Recent incidents involving the Bybit hack and Hyperliquid HLP attack clearly illustrate the dilemma crypto users face between CEX and DEX: CEX requires users to completely depend on trust in a specific institution, while DEX's complete openness creates structural constraints that make it difficult to accommodate institutional investors or general users.

Kinto, as a security-first Layer 2, prevents Sybil attacks and meets institutional investors' compliance requirements by mandating KYC at the chain level and allowing transactions only through dedicated smart wallets with account abstraction.

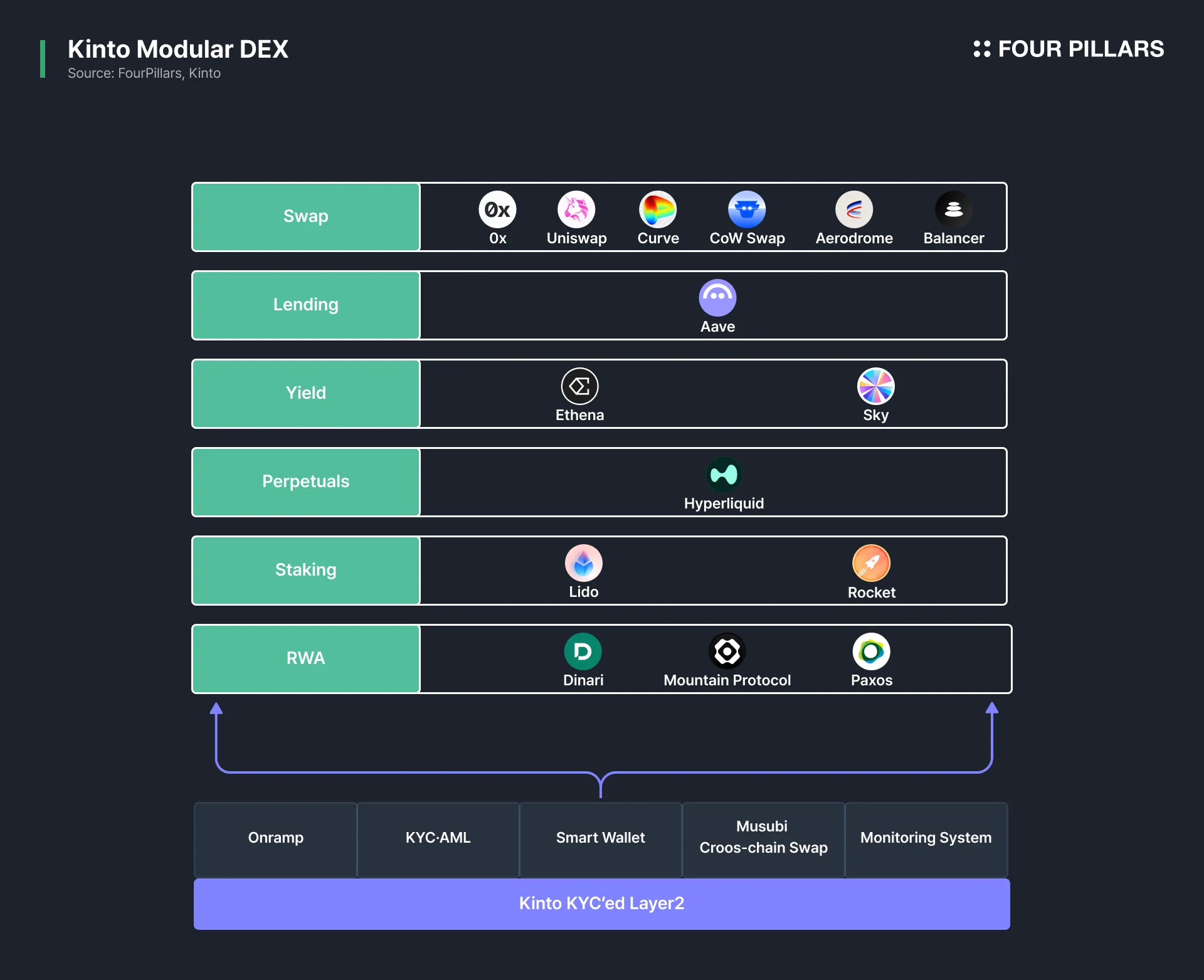

Furthermore, Kinto adopts a modular DEX strategy, integrating its security-first architecture with proven DeFi protocols like Hyperliquid and Ethena to secure robust liquidity and user base.

Kinto's approach presents a new form of on-chain financial system that balances accessibility, security and openness by protecting privacy through user-owned KYC, enhancing user experience with smart wallet convenience features, and providing diversified market opportunities through cross-chain swap infrastructure.

Two recent major incidents—the Bybit hacking crisis and the Hyperliquid HLP attack—clearly demonstrate the dilemma crypto users currently face between CEX and DEX. This dilemma stems from the fact that crypto users cannot guarantee a stable trading environment in either CEX or DEX. Let's briefly review the details of these two incidents to consider the pros and cons of each exchange type and possible alternatives.

On Feb 21, 2025, news broke of a hack during the regular fund transfer process between Bybit's multisig cold wallet and hot wallet. The hack employed a social engineering method that manipulated the wallet signatories' signing interface to approve transactions that appeared to be legitimate transfers. The stolen assets amounted to approximately $1.46B in ETH, representing about 75% of Bybit's ETH holdings, making it the largest asset theft in crypto history.

Source: X(@benbybit)

