The SEC’s statement on tokenized securities signals two things clearly: first, tokenized securities are recognized as an extension of formal securities market infrastructure; second, they fall squarely under the SEC’s regulatory jurisdiction.

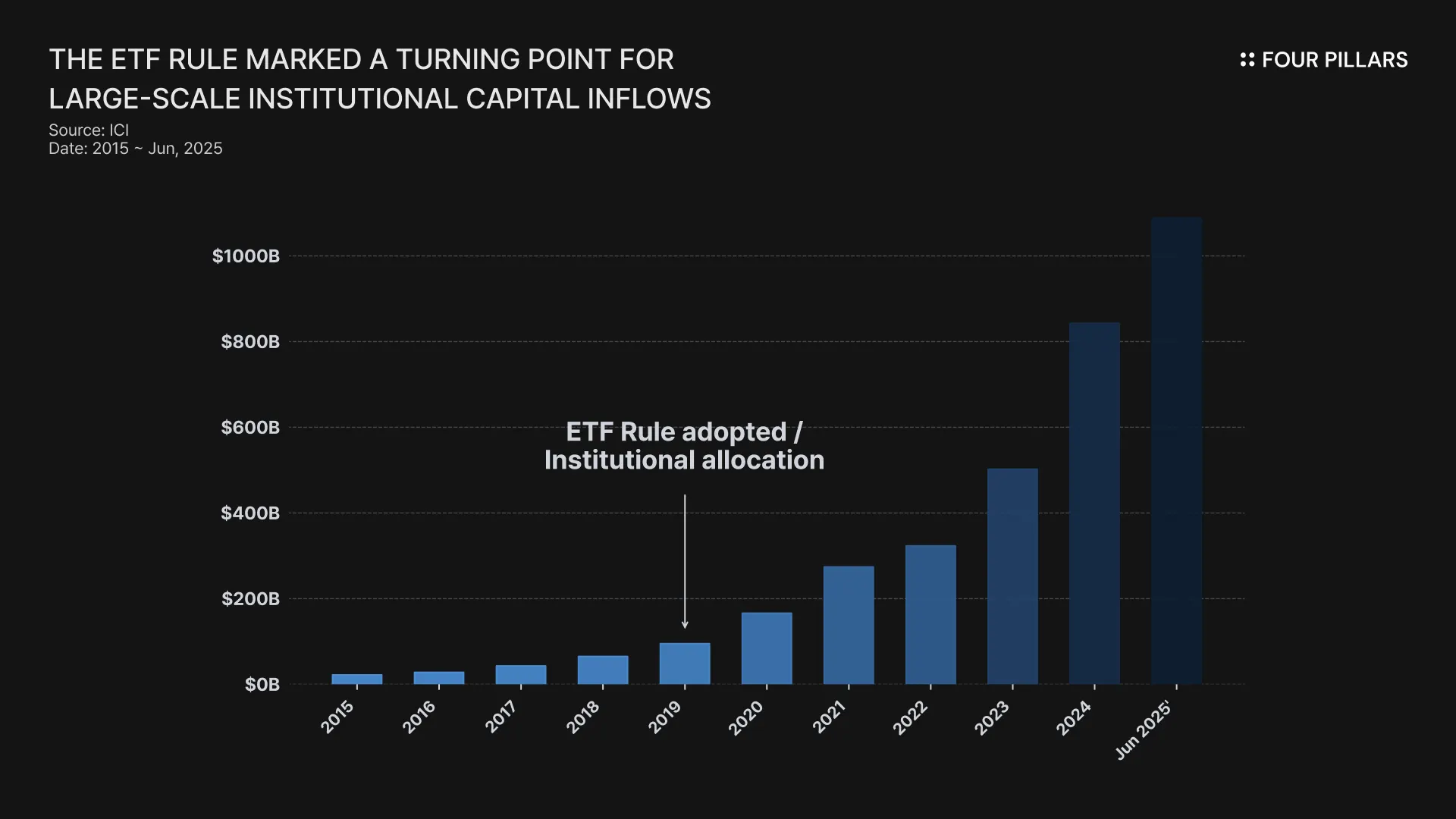

The ETF Rule, fully implemented in 2020, marked a turning point by defining ETFs as a standardized product category and unlocking large-scale institutional capital inflows. For tokenized securities to scale, similar institutional standardization is required, particularly around legal ownership, investor rights, regulatory compliance, and predictable clearing and redemption mechanisms.

