Hyperion DeFi put out its first shareholder letter under new CEO Hyunsu Jung on January 12. The company is explicitly positioning itself as an on-chain operating business built around its treasury.

The deployment timeline they cite is actually pretty impressive. The letter details how Hyperion deployed its treasury within months of its $50M PIPE:

8 days: Launched "Kinetiq x Hyperion" validator

30 days: Created HiHYPE, the first institutional LST on HyperEVM

September 2025: Onboarded Credo as first HAUS client

October 2025: Allocated 500,000 HYPE to Felix for a HIP-3 exchange (equities and commodities, 24/7)

December 2025: Partnered with Native Markets, allocating 300,000 HYPE for USDH incentives

Q3 2025 net income came in at $6.6M, which they note is the most profitable quarter in the company's 10+ year history. That's a weird flex when you remember this used to be an ophthalmic device company called Eyenovia, but the point stands—they're generating revenue from multiple lines now, not just sitting on tokens hoping the number goes up.

This is the thing I keep coming back to with DATs. The ones that survive won't be the "infinite ATM" operators who just raise equity, buy tokens, repeat until the music stops. The interesting ones build revenue streams that don't collapse when HYPE pulls back 50%.

Validator commissions, HAUS fees, exchange revenue sharing with Felix—these generate cash regardless of where the token trades on any given day. Whether the numbers are big enough to matter at scale is still an open question, but the architecture is right. Hyperion seems to understand that the game isn't about accumulating the most HYPE, it's about making each share of equity represent more productive HYPE over time.

Another section that caught my attention was the AI discussion. Jung references Nof1 AI's Alpha Arena from October 2025, where frontier models like GPT5, Claude Sonnet 4.5, and DeepSeek Chat V3.1 were each given $10,000 to trade on Hyperliquid in a live competition.

The thesis he's building toward is that as agentic trading scales, capital will naturally flow to platforms with the deepest liquidity and best technical infrastructure. It's speculative, and maybe a bit early to be putting in a shareholder letter, but if you buy the premise that AI agents will increasingly participate in financial markets, Hyperliquid's positioning does make sense.

Management and the board collectively bought 189,204 HYPD shares in December 2025. Insider buying doesn't guarantee anything, but it's at least consistent with the conviction they're expressing publicly.

The thing I'll be paying attention to is whether crypto-per-share actually grows. Hyperion has a $100M shelf registration in place, meaning they can keep issuing equity to buy more HYPE. That's fine as long as the treasury grows faster than dilution, but if they start issuing into weakness without operational income to backstop it, the math turns ugly.

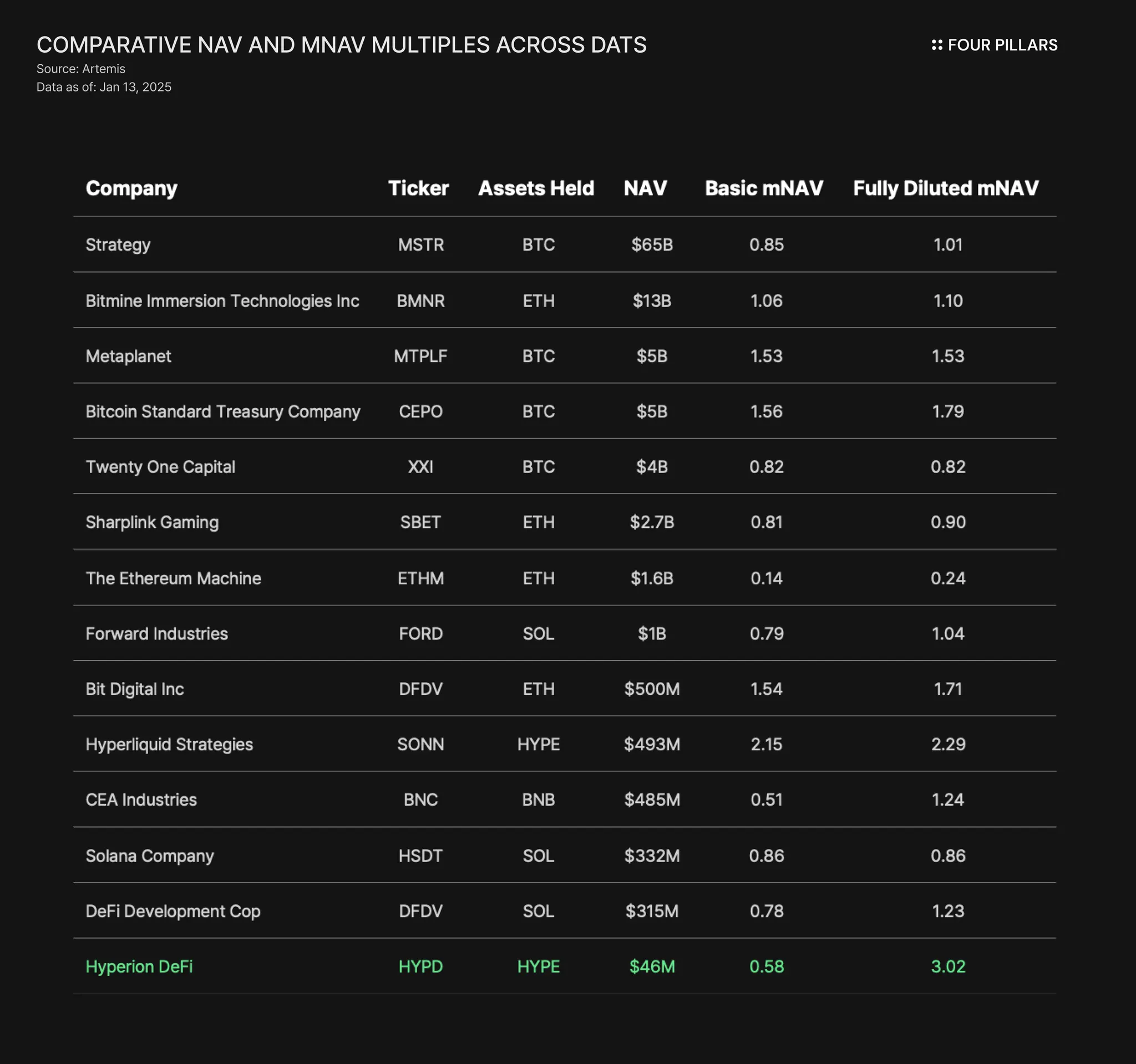

The other variable is whether HYPD trades at a premium or discount to mNAV. A persistent premium validates the thesis that institutions want Hyperliquid exposure but can't hold HYPE directly. A persistent discount suggests the equity wrapper isn't adding much.