution goes bankrupt, stablecoin holders are guaranteed priority claims on reserves ahead of other creditors.

→ This protection, similar to that granted to bank depositors, provides the basis for treating stablecoins as risk-free payment assets.

This regulatory framework allows stablecoins to be viewed not merely as an alternative form of digital money but as payment instruments comparable to the M1 monetary base. What does this shift imply?

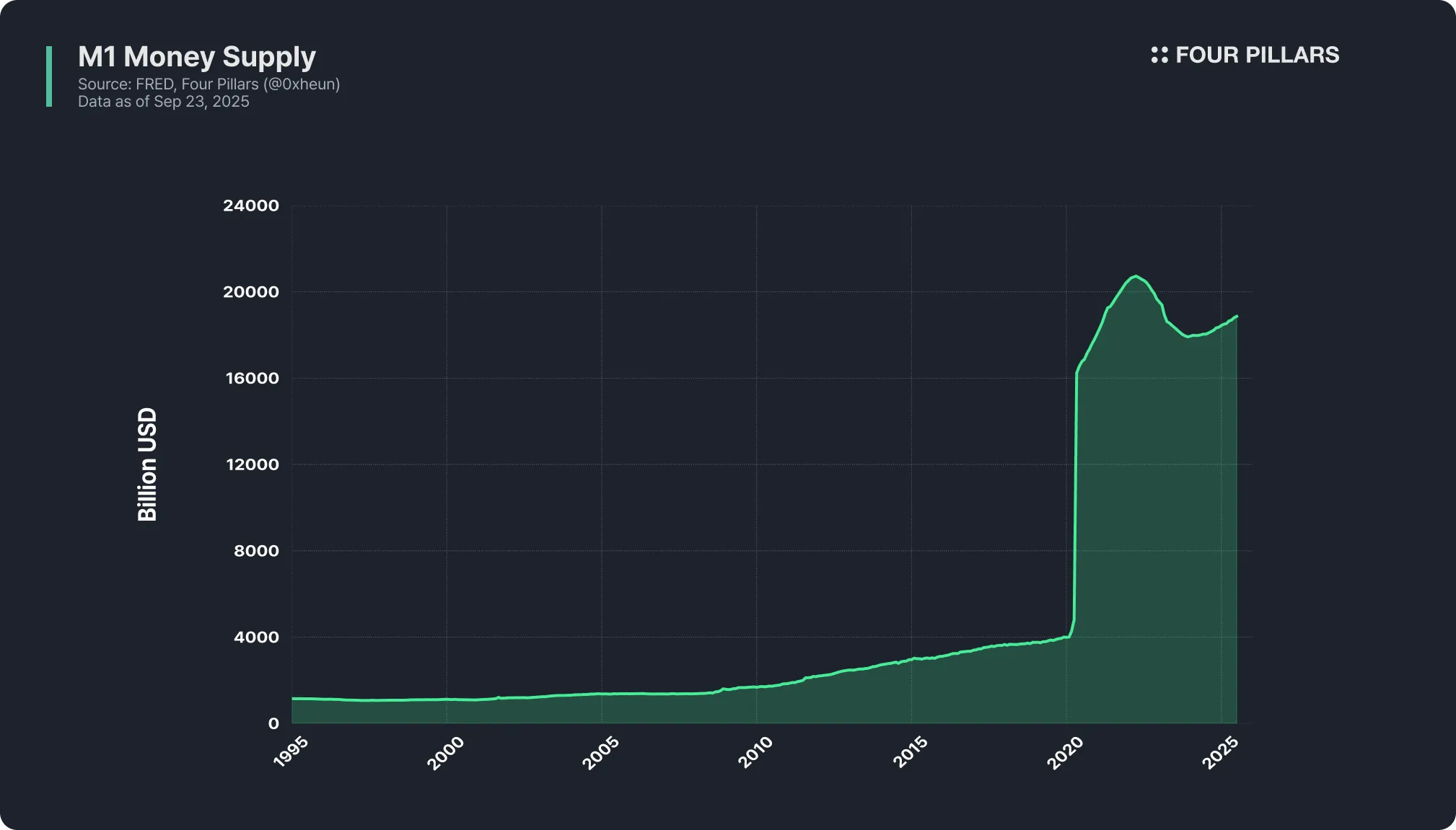

The U.S. M1 money supply is about $19T. It includes currency in circulation, checking deposits, and savings deposits, all regarded as core spendable assets in the U.S. financial system. For the first time in history, stablecoins are positioned to digitize and absorb this 19-trillion-dollar monetary layer. Moreover, by allowing banks, fintechs and DeFi to share the same settlement unit (stablecoins), this development lays the groundwork for a structural transformation of global payment and settlement infrastructure.

Source: Bond Economics

How can the M1 status of stablecoins accelerate a transformation in financial infrastructure? While M1 is typically defined as the sum of assets that can be spent immediately, its meaning goes beyond simply measuring the total quantity of money.

Traditional components of M1 include currency in circulation and checking or demand deposits. For the funds in checking accounts to be considered truly spendable, they must be instantly transferable through banking settlement rails such as the Automated Clearing House (ACH), Fedwire, or card networks like Visa and Mastercard. In other words, M1 implies not just the sum of banknotes and deposit balances but also the deposit systems, payment rails, and real-time settlement networks that support the storage and movement of money.

From this perspective, granting stablecoins a status equivalent to M1 and enabling banks, fintechs, and DeFi to share the same settlement unit signals more than a change in the monetary hierarchy. It also points to the possibility that the financial infrastructure on which those institutions rely could be re-architected onchain. This marks a turning point where decades of inefficiency and complexity in financial infrastructure can be streamlined around stablecoins.

What inefficiencies remain in financial infrastructure, and how can stablecoins address them? Several key domains stand out:

First, payment infrastructure. Although card payments are approved in real time, actual settlement takes one to two days for payment processing and up to five days for final settlement. Cross-border transactions routed through SWIFT face additional delays and fees. By using stablecoins, transaction approval and fund transfer are finalized in a single onchain transaction. Except for unavoidable delays due to disputes or abnormal transactions, much of the multi-layered process involving intermediary banks and acquirers can be eliminated.

Second, international remittances. The existing SWIFT network is merely a messaging system; actual fund transfers are handled separately through correspondent banks. Currency conversion, KYC/AML checks, and time zone differences add significant cost and delay. Stablecoin transfers handle both messaging and fund movement on a single onchain platform, enabling faster and more cost-efficient global remittances.

Finally, securities settlement. The infrastructure for securities trading still relies on centralized clearing structures and indirect custody systems designed in the 1960s and 1970s. For now this applies mainly to U.S. short-term bond funds, but yield-bearing stablecoins directly represent tokenized money market fund shares, allowing holders to stream interest income in real time without going through a separate clearing process. Stablecoins can therefore function not only as stores of value and payment instruments but also as base money transmitting the risk-free rate directly.

In payments, remittances, and securities settlement, the essence is the same: the immediacy of onchain settlement and the reduction of intermediary costs cut across the financial stack to drive efficiency. Recognizing this potential, stablecoin issuers are racing to capture market share at the very start of the transition to onchain financial rails.

