RWAs are at the most opportune moment in the history of onchain finance. While the regulatory environment is becoming clearer and infrastructure is advancing, RWAs still remain largely in the “tokenization” phase, with very few services or asset types available for actual market participants to use.

Avantis segments RWA market participants to identify distinct demand profiles, proposing three tailored growth strategies: ① LP vaults targeting risk‑averse users seeking stable yield, ② an RWA perpetual trading engine for risk‑tolerant users looking to take leveraged bets on volatile RWA assets, ③ an onchain U.S. equities futures market for users with limited access to global assets.

Avantis operates stable‑farming‑enabled LP vaults that pay trading‑fee‑based yield to liquidity providers. The vaults currently offer around 15% APY, significantly higher than U.S. Treasuries, and feature a tranche structure that allows users to select a vault aligned with their risk profile.

The Avantis RWA perpetual trading engine supports leveraged trading and adopts synthetic RWAs to create a liquidity environment optimized for these markets. RWA perpetual markets tend to respond with relatively predictable directional moves to macroeconomic events, allowing traders to build systematic strategies around scheduled volatility, making them a differentiated alternative market.

Today’s traditional financial infrastructure imposes structural barriers such as leverage restrictions, limited asset availability, high fees, and slow settlement/liquidity. Avantis addresses these by leveraging Base Network’s onchain rails to offer a new entry point into the high‑demand U.S. equities and equity index futures markets.

Source: SEC - American Leadership in the Digital Finance Revolution

“Many of the Commission’s existing rules and regulations do not make sense in the twenty‑first century, especially for on‑chain markets. The Commission must revamp its rulebook so that regulatory barriers do not block the entry and competition of both new participants and incumbents, thereby protecting the interests of Main Street.”

”Additionally, many firms seek to tokenize their common stock, bonds, partnership interests, and other securities, or tokenize the securities of third parties. Much of this innovation is taking place offshore today due to regulatory constraints in the United States. I have heard from our regulatory policy staff that firms—from well‑known financial institutions on Wall Street to unicorn technology companies in Silicon Valley—are knocking on the Commission’s door to pursue tokenization. I have directed the Commission staff to work with firms seeking to issue and distribute tokenized securities, and, where appropriate, to provide regulatory relief so that Americans are not left behind in this trend.”

— Paul S. Atkins, Chairman, U.S. Securities and Exchange Commission

RWAs are now at the most opportune moment in the history of onchain finance. Recently, the U.S. Securities and Exchange Commission (SEC) announced in its Project Crypto statement, explicitly announced plans to actively cooperate with companies seeking to distribute tokenized securities in the U.S. and, where appropriate, to provide regulatory relief. This is a remarkable departure from the SEC’s prior stance, which saw it bring enforcement actions against numerous crypto companies for unregistered securities offerings. It signals that the SEC recognizes both the potential and the current state of onchain RWAs and suggests a positive outlook for clearer regulatory frameworks and possible relaxation of restrictions going forward.

On the infrastructure side, onchain RWAs are rapidly advancing. Tokenization is spreading across a growing range of real‑world assets, and issuance, distribution, and settlement infrastructures (such as Securitize and Theo) have matured to the point of attracting institutional adoption. Price oracles (Chainlink, Pyth, Redstone, etc) are delivering real‑time pricing for RWAs, and cross‑chain interoperability solutions (LayerZero OFT) have reached production‑ready maturity. Taken together, the international regulatory environment and industry trajectory indicate that RWAs are already in a phase of steep growth within crypto, with momentum likely to accelerate.

Yet, in my view, the RWA market finds itself in a paradoxical position, possibly for the first time in crypto history. Despite having unprecedented regulatory clarity and pre‑announced flexibility, the market’s response is lagging behind. This is the opposite of previous cycles, such as with ICOs or stablecoins, where crypto markets and DeFi grew rapidly outside the bounds of traditional finance, prompting regulators to respond reactively and attempt to fit them into existing frameworks.

In reality, RWAs remain unfamiliar to most market participants. More specifically, there are very few ways for the retail investors most active in crypto markets to take direct exposure to RWAs. This is because the current discussion around RWAs remains stuck in the “tokenization” phase, and leading tokenization infrastructure providers like Securitize, Ondo, and Superstate still limit their scope largely to U.S. Treasuries (T-Bills). As a result, although RWAs have emerged as one of the most talked‑about and potentially in‑demand sectors this cycle, the actual services and asset types that market participants can actively trade remain extremely limited.

Against this backdrop, Avantis stands out as one of the few players in the RWA market presenting a clear user segmentation strategy. Avantis is a perpetual futures DEX built on Base, and in its early days it drew attention as the first DEX to support trading of assets such as the Turkish lira, commodities, and forex. Since then, it has recorded a cumulative trading volume of $15B and an average daily volume of $100M, establishing itself as the largest perpetual futures DEX in the Base ecosystem.

What stands out in Avantis’ early approach is its departure from the conventional tokenized asset model centered on T-Bills. Instead, it has supported onchain futures trading for highly volatile, real‑world‑linked assets such as gold, silver, and major forex markets. This illustrates Avantis’ market approach to RWAs: moving beyond the tokenization stage to offer an environment where assets can be traded immediately, thereby filling the gap left by the absence of practical RWA‑based trading services in the market.

