On January 8, Optimism announced a proposal to allocate 50% of Superchain revenue to OP token buybacks. The framing was bullish: "OP transitions from a pure governance token to a token that is tightly aligned with the growth of the Superchain."

Buybacks as a value accrual mechanism gained traction after Hyperliquid demonstrated their power. Buybacks as a value accrual mechanism gained traction after Hyperliquid demonstrated their power. In 2025, Hyperliquid directed ~$660M toward buybacks (roughly 7.6% of its circulating market cap), enough firepower to meaningfully support price.

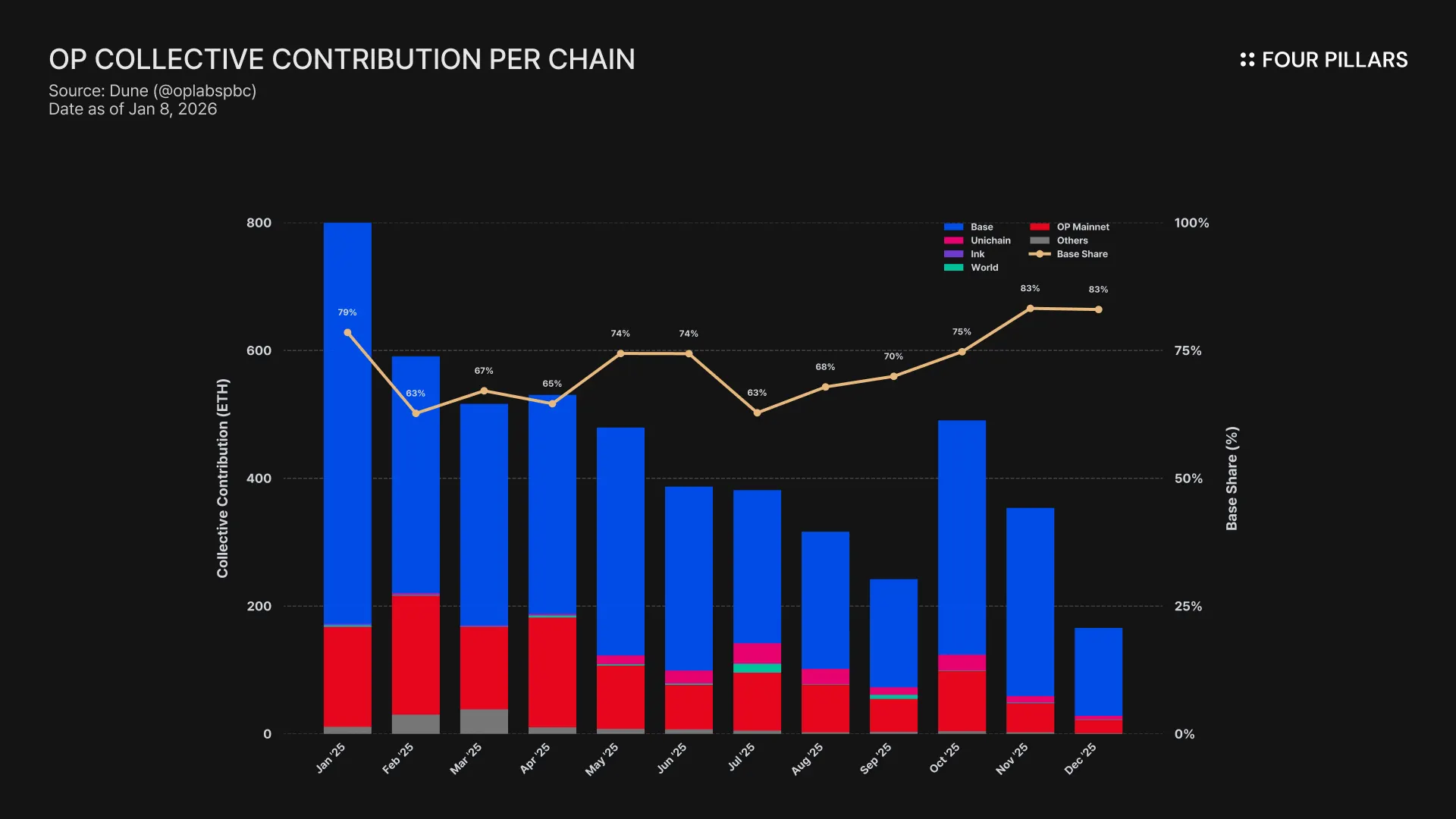

Optimism's situation is different. Superchain revenue has been declining:

2022: $10.9M

2023: $34.7M

2024: $40.7M

2025: $17.3M

The proposal allocates 50% of revenue to buybacks. In 2025 terms, that's roughly $8.5 million annually directed toward buying OP tokens. For context, OP’s circulating market cap is ~$620M (FDV ~$1.35B).

Optimism's proposed buyback represents approximately 1.4% of circulating market cap per year. Hyperliquid's buybacks represented multiples of that ratio. The difference in impact is proportional. Buybacks only work when the numbers are large enough to matter. OP’s case is like dropping a single drop of water into a pond and expecting ripples to reach the shore.

This isn't to say the proposal is bad per se. It's actually a meaningful step forward. For the first time, OP holders get some form of value accrual tied to Superchain success. The token evolves from pure governance to having economic alignment with network growth.

The announcement also signals Optimism's intent to expand OP's role further, potentially into staking rewards, sequencer coordination, and protocol security. These are the right directions for a token seeking long-term relevance.

But investors should calibrate expectations accordingly. The buyback alone won't materially move OP's price. At current revenue levels, the mechanism is more symbolic than substantive. If Superchain revenue continues to decline, the buyback becomes even less impactful.

The more interesting question isn't whether this buyback will pump OP, but whether Optimism can reverse its revenue decline, and that depends almost entirely on Base.

Base accounts for 70%+ of Superchain sequencer revenue. The entire buyback mechanism rests on a single counterparty that pays 2.5% and has every incentive to renegotiate, or leave entirely. Jesse Pollak has already announced that Base is "exploring" a native token—the exact language every L2 used 6-12 months before their TGE. If BASE holders vote on protocol upgrades, whose decision prevails—BASE governance or OP governance? If $BASE funds its own grants program, why would developers wait for RetroPGF? A $BASE token with overlapping governance scope makes Superchain membership ceremonial.

The economic logic supports this path. Exiting would save Coinbase millions per year in perpetuity. Meanwhile, the "value" of Superchain membership remains entirely prospective—future interoperability, future governance influence, future network effects—none of which has materialized. For a publicly traded company with fiduciary duties to shareholders, "future value" is a hard sell when the current cost is concrete and recurring (For a detailed breakdown, see our article “The Case for Selling $OP Before $BASE”).

Buybacks are a tool, not a strategy. Hyperliquid proved that buybacks can be powerful when backed by massive, growing revenue. Optimism frankly has neither at the moment. The proposal is a step toward better tokenomics, but OP holders shouldn't expect it to change the fundamental picture.