One of the clearest shifts in the crypto market is the rapid onboarding of real-world assets such as U.S. equities, Treasuries, and commodities onto onchain rails. This trend is driven by the diminishing likelihood of crypto assets outperforming traditional assets and by the weakening competitiveness of DeFi yields relative to traditional interest rates.

Gold has been one of the most in-demand global assets throughout 2025 due to the combination of rate cuts, a weaker dollar, and heightened geopolitical risk. As a result, the market for tokenized gold has expanded significantly and shows that onchain demand for gold exposure is real.

However, tokenized gold remains difficult to use as a productive asset in DeFi. Gold does not generate cash flow or debt, and it lacks mechanisms that allow it to function as a base asset in DeFi.

Theo’s thGOLD is a tokenized fund that tracks the price of gold while generating interest through a gold-lending structure. As RWA adoption broadens from Treasuries to assets such as gold and equities, thGOLD is well positioned to become a meaningful alternative for improving gold’s onchain utility.

Source: X (@PeterSchiff)

An interesting debate emerged some time ago. Peter Schiff, a well-known gold advocate, argued that Bitcoin is called digital gold, but the asset with actual intrinsic value is still gold. In his view, blockchain is simply a technological tool that improves gold’s mobility and settlement efficiency. Therefore, investors have no reason to prefer an asset like Bitcoin, which lacks intrinsic value, when tokenized gold can function as the real safe asset of the digital era. His view can be dismissed as extreme given his long-standing gold maximalism, but it does reflect a broader trend. Traditional financial assets are moving into crypto markets at an accelerating pace.

Looking back, it is not a strange question at all. If onchain rails offer instant global settlement, uninterrupted yield streaming, and 24/7 markets, why should they be limited to crypto-native assets? The strongest trend in the market is the movement of real-world assets such as equities, T-bills, and commodities onto blockchain networks. Two factors are driving this acceleration.

First, the market environment makes it increasingly difficult for crypto assets to outperform traditional real-world assets.

The era in which new tokens launched at low valuations and delivered triple-digit returns has slowed. As growth moderates, demand is shifting from crypto assets with weak fundamentals toward high-quality assets such as equities, gold, and index-based trading.

Real-world assets also offer greater predictability. They have decades of historical data shaped by inflation cycles, rate decisions, employment reports, elections, and corporate earnings. This allows market participants to better anticipate periods of volatility. It also means traders can apply predictive models and technical analysis with more consistency than in crypto markets.

The demand for onchain perpetual futures on equities reflects this shift. For example, TradeXYZ launched a perpetual futures market on the Nasdaq 100 using Hyperliquid’s HIP-3. The market now processes over $100M in daily trading volume and ranks among the top markets on Hyperliquid.

