Pendle Finance aims to pioneer the funding rate market generated from perpetual futures exchanges through Boros. Considering that funding rates generate daily trading volumes of $150-200B, Boros, which enables trading by tokenizing funding rates, holds significant potential.

While Ethena has successfully integrated funding rates into DeFi through USDe and generates high APY, the protocol still faces limitations as sUSDe's APY shows steep volatility due to the high volatility of funding rates.

Pendle Finance proposes a means to hedge funding rate volatility through Boros. By tokenizing funding rates, Boros enables users to create hedging positions against funding rates or conduct margin trading, allowing them to implement diversified strategies based on funding rates.

As Boros interoperates with DeFi protocols that rely on funding rates as yield sources, such as Ethena, and perpetual futures DEXs, it presents an important opportunity to expand DeFi money legos to the next level. Given this potential, Pendle Finance's upcoming full-scale launch of Boros is highly anticipated.

Source: X(@MacroMate8)

While DeFi may appear to have temporarily moved away from the market mainstream due to memecoin cycles, it continues to innovate. For instance, using RWAs such as short-term bonds as collateral assets for yield generation has become a standard collateral structure. Now, stablecoins continue to expand their scale, and major DeFi protocols are actively interoperating with each other (e.g., SKY - Ethena - Pendle). Through this, DeFi continues to expand its market size and improve quality by focusing on collateral asset diversification, yield sustainability, and interoperability that serves as the starting point for 'Money Legos'.

Nevertheless, DeFi still has an untapped territory - the funding rate market from perp futures exchanges. Considering that futures exchanges generate daily trading volumes of $150-$200B in funding rates, incorporating funding rates into DeFi money legos as a method to expand current DeFi presents significant potential.

Pendle Finance has stepped forward as a player aiming to pioneer this market by proposing Boros. Boros, which aims to tokenize funding rates from futures exchanges, is expected to provide an appropriate solution particularly for DeFi protocols that depend on funding rates for their yield rates. Below, we'll examine how Boros combines funding rates with various DeFi protocols, focusing on interoperability with Ethena and exploring the DeFi problems Boros aims to solve and its potential.

Source: Binance Blog

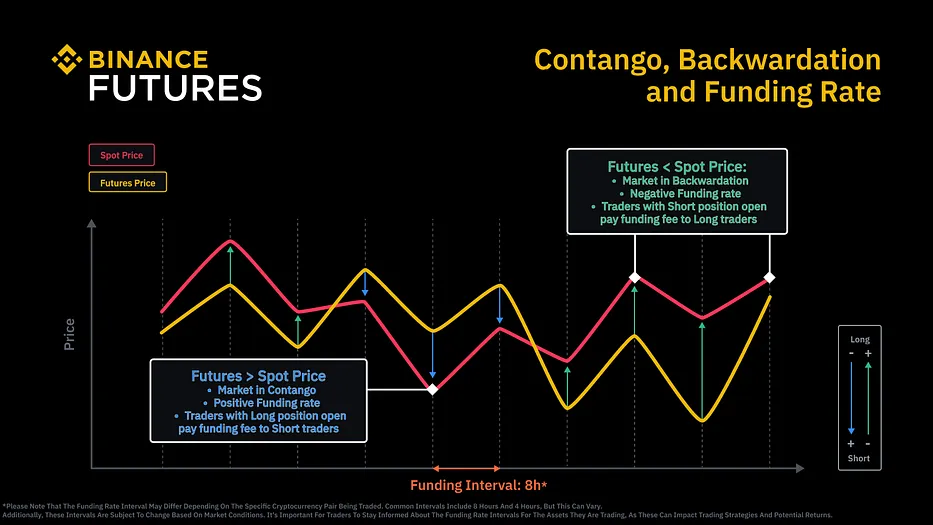

First, funding rate is a mechanism designed to narrow the price gap between spot and futures in perpetual futures exchanges, where price differences don't automatically converge to zero due to the absence of fixed expiration dates. Specifically, it narrows spot and futures prices by imposing penalties or premiums (funding fees) based on position ratios to balance long-short positions. This funding rate has functioned as a fundamental mechanism for operating perp futures trading and has served as a key mechanism in the crypto market, used for market indicators or basis trading strategies.

However, until now, funding rates have remained either segregated on off-chain CEXs or unable to combine with DeFi money legos created through combinations like lending or yield markets. Ethena Protocol has successfully integrated funding rates into DeFi, sourcing yield for their synthetic dollar asset USDe based on funding rates.

