South Korea is rapidly establishing a legal framework for a Korean won-based stablecoin, but the discussion remains focused on issuance requirements and regulation. There is a lack of practical plans for actual use cases—raising concerns that the technology may go unused after issuance.

Lotteries are an already popular and marketable sector. Introducing stablecoins as a payment method and prize payout mechanism, or transitioning to a blockchain-based system, could generate strong synergies in transparency, efficiency, and scalability. This offers a concrete use case for the Korean won stablecoin that can deliver a new user experience.

Combining lotteries and stablecoins could be a way to drive the mass adoption of the Korean won stablecoin. However, there are significant real-world challenges, such as legal regulations, user accessibility, and security. Nevertheless, this model serves as a strong starting point to demonstrate how a Korean won-based stablecoin can create real social value.

As of 2025, one of the hottest topics in South Korea's financial market is undoubtedly the "KRW stablecoin." With the global digital asset market being reorganized around dollar-based stablecoins—and their influence rapidly growing in Korea—the government and financial institutions are accelerating legislative efforts. Their aim is to secure "monetary sovereignty" and foster a new driver for financial innovation. Expectations are soaring as moves to revise the “Basic Digital Asset Act” and establish a legal basis for the issuance and circulation of stablecoins gain momentum.

Key Points of the KRW Stablecoin Legislation Discussion

Issuance Eligibility: Only banks and fintech companies with at least KRW 1 billion in equity and approval from the Financial Services Commission can issue stablecoins.

Reserve Requirements: 100% of the issued amount must be backed by cash or other safe assets, which must be audited regularly and disclosed publicly.

User Protection: Reserves must be segregated from company assets, and issuers must guarantee immediate redemption upon user request.

Supervisory Framework: The Financial Services Commission will take the lead in oversight, with the Bank of Korea participating to help maintain monetary stability.

However, beneath the excitement lies an undercurrent of concern. The Bank of Korea, as the monetary authority, remains cautious, warning of potential systemic risks such as mass withdrawals (bank runs) or diminished effectiveness of monetary policy. Caught between innovation and stability, the KRW stablecoin is only now beginning to knock on the door of institutional legitimacy.

Current discussions around stablecoins are overly focused on who will issue them and how. However, a far more fundamental question remains: Who will continuously use the issued stablecoins, why, and for what purpose? In other words, the conversation around actual use cases is nearly absent.

A KRW stablecoin, which is not backed by a global reserve currency, cannot succeed simply by replacing existing payment methods. In South Korea, where the fintech ecosystem is already one of the most advanced in the world, such a strategy lacks competitive edge. Without providing entirely new value or user experiences through killer content, the KRW stablecoin could end up as a “white elephant”—a costly but unused technology, despite enormous public investment.

Source: Yonhapnews

One of Korea's most infamous "white elephant" cases is the Yeongam F1 International Circuit. The Jeollanam-do Province government spent KRW 430 billion in taxpayer money to build the circuit, but due to poor accessibility from the Seoul metropolitan area and high operating costs, the project failed to attract crowds. The F1 races were discontinued after just four years, and the facility now stands as a prominent example of wasteful public spending.

Likewise, if there is no serious consideration for viable use cases, the KRW stablecoin may also lack a sustainable revenue model for issuers—ultimately draining momentum from the entire ecosystem and reducing what could be groundbreaking innovation into a half measure.

Source: news1

Although the KRW stablecoin is still in the planning and discussion stages, it is essential to find practical answers to the question of “use cases.” This article proposes one such idea: utilizing the stablecoin in the lottery industry. The lottery is already a massive market with broad public recognition, and combining it with the technological features of a stablecoin could create an intriguing synergy.