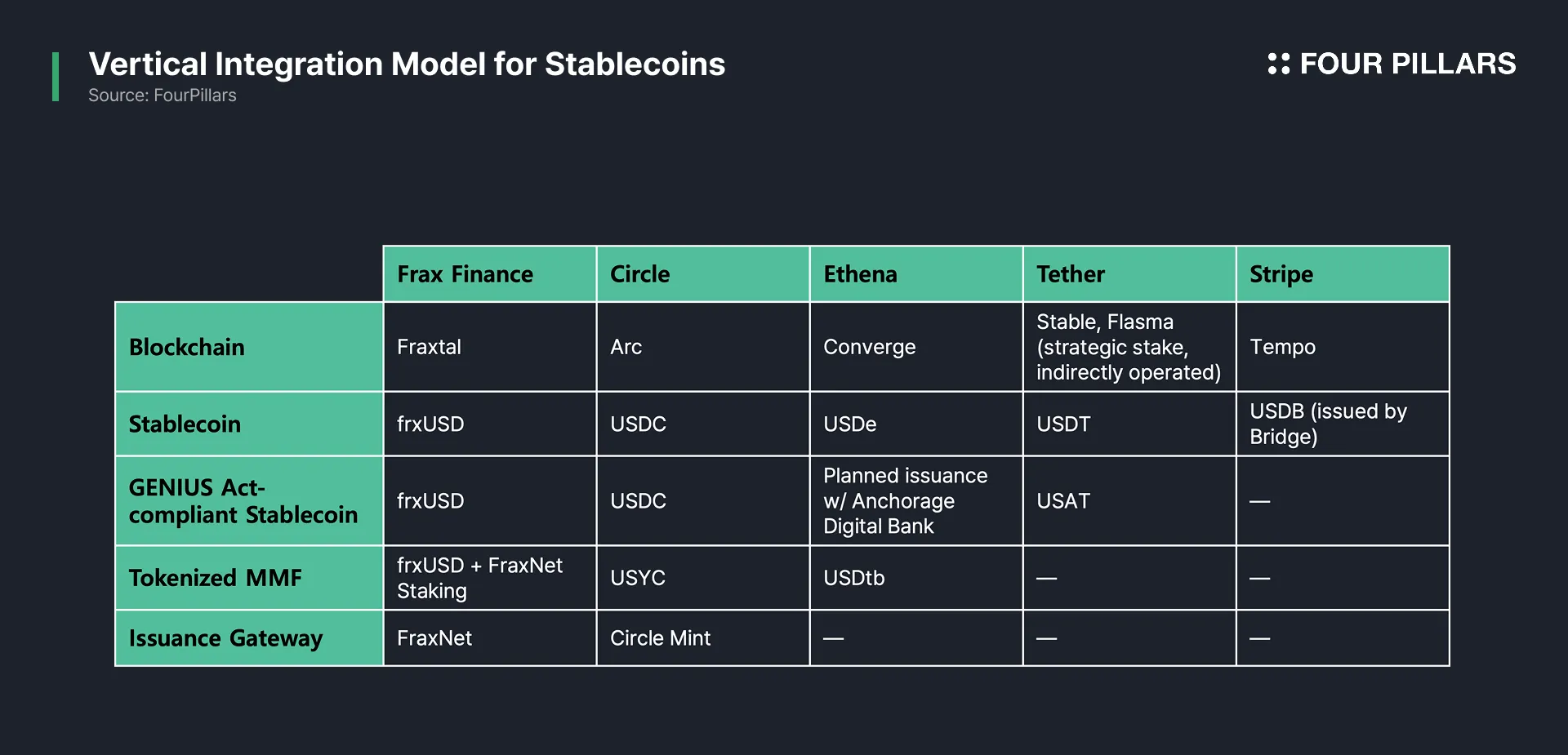

Stablecoin companies are commonly adopting a vertically integrated model that spans the entire financial infrastructure around stablecoins. Unlike the historical evolution of onchain-native finance, which developed by combining various DeFi protocols and blockchain infrastructure in a modular way, the stablecoin infrastructure clearly illustrates a vertical integration model that internalizes the core layers of the financial stack.

This approach reflects not only the advantage of internalizing revenue streams but also two key industry characteristics. First, the vertical integration model allows for rapid adaptation to regulatory changes and minimizes compliance gaps or operational risks. Second, because the target audience includes global retail users who have little or no experience with onchain services, it is essential to provide everything from wallet creation, on/off-ramps, and payments to interest distribution on a single platform to enhance convenience and trust.

To achieve this, companies are building a blueprint that integrates the entire financial infrastructure value chain: stablecoin issuance, proprietary blockchains to support issuance and distribution, regulatory-compliant stablecoins, tokenized money market fund–backed stablecoins, and minting and redemption gateways for enterprises and institutions.

While companies aiming for vertical integration share a similar blueprint, their implementations vary slightly depending on their strengths and target markets. The following three examples demonstrate this well:

Circle:

Circle exemplifies a classic vertical integration strategy by building all assets and services in-house to minimize regulatory and operational risk and to internalize long-term revenue streams. Based on USDC, it has already established bank-level reserve management and regular audit systems, and built its own bridge (CCTP) and multi-chain transfer infrastructure. Circle also provides a payment network linked to card and bank transfers through the Circle Payment Network (CPN), and recently introduced Arc, its own Layer 1 blockchain.

Ethena:

Ethena’s strategy highlights an initial focus on crypto-native markets. Through collaboration with onchain money markets such as Aavethena and integrations with major exchanges like Binance and Bybit, Ethena has rapidly expanded USDe issuance and distribution channels. In addition, the introduction of the institutional MMF-backed stablecoin USDtb, plans to comply with the GENIUS Act, and the announcement of its own chain, Converge, show a gradual move to cover institutional channels while building its own infrastructure.

Stripe:

Stripe began as a payment service provider (PSP) and is now moving to become a stablecoin-native payment network by launching the Tempo chain and acquiring the stablecoin infrastructure company Bridge. This shift can be viewed as an evolution beyond the role of a payment processor to encompass the functions of card networks, acquirers, and issuers. For example, Stripe partnered with Shopify and Coinbase to introduce USDC for online payments. Leveraging its extensive legacy network of enterprise clients, Stripe aims to support stablecoin payments through a vertically integrated payment infrastructure.

This vertical integration model internalizes every step of stablecoin issuance and distribution, providing 1) a long-term structure for internalized revenue, 2) a consistent user experience, and 3) minimized regulatory and operational risk. For stablecoin companies that have already achieved scale and infrastructure maturity, this strategy is solidifying as a clear path to long-term competitive advantage.

Within this trend of vertical integration emerging as a long-term growth strategy, one player envisioned the model early: Frax Finance, which introduced the concept of a “Stablecoin Operating System.”

In February 2024, Frax Finance launched Fraxtal, a blockchain built for the frxUSD stablecoin. Compared to the more recent announcements from Circle and Stripe about building their own blockchains, Frax Finance demonstrated the direction of a vertical integration model at a much earlier stage. When the GENIUS Act was announced, Frax Finance also swiftly converted frxUSD into a GENIUS Act–compliant stablecoin at nearly the same time as Circle’s USDC, proving its ability to respond quickly to regulatory developments.

Frax Finance has consistently adapted to market changes and set the course for the stablecoin industry. From the DeFi Summer period, when stablecoin issuance surged alongside the Curve Wars, to the post-Terra/UST collapse era when the industry shifted from algorithmic stablecoins to fully collateralized models, and now to the passage of the GENIUS Act that recognizes stablecoins as equivalent to M1 payment instruments, Frax Finance has been present at every critical juncture in the history of stablecoins.

Today, as stablecoins rise beyond the crypto market to become a global medium of payment, the timing has never been better. Frax Finance, which has been part of this trajectory from the beginning, is also at an inflection point. The following sections explore Frax Finance’s Stablecoin OS and its ecosystem as the protocol prepares for the next chapter.

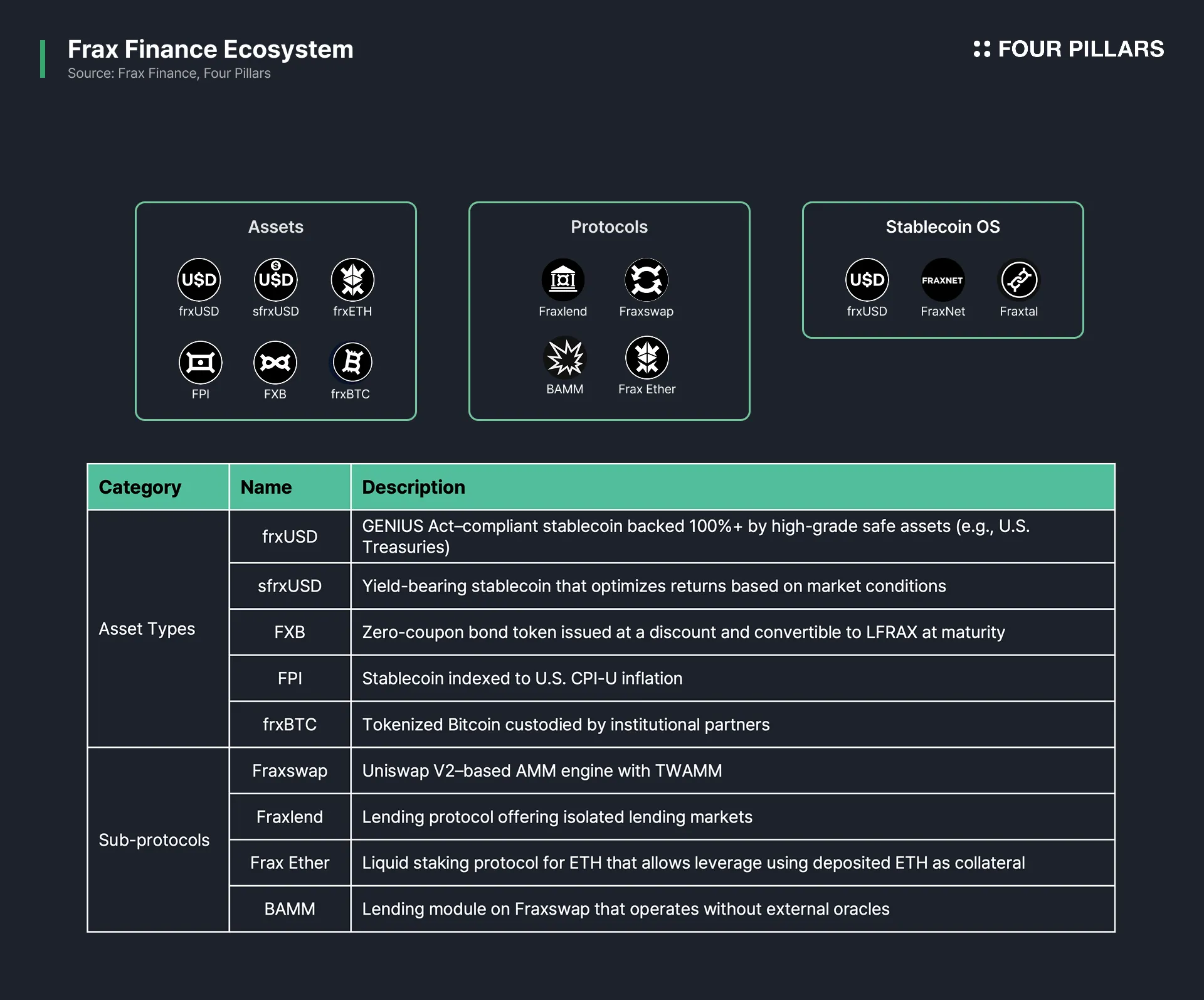

Frax Finance defines the components of its Stablecoin Operating System (OS) as three core pillars:

frxUSD: A regulatory-compliant stablecoin designed to meet the requirements of the GENIUS Act and the core liquidity asset of the Frax ecosystem.