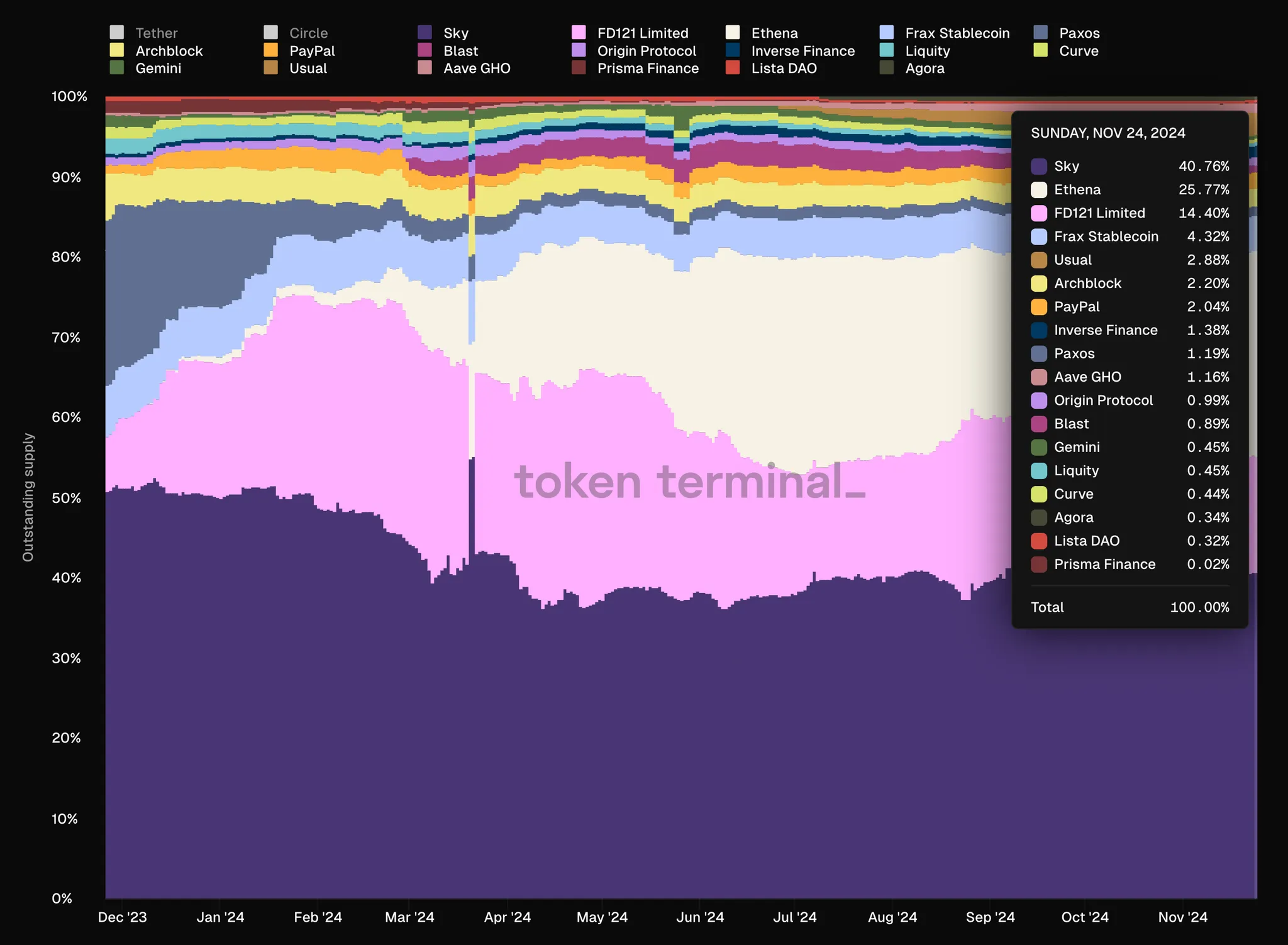

Source: Stablecoin issuers | Markets | Token Terminal

Ethena has grown rapidly by creating delta-neutral USDe. This is achieved through taking short positions on futures exchanges proportional to collateral assets and generating yield through funding fees. With its unique structure, USDe has garnered significant attention since launch, currently maintaining a high 25% market share among all issued stablecoins. Recently, it achieved $4B in TVL, proving its position at the forefront of the DeFi market.

Source: Ethena Labs

Ethena's rapid growth is substantially supported by its ability to provide holders of sUSDe (staked USDe) with an attractive yield rate of 25% APY. The yield generated by Ethena comes from various sources, ranging from basis arbitrage arising from short positions to relatively stable and sustainable yield created by managing yield-bearing stablecoins and LSTs as collateral assets for sUSDe.

