While fixed income markets in traditional finance reach $600+ trillion, which is five times the size of equity markets, they barely exist in DeFi. This gap stems from the absence of standardized benchmark rates and extreme market fragmentation. Treehouse proposes DOR and tAsset as critical infrastructure to bridge this divide.

DOR (Decentralized Offered Rates) isn't just another price oracle. It's a new primitive designed to facilitate DeFi interest rate markets and institutional capital inflows. Through a structure where five stakeholder groups provide checks and balances, combined with game-theoretic incentives, Treehouse creates manipulation-resistant benchmark rates.

tAsset goes beyond simple liquid staking tokens, employing leveraged arbitrage strategies to create market efficiency. By incorporating tAsset as an economic security element for DOR, Treehouse strengthens DOR's position as a trustworthy benchmark rate.

Through its DOR and tAsset primitives, Treehouse aims to elevate DeFi market maturity to the next level, laying the groundwork for meaningful institutional capital participation.

Source: Treehouse

"Institutional adoption is coming" has been the industry's recurring promise for years. From the 2017 ICO boom through DeFi Summer 2020 to the recent Bitcoin ETF approvals, the crypto ecosystem has perpetually anticipated massive institutional capital inflows. But what's the reality? Despite record-breaking inflows through Bitcoin ETFs in H1 2024, institutional interest remains confined to relatively "safe" assets like Bitcoin and Ethereum. Expansion into DeFi or more complex on-chain financial products still seems distant.

The crypto ecosystem has long attributed institutions' reluctance to enter DeFi to regulatory uncertainty or technical complexity. However, when institutional investors actually attempt to explore DeFi beyond simple asset holding, the first wall they hit is the absence of core infrastructure they depend on in traditional finance.

For institutions to invest in specific products, "benchmark rates" like LIBOR or SOFR are essential. Risk management tools that institutions use daily, such as VaR (Value at Risk), duration analysis, scenario testing, all operate on the premise of standardized yield curves. Without these reference points, they cannot measure risk, evaluate performance, or establish hedging strategies.

Therefore, DeFi's most urgent challenge for accepting institutional capital is establishing credible benchmark rate measurement methods for these players. Treehouse is designed precisely with this focus in mind. This article will detail the problems arising from the absence of benchmark rates in the existing DeFi ecosystem and Treehouse's approach to solving them.

Users familiar with the DeFi ecosystem are accustomed to wildly different rates across protocols for the same assets. Various lending protocols like Compound and Aave offer rates based on their uniquely designed logic, resulting in significant rate disparities even for identical assets.

Such fragmentation would be unimaginable in modern traditional financial markets. What would happen if Citibank and JP Morgan offered deposit rates of 1% and 3% respectively—a 3x difference—for the same conditions? Banks, hedge funds, and institutional investors would immediately engage in massive arbitrage (e.g., borrowing from Citi, depositing at JP Morgan), causing rates to converge. Yet in DeFi, even this basic market mechanism fails to function properly.

However, until the 1980s, traditional finance's interest rate markets weren't much different from today's DeFi ecosystem. Each bank provided loans based on its own variable rates, with rates varying significantly by region and institution. Companies had to hire specialists to understand complex rate structures, and banks struggled to manage different risks. But as financial markets globalized and standardized from the late 1980s through the 1990s, IBOR-based benchmark rates like LIBOR (London Interbank Offered Rate), EURIBOR (Euro IBOR), and TIBOR (Tokyo IBOR) emerged, completely transforming the financial ecosystem.

Benchmark rates essentially publish the average rates at which major banks lend to each other daily. IBOR was calculated by averaging short-term rates submitted daily by member banks' representatives. Where previously each bank separately announced "our rate is 3%," the emergence of benchmark rates allowed everyone to use a common reference point like "LIBOR + 1%." This had an effect similar to countries standardizing measurements to the metric system. Once institutions had benchmark rates to reference, entirely new financial products became possible. Interest rate swaps are a prime example. If a company with a variable-rate loan worried about rising rates, they could hedge rate volatility through contracts with other parties.