So, what comes next for Avantis after this strong start? Now that RWAs are becoming a genuinely accessible market, the next step is to segment its users, clearly identify demand segments, and design products tailored to each user group:

Low‑risk profile users who prefer stable, passive yield generation

High‑risk profile users who seek leveraged exposure to volatile RWA assets

Users whose access to global assets is limited by local market entry barriers

Avantis has developed three growth strategies aligned with these user segments. The question now is whether Avantis can position RWAs as a practical asset class, capture each user segment effectively, and close the gaps that remain in the market. We explore this potential in the sections below.

2.1.1 How the LP Vault Works

The first strategy targets low‑risk users seeking stable, passive yield. To serve this segment, Avantis operates LP Vaults that enable stablecoin farming and generate yield from trading fees accrued through liquidity provision. At its peak, the APY exceeded 100%, and it currently remains around 15%, offering a competitive return compared to most stablecoin farming vaults, which typically yield under 10%.

Source: Avantis

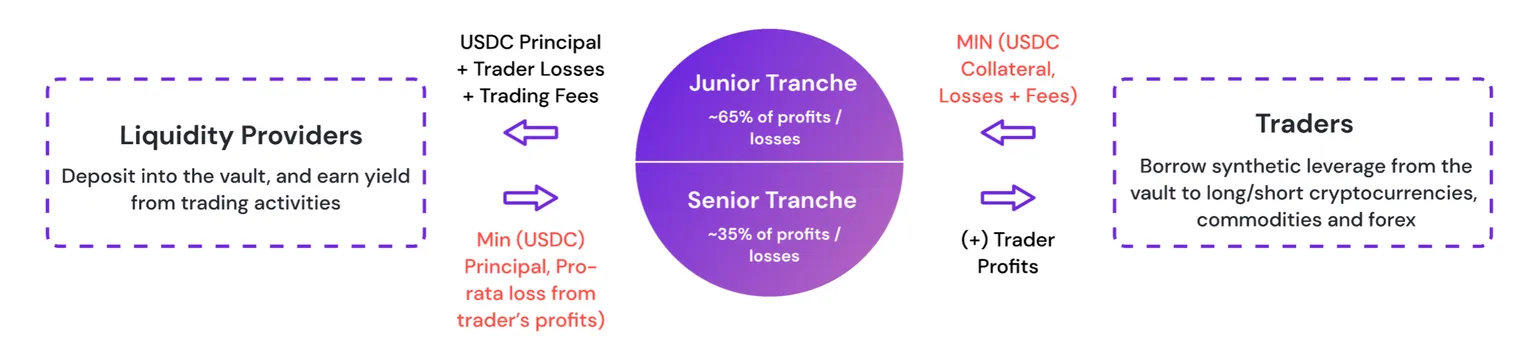

It should be noted, however, that Avantis’ LP Vaults are not risk‑free yield farming. Their mechanism is reminiscent of the GLP Vaults used in GMX. Avantis’ onchain RWAs are implemented as oracle‑priced synthetic assets backed by vault capital. As such, LP Vaults act as the direct counterparty to all trades on the platform: when traders profit, payouts come from the vault; when traders incur losses, those losses accrue to the vault. In return, liquidity providers collect trading fees.

In a vAMM-based perpetual futures DEX, when positions become heavily concentrated in one direction (long or short), the nature of the system causes delta risk from price movements to be concentrated on liquidity providers (LPs), potentially resulting in losses. This is because, if long positions pile up, LPs are forced to take on an equally large short position (and vice versa).

To address this, Avantis continuously monitors the degree of imbalance in open interest, known as Open Interest Skew (OIS), and provides incentives for taking positions on the non-skewed side when the long-to-short ratio becomes lopsided. In addition, Avantis works with multiple professional market makers, including Keyrock, to hedge and reduce open interest imbalances, thereby lowering LPs’ delta risk and maintaining stable market liquidity.

Furthermore, Avantis’ LP Vaults incorporate both time‑based and risk‑based parameters for flexibility. This allows LPs to choose their preferred risk exposure and lock‑up period based on their market outlook:

Senior Tranche (Low‑Risk): Receives approximately 35% of total collected fees while covering roughly 35% of realized losses.

Junior Tranche (High‑Risk): Receives approximately 65% of fees but also absorbs 65% of losses.

Lock‑Up Terms: LP positions can be locked for preset durations, with additional rewards proportional to the chosen lock‑up period.