Securitize is positioning itself to become a regulation-first tokenization platform through a clear strategy: ① a direct issuance model designed for SEC compliance, ② the recruitment of senior leadership with deep ETF market experience, and ③ a transition into a publicly listed company.

Source: SEC

Through its recent statement, the SEC formally articulated a framework for tokenized securities.

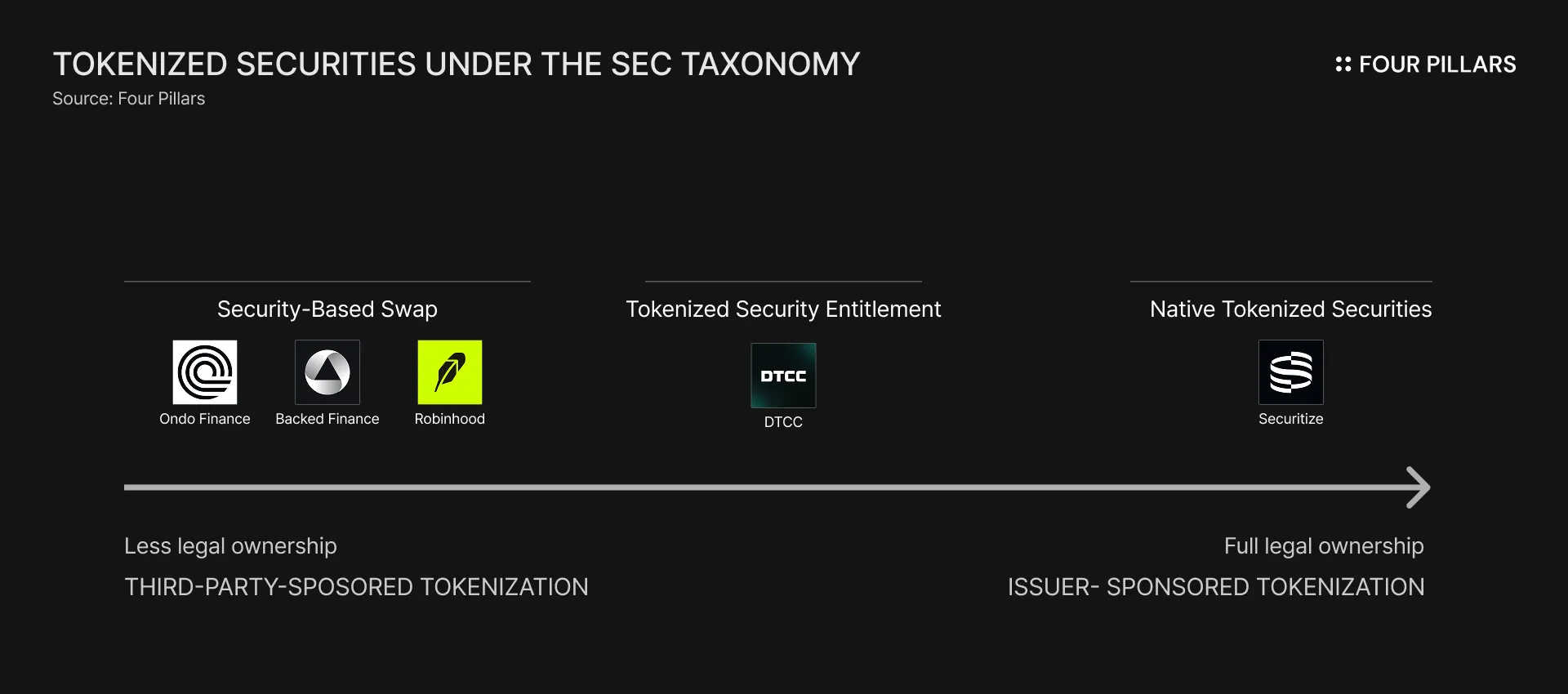

According to the SEC, tokenized securities are financial instruments that qualify as securities under federal securities laws, are represented by crypto assets, and have ownership records maintained on one or more crypto networks. Alongside this definition, the SEC introduced a taxonomy of tokenized securities based on the underlying tokenization model.

