Investors all have their own risk/reward profiles, which has led to the creation of various structured products. Not only in traditional finance but also in the on-chain ecosystem, services like Pendle Finance have grown rapidly by enabling the separation and trading of principal and interest on yield-bearing tokens.

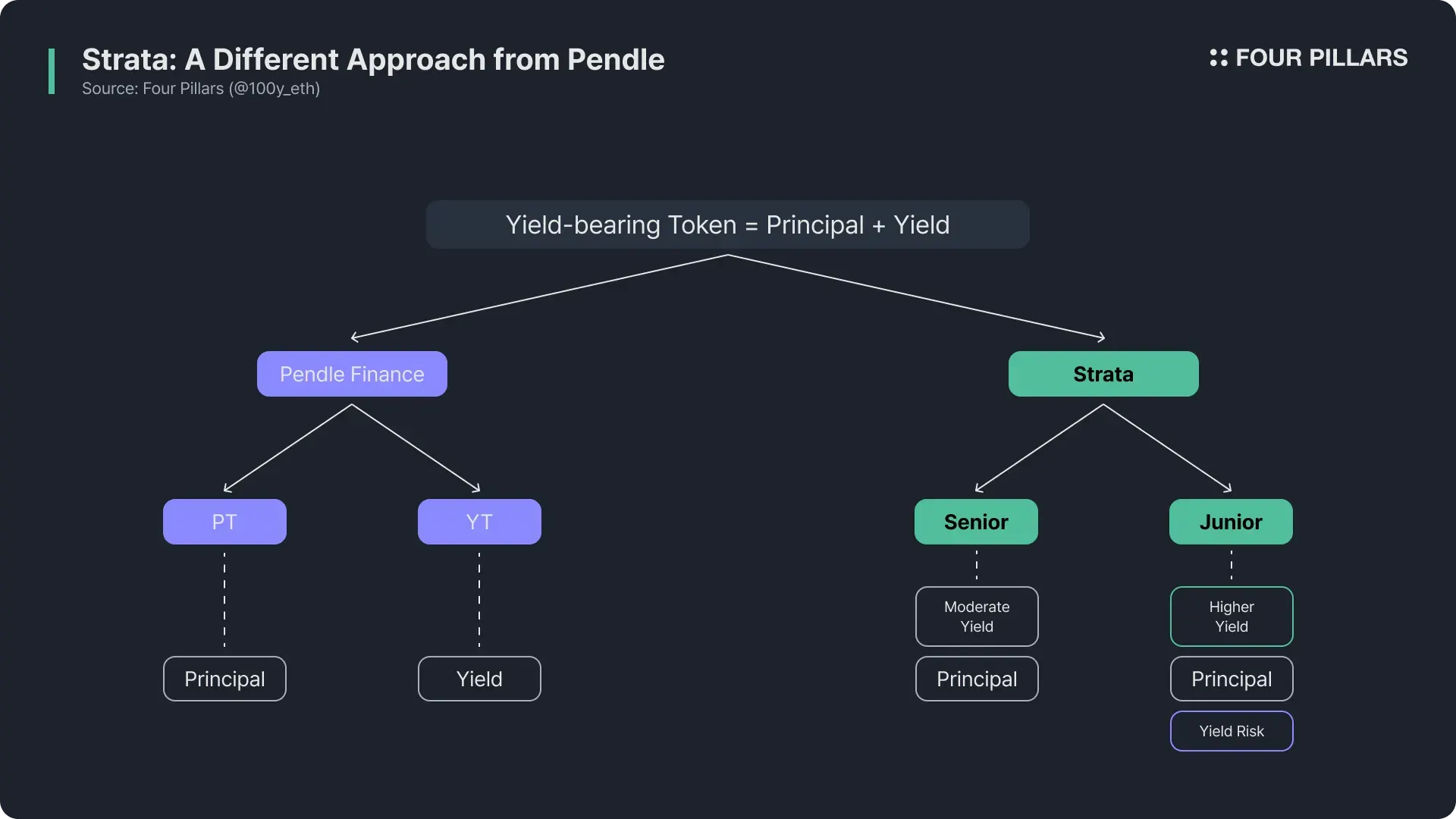

Strata provides structured products for yield-bearing tokens with an approach similar yet fundamentally different from Pendle Finance. While Pendle simply separates principal and interest, Strata divides yield-bearing tokens into senior tranche tokens and junior tranche tokens based on interest rate volatility risk.