Subsequently, numerous structured products emerged, such as mortgage-backed securities (MBS), credit default swaps (CDS), collateralized debt obligations (CDO), and the fixed income market, which was similar in size to equity markets before LIBOR, grew 5x over 40 years to reach an astronomical scale of $600+ trillion. This was miraculous growth started with a single standard.

So why can't DeFi achieve this efficiency?

On the surface, there's liquidity fragmentation. Each protocol's assets operate in independent pools, and moving assets between networks is more difficult than in traditional finance. Networks being public also means constant exposure to congestion and bridging risks. These technical issues are gradually being resolved with fast Layer 2 solutions and cross-chain protocols.

But the fundamental problem is the absence of a common standard—a benchmark rate—to create market efficiency. Even if liquidity fragmentation is solved, without standards to compare and evaluate rates across protocols, arbitrage cannot occur systematically. While retail investors can observe market conditions and seek high yields based on experience, this absence of standards presents an insurmountable barrier for institutions managing large capital. Institutional investors need three key metrics to enter DeFi:

First is a performance measurement baseline. In traditional finance, all returns are measured as excess returns over the risk-free rate. For example, earning 5% when U.S. Treasury yields are 4% means generating 1% excess return. But in DeFi, without this reference point, it's difficult to objectively judge whether a protocol's 10% APY is good or bad.

Second are risk management metrics. Institutional investors routinely use risk management metrics like VaR (Value at Risk), stress testing, and scenario analysis. The problem is these metrics operate on the premise of standardized yield curves, making such analysis impossible in DeFi, being a barrier for institutions requiring risk committee approval.

Last are hedging instruments. Consider Ethereum staking as an example. Current staking yields are around 3-4% annually, but this fluctuates with network activity. What if an insurer promised clients a fixed 3.5% return for three years, but staking yields drop to 3%? Traditional finance offers products like interest rate swaps to hedge such risks, but DeFi lacks these options.

These three elements are interconnected, all premised on standardized benchmark rates. LIBOR and SOFR enabled traditional finance to quantify risk, compare performance, and hedge volatility. Benchmark rates aren't just numbers—they're like the operating system for the entire financial ecosystem. DeFi currently lacks these reference points, structurally limiting institutional investor participation. Without benchmark rates, calculating portfolio risk-adjusted returns is difficult, and preparing risk reports required by regulators becomes impossible.

The problems of rate fragmentation and delayed institutional inflows due to absent benchmark rates were recognized early in DeFi, with several proposed solutions. Some attempted using centralized exchange lending rates or funding rates as reference indicators, but these only reflect individual platform supply and demand, falling short as ecosystem-wide standards. Moreover, benchmark rates managed by centralized entities inherently lack credibility, making them unsuitable as long-term solutions for DeFi.

The DeFi ecosystem has seen various attempts to solve the benchmark rate absence. Aggregators like DeFi Pulse and DefiLlama collected rates from multiple protocols to provide averages, with some projects applying more sophisticated methodologies like weighted or time-weighted averages. However, these approaches fundamentally just aggregated currently observable market rates. With large rate disparities persisting between protocols, simple averages couldn't reflect actual arbitrageable rates. More importantly, they lacked mechanisms to capture market expectations about future rates, like forward rates or term structures. DeFi had no way to capture the "market participants' future outlook" that traditional finance's rate swaps and futures markets provide.

In this context, Treehouse attempted an entirely new approach. Rather than simply observing current conditions, they implemented a mechanism using market participants' collective intelligence and economic incentives through game theory to predict the future while directly resolving market inefficiencies.

Treehouse chose a paradoxical approach to solve DeFi's fundamental problems: generating returns from market inefficiencies while simultaneously aiming to eliminate those inefficiencies. Their solution consists of two core elements: DOR, which creates decentralized benchmark rates, and tAsset, which actively exploits market disparities to directly enhance market efficiency.

