Lido V2's one-size-fits-all design couldn't serve diverse staker requirements. The staking market grew 73% since mid-2023. Lido grew 34%. The gap (2.7M ETH, roughly $20M in annual profit) split two ways: 8.5M to non-liquid staking, 4.5M to competing LSTs. A third segment, yield maximizers, used Lido but treated it as pass-through to EigenLayer and LRTs. V3 is designed to address all three.

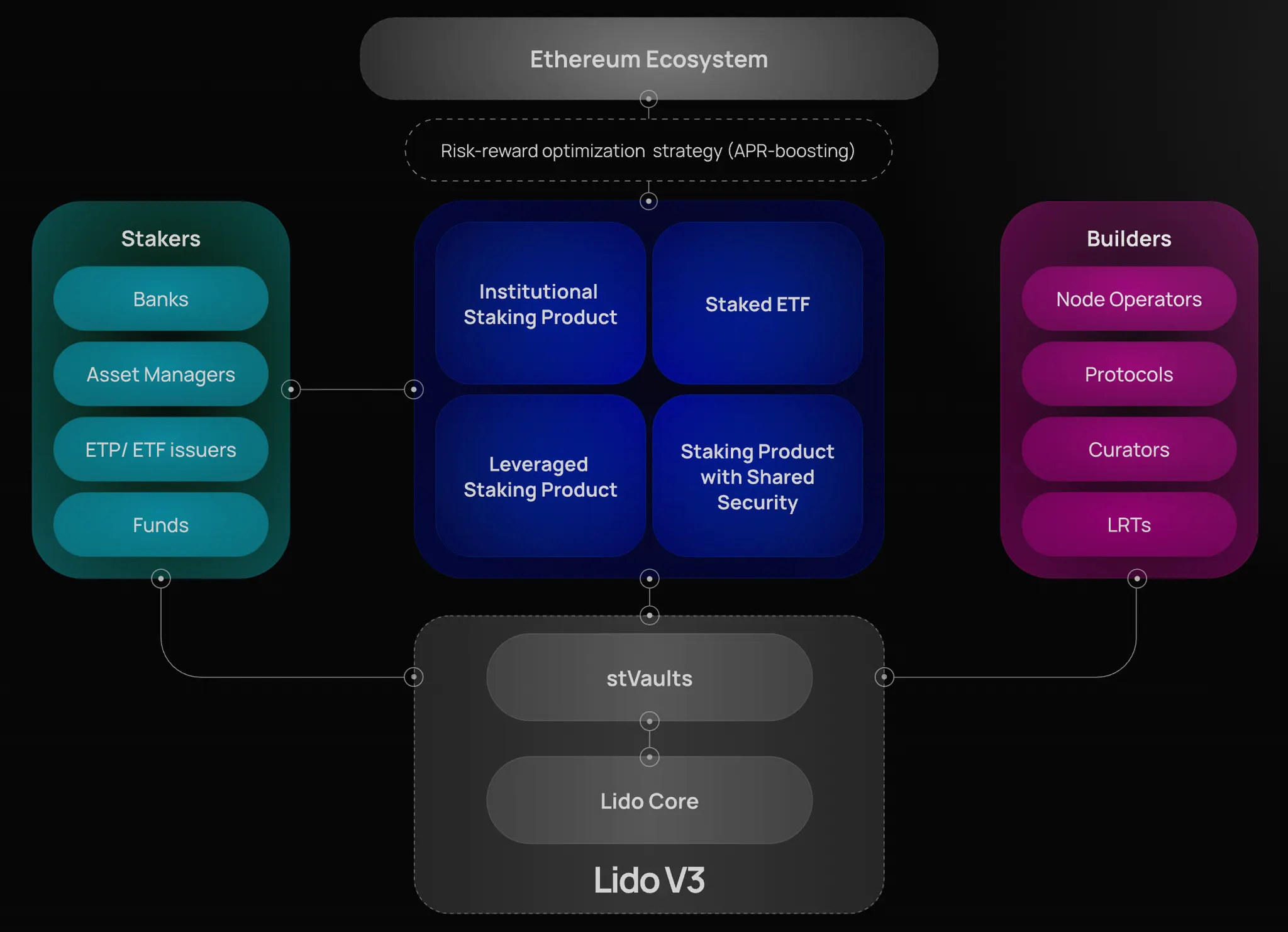

V3 breaks liquid staking's core trade-off. Until now, liquid staking meant accepting a one-size-fits-all risk pool. V3 introduces stVaults—think of them as personal staking accounts where you choose your own operator, fee structure, and risk configuration. You can optionally mint stETH against your vault for liquidity, or skip it entirely.

