Overheated competition and little real differentiation — that’s the impression left by the current wave of perpetual DEX wars. Most DEXs are not presenting clear performance advantages but are instead focusing on incentive battles, whose sustainability remains uncertain.

Avantis is building its own playing field by targeting an asset class that remains largely untapped in onchain perpetual trading: RWAs. Considering the scale of the global derivatives market and the strong demand for global assets, this can represent a meaningful market opportunity.

To secure liquidity for synthetic RWAs, Avantis has adopted an oracle-based perpetual trading engine. At the same time, it has introduced sophisticated price request mechanisms and risk buffers across the system design to minimize oracle vulnerabilities and LP slashing risks.

Representative assets in Avantis’s RWA perpetual markets include U.S. equities such as the Mag 7 and COIN. Avantis offers up to 25x leverage for these markets on borderless onchain rails, providing an alternative venue for existing onchain traders while also capturing global investor demand.

Could Avantis’s development of onchain RWA perpetual trading become the final chapter of perpetual DEX evolution? At the very least, it cannot be ruled out that this path will emerge as one of the ways DEXs evolve by absorbing traditional financial infrastructure.

Overheated competition, weak differentiation. This is the impression of the ongoing “perpetual DEX wars.” Competition is always good for industry progress. However, when competing in a sector that has already reached a certain level of standardization, it becomes increasingly difficult for players to create a differentiated playbook. As a result, it is easy for the competition to devolve into a zero-sum game of bleeding incentives.

This article focuses on Avantis, which is building a new arena for perpetual DEXs through RWA-based onchain perpetual trading. It also examines the possibility that the endpoint of perpetual DEXs may converge on RWA perpetuals, and, based on that premise, explores in detail the synthetic perpetual engine and RWA perpetual markets that Avantis is constructing.

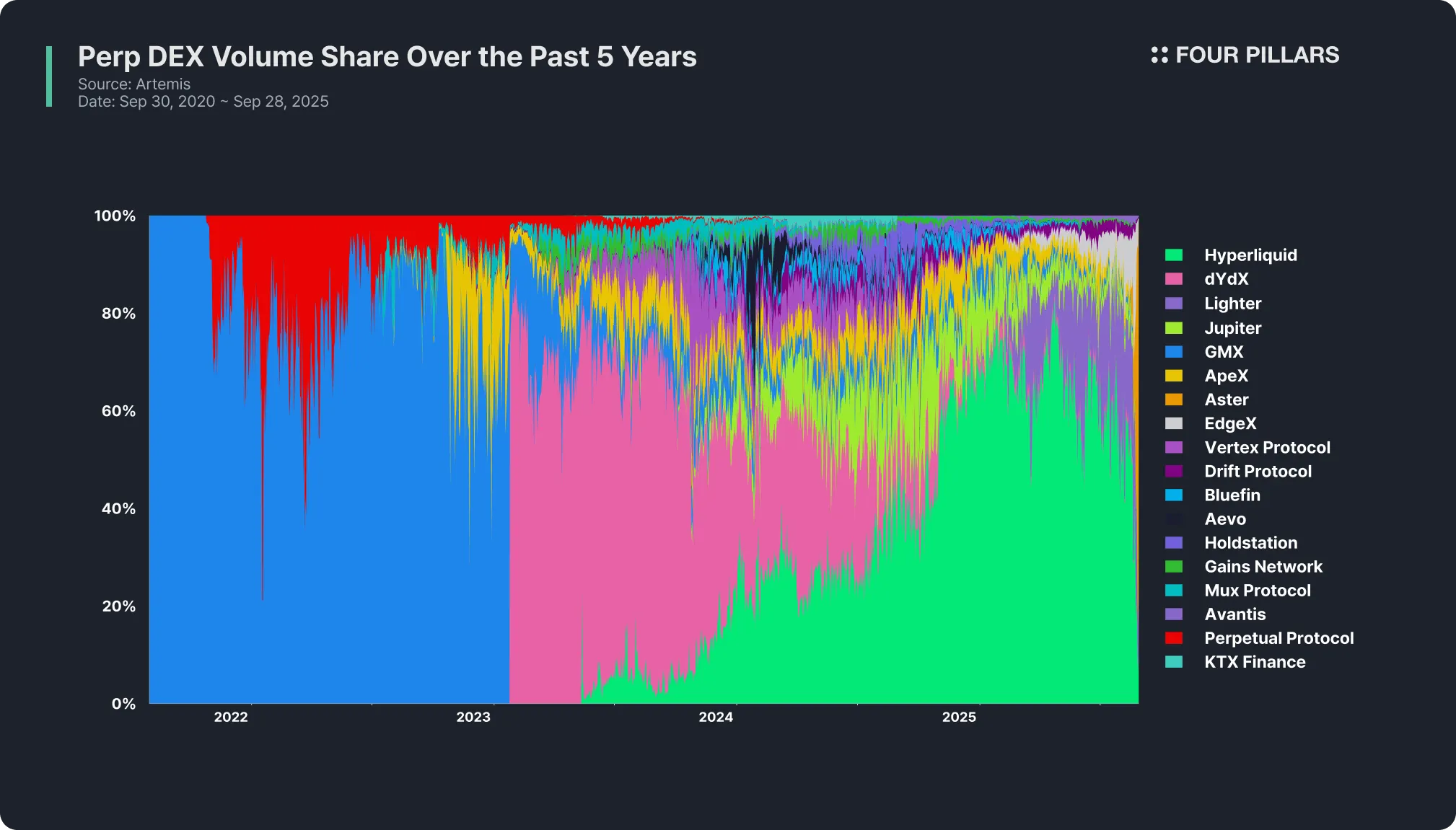

Is there any other sector where competition has been as intense as perpetual DEXs? Proven demand for crypto futures trading, combined with the certainty of a transaction-fee-based revenue model, has long made perpetual DEX market share a coveted prize. From the early battles between Perpetual Protocol, GMX, and dYdX for the throne, the competition has continued to this day.

As competition persisted, Hyperliquid successfully demonstrated that deep liquidity and stable user experience can be achieved even in an onchain CLOB. With significant trading volumes, it conducted meaningful token buybacks, while its founder Jeff Yan’s emblematic leadership helped form a cult-like community. Hyperliquid further positioned itself as a market leader by pushing ecosystem expansion through Hyper EVM centered on Hyper Core. As a result, Hyperliquid managed to sustain over 70% market share for an extended period.

