When NFTs swept through the crypto market, many people struggled to intuitively grasp where their value came from. One of the most commonly used analogies to explain this was the trading card market. Ironically, long before NFTs ever existed, the card market had already embodied the core mechanics that define NFTs today—scarcity, ownership, and transferability.

Today, that same card market is beginning to take shape directly on top of blockchain infrastructure. One of the most prominent examples is Collector Crypt ($CARDS), which gained explosive popularity starting last year. Collector Crypt has positioned itself as a market leader by enabling physical trading cards to be traded as if they were digital assets.

Collector Crypt stores physical cards in partnered vaults, tokenizes them, and provides a marketplace where those tokens can be traded. Because of this structure, it has been widely regarded as a significantly more trustworthy alternative to traditional peer-to-peer card marketplaces (such as eBay), which rely heavily on bilateral trust between buyers and sellers.

Of course, the primary revenue source for TCG marketplaces like Collector Crypt is not limited to transaction fees from secondary trading. In practice, the majority of revenue comes from so-called gacha mechanics—services that allow users to purchase randomized card packs. Users pay a fixed amount to open a pack, hoping to pull a card worth more than what they initially paid. Up to this point, Collector Crypt does not differ meaningfully from other gacha-based products.

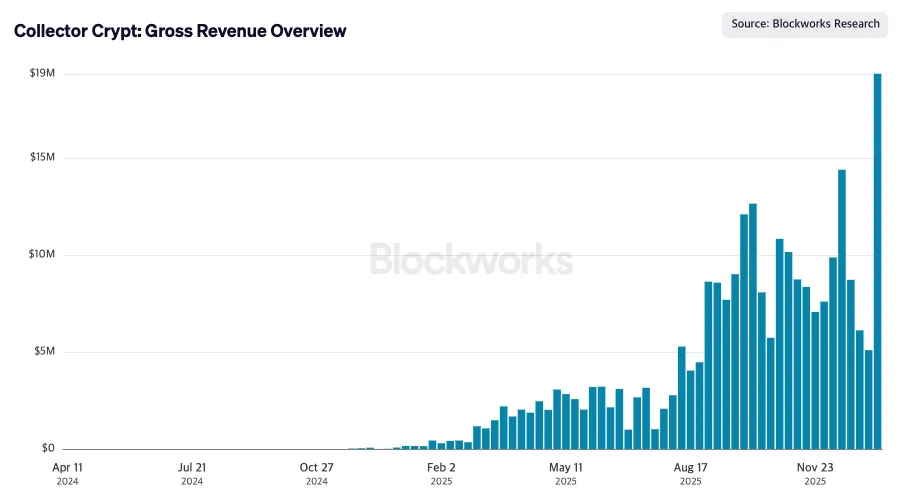

Where Collector Crypt goes a step further is with the introduction of gacha buybacks. Under this system, if users are dissatisfied with the cards they receive after opening a pack, they can immediately sell those cards back to Collector Crypt. While this requires accepting a discounted price relative to market value, the guarantee of instant liquidity makes this mechanism a near-default choice for many users. Users sell their cards at a discount and use the proceeds to purchase additional gacha packs, repeating this cycle until they obtain a card they deem satisfactory. This structure has driven Collector Crypt’s revenue steadily upward. In fact, in just one week, approximately $19 million was spent on purchasing gacha packs on the platform, generating roughly $1.9 million in revenue for Collector Crypt from its gacha products alone.

Source: Blockworks

Considering how few products in the crypto market are capable of generating $1.9 million in weekly revenue, Collector Crypt’s recent performance is undeniably impressive. That said, it is important to be clear about one point: it is far more likely that this revenue is not being driven by fundamental demand for TCGs themselves.

From the author’s perspective, today’s Collector Crypt is not fundamentally different from a new form of casino disguised as a TCG platform. Most users follow a repetitive behavioral loop—paying to purchase gacha packs, opening cards, immediately selling them back at a discount if the outcome falls short of expectations, and using the proceeds to buy another gacha pack. This cycle is repeated continuously.

However, the “real” demand that has historically sustained the traditional card market has never been created solely by such flippers—participants who purchase cards purely for short-term profit. In established TCG markets, demand has emerged across multiple layers: players who need cards for actual gameplay, collectors driven by pure ownership and collection motives, and participants who engage in resale and trading. In contrast, the demand observed in crypto-native TCG products like Collector Crypt is overwhelmingly concentrated on buying and selling alone. This imbalance highlights how the crypto TCG market has yet to meaningfully bridge the gap with the traditional card market, and how much further it still has to go.

The author believes that a truly meaningful crypto TCG market can only be built once players emerge who are capable of closing this gap. To do so, cards traded within crypto TCG ecosystems must move beyond being mere speculative instruments and offer tangible utility, while the overall user experience must also improve. At the same time, the perception of crypto TCG platforms as nothing more than speculative venues needs to be gradually dismantled. From this perspective, while Collector Crypt’s current performance is certainly noteworthy, without a long-term product vision that genuinely attracts existing demand from the traditional card market, its revenue growth is likely to remain temporary.

Viewed more optimistically, this also implies that there is ample room for more advanced and refined products to emerge—products that recognize these limitations and successfully overcome them. In that sense, the crypto TCG market remains in its early stages, and its future evolution is still well worth watching.