Risk isolation works until it doesn't. During normal operations, vault risk stays isolated. During tail events, forced rebalancing still socializes losses through Core Pool. This is 95% unbundling.

V3 positions Lido to serve all three segments under one architecture. Native stakers get full control without sacrificing access to liquidity. Institutions get segregation and compliance wrappers. Yield maximizers get composability with Lido as the base layer rather than a pass-through. With 70% of ETH still unstaked, V3 is Lido's bid to recapture lost ground and expand into the market that hasn't moved yet.

The lazy read on Lido's market share decline is competitive pressure—more LSTs, more restaking protocols, the category fragmenting. But that's not what happened. The market didn't fragment. It grew.

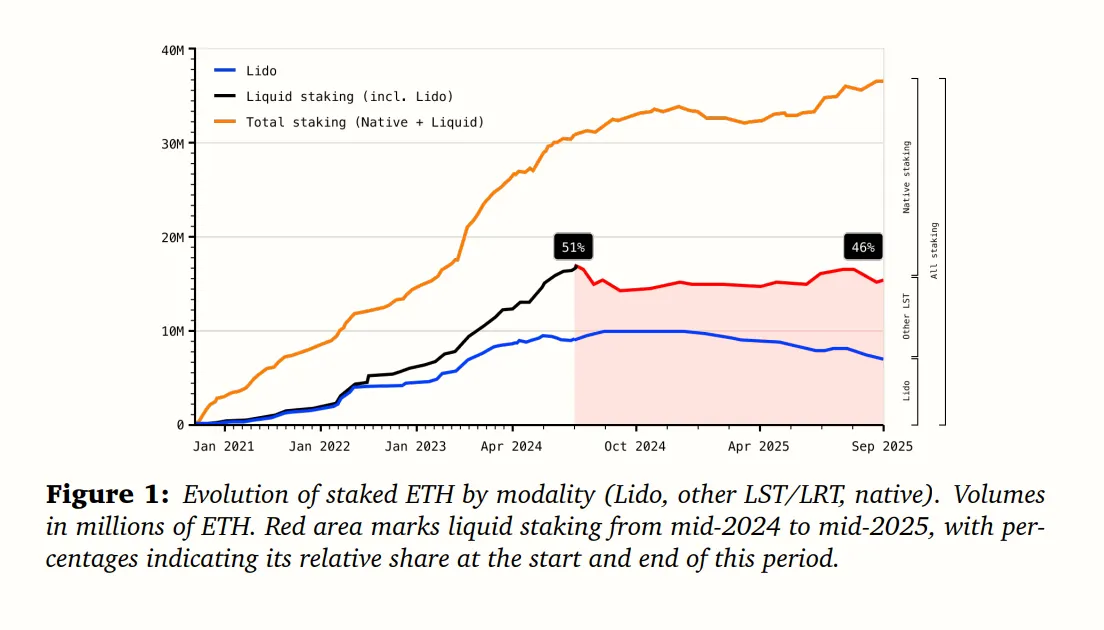

15.4 million ETH entered staking since mid-2023. Lido captured 2.4 million. Where did the other 13 million go?

Source: Lido V3 whitepaper

Non-liquid staking took the majority: 8.5M ETH, 55% of new stake. This includes solo stakers, institutional custodial setups, and anyone who chose direct validator operation over liquid tokens. Liquid staking's share of total staked ETH dropped from 51% to 46% between mid-2024 and mid-2025.