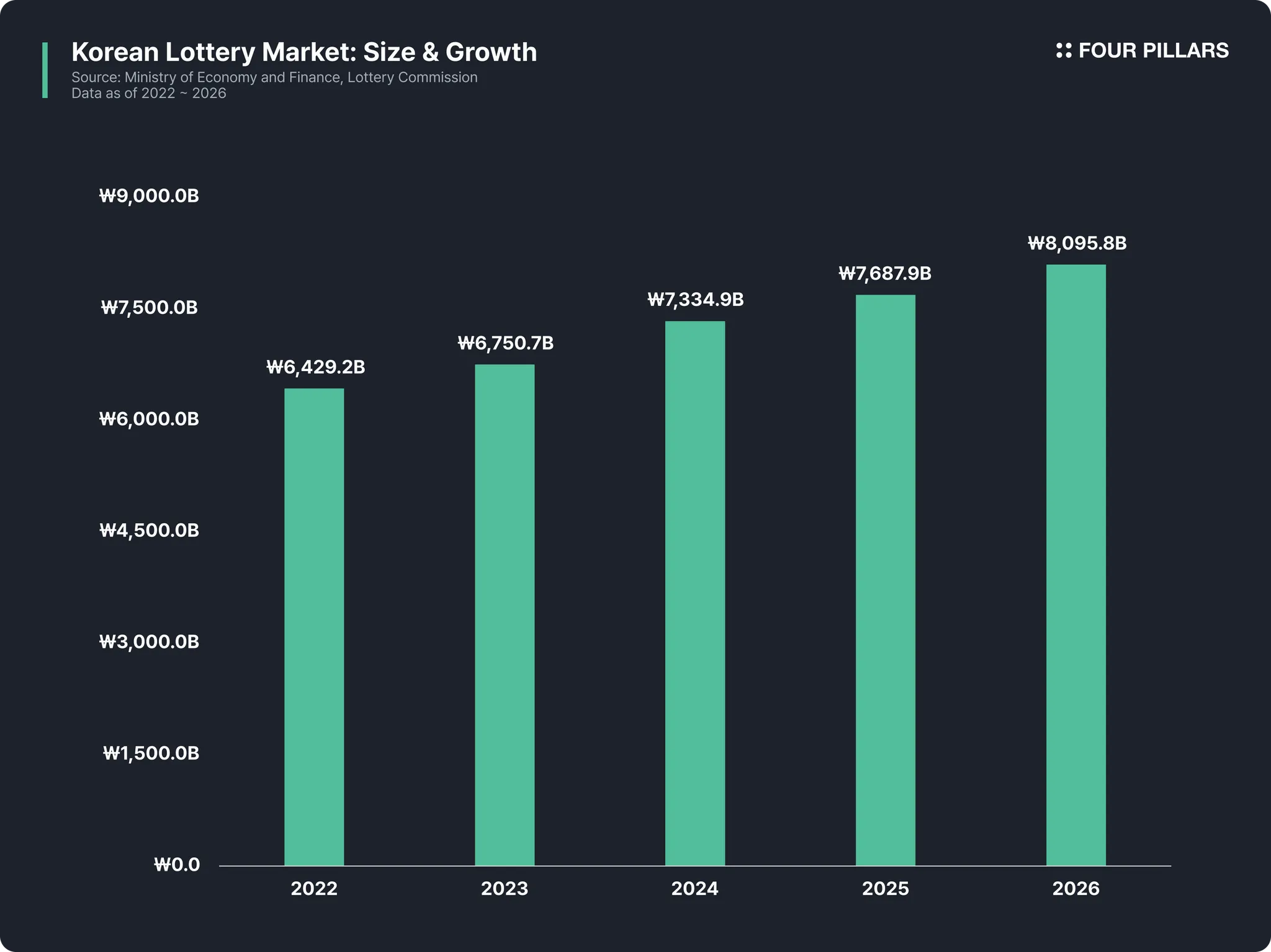

The Korean lottery market has been steadily growing. The Ministry of Economy and Finance projects that lottery sales will reach approximately KRW 8 trillion by 2026. If online platforms are introduced and products such as “pension-type lotteries” are diversified, this growth is likely to accelerate even further.