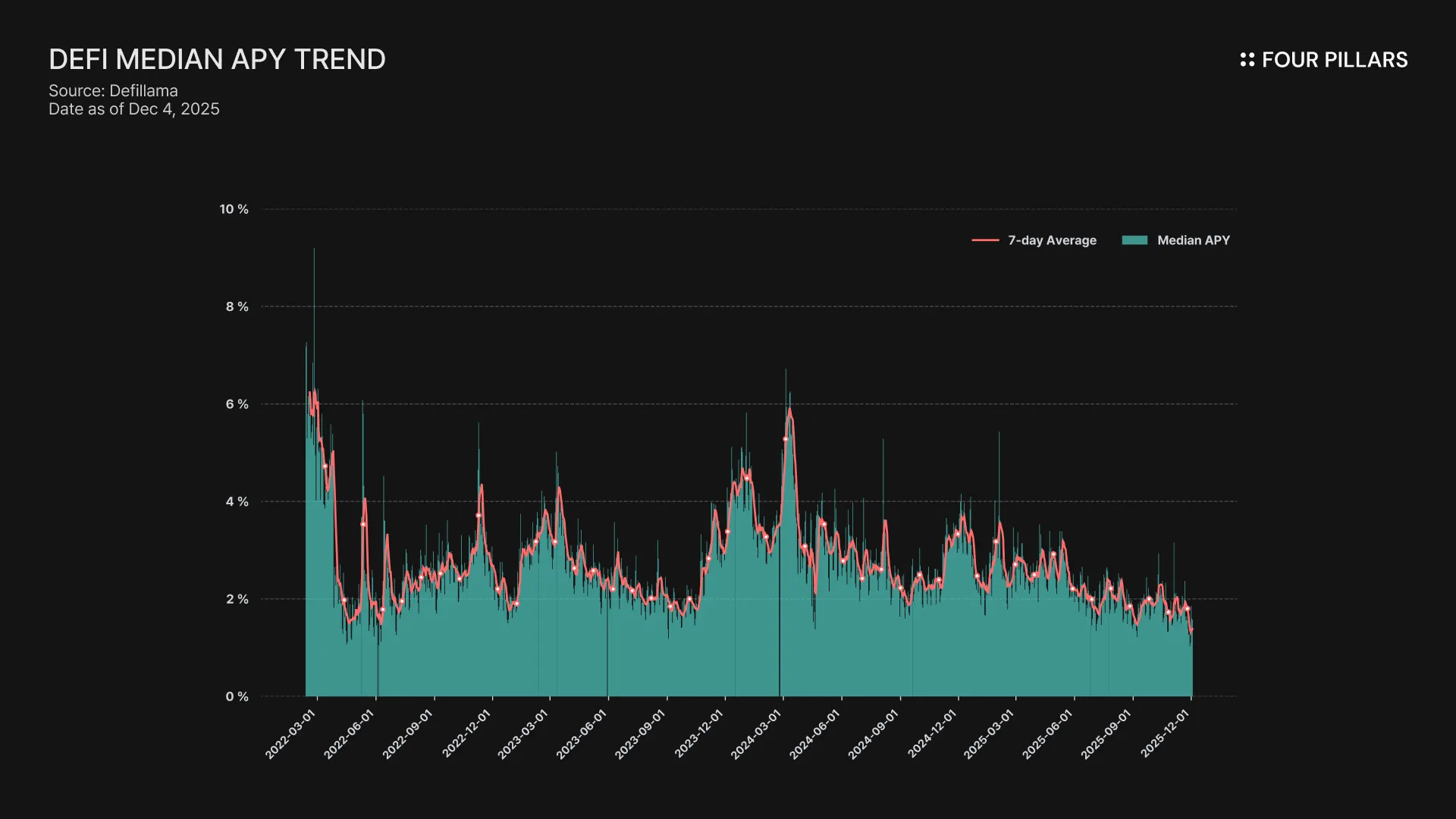

Second, current DeFi yields are not clearly competitive with traditional interest rates.

As crypto yields fell, onchain borrowing declined, trading activity decreased, and fee revenues dropped. Token incentives also weakened as a result. When money market APYs sit around 5% and U.S. Treasury yields remain near 4%, users have little reason to choose DeFi over the safety of government-backed returns.

