Revenue sharing through dividends can provide foundations & insiders with easy liquidity, potentially undermining long-term protocol growth.

A buyback-and-burn approach raises token value while giving smaller holders a proportionate upside, making it a more democratic model.

By reinvesting protocol revenue directly into the token, value that would have leaked via dividends is instead recycled, automatically bolstering scarcity.

As seen with Hyperliquid, buybacks alone are insufficient without real demand, a robust community, and strong product-market fit to ensure long-term success.

Traditional “real yield” from dividends or fee-sharing often looks appealing but can serve as an easy liquidity faucet for foundations or other large token holders. Instead of selling their core stake (an on-chain move that might spook the market) these insiders continuously convert ETH /USDC payouts into real cash. Meanwhile, the community sees little reinvestment, and small holders can’t match that scale of extraction. What appears to be a harmless yield model can turn into an invisible siphon, allowing big holders to tap protocol revenue with minimal accountability or public scrutiny.

Hyperliquid inverts this logic with a buyback-and-burn model. Instead of paying out fees as pseudo-dividends, the protocol allocates revenue to purchasing $HYPE on the open market, then permanently removes those tokens from circulation (see the bonus section at the end for a detailed explanation of the buyback-and-burn mechanism). This approach provides a more democratic upside: whenever Hyperliquid buys and destroys $HYPE, the token price tends to rise, allowing any holder (especially those with smaller positions) to sell profitably at will.

In contrast, the foundation faces significant barriers to dumping. A large sell-off would be immediately visible on-chain, destroying investor confidence and tarnishing the project’s reputation. Some critics claim protocols could buy back tokens merely to inflate prices and then dump on retail, but for a serious team, this scenario makes no sense: reselling tokens after a buyback would annihilate trust and undermine the foundation’s own stake. Even in crypto, where optics can be looser, there was notable backlash when the EF sold modest amounts of ETH.

Moreover, dumping undercuts the very buyback mechanism that sustains the token’s value. By executing buybacks, the protocol sends a powerful message of conviction, demonstrating to investors that there is always a reliable buyer. This boosts confidence and sparks a follow-the-leader effect in the market. It also fosters long-term alignment, since the protocol’s success is what ultimately drives $HYPE’s price higher.

Ultimately, while the foundation does benefit from rising $HYPE prices, smaller holders arguably gain more in relative terms, without the liquidity constraint and reputational blowback tied to large-scale selling. This results in a fairer, more widely shared upside than dividend distributions that disproportionately reward large stakes.

Token value hinges on supply-demand and expectations of future value. A fee-sharing token attracts yield-seekers, but it’s also a leaky bucket. Protocol-generated value flows out of the network rather than compounding in the token. Dividends paid in ETH or USDC regularly leave the protocol’s orbit, weakening growth momentum and letting large holders turn their tokens into immediate cash.

Hyperliquid has a total of 422.6 million $HYPE staked, with 272.7 million (~64%) staked by the foundation. If Hyperliquid paid out yields instead of conducting buybacks, the foundation could theoretically collect about 14 million $HYPE or $352 million (64% of the AF buyback volume as of May 9, 2025). While some portion of that dividend might be transparently reinvested, there is no inherent guarantee: significant value may simply be extracted, with retail holders and the broader community left in the dark on how that capital is truly deployed.

By contrast, a buyback & burn model recycles revenue directly back into the token. Each buyback reduces the supply, incrementally boosting every holder’s percentage stake and sparking a reflexive feedback loop. Investors anticipating further supply contraction hold rather than sell, reinforcing upward price dynamics.

At Hyperliquid, spot trading and listing fees ultimately flow into $HYPE burns, ensuring that higher volume directly equates to deeper scarcity. Dividend-driven models simply cannot match that reflexivity, since they rely on individual holders to re-buy tokens with their payouts. Hyperliquid’s automated burn is more consistent and immediate, forging a clear link between network activity and increased token scarcity.

Hyperliquid’s choice of buyback & burn over fee dividends reflects its founding philosophy of prioritizing community benefit. The project launched without VC allocations, instead conducting a large-scale airdrop of 310 million $HYPE (valued at roughly $1.6B at launch) to over 90,000 users. This broad distribution prevented insider dumping, fostered a deeply engaged user base, and provided immediate liquidity for the ecosystem from day one.

More than 70% of $HYPE has been reserved for the community through ongoing airdrops and incentives, while the foundation stakes a significant portion of its holdings to secure the network. By explicitly avoiding extractive models, Hyperliquid ensures that protocol revenue is funneled back into the token, driving up its value for all participants. In particular, retail investors have greater freedom to profit when buybacks elevate $HYPE’s price.

