Uniswap Protocol has evolved from v1 to v4 since its inception from Vitalik Buterin's AMM (x*y=k) idea in 2016, achieving approximately $2.75T in cumulative trading volume to date.

Each Uniswap Protocol version introduced significant improvements: v2 introduced ERC-20/ERC-20 trading pairs and TWAP; v3 implemented concentrated liquidity for improved capital efficiency; v4 aims to transform Uniswap Protocol into a developer platform through Singleton architecture and Hooks that enable customization of liquidity pools.

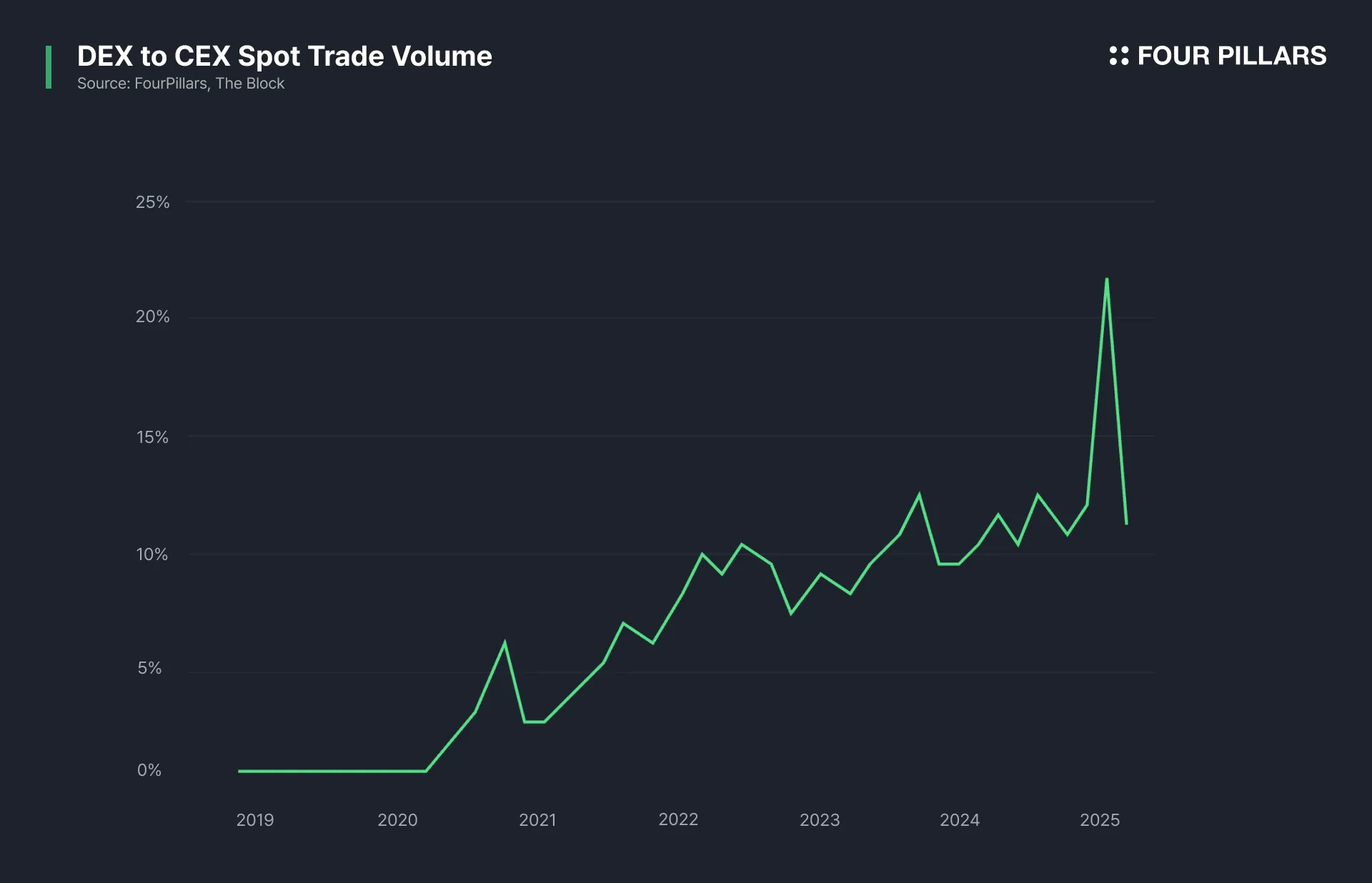

As DEX to CEX trading volume exceeds 20% for the first time, signaling the crypto market's shift toward onchain centricity, Uniswap Protocol recorded $710 billion in trading volume in 2024, showing 91% year-over-year growth, and playing an increasingly important role as the main gateway for new users entering the onchain market.

To this end, Uniswap Labs continues to develop infrastructure to enhance user experience, particularly addressing the fragmented liquidity problem across Layer 2s through cross-chain infrastructure: developing ERC-7643 cross-chain intents with Across Protocol and building Unichain, aiming to become the "Home for DeFi and cross-chain liquidity."

Currently, out of all new wallet transactions executed through the Uniswap interface, approximately 55% represent users performing their first-ever crypto swap. Additionally, around 25% of these users complete their first swap on Uniswap Interface within 24 hours of their first Ethereum transaction. Having refined its protocol over several years, Uniswap Protocol has become the primary gateway for many new users entering crypto to experience DeFi and on-chain trading.

Not only that, the usage ratio of DEX compared to CEX continues to increase, driven by various factors including improved blockchain performance, wallet infrastructure and abstraction solutions, along with increased demand for long-tail assets in recent market trends. In other words, the crypto market is now undergoing a fundamental transformation from CEX-centric to onchain trading.

Against this backdrop, this three-part ‘Uniswap Protocol series’ examines how Uniswap Protocol will play a crucial role in reshaping the crypto markets toward onchain centricity. The series begins by exploring the evolution of the AMM (Automated Market Maker) from Vitalik's initial concept through early Uniswap Protocol deployment. It then traces how Uniswap Protocol has adapted to industry changes throughout its development, and finally provides analysis for Uniswap v4 and Unichain. In this first part of the series, we examine the brief history of Uniswap Protocol.