The common thread varied by segment. Native stakers either didn't need liquidity or preferred direct control. Institutional stakers faced a different constraint: regulatory requirements often mandate operators in specific jurisdictions or carrying specific certifications, requirements that don't square with V2's pooled operator model. V3 enables single-operator configurations with the option to mint stETH for DeFi or liquidity when needed.

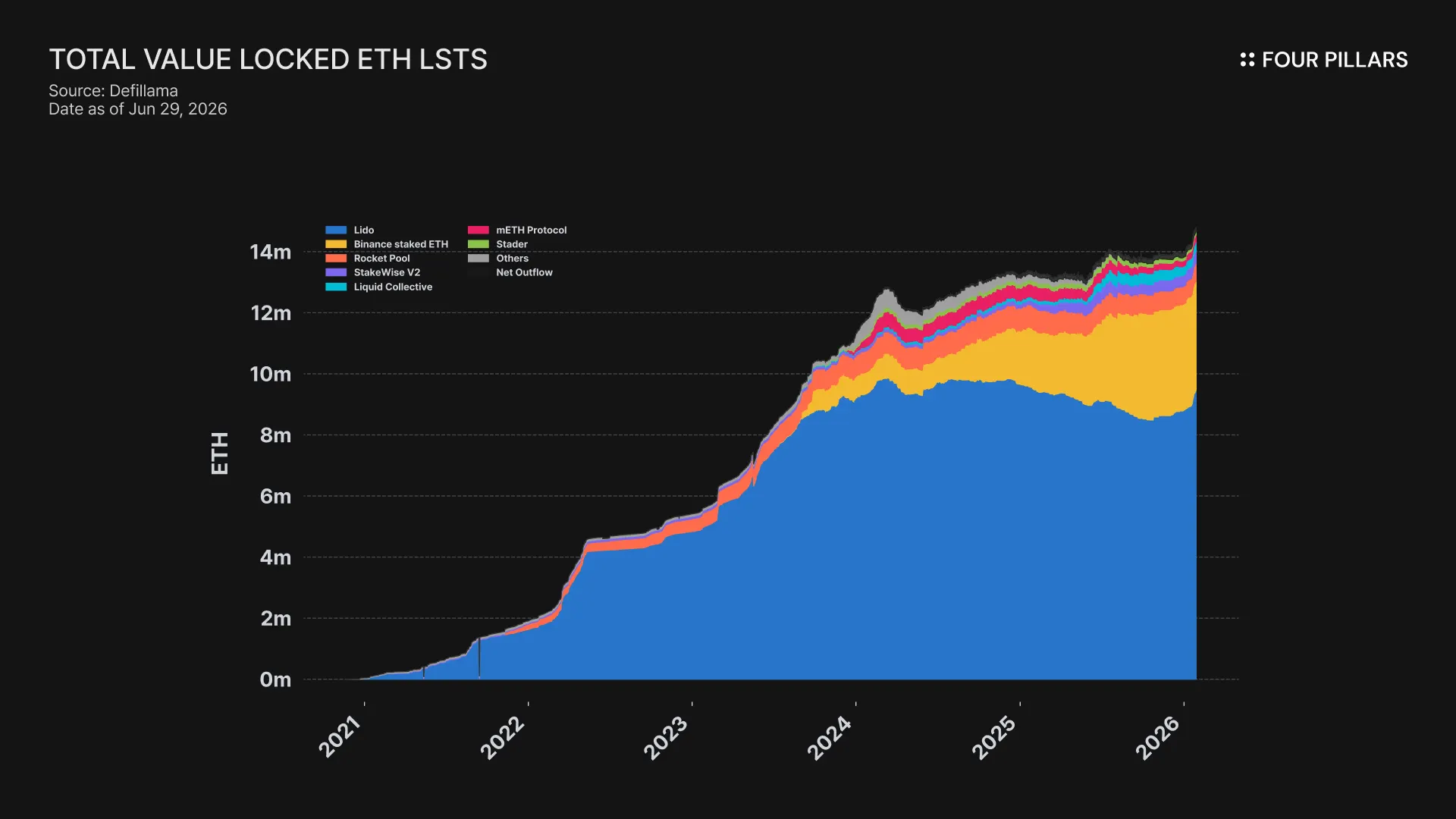

Meanwhile, competing LSTs captured 4.5M ETH, 29% of new stake (Binance staked ETH: +335%. Liquid Collective: +229%. StakeWise: +328%). Lido's share within liquid staking decreased from 90% to 65%.

