Stablecoins—digital assets pegged to fiat currencies—have become a central component of the digital asset ecosystem, particularly as instruments for payment and settlement. However, in South Korea, a comprehensive regulatory framework for stablecoins is not yet established. As a result, corporations exploring the issuance or utilization of stablecoins face a host of legal, accounting, and tax uncertainties.

This article aims to identify the institutional challenges that companies may encounter when issuing or using stablecoins in Korea, referencing international cases and developments. It further offers recommendations for developing a legal and regulatory environment that enables broader adoption of stablecoins in corporate settings.

Stablecoins are designed to maintain price stability by pegging their value to legal tender or other stable assets. As of 2024, leading jurisdictions including the United States, the European Union, and Singapore have begun recognizing stablecoins as legitimate means of payment, while concurrently developing regulatory frameworks. However, these frameworks largely focus on the issuer and issuance structure, rather than on downstream use cases.

Global stablecoin transaction volume has surpassed USD 16 trillion, primarily driven by trading, settlement, and remittance functions. Despite this impressive scale, most transactions still involve inter-exchange transfers related to cryptocurrency trading. Therefore, expanding real-world use cases—particularly in B2B settings—is essential for unlocking the full potential of stablecoins.

Major financial players such as Visa and Mastercard are already developing stablecoin-based payment systems. For corporate adoption to scale, it is imperative that merchants and counterparties be able to accept and settle transactions in stablecoins. Nevertheless, existing legal, accounting, tax, and technical barriers significantly hinder corporate participation in the stablecoin ecosystem.

Notably, regulatory momentum is accelerating in the U.S., with President Biden’s executive actions on digital assets and the anticipated policy stance of Trump administration signaling institutional support for stablecoin development. However, stablecoin issuance inherently affects monetary sovereignty and making policy takes long time. Even if a Korean won-pegged stablecoin is issued, it may not compete effectively with U.S. dollar-based stablecoins in international markets. Given these dynamics, Korea should proactively cultivate an environment where corporations can adopt stablecoins safely and predictably. Establishing clear frameworks for accounting and taxation is a foundational step. By aligning with global trends while tailoring regulations to Korea’s financial landscape, the country can not only mitigate risks but also potentially lead international discourse on stablecoin governance. A forward-thinking regulatory framework would enable Korean companies to leverage stablecoins for innovation and create new digital business models.

The legal nature of stablecoins remains ambiguous in many jurisdictions, including South Korea. Domestically, stablecoins are generally categorized as virtual assets not governed under the Act on Electronic Financial Transactions, which limits their legal utility as formal payment instruments. They are also excluded from the definition of securities under the Capital Markets Act, leaving their classification and enforceability in civil disputes uncertain.

This ambiguity poses significant legal risks, especially in cases involving fraud or third-party transfers. For example, if a stablecoin is misappropriated and transferred to a third party, it remains unclear under current Korean civil law whether the third party’s ownership can be protected or invalidated. To address such uncertainties, some jurisdictions are establishing legal foundations that grant stablecoins chattel-like characteristics.

In the United States, a key step was the introduction of UCC Article 12, which governs "Controllable Electronic Records" (CERs). The Uniform Commercial Code (UCC) is the foundational legal framework for commercial transactions in the U.S. Prior to Article 12, digital assets lacked clear legal provisions for ownership transfer, collateralization, or good-faith acquisition. Adopted by 27 states as of 2025, Article 12 defines CERs as electronic records that are controllable by a specific party,Transferable, and uniquely identifiable.Because stablecoins are recorded on a blockchain and access is governed via private keys, they typically meet these criteria. Under Article 12, a good-faith purchaser of a CER may obtain full legal title even if prior ownership was disputed, and ownership can be transferred along with the digital asset. This makes stablecoins eligible for inheritance, collateralization, and other legal uses. However, some concerns remain for stablecoins like USDT, whose redemption rights are not clearly defined under contract law—potentially disqualifying them from CER treatment.

Germany is also moving toward a more comprehensive legal framework for digital assets. Traditionally, under German civil law, ownership rights (Sachenrecht) apply only to physical objects (Sachen). This definition excludes intangible digital assets such as stablecoins. However, legal uncertainty around ownership, bankruptcy protection, and collateralization has prompted Germany to consider expanding proprietary rights to include digital assets.

For example, the German Code of Civil Procedure (ZPO §857) recognizes digital assets as attachable property, which enables creditors to claim such assets during bankruptcy proceedings. Furthermore, recent amendments under the Crypto Markets Supervision Act (KMAG) and the Banking Act (KWG) stipulate that crypto assets held by custodians are deemed client property, requiring their return in insolvency cases. This gives legal clarity and strengthens ownership protections for stablecoins.