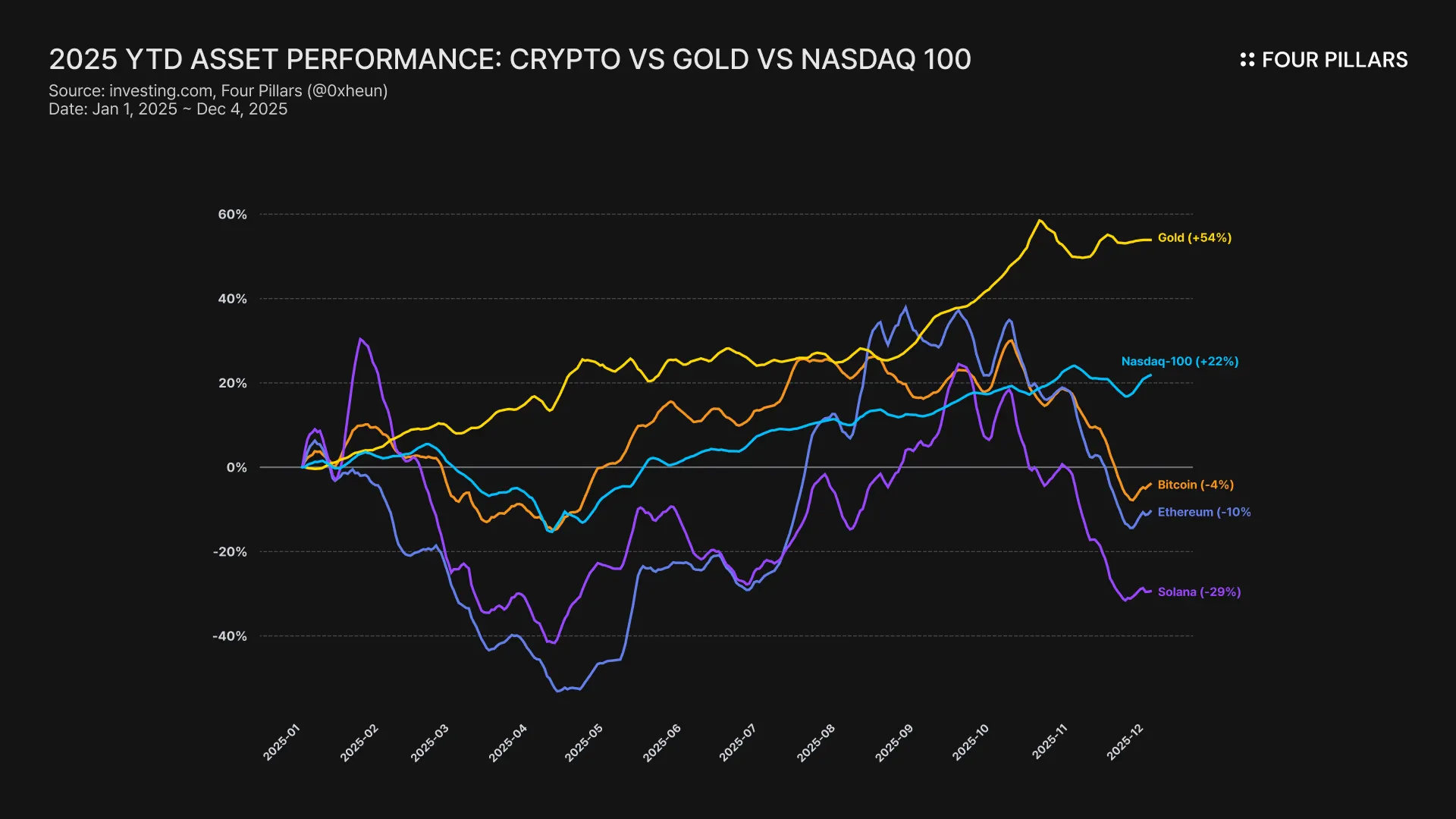

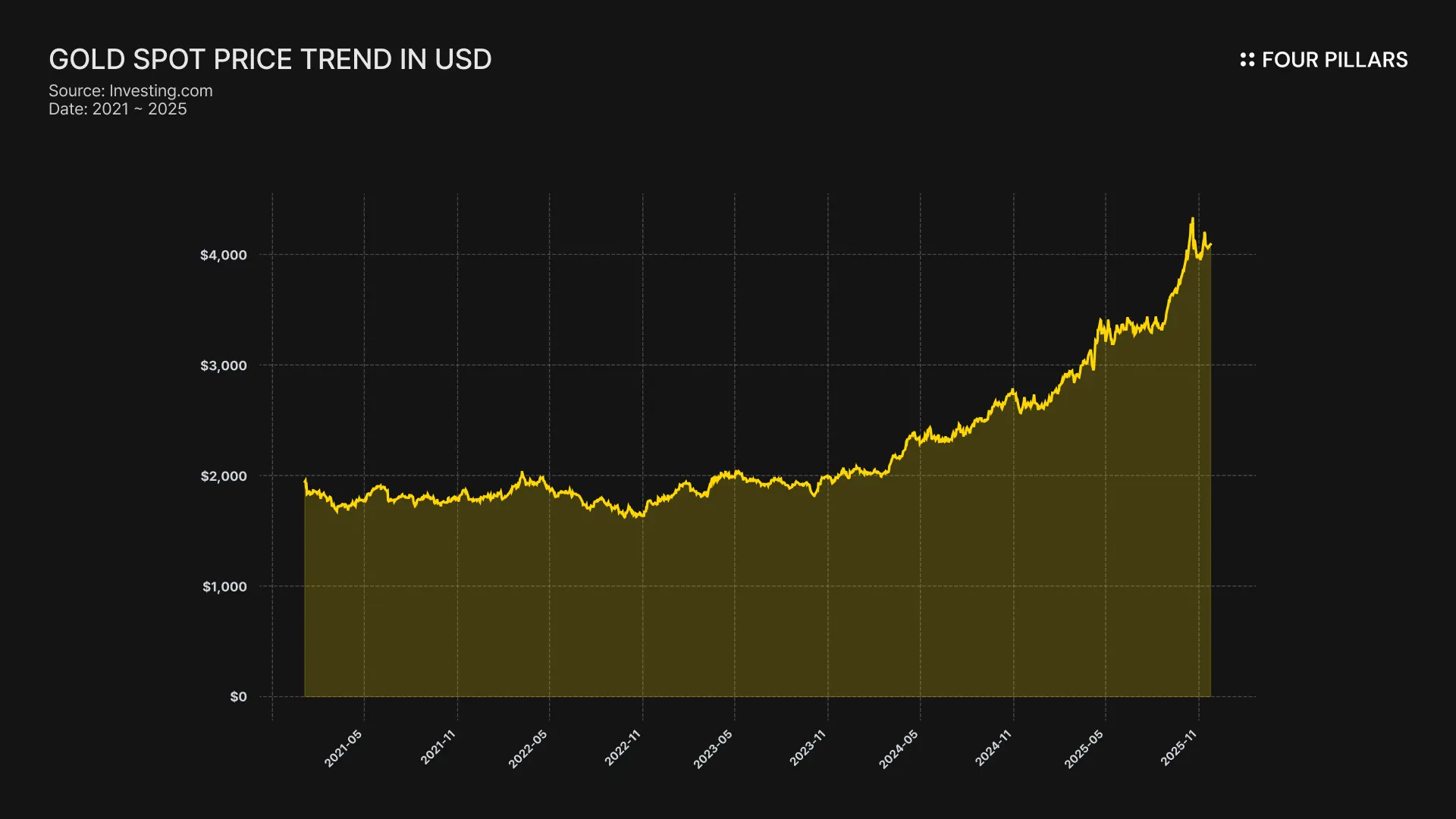

Demand for real-world assets is rising across crypto markets, and interest in gold is growing as part of this trend. Gold was one of the most sought-after global assets in 2025. Rate cuts began, the dollar weakened, inflation-hedge demand increased, and geopolitical tensions in the Middle East and Europe intensified. These factors created strong conditions for gold. The spot price of gold rose above $5,000 per ounce and increased about 80% year over year, reaching a new all-time high.

