Huma 2.0 unlocks short-term settlement yields for all users, shifting from an institution-only platform to an open DeFi protocol.

Borrowers pay daily fees (1–5 day loans), compounding into 10–15% yields sourced from real payment activity.

Only regulated financial entities in developed markets borrow, aiming to minimize default risk and distance Huma from typical P2P concerns.

Leveraging Solana’s speed and composability, Huma expands globally. Sustained success depends on strict credit standards and transparent risk management.

With Huma 2.0, Huma Finance extends its real-world payment financing model to an open, decentralized platform. This marks an evolution from its earlier product, Huma Institutional, which was a permissioned structure focused on accredited and institutional investors. The new permissionless release embraces a broader user base, offering stablecoin depositors an opportunity to earn real yield from short-term payment flows, a model collectively described as “PayFi” (Payment Finance). In this article, we summarize how Huma 2.0 works, highlight key statistics, explore its strategic role in the Solana ecosystem, and evaluate its risks and opportunities.

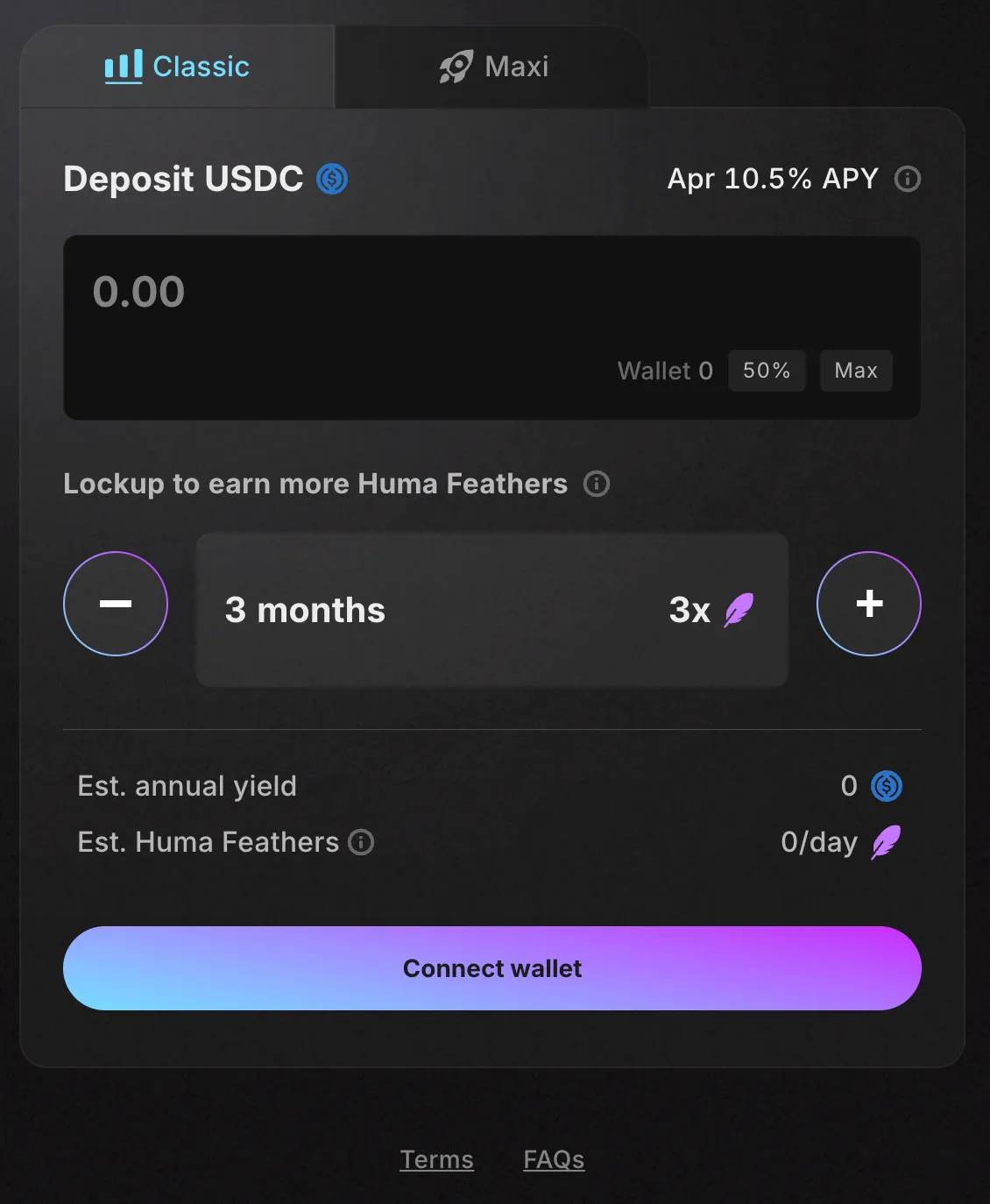

Open Access: Anyone can deposit stablecoins ($USDC) into Huma’s liquidity pool, with no KYC required (except for geoblocking certain jurisdictions).

Payment Financing Mechanism: The deposited funds are provided as settlement liquidity, a form of short-term credit (commonly 1–5 days) to vetted, licensed payment companies. Borrowers use this liquidity to settle transactions promptly rather than waiting on slower banking rails or pre-funding these payments.

Yield Generation: Borrowers pay fees for this liquidity. Because the capital can be “turned over” multiple times per month, depositors can earn robust recurring yields sourced from real economic activity (not token inflation). Historically, Huma’s yields ranged from 10% to 15% APY.

Classic vs. Maxi Modes: Depositors can choose:

Classic Mode pays a stable rate in $USDC (currently ~10% APY) plus a baseline rewards allocation (called Feathers).

Maxi Mode forgoes the $USDC interest in exchange for earning a higher rate of Feathers rewards.

Optional Lockups: Depositors may lock their deposits for 3 or 6 months to multiply Feathers rewards. Locking is voluntary. Those who prefer immediate liquidity can remain unlocked.