To adopt stablecoins as a viable means of transaction in Korea, civil law must evolve to define and protect ownership rights more clearly. This may require amendments to the Civil Act or the enactment of separate statutes governing digital assets. Key considerations include good-faith acquisition, title transfer, escrow arrangements, and the interplay between digital asset rights and traditional contract law.

In addition to the legal safeguards described above, institutional enhancements are needed to facilitate the smooth proof of ownership. Given the nature of blockchain, there is no centralized authority to confirm the ownership of stablecoins. Ownership is determined by control of the associated private key, and therefore companies must implement strong internal controls over private key management. Yet, Korean regulations currently lack guidance on such controls. Lessons from past misuse of bearer bonds and inflated asset values highlight the importance of governance and verification systems.

The direction for corporate account opening and allowing corporations to invest in crypto assets, currently being discussed by domestic regulatory authorities, is based on entrusting verified custodians after acquiring assets from exchanges.These custodians typically store assets in cold wallets, with withdrawals requiring multi-step authentication, creating delays that are incompatible with the practical use of stablecoins.

Given that stablecoins are primarily used for transactions rather than investment, self-custody solutions must be enabled. To facilitate this, Korea must develop internal control guidelines tailored to stablecoin use—detailing wallet management, access controls, audit trails, and asset verification protocols.

Under current International Financial Reporting Standards (IFRS) and Korea’s adoption of IFRS (K-IFRS), there is no explicit guidance on the accounting treatment of stablecoins held by corporations. Stablecoins are generally included under the umbrella of virtual assets and, by extension, treated as intangible assets in line with IFRS Interpretations Committee (IFRIC) guidance. However, in practice, stablecoins often function as cash or cash equivalents, especially when used in transactions, leading to potential discrepancies between accounting treatment and economic reality.

This disconnect may distort corporate liquidity indicators and asset composition, especially when stablecoins are used for payment or revenue collection. Moreover, the lack of clarity around revenue recognition—particularly when goods or services are exchanged for stablecoins—raises questions about when and how to recognize income or expenses.

The U.S. Financial Accounting Standards Board (FASB) is actively reviewing similar issues. In 2024, the FASB issued an exposure draft proposing fair value measurement for crypto assets. Meanwhile, discussions are also emerging in the EU in connection with the implementation of MiCA (Markets in Crypto-Assets Regulation), which may influence future accounting policies.

Given this evolving landscape, Korea must consider amending its standards or issuing interpretative guidelines to define how stablecoins should be classified and reported.

3.2.1 Accounting Treatment for Stablecoin Holders

The FASB has considered whether stablecoins might qualify not as intangible assets but as financial instruments or cash equivalents. In 2023, it initiated discussions on improving crypto asset accounting and, in 2024, published a draft standard proposing a fair value model. However, classification ultimately depends on the nature of the stablecoin—including its redemption structure and underlying risk profile.

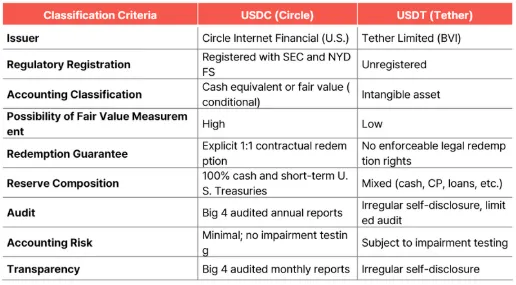

Two commonly used stablecoins, USDC (issued by Circle) and USDT (issued by Tether), are both pegged to the U.S. dollar but differ significantly in transparency and risk. According to both U.S. GAAP and IFRS, cash equivalents must meet the following criteria: short-term maturity (typically within three months), high liquidity (readily convertible to known amounts of cash),insignificant risk of value change, and reliable reserve backing.

USDC generally meets these criteria due to its full backing by cash and short-term U.S. Treasury securities, its 1:1 redemption guarantee, and routine audits by major accounting firms. Although the FASB's Exposure Draft does not explicitly designate USDC as a cash equivalent, it implies that “fully collateralized and redeemable stablecoins” pose lower accounting risk—supporting its treatment as a fair value asset or, in some cases, a cash equivalent under ASC 305.

Conversely, USDT presents classification challenges. Its white paper does not guarantee legal redemption rights, and its reserve assets have historically included riskier instruments such as commercial paper and loans. Additionally, its audit practices lack transparency, and enforcement actions from the SEC and the New York Attorney General have underscored concerns about misleading reserve disclosures. As such, USDT is generally treated as an intangible asset and is not eligible for cash-equivalent classification.