2.1.1 Traditional Finance Benchmark Rate Failures and Treehouse's Solution

As we've seen, DeFi's biggest problem is the absence of reliable benchmark rates. Treehouse presents DOR (Decentralized Offered Rates) as the answer.

Source: Wall Street Journal

DOR's design philosophy originates from traditional finance's failures. The IBOR-based benchmark rates that served as global finance's standard for 40 years collapsed in a massive 2012 manipulation scandal. IBOR wasn't based on actual transactions but calculated from figures submitted by bank experts. Traders at major banks including Barclays were caught by financial authorities for years of collusion, submitting manipulated figures to benefit their trading positions or financial status. After the scandal, LIBOR management transferred to the ICE exchange, and the IBOR system was replaced with new standards like SOFR.

However, the replacement indicators had limitations. SOFR reduced manipulation potential by basing calculations on actual transaction data, but only provided overnight rates, making long-term rate predictions and future expectations difficult to incorporate—a fundamental limitation as a lagging indicator. Products needing long-term rates had to rely on futures data published by CME Group, a single institution, creating new centralization risks.

Treehouse established three design principles to fundamentally solve these traditional finance problems:

First is accuracy. Treehouse designed DOR so participants stake their capital as collateral, receiving penalties and rewards based on prediction accuracy, ensuring accurate predictions through purely economic incentives. Second is decentralization, allowing anyone with expertise to participate as panelists while transparently disclosing all calculations on-chain. Last is universality, making DOR's framework applicable not just to Ethereum staking rates but to all objectively verifiable rates including LP yields and real asset rates.

2.1.2 DOR's Structure

DOR ecosystem participants are divided into five roles, structured to check and balance each other while cooperating through economic incentives:

Operators: Entities building and managing the DOR system, setting rate types and parameters to predict. However, they depend on panelists' expertise for rate prediction accuracy and need referencer demand for system profitability.