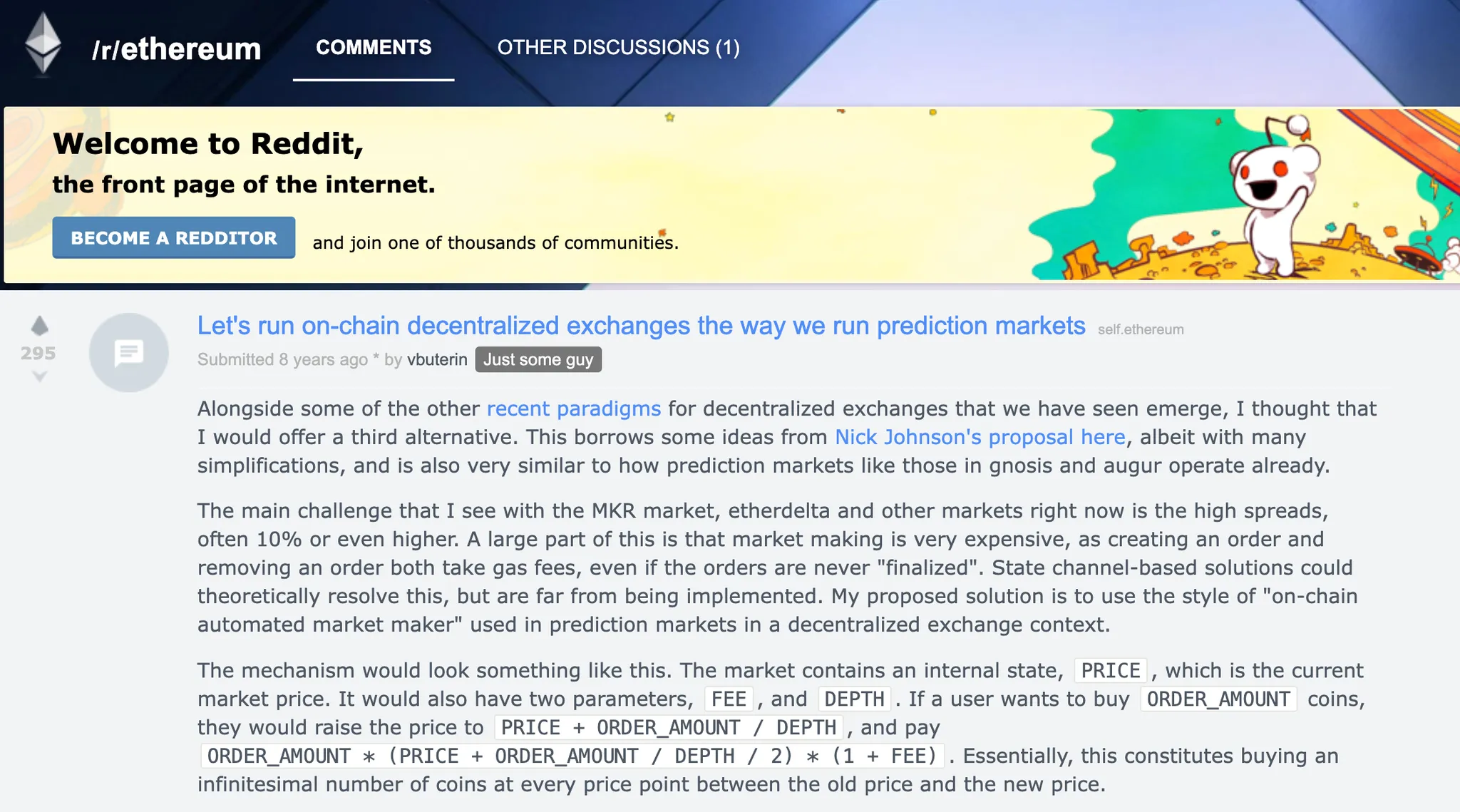

Source: /r/ethereum

The mechanism I propose is a smart contract holding tokens of type T1 and T2, maintaining the invariant that AB=k. Anyone can buy or sell by selecting a new point on the xy=k curve and providing the deficient A tokens in exchange for receiving B tokens.*

-Vitalik Buterin, Ethereum Founder

Today's Uniswap Protocol originated from an idea proposed by Vitalik Buterin on Reddit in 2016. In his proposal, Vitalik highlighted the excessive gas fees required for creating and executing orders on orderbook-based DEXs like Etherdelta. The DEXs existing at that time had adopted the traditional exchange's orderbook model, making onchain trading problematic on Ethereum mainnet due to slow transaction execution speeds and high fees.