FraxNet: A platform that allows users to mint and redeem frxUSD and earn stable yield from U.S. Treasury–backed reserves in a non-custodial manner while remaining fully compliant with the GENIUS Act.

Fraxtal: A high-performance EVM-based blockchain built for frxUSD, with FRAX serving as the native gas token.

This structure mirrors the modern financial system, which is composed of three key layers: money, the frontend, and the backend. In traditional finance, a foundational monetary asset, a convenient frontend provided by fintech companies, and a backend of payments, securities, and settlement infrastructure together form the essential environment for economic activity.

Frax Finance applies the same framework to onchain finance. In a blockchain-based financial system, the three essential components are the stablecoin, the frontend, and the blockchain network as the backend. Frax implements these through frxUSD, FraxNet, and Fraxtal, creating the blueprint for its Stablecoin OS. The following sections examine these three components in detail.

2.1.1 Overview of frxUSD

frxUSD serves as the monetary layer of the Stablecoin OS.

frxUSD is a digital dollar circulating across more than 20 blockchain networks. It is backed with over 100 percent collateral composed of tokenized U.S. Treasury funds managed by global financial institutions such as BlackRock, Superstate, and WisdomTree, all of which use bankruptcy-remote structures.

Bankruptcy-remote means the underlying assets are legally separated so that even if the issuer goes bankrupt, the collateral cannot be seized by creditors or included in bankruptcy proceedings. This structure ensures that holders of frxUSD maintain a secure claim to the collateral regardless of the financial status of the issuer.

Because of this institutional-grade custodial framework, frxUSD can be minted or redeemed 1:1 at partner institutions. It can be issued using not only stablecoins like USDC, USDT, PYUSD, and USDB but also bank wire transfers and even RWA tokens such as USTB and WTGXX.

Source: Frax Finance

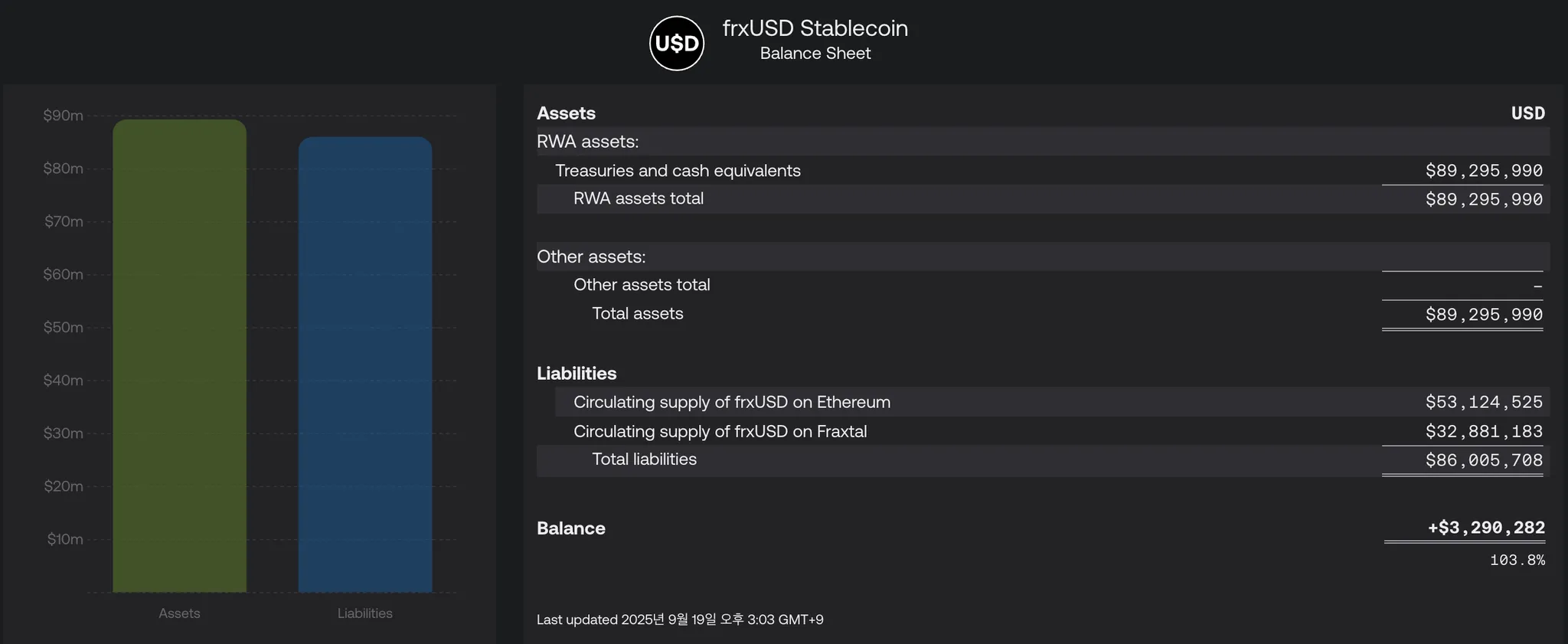

The frxUSD balance sheet shows that its assets consist entirely of real-world assets such as U.S. Treasuries and cash equivalents. With total assets of around $89 million and net assets of roughly $3 million, frxUSD is overcollateralized at about 104 percent. By holding more high-quality collateral than the total supply and publishing transparent reserve data, frxUSD offers both stability and a high level of trust.

2.1.2 GENIUS Act Compliance

One of frxUSD’s most notable features is that it is among the few stablecoins that fully comply with the GENIUS Act. Considering that Circle’s USDC achieved compliance at a similar pace and Tether has only recently announced plans for a regulated stablecoin (USAT), Frax’s rapid response underscores its strong regulatory readiness.

There is a reason for this speed. In March, Frax Finance founder Sam Kazemian met with Senator Cynthia Lummis, co-sponsor of the GENIUS Act, and provided input during the bill’s drafting stage. His direct involvement helped shape the legal framework for the digital dollar, enabling Frax Finance to design frxUSD precisely in line with the law.

Specifically, frxUSD meets the GENIUS Act requirements in the following areas:

Issuance Qualification: Only authorized U.S. issuers may mint stablecoins. These include subsidiaries of banks or credit unions, OCC-approved institutions, or entities approved by state financial regulators.

→ Through the FIP-432 governance proposal, all responsibilities for issuing frxUSD, managing reserves, and ensuring regulatory compliance were transferred to FRAX Inc. Registered in Delaware, FRAX Inc. must obtain approval from either the OCC or a state financial regulator to issue a GENIUS Act–compliant stablecoin and is currently preparing to acquire the necessary license.

Reserve Requirements: The GENIUS Act requires full 1:1 backing with highly liquid assets.

→ frxUSD reserves are entirely composed of tokenized U.S. Treasury funds and similar instruments, including USTB, BUIDL, WTGXX, USDB, and USDC. With more than 100 percent collateralization, these reserves satisfy the law’s requirements.

Interest Payment Restrictions: The GENIUS Act prohibits paying interest to stablecoin holders simply for holding the tokens, in order to avoid treating them like bank deposits or investment products.

→ frxUSD holders can earn yield only when they hold their tokens within FraxNet. In this case, the rewards come from FraxNet, which is operated by Frax Network Labs Inc., a legal entity separate from the issuer. Because the issuer is not paying interest directly, this structure remains fully compliant.

frxUSD also meets other requirements of the GENIUS Act. For a deeper analysis, see “From CRCL to FRAX: The Next GENIUS Act Play”.