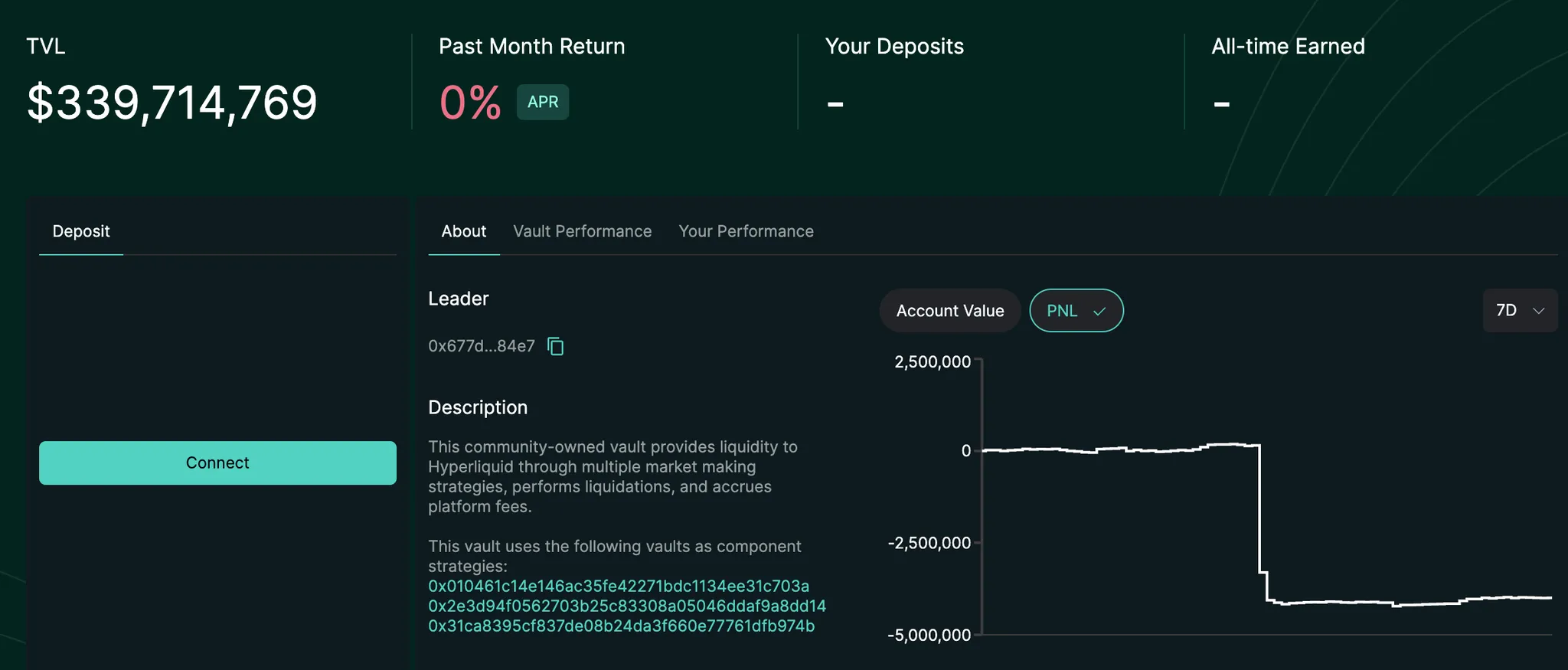

On March 12, 2025, as the Bybit hacking situation was being resolved, abnormal trading activity was detected on Hyperliquid. The community soon learned that Hyperliquid's shared fund pool (HLP) had suffered a loss of approximately $4M. The cause was a trader who exploited vulnerabilities in the liquidity mechanism.

The incident began with a calculated strategic move by a trader who utilized approximately 50x leverage to build a position worth $2B (113,000 ETH). Despite the large position size, the deposited margin was relatively small, only $4-10M in USDC. As ETH prices rose and the position generated profit, instead of completely closing the position to convert unrealized gains into net profit, the trader gradually withdrew margin deposits.

Through these withdrawals, the trader could realize part of the net profit in advance without closing the position, while intentionally lowering the maintenance margin ratio. This behavior can be interpreted as a deliberate strategy to create a situation where the position could be more easily liquidated while securing profits in advance by withdrawing maintenance margin.

Source: Hyperliquid Vault

When ETH price finally reached the liquidation threshold, the trader's large position was forcibly liquidated. At this point, Hyperliquid's liquidation engine was designed to have the liquidity pool (HLP) absorb losses incurred during position settlement. This allowed the trader to realize profits without directly closing the position in the market (avoiding slippage), while transferring all liquidation losses to the HLP shared fund pool. As a result, the trader gained a net profit of about $1.8M, but the HLP vault suffered a loss of approximately $4M.

1.3.1 Bybit Hacking: Not Your Keys, Not Your Coins

What insights can we gain from these two incidents that occurred within a short time of each other? First, the high accessibility of CEX clearly provides value. Users can easily trade crypto assets through CEX without navigating the relatively poor user experience and steep learning curve of on-chain transactions. This accessibility advantage is a major reason why CEX maintains high market share despite frequent large-scale hacking incidents. Although on-chain users are gradually increasing, the fact that DEX usage compared to CEX remains around 20% with no further progress demonstrates CEX's strong moat.

Nevertheless, CEX has the fatal limitation that users cannot fully control their own assets. Since a centralized entity manages users' assets, there is always an inherent risk that assets may be operated non-transparently or stolen through hacking.

Particularly, as seen in the Bybit hack using social engineering methods, CEX is structured with a single entity managing large-scale assets while being vulnerable to human error, making it an easy target for hackers. In fact, cases where CEX misappropriated customer assets or had assets stolen due to security vulnerabilities have occurred countless times throughout crypto history.

Consequently, as the phrase "Not Your Keys, Not Your Coins" suggests, the custodial structure of CEX inherently carries the fundamental risk that users do not have control over their assets. The Bybit hacking incident once again clearly demonstrated the instability of the trust-based model that CEX relies on.

1.3.2 Hyperliquid HLP Attack: DeFi Is Sometimes a Brutal Economic Game

How should we interpret the cause of the Hyperliquid HLP attack? Security firm Three Sigma explained that the incident was "not a bug or exploit, but a brutal game using the liquidation mechanism." DeFi is essentially a market where economic games take place based on openness (permissionlessness), an environment where anyone can identify market inefficiencies and maximize profits through transparently public on-chain financial systems.

From this perspective, the Hyperliquid case can also be viewed as an anonymous user maximizing profits by exploiting DeFi characteristics and system design flaws. Although it may be difficult to fully advocate for abnormal transactions aimed at attacks, this incident clearly shows the unique financial environment characteristics that only DeFi can provide. In other words, there may be a view that the Hyperliquid attacker was simply making maximum use of DeFi's open characteristics.

But would investors who have a primary need to minimize potential risks prefer such a trading environment? For example, DeFi environments where "brutal games" might occur may not be suitable for novice users or institutional investors requiring high levels of security. In situations like the HLP attack where protocol vulnerabilities are exploited, beginners find it difficult to respond rationally. Furthermore, MEV or liquidity fragmentation causing bridge usage or high gas fees also act as significant entry barriers. For these reasons, current DeFi has been reduced to a specialized capital market used only by limited market participants.

1.3.3 Alternatives Derived from CEX and DEX Pros & Cons

In summary, CEX and DEX each have unique pros and cons. CEX provides high accessibility to everyone but has the fundamental limitation that users cannot fully control their assets. On the other hand, DeFi provides an open financial environment with a non-custodial structure, but often exposes users unfamiliar with on-chain operations to brutal economic games.