Issuer-Sponsored Tokenized Securities:

The issuer or its agent integrates DLT into the system that records securities ownership, namely the master securityholder file. When a tokenized security is transferred, the change is reflected directly in the shareholder register. The only difference from traditional systems is that the ownership record is maintained on a blockchain rather than in an offchain database. (i.e., Securitize)

Third-Party-Sponsored Tokenized Securities:

A third party unaffiliated with the issuer tokenizes a security. These models vary widely, including custodial and synthetic structures. The rights, obligations, and economic interests attached to the token may or may not align with those of the underlying security. (i.e., Backed Finance, Ondo, Robinhood)

The message of the SEC statement is straightforward: “tokenized securities are securities.” This simple framing formalizes two key perspectives.

Tokenized securities are an extension of regulated securities infrastructure: Tokenization is no longer treated as a crypto native experiment but as a financial product category on par with ETFs.

The legal nature of securities does not change through tokenization: Regardless of technical structure, existing securities regulations apply. Tokenized securities are clearly within the SEC’s regulatory perimeter.

At least in the context of tokenized securities, code is not law. Law is law. What tokenized securities need today is institutional standardization.

The path ETFs took toward mainstream adoption is instructive. Before the ETF Rule, specifically SEC Rule 6c-11, ETFs relied on product-specific exemptive relief from the SEC. As a result, basket composition, disclosure requirements, and creation and redemption mechanisms were shaped by precedent and market practice rather than a consistent regulatory standard.

The ETF Rule, fully implemented in 2020, marked a structural inflection point. ETFs were formally defined as a standardized product category, active ETFs could launch without prior exemptive approval, and regulatory uncertainty was significantly reduced. This clarity enabled ETFs to be incorporated broadly into institutional portfolios. Over time, ETFs displaced synthetic instruments such as linked notes, ETNs, and CFDs as the dominant access vehicle.

Institutional ownership of US-listed corporate bond ETFs rose from 44% in 2012 to 70% by 2025.

Total US ETF net assets grew from $2.1T in 2015 to $11.5T by June 2025, a more than fivefold increase in a decade.

Institutions demand legal clarity. Tokenized securities will not be an exception. Capital markets will focus on legal ownership, enforceable investor rights, regulatory consistency, and predictable clearing and redemption processes. Even with advantages such as 24/7 trading and global accessibility, tokenized securities cannot attract institutional capital if they are not defined as a standardized product category.

It is also likely that future SEC frameworks will go beyond high-level guidance. The scope of third-party issuance, mandatory inclusion of securities rights, and permitted trading venues are areas where clearer rules are likely to emerge.

In this environment, regulatory compliance for tokenized securities is no longer optional. The regulatory posture of a tokenization platform directly shapes the risk profile of the securities it issues. This includes risks such as invalidation of securities rights, price dislocation from underlying assets, and failed redemptions. These risks increasingly define the long-term viability of tokenized securities.

As with ETFs, institutional standardization will be the condition that allows tokenized securities to enter capital markets and scale. It will also determine which tokenized securities persist and which platforms emerge as trusted infrastructure layers in the next phase of financial market evolution.

Among tokenized securities platforms, Securitize stands out as the player most aligned with the direction of institutional standardization.