USDC(Circle) VS USDT(Tether): A Comparative Overview

If a stablecoin is classified as an intangible asset, it must be recorded as a non-current asset and subjected to impairment testing, which can negatively affect liquidity ratios and restrict its use as collateral. This accounting treatment can also influence how companies report transactions involving stablecoins.

For instance, when stablecoins are used for employee compensation, a token classified as a cash equivalent would be treated the same as fiat currency. However, if the token is classified as an intangible asset, Korean interpretations of IFRS (e.g., the 2022 KASB clarification on share-based payments) would require it to be treated as a non-cash consideration—recognized at the original acquisition cost, not market value at payment.

As a result, firms must carefully consider accounting classification when formulating stablecoin-related strategies. To facilitate broader adoption, regulators should design stablecoin frameworks that allow qualified tokens to be treated as cash equivalents or, at minimum, as financial assets under accounting rules.

3.2.2 Accounting Treatment for Issuers

If Korean regulations require that only banks or bank-like institutions issue stablecoins, their structure would resemble regulated financial products, such as structured deposits or electronic money. In this case, the issuance proceeds would be recorded as financial liabilities, similar to bond or STO (security token offering) treatment. However, to encourage innovation, Korea should also consider allowing non-financial institutions to issue stablecoins—provided that they meet clearly defined requirements. This would enable commerce platforms or fintech companies to develop niche stablecoin ecosystems suited to their business models.

Currently, most stablecoins in circulation, apart from USDC, would be treated as utility tokens under accounting rules, rather than as financial products. IFRS does not yet provide explicit guidance for utility token issuers, but existing interpretations and Big Four firm analyses suggest that IFRS 15 (Revenue from Contracts with Customers) can be applied. Under this model, cash received upon issuance is recorded as a contractual liability, to be recognized as revenue when performance obligations are fulfilled.

This treatment is consistent with current Korean practices for token issuers, but it also exposes them to delayed revenue recognition and increased accounting complexity. Given this situation, uncomfortable debates regarding the conditions and timing of revenue recognition that domestic token issuers face are likely to persist. There is a high demand for payment tokens in the domestic market, and companies strongly desire to issue payment tokens specialized for their own platforms. However, meeting all the conditions to be recognized as cash-like assets, such as 1:1 redemption guarantees, immediate redemption upon request, and reserve formation, is considered challenging. In a context where the accounting treatment for virtual assets is unclear, just as the Financial Supervisory Service provided "Guidelines for Virtual Asset Accounting," it is essential to offer clear guidelines on related accounting treatments if the issuance of stablecoins is allowed for general businesses, facilitating the activation of the stablecoin ecosystem.

One of the core functions of stablecoins is to facilitate cross-border payments and settlements. However, their usage triggers compliance obligations under foreign exchange laws—particularly in jurisdictions like South Korea where conversion between KRW and foreign currencies requires reporting. If a Korean won-pegged stablecoin is issued and circulated overseas, it may effectively operate beyond the reach of Korea’s monetary controls, raising questions about its legal and accounting treatment.

From an accounting perspective, uncertainty remains regarding whether a stablecoin should be treated as a foreign currency-denominated asset or a domestic one. For example, USD-pegged stablecoins could be considered foreign currency in substance, yet their accounting treatment often depends on classification as a digital asset, not a fiat currency. To address these ambiguities, regulatory guidance is needed that defines how to treat volatility, currency translation, foreign exchange reporting, and FX risk management for stablecoins.

3.3.1 Volatility of Stablecoins

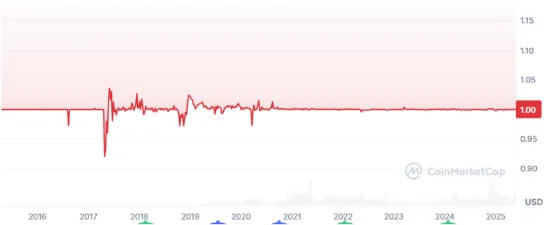

Stablecoins are generally designed to maintain a 1:1 peg to a reference currency, minimizing price volatility. However, short-term deviations can occur due to market conditions, reserve transparency, and liquidity constraints.