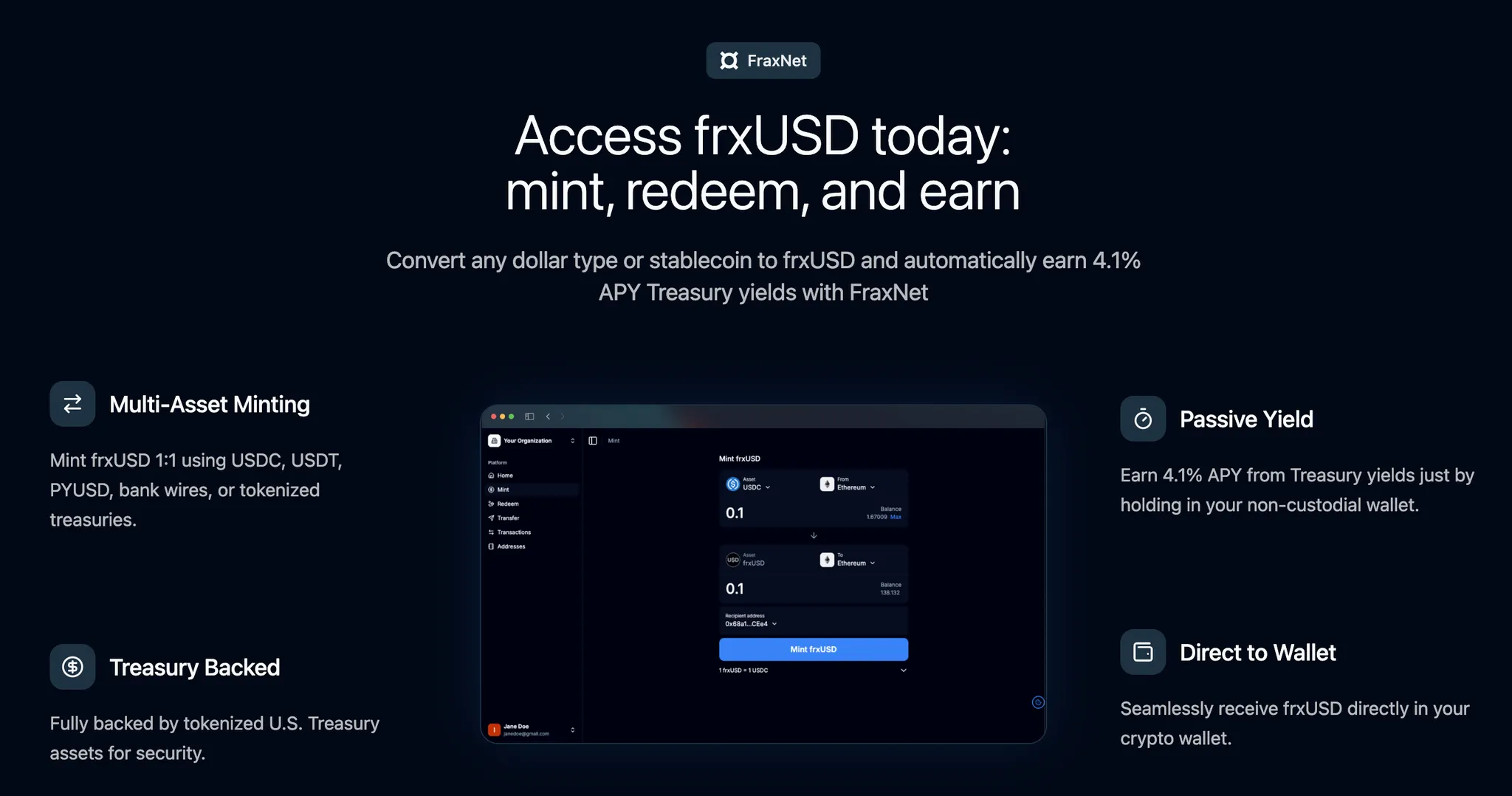

2.2.1 Overview of FraxNet

Source: Frax Finance

FraxNet serves as the frontend of the Stablecoin OS.

FraxNet is the account layer for frxUSD, enabling individuals and institutions to convert bank deposits or money market fund shares into frxUSD and earn real-time yield from U.S. Treasuries. As noted earlier, FraxNet distributes bond yields while remaining fully compliant with the GENIUS Act. This makes Frax the first stablecoin protocol to offer programmable yield distribution without violating regulatory requirements.

2.2.2 Key Features of FraxNet

FraxNet provides the following key capabilities:

Multi-asset issuance: Mint frxUSD using not only stablecoins such as USDC and USDT but also bank wires and RWA tokens like USTB and WTGXX.

Embedded wallet: Log in with a Google account or similar, and a blockchain wallet is automatically created.

Dashboard: View and transfer a wide range of assets across multiple networks through a unified dashboard.

Passive yield: Hold frxUSD on FraxNet to automatically earn stable interest from U.S. Treasuries.

Virtual Visa card: In partnership with Stripe and Bridge, FraxNet plans to launch a virtual Visa card linked to the Visa network, enabling real-world payments directly from FraxNet assets.

Virtual bank accounts: Working with Lead Bank, Frax Finance will offer virtual bank accounts that allow deposits and withdrawals through the traditional banking system, seamlessly connecting DeFi with traditional finance.

FraxNet Mobile: A mobile app planned for 2026 to provide a full mobile banking experience.

Cross-chain interoperability: By using cross-chain messaging standards such as CCTP and LayerZero, FraxNet supports secure transfers of canonical tokens across chains without relying on centralized bridges or wrapped assets.

Fraxtal serves as the backend of the Stablecoin OS.

No matter how user-friendly the frontend may be, if the backend where money actually moves is inefficient, the overall user experience suffers. Fraxtal is designed to deliver high throughput and low fees to support large-scale financial activity and real-time yield distribution. Its goal is to set the standard for blockchain-based financial backends, with frxUSD as the core monetary asset.

Fraxtal initially launched as an EVM-compatible rollup built on the OP Stack, offering the speed and security of networks like Optimism and Base. To meet the demands of global-scale real-time interest distribution, Fraxtal is now transitioning from an Ethereum Layer 2 to a sovereign Layer 1.

This transition is expected to deliver:

Sub-second scalability: Finality in under one second to support real-time interest distribution.

Value capture: Economic value from network growth accrues directly to the stablecoin issuance protocol.

Product customization: Onchain rails optimized for stablecoin-specific requirements such as privacy and regulatory compliance.

FRAX economic alignment: Unlike Circle, which burns USDC gas fees, Fraxtal burns FRAX gas fees, aligning network growth with the Frax Finance economy.

The primary motivation for this move is to handle the massive throughput required for real-time interest distribution. To stream U.S. Treasury yields to frxUSD holders on FraxNet, the network must process millions of microtransactions simultaneously. In the past year alone, more than 300 million addresses globally have transacted USDT or USDC. If even a fraction of these addresses were to receive real-time yield via FraxNet, the required capacity would far exceed that of existing Ethereum Layer 2 networks.

Fraxtal is being built to meet this demand, targeting over 100,000 TPS, real-time block production, and ultra-low fees to enable seamless programmable yield distribution. Frax Finance’s North Star roadmap in governance proposal FIP-428 outlines plans to designate FRAX as the Layer 1 gas token and introduce its own validator set, ensuring the infrastructure can scale to meet the requirements of a global onchain financial system.

Stablecoin issuance alone is no longer a defensible moat. With over 60 stablecoins already in existence, neither peg stability nor U.S. Treasury–level yields are enough to secure a lasting competitive advantage. The challenge for stablecoins has long since shifted from “how to issue” to “how to distribute and drive usage.” Frax Finance distinguishes itself by having spent years building and internalizing a broad range of DeFi protocols, enabling multi-layered utility for its stablecoins.

At the core of these operations are AMO (Algorithmic Market Operations) contracts, which automatically execute pre-programmed monetary policy. Once approved by onchain governance, these contracts can automatically rebalance liquidity or stabilize the peg without manually changing the underlying subprotocol contracts. AMOs provide the flexibility to add or adjust mechanisms entirely through automated operations.

Key examples include:

Fraxlend AMO: Supplies newly minted frxUSD to governance-approved lending market pairs and collects interest from borrowers.

Fraxswap TWAMM AMO: Uses Fraxswap’s time-weighted average market maker (TWAMM) to execute large orders over time. This module gradually acquires collateral to adjust frxUSD’s balance sheet and collateral mix. It can also dispose of collateral or use protocol revenue to buy and burn FRAX, reducing supply when needed.

FXB AMO: Manages the issuance and discounted auction of FXB bonds.

In addition, the North Star roadmap represents a structural transition for the ecosystem. Fraxtal is evolving from an EVM-compatible Layer 2 to a Layer 1 chain, the native token has rebranded from FXS to FRAX, and the stablecoin from FRAX to frxUSD. Beyond a name change, this shift strengthens frxUSD’s regulatory standing under the GENIUS Act and positions FRAX to capture revenue from subprotocols and gas fees, aligning ecosystem growth directly with the Frax economy.

The following sections present a detailed view of Frax Finance’s core assets and subprotocols.

3.1.1 FRAX: Native Token

FRAX is the native token of the Frax Finance ecosystem. It was originally utilized in the pegging algorithm of the legacy Frax Dollar (LFRAX), the earlier version of frxUSD. As the collateral backing frxUSD has transitioned to cash-equivalent assets such as U.S. Treasuries to ensure greater peg stability, FRAX has taken on a new role. Following the upcoming North Star hard fork, FRAX will serve as the gas token for Fraxtal and further expand its function into network security economics by operating its own validator set to maintain consensus and secure the network.

Users can stake FRAX for a period between one week and 208 weeks (up to four years). Staked FRAX is locked as veFRAX, a non-transferable token that grants governance rights across the Frax ecosystem.

veFRAX holders receive a share of ecosystem revenues, including Fraxtal gas and bridge fees, frxUSD yields, and income from various subprotocols. Rewards are distributed based on the amount and duration of the stake. Liquidity providers on Fraxtal-based DeFi protocols can also earn boosted rewards, creating deep economic alignment between veFRAX and the broader Frax ecosystem.