Senior tranche tokens have the advantage of lower risk from interest rate volatility since the downside of interest income is floored while retaining the upside, but the disadvantage is that they cannot fully capture the upside in a high interest income environment. Conversely, junior tranche tokens can capture greater upside in interest income compared to regular yield-bearing tokens, but the disadvantage is that they can suffer losses in a low interest income environment.

Strata is initially applied to USDe, but it also has the scalability to be applied anywhere yield-bearing tokens and strategies exist, such as Hyperliquid HLP, Lighter LLP, and other DEX MM vaults, basis and other delta-neutral yields.

What is the essence of investing? At its core, investing is a bet on the future value of an asset. While it would be ideal if everyone could accurately predict the future, the reality is that no one can. Investors inevitably make different judgments about the future value of assets, and from this divergence arises the struggle to maximize returns relative to risk.

Unfortunately, basic traditional assets such as stocks, bonds, and loans alone cannot satisfy the wide spectrum of investors’ risk reward preferences. As a result, financial institutions have designed and offered structured products based on underlying assets to meet the needs of investors with diverse risk reward profiles.

The most well-known structured products include ABS, MBS, and CDO. ABS pools together various loan receivables with cash flows and issues securities backed by this pool. These securities are then divided into several tranches and sold to investors with different risk reward preferences. Typically, ABS and similar loan-backed securities are split into senior tranches and junior tranches.

Senior tranche: A tranche with priority in principal repayment. Because it is lower risk, the returns are relatively lower.

Junior tranche: A tranche with lower priority in principal repayment. Because it carries higher risk, it offers higher returns compared to senior tranches.

The most representative example of ABS is MBS, which uses mortgage loans as its underlying assets. CDOs, on the other hand, are created by pooling together various ABS and restructuring them into new securities. This process of pooling different underlying assets and dividing them again into tranches provides investors with diverse types of risk reward profiles that match their different investment preferences.

Today, countless financial activities are taking place not only in traditional finance but also on blockchains. Naturally, this has created demand for structured products based on underlying assets, and Pendle Finance has emerged as a frontrunner.

Pendle Finance is a protocol that allows investors to split and trade the yield portion (YT) and the principal portion (PT) of yield-bearing tokens. For example, with sUSDe, investors would normally just hold it to receive both principal protection and interest. But with Pendle Finance, they can purchase YT-sUSDe to hold only the rights to interest, or purchase PT-sUSDe to hold only the rights to principal.

One of the key drivers of Pendle Finance’s rapid growth has been point programs. Recently, it has become almost an industry standard for new projects to distribute points to holders of yield-bearing tokens in preparation for future token airdrops. Because investors value these points differently, those who believe the future value of points will be high tend to buy YT to maximize exposure to interest, while those who believe the future value of points will be low tend to buy PT to protect principal and receive stable, high interest.