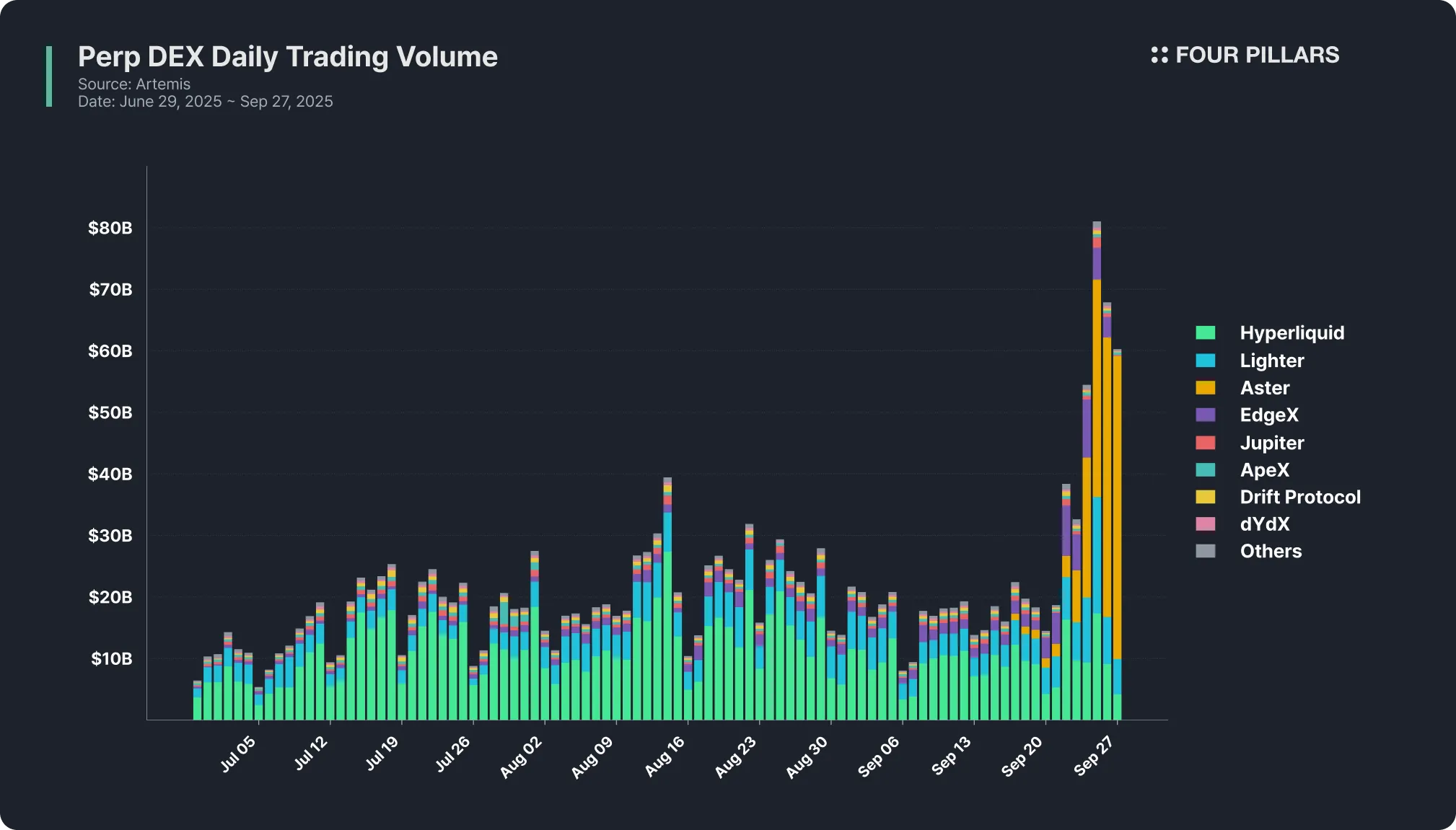

But markets rarely allow any player to maintain absolute dominance. New DEXs such as Aster, Lighter, EdgeX, and Pacifica have entered the field, among which Aster emerged as a strong contender with the full support of Binance founder CZ. Following a high valuation for the ASTER token and expectations for seasonal incentive rewards, daily trading volume quickly surpassed $80B, absorbing market share in a short time. This has reignited the perpetual DEX wars.

A notable feature of the current perpetual DEX race is that most DEXs focus more on incentive battles than on introducing significant innovations in performance. In fact, key innovations such as off-chain matching with onchain settlement orderbooks, dedicated appchains, the first introduction of oracle-based synthetic perpetuals, buybacks proportional to trading volume, and vault-based liquidity provision with insurance mechanisms have already been implemented years ago.

As a result, the industry is now in the situation described earlier: competition is overheated and differentiation is weak. More specifically, the dynamics look like this:

Trading Infrastructure Edge: With speed improvements in general-purpose L1/L2 chains and the advent of dedicated appchains, latency has been optimized and most order processing engines have already reached CEX-level performance. Now differentiation is sought mainly through details such as fee competition or private order functionality. While these features add convenience and meet niche demand, they do not create decisive competitive advantages.

GTM Strategy: Running seasonal point programs around TGEs to drive trading and liquidity lock-in has become a stdfandard playbook. The long-term strategy is to convert users drawn by incentives into real users of the DEX, but the sustainability of this approach remains uncertain.

These dynamics are directly reflected in shifts in market share. During periods when expectations for incentives are high, users and liquidity flood in. However, liquidity quickly departs when rewards weaken or a competitor offers more attractive incentives. As a result, market share fluctuates in cycles of roughly two weeks.

In such a competitive landscape, what strategic choices are available to perpetual DEXs? The most straightforward approach is to jump into the middle of the competition and offer slightly more attractive incentive structures than existing players.

From the user’s perspective, this is not necessarily a bad thing since it increases the variety of choices. At the same time, in today’s market environment where adoption is often driven by incentives, this approach also provides DEXs with a relatively low-risk and rational way to secure a certain level of trading volume.

However, the question of which perpetual DEXs can achieve long-term success is a different matter. The reason Hyperliquid was able to sustain market dominance over a long period was its clear differentiation from earlier players. Large-scale rewards and token buybacks and burns for loyal users, liquidity management through HLP, and ecosystem expansion via HIP-3 all contributed to making Hyperliquid a game changer in the market. Ultimately, this differentiated playbook mobilized the community to rally behind the vision of becoming an “onchain Binance.”

In other words, without differentiation at this level, other DEXs can only remain “onchain Binance-lite” or forks of Hyperliquid. Those that fail to go beyond incremental competitive advantages are likely to disappear as soon as the temporary “perpetual DEX meta” ends.

Source: X(@avantisfi)

Against this backdrop, Avantis stands out because it is creating its own competitive arena by targeting an asset class that remains largely untapped in onchain perpetual trading: RWAs. By bringing real-world assets such as equity indices, commodities, forex, and individual stocks into onchain futures markets, Avantis is not merely striving to become another onchain Binance but is instead positioning itself as an onchain Robinhood, competing on a fundamentally different basis.

In fact, Avantis has already moved beyond speculative anticipation around its TGE and entered a stage driven by real user-based trading activity. A notable indicator is that Avantis has achieved meaningful traction in perp volume, TVL and protocol fees among major DEXs such as Hyperliquid, Drift, and dYdX, which have been operating for years. This demonstrates that Avantis, as a late entrant, has successfully entered the market by delivering a compelling value proposition. It also suggests that its current multiples still have room for revaluation going forward.

Meanwhile, some emerging DEXs like Lighter and EdgeX have recorded higher perp volumes than most competitors, but these figures largely stem from incentive-driven programs designed to test early infrastructure. As mentioned above, it remains uncertain whether their current traction can translate into sustainable, user-driven fundamentals once the incentives taper off. By contrast, Avantis continues to show steady growth even after its TGE, making it particularly noteworthy.

So, what enabled Avantis to achieve such a strong market entry? And why could targeting the on-chain RWA perp market serve as a strategic advantage in the cycles ahead? The following section explores Avantis and the potential of its target market in greater detail.

Compared to global markets, the crypto market is still relatively small. By the end of 2024, the notional value of the global derivatives market was estimated to have exceeded $700T. For reference, even just the futures and options traded on CME Group, which cover equity indices, commodities, and forex, surpassed an average of 6B contracts per month in 2024. This translates into hundreds of trillions of dollars in notional value.

By comparison, the cumulative trading volume of crypto futures in 2023 was about $28T, and in 2024 it more than doubled to $58T. Yet this remains minuscule relative to the size of the global market.

In conclusion, even though the annual trading volume of the crypto perpetual market is growing rapidly compared to traditional futures markets, it still represents only a fraction of the total derivatives market. This wide gap highlights why RWAs such as tokenized U.S. T-bill MMFs or onchain private credit are seen as having massive market potential.