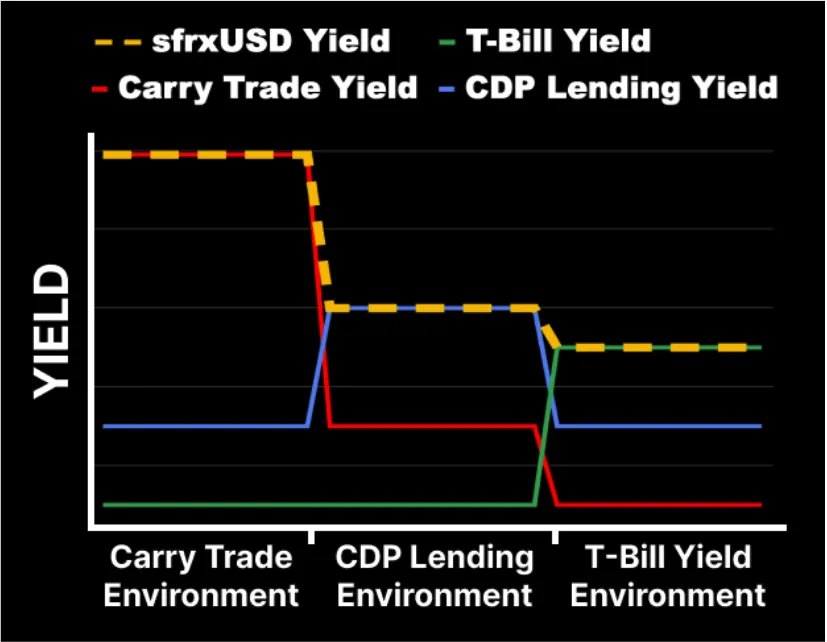

3.1.2 sfrxUSD: Yield-Bearing Stablecoin with Dynamic Benchmark Strategy

sfrxUSD (Staked Frax USD) provides yield through a Benchmark Yield Strategy (BYS) that automatically allocates capital to the highest-yielding venue. It can be redeemed for the underlying frxUSD at any time, with the redemption rate increasing as yield accrues.

Carry trade: Deploy frxUSD to higher-yield opportunities to capture interest rate differentials.

DeFi strategies: Supply liquidity or engage in lending and derivatives on DeFi protocols such as Curve to generate yield.

RWA strategies: Allocate to real-world assets such as short-term U.S. Treasuries to capture stable yields.

Source: Frax Finance

BYS automatically reallocates frxUSD staked in the yield vault to the most attractive yield source depending on market conditions. If carry-trade returns exceed DeFi yields, funds are allocated to carry-trade strategies. If DeFi yields outperform, capital moves to DeFi AMO strategies. If the T-Bill rate is highest, the vault allocates to RWA strategies with short-dated U.S. Treasury Bills. This ensures that sfrxUSD holders consistently earn one of the most competitive risk-adjusted yields onchain without needing to hold other yield-bearing stablecoins.

3.1.3 FXB: Zero-Coupon Bond Tokens

FXB (Frax Bonds) are zero-coupon bond-like tokens designed to stabilize the peg of the legacy Frax Dollar (LFRAX). FXBs are issued at a discount and redeemed at face value upon maturity, effectively providing a fixed yield while helping control LFRAX supply.

Source: Frax Finance

The FXB auction and redemption process works as follows:

The FXB AMO auctions FXBs at a price below par.

Participants bid in LFRAX to purchase the discounted FXBs.

The LFRAX raised through the auction is managed by the AMO to generate yield.

At maturity, FXBs can be redeemed for their full face value in LFRAX, allowing buyers to earn the discount as yield comparable to U.S. Treasury returns without taking on RWA risk.

Because the LFRAX used to purchase FXBs remains locked until maturity, FXB issuance helps reduce circulating supply and supports the LFRAX peg.

FXBs can be redeemed only for LFRAX and confer no claims on any other assets. They are not backed by or redeemable for U.S. Treasuries or other real-world assets. Their sole function is to convert trustlessly into LFRAX at the pre-programmed maturity timestamp set at minting.

3.1.4 FPI: Stablecoin Pegged to a Basket of U.S. Consumer Goods

FPI (Frax Price Index) is another Frax stablecoin, pegged to the U.S. CPI-U basket of consumer goods. It tracks the purchasing power of a representative consumer goods basket and maintains this peg through onchain stabilization mechanisms.

Source: BLS

FPI’s peg is based on the unadjusted 12-month CPI-U inflation rate. Its base price of $1 was set according to December 2021 CPI-U data. Each month, after the Bureau of Labor Statistics releases updated CPI figures, a Chainlink oracle records the data onchain. The CPI Tracker Oracle updates the FPI redemption price every 30 days to reflect inflation.

Traders can use FPI as a strategic asset. Buying FPI with volatile assets such as ETH is effectively a bet that U.S. CPI will rise faster than the value of ETH over time. Selling FPI for ETH reflects the opposite view, that ETH will outperform U.S. inflation.

3.1.5 frxBTC: Tokenized Bitcoin

Source: Frax Finance

The upcoming frxBTC (Frax Bitcoin) will be a secure, highly liquid tokenized bitcoin backed by the same institutional custodians that safeguard frxUSD. It will provide transparent and secure bitcoin exposure across all chains supported by Frax. Because bitcoin is a unique asset widely used in derivatives and as collateral, frxBTC will expand the utility of the Frax ecosystem and integrate with its other assets and subprotocols.

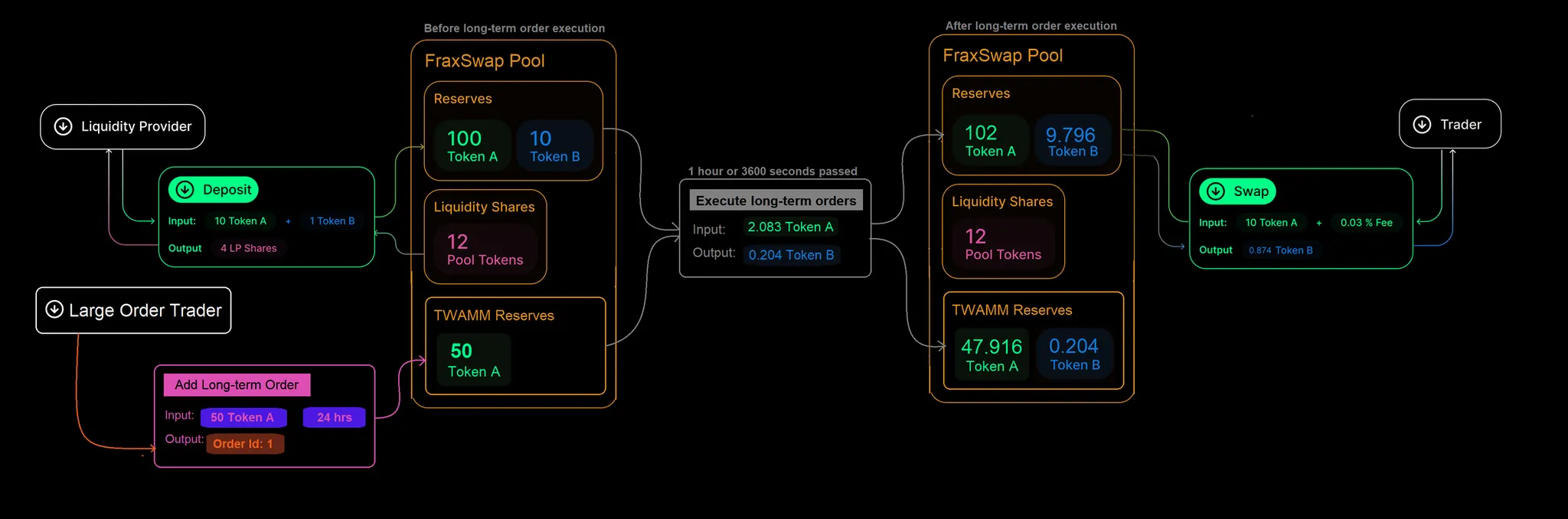

3.2.1 Fraxswap: TWAMM-Enabled Swap Engine

Fraxswap is a trading engine with an embedded TWAMM (Time-Weighted Average Market Maker). Built on Uniswap V2, it provides a constant product market-making mechanism (xy=k) and a permissionless environment where anyone can create a liquidity pool for any token pair. The TWAMM feature enables large orders to be automatically split into smaller trades and executed gradually, reducing price impact and slippage.

Source: Frax Finance

TWAMM executes large buy or sell orders over an extended period at a steady rate. For example, if a trader submits a long-term order to sell 100 ETH over 2,000 blocks, TWAMM breaks it into many small transactions for gradual execution.

Frax Finance built Fraxswap to automate monetary policy and liquidity management for assets such as frxUSD and FRAX. Through the Fraxswap AMO, the protocol can engage in market operations itself, enabling:

Supply adjustment: Use AMO profits to buy and burn FRAX, controlling token supply.

Peg stability: Strengthen the $1 peg of stablecoins such as frxUSD and FPI.

Progressive accumulation of real-world assets: Gradually sell frxUSD to acquire collateral without causing disruptive price moves.

Protocol-owned liquidity: Manage frxUSD/FRAX and other protocol-owned pools to provide ecosystem liquidity while generating revenue.

Frequent trading is essential for Frax Finance to maintain frxUSD peg stability and manage circulating supply. Using external protocols would result in value leakage through swap fees and Loss-Versus-Rebalancing (LVR). Fraxswap eliminates this by internalizing trading and executing transactions efficiently with TWAMM.

