*Asia Stablecoin Alliance is launched by Heechang Kang and Jinsol Bok from Four Pillars, along with Alex Lim (Jongkyu Lim), the Korea lead at LayerZero, to accelerate stablecoin adoption across Asia and to serve as a research and community hub for establishing clear stablecoin strategy and technical infrastructure. (X Link, Substack Link)

A KRW stablecoin should be viewed not as an end in itself but as a means to an end. Its value lies in being deployed for specific use cases. In this respect, stablecoins can play a meaningful role as infrastructure for the distribution and settlement of security-like assets.

Tokenizing Korean government bonds could bring technical efficiency to a structure that is already actively used in traditional markets. Beyond government bonds, assets such as unlisted equities and private equity funds are also strategically well-suited for tokenization.

For the stablecoin industry to grow, it’s important to develop and promote Korea’s “three digital asset laws” — the Basic Act on Digital Assets, STO regulation, and crypto ETFs — in a coordinated and integrated manner. Only with such a holistic approach can a KRW stablecoin become a true cornerstone of the digital asset market.

There is already a strong consensus in Korea regarding the need for a KRW stablecoin. As a means to maintain monetary sovereignty in the digital age at a national level, many argue that a KRW stablecoin must exist. However, the truly important question comes next: where and how can it actually be used? Technological experiments without real use cases often result in policy failures. As was once the case with the ‘Metaverse’, KRW stablecoins also risk repeating similar failures if promoted without a clear purpose.

In particular, USD-based stablecoins (like USDC, USDT) can function as a hedge against inflation or a tool for gaining access to dollar-denominated assets in emerging markets. However, since KRW is not a globally accepted currency, a KRW-based stablecoin cannot serve as a purpose in and of itself. Thus, it must function as a means, and its existence must be grounded in specific use cases.

So, in which sectors could KRW stablecoins realistically be used? Possibilities include simple payment systems, online commerce, digital asset platforms, and cross-border payments. Among these, the most promising direction currently is in combination with financial assets, particularly through synergy with tokenized securities. In fact, according to a recent BCG report, of the $26.1 trillion in total stablecoin transaction volume in 2024, approximately $800 billion (3%) was used in the settlement of tokenized securities. This is the largest proportion among non-crypto trading (88%) or on/off ramping (4%) use cases, showing that stablecoins are beginning to serve a practical role in the distribution and settlement infrastructure of security assets.

These data indicate that the “KRW stablecoin – tokenized securities” pairing is not just a conceptual idea, but a structure that is already being tested in global markets. This supports the possibility that it could become a major use case within Korea’s financial system as well.

Currently, the most watched assets in the tokenization market are U.S. Treasuries (UST). Various cases such as BlackRock’s BUIDL and Franklin Templeton’s BENJI have already emerged, drawing great interest as stable income-generating assets operable on-chain. So could a structure like “KRW stablecoin – KTB token” have a similar appeal as the “USD stablecoin – UST token” combo?

First, the main demand sources for tokenized U.S. Treasuries can be divided into two groups: traditional financial institutions that want access to treasuries themselves, and retail investors who want to participate in onchain finance. In the case of KTBs, there is little reason for global investors to access them, so the latter group is likely limited. However, the former, domestic institutional investors who require KTBs, certainly exists.

For instance, domestic banks and insurers hold large volumes of KTBs as High-Quality Liquid Assets (HQLA) to meet Basel III regulations. Securities firms use KTBs as collateral for RP, futures, and options trades. In this way, KTBs already function as a core collateral asset in the Korean financial system. The next question is whether tokenization can make this structure more efficient.