With such clear pros and cons between CEX and DEX, what approach is needed to expand on-chain finance to the next level? An environment that provides CEX-level accessibility while allowing users to fully manage their assets with a non-custodial structure could be an alternative to this. Additionally, users may find greater utility in a safer environment even if the level of openness or decentralization is partially reduced. For example, having security measures at the protocol level that can identify and restrict abnormal transactions that might cause substantial damage to HLP, or being able to verify trader identity.

At a time when exchanges are generally perceived as the two extremes of CEX and DEX, a compromise somewhere in the middle within the paradigm created by these two extreme entities has become an important topic in the current crypto market. That is, a design that appropriately balances accessibility, security, and openness while being based on on-chain systems where users fully own their assets.

Kinto has emerged as a new on-chain financial infrastructure designed with security and user experience as top priorities while maintaining DeFi's core value of openness.

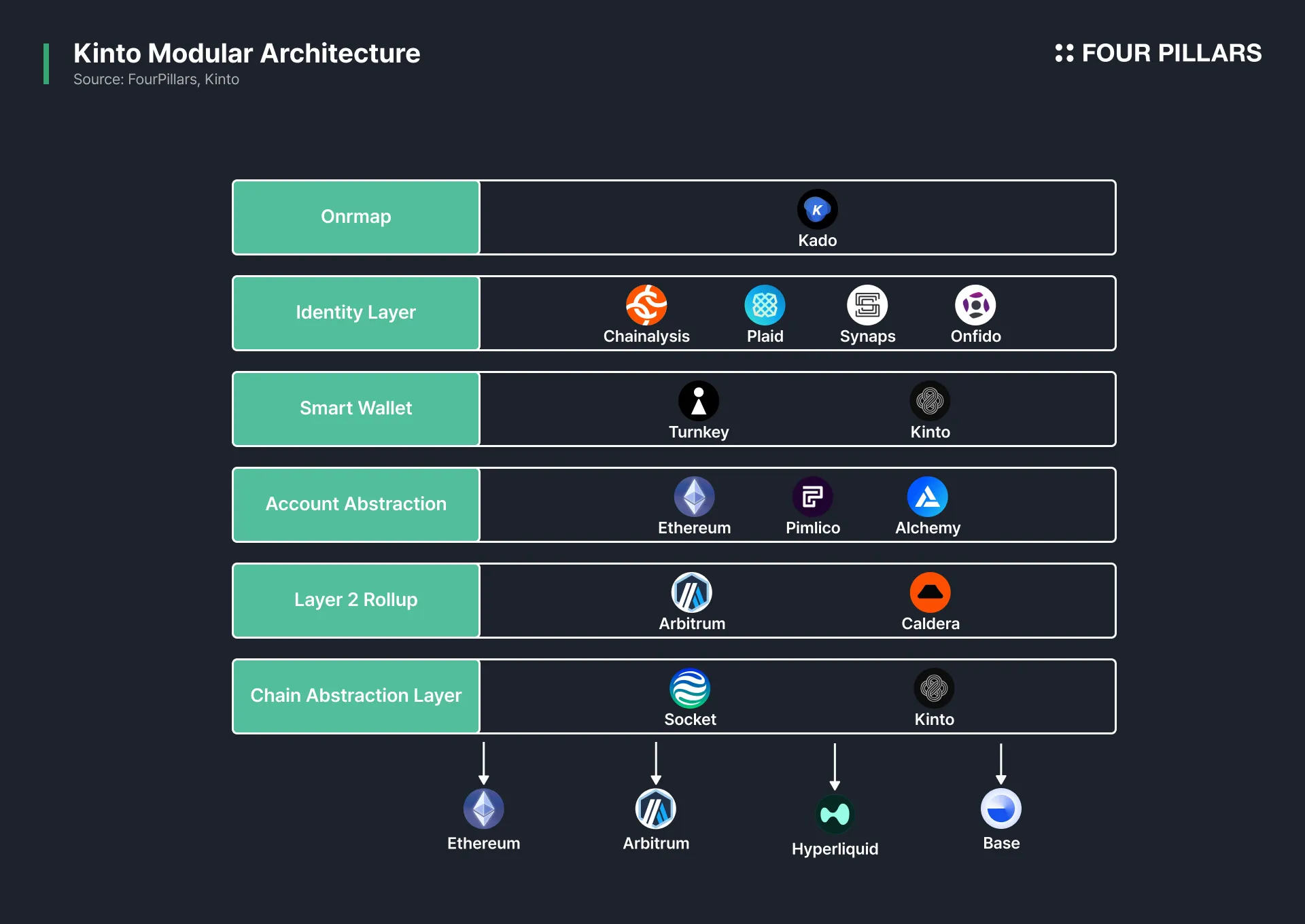

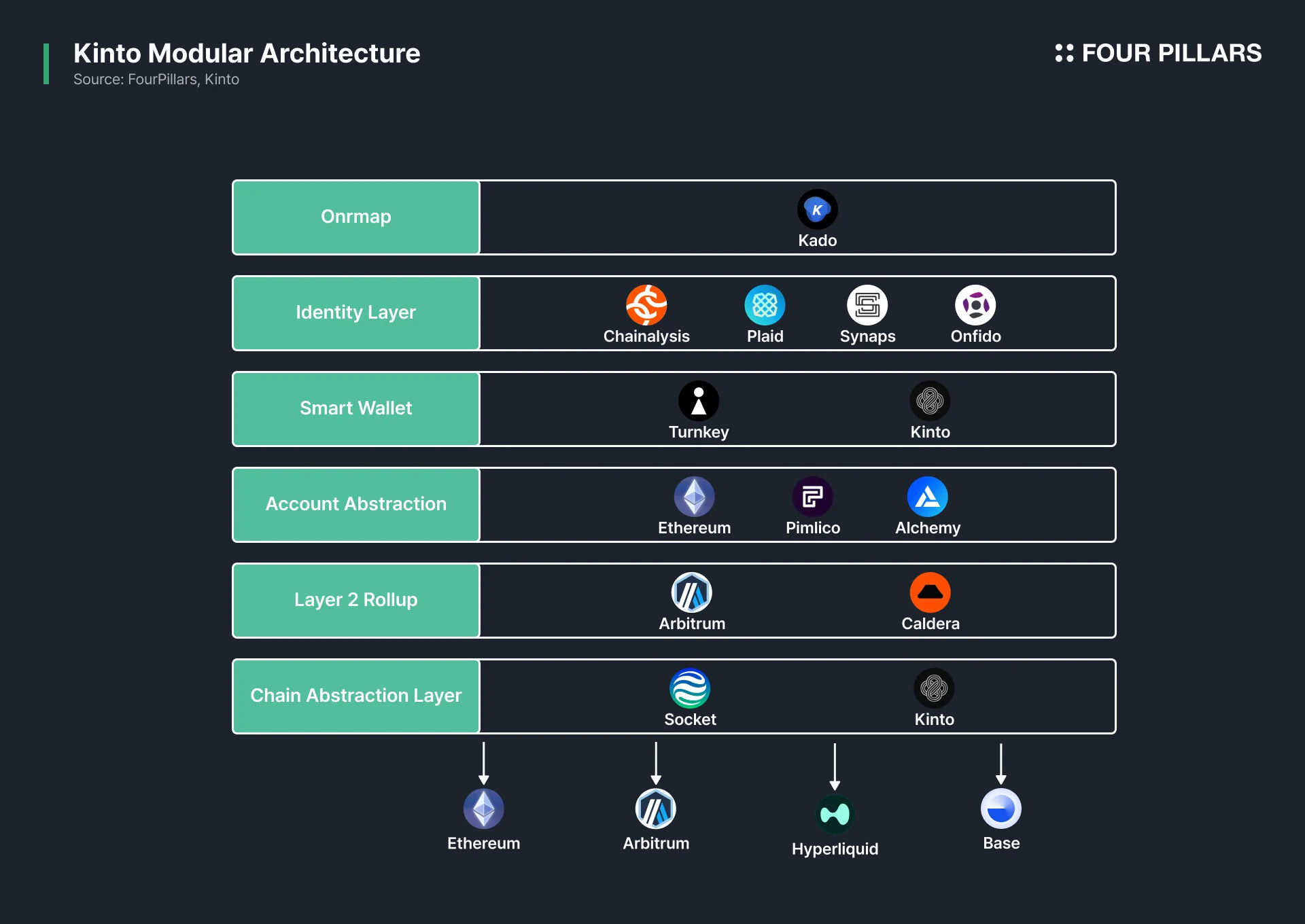

Kinto is fundamentally an Ethereum Layer 2 based on optimistic rollup built using Arbitrum's Nitro stack. It secures data availability through connection with the Celestia network and obtains transaction finality through settlement via the Ethereum mainnet. The sequencer plans to transition to a decentralized sequencer through Espresso in the future.

Up to this point, it appears like a typical Ethereum Layer 2 with a modular architecture, but Kinto's key differentiator can be found in its security-first Layer 2 structure. At Kinto's core is a design that embeds KYC·AML certification procedures at the chain level. As we'll explore further later, all users wishing to trade on the Kinto Layer 2 must complete KYC·AML certification and can only trade using Kinto dedicated wallets that implement account abstraction with the ERC-4337 standard. Additionally, Kinto does not focus on securing its own liquidity like other Layer 2s but closely integrates with existing DeFi protocols.