Yield maximizers were a different problem. According to Lido's Q3 2025 tokenholder update, the "APR Maxi" segment grew from 2% to 20% of all staked ETH. Many used stETH, but as pass-through, not destination. Deposit into EigenLayer. Wrap through Ether.fi. Stack points on Renzo. Lido captured the staking layer but lost the value-add layer on top.

Here's what makes this worse: only 30% of ETH is even staked. 36.4 million out of 120.7 million. The other 70% hasn't moved yet. And in just the portion that has, Lido's share dropped from 33.5% to 26%. They're losing ground before the game has started.

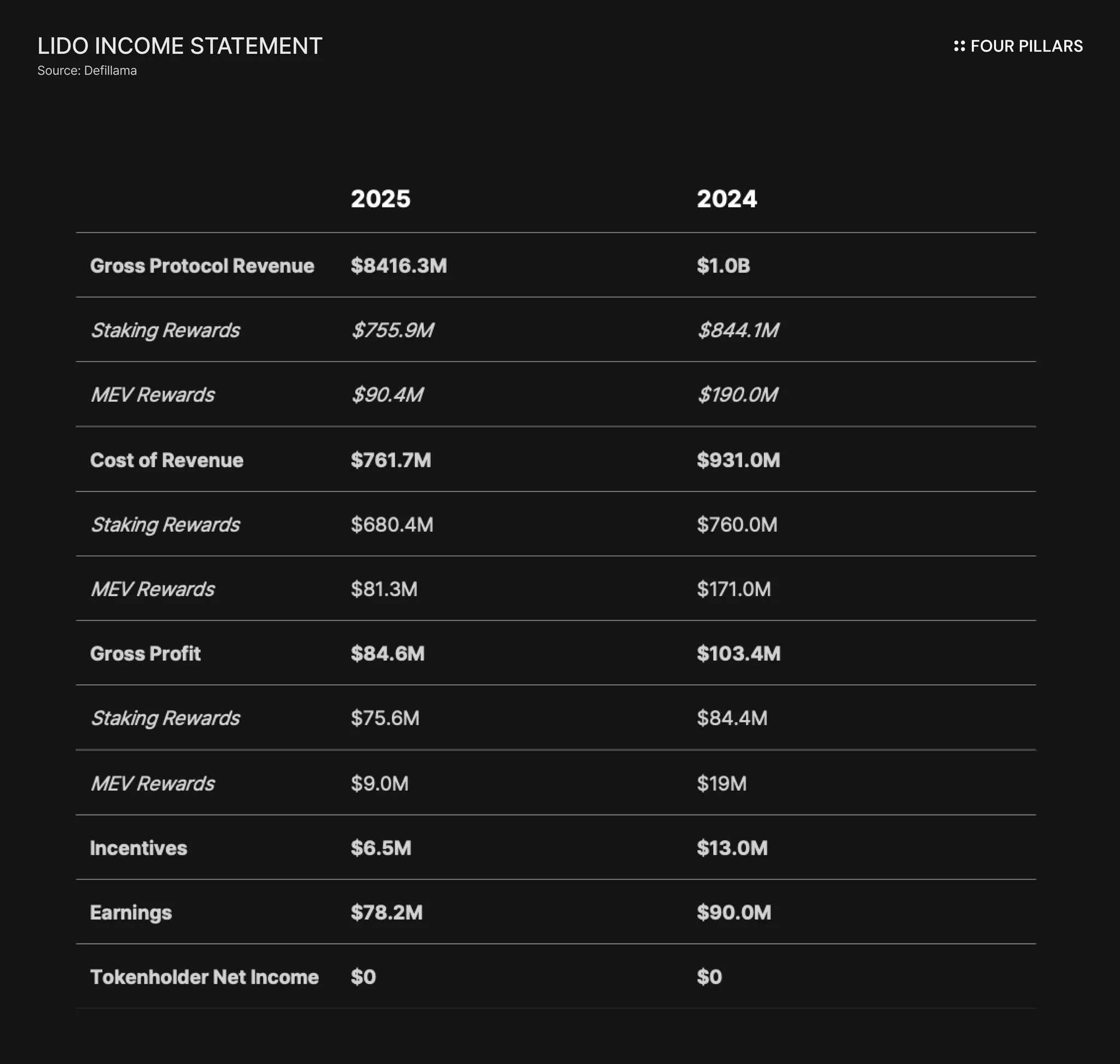

The cost is quantifiable. If Lido had maintained mid-2023 share, it would hold 2.7 million more ETH today, roughly $20 million per year in foregone gross profit. 2024 gross profit was $103 million, but 2025 came in at $85 million, signaling an 18% decline.

V3 is the response and Lido's bet on what the answer should be.

V2's architecture was deposit ETH, receive stETH, your assets enter a shared pool managed by Lido's Staking Router. Everyone got the same operator set, the same risk exposure, the same returns. If you wanted customization, you went elsewhere. Millions of ETH did exactly that.

V3 splits what V2 bundled. Risk and liquidity are now separate layers.

Source: https://v3.lido.fi/

The risk layer is the stVault, a non-custodial smart contract where you configure your own staking setup. You choose the operator. You set the fee arrangement. You decide the MEV policy, the client software, whether to bolt on DVT or restaking modules. Your ETH, your validators, your exposure. And critically, you retain the withdrawal credentials. The operator runs the infrastructure, but they can't touch the principal. EIP-7002 made this enforceable at the protocol level (you can trigger validator exits without operator permission).

The liquidity layer is stETH, but it's now optional. If you want liquidity against your vault position, you mint stETH as collateral. If you don't, you don't. The minting is overcollateralized; reserve ratios range from 2% to 50% based on a multi-factor risk assessment framework. DVT-enabled operators with client diversity can qualify for ratios as low as 2%, while concentration, track record, and operational setup all factor into the calculation. Higher-risk configurations require larger reserves, reducing mintable stETH.

