Since October’s roadmap, Spark Savings (V1 + V2) has doubled deposits to roughly $1.7 billion. While Savings V2 now holds around $313 million across the new spUSDC, spUSDT and spETH vaults, the legacy sUSDC (V1) pool continues to account for the majority of deposits.

Institutional inflows accelerated, with around $500 million funding Coinbase loans, ~$330 million ($1 billion target) bootstrapping PYUSD liquidity, and $4 billion in SparkLend TVL.

Spark is emerging as the liquidity backbone for DeFi, fintech & institutions, supplying unified yield, liquidity, and credit.

The October roadmap marks a step-change in Spark’s evolution, from a protocol primarily allocating Sky liquidity to a broader financial platform coordinating capital formation, deployment, and yield across multiple venues.

Savings V2 and Institutional Lending collectively establish Spark as a unified liquidity and credit infrastructure layer: a base yield for stable assets and programmatic cross-chain deployments. In a market where users want one place to save, spend, send, and earn, Spark’s engine supplies the yield, liquidity, and credit these frontends need with onchain transparency.

Spark’s architecture interlocks 3 layers:

Funding comes from Sky/Maker’s stablecoin reserve and the Sky Savings Rate (SSR), providing a mid-single-digit base cost of capital.

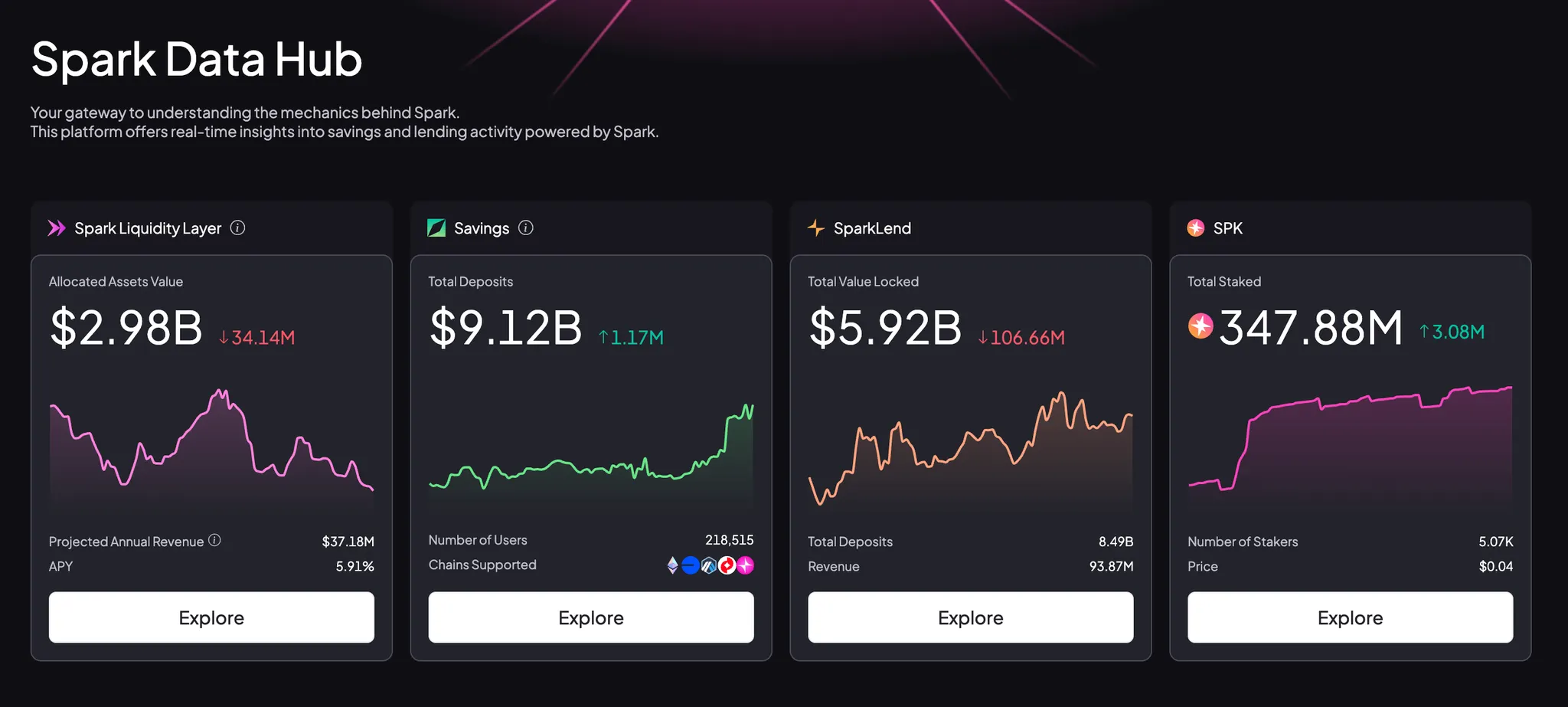

Allocation is handled by the Spark Liquidity Layer (SLL), a cross-chain, multi-asset treasury that has scaled to ~$2.6 billion allocated at ~5.1% APY and retains the entire spread above the 4.8% Sky base rate.