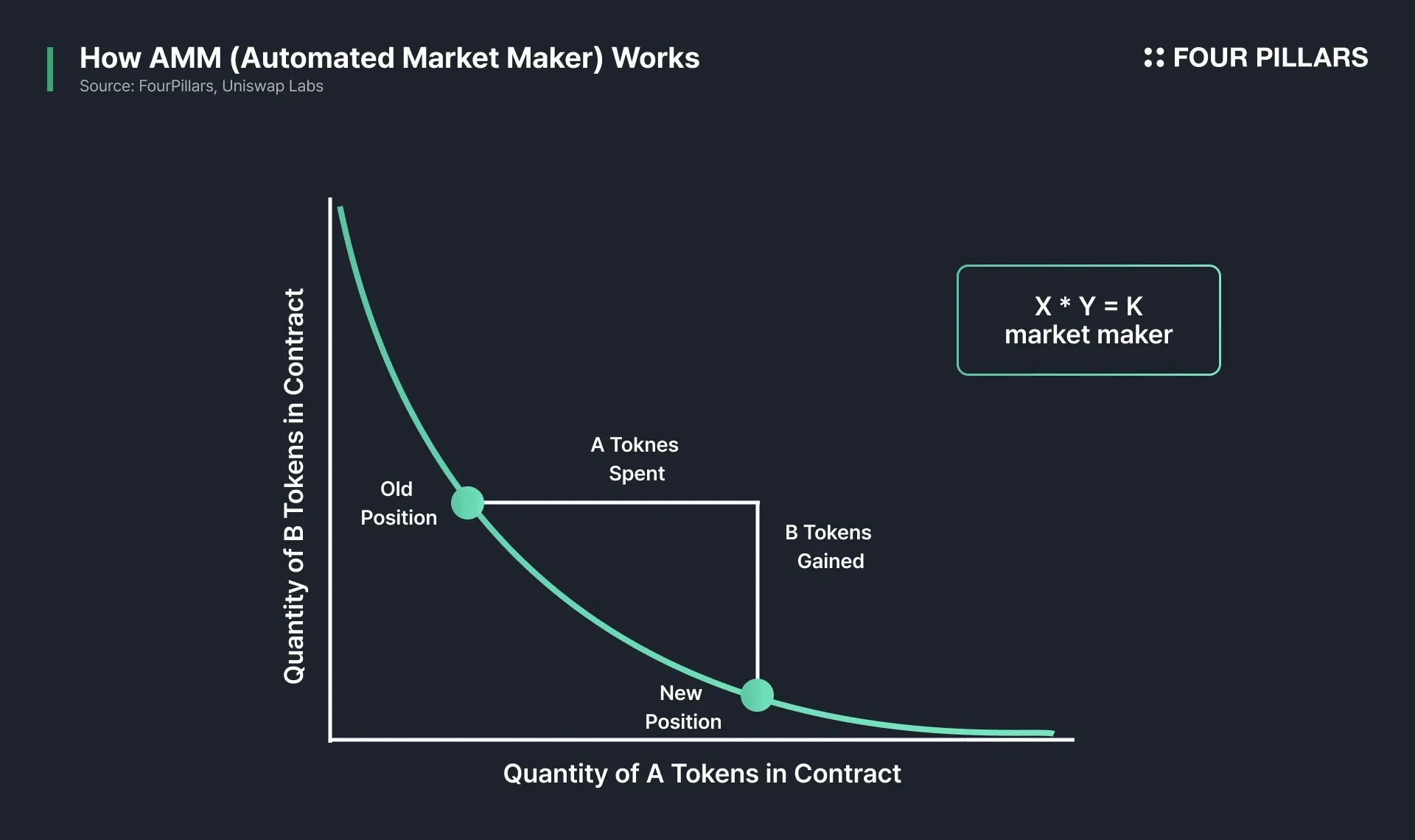

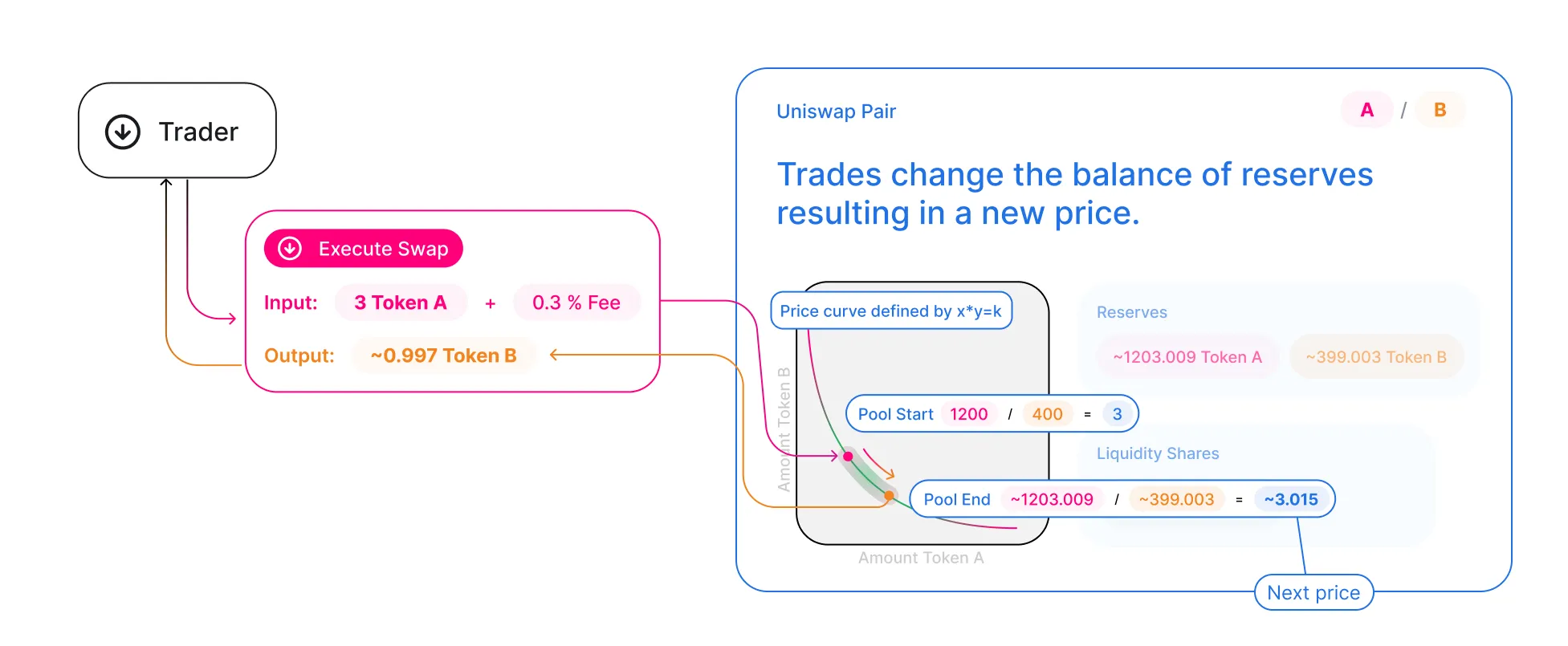

His proposed solution was the AMM based on the x*y=k formula, where the product of two tokens always maintains a constant value K. That is, it is a method that executes price discovery by proportionally decreasing the quantity of one token as the quantity of the other token increases in the liquidity pool.