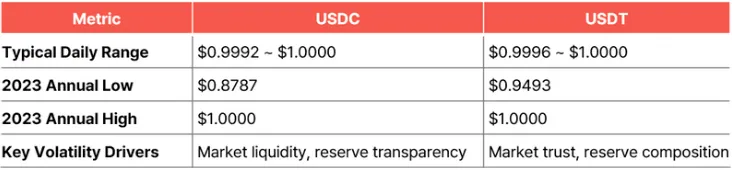

For instance, the daily trading range for USDC and USDT typically fluctuates between $0.9992 and $1.0000, suggesting high short-term stability. Yet, during periods of market stress, peg deviations become more pronounced. In 2023, USDC fell as low as $0.8787 and USDT to $0.9493 on certain exchanges.

USDC Volatility

Source: CoinMarketCap

USDT Volatility

Source: CoinMarketCap

USDC(Circle) VS USDT(Tether) Volatility Comparison

While these fluctuations are usually short-lived, they pose important implications for accounting. The key question is whether companies should recognize stablecoins at nominal value (assuming $1 fixed peg) or fair value, accounting for any deviation.

Under the FASB Exposure Draft (2024), crypto assets—including stablecoins—should be measured at fair value at reporting date, with unrealized gains and losses recognized in earnings. If treated as a cash equivalent, no remeasurement is required; however, if treated as a crypto asset, stablecoins would be subject to either impairment testing or fair value remeasurement depending on classification.

In practice, most corporations assume USD parity and record stablecoins at face value. However, when peg deviations exceed 1%, many firms initiate risk reviews and impairment assessments. If market prices fall below a threshold (e.g., $0.98) at year-end, auditors often recommend fair value adjustments or impairment charges.

A case in point: during the March 2023 Silicon Valley Bank crisis, a portion of USDC’s reserves became temporarily inaccessible, causing the token’s value to drop to $0.8787. Following this event, Coinbase’s auditors reportedly requested a fair value adjustment for USDC holdings.

These examples underscore that stablecoins are not immune to volatility. Corporate holders must therefore build internal policies to evaluate pricing deviations and reflect them appropriately in financial reporting. In Korea, volatility is not only an accounting concern but also a regulatory one. If a Korean won-denominated stablecoin trades on an exchange and exhibits principal risk, it may be classified as a security under the Capital Markets Act. This raises the urgent need to determine whether a stablecoin should be regulated as a payment instrument or a financial investment product.

3.3.2 Foreign Currency Translation

Because stablecoins are pegged to foreign currencies, they are inherently exposed to FX risk. Yet current accounting standards do not offer clear guidance on whether these tokens should be subject to foreign currency translation.

Under both IFRS and U.S. GAAP, stablecoins are not considered legal tender, and therefore do not qualify as “foreign currency” under standards such as ASC 830 or K-IFRS 21. This means USD-pegged stablecoins are not subject to traditional currency translation rules (i.e., they are not remeasured based on spot exchange rates), but are instead treated based on their classification—usually as intangible or fair value assets.

If the FASB Exposure Draft is adopted, stablecoins may be reported at fair value, with gains and losses reflected in earnings. However, this is a market revaluation, not a foreign currency translation.

In practical terms, this can cause a disconnect between economic substance and accounting results. For example, a company holding USD and a USD-pegged stablecoin for payment purposes is exposed to identical economic risks—but may record different accounting outcomes.

Therefore, Korea’s regulatory bodies should provide pre-emptive guidance on how to evaluate and report stablecoins held in corporate accounts. If corporate wallets become legally permissible, stablecoins will likely become the most commonly held digital asset. Providing a unified translation and valuation framework—especially for reporting and audit consistency—is essential.

Tax law typically prioritizes economic substance over form, requiring that taxation be based on the real economic impact of transactions. Stablecoins, with their inherent price stability, are increasingly being used as alternatives to fiat currency for payment purposes. However, most tax regimes still classify stablecoins not as currency but as property, triggering taxable events upon each transaction. This significantly increases the compliance burden and discourages practical use. Additionally, variations in stablecoin structures and redemption mechanisms further complicate tax treatment.

To enable stablecoins to function as legitimate payment instruments, tax systems must offer predictability and clarity. Without explicit rules, users—especially businesses—face legal ambiguity and risk of inconsistent application.

3.4.1 Corporate Income Tax and Individual Income Tax

Currently, most jurisdictions—including the United States, United Kingdom, and Australia—treat stablecoins as property, not currency. This classification means that every use of a stablecoin (e.g., payment or conversion) may trigger a capital gains or ordinary income recognition event.

United States: All digital assets, including stablecoins, are classified as property. When a company sells or uses stablecoins for transactions, any appreciation in value (relative to cost basis) is taxable as either capital gains or business income, depending on the holding context.

United Kingdom: Similar to the U.S., stablecoins are treated as property, not money. Corporate taxpayers may apply either a cost or fair value method, depending on accounting policies. Disposal through sale or payment generates a taxable gain or income.