Distribution occurs through SparkLend and Spark Savings. This setup (cheap, sticky deposits → programmatic deployments → spread capture) has begun to translate into durable, cash-converting earnings, with the SLL estimated at ~$26 million run-rate profit and $5.93 million USDS transferred to the treasury for July–August.

Source: Spark Dashboard

As of late November 2025, Spark’s combined deposits across Ethereum and L2s were approximately $8.2 billion, placing it among the larger liquidity allocators in the sector.

Prior to the upgrade, Savings had reached ~$600 million TVL across 6 chains (Ethereum + 5 EVMs). Post-V2, total Savings TVL (V1 + V2) rose to ~$1.7 billion. Savings V2 now holds around $313 million across the new spUSDC, spUSDT, and spETH vaults, while the legacy sUSDC (V1) pool continues to account for the majority of deposits. Several design factors explain the additional ~$1.1 billion in deposits since the roadmap launch:

Yield anchoring: Each Savings vault references the Sky Savings Rate (SSR), offering a predictable, governance-set baseline. Access to Savings USDS across multiple chains allows users and treasuries to earn governed yield without active management.

Liquidity structure: A 10% instant-liquidity buffer absorbs withdrawals, while 90% of capital is deployed into established venues such as blue-chip money markets, RWAs, and, for ETH, staking and lending blends (SparkLend ETH and Lido stETH).

Market context: Following the large liquidation event on October 10, leverage across DeFi rapidly contracted, flattening funding and basis spreads and driving down yields on stablecoin lending, LP positions, and delta-neutral strategies. As returns on competing strategies compressed sharply, Spark Savings, anchored to the stable and governance-set SSR, became a comparatively attractive low-risk alternative, resulting in increased inflows., particularly sUSDC.

Incentives: Spark Points encourage migration from V1 without mandating it.