Looking more closely, the yield that Ethena currently supplies to sUSDe comes from three main sources. First, it receives staking yields from Ethereum's PoS system by holding LSTs as collateral assets. Second, as mentioned above, it generates yield from funding fees arising from short positions. Finally, it maintains stable yield generation through stablecoin-derived revenues, such as earnings from Coinbase's loyalty program for holding USDC and borrowing fees from the Sky protocol.

In fact, Ethena has consistently faced questions about the sustainability of its funding rate-based yield rates since the protocol's inception. Critics point out a potential risk scenario in downtrend markets where short position ratios increase in exchanges, leading to negative funding rates. In such cases, the protocol would need to pay funding fees to long position holders, potentially eroding protocol profits and decreasing yield rates.

Source: Ethena Labs

Ethena appears to have addressed these concerns over time through various measures, including plans to collateralize BlackRock's BUIDL fund (U.S. Treasury-backed assets) based UStb, diversifying collateral assets, and maintaining sufficient reserves. As evidence, sUSDe's APY rarely fell below 10% over the past year. Considering these facts, Ethena seems to be maintaining adequate yield rates contrary to initial market concerns.

Source: Hedging | Ethena

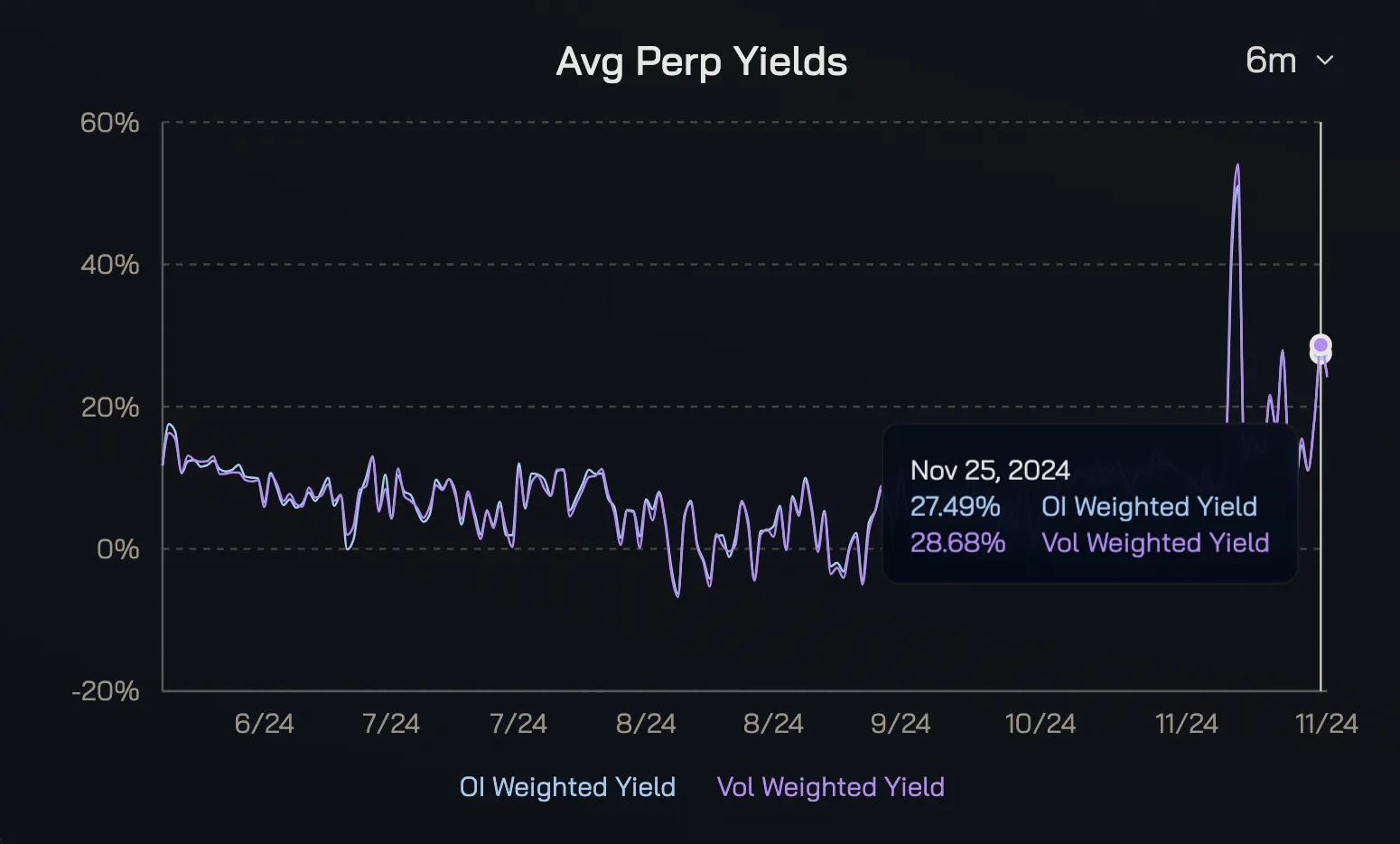

However, the next metric we should focus on in the Ethena protocol is APY fluctuation. While appropriate APY levels are maintained, the fluctuations are quite steep. This is because crypto asset price volatility leads to high volatility in perp futures exchange funding rates, and Ethena's yield structure depends on these funding rates. Even with collateral asset diversification for stable yield generation, there are limitations in guaranteeing consistent APY with low fluctuation due to the high-volatility funding rates serving as the yield source.

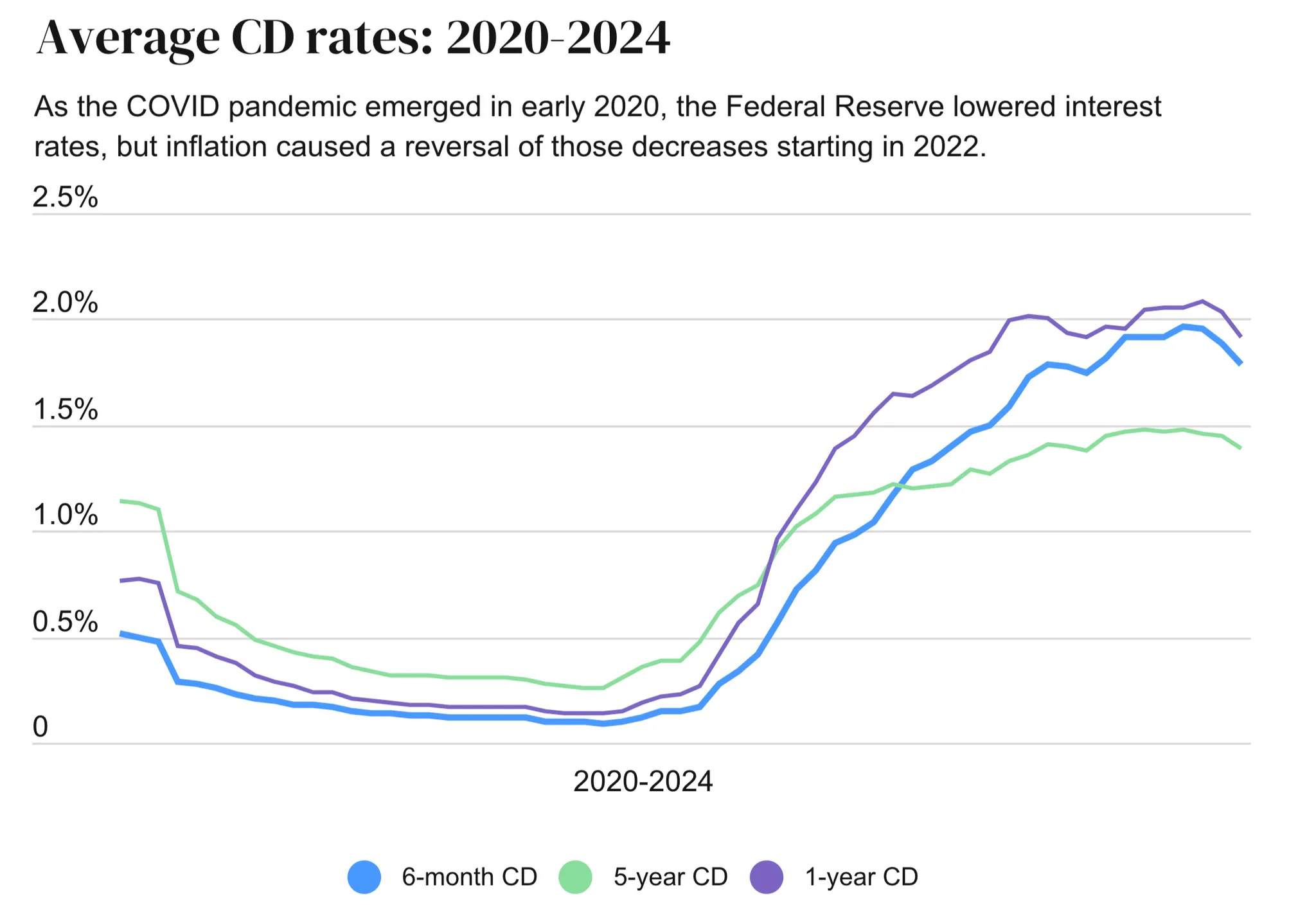

Source: Historical CD Interest Rates 1984-2024 | Bankrate

The high volatility of yield rates becomes even more apparent when compared to traditional finance rates. Minimizing yield rate volatility should be considered a crucial challenge to address, as it increases predictability in asset management for both DeFi protocols and users. Addressing this limitation becomes even more critical as DeFi works to either completely blur the boundaries with traditional finance or establish itself as a viable alternative.