2.1.2 Differentiating from Treasury Yields

Source: StableWatch

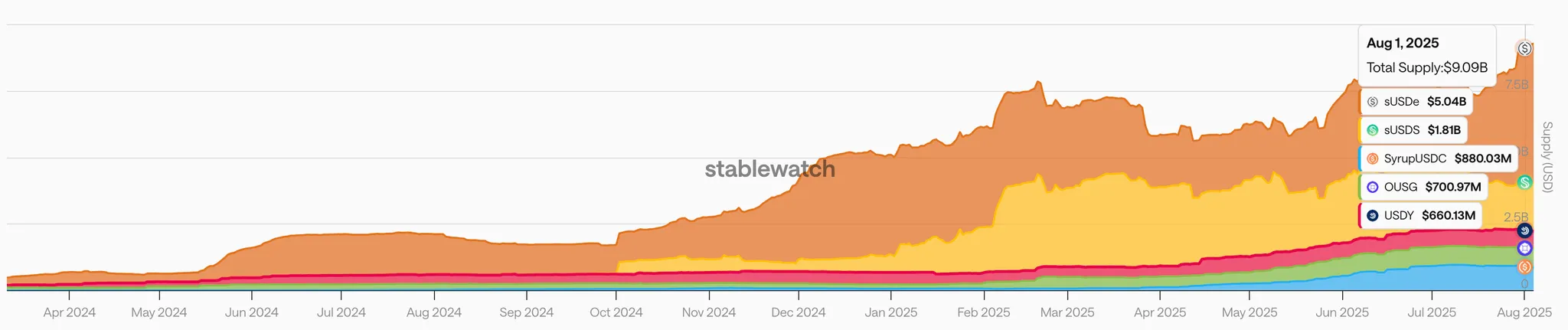

As noted earlier, more than half of the current RWA market is concentrated in T-Bills, account for over $6.8B of the roughly $13B non‑stablecoin RWA market cap. These assets provide low‑risk yields of around 4–5% with virtually no default risk, serving as a reliable source of fixed income. A prominent example is yield‑bearing stablecoins backed by tokenized T-Bills, which have proven their market viability; their combined market cap reached around $13B in Q3 2025, up nearly 4× from the end of 2023.

However, there are concerns about the market’s heavy reliance on T-Bills. Yields are closely tied to the Federal Reserve’s interest rate policy, which is inherently cyclical. With the Fed likely entering an easing cycle, and major institutions such as Goldman Sachs and Bank of America projecting three to four rate cuts in 2025, it is entirely possible on T-Bills yields to fall from current levels near 5% to below 3%. In such a scenario, demand for onchain RWAs fully backed by T-Bills could decline.

Avantis’ LP Vaults offer an alternative form of exposure to RWA‑based yield. While they differ from fully Treasury‑backed products in terms of yield generation and risk profile, backtests show that vault loss and profit ratios tend to remain near delta‑neutral, with traders’ wins and losses largely offsetting each other. This implies LPs can expect relatively stable, fee‑based returns.