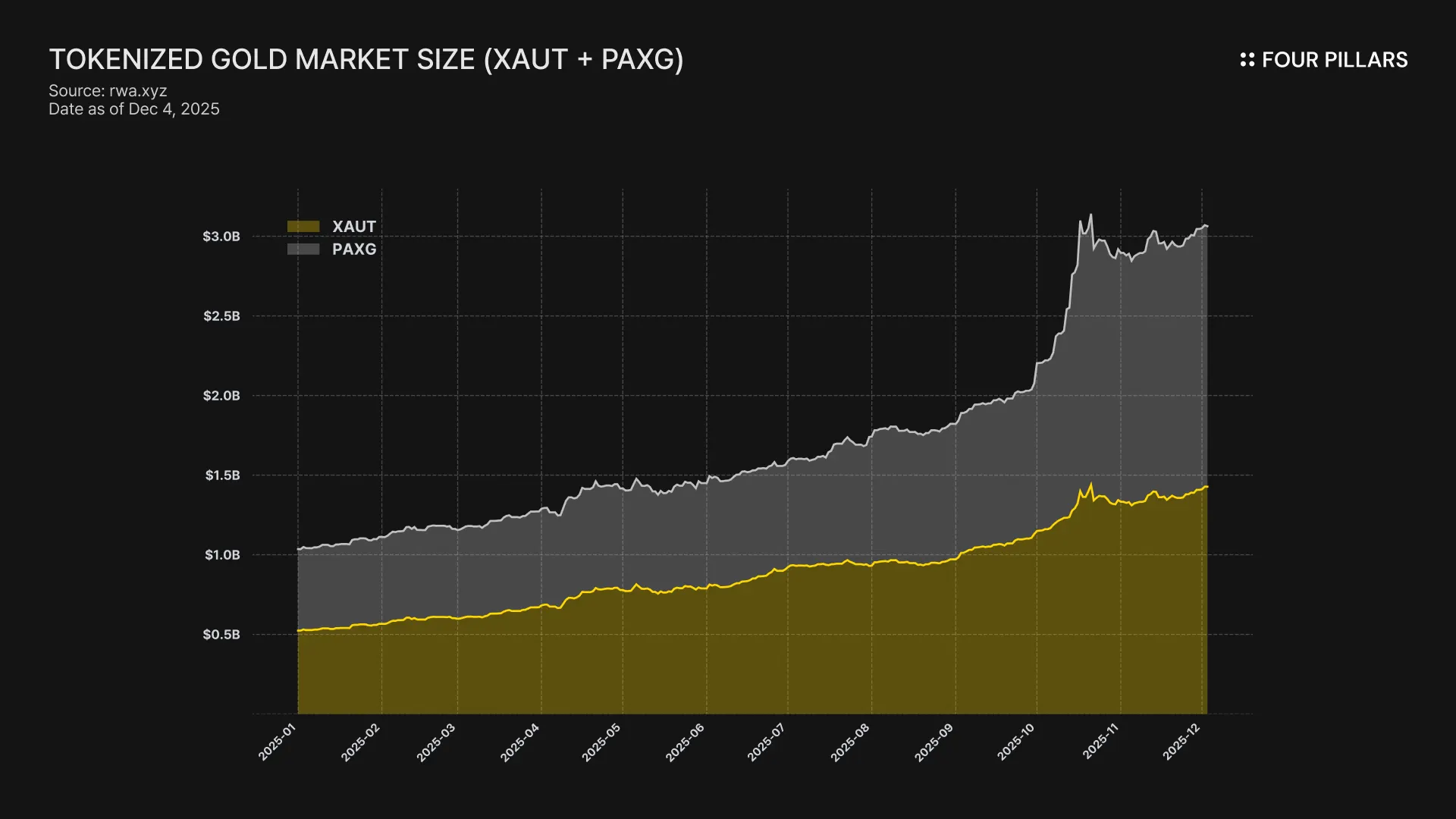

Until now, the most common way to gain gold exposure onchain has been through tokenized gold. The primary examples are Paxos’ PAX Gold (PAXG) and Tether Gold (XAUT), which hold physical gold in professional vaults in London and Switzerland and tokenize the ownership of that gold.

The combined market cap of PAXG and XAUT has more than tripled since the start of the year due to higher issuance and the rise in gold prices. This growth shows that tokenized gold is a valid tool for gold exposure in the same way that physical gold, gold certificates, and gold ETFs are used. It also demonstrates that clear onchain demand for gold exists.