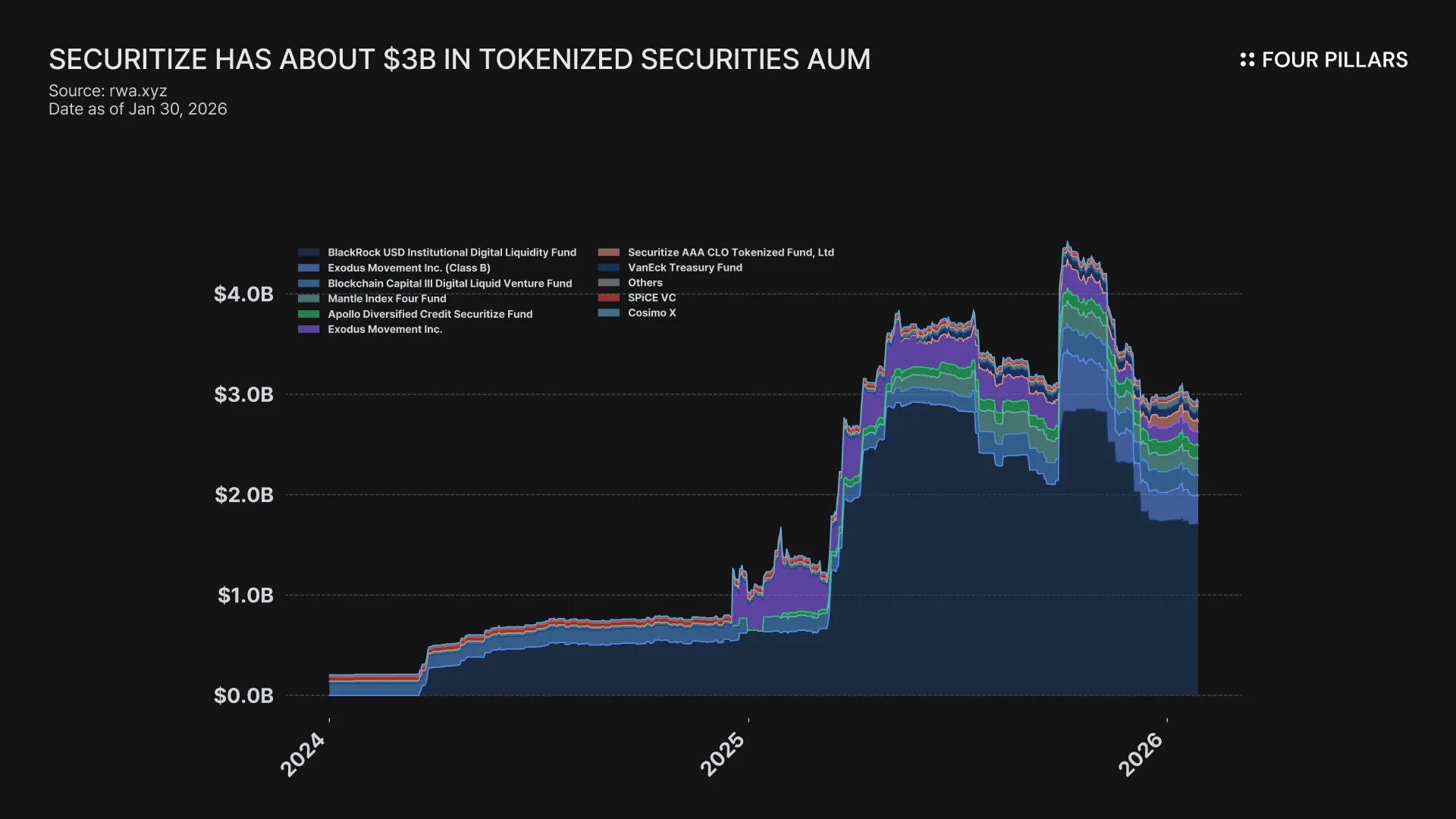

Founded in 2017, Securitize manages about $3B in tokenized assets as of early 2026. Its work includes the tokenization of BlackRock’s BUIDL fund, as well as partnerships with Apollo Global Management, KKR, and BNY Mellon. These relationships indicate that Securitize operates not as an experimental sandbox, but as a production-grade tokenization partner for major financial institutions.