With this design, Kinto can achieve institutional-level compliance and risk management requirements. Additionally, through non-custodial wallets, users can fully control their assets while utilizing on-chain trading based on proven DeFi protocols. Through this, Kinto ultimately aims to build a trading environment that balances the high accessibility of CEX and the openness of DEX on a security-first Layer 2.

Kinto is closer to a position as a secure DeFi hub for identity-verified users rather than a space for anonymous users to freely play economic games. This direction inevitably makes it difficult to attract hardcore DeFi enthusiasts who pursue permissionlessness or decentralization at a complete level as main users. Anonymous users who don't want to leave any personal identifying information on the internet are not Kinto's main target users, and crypto degens who typically create multiple wallet accounts mainly for airdrop farming are naturally excluded due to Kinto's structural design.

On the other hand, Kinto builds optimal infrastructure to embrace beginner users and institutional investors through its security-first design. It also serves as an attractive alternative for crypto users already familiar with on-chain infrastructure but selectively seeking security-first transactions. While this approach may seem to target niche users in the current crypto market, if we include the majority of general users who haven't yet experienced on-chain and institutional investors, it can be seen as targeting the broadest user base. Kinto's potential for expansion also lies in this unexplored territory.

Among Kinto's features, one notable aspect is its design as a Layer 2. Layer 2 enables Kinto to maximize security levels and DeFi composability in building the secure DeFi hub it aims to create.

