Source: X(@KobeissiLetter)

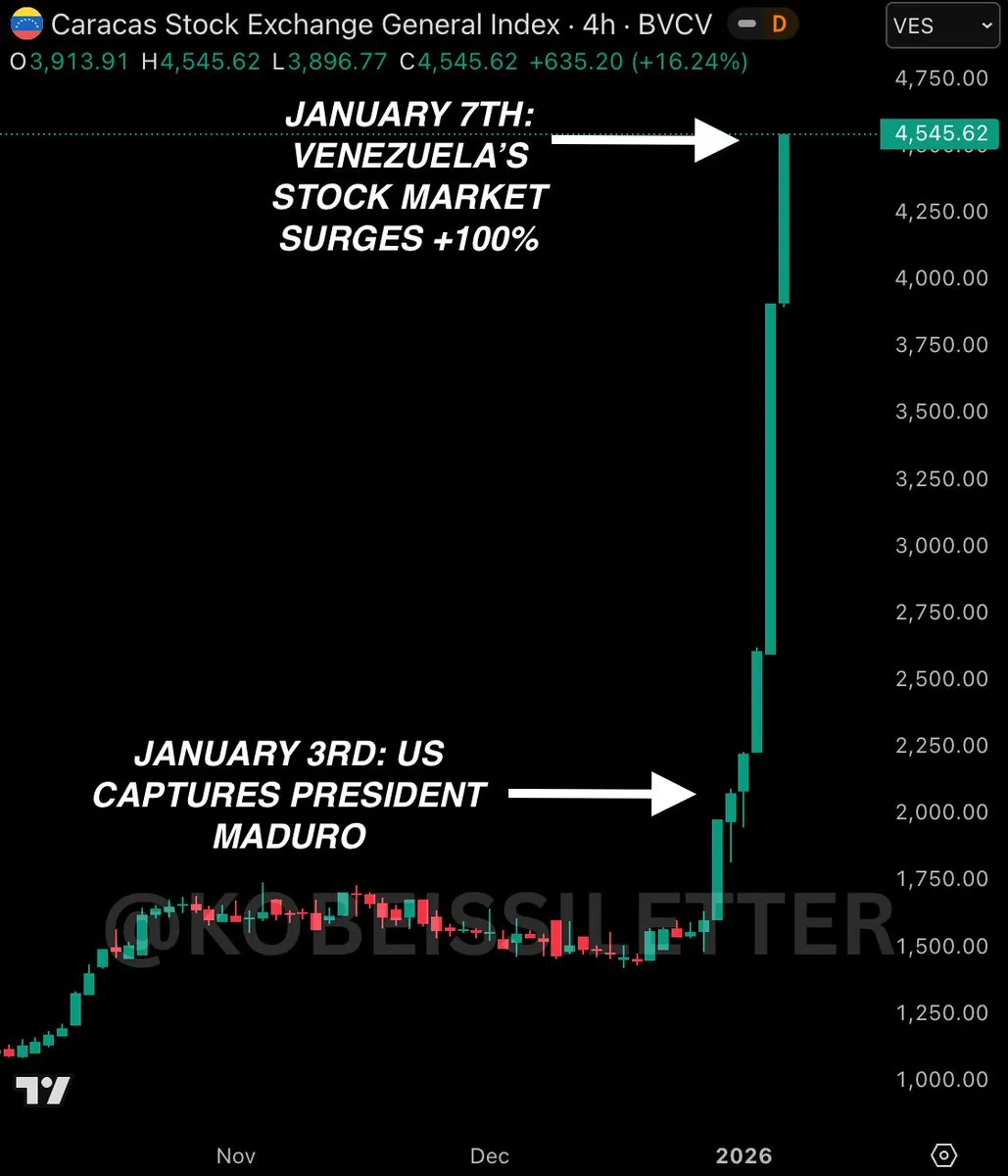

Late Friday night, US special forces struck areas around Caracas. The objective was to capture Venezuela’s leader, Nicolás Maduro, and transfer him out of the country. Unsurprisingly, this political and geopolitical event quickly spilled over into financial markets as a major surprise.

Caracas Stock Exchange General Index: 100%+ since Maduro’s capture on January 3

Last 10 trading days: 207%+ cumulative

In particular, BVCC, the Caracas Stock Exchange’s own stock, surged 75%+ after Maduro’s capture. The move was driven by growing expectations that the Maduro regime could be coming to an end, US sanctions might be lifted, and foreign capital and economic normalization could follow.

As always, events generate volatility, and volatility attracts speculative demand. This time, though, global retail investors all hit the same wall. Venezuela’s equity market is highly closed and extremely illiquid, which means there’s basically no way for foreigners to directly buy BVCC. In reality, the only option is to open a local brokerage account in Venezuela and go through the exchange that way.

At first glance, the solution feels obvious: just tokenize Venezuelan equities. Tokenization seems like a clean way to enable onchain trading without geographic barriers.

But once you look a bit closer, it becomes clear why tokenizing BVCC doesn’t really make sense. This is an extremely event driven market, and Venezuela’s equity market has been deeply depressed for years. Its entire annual trading volume is roughly on par with the daily trading volume of G20 major exchanges.

Caracas Stock Exchange 1y volume: $100M - $300M

NYSE 1d volume: $100B+

KOSDAQ 1d volume: $100M+

In short, tokenization platforms have very little incentive to tokenize BVCC for what is basically a few weeks of event driven demand. Depending on the model (SPV, transfer agent, etc.), tokenization involves legal overhead and often real inventory risk. On top of that, there just isn’t much demand for voting rights or dividend entitlements tied to Venezuelan equities in the first place.

This is where equity perp come in as an alternative. Their role is simple: take assets with limited global access and bring them onchain, backed by deep liquidity. As long as a reliable price oracle exists, almost any asset can be turned into a perp market.

Recent weekly BVCC volume (estimated): $5.2M

Considering this volume is generated solely by domestic investors and a handful of brokerages through spot trading, it’s not trivial. Surprise events always create strong speculative demand. That demand is a clear market opportunity for someone and a revenue opportunity for exchanges. The problem isn’t demand. It’s restricted access and the fact that the underlying exchange infrastructure is still far from mature.

The Venezuelan episode makes it clear that equity tokenization and equity perps are building fundamentally different markets.

Equity tokenization: focuses on high quality assets such as the Magnificent Seven. Its purpose is to provide full ownership onchain, including voting rights and dividend streaming. Onchain money market lending using tokenized equities as collateral is a good example.

Equity perpification: focus on event driven long tail equities, enabling exchanges to launch perpetual markets quickly. This mirrors how platforms like Hyperliquid or Bybit rapidly open perpetual markets for micro scale crypto assets such as meme coins or newly listed tokens to capture short term trading demand. The key difference is that equity perps are not limited to crypto native assets, but extend coverage to global events and traditional financial assets.

The takeaway is simple. There’s no real need for a tokenization vs. perpification debate. These two approaches are targeting entirely different markets.

Perps act as volatility provider around events, absorbing speculative demand. Compared to prediction markets, they support much richer positioning, including leverage, long/short exposure, and even high frequency trading. Equity tokenization, by contrast, is about plugging equities into onchain finance itself. It builds long term leverage as an infra layer.

Looking ahead, watching how this landscape evolves over the next few quarters will be genuinely important for anyone paying close attention to this market.