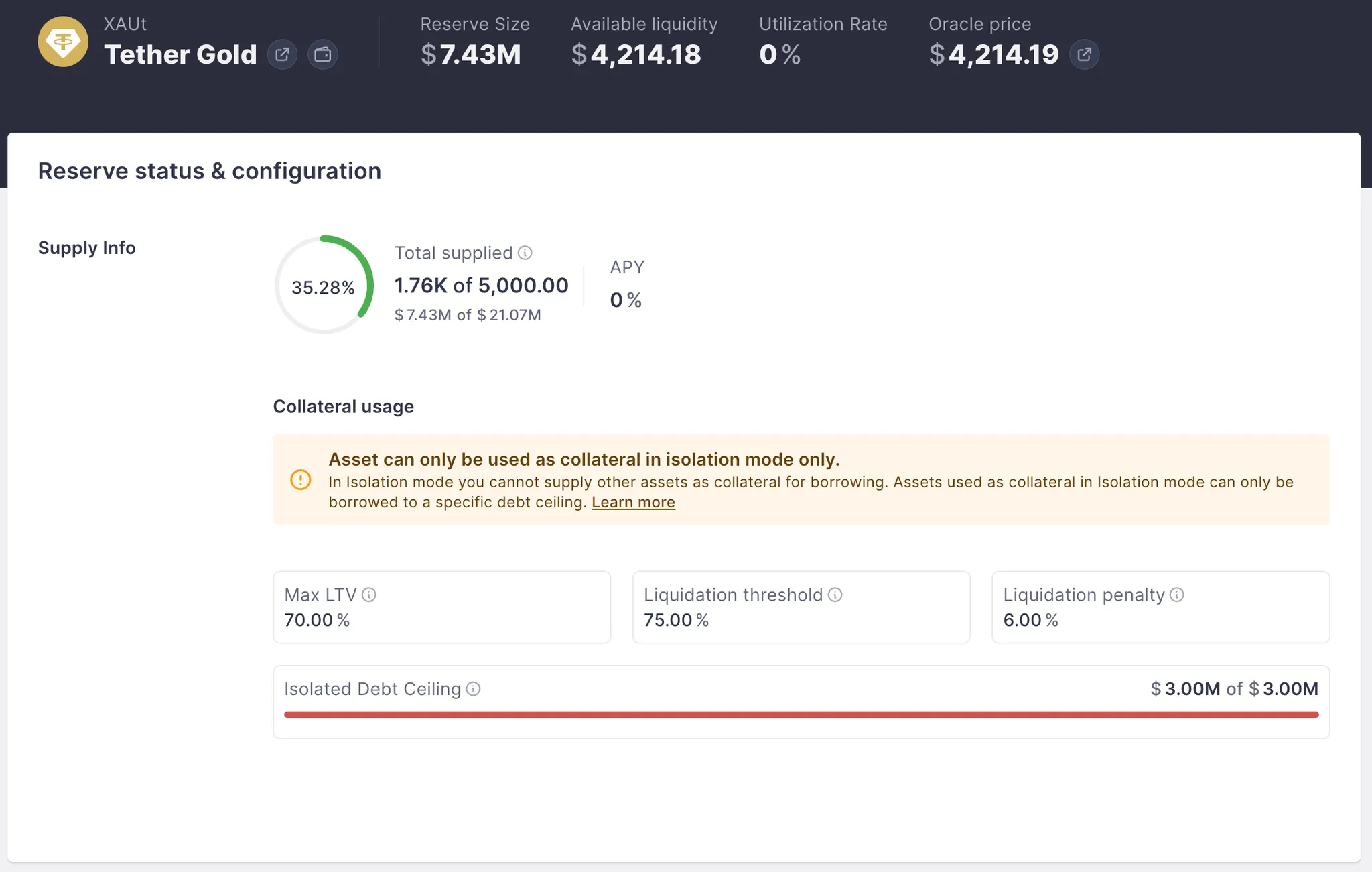

Source: Aave

Despite the demand, tokenized gold is still difficult to use as a productive asset in DeFi. Gold does not generate cash flow or debt, and it lacks mechanisms that allow it to function as foundational collateral within DeFi systems.

Today, the only path to earning interest on gold onchain is through lending markets. However, the only active example, Aave’s XAUT collateral market, is effectively inactive. The reasons are clear.

Conservative risk parameters: Aave’s XAUT collateral market shows zero utilization. Roughly $7.4M of XAUT is supplied, but the debt ceiling of $3M is already counted as potential bad debt and is fully occupied. This makes borrowing impossible. The pool appears active on the surface since deposits are allowed, but no loans occur, so no interest is generated. It functions as a stalled reserve rather than a productive market.

These conservative parameters reflect shallow order depth and lower trading volume for tokenized gold compared to assets like ETH or USDC. Aave cannot be confident that XAUT can be liquidated without slippage during a major market event. The oracle update frequency for XAUT is also lower. As a result, Aave classifies it as isolated collateral and keeps the debt ceiling low. Under these constraints, meaningful yield generation is impossible.

Lack of borrowing demand for gold: Lending yields come from borrowers, but leverage and borrowing demand for gold are low. ETH generates borrowing demand through staking yields, volatility-driven leverage trading, and its role as base collateral across DeFi. Gold, in contrast, is primarily a hedge and a store of value, with annual volatility around 10%. There is little incentive for users to borrow gold, pay interest, and take liquidation risk simply to apply leverage to an asset designed for stability.