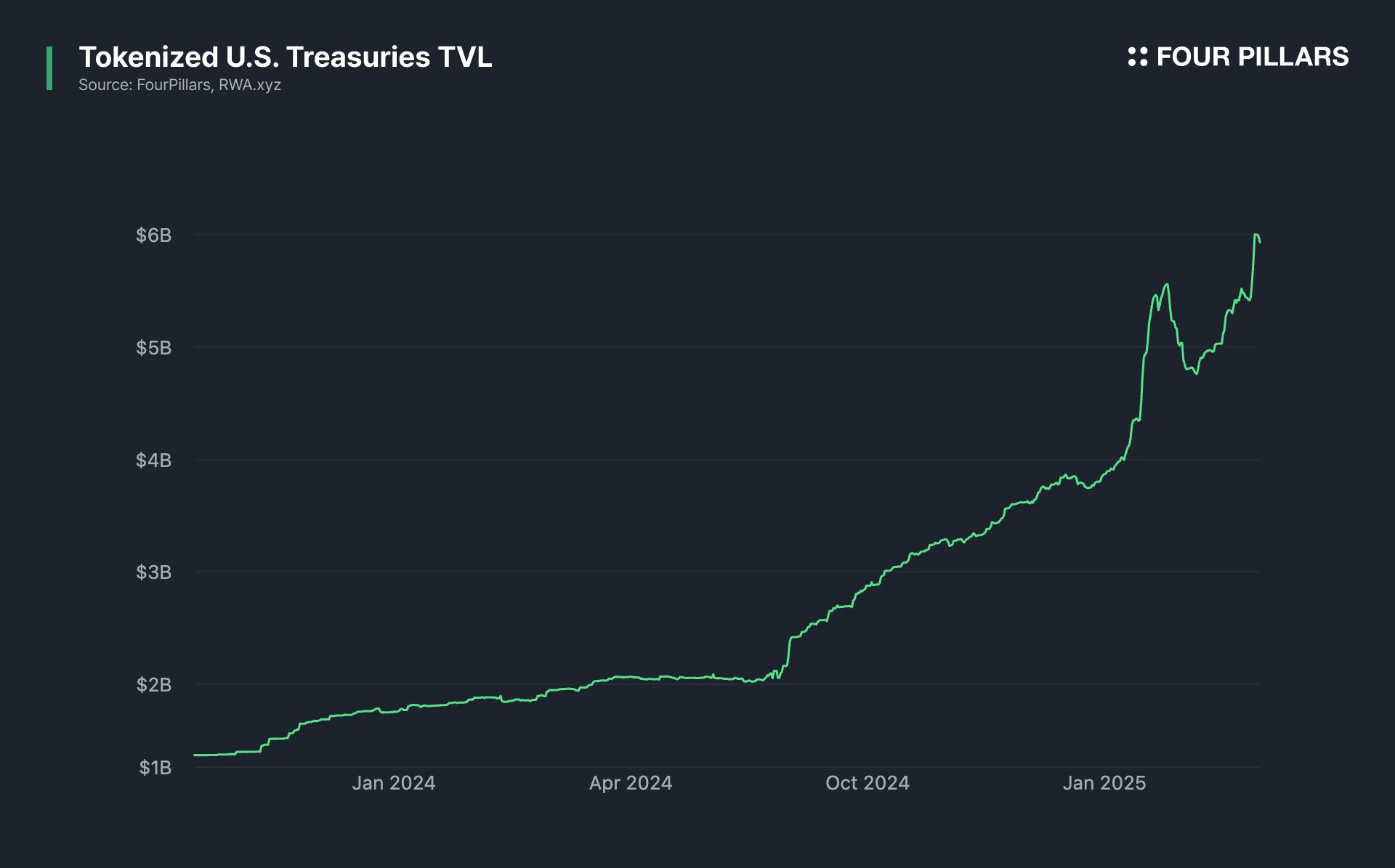

The phenomenon of traditional financial assets being tokenized and crypto assets being incorporated into traditional financial products is accelerating, and now DeFi and traditional finance are so closely integrated that it's becoming difficult to distinguish between them. For example, tokenized US bonds have a total TVL exceeding $4.6B, growing 475% year-over-year. Additionally, BlackRock, the world's largest asset manager, has tokenized BUIDL, their USD institutional fund, designing it for real-time dividends and interest payments on-chain. In line with this, the Ethena protocol has issued USDtb using this BUIDL fund as collateral, clearly demonstrating the accelerating combination of DeFi protocols and traditional financial assets.

However, compliance requirements such as KYC·AML act as major obstacles for banks and traditional financial institutions trying to utilize DeFi. This is because DeFi, which has developed with openness as its core value from the beginning, was not designed to satisfy institutional compliance or risk management requirements.

Institutional DeFi solutions catering to institutional investors' needs have emerged previously. For example, Aave Protocol's Aave Arc existed as a single application or individual liquidity pool based on the Ethereum mainnet. However, these solutions had a fundamental limitation in common: when combined with other DeFi protocols, they couldn't consistently apply their regulatory compliance requirements across all DeFi protocols, which is why most were built as permissioned pools.

To bridge this gap, Kinto has built security measures at the Layer 2 chain level, including KYC mandates, on-chain firewall, and continuous AML monitoring. This fundamentally blocks network access for blacklisted individuals or companies, minimizing illegal activities like money laundering and terrorist financing, and fundamentally preventing security vulnerabilities like large-scale hacking. Additionally, since consistent compliance standards are applied to Kinto-based DeFi protocols, users can utilize both an integrated user experience and the interconnectedness of open DeFi simultaneously.

Kinto's solution greatly lowers the entry barrier to DeFi for institutional investors and traditional financial institutions by providing a trustworthy on-chain financial environment. This enables higher potential for combining on-chain and tokenized assets without sacrificing interconnectedness, while meeting regulatory compliance requirements. As a result, Kinto can take an effective approach to building an on-chain financial infrastructure designed with security and user experience as priorities while maintaining DeFi's core value of openness.

Ultimately, Kinto's security elements support the vision Kinto aims to show. Let's examine Kinto's security-first designs in more detail and learn more about how Kinto can become a differentiated and independent DeFi hub compared to existing solutions.

3.1.1 Chain-Level KYC

All Kinto users must pass KYC·KYB certification before fully participating in the network, and continuous AML monitoring is conducted at the network level. KYC providers such as Onfido, Synaps, and Plaid, which meet security and privacy protection standards, conduct user identity verification and AML checks, and this process involves typical KYC procedures such as ID submission or liveness verification.

An EOA (Externally Owned Account) generated with a non-custodial passkey is issued to users whose KYC certification is approved - however, an important difference is that in other blockchains, EOAs can be created as many as desired through wallet creation, but in Kinto, EOAs are only created after completing KYC. This means that users who have not completed KYC certification cannot execute transactions at all. Through this network-level transaction gatekeeping, Kinto blocks unauthenticated users' access at the source.

Once an EOA is created in a state linked to KYC verification status, Kinto's soulbound token, 'Kinto ID', is issued to the on-chain account. Since Kinto ID is in the form of a non-tradable NFT, it serves as proof that the user has completed KYC certification. This token displays flag information such as whether the user has completed KYC, has investor certification qualifications, and has AML violations. Obtaining this Kinto ID is the most crucial procedure in Kinto's entire user journey, as only accounts holding a Kinto ID can execute transactions within Kinto.

Kinto's KYC providers not only verify users' identities but also continuously perform AML monitoring to check if users are registered on sanction lists such as terrorist financing support or sanctions lists. If a user subsequently gets on a sanctions list as a result of monitoring, it is immediately reflected and indicated on the Kinto ID NFT. At this time, the Kinto ID is linked to a plug that can sanction transactions in real-time, so if a user gets on the OFAC sanctions list while using Kinto, their ID will display the sanctioned status, allowing transactions to be restricted or suspended.

3.1.2 User-Owned KYC

The User-Owned KYC model is designed to mandate identity verification at the chain level while allowing users to have control over their KYC data. Kinto's structure of mandating KYC is effective in increasing network trust but can cause privacy issues. If all users' identity information and transaction history were viewable at the chain level, this would be no different from the privacy level of a CEX. To solve this problem, Kinto strengthens privacy by separating Personally Identifiable Information (PII) and on-chain accounts through user-owned KYC.

A user's actual name, address, ID copy, and other personally identifiable information are stored encrypted only in the KYC provider's database. The important point is that this data is not connected to wallet information. In other words, the KYC provider knows that person A has passed KYC certification but is separated so they don't know which wallet that person uses on Kinto.