To address the problems caused by high funding rate volatility, Pendle Finance proposes hedging tools through Boros. While detailed mechanisms haven't been disclosed, we can infer Boros's ideas through Pendle's core functionalities. These functionalities have primarily centered on mechanisms that enable trading of previously non-liquid assets.

Pendle Finance's basic functionality is to separate yield-bearing assets like LST, LRT, and stablecoins into Principal Tokens (PT) and Yield Tokens (YT). This separation allows for trading of yield from yield-bearing assets until a specific maturity date. This enables users to execute strategies such as arbitrage trading YT and PT based on predictions of yield-bearing asset APYs, or maximizing arbitrage fees by depositing discounted PTs as collateral assets in money market.

Source: Pendle Blog

Additionally, Pendle Finance has successfully found PMF by closely integrating with point-nomics conducted for airdrops in other projects. This approach adopted the YT, PT mechanism to enable strategies such as point arbitrage trading, leverage farming, or hedging risks from point farming, particularly integrating closely with pointnomics designed by restaking infrastructure like Eigenlayer and liquid restaking protocols like Ether.Fi. This enabled Pendle Finance to successfully establish itself as a leading yield trading market in the DeFi ecosystem.

Pendle Finance has found PMF with its unique yield trading functionality. The platform recently signaled its focus on funding rates as the next target market by announcing the launch of Boros. Of course, funding rates are just one of Boros's major target markets; ultimately, Boros aims to expand beyond the on-chain yields primarily handled by existing V2 to become a market for trading yields generated off-chain, like funding rates. Based on its mechanism for tokenizing funding rates as its primary target market, Boros is expected to provide two major utilities.

First, it can hedge risks arising from funding rates. According to Pendle, there are currently no reliable means to hedge large-scale funding rates. Boros addresses this by enabling users to create hedging positions against funding rate exposure through tokenized funding rates, allowing for more diversified strategies using funding rates. For example, they mention that Ethena Protocol's USDe holders can achieve fixed APY by hedging funding fee exposure based on Boros's tokenized funding rates.

Second, it enables margin trading on funding rates. Since Boros tokenizes funding rates, it can provide margin trading opportunities based on funding rate fluctuations. This allows traders to create additional arbitrage opportunities through funding rate-based strategies.

The greatest potential of Pendle Finance's Boros lies in its ability to incorporate the funding rate market, which generates $150-200B in daily trading volume, into the DeFi ecosystem, creating an opportunity to expand DeFi money legos to the next level. While the existing funding rate market has played an important role in the crypto market despite its size, it has remained disconnected from DeFi. If Ethena Protocol first brought funding rates to DeFi through basis yields, Boros aims to build money legos based on funding rates and enable arbitrage trading with funding rates themselves.

In my opinion, Boros's future developments could be expected to synergize with perp DEXs that are expanding their scale in the DeFi ecosystem. Recently, perp DEXs' daily trading volume has reached around $8.4B with platforms like Hyperliquid and dYdX establishing unique market positions through advantages such as computation speeds comparable to CEXs and long-tail asset listings.

Perp futures DEXs themselves continue to evolve in terms of trading environment and performance aspects with features like on-chain orderbook engines, pre-markets, and strategy pools. However, they remain disconnected from DeFi money legos built through interoperation with yield and lending markets. Boros presents possibilities for combining perp futures DEXs and itself in various DeFi interoperability and trading strategies. For example, it enables designing structured products derived from DEX funding rates and conducting arbitrage trades through tokenized funding rates by comparing rates across different perp DEXs.

Pendle Finance has successfully built a basic engine for on-chain interest through V2, covering staking, restaking, RWA, and BTCfi. Moving forward, Boros creates opportunities to capture all types of yields beyond on-chain, starting with funding rates. This makes Boros's upcoming launch highly anticipated, as it presents an important opportunity to expand not only Pendle Finance's growth but also the DeFi ecosystem as a whole.

Related Articles, News, Tweets etc. :

Dive into 'Narratives' that will be important in the next year