So far, the RWA market has been dominated by tokenized Treasuries issued by players such as Securitize, Ondo, and Superstate. These account for more than $6.8B of the total $13B on non-stablecoin RWA market cap, representing over half the market. Yet equities stand out as another real-world asset category with strong growth potential. Onchain equities open new opportunities in several ways:

2.2.1 Enhanced Global Accessibility

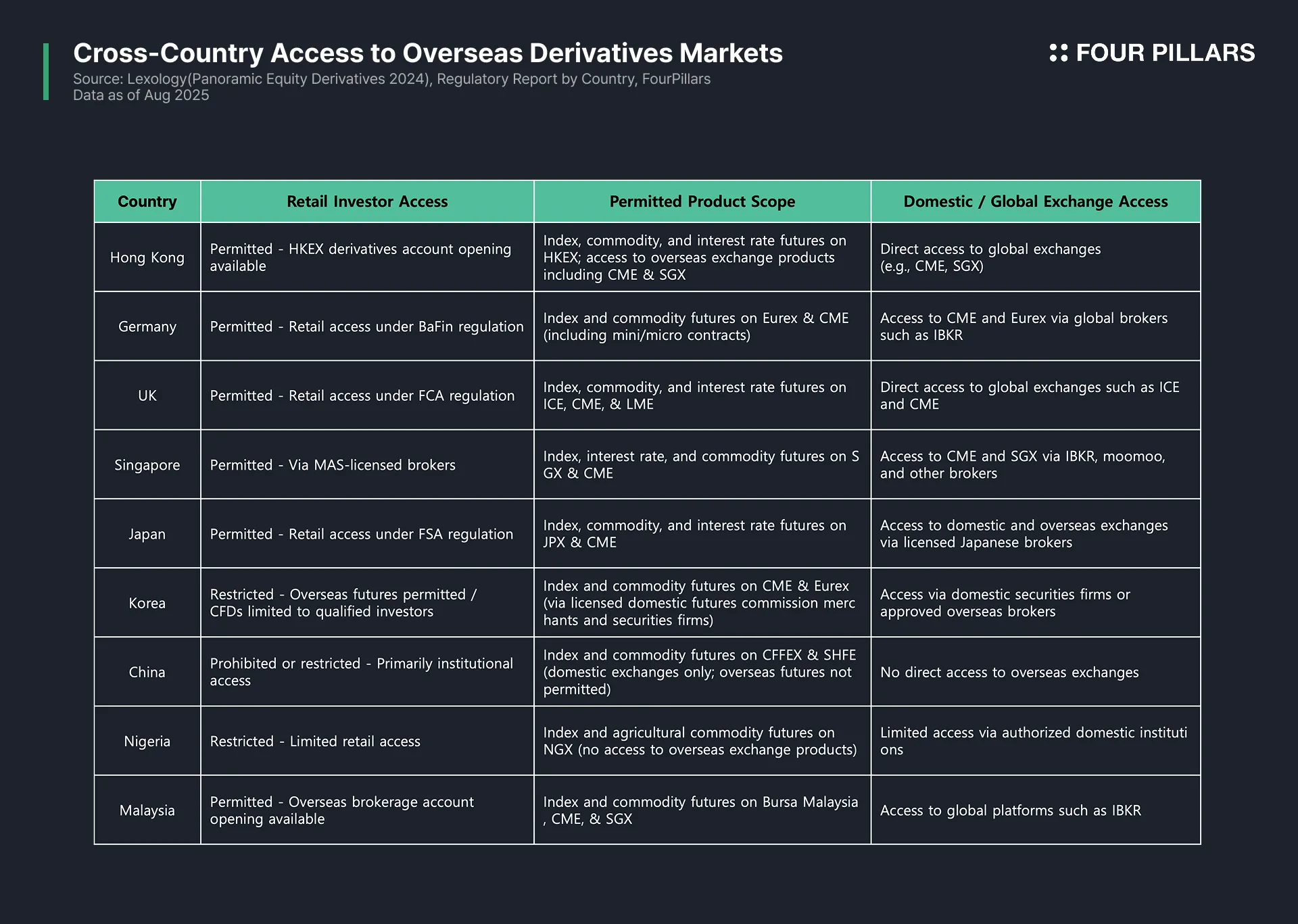

The instant settlement and borderless infrastructure of onchain rails increase access to global equities. Traditional financial infrastructure imposes structural constraints such as leverage restrictions, limited asset classes, high fees, slow settlement, and limited liquidity. For investors seeking to directly access high-demand global assets such as U.S. equities, hurdles include opening overseas brokerage accounts, dealing with complex FX processes, and facing tax risks.

In addition, some countries impose capital controls or operate under underdeveloped financial systems, which restrict access to volatile assets. Shorting and margin trading, in particular, are either prohibited or severely restricted for retail investors in most jurisdictions. Against this backdrop, onchain equities can serve as a compelling alternative for global investors by removing these local barriers.

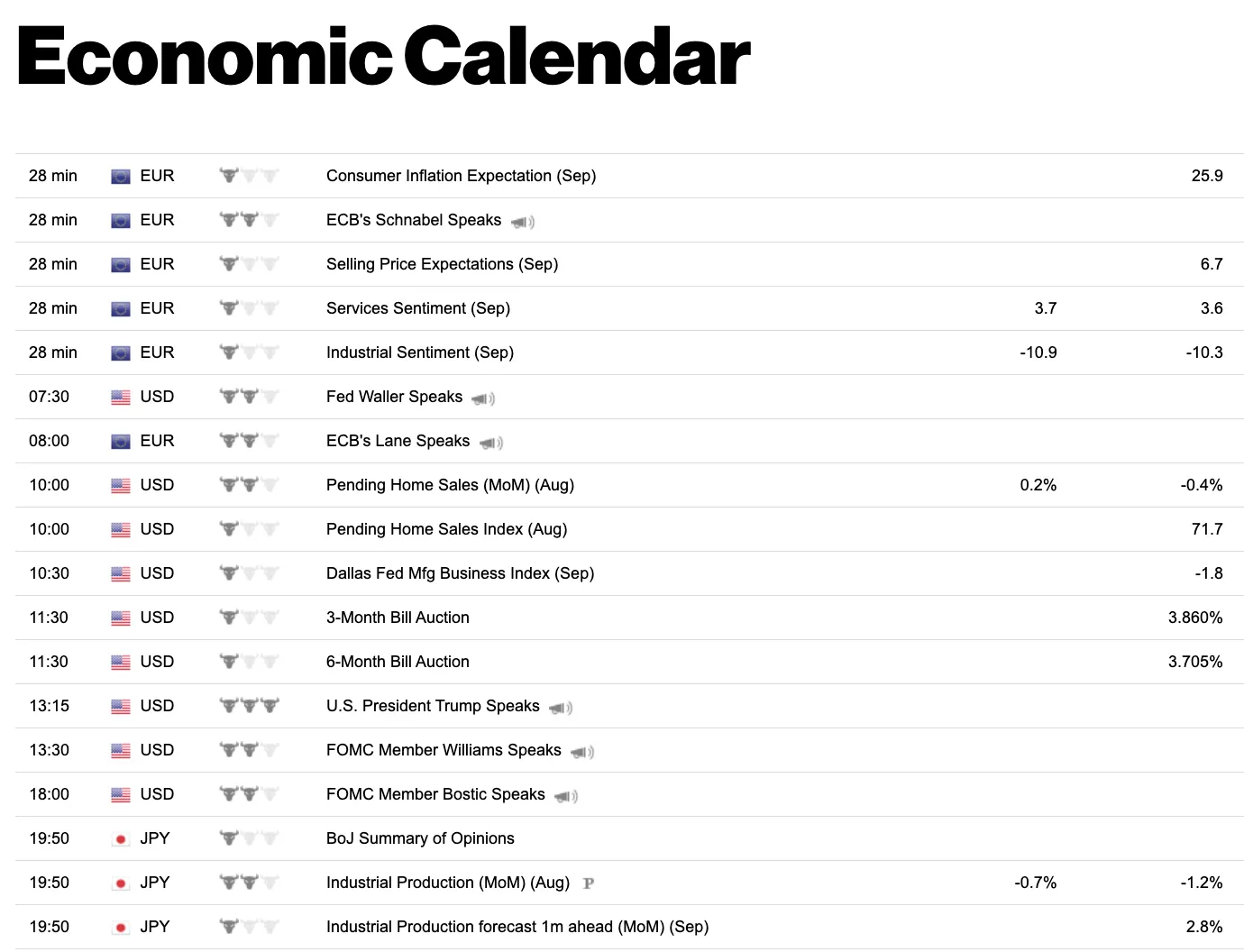

2.2.2 High Predictability via Economic Calendars

Source: Bloomberg

Onchain equities also present clear value propositions as alternative trading assets for existing onchain traders. Futures trading of crypto-native assets tends to be influenced by crypto-specific narratives and short-term events, making directional and timing predictions more challenging. Altcoins in particular often fluctuate more than 10% within a single day, reflecting a market that is highly sensitive to sentiment and liquidity rather than fundamentals.