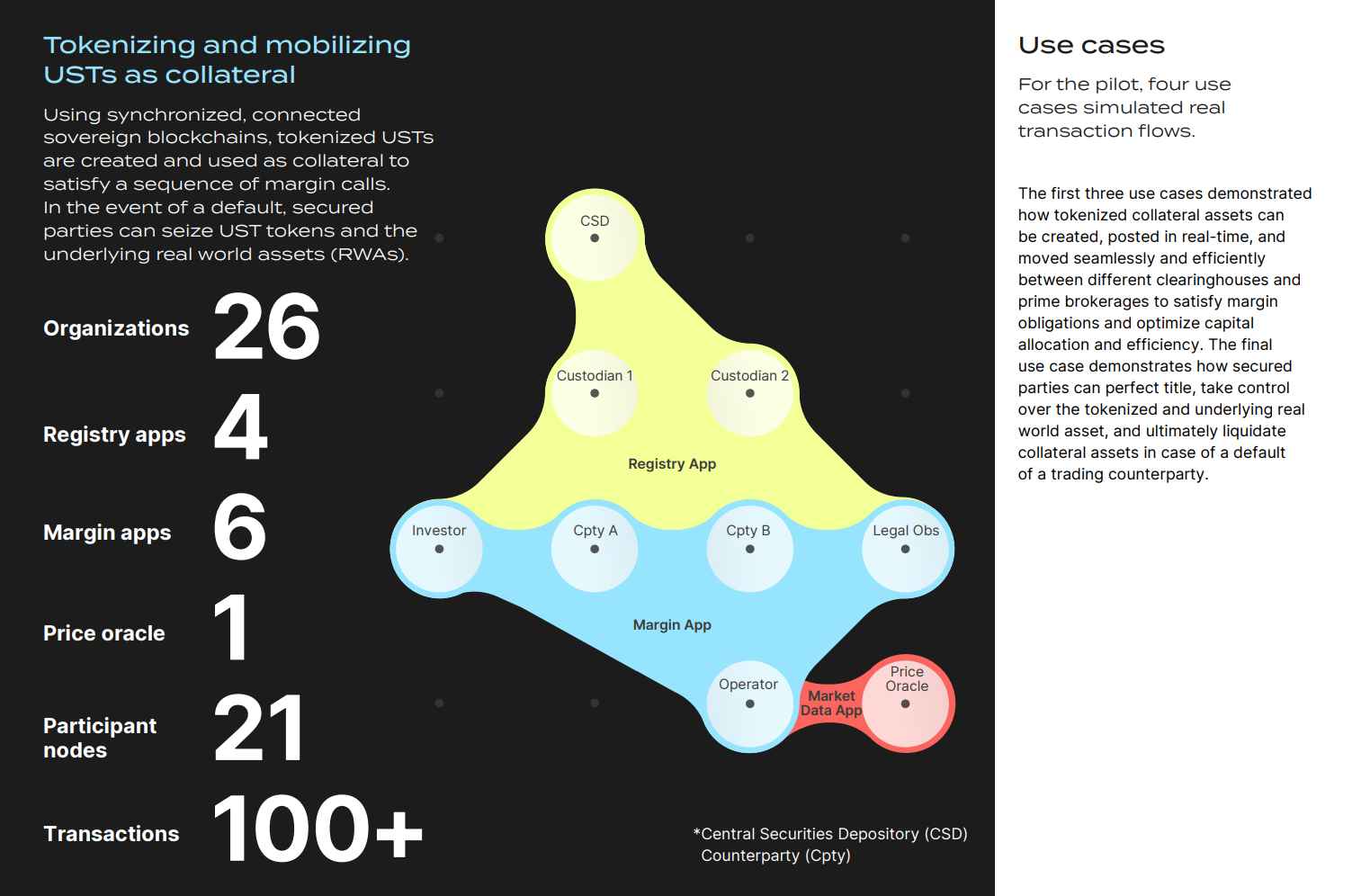

Source: DTCC, Digital Asset Tokenize US Treasuries for Collateral

The answer can be found in the UST tokenization pilot jointly run by the U.S. Depository Trust & Clearing Corporation (DTCC) and Digital Asset. This pilot involved 26 banks, investors, CCPs, and custodians, demonstrating that tokenized USTs could practically improve the full lifecycle of margin transactions as collateral.

Key functions tested in the pilot include:

Tokenized asset issuance: Investors request the creation of tokenized assets based on their USTs, and custodians isolate actual USTs matching DTCC balances.

Collateral submission: When CCPs or Prime Brokers issue margin calls, investors select UST tokens as collateral, which are set in real-time.

Collateral release: Upon investor request, tokens are immediately unlocked, enabling reuse in other transactions. This dramatically improves liquidity turnaround compared to T+1/T+2 settlement.

Default settlement: In simulated defaults, ownership of collateral is automatically transferred based on smart contracts, in line with master agreements (e.g., ISDA).

This experiment shows that tokenization can go beyond merely digitizing bonds—it provides experimental proof that margin, collateral, and repo structures can be fundamentally redesigned.

In particular, Korean Government Bonds (KTBs) are already widely used as key collateral assets by domestic financial institutions. Banks and insurers hold KTBs to meet the Liquidity Coverage Ratio (LCR) under Basel III, and securities firms use them for RPs, futures/options margin, securities lending, and more.