Even if a KYC provider is hacked and data is leaked, on-chain wallets cannot be identified with the leaked personal information. Conversely, no user's personal information is stored on the Kinto blockchain, only whether KYC was performed and the results are tokenized as KYC ID. Through this structure, Kinto can achieve Sybil prevention and regulatory compliance at the chain level while ensuring user privacy.

In addition, Kinto is designed with importance placed on not sharing personal information without user consent, including situations where dapps need user identity information. For example, if a dapp needs identity information to provide a specific service, it must request consent from the user to provide that data.

At this point, if the user consents through signing with their Kinto wallet, the dapp calls Kinto's KYC node API and receives only the information approved by the user, so that only the minimum necessary information is delivered to the desired party. This means that while KYC information and on-chain accounts are separated by default, users selectively provide information to specific services only under their own decision.

Of course, exceptions exist. Generally, KYC information and on-chain accounts are separated, but limited connections are allowed in urgent situations such as serious crimes or hacking. Even this is not arbitrarily connected at the chain level, but under the approval of Kinto governance, the KYC information of suspicious accounts is requested from the KYC provider and matched, so on-chain addresses and off-chain identities can only be connected through the decision-making of a decentralized community.

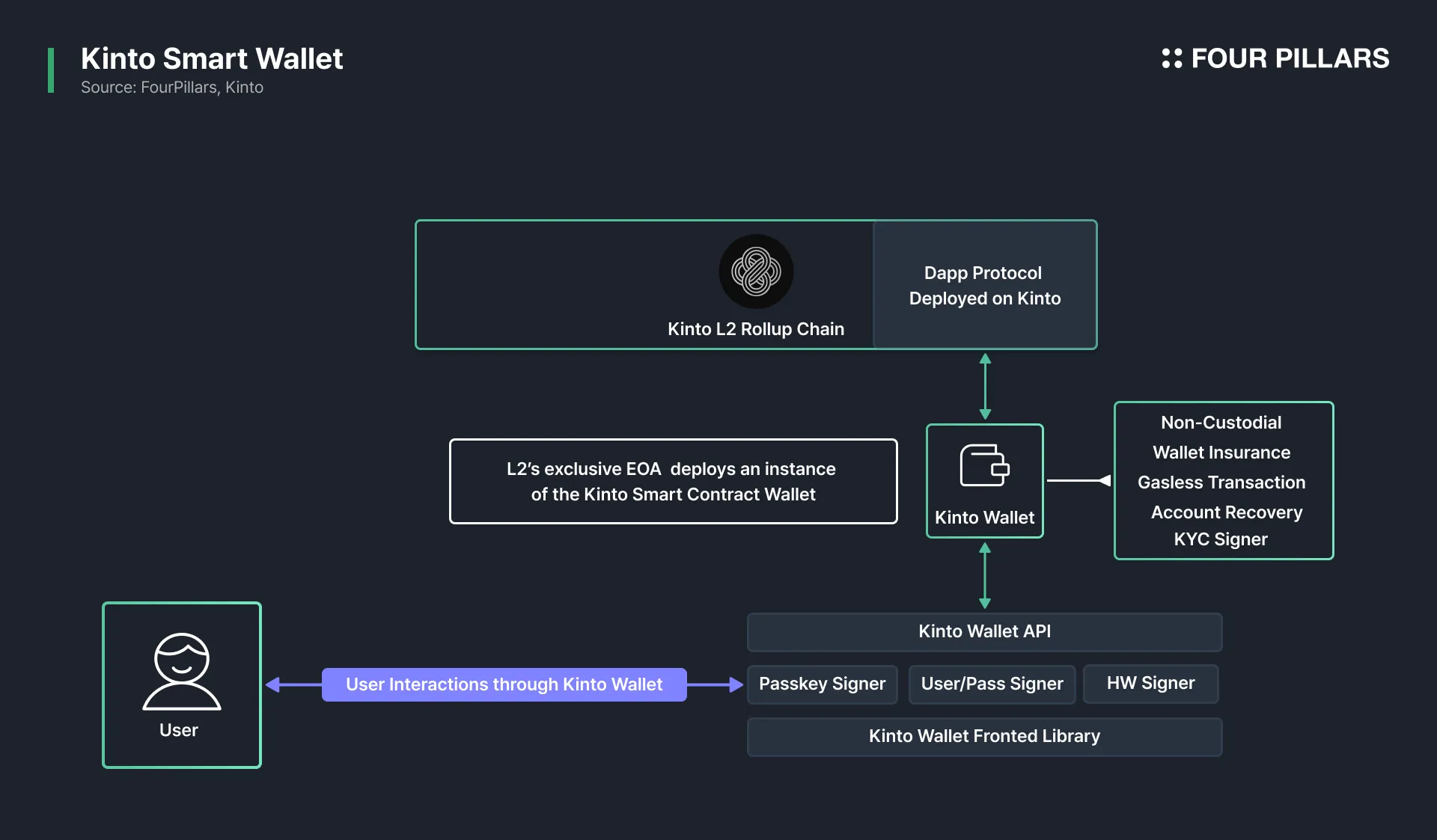

While Kinto secures protection through its embedded KYC architecture, it has also actively adopted account abstraction to provide a simple on-chain experience for users. Kinto adopts its own wallet that smart-contracts all users' on-chain accounts, enabling the application of consistent security policies and allowing basic use of convenient wallet functions.

The Kinto wallet was implemented for two purposes: 1) to seamlessly provide enhanced security by integrating the KYC architecture into the user experience, and 2) to provide a unified user experience with improved accessibility through smart wallet functions.

As explained earlier, trading through external wallets such as Metamask is disabled in Kinto. All transactions can only be executed through the Kinto smart wallet utilizing account abstraction. More precisely, sending transactions directly to Kinto through a regular EOA is not allowed, and transactions are only executed by the Kinto wallet implemented by smart-contracting on-chain accounts that have completed KYC.

Additionally, the Kinto wallet provides various convenience features through the smart wallet. A representative feature for a seamless user experience is the function where dapps pay for the gas fees of user transactions. Dapps place deposits in the Paymaster contract in advance and pay gas with those deposits when users call the dapp's contract. The cost is later recovered through separate service fees or token models to users. Other convenience features provided by the Kinto wallet include:

Wallet Insurance

Kinto's insurance function built into the wallet is a structure difficult to find in other rollups. Kinto users are guaranteed insurance within a certain limit for asset damage due to smart contract hacking.

Partnering with a digital asset insurer called Breach Insurance, this insurance automatically provides all users holding assets worth over $100 in the Kinto wallet with insurance worth $2,500.