By contrast, onchain equities are influenced by macro events tied to the real economy, such as inflation, interest rate decisions, employment data, and elections—all of which are announced in advance on economic calendars. The resulting price moves also tend to follow more logical and predictable directions. This provides onchain traders with an alternative trading environment where they can harness scheduled volatility. Knowing in advance when volatility will concentrate allows them to apply predictive models and technical analysis with greater consistency.

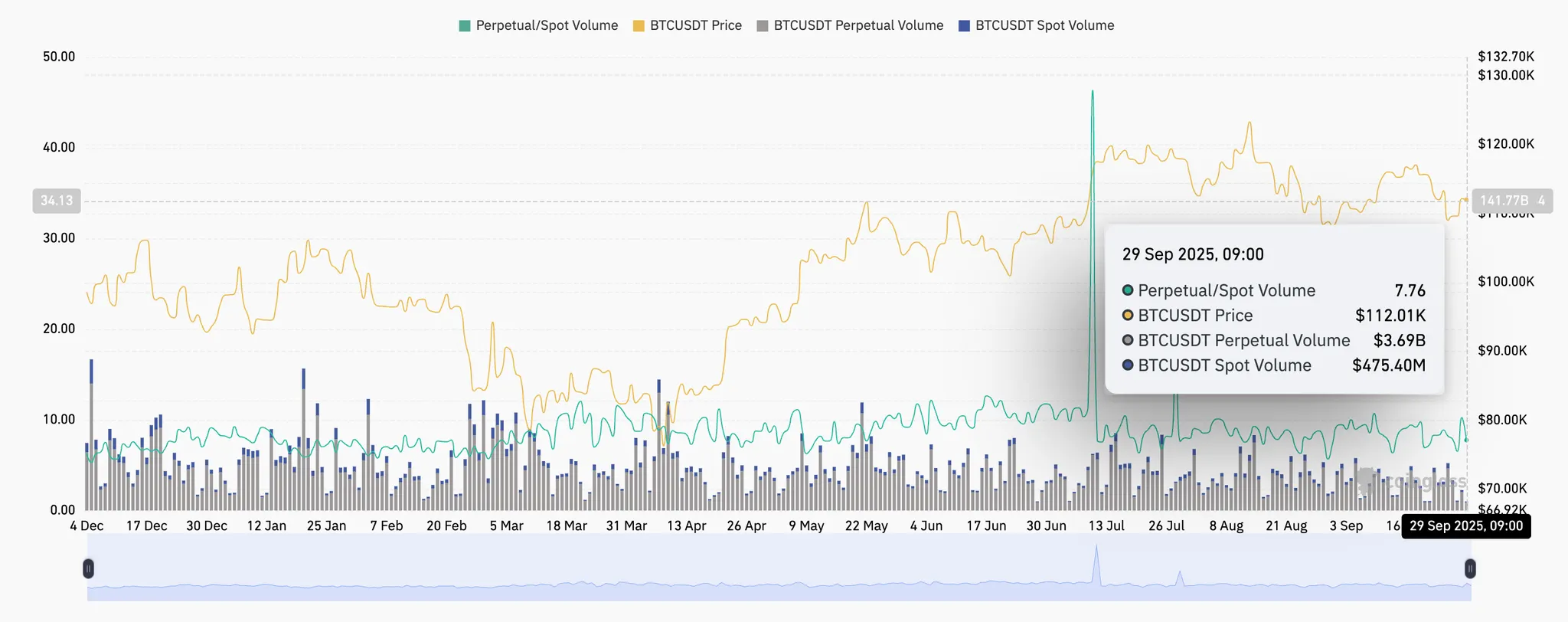

Source: Coinglass

Onchain equities are emerging as important assets within the RWA space and as alternative trading assets within crypto markets. Yet a major gap remains: there is still no way to trade them via perpetual contracts.

Perpetuals account for about 74% of all crypto trading volume. As of September 2025, BTC perpetual volume alone was roughly 8x higher than daily spot volume. In fact, about 88.6% of BTC’s daily trading volume occurs in perpetual markets. Despite this enormous opportunity, there is still no onchain perpetual market where investors can trade equities on a 24/7 self-custodied basis.

2.3.1 Alignment Between Crypto Equities and Onchain Equity Perpetuals

A useful case study for the potential of onchain equity perpetual markets is crypto equities. By crypto equities, we mean publicly listed companies on NASDAQ or NYSE that either hold significant digital assets in treasury, operate as mining firms, run crypto exchanges, or provide crypto infrastructure.

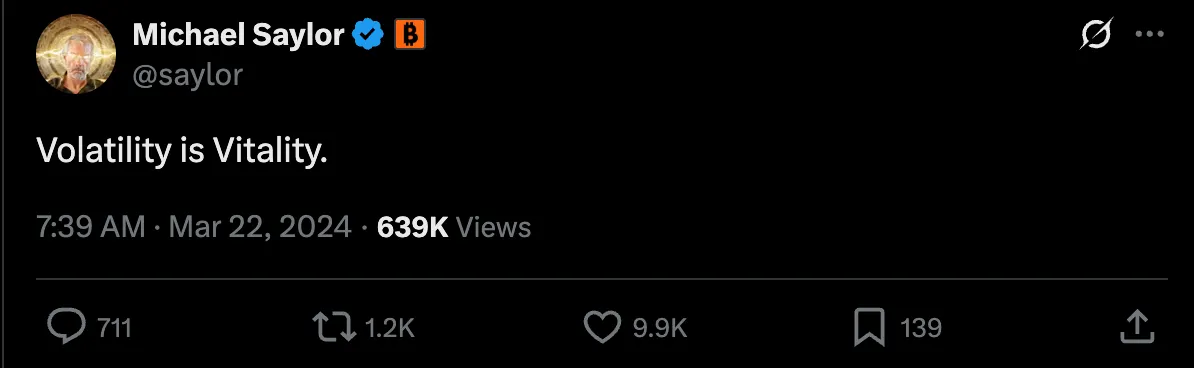

Source: X(saylor)

So what would change if crypto equities could be traded as perpetuals on onchain rails?

Take MicroStrategy (MSTR), which holds a large amount of Bitcoin. Its stock price has historically shown a strong correlation with BTC’s price. As a result, MSTR often serves as a leveraged BTC proxy in equity markets, and is actively traded alongside BTC in various structured strategies.

For example, MSTR’s stock price and BTC’s price frequently diverge due to market flows, creating premiums or discounts. Traders can exploit this short-term dislocation by shorting the overvalued asset and going long the undervalued one in a pair trade. Michael Saylor, Chairman of MicroStrategy, has even described MSTR as a “Volatility Engine”, emphasizing the additional value that can be generated from its volatility.

If such crypto equities were brought onto onchain perpetual markets, traders would no longer need to rely on traditional financial infrastructure such as prime brokers, clearinghouses, or bank accounts. Instead, they could execute strategies like taking a 10x long on MSTR and a 10x short on BTC from a single collateral account within a unified onchain platform.

2.3.2 The Potential Market Size for Onchain Equity Perpetuals

Building on the advantages of onchain rails, if onchain equity perpetual markets gain adoption and gradually absorb trading volume away from traditional financial rails, the market opportunity could be significant.

To estimate this potential, let us take a basket of representative crypto equities. As of Q3 2025, the combined market capitalization of 14 major stocks, including MSTR (MicroStrategy), COIN (Coinbase), and GLXY (Galaxy Digital), amounts to approximately $377.5B.

Based on market cap, this basket of equities has been growing faster than altcoins:

The total crypto market cap is about $4T, of which BTC accounts for 59.5% and ETH 12.6%. The remaining altcoin market is about $1.1T.

By contrast, the basket of 14 crypto equities already represents about 34% of the altcoin market size and is expanding rapidly.