Source: X(@haydenzadams)

While the AMM is now considered one of crypto's most important innovations, it was initially just a theoretical concept until Hayden Adams, CEO of Uniswap Labs, implemented it as a protocol. This led to the creation of Uniswap v1, marking the beginning of a notable founder story - creating Uniswap Protocol after being introduced to Ethereum by a friend following his dismissal from his first job.

Though basic compared to today's Uniswap Protocol, v1 delivered the fundamental functions of an AMM-based DEX similar to what we see today. Anyone could create AMM pools consisting of trading pairs, and liquidity providers could earn fees proportional to trading volume by depositing assets, thus gaining economic incentives to provide liquidity. Traders could also utilize onchain trading through swaps, exchanging one token for another.

Since the launch of v1, Uniswap Protocol has continuously evolved — with Uniswap v2 and v3, currently the most widely used versions, having processed approximately $2.75T in all-time trading volume.

Below, we'll briefly examine the features and improvements of each version to trace this development process. As v4 and Unichain will be covered in detail in the next series, we'll only provide a brief overview here.

1.2.1 Uniswap v1-v2

Source: Uniswap Protocol Docs

Uniswap v1 successfully completed the proof of concept for AMM and demonstrated that AMM could be a more suitable alternative for onchain trading compared to the orderbook model at that time. In particular, it could support smooth trading even in early markets with low trading volume.

However, since Uniswap v1 was at an initial stage of proving AMM to the market, despite presenting sufficient potential as a suitable alternative for onchain trading, it still had some limitations.

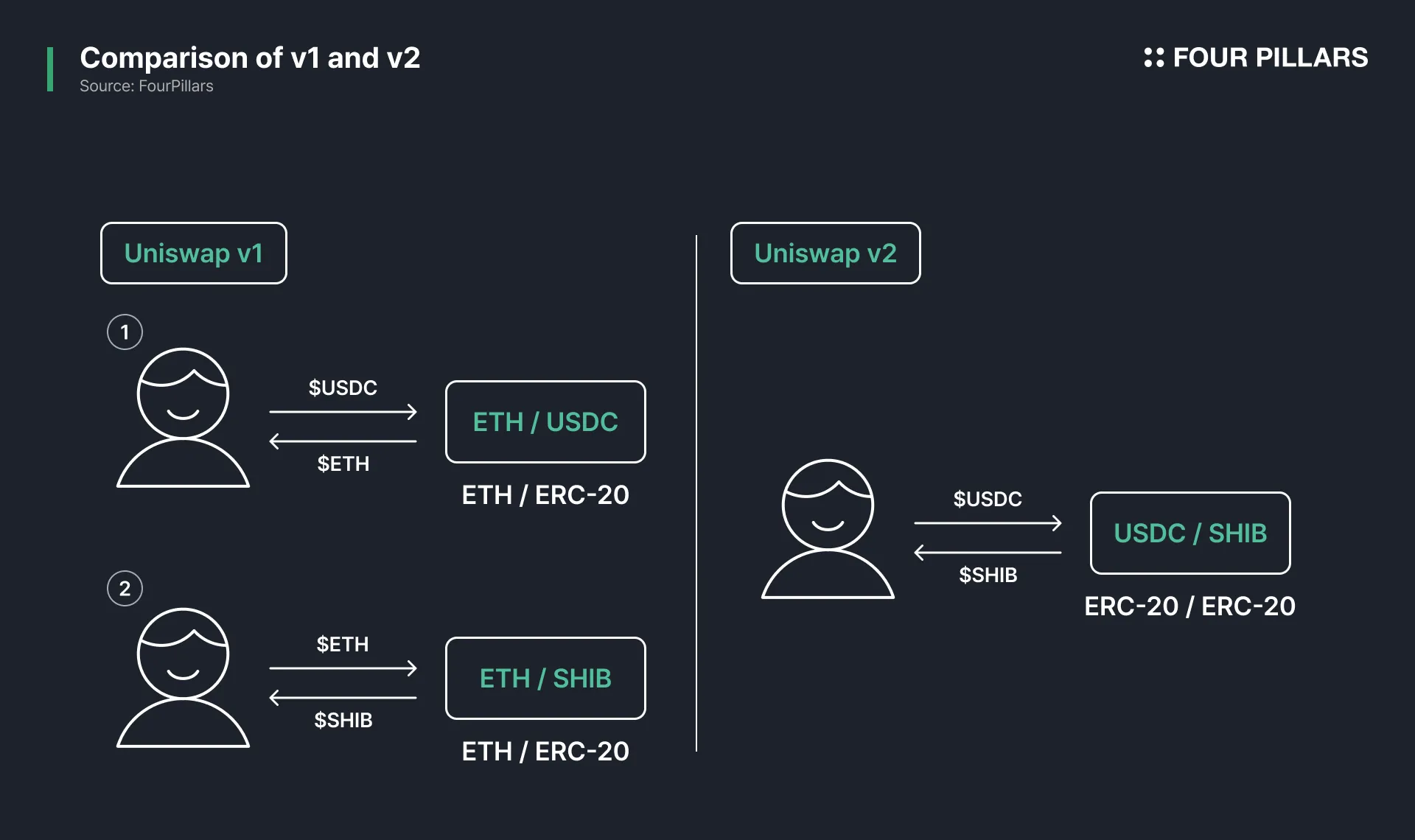

One issue was that the v1 protocol only supported liquidity pools consisting of $ETH/ERC-20, which meant that if a trader wanted to buy $SHIB with $USDC, they had to first exchange $USDC to $ETH, and then exchange $ETH to $SHIB, causing inconvenience. In response, Uniswap v2 added the ability to create ERC-20/ERC-20 liquidity pools, enabling the creation of liquidity pairs between any tokens, greatly enhancing trading convenience.