In summary, gold is not well suited for DeFi’s traditional interest-bearing model. It functions mainly as an exposure or hedge asset rather than a productive one. To create yield from gold, alternatives beyond general-purpose money markets are required. Gold-backed structured credit products or hybrid models that combine onchain and offchain lending provide more viable paths.

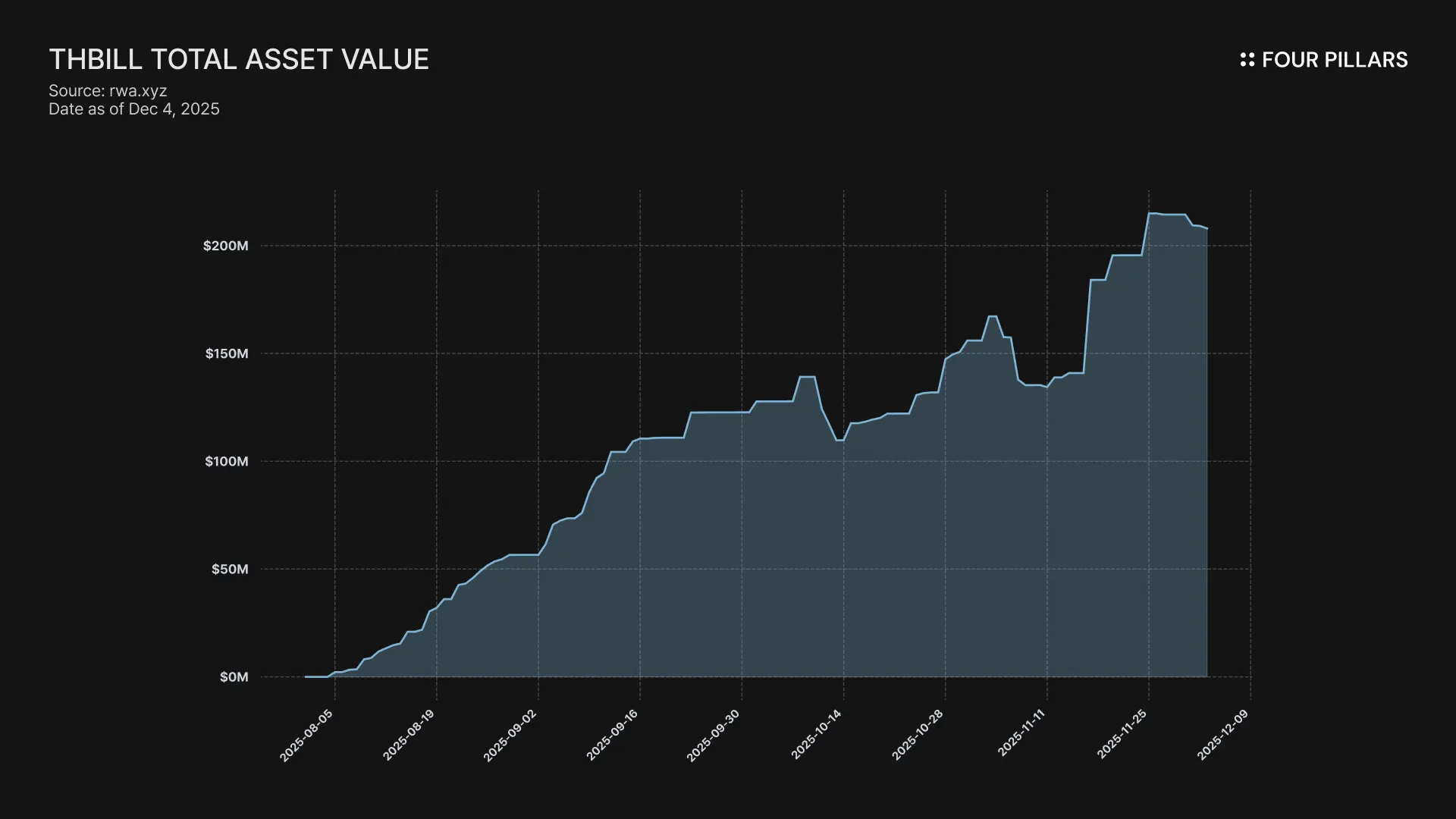

Source: RWA.xyz

Given this backdrop, Theo’s thGOLD offers a meaningful alternative. thGOLD is the second RWA product released by Theo and builds on the success of thBILL, a T-bill-based token. It provides exposure to gold price movements while also delivering interest income.