Yet there is still no infrastructure to support perpetual trading of these equities onchain, which leaves a significant gap:

Based on the $377.5B basket, if we conservatively assume a monthly spot turnover ratio of 8%, that implies around $30.2B in monthly spot volume.

Applying the typical futures-to-spot ratio in crypto (2–3x), monthly perpetual volume could reach between $60.4B and $90.6B.

This suggests a potential market capable of absorbing tens of billions of dollars in monthly notional volume. Even on conservative assumptions, the potential of an onchain equity perpetual market far exceeds that of perpetual DEXs limited to crypto assets.

Furthermore, crypto equities are only one example. If indices like the NASDAQ-100 or the S&P 500 tech sector index were to become tradable as onchain perpetuals, the market size and opportunity would expand far beyond current levels. In short, it is difficult to regard onchain equity perpetual markets as merely a niche opportunity when the scale of potential trading volume is this significant.

From here, we turn to Avantis’s trading engine, LP vault mechanics, and onchain equity markets to see how the protocol is addressing this opportunity.

Source: Avantis

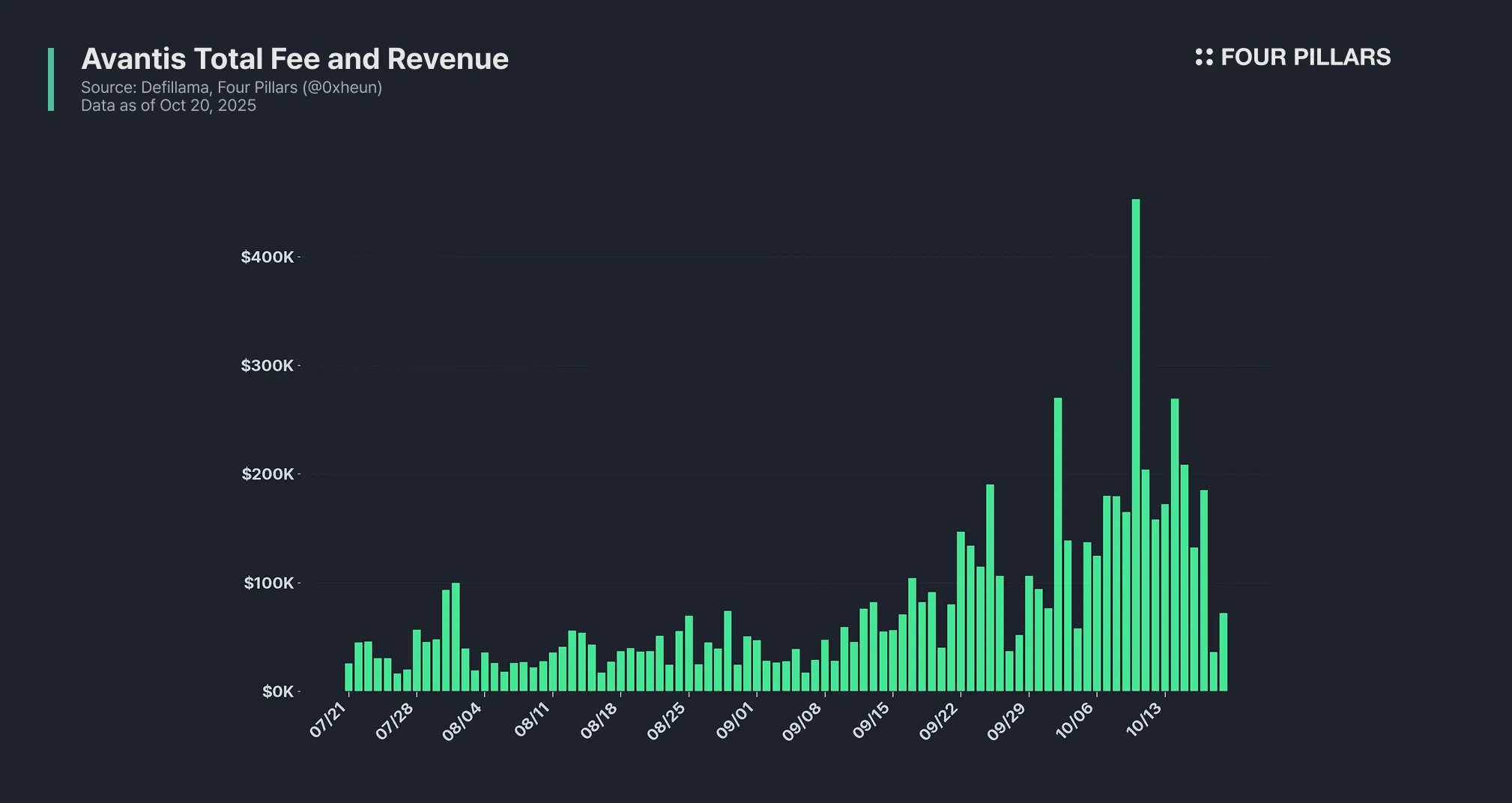

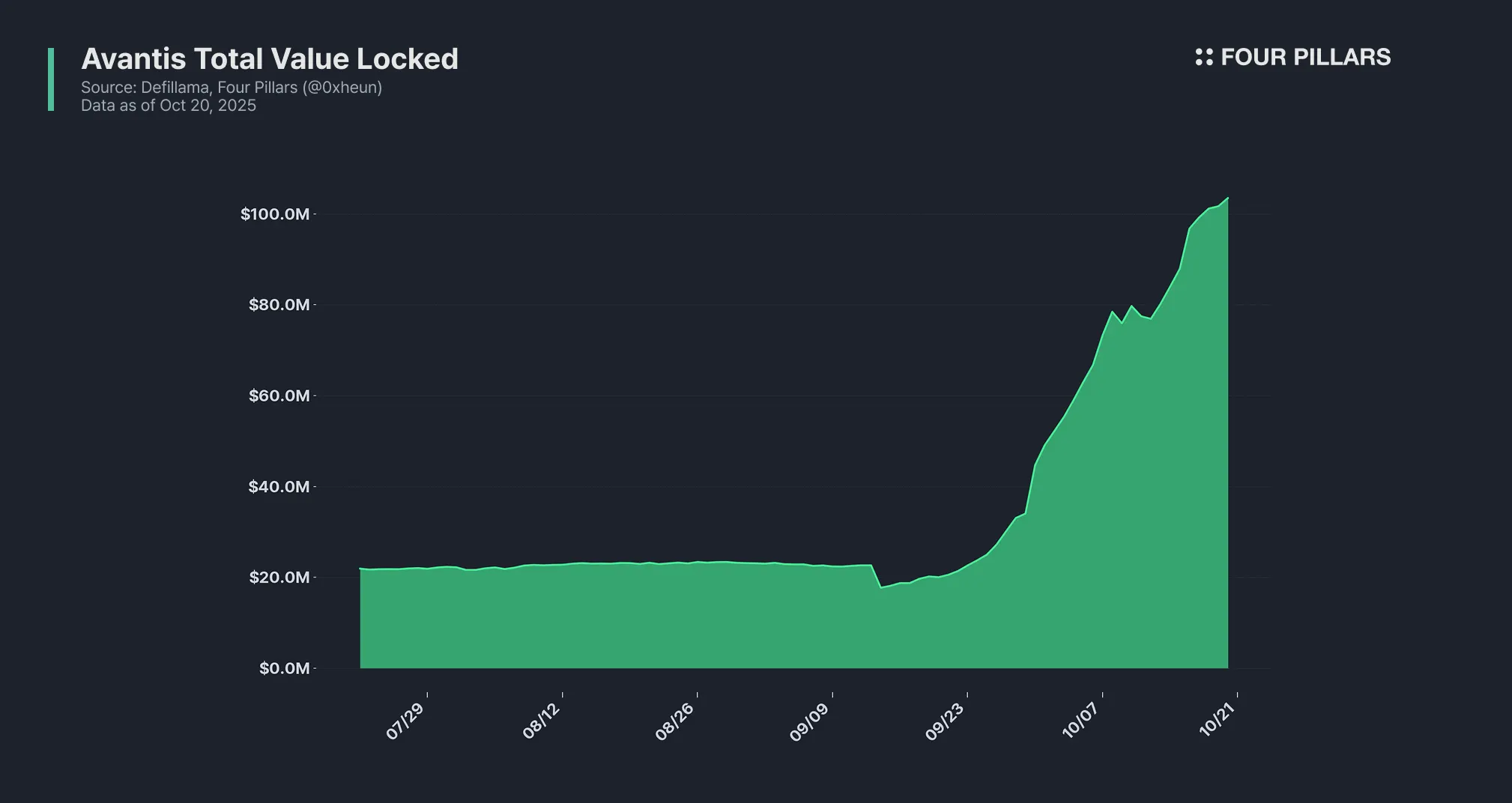

Avantis is a perpetual DEX built on Base. At launch, it attracted market attention by offering zero trading fees, up to 500x leverage, and support for real-world assets such as the Turkish Lira, commodities, and forex pairs for the first time. It has since expanded into onchain equities, including Coinbase stock and the Mag7, and today records over $40B in cumulative trading volume and $102M in TVL, establishing itself as the largest perpetual DEX in the Base ecosystem.

The reason Avantis can frictionlessly offer perpetual trading not only for crypto assets but also for a wide range of RWAs is that it has adopted an oracle-based synthetic futures model. While oracle-based synthetic futures have been widely used since the GMX era due to their flexibility in expanding asset pairs, many DEXs eventually shifted to orderbook models because oracle risks and LP slashing exposure reduced incentives for liquidity provision.

Avantis, however, has chosen to maintain the oracle-based model in order to pioneer the onchain RWA perpetual market. Instead of abandoning it, Avantis has built stability into its design by introducing refined price-request mechanisms and risk-buffering measures to mitigate oracle vulnerabilities and protect LPs from slashing risk.

3.1.1 How Synthetic Perpetuals Work

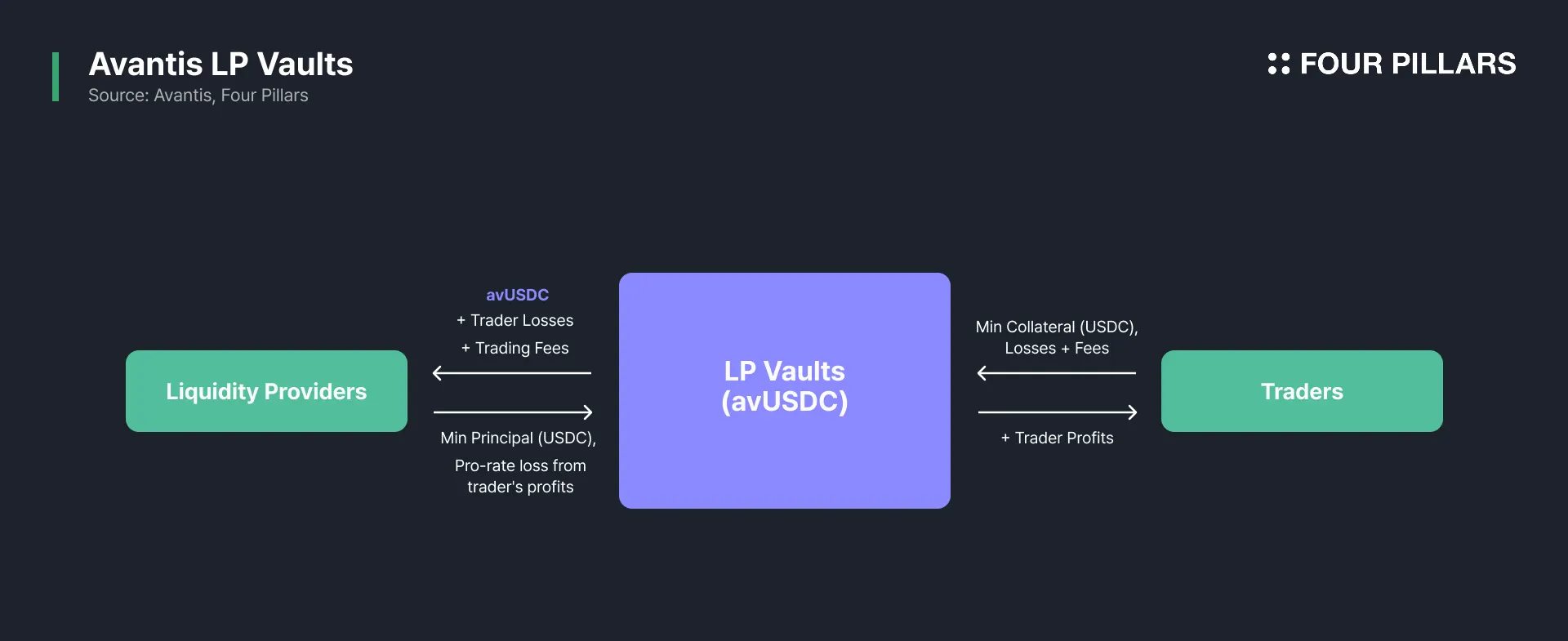

Avantis implements synthetic perpetual trading through USDC-based LP vaults. The mechanism is similar to GMX’s GLP vault. The LP vault acts as the counterparty to all trades on the platform. If traders generate profits, payouts are drawn from the vault. If traders incur losses, the losses accrue to the vault. In return, LPs earn a share of trading fees, distributed proportionally to their vault share.