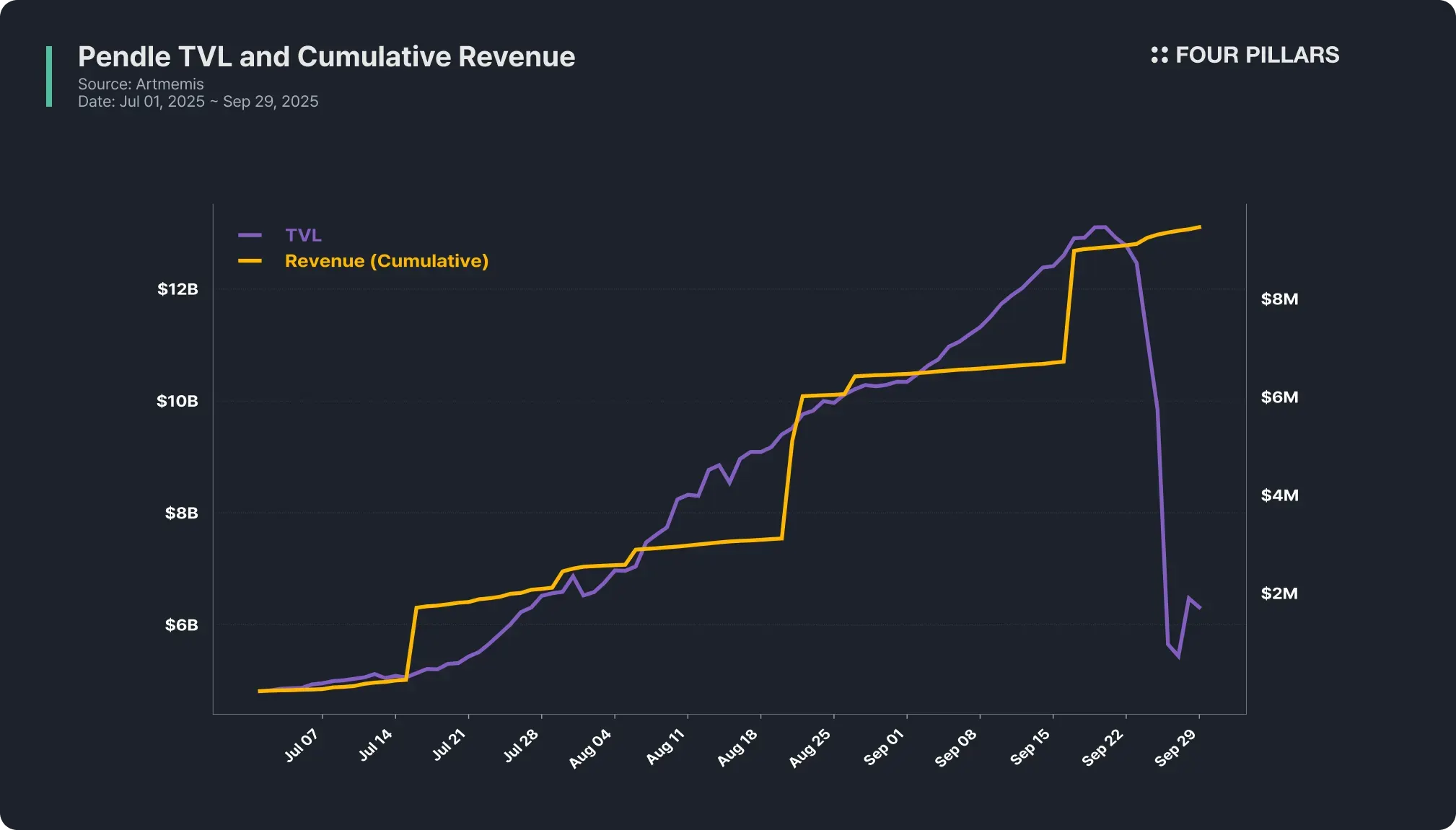

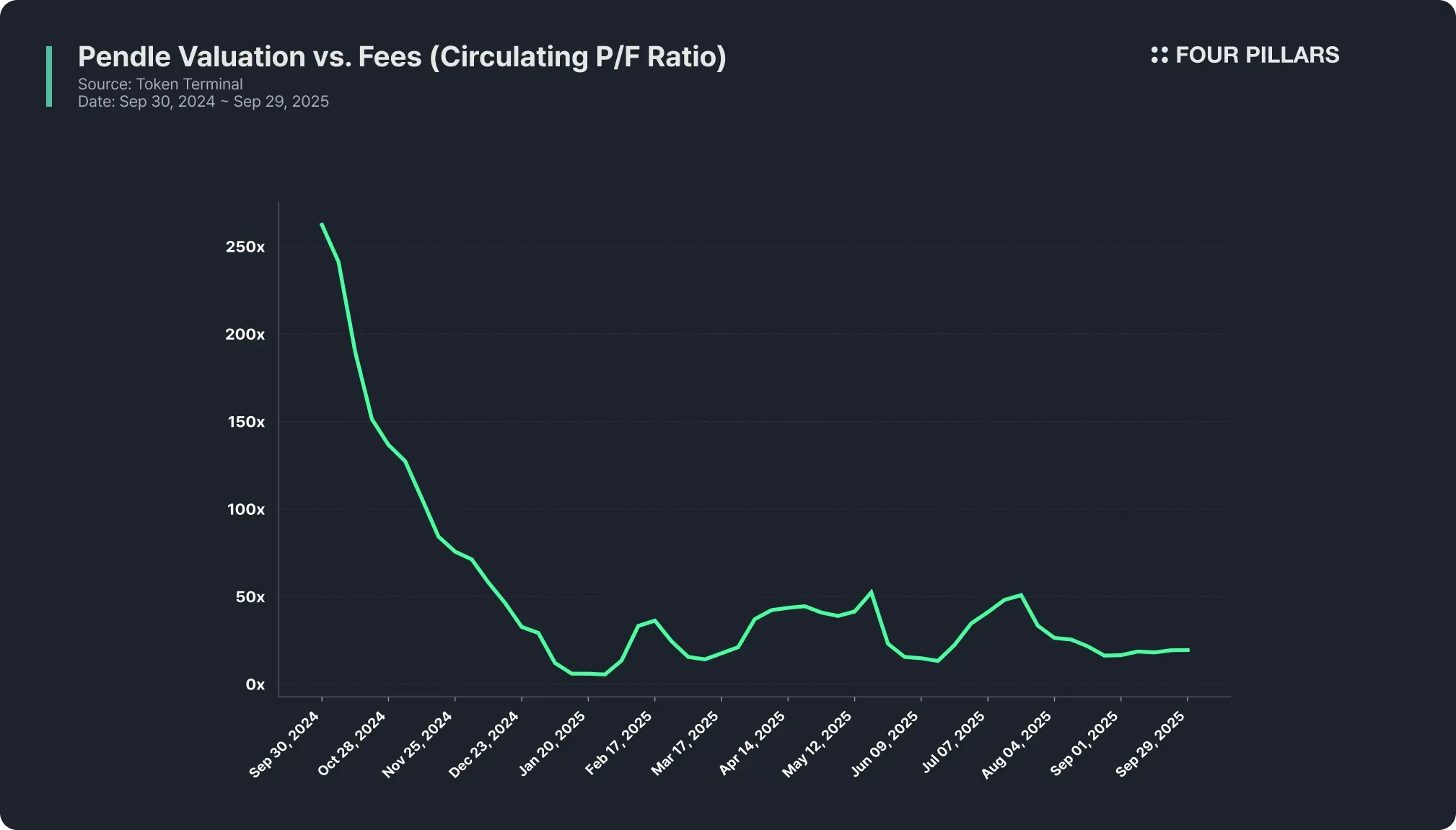

In short, Pendle Finance has gained popularity among investors with different risk reward profiles and has achieved over $6B in TVL (at one point exceeding $12B, though TVL later decreased as a massive trading pair reached maturity). In particular, the ratio of Pendle’s token market capitalization to fees generated on the platform converging toward 10–20x demonstrates that Pendle Finance is one of the few on-chain structured product protocols to achieve PMF, embedding sustainability.

However, in traditional finance, there are various types of structured products. There are also products similar to Pendle Finance, such as strip bonds, which allow investors to separately trade the principal and interest of specific bonds, but this market is relatively small compared to the overall bond market.

The larger structured product market in traditional finance lies in tranching. As noted earlier, tranching separates the same underlying asset into products with different risk reward profiles, satisfying investors with varying risk preferences. Such structured products are also indispensable in on-chain finance. Here enters Strata, a protocol aiming to tranche all crypto-native yields based on interest rate volatility.

Pendle split yield-bearing tokens into principal and yield portions. Strata also divides yield-bearing tokens into two parts, one being the senior tranche token and the other the junior tranche token.

The senior tranche token aims to hedge against the risks of interest rate volatility and provide a stable return at a moderate level of interest, while the junior tranche token takes on the risk of interest rate volatility in exchange for potentially higher returns than before.

As its first showcase, Strata applies this model to Ethena’s sUSDe. Let’s take sUSDe as an example to better understand Strata.