Source: Avantis Analytics

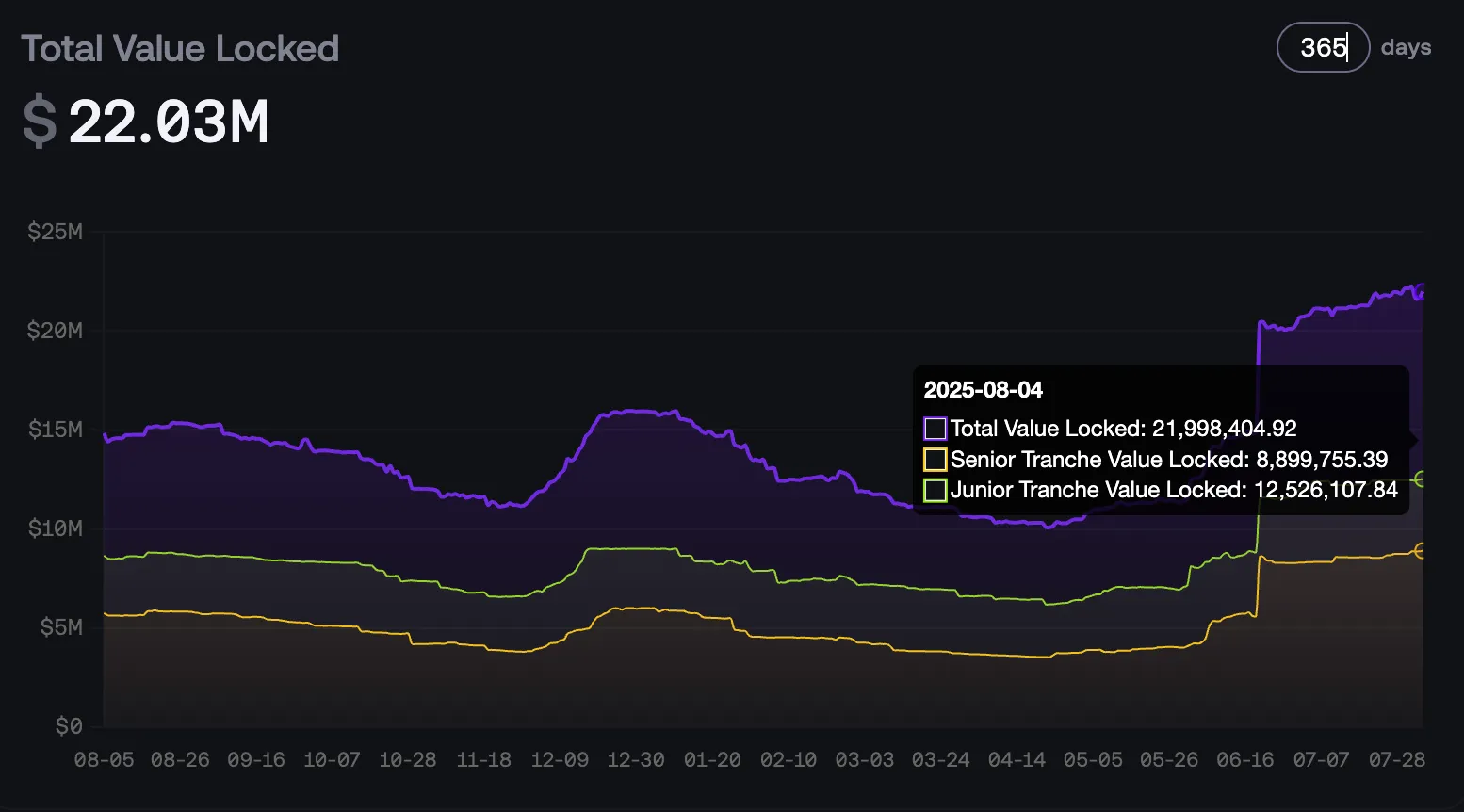

Currently, around $22M in USDC is deposited in LP Vaults, generating APYs of roughly 15%, far exceeding returns from Treasury‑backed RWA products. This positions Avantis’ LP Vaults as a viable alternative to T-Bill‑dependent RWA structures, offering both yield potential and resilience against interest rate shifts.

2.2.1 Why Avantis Chose Synthetic RWAs

Source: Avantis

In a crypto market accustomed to high‑volatility trading, passive yield alone is not enough to position RWAs as a practical asset class. One of the main reasons existing RWAs have seen limited active use is that most remain structured as passive, T-Bills‑backed products. These are unattractive to traders who prefer high‑volatility environments and leverage. Avantis addresses this gap by bringing physically linked perpetual futures markets onchain, creating new sources of demand.

The core reason Avantis chose an oracle‑based synthetic product model for its perpetuals engine is to solve the liquidity shortfall in RWAs and enable seamless futures trading. While there have been repeated attempts to offer tokenized equities or commodities, actual market liquidity has been so thin that traders face severe slippage or find normal execution impossible. The issue stems from the structural difficulty of maintaining stable bid‑ask spreads for RWAs in a traditional orderbook‑based perpetual market.

Difficulty Securing Large Circulating Supply: Since RWAs are backed by real‑world assets, supplying sufficient inventory for market making requires pre‑purchasing and issuing a corresponding amount of physical assets. This creates significant capital burdens, making it hard for market makers to secure deep liquidity from the outset.

Lack of Hedging Instruments: Market makers have limited means to hedge the price risk of holding spot RWA positions via futures. Without effective hedging tools, their risk exposure increases significantly, reducing incentives to participate in market making.

Avantis solves these issues through oracle‑priced synthetic RWAs. Once an oracle price is available, a wide range of RWA perpetual markets can be launched without needing actual spot inventory. This approach allows Avantis to currently offer major forex markets such as USD/JPY and GBP/USD, as well as commodity futures markets tracking gold, silver, and oil. Furthermore, by the end of this year, Avantis plans to add more than 25 new off‑chain assets, including on‑chain stocks, and will also expand the list of assets covered by its unique ZFP (Zero‑Fee Perpetuals) feature, under which traders pay transaction fees only when closing a position at a profit.

2.2.2 The Potential of the RWA Futures Market

Source: X (@0xSehaj)

There are two main reasons Avantis is focusing on the RWA futures market:

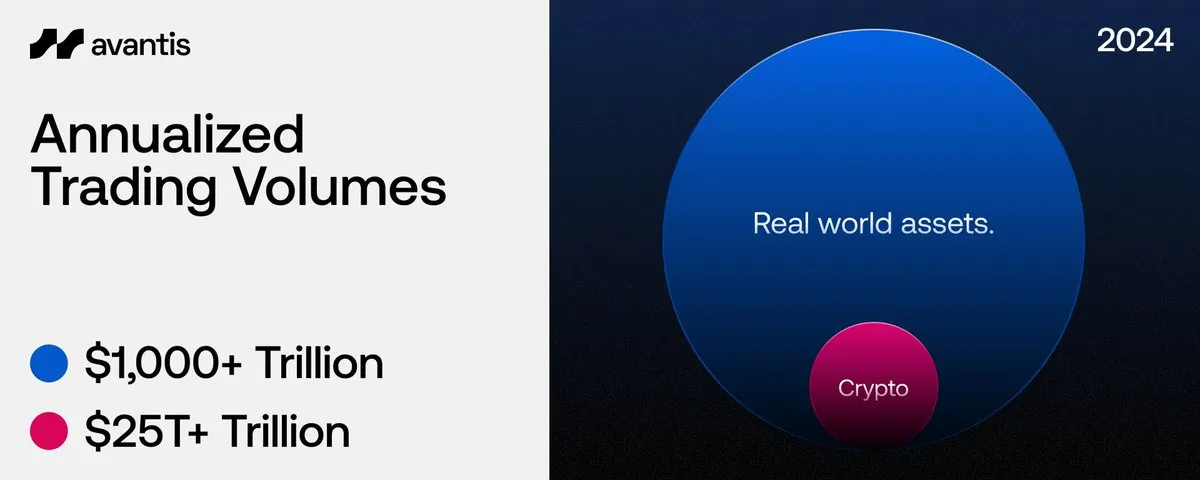

First, the global RWA futures market is vastly larger than the crypto futures market, offering enormous growth potential if migrated onchain.