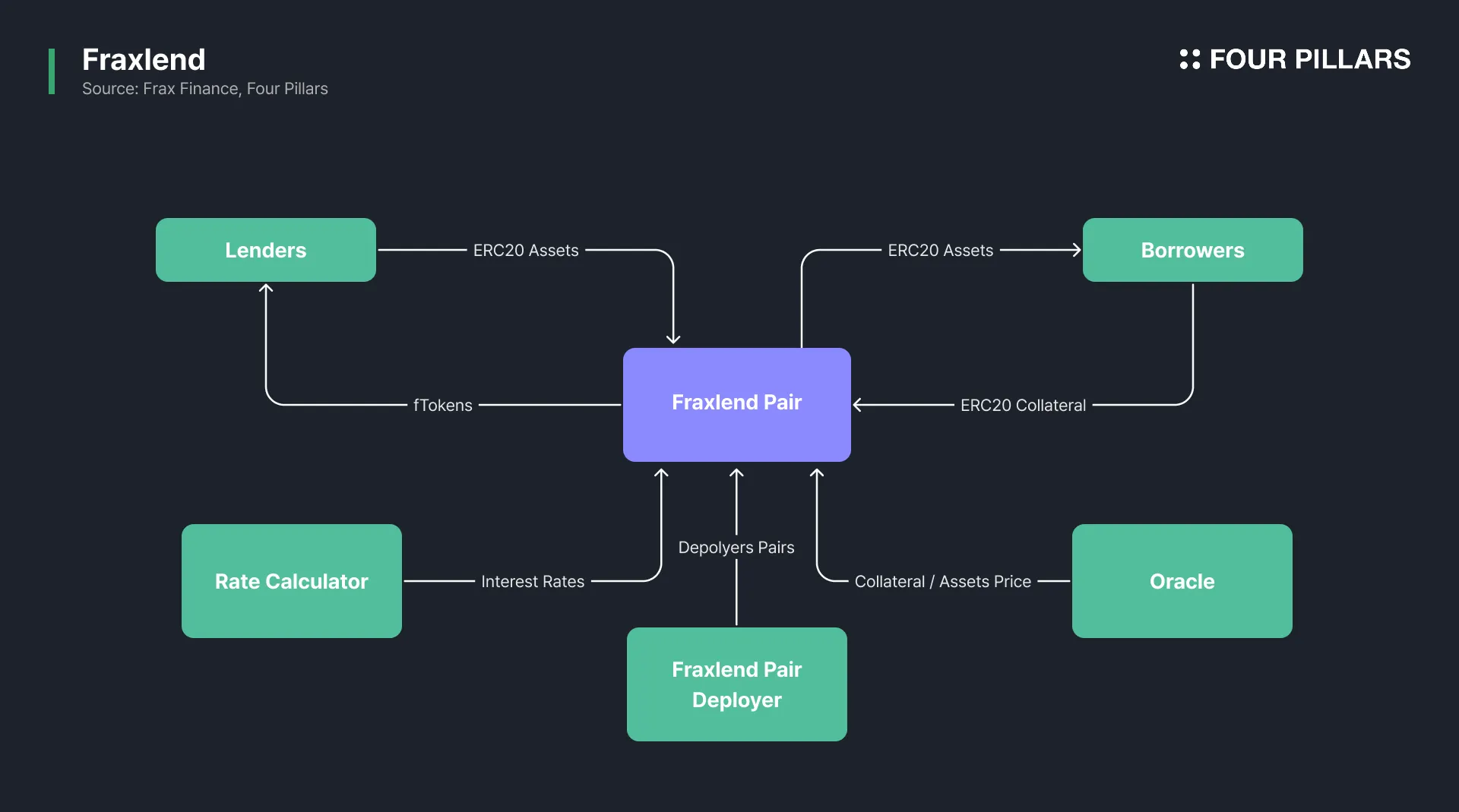

3.2.2 Fraxlend: Isolated Lending Markets

Fraxlend offers isolated lending markets, where each market consists of a pair of ERC-20 assets and its risk is contained within that pair. This structure prevents volatility in one market from spilling over into others. Users can deposit one ERC-20 token as collateral and borrow another, allowing permissionless participation in both lending and borrowing.

Source: Frax Finance

Key participants are lenders and borrowers:

Lenders deposit the lending asset into the pair and receive fTokens.

Borrowers deposit collateral tokens and borrow the asset token, paying interest, which accrues to lenders as fTokens appreciate in redeemable value.

Each pair relies on three components to function:

Oracles: Provide robust, manipulation-resistant price feeds for both collateral and asset tokens.

Rate Calculator: Computes interest rates based on utilization. Lower utilization results in lower rates, while higher utilization increases rates.

Deployer Contract: Automates the creation of new lending pairs with standardized parameters such as oracle feeds, rate calculator, and token addresses.

The maximum loan-to-value (LTV) ratio is set through governance votes. Typically, pairs with volatile tokens have an LTV around 75%, while stablecoin-stablecoin pairs can reach 90%. While the protocol maintains a liquidation bot, any user can execute liquidations on undercollateralized positions.

Source: Frax Finance

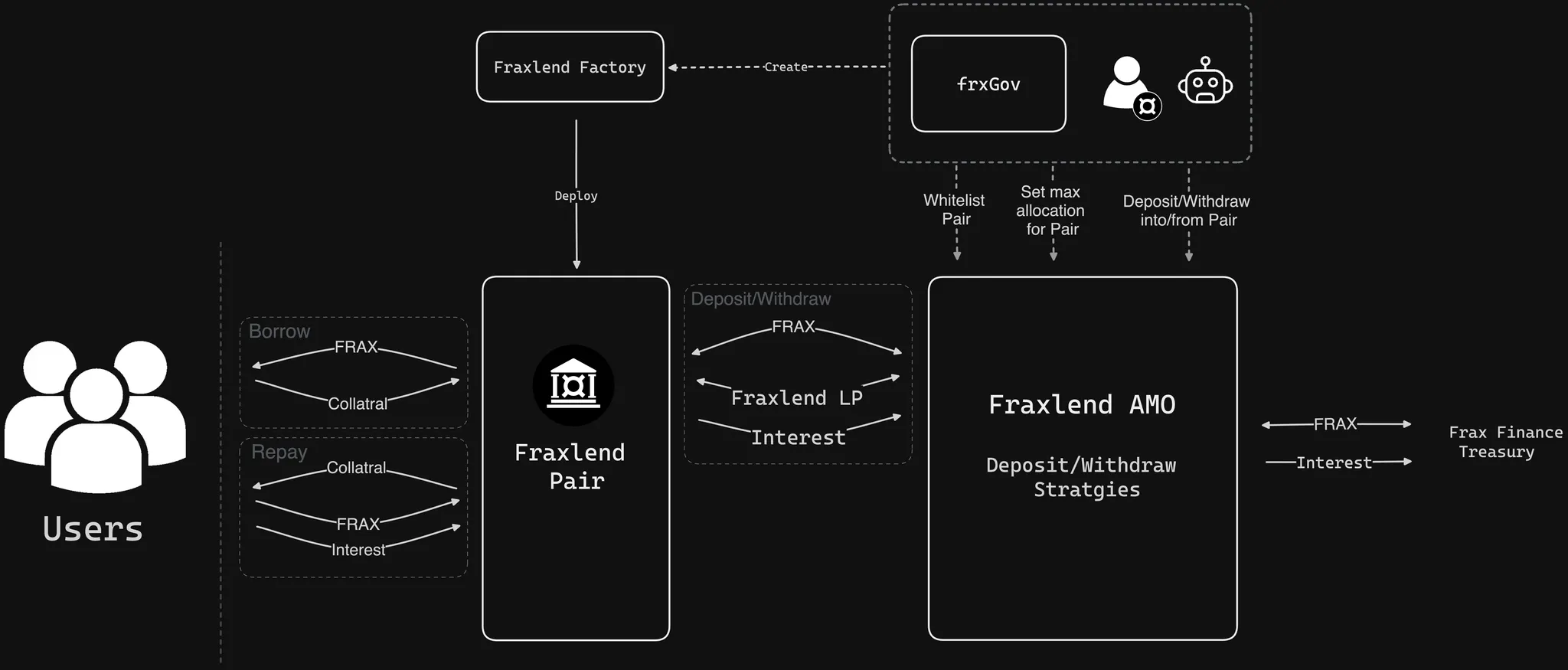

Fraxlend was designed to improve capital efficiency across the Frax ecosystem while generating income from protocol-owned liquidity.

The Fraxlend AMO plays a critical role by supplying protocol-owned FRAX, frxETH, and sfrxETH to lending pairs. Users borrow these tokens by depositing collateral and paying interest, enabling leveraged farming or position diversification. The protocol earns revenue by lending its own assets and collecting interest.

3.2.3 BAMM: Borrow-AMM Module on Fraxswap

BAMM (Borrow Automated Market Maker) is a lending module that operates on top of Fraxswap, designed to function without external oracles or separate liquidity sources. Traditional lending protocols require real-time price feeds from oracles and dedicated liquidity provisioning. In contrast, BAMM directly utilizes Fraxswap liquidity pools, enabling lenders and borrowers to interact with the pool’s liquidity itself.

The core mechanism of BAMM is the use of √k (the square root of the constant product) derived from the Uniswap V2 constant-product formula as the collateral valuation metric. In a Fraxswap liquidity pool, the product of the two assets x and y remains constant as k. √k represents the linearized depth of the liquidity pool. Because √k remains relatively stable even when price ratios fluctuate temporarily, BAMM can evaluate collateral value with reduced sensitivity to short-term price volatility.

