Source: Zmanian’s Twitter

In the aftermath of the sharp market crash on October 10, an intense debate has emerged around the question: “Who should be held responsible?” In this process, Binance and its founder, CZ, have become the primary targets of criticism on Crypto Twitter (CT). At the same time, another project has also been singled out as a potential culprit behind the crash — Ethena.

The core of the argument placing responsibility on Ethena is based on claims put forward by @zmanian (Zaki), a core contributor to Cosmos. His argument can be summarized as follows. Due to the nature of Ethena’s product — which requires maintaining a delta-neutral position — the protocol was structurally compelled to build up a large amount of short open interest in the market. The issue, according to this view, is that these short positions were structured in a way that made them ineligible for Auto-Deleveraging (ADL) on centralized exchanges (CEXs).

As market volatility increased, this allegedly led to a situation where Ethena’s large short positions were excluded from liquidation, while other traders’ short positions became the primary targets of ADL. In other words, the presence of structurally non-ADL-eligible short positions destabilized other market participants’ hedging strategies, causing risk to become concentrated in a single direction.

In addition, critics argue that Binance lacked a redemption or liquidity mechanism that would have allowed Ethena’s capital to be utilized in real time during periods of stress. As a result, during the rapid market deterioration on October 10, Ethena’s capital failed to function as a potential shock absorber, and ultimately proved insufficient to prevent a cascading wave of liquidations. This, in essence, forms the basis of the argument attributing responsibility for the crash to Ethena.

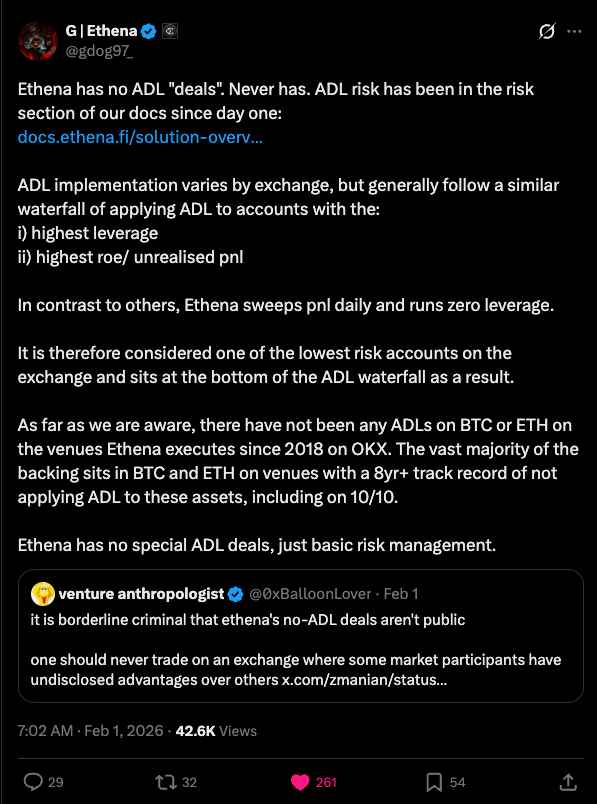

Source: Guy Young’s Tweet

In response to these claims, Ethena’s founder, Guy Young, offered the following rebuttal.

First, Ethena stated that it has never entered into any special or preferential ADL arrangements with centralized exchanges (CEXs). Furthermore, ADL-related risks were explicitly disclosed in the project’s official documentation from the very beginning. In other words, ADL was neither a hidden mechanism nor a structure uniquely designed to exempt Ethena, but rather a well-known and openly communicated risk from day one.

While ADL policies may differ slightly across exchanges, their underlying principles are largely consistent. In general, ADL is applied with priority to:

① accounts employing high leverage, or

② accounts with the highest return on equity (ROE) or unrealized profit and loss (PnL).

By contrast, Ethena operates under a structure that settles profit and loss daily (PnL sweep) and does not employ leverage. As a result, Ethena’s positions are categorized as low-risk under standard ADL criteria and therefore naturally fall toward the bottom of the ADL priority waterfall, according to the company.

Ethena further noted that across the CEXs it utilizes, there have been no recorded instances of ADL being applied to BTC or ETH — the primary assets Ethena trades — since 2018, and that this remained true even during the market crash on October 10.

Whenever problems arise in the market, people instinctively begin searching for someone to blame. To appease an angry crowd, someone must be brought to the square and placed on the guillotine. Of course, if the root cause of an issue can be clearly identified and a specific party is truly responsible, holding them accountable is entirely justified. However, what matters even more is putting structural safeguards in place to ensure that similar problems do not recur, and, through that process, strengthening the resilience of the market as a whole.

Source: Guy Young’s Tweet

Setting aside the question of Binance for the moment, there appear to be significant aspects of the Ethena case that are being unfairly interpreted. While large-scale liquidations on October 10 occurred simultaneously across most exchanges, the depegging of USDe — which many have focused on — was observed exclusively on Binance. Moreover, the USDe depeg did not occur prior to the liquidation cascade, but rather after large-scale liquidations were already underway. Framing the USDe depeg as the “cause” of the mass liquidations therefore seems to stretch the bounds of causality.

Separately from this debate, it is also true that $ENA’s price performance has been disappointing. This is likely due, at least in part, to unfavorable broader market conditions and the growing dominance of short positioning, which has limited Ethena’s ability to generate meaningful returns through funding rates. That said, USDe has now been listed on multiple centralized exchanges — including Upbit — and liquidity is steadily being established. As market conditions stabilize, it is reasonable to hope for additional initiatives centered around $ENA to follow.