Users who have suffered damage from hacking can directly communicate with the insurer to claim insurance, and Kinto supports the role of verifying the user's identity and the fact of damage.

Private Key Social Recovery

In preparation for situations where users lose all signing methods for their wallet, a separate recovery key is set for each Kinto wallet. The recovery key is stored in a custodial form and provides the authority to reset the wallet signer after a one-week delay period when a user loses their wallet.

When the recovery procedure is initiated, the wallet is immediately frozen and a 7-day timer starts, after which the recovery key transfers the wallet ownership to a new passkey, allowing the user to regain the wallet.

Through this mechanism utilizing social recovery and timelock, users can greatly reduce the risk of asset loss due to private key loss.

Deposit Address Restriction

Users can also create app keys, which are dedicated signers for specific applications within the Kinto wallet. For example, they can set up a signing key with limited permissions for commonly used dapps for continual approval, while separating main keys to be used only when moving large assets.

This divides the security area, creating an additional safety measure where even if a key is leaked during the process of using a specific dapp, it cannot access the rest of the wallet's assets.

In addition, Kinto actively adopts convenience features utilizing account abstraction, such as deposit address restrictions to limit the source of funds flowing into the wallet, or multisig and passkey login. This Kinto wallet is designed considering that the mandatory KYC procedure might act as an initial entry barrier for users.

In an on-chain environment where anonymous wallets can be created within minutes, the process of necessarily going through KYC inevitably requires patience from users. However, it can be seen that Kinto intends to offset the initial friction by enabling the use of a trustworthy DeFi environment and convenience features based on the Kinto wallet after overcoming the initial barrier.

When Kinto started building its Layer 2, it declared it would not fragment liquidity. Behind this declaration lies the serious liquidity fragmentation problem in the Ethereum ecosystem. The current environment with liquidity distributed across more than 100 Layer 2s has caused considerable inefficiency for DeFi users. As a result, users face the problem of having to bear additional costs and delay times due to the inevitable use of bridges, or excessive slippage due to insufficient liquidity.

In this situation, Kinto focuses on implementing chain abstraction in an alternative way instead of building its own liquidity and creating another isolated liquidity pool - here, chain abstraction refers to technology that provides multiple blockchain networks as a single integrated platform, enabling users to interact seamlessly on-chain without being aware of differences between networks. To implement chain abstraction, Kinto has newly built Musubi, a cross-chain swap infrastructure, in collaboration with Socket Protocol, which forms the core technical foundation of Kinto's strategic initiative, the modular DEX, which we will examine in the next chapter.

3.3.1 Cross-Chain Swap Infrastructure

Kinto's cross-chain swap infrastructure, Musubi, allows for seamless swapping with assets from various networks such as Ethereum mainnet, Arbitrum, and Base from the Kinto wallet. The method involves comprehensively aggregating DEX liquidity from various chains, allowing users to trade by selecting the most abundant liquidity pool, greatly reducing price slippage and time costs for users.

Whereas previously users had to perform individual swaps through bridges between mainnet and Layer 2 or between Layer 2s, Musubi automatically handles these intermediate procedures. For example, without Musubi, to exchange ETH on Arbitrum for USDC on the Base chain, users would have to perform complex procedures directly such as 1) bridging from Arbitrum to mainnet, 2) swapping on mainnet, 3) bridging from mainnet to Base. In contrast, Musubi simplifies all these processes to something close to a one-click swap. As a result, users can shorten multiple transactions to just one, significantly reducing duplicate gas fees and waiting times.

From a user experience perspective, swaps through Musubi are completed by directly receiving the swap result in the Kinto wallet. This means users can complete transactions with just two signatures without needing to transfer assets outside of Kinto throughout the entire process. Thanks to this, Kinto users can efficiently utilize the entire Ethereum ecosystem like a single integrated liquidity pool.

3.3.2 Musubi Operating Process

Socket's cross-chain liquidity protocol plays a key role in Musubi's operating process. The user journey and asset flow during cross-chain swaps through Musubi are as follows:

When a user enters the assets and quantities to be exchanged in the Kinto dapp and requests a swap, the Socket module calculates the optimal chain and liquidity path. For example, if the Ethereum mainnet has the most abundant liquidity to swap with minimal slippage, the Destination Chain is set as the Ethereum mainnet.

The Kinto backend requests the first signature from the user. This is approval for a transaction to send assets from the user's Kinto wallet to the destination chain. Once the signature is completed, the asset from the Kinto wallet is bridged to Arbitrum, and a temporary contract account exclusively used by that user is deployed on the Arbitrum chain to store the asset.

The relay contract then executes the swap on the designated DEX and bridges the resulting token back to Kinto. At this point, it requests a second signature from the user to execute the transaction. The cross-chain swap is completed when the exchanged token is deposited into the Kinto wallet.

During the process above, while approving the two stages of signatures, the user does not need to intervene except for the two stages they explicitly approve. The user's control over assets is maintained at each stage. The temporary contract account created on another chain in the middle is also required to be signed with keys connected to the user's Kinto wallet for fund movement or swap execution, and Kinto uses solutions like Turnkey to safely assist in managing users' keys for this. As currently implemented, users need to sign twice, but there are plans to improve the procedure to complete swaps with a single signature by simplifying the process through Paymaster, where the Kinto network provides liquidity in advance.

In this way, the reason Kinto focuses on continuously advancing Musubi is to further enhance user accessibility along with security. Even if account abstraction-based Kinto wallets and various convenience features are introduced to lower the learning curve for on-chain infrastructure, cross-chain swaps frequently required for DeFi use still remain the process providing the poorest experience for users. To this end, Kinto aims to provide utility through Musubi, allowing users to save delay time, reduce slippage by up to 2%, and save on repetitive gas fees instead of using bridges directly.

3.4.1 The Premise of Modular DEX: TVL is a Dead Metric

Kinto presents a market approach called modular DEX based on its security-first architecture. Before examining modular DEX in detail, we need to reconsider the TVL (Total Value Locked) metric. Currently, TVL is used as one of the primary indicators for evaluating protocols in the crypto market. The scale of assets deposited in a specific protocol is considered a key parameter indicating user trust or activity level in that protocol.

As a result, the first initiative most new protocols deploy after launch usually culminates in liquidity mining campaigns. Providing incentives to users to secure maximum liquidity and increase TVL is perceived as the most important prerequisite task.