The risk in this setup is that when positions become too one-sided (long-heavy or short-heavy), delta exposure accumulates against LPs. For example, if a majority of traders pile into long positions, LPs effectively hold the offsetting short, exposing them to concentrated losses. The same applies in the reverse direction.

To address this, Avantis continuously monitors open interest (OI) imbalances. When long-short ratios become skewed, the protocol introduces incentives to attract traders to the opposite side. In addition, Avantis collaborates with professional market makers such as Keyrock to alleviate OI imbalance, thereby reducing LP risk and ensuring liquidity stability.

3.1.2 Pricing Mechanism

Because Avantis is oracle-based, it does not engage in price discovery itself. Instead, real-time execution prices for all listed assets are sourced externally through oracle feeds.

The primary vulnerability of oracle-based trading is the possibility of price-feed manipulation. Attackers can temporarily distort market prices, pushing inaccurate data into the oracle and settling trades at artificially favorable levels. This can trigger forced liquidations or cause LPs to absorb large losses.

To mitigate oracle risk, Avantis collaborates with Pythnet and Chainlink to source high-quality price feeds. In combination, Avantis ensures fair asset prices through the following methods:

Dynamic Spreads: Avantis uses the most liquid orderbooks (like Binance and CME) to price spreads. This gives traders the best prices on crypto and RWAs, while ensuring that LPs are only providing liquidity at fair market prices.

Weighted Price Feeds: When volatility is high or updates are delayed, manipulation risk increases. To counter this, Avantis does not rely on a single source. Instead, it aggregates inputs from over 70 first-party publishers in Pythnet, assigning greater weight to more accurate feeds and filtering out anomalies to derive manipulation-resistant final prices.

On-Demand Pricing: Another common oracle issue is latency when feeds fail to update in time. Avantis solves this by requesting on-demand prices on-chain for every user transaction, ensuring execution prices are always fresh and reliable.

Fail-Safe Smart Contracts: If price deviations exceed the acceptable range, transactions are automatically blocked. This prevents adversaries from forcing execution at distorted prices.

Chainlink Comparison: Whenever possible, Chainlink serves as a backup feed. For each trade, the contract fetches the latest on-demand Pyth price and cross-checks it against Chainlink. If the deviation exceeds a set threshold, the trade fails and the user must resubmit.

3.1.3 Guaranteed Stop Loss and Take Profit

Stop Loss (SL): Automatically closes a position at a predetermined price to cap losses.

Take Profit (TP): Automatically closes a position at a predetermined price to lock in gains.