According to Avantis, the annual trading volume of the crypto perpetuals market in 2024 is roughly $25T. In comparison, the global RWA futures market is about $1 quadrillion, more than 40 times larger. For context, CME Group’s monthly futures and options volumes, spanning asset classes such as equity indices, commodities, and FX, have averaged over 6B contracts in 2024, representing hundreds of trillions of dollars in notional value. Meanwhile, even Hyperliquid, the largest onchain perpetuals venue, has processed around $330B in the past 30 days, underscoring the vast gap between onchain trading activity and traditional capital markets.

Currently, however, there are very limited ways to access RWA futures onchain. Traders must leave the onchain rails and open brokerage accounts to trade on traditional venues such as CME or CBOE. By offering synthetic RWA futures natively onchain, Avantis can capture even a fraction of this enormous global market, which would be enough to meaningfully scale its growth.

Second, RWA futures offer a clear value proposition to existing onchain traders as an alternative trading asset, serving as a catalyst for new platform inflows.

Perpetual trading of crypto‑native assets is often driven by idiosyncratic narratives or short‑term events, making directional and timing predictions more challenging. In the altcoin space, price swings of over 10% in a single day are common, reflecting markets that are highly sensitive to sentiment and order flow rather than fundamentals.

RWAs, by contrast, move in response to macroeconomic events that are publicly scheduled and tied to the real economy, such as inflation data releases, central bank rate decisions, employment reports, and elections. Moreover, the price reactions to these events tend to follow more logical directional patterns. This makes the RWA futures market an environment where traders can systematically incorporate economic calendars, harness scheduled volatility, and apply predictive models and technical analysis with greater consistency.

While Avantis’ earlier growth strategies targeted trading demand based on varying risk appetites, its final growth strategy focuses on users whose market access is constrained by geographic or regulatory barriers. Given that Avantis has long pursued the vision of becoming a “Universal Leverage Layer for Global Assets,” providing a new entry point into global asset markets is a natural extension of that vision.

To achieve this, Avantis aims to build an RWA futures market that lowers the high entry barriers of traditional offchain venues. Among its priorities is enabling futures trading in U.S. equities with strong global demand (such as Coinbase, Nvidia, and Tesla) and major equity indices like the Nasdaq.

2.3.1 Global Demand and Barriers for Asset Access

Demand for certain global assets is already well‑established across multiple indicators. Interest in U.S. equities is especially strong. Over the past five years, the NASDAQ‑100 and S&P 500 Technology Index have both delivered average annual returns of more than 20%. Few asset classes have matched the sustained upward trajectory of a U.S. big‑tech‑focused portfolio. Moreover, when domestic equity markets in various countries stagnate for extended periods, investor preference for high‑growth U.S. equities tends to strengthen.