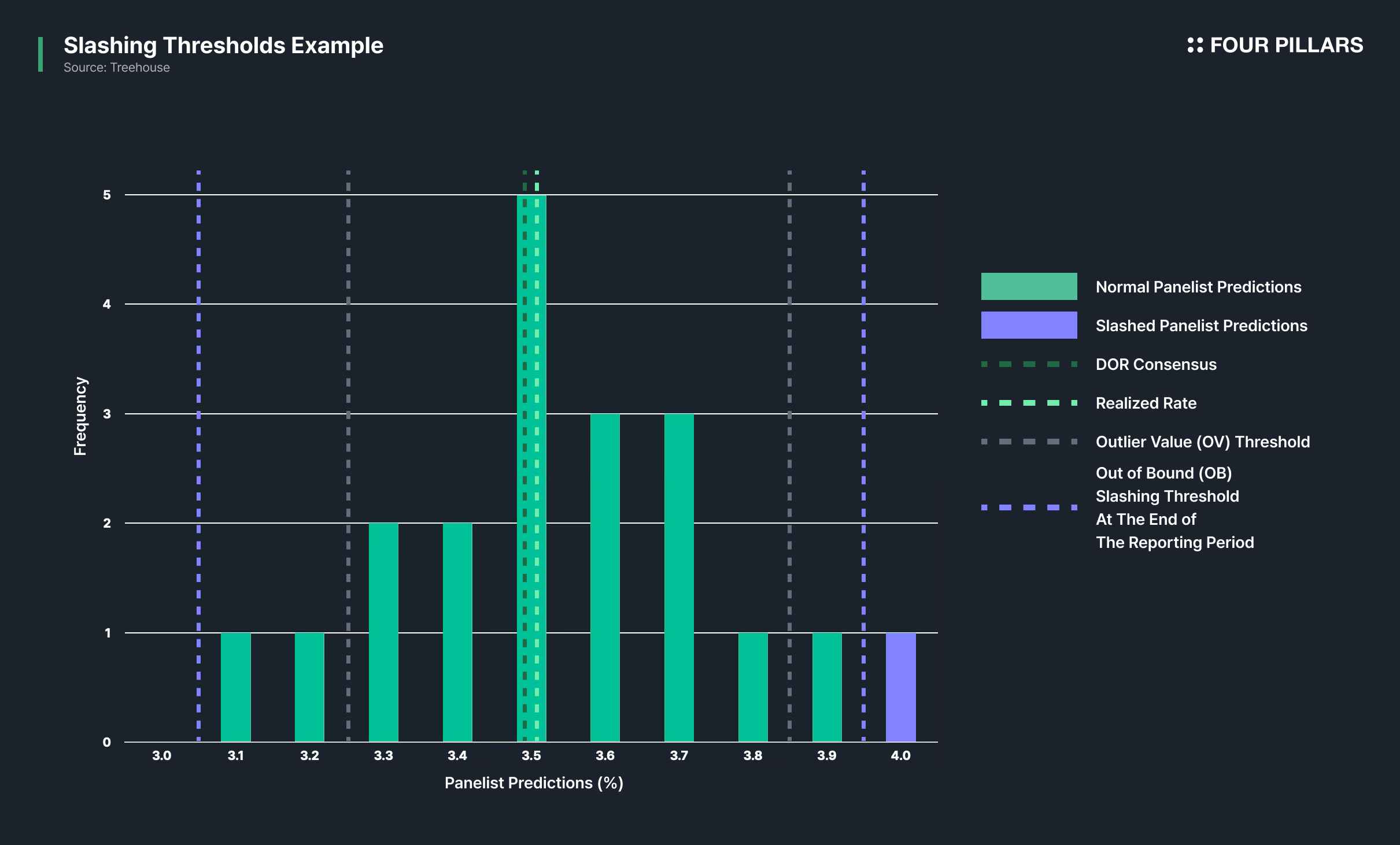

Panelists: DOR's core participants, the experts actually predicting future rates. They must prove confidence in their predictions with capital. Accurate predictions earn $TREE rewards, while incorrect ones result in losing staked assets. Panelists' past prediction records are public, serving as important indicators for delegators choosing whom to delegate assets to.

Delegators: Participants with capital but lacking rate prediction expertise. They indirectly participate in the rate consensus process by staking and delegating their tAssets (explained later) or $TREE to trusted panelists. Delegated assets strengthen DOR's economic security while enabling panelists to exert greater influence.

Referencers: Entities actually using DOR's rate data. They utilize DOR data for various purposes including financial product pricing, risk management, and research, paying usage fees.

End Users: Actual users of DOR-based financial products, who benefit from more efficient financial products without awareness of the complex mechanisms.

DOR is thoroughly determined by panelists' game theory. At designated daily times, panelists submit future rate predictions. Treehouse refines their highest/lowest values, then derives final consensus rates through mean and standard deviation calculations. Panelists succeeding with predictions within tolerance of the final consensus rate receive differentiated rewards based on accuracy, while those with out-of-range predictions receive penalties. Penalties increase exponentially for consecutive out-of-range predictions, giving panelists who accidentally submit inaccurate results opportunities to correct while strongly responding to malicious/persistent inaccuracy.

DOR also employs a multi-maturity structure, requiring panelists to simultaneously predict rates for multiple maturities like 1 / 7 / 14 / 30 day. Rewards are allocated more for longer maturities due to greater uncertainty in long-term predictions.

2.1.3 DOR Use Cases: ESR and Interest Rate Swaps

Treehouse presents various traditional finance fixed income products as potential DOR applications, choosing the Ethereum Staking Rate (ESR) curve as the first actual implementation.

Ethereum staking currently has over $100 billion in deposits, crypto's largest yield-generating mechanism. However, staking yields have a variable rate structure fluctuating block by block with network activity. While similar to traditional finance's variable rate bonds, DeFi critically lacks various derivatives to convert variable rates to fixed rates.

The ESR curve solves this problem. By synthesizing rate predictions for various maturities collected through DOR, it creates a complete yield curve for Ethereum staking. This doesn't simply show current staking yields but visualizes the market's expected future staking yields. Expected staking yields for 1 day, 7 days, and 30 days ahead become visible at a glance.