Because Avantis executes trades through oracles, user SL and TP orders are always filled at the exact requested price. In contrast to orderbook systems, where execution depends on liquidity and may suffer slippage, Avantis references oracle prices as the sole execution standard. Once the oracle price reaches the requested level, the position is closed precisely at that price.

Guaranteed SLs only apply when set in loss-making zones. SLs placed in profit zones (to secure gains) still execute as limit orders and therefore are not guaranteed.

For example, assume a trader enters a long at $100 and sets an SL at $90:

Loss-Zone SL: Even if the oracle jumps from $92 straight to $88, the SL is guaranteed to close at $90.

Profit-Zone SL/TP: If the same trader sets a TP at $110 but the oracle jumps from $109 to $112, the TP will be skipped and not guaranteed at $110.

Thus, SLs set for loss protection are always honored at the exact price, while SLs or TPs for profit-taking may not be guaranteed if an oracle gap occurs.

3.2.1 ZFP Overview

Source: Avantis

An interesting statistic in futures trading is that roughly 90% of traders close positions at a loss. To address this, Avantis introduced Zero-Fee Perpetuals (ZFP). Under ZFP, no fees are charged if a trader’s gross PnL at close is zero or negative. In other words, fees are only paid on profitable trades, while losing trades incur no closing or borrowing costs. Currently, ZFP supports BTC, SOL, ETH, HYPE, and more, with leverage up to 500x.

Traditionally, perpetuals impose holding costs:

Orderbook Perpetuals: Funding rates are charged to traders taking the more popular side of the trade. Since crypto markets are typically long-biased, long traders continuously pay funding to shorts.

AMM Perpetuals: Onchain AMM-style perpetuals, backed by LP pools (like GMX or Gains), charge borrowing fees that gradually erode collateral.

In both cases, fixed fees reduce profitability, forcing traders to wait for larger price moves just to break even. Over time, borrowing costs also push liquidation prices closer, creating inefficient risk management.

ZFP removes upfront fees. Losing trades pay nothing. Profitable trades pay only a fraction of gross profits, starting at 2.5%, shared with LPs. This “win-fee” model is designed so that lower ROI trades pay a higher fee share, while higher ROI trades allow traders to keep more. On average, traders retain over 80% of profits. The result is an incentive structure that rewards traders for maximizing performance while ensuring LPs remain fairly compensated.

3.2.2 ZFP Quantitative Modeling

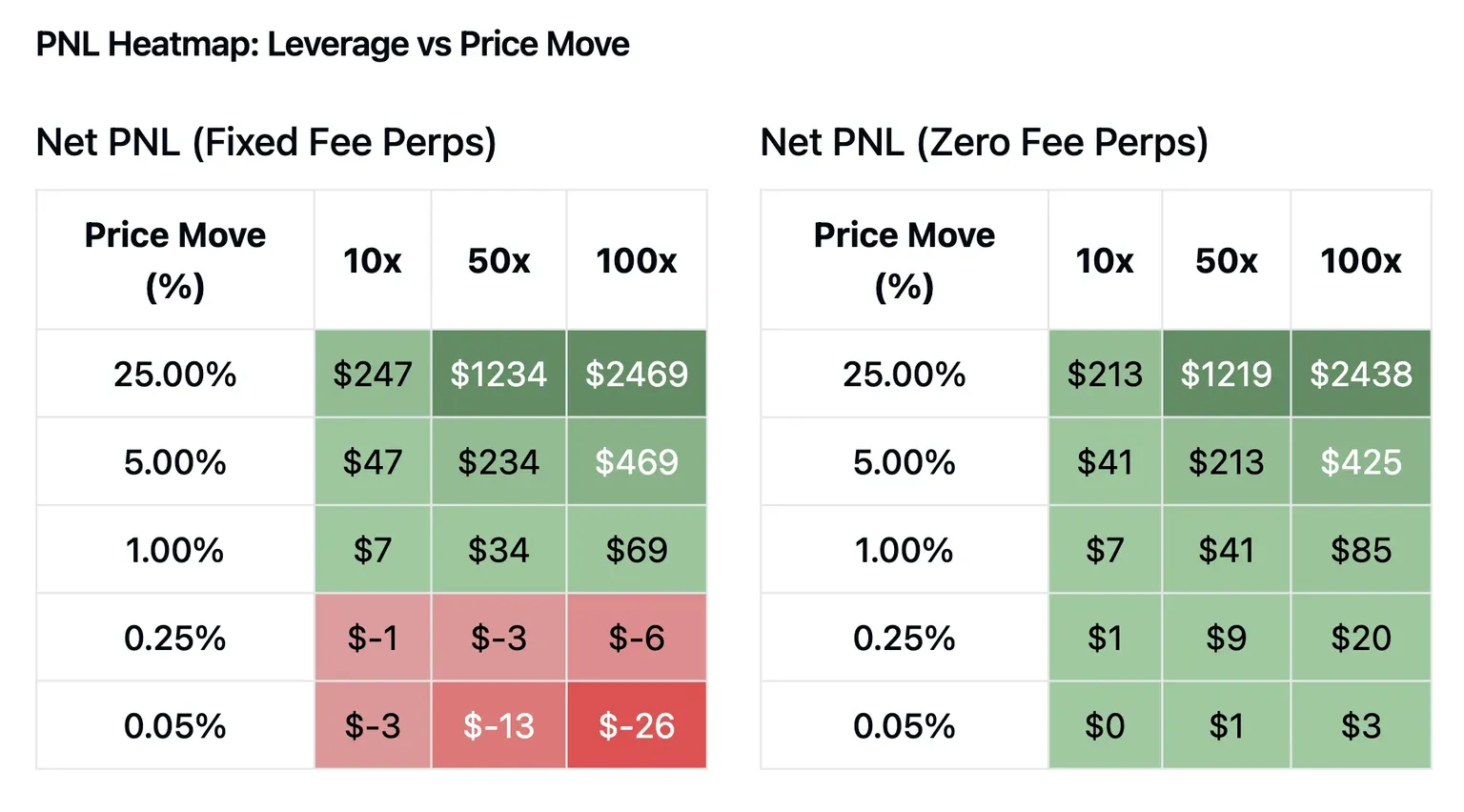

This gives traders two options: fixed-fee or ZFP. Neither is inherently superior. The optimal choice depends on factors such as volatility, leverage, and trade duration. Avantis has tested both models extensively through quantitative simulations.

Assumptions for comparison:

Spread: Both models apply identical dynamic spreads.

Duration: Trades assumed to last 7 days.

Collateral/Leverage: $100 collateral, leverage between 10x and 100x.

Underlying (BTC) price moves: Range of 0.05% to 25%.

Fee conditions:

ZFP: No fees on losses. For profitable trades, variable win-fees apply based on ROI, starting at 2.5% of gross PnL.

Fixed-Fee Perps: 0.06% open/close fee on position size for BTC. Annualized borrowing fee of 10% on position size.

Source: Avantis

Results show that fixed-fee models require significantly larger price moves just to reach profitability. In contrast, ZFP allows small price moves to remain profitable, with no collateral decay over time. This makes ZFP particularly attractive to loss-averse traders.

For longer holding periods, the advantage becomes even greater. Borrow fees in fixed-fee models continuously eat into collateral, while ZFP positions can be held indefinitely without liquidation prices changing. The only caveat is that ZFP requires a minimum of 75x leverage.

In short, Avantis provides traders with a meaningful choice between fixed-fee and ZFP models. Traders can select the option best aligned with their leverage level and risk preferences.

Source: Avantis

As with all perpetual DEXs, the central challenge in implementing synthetic futures is liquidity management. Avantis reduces LP risk significantly compared to earlier vault-based synthetic futures models by introducing multiple mechanisms that minimize slashing.

Currently, anyone can deposit USDC into the vault and earn fee-based yield. At peak levels, yields have exceeded 100% APY, and they currently remain around 25%, which is highly competitive compared to stablecoin farming yields that typically stay below 10%.