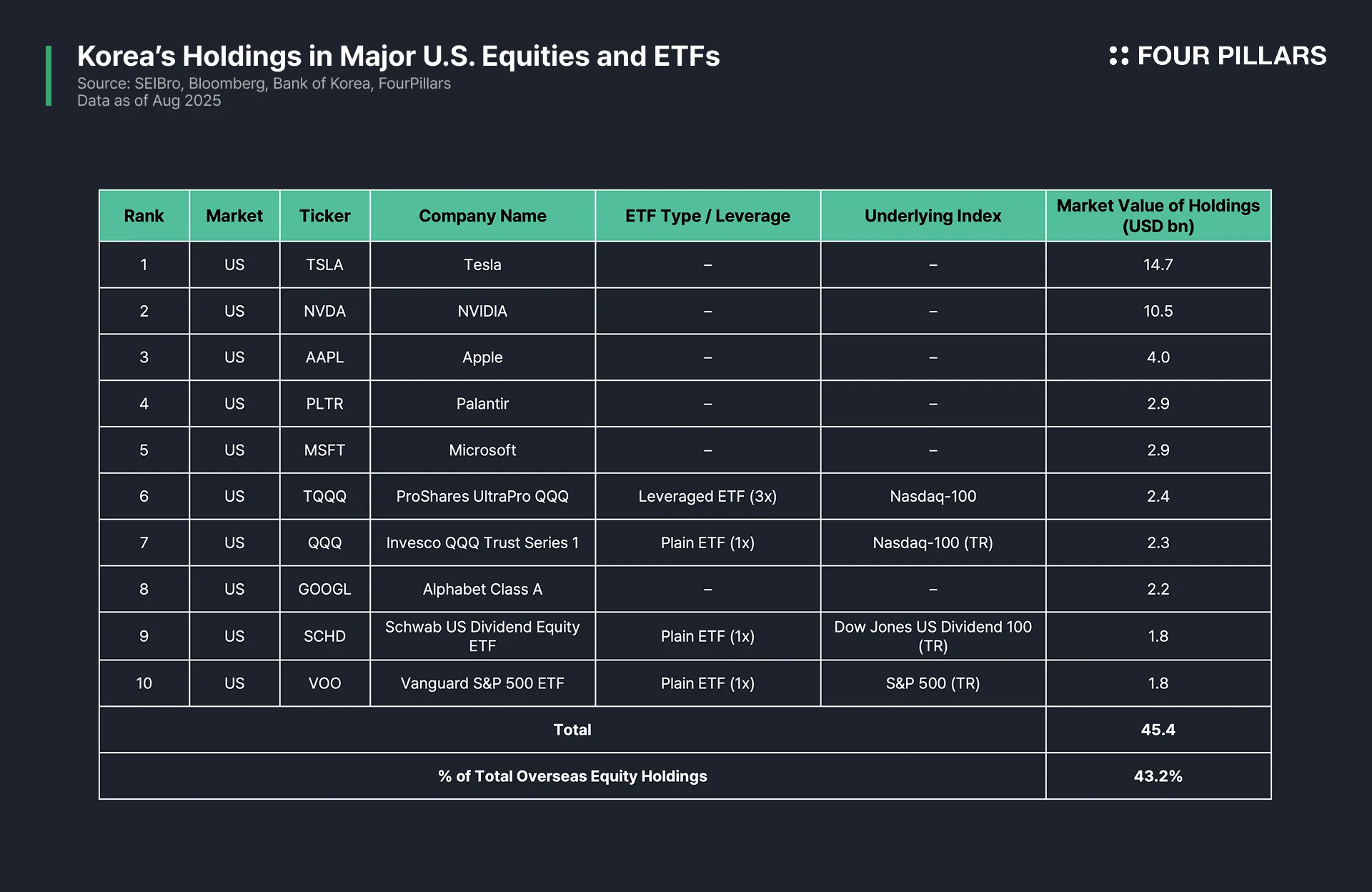

A clear example can be seen in South Korea, where Korean investors’ holdings of U.S. equities reached around $100B by the end of 2024, up more than 65% year‑over‑year. Top‑traded names include Nvidia (NVDA), Tesla (TSLA), Apple (AAPL), and Microsoft (MSFT), all large‑cap U.S. technology stocks.