This serves the same role as treasury yield curves in traditional finance. Just as U.S. Treasury yield curves serve as reference points for entire financial markets, the ESR curve can become DeFi's "risk-free rate" baseline. All DeFi product yields can be expressed as spreads over the ESR curve, enabling risk quantification and comparison.

The ESR curve's true potential lies in enabling derivatives based on it. Interest rate swaps particularly deserve attention—they're traditional finance's largest and most important derivatives market, with over $600+ trillion in notional value currently traded. The basic concept of interest rate swaps is simple: parties receiving variable rates and fixed rates exchange their rates. For example, if an Ethereum staker wants a fixed 3.5% yield instead of variable staking yields, they can enter a swap contract with a counterparty wanting variable yields. Institutional investors like pension funds and insurers who must promise fixed returns to clients need to swap Ethereum's variable staking yields for fixed returns—ESR curve-based interest rate swaps enable this.

Source: Treehouse

Furthermore, the ESR curve can serve as the foundational mechanism for implementing various traditional finance fixed income products in DeFi. Treehouse presents the following products as implementable through the ESR curve:

Perpetual Notes: Bonds paying interest perpetually without maturity, continuing coupon payments unless issuers exercise call options. The ESR curve enables issuing perpetual notes linked to staking yields.

Swaptions: Options to enter interest rate swaps, granting rights to execute rate swaps under predetermined conditions at future points. These can hedge against rate volatility.

Forward Rate Agreements: Contracts fixing rates for specific future periods at current points. The ESR curve provides the baseline for calculating fair value of such forward rates.

Term Loans: Loan products with defined maturities and repayment schedules, enabling appropriate rate pricing based on the ESR curve. This will promote DeFi lending market standardization.

Interest Rate Swaps: As previously explained, the most basic derivative exchanging variable and fixed rates, with the ESR curve as the key element in swap pricing.

Callable Notes: Bonds where issuers have early redemption rights before maturity. The ESR curve provides essential information for valuing call options.

Total Return Swaps: Contracts exchanging underlying asset total returns (price changes + interest/dividends) for fixed or variable payments, useful for synthetic leverage or short positions on staking positions.

Floating Rate Notes: Bonds with interest rates periodically reset linked to ESR, preferred by investors during rate increases. In DeFi, these can be implemented as tokenized bonds directly linked to staking yields.

DOR goes beyond simple technical innovation—it's infrastructure enabling DeFi to compete with traditional finance. It relies on collective intelligence rather than centralized authority, uses transparent algorithms rather than opaque processes, and operates through economic incentives rather than trust. Isn't this exactly what benchmark rates have needed, not just for DeFi but for all financial ecosystems?