On the other hand, Uniswap v2 introduced a feature to derive the current price of assets based on Time-Weighted Average Price (TWAP). Through this feature, the current price of an asset is determined based on the average of price information recorded in each block. The current price is determined by taking the average based on how long the asset prices recorded across multiple blocks over a certain period have persisted. This time-weighted mechanism provides more stable price information because it is less affected by short-term price fluctuations. This allows Uniswap Protocol to address vulnerabilities to flash loan attacks and sandwich attacks that complete transaction manipulation and settlement within a single block.

With these improvements, Uniswap v2 has recorded nearly $750B in cumulative trading volume, and the v2 contract has been forked 675 times, becoming the most forked protocol across all DeFi protocols.

1.2.2 Uniswap v3

As mentioned, Uniswap Protocol's AMM operates as a Constant Product Market Maker (CPMM), maintaining a constant K value as the protocol of two tokens. Beyond enabling price formation without orderbooks, CPMM theoretically allows trading at all price points through equally distributed liquidity across the price curve. However, this creates capital inefficiency due to excessive idle liquidity, as most trading occurs near current market prices while capital remains allocated across the entire price range.

This "Lazy Liquidity" problem makes it difficult for liquidity pools to maintain sufficient liquidity for current price trading. Consequently, traders face high slippage due to insufficient liquidity, and increased price impact makes pools vulnerable to MEV attacks like sandwich attacks. MEV refers to the extractable value based on transaction ordering in the block creation process. As price impact increases, it becomes easier for attackers to profit through front-running and back-running around target transactions - buying at favorable prices before the target transaction and selling immediately after it executes.

For liquidity providers, lower capital efficiency means a lower ratio of actual trading volume to deposited assets. This reduces trading fees proportional to volume and liquidity providing incentives, potentially creating a negative cycle of diminishing pool liquidity.

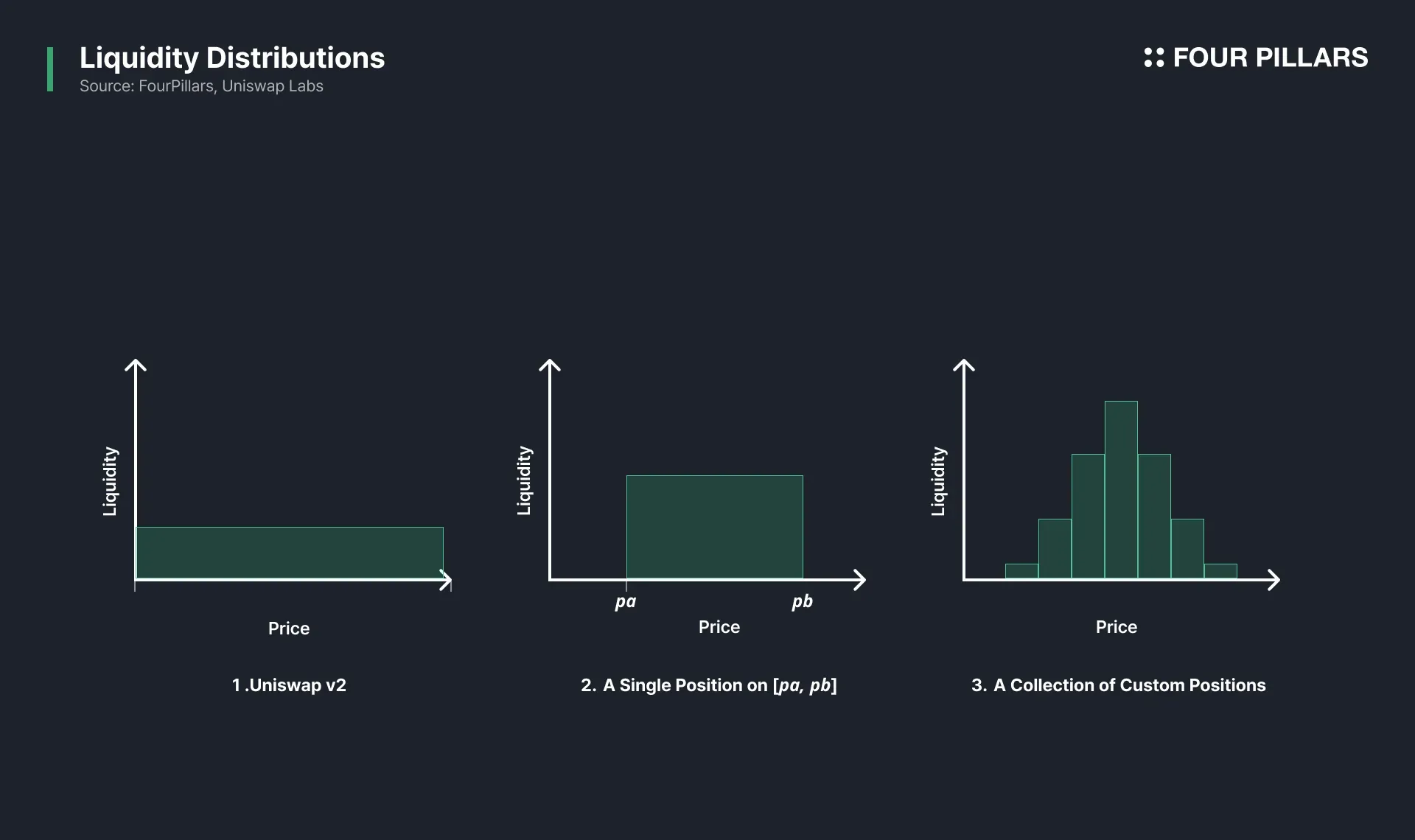

To address liquidity issues, Uniswap v3 introduced Concentrated Liquidity. This allows liquidity providers to deposit liquidity within custom price ranges, so LPs can focus liquidity near current prices where it’s actually utilized.

For example, an LPs can concentrate liquidity in the $1,800-$2,000 range for the ETH/USDC pair. This allows the LPs to earn more fees when the ETH price fluctuates within this specific range while achieving a higher liquidity effect with significantly less capital compared to the previous model where liquidity was spread across the entire price curve.