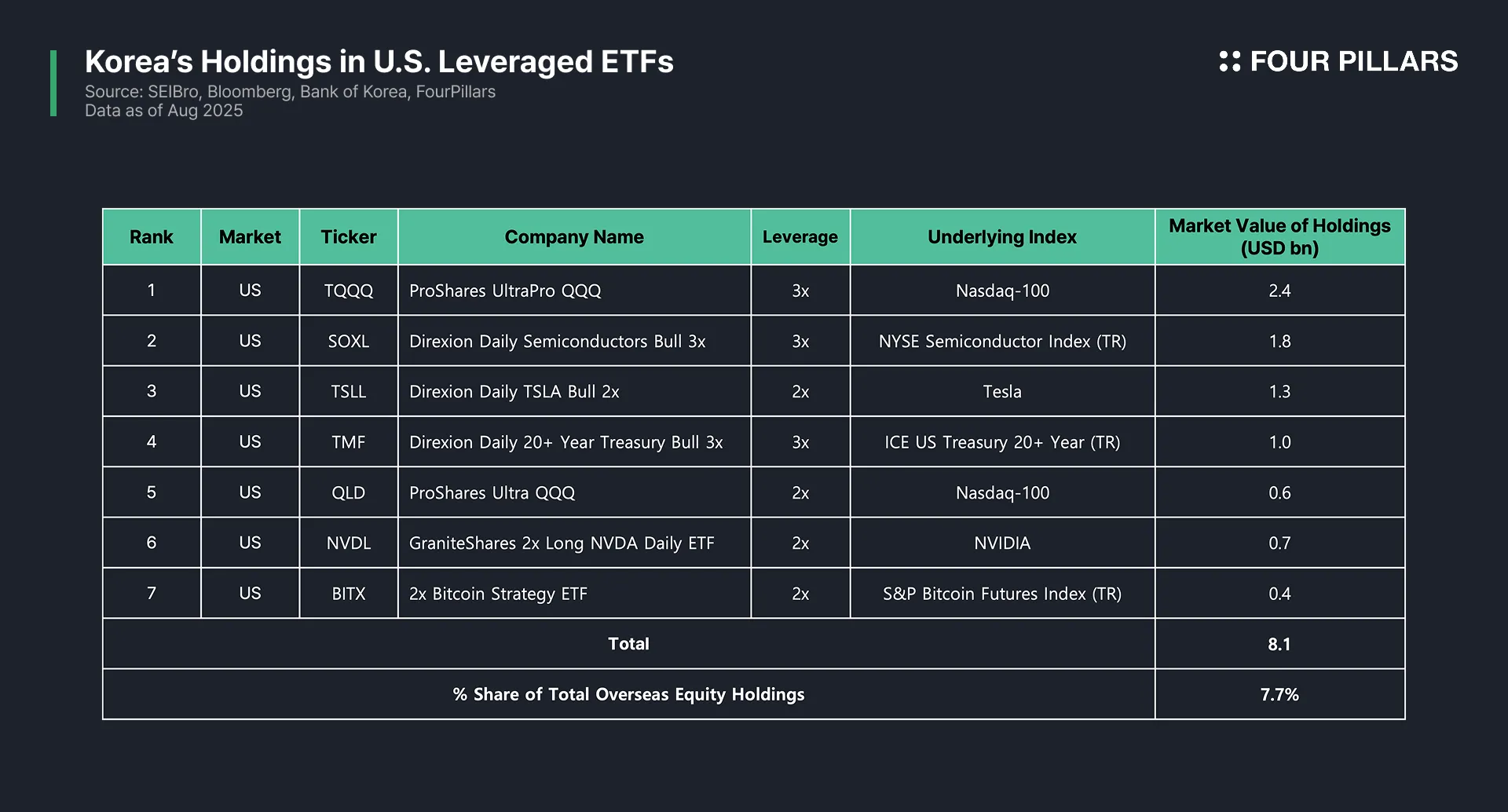

Data also shows high demand for U.S. equity and index‑based derivatives, with retail investors making up the majority of activity. Korean investors’ trading volume in overseas futures and options totaled $8.6T in 2024, with retail accounting for 84% of trades, far exceeding the participation of institutional players who typically use derivatives for hedging. Futures products with low margin requirements, such as the NASDAQ‑100 E‑mini and Micro E‑mini Nasdaq, rank among the most traded by volume due to their accessibility to individual traders.

Globally, demand for U.S. big‑tech equities and index products remains strong. As of late 2024, about 20% of U.S.-listed equities were held by foreign investors. In derivatives markets, around 30% of trading in CME’s S&P 500 and NASDAQ‑100 futures originates outside the U.S.. Country‑level data also reflects strong global preference for U.S. equities. In Japan, U.S. stocks make up over 60% of individual overseas equity trades. In Singapore and Hong Kong, U.S. equities and ETFs dominate international investment flows.

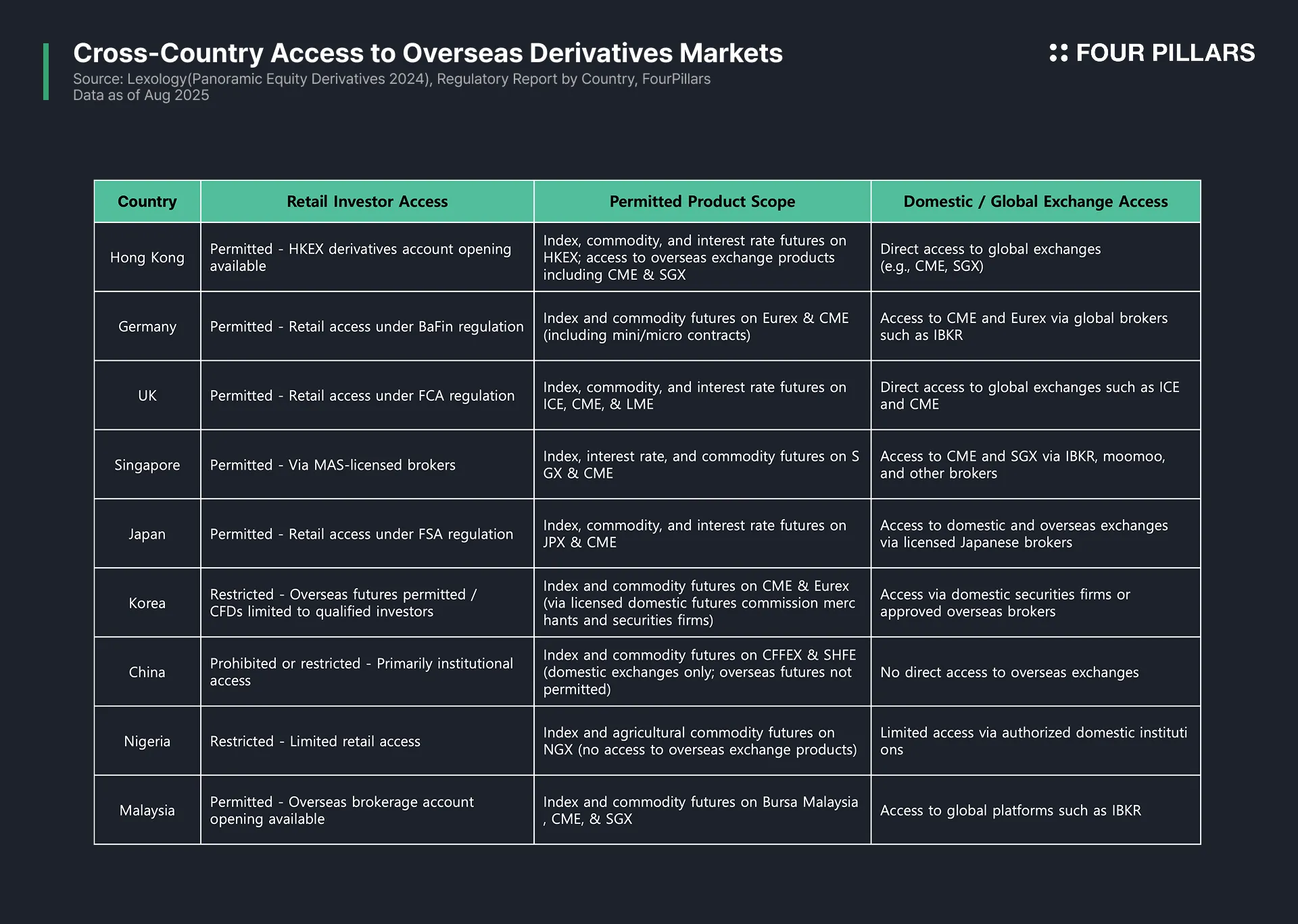

However, today’s traditional financial infrastructure imposes significant constraints: leverage limits, restrictions on tradable asset classes, high fees, slow settlement, and illiquid offboarding. For investors to gain direct access to U.S. equities and other assets, they must open overseas brokerage accounts, navigate complex FX conversion processes, and manage tax liabilities. In some jurisdictions, capital controls and underdeveloped financial systems limit access to volatile assets, while short‑selling and margin trading are either prohibited or heavily restricted for retail investors.