Core Pool (the old V2 mechanism) still exists for passive stakers who want a simple user experience. But it now serves a second function—liquidity buffer and APR oracle for the entire system. All stETH redemptions route through Core Pool first, which protects stVault owners from having their positions unwound by random withdrawals. And stVault fees are benchmarked against Core Pool's APR, which prevents operators from gaming their own performance metrics. The system needs an honest reference rate; Core Pool's size and diversity make it hard to manipulate.

stVaults can't exceed 30% of Core Pool's size, so there's also a hard cap at launch. Lido is being conservative here, and honestly that's probably right because the mechanism needs to prove itself before it scales.

The architecture is live. The question is whether the segments Lido lost actually want what it's offering.

As mentioned above 55% of the 15.4 million new ETH went to non-liquid staking. Whatever their reasons, they chose not to use liquid staking tokens. V3's pitch to them is that everything direct staking offers, plus an optional liquidity layer you can ignore. stVaults give you full operator configuration, execution-layer exits via EIP-7002, MaxEB support for validators up to 2,048 ETH with auto-compounding. If you never mint stETH, you're effectively running a native staking operation with better tooling.

The institutional segment is where competing LSTs grew fastest (Binance staked ETH up 335%, Liquid Collective up 229%). What they offered was what Lido couldn't: segregation, compliance, auditability, actual legal agreements with known operators. V3 addresses this through partners like Northstake, which is building a Staking Vault Manager specifically for regulated entities—API/SDK for multi-vault orchestration, clear attribution, audit trails, the full compliance stack. P2P.org is launching Dedicated Vaults with similar institutional controls.

The pitch here is Lido's liquidity network with institutional wrappers. Whether that's enough to pull capital back from Binance is an open question (and honestly, the answer probably depends more on BD than architecture).