While it's true that this gathered liquidity contributes to bootstrapping the initial ecosystem, the problem lies in the repeated phenomenon where most funds are withdrawn simultaneously right after liquidity mining ends. This implies that TVL is governed by temporary incentives rather than the protocol's actual value or sustainability, and consequently, a reasonable evaluation of a protocol based solely on the TVL metric becomes difficult. As this phenomenon is repeatedly observed, the perception that 'TVL is a Dead Metric' is gradually spreading.

Recognizing the limitations of the conventional approach relying on TVL, Kinto has presented a new approach called modular DEX in the process of finding market fit for its rollup, rather than focusing on artificially raising TVL. Instead of building new DeFi protocols from scratch and going through the process of bootstrapping liquidity, Kinto adopts a strategy of integrating leading, already well-established DeFi protocols with Kinto's modular architecture.

3.4.2 DEX Born from Modularism

Kinto's consistently demonstrated core direction is creating synergy through combination and cooperation rather than building isolated proprietary solutions to compete. Instead of independently building every element from blockchain structure to KYC management and DeFi markets, it consistently implements modularism throughout its entire architecture, aiming for an open ecosystem by sharing and combining specialized modules.

Onramp: Facilitates smooth conversion between fiat and crypto to enable users to easily onboard to the Kinto network. It is designed to allow users to purchase cryptocurrencies directly through bank accounts or debit/credit cards by partnering with Onramper, which aggregates 23 different onramp providers.

Identity Layer: Kinto has a unique security system that mandates KYC and AML at the chain level. It is designed so that all users can participate in the network only after completing identity verification with providers and receiving a Kinto ID. The AML system is integrated with security analysis tools like Chainalysis KYT (Know Your Transaction) to automatically detect and preemptively block suspicious transactions. This provides an identity layer that ensures user data privacy by not connecting on-chain information with users' personally identifiable information, while meeting regulatory compliance requirements.

Smart Wallet: Natively provides smart wallets to all users to solve security vulnerabilities of existing wallets and provide enhanced accessibility. It is a non-custodial smart wallet that provides user-friendly functions such as recovery even if all signing means are lost, built-in insurance services, social login, or gas fee sponsorship.

Layer 2 Rollup: Built a basic rollup execution environment through the Arbitrum Nitro stack. It is a Layer 2 rollup customized to maintain KYC·AML compliance requirements, functioning as the technical foundation of the security-first on-chain financial system implemented on Kinto.

Chain Abstraction Layer: Integrates liquidity from various Layer 1s and Layer 2s through chain abstraction, supporting users to use DeFi services from multiple chains in a single interface. It is designed to provide seamless cross-chain swaps by searching for optimal trades in real-time.

In this way, Kinto presents a new third exchange environment that is not bound by the existing categories of CEX and DEX through a security-first architecture combining various modules. Kinto can provide market opportunities distributed across various networks such as Hyperliquid, Ethereum, and Base through a single interface based on its security features and cross-chain swap infrastructure like Musubi.

This means Kinto can provide users with secure on-chain financial services based on the rich liquidity and user base of leading DeFi protocols like Hyperliquid or Ethena, and conversely, DeFi protocols can outsource Kinto's security-first infrastructure to target a wider range of users including institutional investors.

Source: Musubi — Hyperliquid Perpetuals

Hyperliquid: Hyperliquid is a perpetual futures DEX pursuing an on-chain Binance, which has recorded over $1 trillion in trading volume so far, establishing itself as the first DEX to rival CEX scale. Users can deposit assets into Hyperliquid through the Kinto wallet and use futures trading, and deposits, withdrawals, and fee settlements occurring during trading are safely and easily done through Kinto's integrated interface.

Kinto ICO Platform: Recently, Kinto announced the upcoming launch of a new ICO platform that improves on the problems of the past ICO boom era. This platform is integrated with the Kinto Layer 2 execution environment, allowing users to transparently participate in token sales through wallets with embedded KYC. Since regulatory compliance and Sybil resistance are natively incorporated into the token sale process, participants are protected from gas fee competition or sniping using multiple wallets that were frequent in past ICOs, ultimately enabling fair token sales and balanced distribution.

As the total TVL of the entire DeFi ecosystem approaches $100B and shows a steady upward trend, traditional institutions' inflow is also gradually accelerating, as seen in the case where BlackRock collaborated with Ethena to launch USDtb based on the tokenized fund BUIDL.

However, since DeFi has inherently focused on openness and decentralization, it has a fundamental limitation of not being able to meet the strict regulatory compliance requirements or risk management frameworks of institutional investors. In this context, Kinto's modular on-chain financial system specializing in security and regulatory compliance acts as a unique value proposition for dapps onboarding to the Kinto ecosystem as well as in strategic integration with DeFi protocols already proven in the market, providing mutually complementary growth opportunities for both sides.

Kinto deploys a playbook clearly distinguished from existing rollups with a bold architectural design. From the beginning, it declared it would not fragment the liquidity and did not follow the practice of artificially inflating TVL, a major market indicator, for short-term performance.

Instead, it built an architecture optimized for the goal of a 'security-first Layer 2' by organically integrating KYC mandates, dedicated smart wallets, chain-level insurance, and real-time monitoring systems. It also presents a clear goal of an on-chain financial system that both institutional investors and general users can trust and utilize.

However, bold design for achieving clear goals inevitably entails trade-offs that concentrate resources in specific areas and compromise in others. To this end, Kinto has infused modularism throughout the entire architecture, sharing and efficiently combining modules specialized in each area, rather than building and competing with proprietary solutions. In particular, the strategic approach of the modular DEX creates high synergy with Kinto's security-first design, becoming a new solution to the liquidity fragmentation problem in the Ethereum ecosystem and a differentiated competitive advantage in the process of building a sustainable PMF.

Of course, as Kinto's history is not that long, there are points that need to be improved. Particularly in terms of governance, Kinto's governance committee has more significant authority compared to other networks, such as being able to connect on-chain accounts with KYC information or restrict transactions midway. While such centralization of authority is inevitable to some extent, given the architecture designed with security at its core, it can also be a risk factor. Therefore, case accumulation for security threat situations and process sophistication are inevitably required. Additionally, discussions on controlling governance authority, such as collusion in governance, should continue.

Nevertheless, Kinto is building a new category of on-chain financial system that goes beyond the distinction between traditional DEX and CEX, and is gradually establishing itself as a Layer 2 with a unique position targeting a wide range of potential markets from general users to institutional investors. The KYC and modular DEX strategy they present will be closely watched to see if it can be an innovative alternative to the dilemma faced by the current crypto market, namely the unstable balance between accessibility, security and openness.

Dive into 'Narratives' that will be important in the next year