PayFi Strategy Token (PST): Huma mints $PST (an LP token) for deposits in Classic Mode. PST automatically accrues interest and is freely transferrable on Solana, enabling integration with other defi protocols.

Previously, Huma operated a permissioned platform, admitting only accredited and institutional investors. Tranche-based structures and legal frameworks were in place to tokenize receivables. With Huma 2.0, these restrictions have been lifted. Depositors need only connect a Solana wallet (with location-based restrictions applied in the background). While the new platform has no formal accreditation checks, Huma still performs compliance and due diligence on borrowers.

Source: app.huma.finance

Huma’s mission is to give everyday users the same financing returns banks and large institutions enjoy. As Huma put it, “the opportunities previously reserved for institutions are now available to everyone, and it’s about time.” Traditionally, banks and financial institutions provide the settlement liquidity for cross border payments and card transactions, charging high fees. Such returns have been inaccessible to small investors. By bringing these payment flows on-chain, Huma seeks to “open the market to everyone,” aligning with defi’s ethos of permissionless participation.

From a market timing perspective, Huma 2.0’s launch comes at an opportune moment. The crypto industry has gone through a deleveraging bear market where many defi yields dried up, while off-chain interest rates climbed (e.g. U.S. Treasury bills yielding ~5%). Investors large and small are seeking stable, uncorrelated yield sources. Moreover, crypto has witnessed swings from high-yield “farming” in bull markets to near-zero yields in bear markets. Many yields depended on token emissions rather than real revenue. Huma’s PayFi model offers a yield that is decoupled from crypto market cycles, since people continue to make payments and trade in any market condition.

Last but not least, scaling liquidity. Huma’s pilot phase saw roughly $55 million in the pool. Transitioning to a permissionless, globally open platform lets Huma tap into the broader defi capital base. Increased liquidity can support more payment clients, in turn generating higher fees and potentially higher returns. This reflexive cycle of “more liquidity → more payments → more yield” underpins Huma’s growth thesis.