The APR Maxis are the segment Lido technically kept but failed to monetize. They used stETH, but as an input to EigenLayer, Ether.fi, Renzo, not as a destination. The value accrued to the restaking and LRT layers, not to Lido.

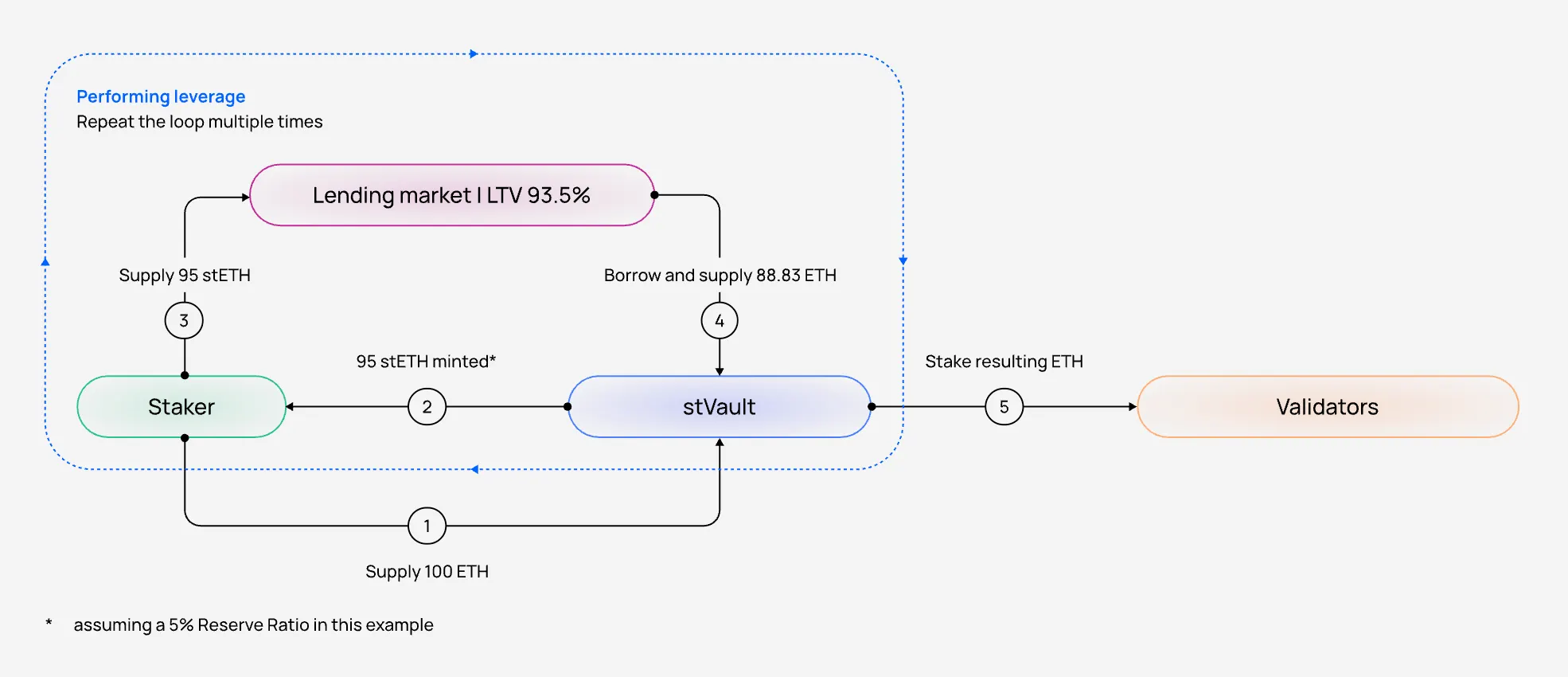

V3's play is to bring operators who might otherwise compete with Lido into its infrastructure instead. Symbiotic integration lets stVault operators offer restaking directly. Mellow wrapping lets them build custom LRT products. Rather than Lido sitting underneath these layers as dumb pipes, V3 creates a fee-generating partnership model (infrastructure fee, liquidity fee, and reserve fee) that aligns incentives between Lido and operators serving yield-seeking users. The leverage loop math works out as follows:

Vanilla staking: ~3% effective APR

Defi vault (Mellow): ~5.5% effective APR

Leverage loop (~9x): ~9% effective APR

Source: Example of leveraged staking, Lido V3 website

The integration ecosystem is already taking shape. Symbiotic and Mellow are named as integration partners in the whitepaper, with live deployments at launch. These integrations expand what's possible for stVault users while keeping stETH as the liquidity layer. The architecture is designed to be additive to the broader DeFi ecosystem.