Source: FraxFinance

To better understand this mechanism, the interactions between lenders and borrowers in BAMM can be summarized as follows:

Lenders

Lenders deposit Fraxswap LP tokens into the BAMM lending pool. Lending capacity is based on the √(x*y) value of the pool, which remains stable despite price fluctuations, allowing it to serve as a reliable solvency benchmark.

Lenders earn both the trading fees generated within Fraxswap and interest paid by borrowers who rent liquidity, securing two sources of yield from the same liquidity position.

Borrowers

Borrowers must first deposit collateral into a vault before borrowing. When liquidity is borrowed from the BAMM pool, the corresponding LP tokens are burned and the underlying assets are transferred to the borrower’s vault and locked. In effect, the rented liquidity becomes collateral in the form of the underlying tokens.

Borrowers may withdraw tokens as long as the borrowed liquidity does not exceed 98 percent of the vault’s √(x*y) value. If the utilization exceeds this threshold, withdrawals are blocked or the position is liquidated to protect collateral integrity.

This model requires lenders to manage layered impermanent loss and risk dynamics, distinguishing it from conventional deposit-based lending. Borrowers may also face conservative loan-to-value ratios. Despite these considerations, BAMM provides meaningful advantages by increasing capital efficiency for liquidity providers and offering borrowers access to leverage in a structure that reduces liquidation risk during sharp price movements. As a result, BAMM can serve a selective yet clear market demand for capital-efficient liquidity use under lower volatility risk conditions.

3.2.4 Frax Ether: Leverage-Enabled Liquid Staking

Frax Ether simplifies Ethereum staking and provides a DeFi-native way to earn ETH staking yield. Ten percent of staking revenue is retained: 8% as a protocol fee and 2% for an insurance fund.

The system consists of three main components:

frxETH: A token pegged to ETH with a defined peg range of 0.99 to 1.01 ETH per frxETH.

sfrxETH: An ERC-4626 vault version of frxETH that accrues staking rewards from Frax Ether validators. By converting frxETH to sfrxETH, users earn staking yield, which is realized when converting back to frxETH.

Frax ETH Minter: Allows users to exchange ETH for frxETH. The protocol spins up validator nodes and mints frxETH equivalent to the ETH deposited.

This design removes the need to run a validator node or deposit 32 ETH. Users can stake any amount of ETH, withdraw at any time, and use frxETH across DeFi.

frxETH V2 opens validator participation to external operators. Individuals or institutions can run validators and join the Frax Ether system. External validators can use escrowed exit messages as collateral to borrow additional ETH, enabling them to run more validators or leverage ETH positions.

frxETH V2 generates revenue from two sources:

Idle ETH deployment: Unused ETH collateral from validator deposits can be deployed into DeFi strategies such as Curve AMOs to earn additional yield.

Borrowing interest: External validators borrowing ETH through the credit facility pay interest, which becomes a key income stream for the protocol.

Source: Frax Finance

Frax Finance excels at deploying capital efficiently. It supplies liquidity to Curve pools and RWA products through AMO contracts and reallocates sfrxUSD dynamically to the best yield strategies based on market conditions, maximizing capital efficiency.

To support this strategy, Frax Finance has built a dedicated cross-chain solution using the LayerZero Omnichain Fungible Token (OFT) standard. This allows Frax subprotocols to seamlessly explore yield opportunities across multiple chains and enables Frax ecosystem assets to connect not only to Fraxtal but also to many other networks.

3.3.1 LayerZero OFT Standard

Assets such as frxUSD and frxETH are represented as LayerZero OFTs on chains other than Fraxtal and Ethereum. These tokens function exactly like ERC-20 tokens but include native bridging capability through the LayerZero protocol. Today, Frax assets using the OFT standard are integrated with more than 25 chains including Arbitrum, Optimism, Unichain, Aptos, Base, BSC, and Solana.

Before adopting the OFT standard, Frax built its own multichain bridging solutions, but as the number of supported chains grew, managing N² connections became increasingly complex. For example, supporting 10 chains required 45 separate bridge connections. To solve this, Frax partnered with LayerZero in February 2025 to implement a hub-based cross-chain architecture.

Through this architecture, seven key Frax assets (frxUSD, sfrxUSD, frxETH, sfrxETH, WFRAX, FXS, and FPI) were upgraded to the OFT standard, and Fraxtal was established as the central hub. All cross-chain transfers of these assets route through Fraxtal, reducing the network’s complexity from N² connections to N.

3.3.2 Dual-Lockbox Design

Frax Finance also operates a dual-lockbox system so that users can redeem OFT tokens for native Frax assets on both Ethereum and Fraxtal.

This design places lockboxes on both chains. If one side experiences heavy traffic or runs low on liquidity, the other can process redemptions and bridging, significantly reducing bridge failure risk. Users holding OFT tokens can redeem them for native Frax assets directly on either chain without additional unwrapping steps, preserving the native characteristics and full value of the assets.

Stablecoin adoption has moved beyond early optimism and is now viewed as an inevitable development to address inefficiencies across the financial system, from payments to international remittances and securities settlement. Yet according to a BCG report, as of 2024 about 88% of stablecoin transaction volume remains concentrated in crypto trading. This shows that broad adoption in the real economy is still at an early stage.