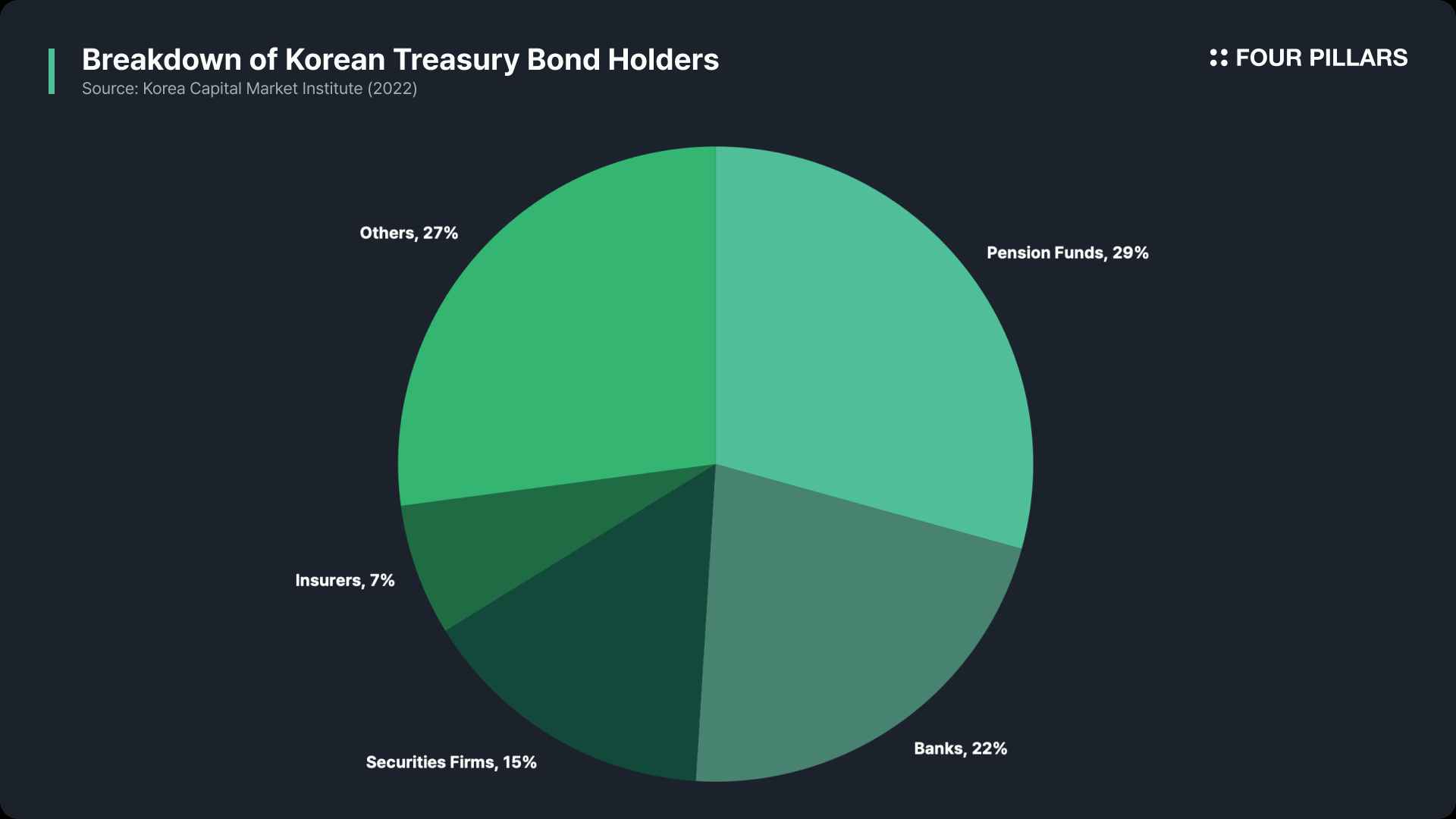

As of 2022, pension funds held 29.3%, banks 21.7%, securities firms 15.2%, and insurers 6.7% of all outstanding KTBs. These institutional holders account for about 77%, indicating that KTBs are real-use assets with steady institutional demand, not merely speculative instruments.

Tokenizing KTBs in this structure would combine technological efficiency with already-functional asset structures. It would enable automation of collateral registration and release, 24/7 use, real-time recall and reuse, and automatic liquidation via smart contracts in RP systems, margin management, and inter-institutional collateral exchange. This is not just a tech experiment, it’s a realistic transformation grounded in institutional demand.