The architecture addresses all three segments. What it can't do is guarantee adoption. That depends on whether the value prop actually lands, but the infrastructure is in place, and the early adopter pipeline is already building on it.

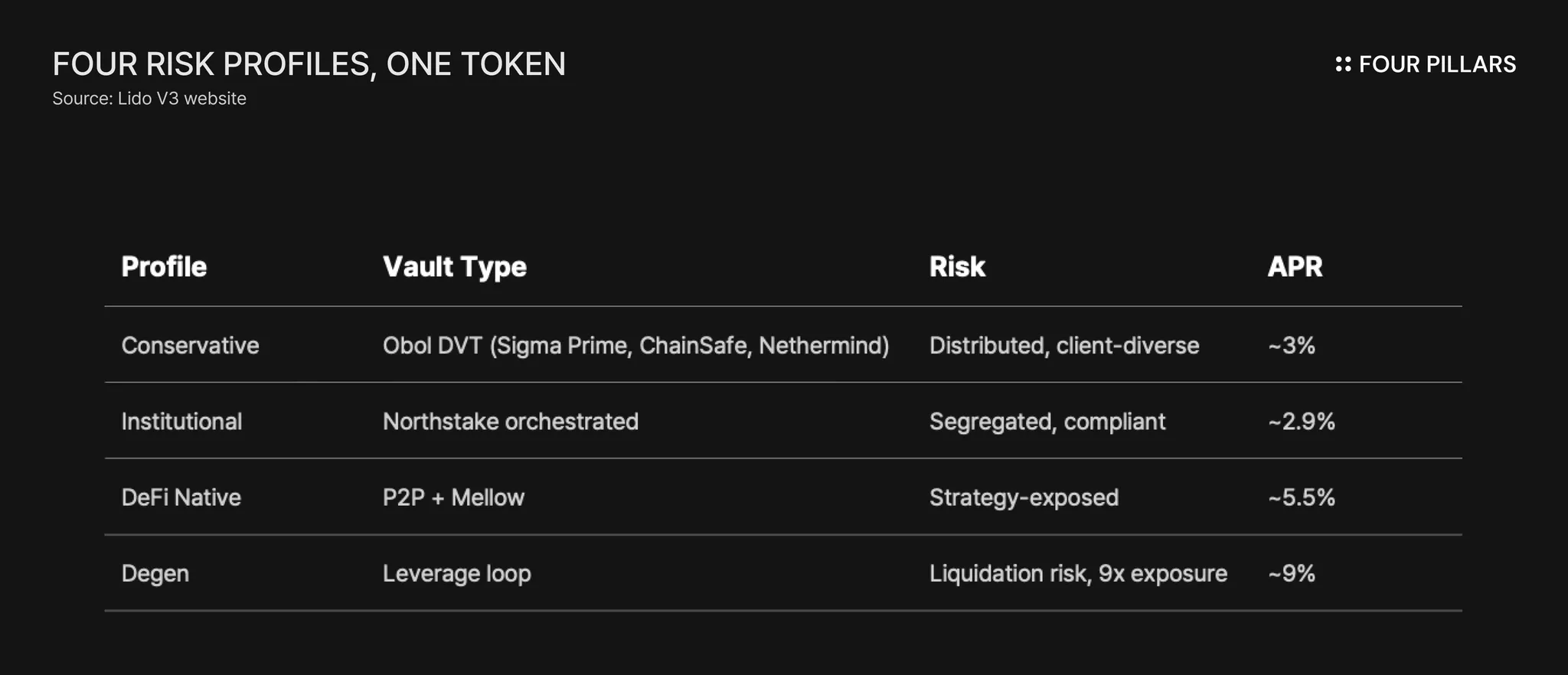

All four hold the same fungible stETH. A conservative institution running a DVT vault operated by Ethereum client teams (Sigma Prime, ChainSafe, Nethermind) and a high-risk participant running 9x leverage loops through Aave both use stETH as their liquidity layer, accessing the same liquidity depth, the same Curve pools, the same collateral eligibility.