Securitize’s core thesis mirrors the ETF story. Just as ETFs reshaped markets once they were standardized, Securitize sees tokenization as the next structural phase. Its strategy is consistently oriented toward building a regulation-first tokenization platform.

Securitize tokenizes securities by embedding investor rights directly into the token, including dividends, voting, and disclosure rights. Under the SEC’s taxonomy, this model falls under issuer-sponsored tokenized securities, where the transfer agent records ownership changes directly on an onchain register.

Securitize holds the following licenses:

SEC-registered broker-dealer

SEC-registered transfer agent

SEC-regulated alternative trading system

Licensed fund administrator

EU regulatory licenses

This model preserves the legal nature of traditional securities and is designed to meet future tokenized securities standards as regulation becomes more explicit. As the SEC has acknowledged the use of blockchains as authoritative ledgers for securities records, licenses such as transfer agent status have become increasingly central. These regulatory capabilities represent a barrier to entry that exceeds purely technical infrastructure.

Source: X(@Securitize)

Securitize’s hiring strategy reinforces this positioning.

The company recently appointed Giang Bui as Vice President and Head of Issuer Growth. Bui spent approximately five years at Nasdaq, where she oversaw US equities and ETF strategy. She also played a key role in the 2024 spot Bitcoin ETF approval process.

The launch of Bitcoin ETFs required close coordination among issuers, regulators, and liquidity providers to integrate the Bitcoin ETF market into regulated financial infrastructure. This process closely mirrors the challenges that tokenized securities are currently facing.

For example, tokenized securities issued by tokenization platforms without issuer authorization are unlikely to meet the requirements of traditional capital markets. Providing full legal ownership of a security, native tokenization requires the issuance structure to be designed and executed in direct collaboration with the official issuer. In this context, the ability to work directly with issuers, along with proven experience collaborating with them, becomes the most critical prerequisite for any tokenization platform.

Securitize’s recent leadership hires can be understood within this framework. At a moment when tokenized securities are approaching entry into mainstream capital markets, leadership recruitment is likely to play a key role in establishing a durable trust line between regulated financial markets and tokenization infrastructure.

Securitize is pursuing a public listing through a merger with Cantor Equity Partners II, a Nasdaq-listed SPAC, and has publicly filed a registration statement on Form S-4 with the SEC. This filing marks the formal start of the de-SPAC listing process.

It also reinforces Securitize’s position as the only tokenization platform operating as a US company directly under SEC oversight, further strengthening institutional credibility.

Financial disclosures in the S-4 highlight meaningful revenue growth:

Revenue reached about $55.6M in the nine months ending September 30 2025, up 841% year over year.

Fiscal year 2024 revenue of $18.8M, up 129% year over year

While final approval remains subject to SEC clearance and shareholder approval, completion of the merger would make Securitize the first tokenization platform publicly listed in the US market.

The SEC’s statement reinforces that tokenized securities are not a transient crypto experiment, but an extension of regulated financial infrastructure, similar in trajectory to ETFs. It signals a future in which tokenized securities are integrated into mainstream capital markets.

In this transition, Securitize’s strategy is consistent and deliberate: ① a direct issuance model built for SEC regulation, ② leadership with ETF market expertise, and ③ a path toward public company status.

Securitize has already established a precedent by partnering with BlackRock to tokenize the BUIDL fund, valued at approximately $1.7B. It is now clearly pointing toward equities as the next phase of tokenized securities following bonds. The recruitment of leadership with direct experience working with stock issuers, along with Securitize’s own transition into a publicly listed company, can both be interpreted as steps that support its expansion into tokenized equities.

BlackRock’s Bitcoin ETF, IBIT, became the fastest-growing ETF in history, surpassing gold ETFs shortly after launch. This demonstrated how quickly new markets can form when institutional capital and regulated infrastructure align.

Whether this precedent will repeat through BlackRock, Securitize, and the standardization of tokenized securities remains to be seen. What is clear is that the pace of change is accelerating rapidly.

Dive into 'Narratives' that will be important in the next year