If not KTBs, what other securities are attractive for tokenization? I believe the fundamental value of tokenization lies in making illiquid securities liquid.

From this perspective, private stocks and private funds are appealing. Private stocks are seen as the first logical target, Robinhood, for instance, recently announced plans to support trading of private stocks like OpenAI and SpaceX for European investors. As for private funds, they are essentially the pinnacle of illiquidity, requirements in the hundreds of millions of KRW, no redemption before maturity, making them prime candidates for improvement through tokenization.

Examples include the Apollo Diversified Credit Securitize Fund (ACRED) and Blockchain Capital III Digital Liquid Venture Fund (BCAP), both issued via Securitize and representing private credit and venture capital, respectively.

The Apollo Diversified Credit Securitize Fund (ACRED) is a multi-strategy private credit fund managed by global alternative asset manager Apollo, tokenized via the Securitize platform. It’s registered under Regulation D of the U.S. Securities Act and targets accredited investors in the U.S., with the entity incorporated in the British Virgin Islands.

ACRED invests across five core credit strategies: senior corporate loans, asset-backed loans, high-liquidity quality bonds, opportunistic distressed assets, and structured debt (CLOs, RMBS, CMBS). It targets both stable yield and capital appreciation.

The minimum investment is $50,000, and tokens are issued as ERC-20s or native formats across Ethereum, Solana, Aptos, and Avalanche. As of 2025, it manages around $98M in total assets, has a NAV of $1,036, and charges a 2% annual management fee with no performance fee.

The Blockchain Capital III Digital Liquid Venture Fund (BCAP) is the world’s first tokenized venture fund, issued in 2017 by Blockchain Capital via a Singapore-based entity, TokenHub. It is also a Regulation D private offering with legal jurisdiction in the Cayman Islands.

BCAP invests in blockchain-native companies such as Coinbase, Circle, Kraken, Securitize, OpenSea, and Ripple, as well as assets like Filecoin, Bitcoin, and Ethereum. It follows a venture strategy using SAFEs, SAFTs, convertible notes, and private equity.

The minimum investment is $20,000. As of June 2025, it is distributed as an ERC-20 token on zkSync Era, with $148M in total assets, NAV of $16.29, a 2.5% management fee, and a 25% performance fee. Profit is distributed annually as carried interest, with some retained for reinvestment.

For tokenized securities to succeed, a suitable blockchain infrastructure is critical. Various players are competing in this space.

First, Ethereum and other EVM chains face structural limitations for tokenized securities. These securities must account for investor information (KYC), nationality, and eligibility, requiring added features. To solve this, many projects use specialized tokenization platforms like Securitize, which uses its proprietary DS Protocol to restrict token transfers based on investor credentials. Securitize handles major tokenized offerings from BlackRock, Apollo, and VanEck.

Other chains like Stellar provide this functionality natively. For example, Franklin Templeton’s BENJI is the largest tokenized fund on Stellar, thanks to its “trust-line” feature, which allows pre-approval of asset holders. Ripple has similar mechanics, which is why it’s increasingly mentioned in RWA tokenization contexts.

A third category involves private blockchain infrastructure. A key example is the Canton Network, which uses the Daml smart contract language and provides privacy by ensuring only participants see transaction data. The UST pilot mentioned above ran on Canton, and institutions like Circle, Hashnote, and Broadridge are testing on it.

From my perspective, the most critical factors for tokenized security infrastructure are:

Built-in RBAC (role-based access control)

Integration with fund back-office systems (e.g., accounting, trade matching, compliance)

Balance between public chain openness and private chain control

Delta Network aims to meet these requirements through its two-tier architecture, consisting of a global asset ledger and private domains.

Tokenized securities are not just the next stage of stablecoins; they represent one of the most practical use cases for KRW stablecoins. In the U.S., traditional financial institutions are already tokenizing treasuries, private funds, and real estate, creating new onchain financial infrastructure.

Korea, too, if considering KRW stablecoin issuance, should also explore tokenized securities (STOs). As mentioned in Rep. Min Byung-deok’s interview, it is desirable to jointly pursue the so-called “Digital Asset Three-Laws”—comprising the Digital Asset Basic Act, STO framework, and crypto ETF policies. Such an integrated approach is essential for KRW stablecoins to become truly central to the digital asset ecosystem.

Dive into 'Narratives' that will be important in the next year