Deposits and $PST: Users deposit $USDC, receiving $PST (PayFi Strategy Token) in Classic Mode. PST represents a claim on the underlying liquidity. The token’s value accrues interest in real time, reflecting the fees that borrowers pay.

Short-Term Loans: Vetted payment companies use these stablecoins as settlement liquidity. Each loan spans a short window (one day to a few days) ensuring quick recycling of capital.

Fees and Automatic Rollover: Borrowers pay daily fees for liquidity, which accumulate into the pool. The protocol continuously updates the $PST token price to reflect earned interest. If deposits remain, those funds get redeployed to new borrowers automatically.

Maxi Mode: Users choosing Maxi Mode receive no direct $USDC interest but earn more Feathers (Huma’s reward points). They can switch between Classic and Maxi to balance immediate yield vs. future reward potential.

Withdrawals: Since many loans mature daily, withdrawals are processed quickly. Huma’s short cycle times minimize liquidity lockups, although in a major bankrun, Huma could impose daily withdrawal caps or short redemption pauses to orderly unwind loans. A small portion of the deposits are held in liquid DeFi positions to help meet redemption requests quickly.

As mentioned above, Huma 2.0 also introduced Feathers, a reward system for both Classic and Maxi depositors. Maxis get larger Feathers allocations to compensate for the forgoing of interest. Feathers themselves are not yet tradeable tokens. However, Huma states that they will be convertible or have governance utility if/when a future token launches. This gives early depositors upside beyond the base APY. Optional 3- or 6-month lockups further multiply Feathers for those comfortable with less liquidity, although even the 6-month locked PST can be swapped to USDC at a slight discount in secondary markets.