3.3.1 LP Vault Token: avUSDC

The LP vault in Avantis functions as a market-making vault. All user deposits flow into this vault and are converted into avUSDC, an ERC-4626-based token that is distributed to depositors. This represents a simplification of the previous structure, which was divided into junior and senior tranches based on depositor risk preferences. Under the new unified system, 100% of all trading fees, excluding liquidation fees, are distributed directly to avUSDC holders.

Previously, depositing into the vault was the entirety of an LP’s yield strategy. However, with the transition to avUSDC, capital efficiency for LPs has significantly improved. As LP positions have become liquid, several new advantages have emerged:

Composability: avUSDC can be integrated with various DeFi protocols. For example, it can be split into principal and yield tokens on Pendle, enabling speculative, hedging, or structured yield strategies.

Leverage: avUSDC can be used as collateral within Avantis. Users can deposit USDC, mint avUSDC, and then borrow USDC against it to build leveraged positions.

Capital Efficiency: In the future, idle capital within the vault will be deployed into external yield sources such as Maple USDC or Ethena’s sUSDe, securing additional revenue streams beyond trading activity. Through this, avUSDC evolves beyond a simple vault token into a composable money lego within the broader DeFi ecosystem.

3.3.2 Current State of avUSDC

The essence of DeFi lies in openness. Liquidity should not remain stagnant; it must move efficiently, compound, and grow. Through avUSDC, LPs no longer need to lock their liquidity in static vault positions. Instead, they can earn fees based on Avantis’s trading volume while simultaneously participating in broader DeFi opportunities.

Since the transition to avUSDC, the vault’s TVL has exceeded $100M, showing rapid growth. In the past, vault tokens that served market-making, liquidation, and insurance functions often experienced sudden slashing events or unpredictable PnL fluctuations depending on market conditions and position flow.

In contrast, Avantis’s avUSDC provides stable, fee-based yields. Its clear differentiator lies in delivering strong profitability through market-making while ensuring consistent returns for LPs via a multi-layered risk buffer structure.

Source: Avantis

As a result, avUSDC has established itself as the highest yield generating vault token on Base, maintaining an APY above 20%, with this performance reflected in its sharply rising TVL. Considering that Hyperliquid’s HLP vault and yield-bearing stablecoin-based structured vaults generally maintain around 10% APR, avUSDC stands out with yields in the range of approximately 25%.

Although each vault differs in its risk profile and exposure, it is clear that with its robust risk buffer, the consistent growth in Avantis’s perpetual trading volume, and the compounding effect of accumulated fees, avUSDC has secured one of the most competitive vault positions across the entire DeFi ecosystem.

Up to this point, we have examined Avantis’ oracle-based trading engine in detail. Since Avantis opted for an oracle-driven perpetual trading model rather than an orderbook design, the protocol needed to introduce multiple safeguards to compensate for structural risks. Nevertheless, this engine represents Avantis’ most strategic choice in targeting its market.

In other words, the primary reason Avantis adopted its current model was to solve the liquidity constraints of RWAs and enable smooth perpetual trading. This strategic decision stems from the inherent liquidity limitations of onchain equities. Unlike crypto-native perpetuals, RWAs cannot easily sustain stable bid-ask spreads in an orderbook model due to their structural features:

Difficulty of Securing Physical Assets: RWAs are backed by real-world assets, which means that market makers would need to pre-purchase and issue equivalent amounts of physical assets to provide sufficient float for market making. This creates significant capital burdens and makes it difficult to bootstrap initial liquidity.

Lack of Hedging Instruments: Market makers holding RWA spot assets lack effective instruments to take offsetting positions and hedge against price volatility. As a result, their inventory risk increases substantially, diminishing their incentives to participate.

Source: Avantis

To address these challenges, Avantis adopted synthetic RWAs, thereby overcoming liquidity barriers. As long as oracle price feeds are available, Avantis can offer perpetual markets for diverse RWAs without requiring direct spot asset custody. On this basis, Avantis now provides futures markets for major FX pairs such as JPY/USD and EUR/USD, commodities including gold, silver, and oil, and U.S. equities. It also supports leverage ranging from 50x up to 1000x.

The strong demand for global assets offered as synthetic RWAs on Avantis has already been verified through multiple indicators. Among these, interest in U.S. equities is especially notable. With indices like the NASDAQ-100 and the S&P 500 technology sector recording average annual returns of over 20% in the past five years, few asset classes have delivered such sustained growth. Moreover, when domestic equity markets stagnate for extended periods, investor preference for the growth potential of U.S. equities tends to strengthen further.

For example, Korean investors held nearly $100B in U.S. equities by the end of 2024, representing more than a 65% year-over-year increase. Top traded stocks among these investors include NVIDIA (NVDA), Tesla (TSLA), Apple (AAPL), and Microsoft (MSFT), all large-cap U.S. tech names.

Globally, the demand for U.S. big tech equities and index products remains strong. As of late 2024, foreign investors held around 20% of U.S.-listed equities. Meanwhile, about 30% of CME’s S&P 500 and NASDAQ-100 futures volumes originate from outside the U.S.. By country, Japanese retail investors allocated over 60% of their overseas equity trades to U.S. stocks in 2024, while investors in Singapore and Hong Kong also concentrated their foreign investment predominantly in U.S. equities and ETFs.

Source: Avantis

Avantis has seized this opportunity by offering perpetual markets for the most in-demand U.S. equities, most notably the Mag7 (Magnificent Seven) with leverage up to 25x. The Mag7 refers to seven leading U.S. big tech firms, including Microsoft, Apple, Google, and Amazon. Coinbase (COIN) is also supported, representing a highly demanded crypto stock.

By bringing these equities onchain, Avantis removes geographical barriers to global investment infrastructure and expands growth potential by tapping into proven demand. For traders, positions can be held indefinitely as long as funding costs are manageable, without the risk of forced expiry. With up to 25x leverage, traders can also optimize capital efficiency for event-driven strategies such as quarterly earnings announcements.

Could the onchain RWA perpetual markets pioneered by Avantis represent the final chapter of perpetual DEXs? At the very least, it cannot be ruled out that they will become one of the evolutionary paths through which DEXs absorb traditional financial infrastructure.

Indeed, the trajectory of onchain finance thus far supports this view. While it began with trading of crypto-native assets, onchain finance has steadily evolved to distribute real-world assets via blockchain rails, ultimately moving toward integration with traditional financial markets.

Yield-Bearing Stablecoins: Initially positioned as a store of value or payment medium distinct from volatile crypto assets, stablecoins have since evolved into yield-bearing instruments backed by low-risk real-world assets like U.S. T-Bills. This represents the absorption of traditional short-term liquidity products into blockchain rails.

Institutional Lending Protocols: Lending has also moved beyond crypto-collateralized loans. Protocols such as Centrifuge now support diverse institutional debt products, including trade finance and SME receivables, onchain, gradually integrating segments of the traditional institutional credit market.

Within this evolutionary flow, perpetual DEXs need not remain limited to leveraged trading of crypto assets. Real-world assets previously traded exclusively via traditional infrastructure can now be brought onto blockchain rails, creating a new trajectory of growth.

In summary, the evolution of perpetual DEXs may diverge along two distinct paths:

Continued refinement as crypto-native perpetual DEXs, focusing on digital assets.

Expansion into RWA perpetual DEXs, absorbing traditional financial market liquidity.

The latter aligns with the consistent historical progression of onchain finance.

Avantis is clearly at the forefront of this second trajectory. While token incentives initially played a central role in driving early inflows, following a successful TGE the key challenge now is to scale TVL, OI, and DAU by multiples while converting early participants into long-term active users.

In fact, Avantis has continued to show consistent growth across key metrics even after the TGE. Both trading volume and fees have steadily increased. This has led to higher distributed rewards, which in turn boosted demand for liquidity provision and ultimately resulted in a significant rise in TVL.

If this growth momentum continues, Avantis will further realize its vision of “One DEX, Infinite Possibilities” by evolving into a perpetual DEX that transcends asset classes and encompasses a diverse range of real-world assets, ultimately demonstrating the final evolutionary stage of perpetual DEXs.

Dive into 'Narratives' that will be important in the next year