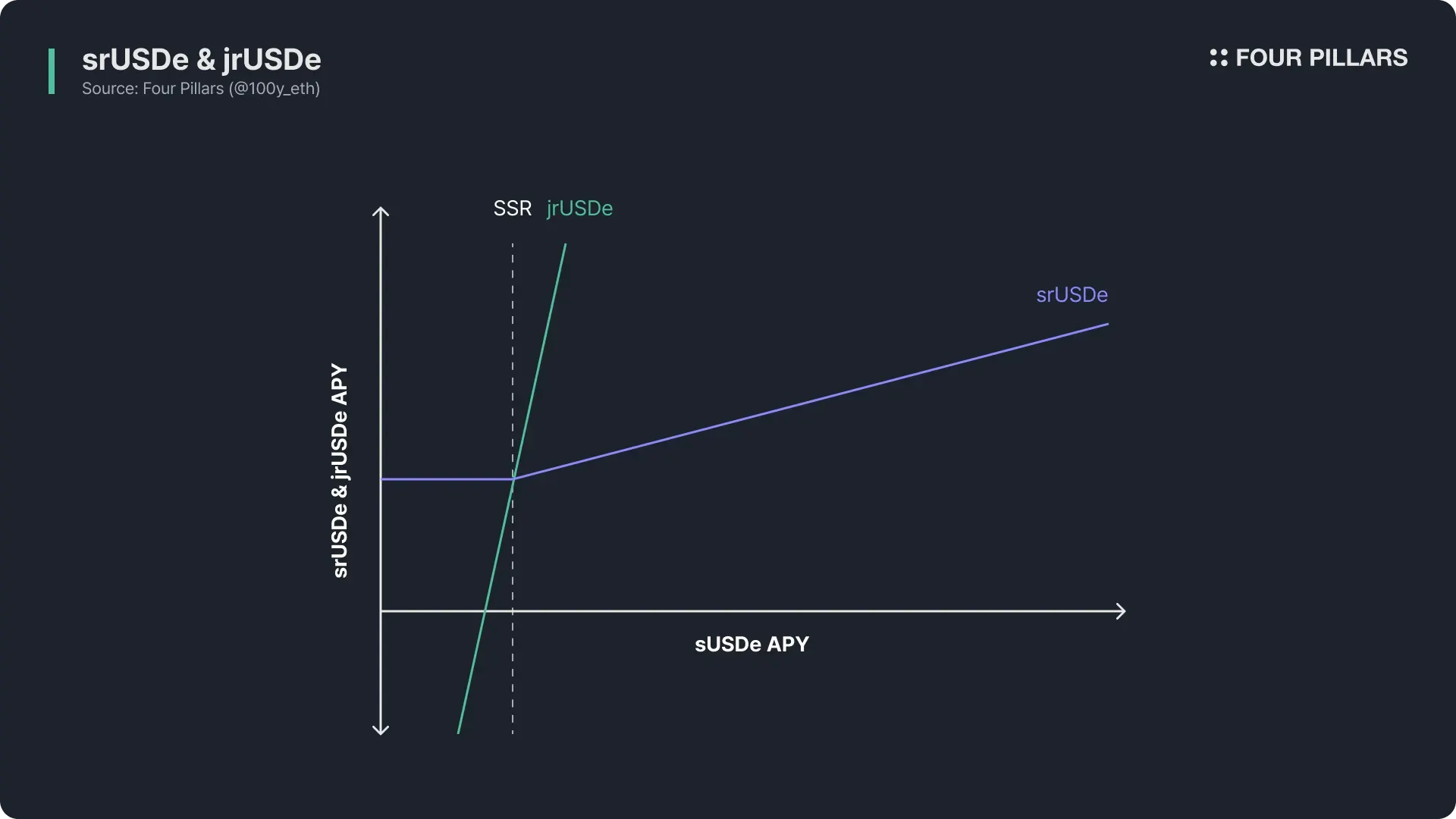

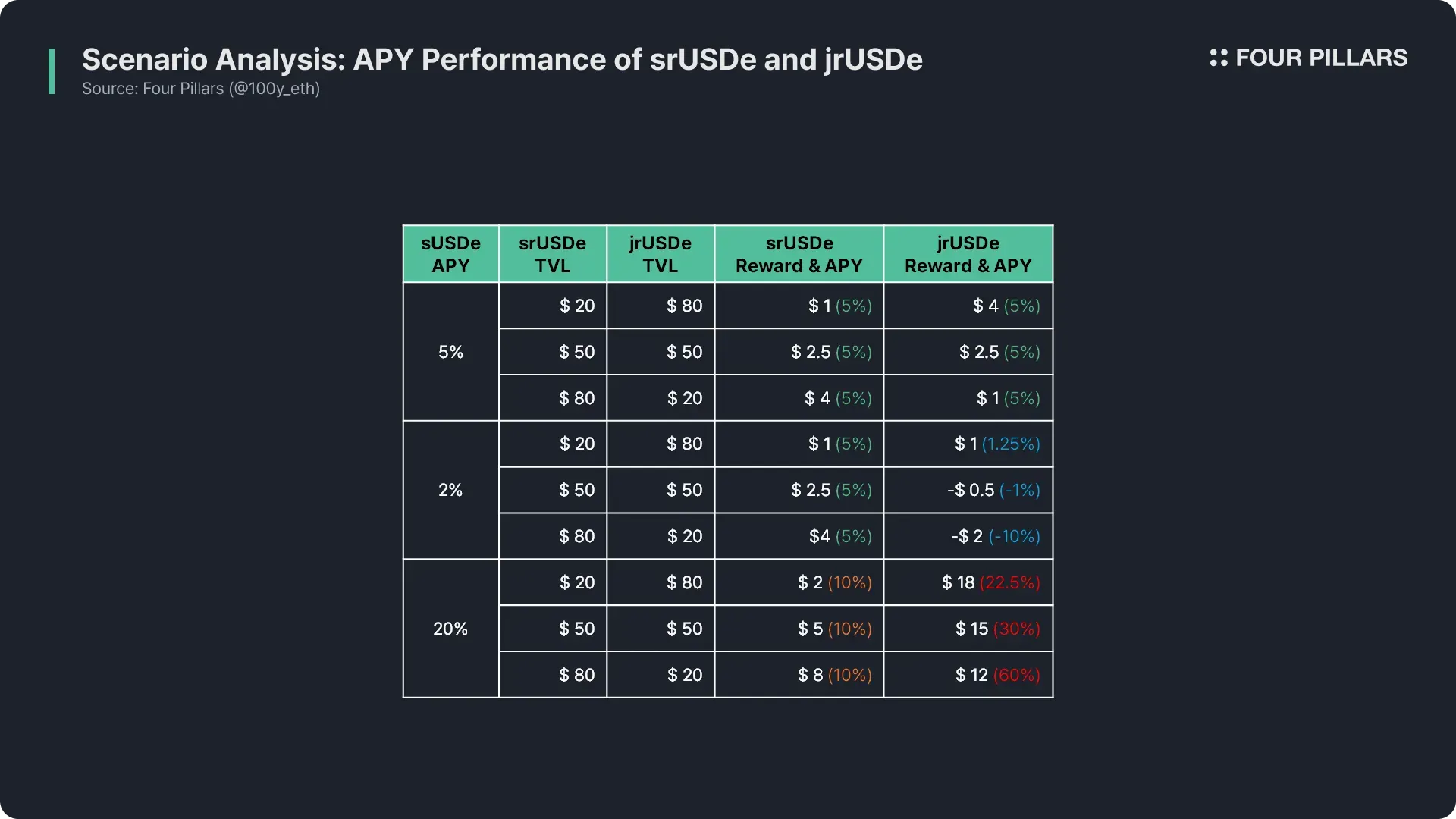

(The figure above is for illustrative purposes only. In addition to the sUSDe APY, the ratio between srUSDe and jrUSDe is also very important in determining the interest rate.)

2.2.1 srUSDe

srUSDe is the senior tranche token of sUSDe. The minimum yield is guaranteed at the SSR (Sky Savings Rate) provided by Sky, and holders can also expect a reasonable level of upside interest.

For example, if the SSR is 5 percent, even when the sUSDe APY falls below 5 percent, srUSDe holders will still receive a 5 percent yield. Conversely, if the sUSDe APY is higher, say 20 percent, srUSDe holders will not capture the full 20 percent, but they will still earn a yield higher than 5 percent and slightly below 20 percent.

However, in an extreme scenario where the jrUSDe TVL is close to zero and the sUSDe APY falls below 5 percent, there would be no jrUSDe holders to absorb the interest rate risk. In that case, srUSDe holders would simply receive the same yield as the sUSDe APY.

2.2.2 jrUSDe

jrUSDe is the junior tranche token of sUSDe, and its yield can be higher or lower depending on the sUSDe APY.

The interest income remaining after paying srUSDe holders goes to jrUSDe holders. If the sUSDe APY falls short of the SSR, jrUSDe absorbs the shortfall, which may result in negative returns. However, with risk comes reward. In an environment where the sUSDe APY is much higher than the SSR, the yield order becomes srUSDe < sUSDe < jrUSDe, meaning jrUSDe holders can enjoy significantly higher yields than standard sUSDe holders.

2.2.3 Scenario

Disclaimer: This illustration is for explanatory purposes only and may differ from the actual figures.