While the lottery has long served as both a source of hope and entertainment for ordinary citizens, it still faces several structural limitations:

Lack of Trust: Since sales, winnings, and fund operations are controlled by a centralized organization (Donghang Lottery), suspicions about fairness continue to emerge. Persistent rumors about lottery manipulation reflect this.

Inconvenience and Inefficiency: Legal restrictions that only allow cash purchases create user friction in an era where digital payments are the norm. The prize claim process is also cumbersome.

Rigid Structure: Product diversification is limited, and the system lacks flexibility to adapt to new demands or changing times.

The KRW stablecoin could be the key to directly addressing these limitations while adding new value to the lottery system. Even partial integration could significantly enhance the user experience, and a full digital transformation could solve core structural issues.

2.3.1 Maintaining the Existing Lottery System + Using KRW Stablecoin for Payment and Payout Only

Improved Purchase Convenience: By integrating stablecoins, users could easily and quickly purchase lottery tickets using their digital wallets, without the need for cumbersome installations or separate authentication steps. Currently, Korean law mandates cash-only purchases for lotteries. However, if safeguards against overspending are programmed into the lottery system, stablecoin payments could offer a more user-friendly experience.

Faster Prize Distribution: While Know Your Customer (KYC) verification would still be required for winners, the prize money could be sent directly to a personal blockchain wallet—eliminating the need to open a bank account or visit a bank branch. This would improve or eliminate inconvenient and unreasonable experiences, such as having to visit a bank headquarters or being pressured into purchasing financial products during prize claims.

2.3.2 Converting the Entire Lottery System to a Blockchain-Based Model

Full Transparency and Verifiability: All data related to the lottery—purchase history, prize amounts, draw algorithms, winner confirmations, and payout records—can be recorded on the blockchain in real time and made publicly accessible. Anyone could review this data directly or use verification tools to confirm the fairness of results, structurally eliminating doubts about integrity.

Operational Efficiency and Cost Reduction: Smart contracts can automate everything from ticket sales to prize distribution, drastically reducing legacy costs such as logistics, printing, and labor. These savings could be redirected into larger prize pools or public funds.

Programmable Scalability: New lottery models—such as charity lotteries that automatically donate a portion of winnings or micro-jackpots offering small hourly rewards—can be freely designed through programmable logic. This enables the creation of innovative products that offer both entertainment and social value.

Abroad, lotteries using stablecoins such as USDT and USDC are already in operation. For example, crypto.games’s Tether Lottery runs a system where users “buy tickets for 3 USDT each, and winners are instantly paid out in USDT.”

Additionally, platforms like Lottoland, DuckDice, and Lucky Block use stablecoins such as USDT and USDC for both ticket purchases and prize payouts. These platforms employ RNG (Random Number Generation) and Provably Fair technologies to institutionally guarantee fairness.

These examples demonstrate that stablecoin-based lotteries are no longer experimental concepts, but validated models with real-world demand and technical feasibility. They offer valuable insights into how a Korean-style KRW stablecoin could be implemented—both from a technological standpoint and in terms of enhancing the user experience.

Integrating stablecoins into the lottery system is more than just a technological experiment—it carries the potential for a wide range of positive economic and social effects.

Enhanced Transparency in Lottery Fund Management: A blockchain-based lottery can make not only ticket sales and prize payouts transparent, but also reveal how public funds are actually spent. While it is commonly stated that lottery revenue is used for public projects, the real flow of funds remains unclear to the public. By moving fund disbursement on-chain, it would become a practical tool to strengthen citizens’ ability to monitor public spending.

Re-engagement of Youth and Digital-Native Generations:

Korea's current lottery buyer demographic skews toward middle-aged and older adults, with those aged 60 and above accounting for 27.4% of total buyers—the highest proportion. In contrast, stablecoins and blockchain technology are more familiar to younger, digitally savvy generations. Digitally transforming the lottery system could offer a fresh entry point for youth who have traditionally shown little interest in lotteries.