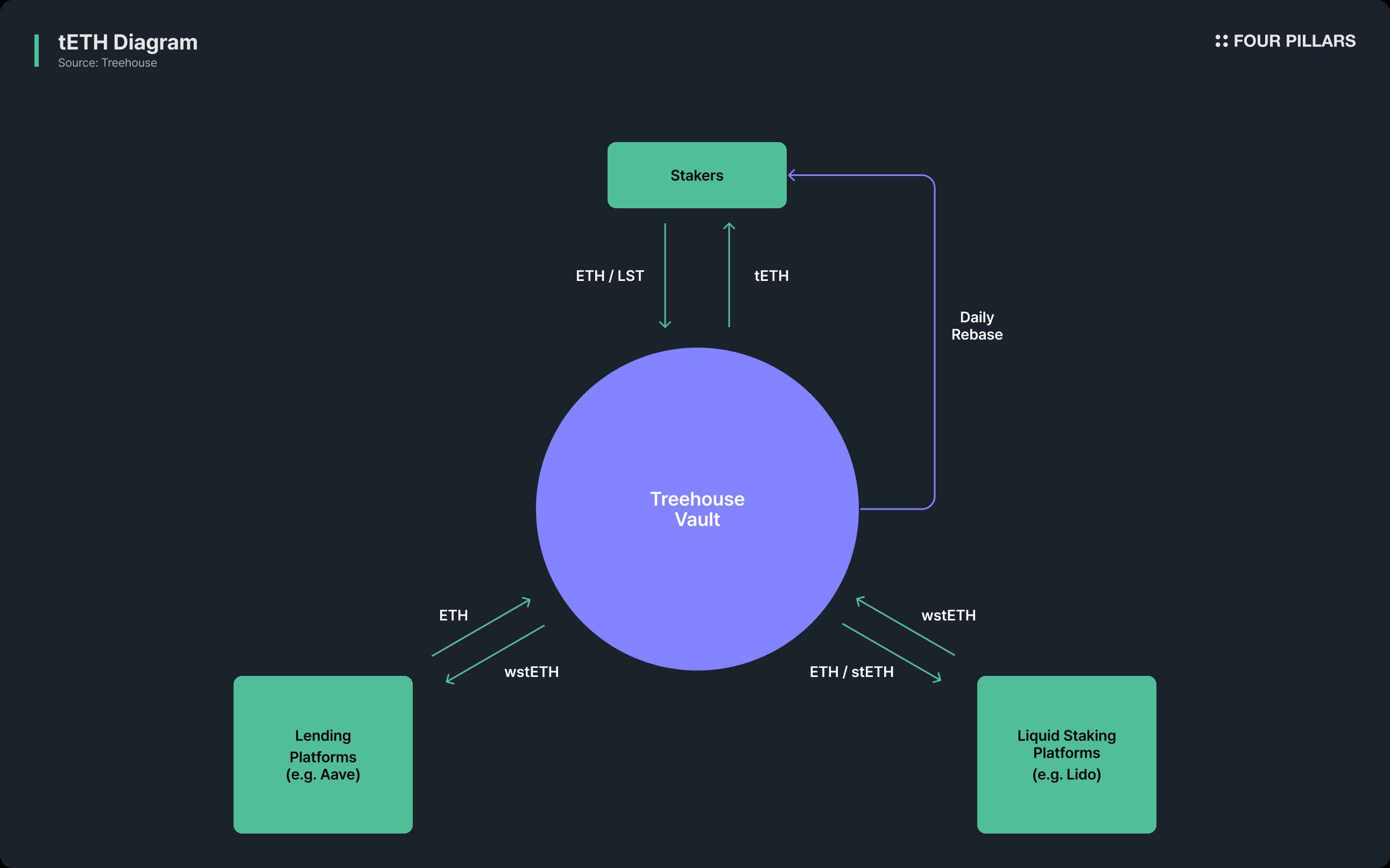

While Treehouse created DOR for DeFi's benchmark rates, tAsset is the liquid staking token providing necessary economic security for the DOR ecosystem. tAsset is similar to Lido's stETH or Rocket Pool's rETH in that users deposit Ethereum and receive tokens automatically accumulating staking rewards, but differentiates itself by pursuing additional returns through leverage.