The factors that determine the interest rates of srUSDe and jrUSDe include not only the sUSDe APY but also the ratio between srUSDe and jrUSDe. For example, if the total TVL of sUSDe deposited in Strata is 100 dollars, the APY performance of srUSDe and jrUSDe depending on sUSDe APY and the TVL ratio can be understood as shown in the table above. (Assume SSR = 5 percent)

sUSDe APY = 5% = SSR

If the sUSDe APY is equal to the SSR, then regardless of the TVL ratio between srUSDe and jrUSDe, all of them receive 5 percent interest.

sUSDe APY = 2% < SSR

Now assume the sUSDe APY is 2 percent, which is lower than the SSR. In this case, 100 sUSDe generates 2 dollars of annual interest, which must be shared between srUSDe and jrUSDe holders. As noted earlier, the minimum interest rate for srUSDe is guaranteed at the SSR of 5 percent. This means that srUSDe holders still receive 5 percent interest even when the sUSDe APY is 2 percent, and the shortfall must be covered by jrUSDe holders. As shown in the table, jrUSDe holders take on losses because they absorb the negative interest gap.

When the sUSDe APY is below the SSR, the higher the srUSDe/jrUSDe ratio, the fewer jrUSDe holders there are to cover the interest shortfall for a larger group of srUSDe holders, leading to greater losses for jrUSDe.

sUSDe APY = 20% > SSR

Now assume the sUSDe APY is 20 percent, which is higher than the SSR. In this case, 100 sUSDe generates 20 dollars of annual interest, which is split between srUSDe and jrUSDe holders. srUSDe holders are protected with a minimum yield at the SSR. If the sUSDe APY is higher than the SSR, they cannot capture the full upside, but they can still expect a moderate increase. Let’s assume this is 10 percent.

srUSDe holders would then receive 10 percent interest first, and the remaining yield would go entirely to jrUSDe holders. Since srUSDe holders capture less than the sUSDe APY, the excess yield flows to jrUSDe holders, making jrUSDe APY higher than the sUSDe APY.

When the sUSDe APY is above the SSR, the higher the srUSDe/jrUSDe ratio, the more excess yield from a larger pool of srUSDe flows into a smaller pool of jrUSDe holders, increasing the returns for jrUSDe holders. For example, as shown in the table, when srUSDe TVL is 80 dollars and jrUSDe TVL is 20 dollars, with an sUSDe APY of 20 percent, the jrUSDe APY can rise to as much as 60 percent.

2.2.3 Characteristics of srUSDe and jrUSDe

Strata enables investors to use interest rate volatility-based tranching with a high-quality user experience.

Seamless minting and redemption: Investors can mint or redeem srUSDe or jrUSDe from USDe or sUSDe at any time without lockups.

Seamless cross-chain: Since srUSDe and jrUSDe use LayerZero’s OFT standard, investors can freely bridge and use them across multiple chains.

Seamless DeFi integration: As srUSDe and jrUSDe are based on the ERC-4626 tokenized vault standard, interest value accrues directly into the tokens, making them easily integrable into a wide range of DeFi and CeFi services.

Sometimes skeptics question whether DeFi truly delivers any real PMF. However, whether DeFi has already found PMF or not, Pendle Finance has clearly demonstrated that within the DeFi ecosystem there is indeed a PMF around diversifying risk reward profiles for the principal and interest components of yield-bearing tokens.

If Pendle separates the principal and interest of yield-bearing tokens, Strata provides two types of risk reward profiles based on interest rate volatility risk. This is a similar yet distinctly different approach, opening the door to an investment method that Pendle Finance has not been able to offer to DeFi users.

Strata has not yet launched a complete product and is currently only running a pre-deposit campaign, so it is difficult to predict what the final product will look like. That said, I see two key points worth noting.

Mitigating counterparty risks: If USDe experiences a liquidity issue, the senior tranche has priority over the junior tranche in terms of repayment. This structure means that the liquidity of the junior tranche tokens serves as a kind of insurance, increasing the likelihood that senior tranche token holders can have their principal protected.

Point programs: The rapid growth of Pendle Finance was not only driven by interest income but also by the role of point programs from projects preparing for airdrops. The question is whether Strata’s tranche structure will allow for differentiated risk reward profiles for points as well.

jrUSDe concentration: Given the nature of on-chain users, many are likely to take on greater risk in pursuit of higher returns. This could lead to jrUSDe TVL being larger than srUSDe TVL. If this happens, the risk reward profile of jrUSDe holders may not be substantially different from that of traditional yield-bearing token holders.

This article has explained Strata with USDe as an example, but Strata has the potential to be applied not only to USDe but to any kind of yield-bearing token that generates interest. In fact, after USDe, Strata is expected to be applied to Hyperliquid HLP and Lighter LLP.

Can Strata follow in Pendle’s footsteps? Time will tell.

Dive into 'Narratives' that will be important in the next year