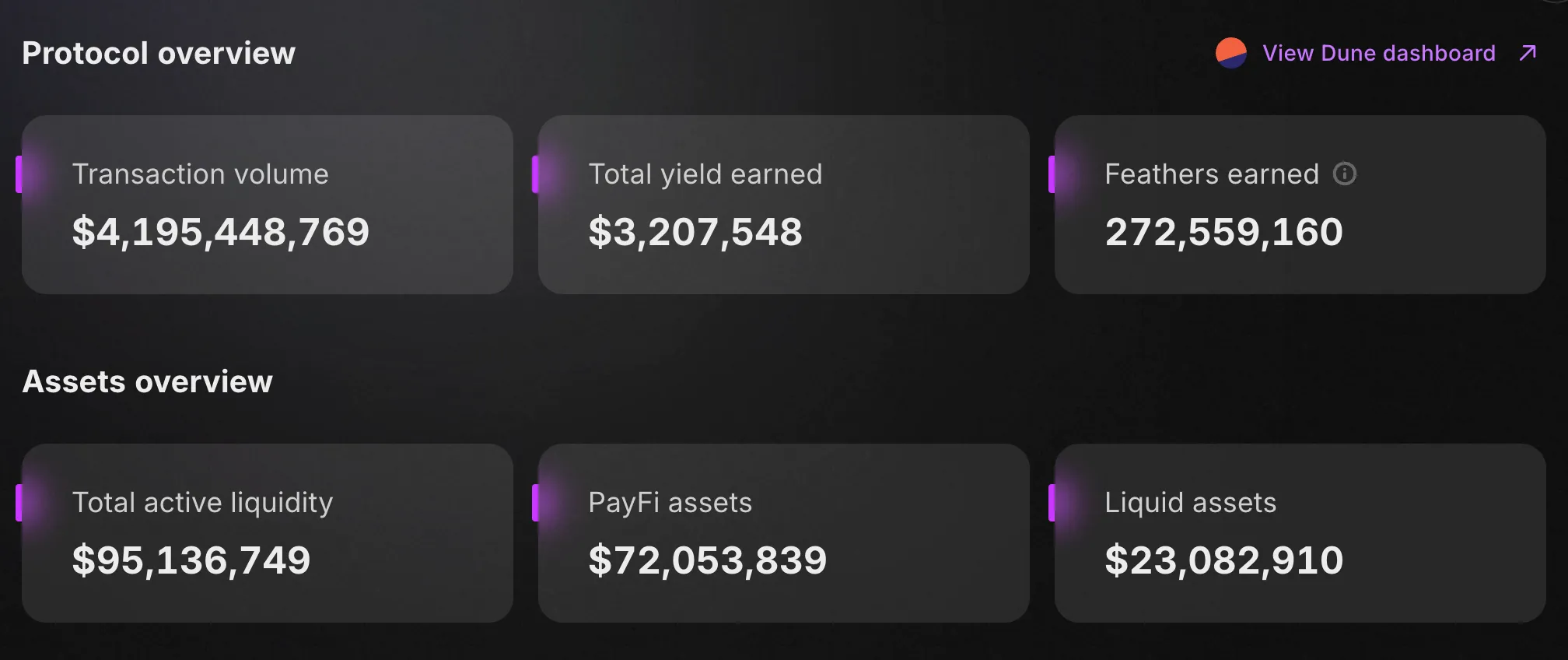

Despite being newly permissionless, Huma’s underlying payment financing has existed for over two years. According to Huma’s data room, the platform has facilitated over $4.1 billion in cumulative payment volume through its underlying institutional structure. Annualized revenue sits at approximately $8 million, enough to fund double-digit interest rates for depositors. Huma reports no defaults to date, attributing this outcome to only having licensed financial institutions as borrowers and the inherently low credit risk of funding payment flows that are already in flight.

As of April 15 2025, Huma 2.0 holds nearly $70 million in active liquidity, up from around $20 million under the older institutional system. During the transition to a permissionless model, the average APY for Classic Mode stands near 10%, though previous returns were often in the 12–15% range. Huma cautions that APYs may adjust based on borrower demand and the supply of deposits.

Source: Huma Finance Data Room

Solana is positioned as a blockchain capable of handling real-time payments due to its high throughput and low transaction fees. Huma’s decision to launch on Solana enables near-instant minting and burning of $PST, along with rapid daily fee settlements. A central idea in Solana’s PayFi narrative involves using stablecoins for immediate settlements, plus merging payment rails with defi services such as factoring, lending, and yield aggregation. Huma’s system aligns with this vision by tokenizing the time value of money in commercial transactions. Merchants or remitters get instant settlement via stablecoins, and Huma’s depositors collect fees for bridging any timing gap in those settlements.

The PST token is built using the Solana Program Library (SPL) standard, which is recognized across multiple defi applications on the network. Huma has announced integrations with protocols like Jupiter Swap, where $PST holders can exchange their tokens for $USDC without waiting for official redemption. Additional collaborations with projects like Kamino Finance and prospective interest rate derivative platforms illustrate Huma’s goal of embedding its yield-bearing token throughout the Solana ecosystem. For example, defi protocols seeking stable returns might deposit into Huma. Meanwhile, Huma benefits from Solana’s stablecoin liquidity and its broad user base.

Source: Huma Finance

A recent debate questioned whether Huma 2.0 (promising double-digit yields) was essentially a high-interest lending pool mirroring traditional P2P. Critics argued that in P2P settings, borrowers unable to secure lower rates often resort to costlier loans with higher default risks, citing past failures under weak underwriting. They noted that businesses typically borrow at lower rates (e.g. 4–5%), suggesting only riskier clients might pay more.

Huma’s team strongly refuted the P2P comparison, stressing three core distinctions that ultimately helped dispel much of the skepticism:

Licensed, Payment-Centric Borrowers: The protocol lends to regulated financial institutions (default risk expected to be under 0.5%) in developed markets for payment-related tasks (cross-border settlements, near-instant payouts), not unsecured consumer or SME loans.