After the “real yield” trend of 2022, 2024~2025 is showing the power of “protocol as its own best buyer.” We see dYdX and others adding buyback programs to capture more revenue in their tokens. Market evidence is increasingly clear: when your token captures revenue via buybacks, it builds trust that the token isn’t just monopoly money.

Hyperliquid has embraced this principle from day one. By funneling fees into burns, Hyperliquid avoids both heavy insider extraction and murky legal territory around dividends. Holders see tangible financial impact every time the protocol earns fees.

Not every token with a buyback mechanism has succeeded, however. Projects that launched buybacks yet failed to sustain token value often lacked real demand, robust fee generation, or a strong community foundation. A buyback-and-burn strategy alone cannot salvage a weak protocol. For it to flourish, a project must also demonstrate genuine usage, reliable revenue streams, compelling pmf, and a cooperative user base that believes in its long-term viability.

From this vantage point, buyback-and-burn emerges as the linchpin value-accrual loop for well-designed tokens. It creates a system in which the foundation and other major holders cannot profit without raising the token’s value for everyone else. Traders get a CEX-grade experience, confident that their fees feed an enduring burn loop rather than insider wallets. The outcome is an enthusiastic user base, reflexive growth, and, critically, a framework that rewards genuine activity.

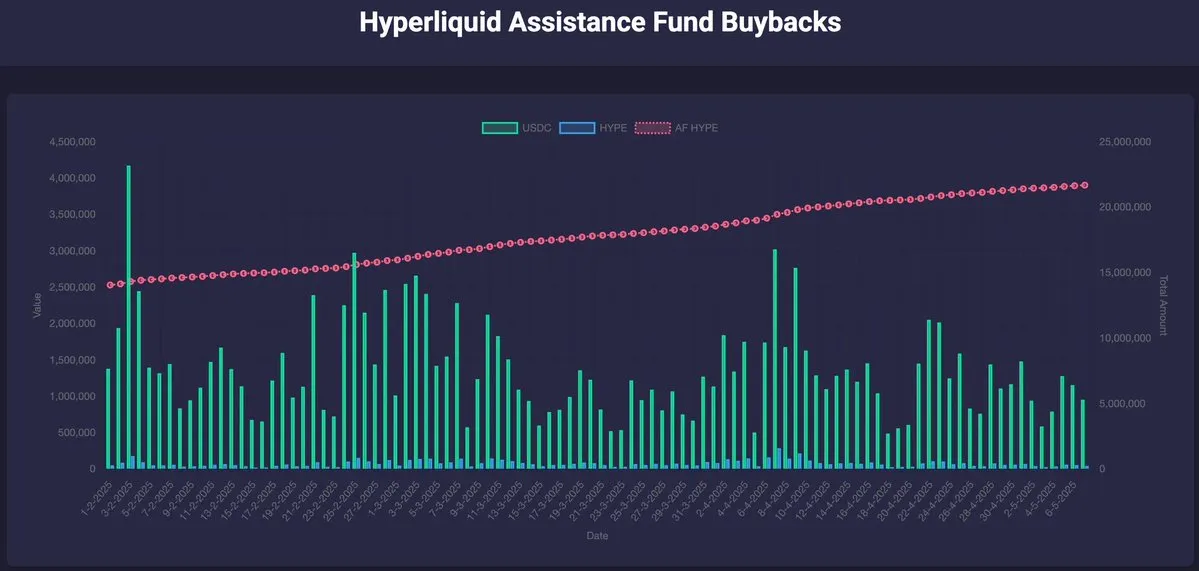

Hyperliquid’s buyback loop is already material: the Assistance Fund (AF) has purchased 22m $HYPE (~$556 million, 10 May 2025) and the protocol has burned 226k HYPE from trading fees alone.