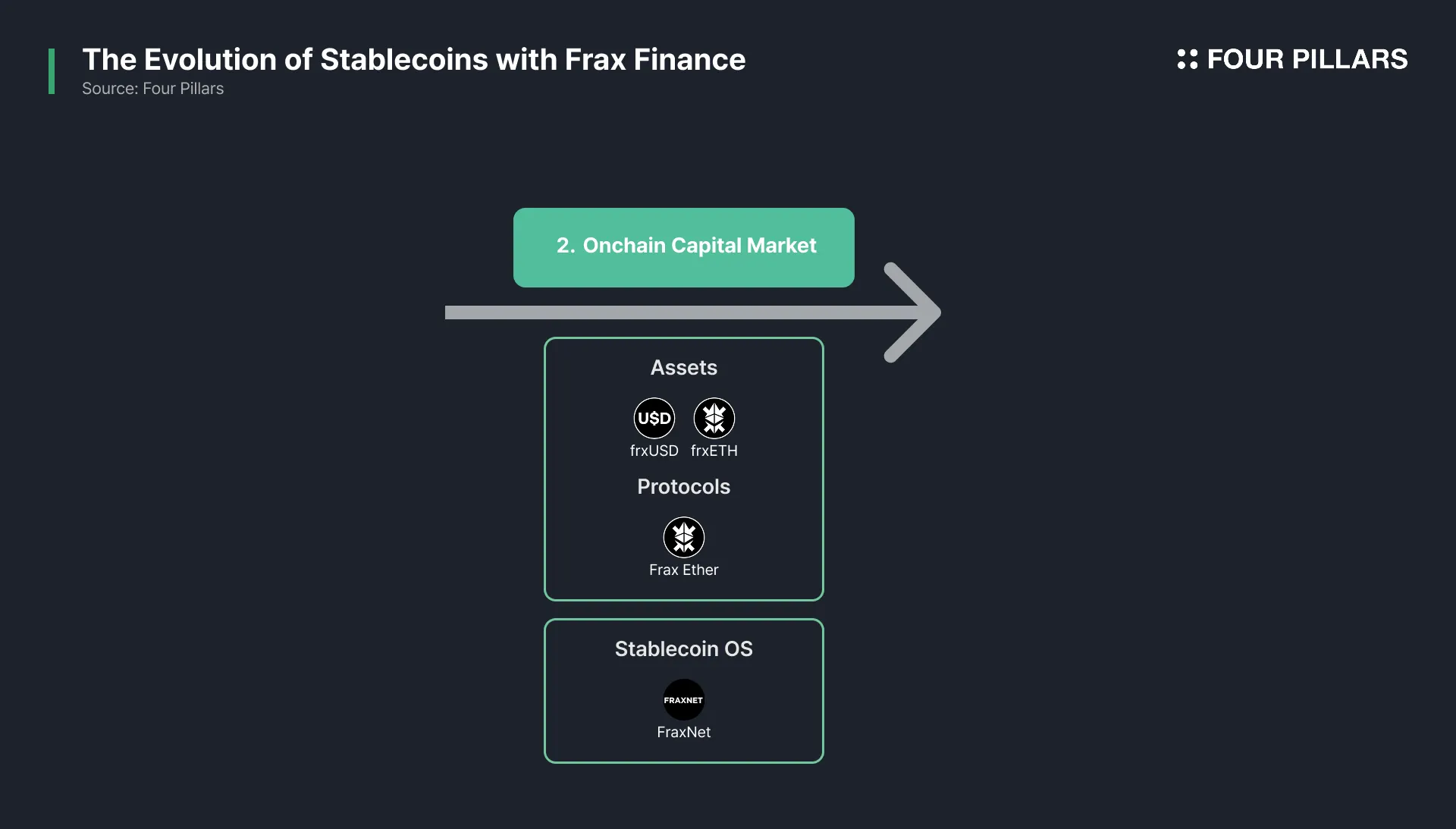

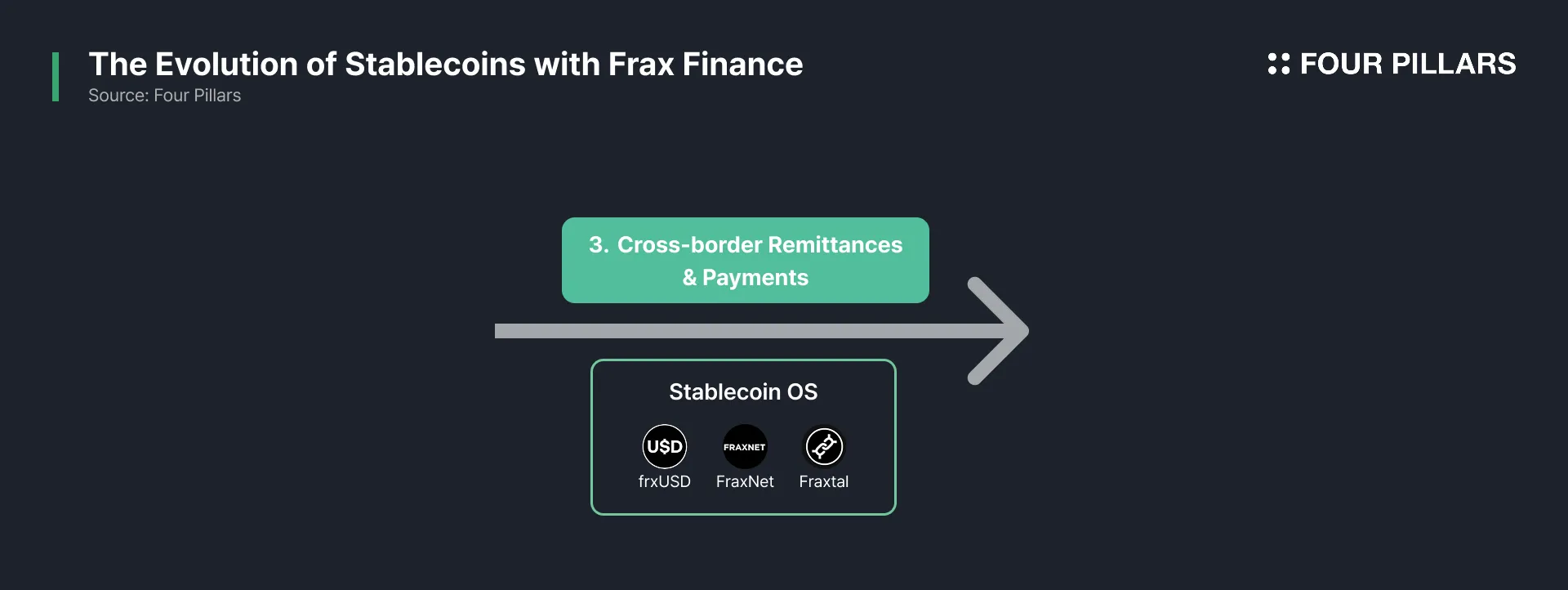

Stablecoin adoption will likely proceed in three phases. First, it will expand within crypto trading and DeFi, then into onchain capital markets where traditional financial liquidity merges with blockchain infrastructure, and finally into real-world economic use cases such as international remittances and global payments. While these stages may overlap, the overall trajectory will follow this progression as infrastructure and regulation mature.

Frax Finance is uniquely positioned with the infrastructure to grow across all three phases:

Crypto Trading

frxUSD is already used as a base asset on major exchanges and DeFi protocols, and LayerZero OFT connectivity provides deep liquidity for crypto trading across many chains including Solana and Base. sfrxUSD and other Frax assets diversify positions through fixed or optimized yields.

Frax Finance has built an extensive set of native DeFi protocols, giving it a structural advantage over other stablecoin issuers. Fraxswap uses TWAMM to handle large trades efficiently, while Fraxlend and BAMM provide a robust lending infrastructure that supports leverage trading with strong stability.

Onchain Capital Markets

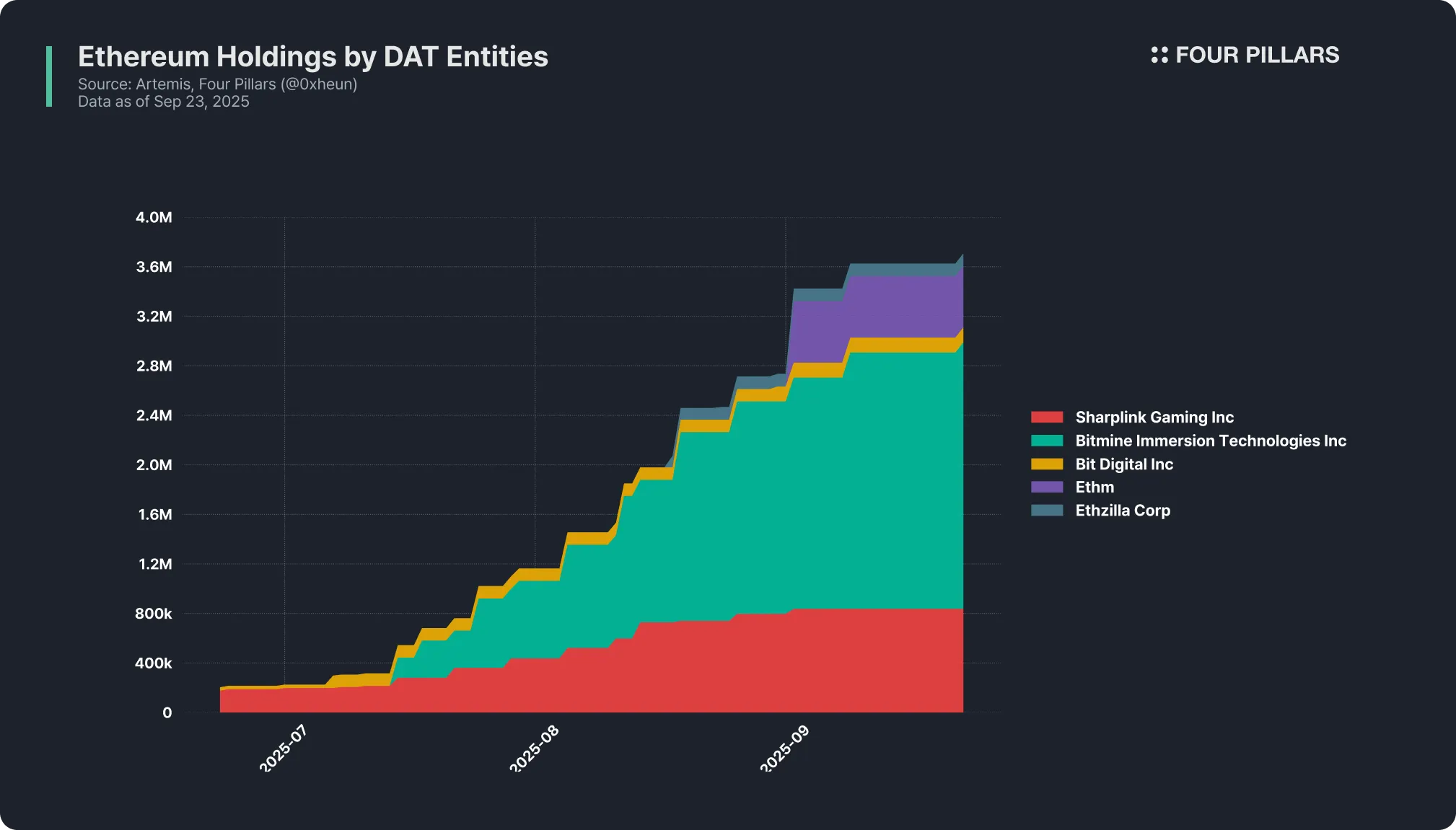

Institutional demand for ETH liquidity continues to grow. Mining firms like Bitmine, companies such as Sharplink, and Digital Asset Treasuries (DATs) are accumulating ETH treasuries to earn stable staking yields. Frax Ether captures this demand by providing a staking infrastructure that attracts institutional participants to the Frax ecosystem and deepens exposure to frxUSD and other Frax assets.

Fraxnet is also prepared to accommodate institutional liquidity with its GENIUS Act-compliant yield distribution. Institutions and individual investors can stake frxUSD on Fraxnet to earn T-Bill-based risk-free yield without regulatory friction.

International Remittances and Payments

Frax Finance is building its stablecoin OS with the final stage of international remittances and payments in mind:

Monetary unit: frxUSD meets GENIUS Act standards for USD settlement and can integrate directly with global payment rails.

Frontend: Fraxnet plans to offer features like bank wire integration, embedded wallets, a mobile app, and a unified asset dashboard, delivering a neobank-level user experience.

Backend: Fraxtal provides fast transaction throughput and instant settlement as a high-performance Layer 1 infrastructure, positioning it as a potential global network for payments and cross-border transfers.

Frax Finance has already built a highly mature financial infrastructure that aligns with the progressive phases of stablecoin adoption. It is prepared to continue advancing on top of this foundation, adapting swiftly to regulatory and technological changes.

Ultimately, the Frax Finance vision for a stablecoin OS points toward a time when the term “stablecoin” may no longer be needed. In a world where most money circulates onchain as dollar-pegged tokens, distinguishing between physical cash and onchain dollars becomes unnecessary. When this point arrives, with an M1-level financial stack in place, Frax Finance is poised to occupy a central role in the global financial infrastructure.

Dive into 'Narratives' that will be important in the next year