Lending is one of the major use case in onchain finance, and has seen adoption over the year. Notabley, AAVE now has $35 Billion supplied, and $22 Billion borrowed.

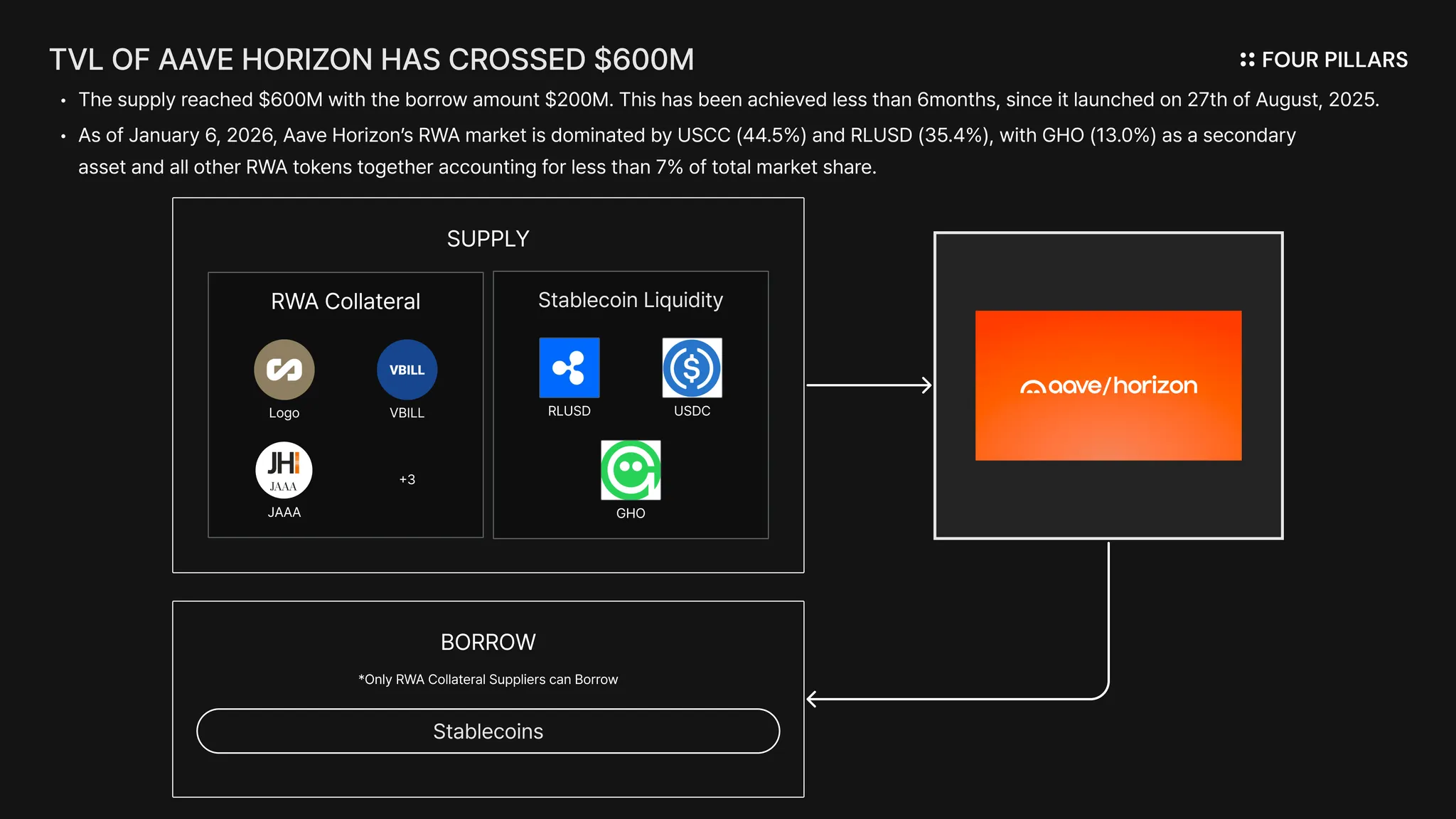

It also has a RWA focused lending market called AAVE Horizon, and the supply reached $600M with the borrow amount $200M. This has been achieved less than 6 months since it launched on 27th of August, 2025.