Since launch, thBILL has seen rapid growth through integrations with Morpho, Pendle, and other major protocols. The Stable network, which focuses on USDT, allocated one $100M into thBILL, pushing total issuance above $200M. Its market capitalization now ranks among the largest T-bill-backed tokens. This growth provides the foundation for evaluating Theo’s next asset, thGOLD.

Source: X (@Theo_Network)

thGOLD is a tokenized fund that tracks the price of gold while generating yield. thGOLD is different from tokenized gold products like XAUT or PAXG, which are pegged one-to-one to physical gold. Instead, thGOLD represents shares in an institutional gold lending fund. In other words, it reflects stakes in a private credit fund that operates against gold as collateral, rather than direct ownership of vaulted gold.

thGOLD is backed one-to-one by MG999, a tokenized gold fund issued by Libeara under Standard Chartered, FundBridge Capital, and Singapore-based gold merchant Mustafa Gold. Although stablecoins or thBILL may temporarily appear in the backing during mint or redemption processes, the structural backing of thGOLD is always MG999.

The core of MG999 is a collateralized loan portfolio denominated in gold. The fund lends gold to companies in the precious metals industry, such as jewelers, refiners, and mining firms. These companies post collateral for each loan, which keeps risk relatively low because collateral can be recovered in case of default.

MG999 generates interest from the borrowing companies. It functions like a traditional private credit fund in which the interest paid by borrowers becomes yield for the fund. This yield is then distributed to investors. As a result, thGOLD provides both gold price exposure and interest income.

Why do precious metals companies borrow gold? Although the concept is unfamiliar to most investors, gold lease has been used in the industry for decades. Companies have two clear incentives.

Risk hedging: A company borrows gold in ounces, manufactures and sells its products, and repays the same weight of gold plus interest. It does not buy gold with cash. It borrows gold or cash denominated in gold. This structure naturally removes gold price risk.

The company’s liability is measured in weight, not price. If gold prices rise, the selling price of their products rises as well and offsets the repayment. If gold prices fall, the company can purchase cheaper gold to repay the loan. The only requirement is to repay the borrowed weight. Therefore, gold price fluctuations do not affect operating profitability. Companies can maintain stable production without exposure to gold price volatility.

Working capital efficiency: Buying gold with cash forces companies to lock large amounts of capital into inventory. That cash cannot be used for operating expenses until the gold is sold again. Gold lease solves this problem. Companies obtain the gold needed for production while keeping cash available for manufacturing, inventory management, payroll, and other operational needs.

Gold has historically been one of the heaviest and least efficient assets. It is physically heavy, costly to store, and difficult to mobilize. Gold is a strong store of value, but it has struggled to align with DeFi markets where capital efficiency and composability are core features.

In this context, Theo’s attempt to expand the gold-lending market onto onchain rails represents meaningful progress. Gold lease has long been a specialized profit center for bullion banks and has typically taken the form of private lending agreements that remain inaccessible to most investors. thGOLD opens this market through an onchain, transparent fund structure and improves the practical utility of onchain gold.

Preparations to bootstrap thGOLD are already in place. thGOLD will support fast bridging across chains through LayerZero OFT at launch, and liquidity will be available on major venues such as Uniswap and Hyperliquid. Continuous participation from professional market makers, including the Theo team, will help secure stable initial liquidity.

The most important milestone is the integration of thGOLD with DeFi protocols that can scale the utility of its interest-bearing structure. thGOLD can improve capital efficiency through lending integrations on platforms such as Morpho and Euler, where it can be used alongside USDC and thBILL as collateral. A Pendle integration will also allow users to take positions on thGOLD yield and accumulate Theo points.

In 2025, Treasuries became firmly established onchain. The RWA market is now beginning to expand from Treasuries to assets such as gold and equities. In this transition, thGOLD is well positioned to become the next major product following the success of thBILL. Whether it achieves this role will be an important test for Theo over the course of the year.

Dive into 'Narratives' that will be important in the next year