The risk and reward differences come from their respective strategies, not from stETH itself. stETH functions as the common liquidity infrastructure that makes these diverse strategies possible; the varying exposure sits in the vault configuration and DeFi positions built on top.

If this works, stETH becomes something closer to a liquidity primitive that floats on top of whatever risk configuration you choose. The token's utility decouples from any single vault's exposure. You're not buying into Lido's operator set anymore. Instead, you're buying into the liquidity network, and you bring your own risk underneath.

Now, whether this framing actually holds depends on adoption. If 90% of stETH still comes from Core Pool a year from now and stVaults stay niche, nothing has changed in practice. The market decides if it matters. I lean toward it mattering, but I've been wrong about adoption curves before, and frankly this one requires institutional BD cycles that move slower than CT wants them to.

The architecture isolates more than V2. But "more" isn't "complete," and if you're sizing positions based on the assumption of full isolation, you're going to learn an expensive lesson in a tail event.

Here's what's isolated: operator performance stays in your vault. Your operator takes downtime, that's your APR drag, not mine. Slashing hits your reserve buffer first. Your leverage liquidation is your problem. In normal operations, vault risk is genuinely siloed.

But forced rebalancing isn’t isolated. If your vault's health factor drops below threshold, ETH transfers to Core Pool to cover the stETH liability. You don't lose principal, but you lose the position. Your leverage unwinds whether you wanted it to or not. And in a correlated slashing event (mass validator failure from a client bug, say), the 5-50% reserve buffer won't cover it. Core Pool absorbs tail risk. Protocol-level failures (oracle manipulation, governance attacks, smart contract bugs) hit everyone holding stETH regardless of vault configuration.

The mitigations are real. Tiered collateral means concentrated operators require higher reserves, which creates first-mover advantage in each tier. LIP-23 proposes zkOracle verification with auto-pause on mismatch. Dual Governance is already live.

But this is 95% unbundling. On normal conditions, it’s your risk, your vault. During black swan events, still socialized. If you're building a thesis on complete isolation, you're building on sand. The architecture is meaningfully better than V2. It's not a different category of safe.

For Lido, the TAM expands. The question shifts from "who will accept pooled risk for liquidity" to "who wants ETH liquidity with configurable risk underneath,” a substantially larger set. The segments that moved elsewhere are now architecturally addressable without forcing them into a one-size-fits-all model.

For stakers, the choice matrix expands. Passive users can remain in Core Pool with no changes. Active stakers can select vaults where diligence translates into tiered reserve advantages. Yield-seeking users gain native composability options that previously required building around Lido. The UX complexity increases (choosing among dozens of vault configurations is not simpler than "deposit and forget"), but optionality exists for those who want it, and Core Pool remains available for those who don't.

For the broader DeFi ecosystem, V3 is designed to be additive. Restaking and LRT protocols gain a cleaner integration path with stETH as the liquidity layer. The architecture creates partnership opportunities, aligning incentives across the stack.

70% of ETH isn't staked. The game is early.

Here's what I'll be watching: stVault TVL as a percentage of total Lido TVL—GOOSE-3 targets 1M ETH, which is the internal benchmark for whether this is working. Yield maximizer capital flowing back through Mellow and Symbiotic integrations; if APR Maxis start building through Lido rather than on top of it, the thesis is playing out. Institutional adoption through Northstake and P2P, which moves slower but stickier.

Lido built stETH into the most liquid staking token in crypto over five years. V3 is the bet to recapture the 2.7M ETH that left, and to become the infrastructure layer for however the next 70% decides to stake.

Dive into 'Narratives' that will be important in the next year