With this feature, v3 improved liquidity utilization inefficiencies, allowing liquidity providers to provide more efficient liquidity with the same amount and offering traders better pricing with minimized slippage. v3 now handles most Uniswap Protocol transactions, recording approximately $2T in cumulative trading volume and positioning itself as a central protocol in the onchain ecosystem.

1.2.3 Uniswap v4

Source: Uniswap Blog

v4 aims to transforms Uniswap Protocol into a developer platform. While v1 through v3 focused on improving trader convenience and capital efficiency, v4 represents an evolution toward becoming a developer platform through Hook-enabled pool customization.

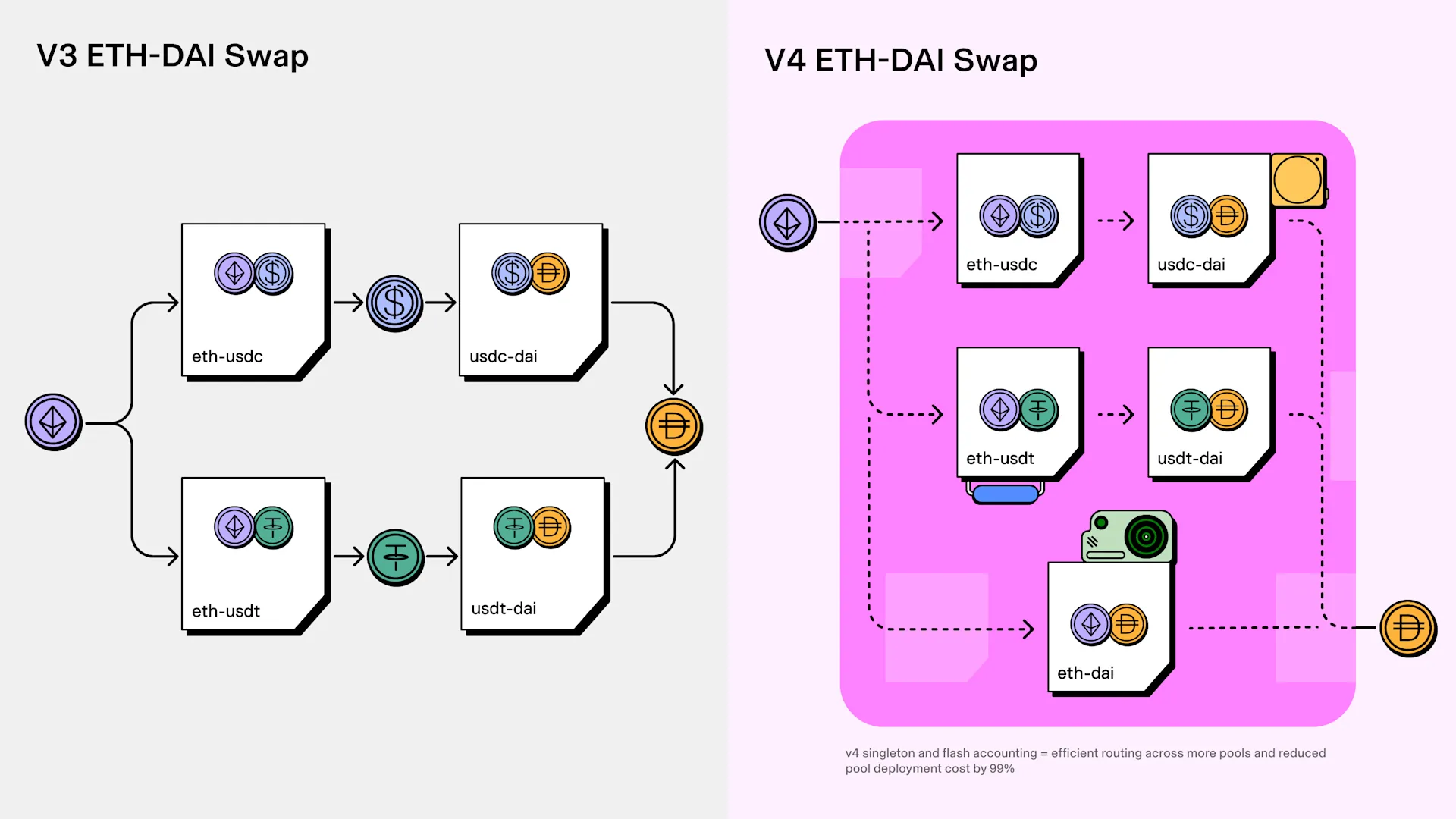

v4 notably introduces two major features: Singleton and Hooks. Singleton represents a new architecture where all liquidity pools are managed under a single contract, unlike previous versions where pools existed as separate contracts. This enhances the efficiency of the routing process to achieve lower transaction fees, and additionally reduces deployment costs from a development perspective by managing liquidity pools within a singleton instead of deploying each pool as an individual contract.

The second feature is Hooks. The Hooks are a programmable, modular feature in Uniswap v4 that allows developers to attach custom logic to liquidity pools. Specifically, it enables the execution of pre-configured specific logic when certain events occur in the liquidity pool, such as pool creation, swapping, adding, or removing liquidity. For example, it's possible to introduce various functions to existing liquidity pools, such as Lending Hooks that maximize liquidity provision rewards by connecting idle liquidity not used in transactions with lending protocols, or MEV Hooks that reduce losses caused by MEV.

A notable example is Flaunch, a token launchpad that utilizes the Progressive Bid Wall (PBW) hook to execute automatic token buybacks. Through this mechanism, whenever a token generates a 0.1 ETH trading fee, it creates a limit order worth 0.1 ETH just below the token's spot price, helping to reduce the impact of selling.

Additionally, Coinbase recently launched Verified Pools. Verified pools available on Base chain can only be accessed by users who have completed the verification credential. Through this, Coinbase is able to provide institutional-grade secure liquidity pools that meet KYC/AML standards.

As mentioned in the introduction, the anticipated change is a market transformation toward onchain centricity. According to The Block, for the first time, the ratio of DEX to CEX trading volume has exceeded 20%, indicating a rapid increase in DEX users.