Source: https://data.spark.fi/savings/sUSDC

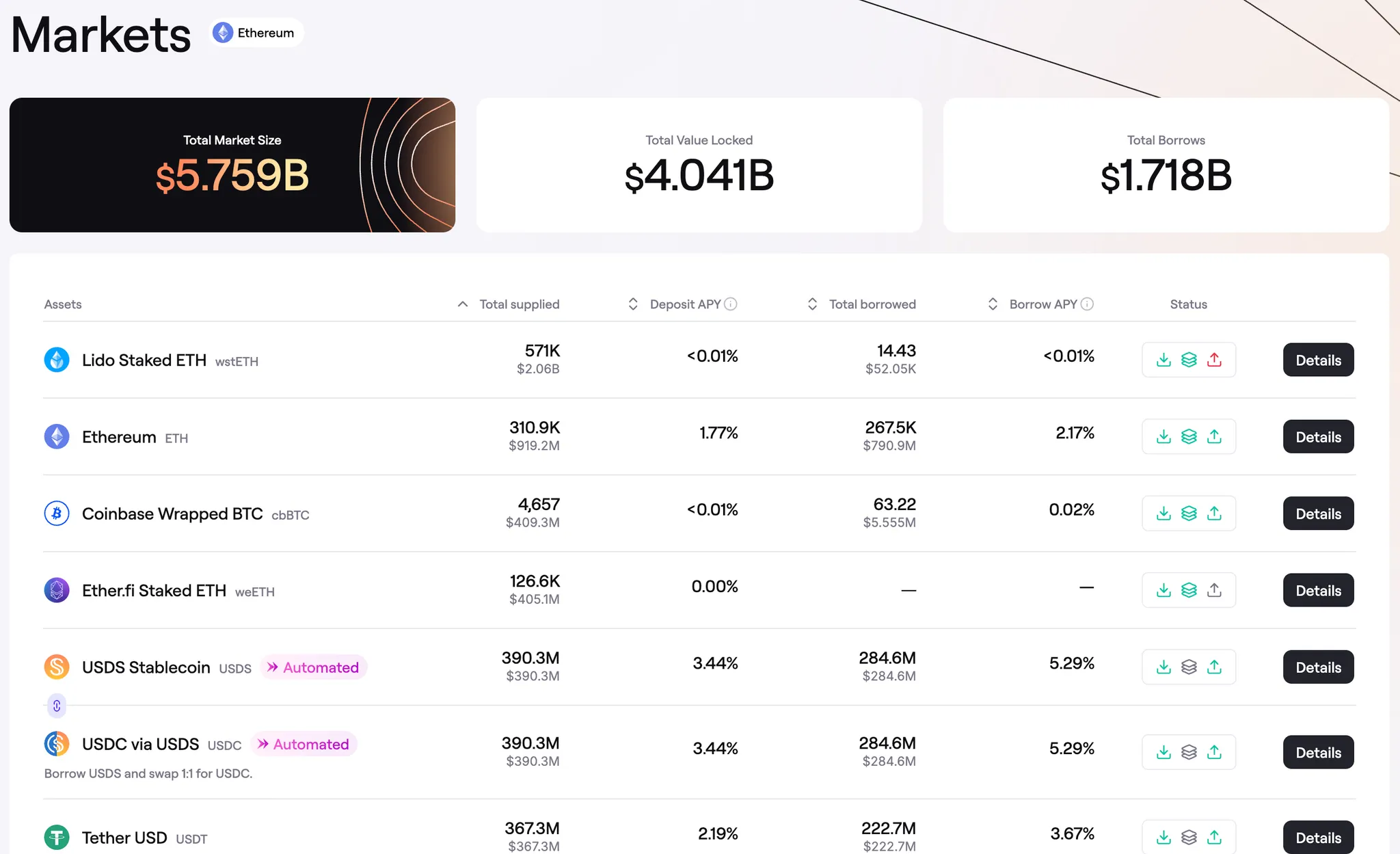

Alongside Savings, SparkLend remains the network’s core money-market engine and the main venue for market-driven liquidity. It currently holds roughly $4 billion in deposits. The base markets are composed of highly liquid, over-collateralized assets (ETH, stETH, wBTC, USDC), while higher-risk assets are isolated through Morpho, ensuring volatility in peripheral pairs cannot bleed into the core.

SparkLend’s USDT market expanded from under $30 million to about $367 million by late November. The new PYUSD market, launched in Q4, added another $333 million (aiming for $1 billion) in deposits, anchoring PayPal’s stablecoin to usable on-chain credit rails. These two markets illustrate Spark’s dual role: USDT supports trading liquidity; PYUSD powers fintech and payments infrastructure. Together they reinforce Spark’s positioning as a source of structured, over-collateralized liquidity for institutions.

The Spark Liquidity Layer (SLL) functions as Spark’s treasury and liquidity allocator. As of 26 November 2025, it manages approximately $2.7 billion in deployed assets across money markets and RWAs, earning an average yield of ~5.2% against a base funding cost near 4.8% — the spread that accrues directly to the treasury. Between July and August alone, $5.93 million in USDS profit was transferred to the DAO.

The SLL acts as the strategic counterparty behind several institutional programs:

Coinbase BTC-backed loans (Base): ≈ $500 million in on-chain, over-collateralized credit, with Coinbase managing customer-facing flows.

PayPal PYUSD liquidity: ≈ $333 million seeded across lending / DEX markets to ensure launch-day depth.

Superstate allocation: $100 million rotated into short-duration basis-trade funds as U.S. Treasury yields fell, maintaining carry while staying within governed risk bands.

These lines are governed by explicit policy caps and counterparty limits set by Sky governance. The same framework underpins the next phase: fixed-term, fixed-rate institutional lending via Morpho V2. Spark will post large, evergreen offers (initially >$100 million, ramping >$1 billion) matched at market rates and backstopped by the SLL.

Taken together, Spark Savings, SparkLend, and the SLL compose a single governed liquidity system: cheap funding via Savings, efficient deployment through SparkLend and the SLL, and risk controls visible on-chain. That architecture explains why Spark has scaled to around $8.2 billion in total TVL and a run-rate profit near $26 million without any loss events or structural stress.

Source: https://app.spark.fi/markets/

Platform TVL: ~$8.2 billion as of late November, up sharply since mid-year and post-roadmap.

Savings: $620 million → ~$1.7 billion since V2.

SparkLend: ~$4 billion deposits; USDT market ~$740 million deposits; PYUSD market live with rapid growth (SLL dashboard shows ~$333m TVL in the primary PYUSD pool end-November).

SLL allocations $2.6 billion deployed across money markets/RWAs/basis, avg ~5.2%; $100m into Superstate to diversify as rates shift; $100m+ quarterly stablecoin swap ops targeted.

Treasury flow: Protocol began retaining revenue July 1; $5.93m USDS transferred to Treasury (July–Aug close); SLL ~$26m ARR refers to spread above the 4.8% Sky base rate at current allocation mix.

Deposits, allocations, and treasury performance remain concentrated in a few core markets, reflecting Spark’s shift from isolated product lines to a consolidated liquidity management framework.

The broader shift toward transparent, on-chain liquidity systems continues to shape institutional behavior.

After repeated CeFi breakdowns, demand has grown for verifiable reserves, predictable yield frameworks, and standardized credit access. Major fintech and Web2 entities such as PayPal, Stripe, Robinhood, and Coinbase are building on-chain liquidity channels and increasingly prefer counterparties that can operate across stablecoins and venues under governed, transparent conditions.

Spark’s architecture addresses that requirement. Savings provides the deposit mechanism anchored to the Sky Savings Rate; the Spark Liquidity Layer (SLL) manages allocation and treasury functions; and institutional lending introduces fixed-term, fixed-rate credit structures.

Taken together, Spark functions less as a standalone lending platform and more as a neutral liquidity and settlement layer — a wholesale infrastructure connecting funding sources, institutional credit lines, and application-level frontends such as Plasma One, Tria, UR, or EtherFi-style wallets. Its trajectory suggests a gradual consolidation of Spark’s role as a foundational coordination layer within the on-chain financial stack.

Dive into 'Narratives' that will be important in the next year