Against this backdrop, onchain RWAs offer a compelling alternative for global investors by lowering local access barriers. Onchain rails provide instant settlement and efficient trading infrastructure, while synthetic RWAs address liquidity and product‑variety bottlenecks in the RWA market. This is particularly relevant for users in markets where regulation or infrastructure limits access to global assets.

Avantis has identified this opportunity and plans to enable futures trading in U.S. equities over borderless onchain rails. This approach seeks to break down local market barriers, tap into already‑proven demand, and expand growth potential.

2.3.2 Strategic Fit Between Base and Avantis

For Avantis’ plan to eliminate local access barriers and maximize market reach, simply offering RWAs onchain is not enough. The platform must operate as a 24/7 global marketplace capable of accommodating varied regulatory and technical environments, supporting seamless fiat‑to‑crypto conversion, and processing high‑volume transactions without delay. Base serves as an optimal infrastructure to meet these requirements.

Regulatory Alignment: Base is a Layer 2 network closely integrated with Nasdaq‑listed Coinbase, inheriting the company’s extensive regulatory expertise as a leading exchange. Coinbase has operated under strict compliance in the U.S. and other major markets for years, maintaining a regulation‑friendly approach since its 2021 IPO. Coinbase’s onramp service to Base operates with the necessary licenses and regulatory clearances for fiat transactions. Base benefits directly from this framework, providing Avantis with a regulatory foundation that supports credibility and operational stability for onchain RWAs.

On/Off‑Ramp Infrastructure: Leveraging Coinbase’s fiat on/off‑ramp significantly streamlines user onboarding. For Avantis, whose strategy hinges on attracting new user segments by removing local market barriers, this is critical. Coinbase supports over 60 fiat currencies and complies with all relevant licensing and regulatory requirements in each jurisdiction. A recently launched P2P onramp feature enables users to purchase stablecoins in local currency and complete transactions within minutes. For Coinbase Wallet users, transferring assets to Base and accessing Avantis takes only a few clicks.

Technical Scalability: Base has made notable scalability gains with the introduction of Flashblocks. By reducing block times from around 2 seconds to 200 milliseconds, transaction processing speeds have increased by more than 10×. Pre‑confirmation capabilities now approach real‑time, ensuring low‑latency execution essential for high‑frequency and leveraged futures trading. This performance profile aligns closely with Avantis’ RWA futures and high‑leverage product requirements.

In short, Base offers the ideal combination of regulatory alignment, fiat on/off‑ramp accessibility, and technical scalability to support onchain RWA futures trading. Avantis’ choice of Base as the foundation for its three‑pronged growth strategy reflects a deliberate alignment between infrastructure capabilities and strategic objectives.

You would find no other capital market where Fartcoin, Bitcoin, and BlackRock’s tokenized T-Bills (BUIDL) coexist. That uniqueness is what defines crypto. It has evolved into a financial infrastructure optimized for extreme asset diversity and freedom.

As a result, user segments within the broader crypto market are becoming increasingly well‑defined based on asset size, risk profile, and trading style. The spectrum is broad, ranging from long‑term holders of large‑cap blue‑chip assets to degens making high‑risk bets on niche micro‑cap assets such as memecoins, to airdrop farmers, high‑frequency leveraged traders, and yield lovers who focus on stable farming or DeFi money‑legos.

This kind of segmentation is important because it provides a core framework for how projects design their strategies to serve these distinct user profiles. It also encourages the emergence of specialized playbooks and competitive services targeting each user segment, ultimately acting as a starting point for advancing the entire industry.

For RWAs in particular, several strategic questions emerge:

How can RWA‑based yield products offer a range of options that balance return and stability?

What trading environments are most effective for securing liquidity while delivering strong user experience?

Which categories of real‑world assets align best with specific user demands?

For the RWA market to meaningfully scale, it must clearly identify which types of users are entering the market and what motivates them. Once the conversation moves beyond tokenization itself and begins to address these questions, RWAs have a much greater chance of entering a high‑growth phase. As we have seen, Avantis is actively thinking about these questions and embedding them into its growth strategy:

Offer yield products that generate attractive returns relative to T-Bills through fee‑based income, while enabling differentiated exposure by risk appetite via a tranche structure.

Adopt synthetic RWAs as the most practical solution for securing liquidity in futures trading.

Build an onchain futures market for U.S. equities, a category with proven high demand but limited access, on borderless onchain rails.

The question now is whether this growth plan can evolve into a playbook or end‑game model that other players in the space will look to emulate. As RWAs open new market opportunities, Avantis’ next moves will be worth watching.

Avantis Docs – https://docs.avantisfi.com/

Dive into 'Narratives' that will be important in the next year