Looking at Uniswap Protocol's annual trading volume, after recording $370B in 2023 compared to $530B in 2022, 2024 has already seen a volume of $710B, representing over 91% year-over-year growth. Even considering the macroeconomic conditions of each year, the gradually increasing DEX trading volume represents growing DEX adoption.

Despite the growth trend in onchain activities, DEX market share compared to CEX remains at around 20%, suggesting a significant gap still exists relative to CEXs. The main reasons for this phenomenon include the relatively poor user experience in the onchain environment and steep learning curve, resulting in a situation where only limited market participants continue to utilize onchain solutions.

Against this backdrop, the importance of DEXs as the first gateway users experience in the onchain environment is growing. Uniswap Labs aims to provide trading convenience and excellent user experience comparable to CEXs, lowering entry barriers for users unfamiliar with the onchain environment, and ultimately continuing efforts necessary to expand the onchain market to the next level.

Uniswap Labs continues to develop consumer-friendly user experiences at the infrastructure level. In particular, it consistently contributes to improving infrastructure for more efficient utilization of liquidity by participating in the development of cross-chain intents and Unichain. Despite Uniswap Protocol's evolution from v1 to v4 with the goal of implementing better onchain trading, if the liquidity that forms the foundation of trading is not efficiently utilized, an ideal trading environment cannot be provided to users.

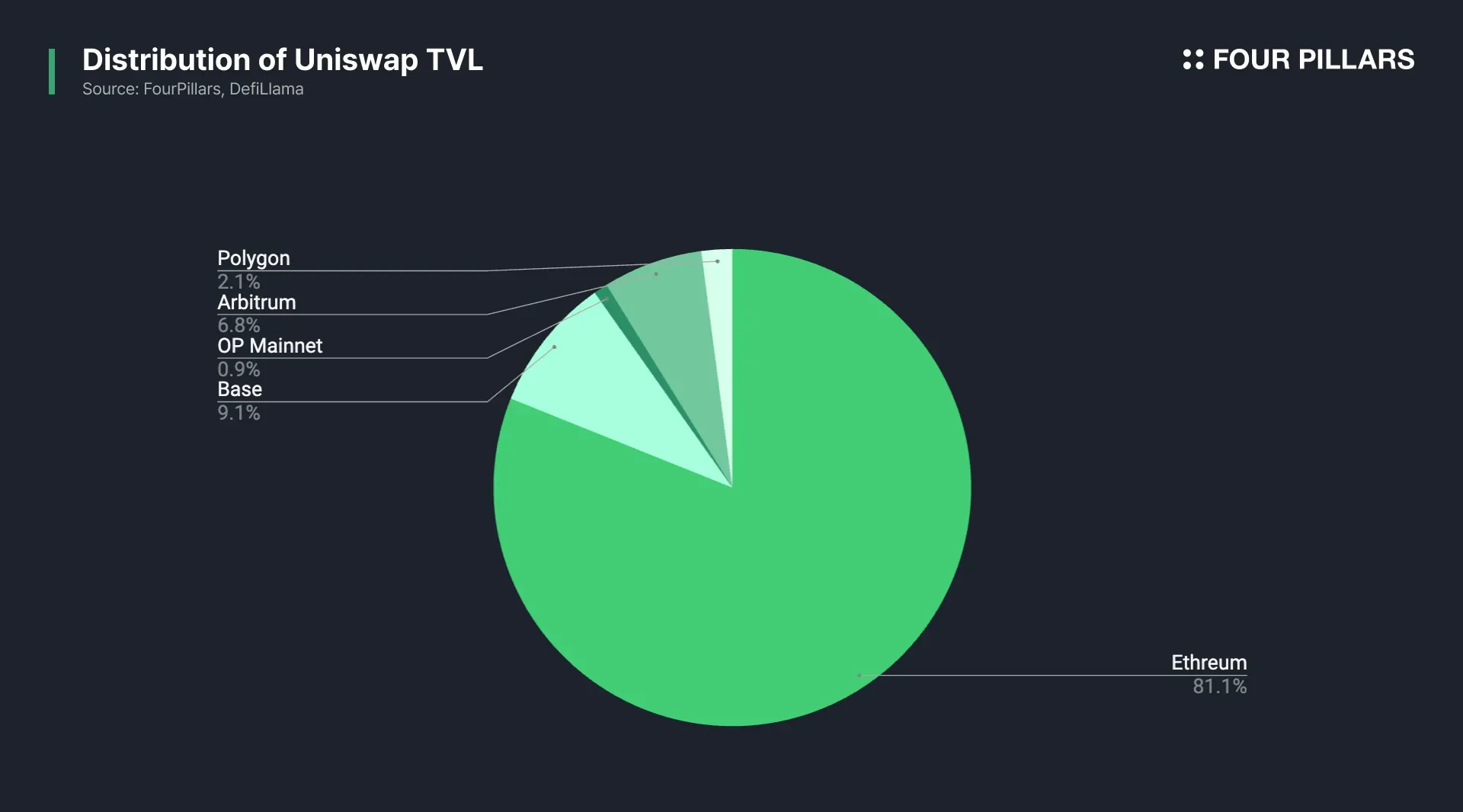

Ethereum has pursued a rollup-centric scaling roadmap since 2020 to secure scalability. As a result, there are now over 100 Layer 2 solutions based on Ethereum Layer 1. While Layer 2s have successfully contributed to improving Ethereum's scalability, they have also caused the side effect of dispersing the limited liquidity in the Ethereum ecosystem across various Layer 2s, ultimately forcing users to endure poor user experiences due to insufficient liquidity.

For example, examining the TVL of Uniswap Protocol running on most Layer 2s shows significant liquidity gaps between chains. While approximately $3.9B in liquidity is deposited on Ethereum mainnet, Base has only about $360M, Arbitrum has $310M, and OP mainnet has just $49M. This significantly degrades the user experience. Users must process multiple transactions to move assets dispersed across various Layer 2s, accumulating network fees and delays in the process. Additionally, since liquidity is not secured at a sufficiently deep level for efficient AMM operation, users must accept high slippage when trading large volumes or long-tail assets.