Ultra-Short Maturities: Elevated APYs arise from daily fee structures (1–5 days), unlike months-long P2P. Huma’s clients view rapid turnover as operationally beneficial for time-sensitive transactions. The 6-10bps fee charged per business day, a highly competitive rate compared to alternatives, accumulates to 15-20% annualized yield due to rapid recycle of funds.

Compliance Framework: Huma partners with Arf, emphasizing “conservative underwriting” (verifying transaction volumes, collateral, licensing) to avoid unregulated P2P pitfalls.

Selective Payment Financing: Huma rejects many invoice-financing requests, focusing instead on bridging funds already in the system. The team likens it to replacing “traditional mail” with stablecoin “email,” lowering risk relative to factoring unverified invoices.

Huma acknowledges that no credit-based system, especially one offering daily liquidity, can eliminate default risk. A borrower’s sudden distress or oversight lapses could still result in losses. While high yields may attract borrowers needing premium-priced capital, Huma insists these are legitimate institutions with short, predictable cash-flow cycles.

Key Mitigating Factors

Short Duration: Daily or near-daily renewals enable early detection of problems.

Payment-Focused: Most funds support T+0 cross-border settlement or same-day merchant payouts. Borrowers use safeguarding accounts to secure payment flows.

Measured Expansion: Huma prioritizes thorough underwriting over rapid scaling.

Skeptics likened high rates to P2P models attracting weaker borrowers. However, Huma’s focus on verified institutions, strict compliance, ultra-short maturities, and avoidance of invoice financing largely addressed these concerns. Though short-term lending carries inherent risk, broad criticism has subsided, underscoring Huma’s divergence from traditional P2P or factoring models.

Community response, especially in online Spaces with KOLs, turned positive. Many observers concluded that Huma differs substantially from P2P, offers credible yields from real payment flows, and demonstrates careful compliance and risk management. Notable figures like @CalmanBTC highlighted Huma’s openness on revenue mechanisms and lockup incentives. The community requested more transparency on underlying assets, and Huma pledged additional disclosures. Meanwhile, accelerated deposits (on-chain data) suggest confidence surged, indicating that Huma succeeded in attracting new capital.

Huma 2.0 signifies a transition from a closed, institution-oriented credit scheme to a permissionless defi protocol enabling everyday users to finance short-term payment flows. Its guiding principle is straightforward: borrowers pay daily fees for settlement liquidity, while depositors earn returns from these structured transactions. By leveraging Solana’s high throughput and composability, Huma aims to broaden the protocol’s liquidity base and integrate seamlessly with various defi platforms.

Recent statistics reinforce Huma’s potential: over $4.1 billion in historical payment volume, no credit defaults to date, and steadily rising TVL. Although questions linger about whether double-digit yields might draw inherently higher-risk borrowers, Huma underscores that its clientele consists primarily of licensed institutions seeking short-duration liquidity for real-time settlement, a demographic it contends is fundamentally different from typical P2P or invoice-financing borrowers. By intentionally specializing in cross-border payments and credit card flows rather than venturing into areas like truck financing or long invoicing periods, Huma believes it can mitigate many of the sector-specific risks tied to conventional trade finance.

Looking ahead, Huma’s capacity to maintain strict underwriting standards, match depositors’ capital with legitimate payment flows, and adapt to shifting market or regulatory environments will be crucial. Historically, high-yield lending initiatives have struggled to scale without experiencing spikes in default. If Huma can preserve its compliance-driven, operational focus while meeting growing demand, Huma 2.0 could solidify its place in Solana’s evolving PayFi narrative. Its combination of genuine revenue streams, composable token structures, and rapid credit turnover exemplifies both the promise and intricacy of uniting real-world financial processes with decentralized networks. Ultimately, whether Huma continues to deliver stable yields without compromising on credit risk remains a core question, but one in which the team’s consistent track record and specialized sector strategy offer growing reassurance.

Dive into 'Narratives' that will be important in the next year