Soure: https://assistancefund.top/

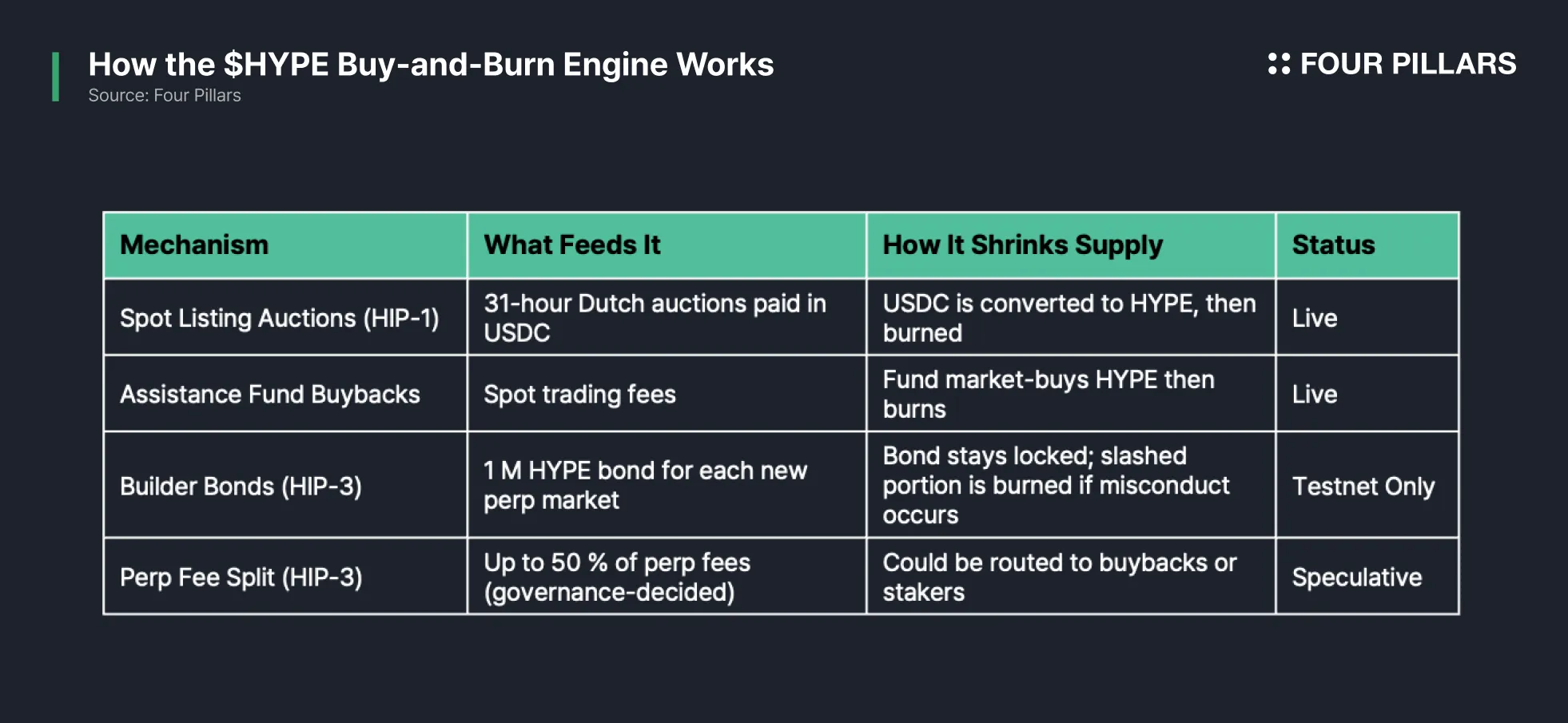

Key highlights of $HYPE’s buyback and burn model:

Listing Auctions & Fee Burn (HIP-1)

31-Hour Dutch Auctions for Spot: Every 31 hours, a spot listing slot is auctioned in USDC.

Guaranteed Buyback: The USDC raised must buy $HYPE on the open market, which is then burned.

Steady Burn Pressure: As more tokens seek a listing on Hyperliquid, these regular auctions generate ongoing demand for $HYPE, locking in a predictable burn model.

AF (Assistance Fund) Buybacks

Protocol Fees: Spot trading fees flow into an on-chain Assistance Fund.

Validator-Directed Burns: The community has voted to use part of this fund to buy and burn $HYPE.

Reflexive Impact: As volume grows, the fund swells, enabling larger burn orders; a virtuous cycle for price support.

Builder-Staked Perpetuals (HIP-3)

1M HYPE Bond: To launch a new perp market, builders must post 1M HYPE as collateral, a lockup that removes tokens from active circulation.

Slashing Risk: If operators manipulate oracles or violate rules, part (or all) of this bond can be slashed, effectively burning those tokens.

Fee Split = Potential Burn: Deployers (builders) can set a fee share of up to 50%.The remaining 50% may eventually go to the protocol, which might allocate it to buybacks or stakers. No guarantee until a final proposal passes. HIP-3 is still evolving via governance.

Dive into 'Narratives' that will be important in the next year