2.2.1 tETH's Profit Generation Mechanism

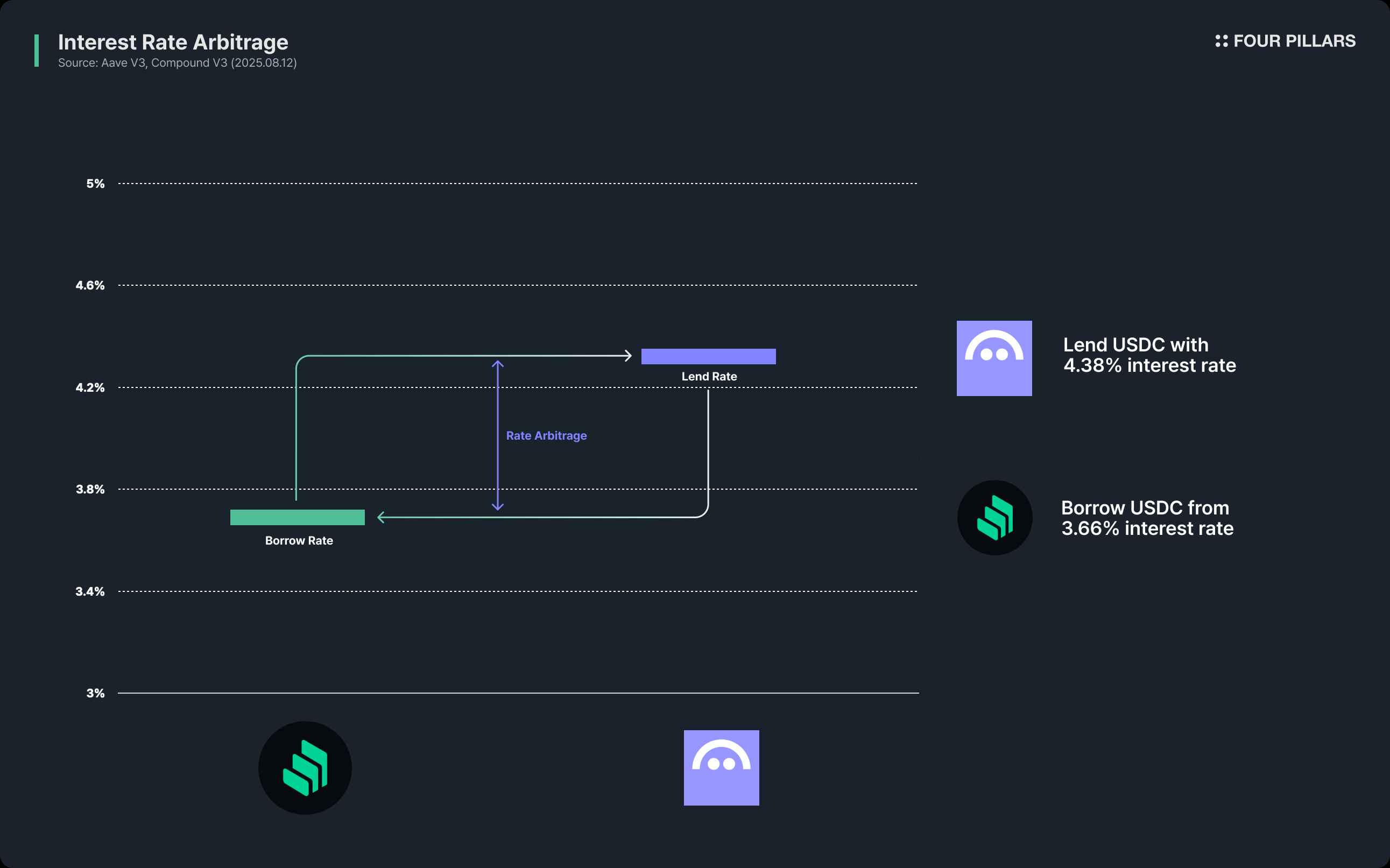

tETH, tAsset's first implementation, generates returns using a leveraged staking strategy utilizing Lido and Aave. The strategy's core exploits the spread between lending market borrowing costs and Ethereum staking yields, maximizing returns through a structure that cycles user-deposited ETH.

When users deposit ETH, Treehouse gives them tETH in return and stakes the deposited ETH in Lido to receive wstETH. The wstETH is then supplied as collateral to Aave, which is used to borrow ETH again. The borrowed ETH is staked again in Lido, and this process repeats until reaching the target risk tolerance level. The number of staking-borrowing iterations is determined by the lending platform's Loan-to-Value (LTV) ratio and the prices of wstETH and ETH at strategy execution.

Consequently, tETH's profit derives from the gap between: 1) staking yields from user-deposited ETH and 2) ETH lending rates using wstETH as collateral. The Treehouse team performed backtesting using historical data from June 9, 2023 to June 9, 2024, confirming tETH strategy could achieve approximately 0.6% excess returns compared to simple Lido staking.