Global Expansion Potential:

If a KRW stablecoin-powered lottery model gains institutional traction, it could be expanded globally—particularly in connection with K-content and the tourism industry. For example, lottery products targeted at international visitors to Korea could become a strategic export model combining Korea’s digital capabilities with its cultural content. This would open up new opportunities to strengthen soft power while also generating economic returns.

Naturally, several real-world obstacles must be overcome for this transformation to become reality. The most significant hurdle is legal and regulatory. The lottery business in South Korea is a tightly controlled, government-licensed industry governed by laws such as the Act on the Regulation of Conducting Speculative Acts and the Game Industry Promotion Act. As a result, it is highly unlikely that a private stablecoin issuer could operate a lottery business independently.

To address this, strategic approaches may include:

Forming technical partnerships with the government or the current lottery operator,

Or structuring offerings as prize-based promotions rather than formal lotteries, with thorough legal review to navigate regulatory constraints.

In addition, it will be essential to overcome the general public’s entry barriers to using cryptocurrency wallets. This requires intuitive UX/UI design and the implementation of robust security systems to protect user assets.

“Born too late to explore the Earth, born too early to explore the galaxy.”

This quote captures precisely where modern humanity stands amid the rapid advancement of science and civilization. But where do we stand in the evolution of money? Currency has progressed from bartering systems to the gold standard, to paper money, and then to partially digital forms. Now, we are on the cusp of the fully digital era of money—living at the very turning point of this transformation.

One of the key drivers of this financial revolution is the stablecoin, and in South Korea, the introduction of a KRW stablecoin is actively being pursued. However, issuance alone is not enough. Without clear, practical use cases, a stablecoin’s long-term viability remains uncertain. Just because something is technically possible doesn’t mean the public will adopt it. People ultimately trust and adopt currency when they see where and how it is used in real life.

Source: marketin

This is where integration with the lottery system can serve as a meaningful experiment. Beyond being just a new business model, it can become a tangible example of how a KRW stablecoin, as a programmable asset, enters daily life. In this sense, it marks the beginning of a truly digital monetary era. Such integration could also convert vague anxieties about new technology into real trust, becoming a strong catalyst for mass adoption of digital assets.

Now is the time to move beyond debating whether to introduce a stablecoin—and instead begin exploring practical applications and their ripple effects in everyday life. The lottery system offers a promising first use case to examine how the KRW stablecoin can create real, tangible value in society.

While stablecoins have the potential to resolve many of the transparency and efficiency issues currently plaguing Korea’s lottery system—as discussed above—the introduction of any new technology inevitably comes with trade-offs. If stablecoins were to be integrated into the lottery industry today, there are several key concerns that must be carefully considered.

One of the most pressing concerns is the potential for encouraging excessive gambling behavior. According to Article 5, Paragraph 4 of Korea’s “Lottery and Lottery Fund Act,” lottery sellers are explicitly prohibited from accepting credit card payments for ticket purchases. This restriction is in place to prevent impulsive or excessive gambling. Unlike cash, card usage often reduces the psychological perception of spending, which could lead to higher risk behavior.

If stablecoins are introduced, they may function in a psychologically similar way to credit cards—minimizing the sense of financial loss at the point of purchase. As a result, without proper safeguards and legal revisions, stablecoin-based transactions could unintentionally exacerbate gambling issues, necessitating new regulations and system-level countermeasures to manage risk.

Another major challenge lies in education and accessibility, especially given the current demographic makeup of lottery buyers. Korea’s lottery consumer base is predominantly middle-aged and older, many of whom are not familiar with blockchain or even mobile fintech apps. If the entire lottery system were to shift to a blockchain-based infrastructure, significant educational efforts would be required to ensure users can comfortably adopt and use stablecoins in retail environments.

Additionally, public perception may not shift easily. Even if blockchain-based draws are provably fair, users may trust traditional offline methods more, simply because they are familiar. Thus, educating the public not just on how to use stablecoins, but on why the blockchain system is actually more transparent and fair, will be critical. However, because lottery products target the general retail population, achieving this level of education and trust will likely be a long and difficult journey.

Dive into 'Narratives' that will be important in the next year