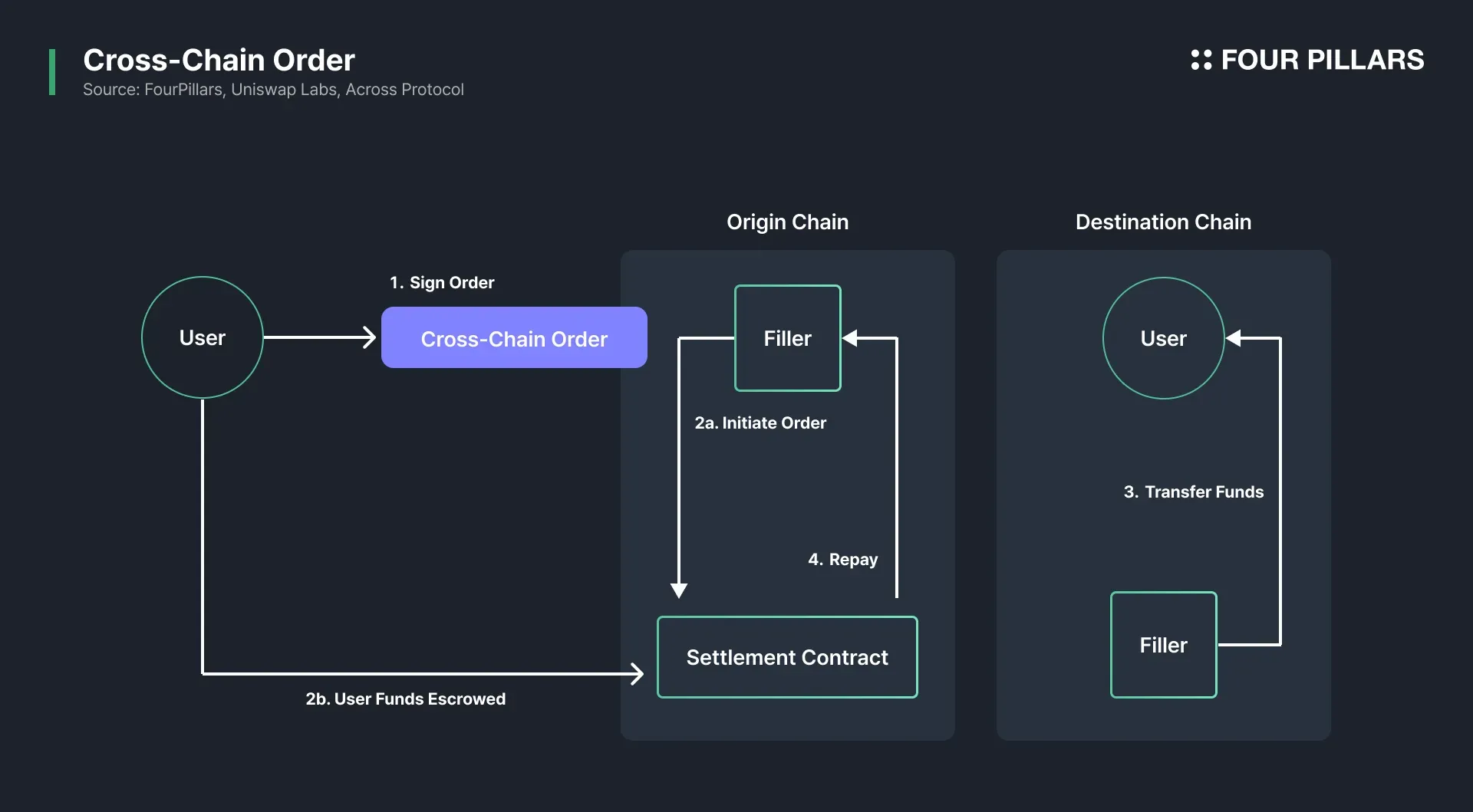

In response, Uniswap Labs is developing the ERC-7643 cross-chain intent with Across Protocol. Through this, when users submit an intent for cross-chain trading, fillers participating in the auction mechanism find the most efficient and affordable swap route. Thanks to the competitive structure where fillers must offer optimal prices by comparing various bridge options and DEX prices, users naturally receive favorable prices and low fees. This allows users to execute cost-efficient cross-chain trades without complex procedures involving direct intermediary bridges and multiple approvals. These cross-chain intents will be applied to Uniswap X in the future, greatly streamlining multi-chain swap functionality.

Additionally, Uniswap Labs has participated in the development of Unichain in collaboration with Flashbots. Unichain is a Layer 2 based on the OP Stack, built with the goal of being a "Home for DeFi and liquidity across chains." While Unichain includes various technology stacks for improving user experience such as rollup boost and flash blocks, UVN (Unichain Validation Network) plays a crucial role in minimizing friction in cross-chain swaps.

The problem that could occur in existing cross-chain swaps was that liquidity flow could be blocked if rollup transactions had to wait through a 7-day challenge period to achieve finality, or if a chain needed to be rolled back due to disputes. However, UVN secures economic finality for the rollup itself through its own validator set and economic security, making cross-chain transactions safer and more efficient. This positions Unichain to have a complementary relationship with cross-chain intents, continuously developing infrastructure-level improvements for efficient utilization of liquidity.

In summary, as the market shift from CEX to DEX centricity accelerates, Uniswap Protocol's role and importance in the crypto market are expected to grow. Uniswap Protocol has evolved from Vitalik's idea to become a core DEX processing trillions of dollars in cumulative trading volume, while continuing to develop infrastructure-level improvements for low fees and efficient onchain market construction. How cross-chain liquidity, considered the next stage of development, will improve Uniswap Protocol's user accessibility and ultimately impact the integration of the dispersed Ethereum ecosystem is the most noteworthy aspect of upcoming changes.

Dive into 'Narratives' that will be important in the next year