2.2.2 Risks of tAsset and Mitigations

Since tETH's structure is based on recursive lending, repeatedly staking user assets and borrowing against liquid staking tokens as collateral, several risks exist as follows:

First is wstETH depegging risk. Historically, the worst depegging for wstETH was 6.7% in June 2022, but this was pre-Shanghai upgrade data when staked Ethereum withdrawals were fundamentally impossible. Post-Shanghai upgrade, arbitrage on staked Ethereum has been more active, and no depegging of that magnitude has occurred since. Treehouse set Aave's LTV at 80%, theoretically allowing avoidance of liquidation up to 15.79% wstETH depegging.

Second is interest rate spike risk from excessive Aave lending pool utilization. During Treehouse's backtesting period, borrowing rates exceeded staking yields 8 times, with 7 instances resolved within a day through market supply-demand adjustment. However, considering August 4-5, 2024, when high borrowing rates persisted for 2 days causing actual losses, tETH implemented a mechanism setting internal utilization floor limits to automatically repay portions of debt when market conditions deteriorate.

Additionally, Treehouse considered risk management as an initial implementation, currently setting tETH to perform the leverage process only once. As a safety mechanism for unexpected market conditions, not all wstETH is provided as collateral to lending platforms—some liquidity is reserved for emergency repayment, reducing tETH's risk.

2.2.3 tAsset's Role: DOR Ecosystem's Economic Security, and Beyond

Given tAsset's structure, it might seem like just another yield-maximizing liquid staking token variant. However, Treehouse aims to incorporate tAsset into the DOR ecosystem, creating incentives for DOR members to more actively participate in the DOR derivation process.

Similar to how EigenLayer provides economic security to AVS (Actively Validated Services) through restaking token delegation, Treehouse intends to grant DOR economic security through tAsset delegation.

tAsset holders can delegate their tokens to DOR panelists, enabling panelists to secure more economic security and exert greater influence in DOR. Additionally, tAsset holders can receive DOR participation rewards on top of leveraged staking yields provided by Treehouse.

This structure creates a virtuous cycle. As DOR provides more accurate and reliable benchmark rates, more financial products reference it, leading to increased panelist revenues. Consequently, users delegating tAsset also earn higher returns, forming a structure attracting more capital into tAsset.

Interestingly, as the tAsset market becomes more active, excess returns generated by tAsset paradoxically converge toward zero. Since tAsset fundamentally creates excess returns by exploiting gaps between lending markets and staking yields, as tAsset operates successfully and attracts more capital, liquid staking token prices adjust, gradually reducing arbitrage opportunities.

Treehouse views tAsset's excess returns converging to zero as a success indicator. This proves the market is operating efficiently. Treehouse's ultimate value lies not in generating returns but in building DOR, a reliable benchmark rate. As capital flowing into tAsset increases, DOR's economic security strengthens, resulting in a more trustworthy decentralized rate system.

Treehouse aims to evolve the DeFi ecosystem by introducing institutionalized financial system mechanisms into what resembles a dark forest. The blockchain ecosystem has been like a dark forest—difficult to navigate due to fragmented liquidity, inconsistent rates, and absent standards. Different protocols offer wildly varying rates for the same assets, and market participants move in their own ways without common standards. DeFi hasn't yet established the standards and conventions traditional finance built over time, becoming the biggest barrier preventing institutional investor entry. Treehouse positions itself as an observatory above the dark forest, showing these institutions the right path.

Just as LIBOR created the $600+ trillion fixed income market 40 years ago, DOR could be the key opening DeFi's new era. But this time, thousands of panelists rather than a few banks, transparent algorithms rather than opaque negotiations, and economic incentives rather than trust will move the market. The observatory Treehouse built above the dark forest has the potential not just to show the way but to reshape the forest itself. At the point where inter-protocol rates converge, markets become efficient, and boundaries between institutions and individuals disappear, we'll witness DeFi's next stage—one we've never encountered before.

Related Articles, News, Tweets etc. :

Dive into 'Narratives' that will be important in the next year