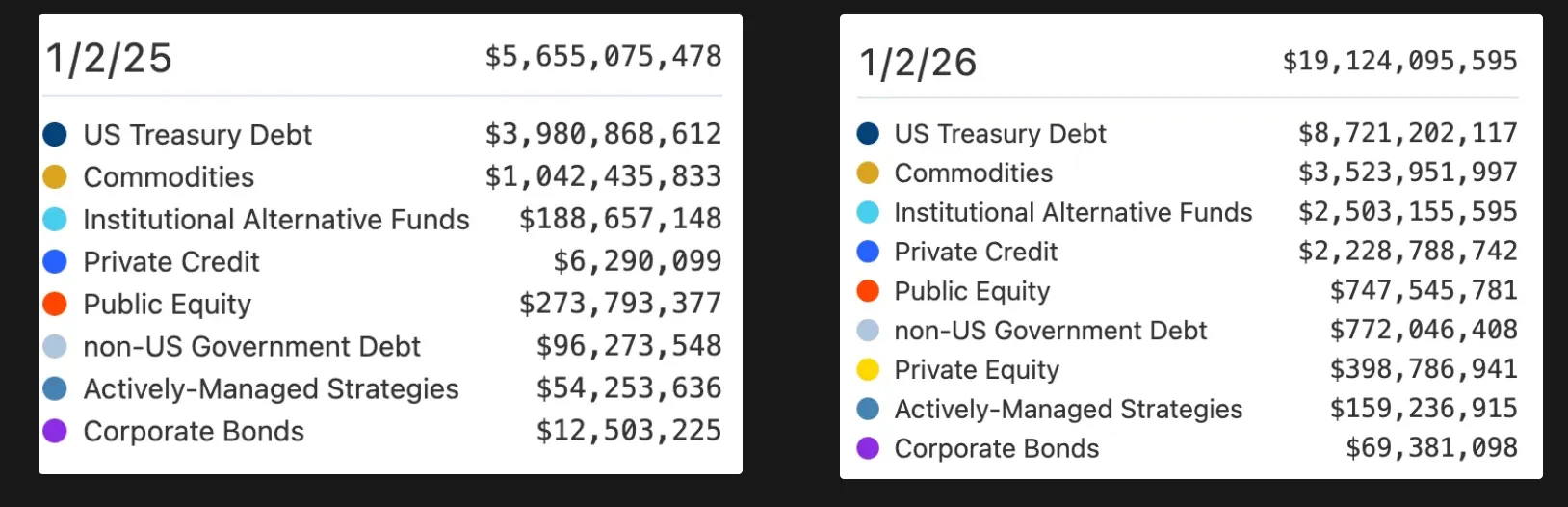

Also, the RWA market is growing fast. In recent one year, the onchain RWA market has grown from $5.1B to $19.1B, nearly a 4× increase in total value.

This growth has been seen across all different assets:

tokenized U.S. Treasury bills more than doubled from about $3.9B to $8.7B

commodities including gold, surged from $1.0B to $3.5B

institutional alternative funds jumped from $0.189B to $2.5B

private credit scaled from near zero to over $2.2B

Onchain public equity, non-US government debt, private equity, and corporate bonds further increased and showed that RWA adoption is no longer concentrated in a few asset class.

Source: RWA.xyz

On the supply side, participation is deliberately segmented by asset type.

RWA collateral suppliers must be qualified and allowlisted by the specific RWA issuer. Only approved users can supply tokenized RWAs into the market. These assets are collateral-only, represented by non-transferable aTokens, and cannot be borrowed by other participants. This design enforces issuer-level control, prevents secondary trading of collateral positions, and preserves regulatory and risk integrity.

In contrast, stablecoin liquidity supply is permissionless. Any user can supply supported stablecoins - such as USDC, RLUSD, and GHO - to earn yield. However, stablecoins supplied to the market cannot be used as collateral and serve purely as liquidity for borrowers.

On the borrowing side, access is strictly gated by collateral eligibility. Only users who have supplied and enabled approved RWA collateral can only borrow stablecoins (e.g., USDC, RLUSD, GHO).

Borrowers must maintain required collateralization ratios determined by the risk parameters of their underlying RWA assets.

Source: Aave: Horizon RWA | Dune

Access to on-chain RWA lending remains limited today, but even in its early form, it is already beginning to pull meaningful capital onchain. Most current activity is concentrated around tokenized U.S. Treasuries, which serve as a low-risk entry point for institutions experimenting with onchain.

As the universe of tokenized assets expands beyond treasuries, into tokenized equities, non-USD stablecoins, and other financial instruments, lending is likely to become the primary mechanism through which traditional capital migrates onchain.

Lending turns tokenization from a passive representation of assets into an active financial asset and will enable more advanced use cases - such as RWA looping, on-chain trading strategies, and cross-currency financing.

Consider a simple example: a user deposits tokenized TSLA as collateral, borrows USDC, and uses that liquidity for payments or reinvestment. Alternatively, a user deposits USDC and borrows JPY-denominated stablecoins to hedge currency exposure. These are familiar financial behaviors, but executed natively onchain, with programmability and composability layered on top.

The access is now limited, but the growth just started to kick-off.