Recently, Trump strongly criticized US credit card companies for charging delinquent interest rates above 20%, arguing that these rates should be capped at 10%.

But this is the wrong approach.

High delinquent interest rates are not a US only issue. In the UK, delinquent rates are even higher than in the US. In South Korea and Japan, they typically fall in the 15 to 20% range.

Given that US Treasury yields sit around 4%, it is fair to ask why credit card delinquent rates are so high. The answer is simple. Interest rates reflect risk pricing.

First, credit card debt is unsecured. Unlike mortgages, there is no collateral, which makes recovery difficult.

Second, default risk is real. Borrowers who fall behind on credit card payments often have volatile income or are financially vulnerable. As a result, defaults are common. In the US, the average charge off rate is around 5 to 6%.

Third, marketing costs are significant. Credit card companies spend heavily on rewards programs, promotions, and advertising to acquire customers.

Fourth, the market structure is closed and concentrated. The credit card market is dominated by a small number of large players, which limits competition.

Because of this, delinquent interest rates should be shaped by market forces. If they are capped by law, unintended consequences are likely. For example, if delinquent rates are limited to 10%, credit card companies may simply stop issuing cards to financially vulnerable consumers altogether.

That said, it is also true that credit card companies earn very high interest income. In 2024, Discover reported $3.6B in Q4 credit card interest revenue, while losses from defaults totaled $1.2B.

On Chain Lending Can Fix This

In the end, fair interest rates should be set by market forces. Today, the biggest reason delinquent credit card rates stay high is the oligopolistic structure of the credit card industry.

To fix that, more people and more capital need to be able to participate in lending markets. On chain lending can make that possible.

A clear example is Morpho. On Morpho, anyone can supply capital and create lending markets. Curators then manage these markets based on different risk and return profiles, allocating capital more efficiently within the lending ecosystem.

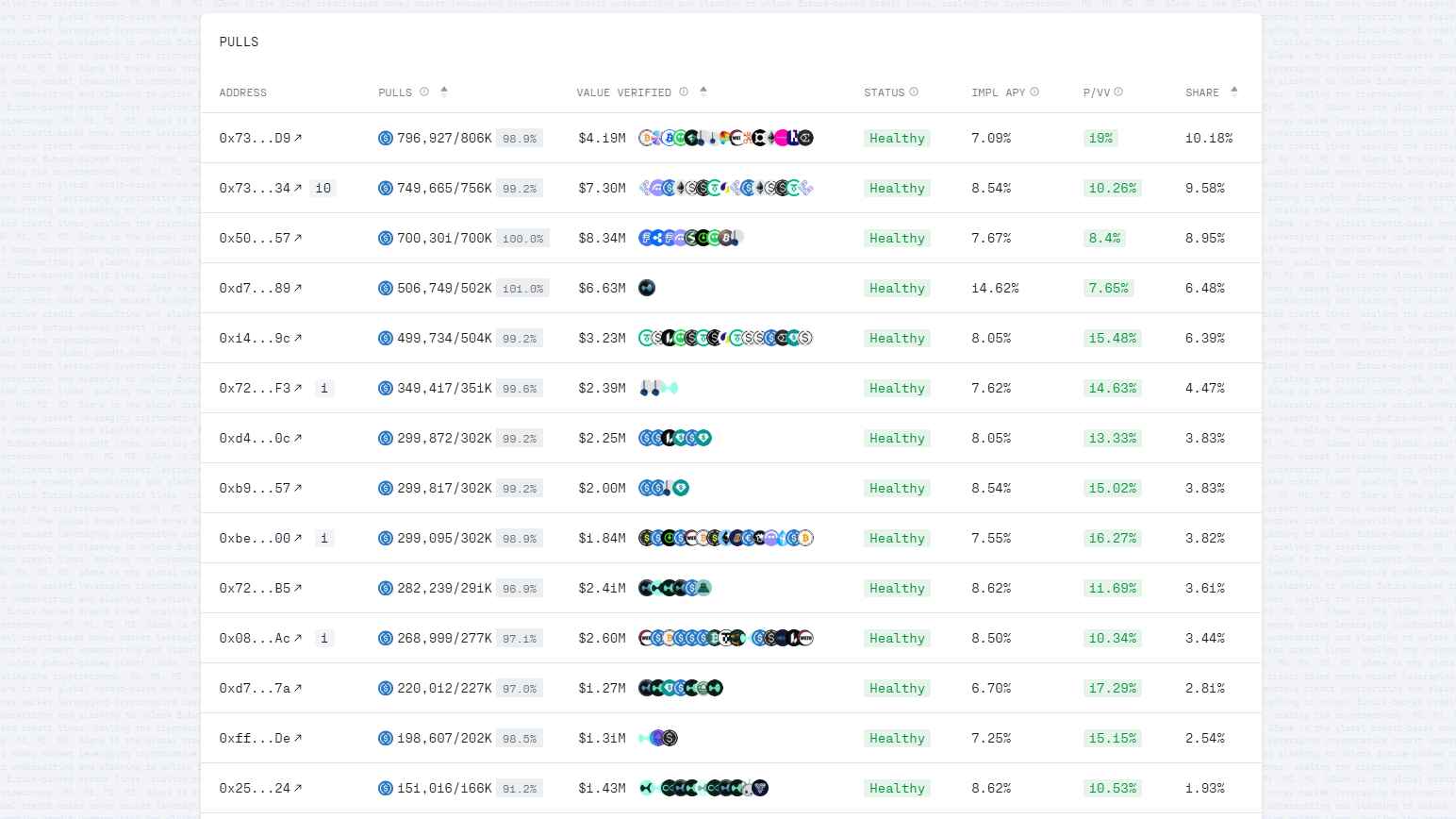

Source: 3Jane

A protocol closer to unsecured credit card style lending is 3Jane. On 3Jane, anyone can supply capital, and borrowers receive credit limits based on their credit score and the size of their on chain assets. Within those limits, they can borrow freely. In practice, interest rates are set much lower than 20%, typically around 8%.

Final thoughts

High interest rates are not the real problem. Interest rates simply reflect market forces. The real issue is a closed credit market that most people and capital cannot participate in.

On chain lending still has many hurdles to overcome, especially in unsecured credit. But as more data accumulates and better mechanisms are built, it has real potential to reshape and improve the traditional credit lending market.