Australia: The tax treatment of stablecoins depends on the holding purpose. When held as trading stock or used in business activities, gains are subject to corporate income tax.

In Korea, there is no specific tax rule for stablecoins. Under the current framework, virtual assets are taxed based on general principles outlined in the Corporate Tax Act (Article 93-10-ka) and the Income Tax Act (Article 21-1-27). These provisions reference the “Virtual Asset User Protection Act” but do not distinguish stablecoins from other crypto assets.

According to guidance from the Ministry of Strategy and Finance, digital assets are treated as property. Consequently, any exchange, disposal, or use constitutes a taxable event. For stablecoins, this approach creates excessive burdens: taxpayers must calculate and report gains or losses for each transaction—even for simple payments or transfers. Given their use in remittance and settlement, this results in significant tax friction and discourages real-world utility.

To address this, stablecoins used in business should be taxed more like foreign currency transactions. Under the current Korean system, foreign exchange gains or losses are recognized on an annual basis, and only realized amounts are subject to tax. This approach would reduce complexity and better reflect economic substance.

3.4.2 Value-Added Tax (VAT)

In most countries, the provision or exchange of fiat currency is excluded from VAT. Money is not considered a good or service but a medium of exchange. However, due to their linkage to other assets (e.g., fiat, gold), stablecoins are not always treated as currency.

European Union: The European Court of Justice (ECJ) ruled in the Hedqvist case that Bitcoin (and by extension, digital currencies used solely for payment) is exempt from VAT. This principle likely extends to stablecoins when used purely for settlement.

Australia and Singapore: These jurisdictions classify pegged stablecoins as either financial services or derivatives, and exempt them from VAT—but impose reporting obligations. This allows tax authorities to monitor transaction flows, amounts, and user profiles. These governments chose VAT exemption—not non-taxability—to prevent misuse of stablecoins for VAT arbitrage. For example, if a stablecoin were pegged to gold and used for transactions, it could potentially circumvent gold VAT rules.

In Korea, the Value-Added Tax Act does not directly address virtual asset or stablecoin transactions. Historical interpretations have evolved:

In 2016, the National Tax Service (NTS) ruled that Bitcoin used as money is not subject to VAT, but when traded as an asset, it is taxable. In 2021, the Ministry of Strategy and Finance reversed this view, stating that virtual assets do not qualify as "goods" under the VAT Act, and thus their provision is not taxable.

To ensure clarity and consistency, Korea needs to formally define whether stablecoin-linked transactions are subject to VAT, and if so, under what conditions. This will require revisions to existing law or interpretive guidance, particularly for business-to-business transactions or merchant payments involving stablecoins.

In 2023, the OECD introduced the Crypto-Asset Reporting Framework (CARF) to enable the automatic exchange of information related to crypto asset transactions across jurisdictions. CARF extends the scope of the existing Common Reporting Standard (CRS)—originally designed for traditional financial assets—to encompass digital assets. Under CARF, virtual asset service providers (VASPs) are required to report user transaction data to their respective tax authorities, which are then shared with foreign counterparts to ensure tax compliance.

As stablecoins are increasingly used for payments and settlements, such transactions may fall within CARF's reporting scope in the future. However, CARF imposes obligations only on VASPs, not on individuals or businesses transacting directly via P2P networks or self-custodied wallets. This creates a reporting blind spot—especially for corporate entities conducting cross-border transactions without intermediaries.

This vulnerability has been acknowledged by both the OECD and the Financial Action Task Force (FATF). Without appropriate controls, stablecoins could facilitate unmonitored capital outflows, AML/KYC evasion, and trade data distortions.

There are various types of cross-border transactions that CARF cannot capture. When a general company uses a DeFi wallet or P2P to transfer stablecoins, the transactions are not reported since they do not go through a VASP. Furthermore, if a foreign company's Korean subsidiary transfers funds to its parent company using stablecoins, it may be classified as an internal transaction requiring a report on capital transactions, which could be overlooked. Additionally, the difficulty in identifying the actual owner in corporate remittances could lead to AML and KYC blind spots, potentially distorting balance of payments and trade statistics.

To close the reporting gaps created by CARF’s limited scope, several policy options can be considered:

Expand VASP Obligations:

Korea could broaden the definition of VASPs to include certain stablecoin users or impose limited reporting obligations on corporations. For example, transfers above a defined threshold (e.g., KRW 50 million per transaction or KRW 100 million annually) could require mandatory reporting via a registered VASP.

Mandatory Reporting under Foreign Exchange Act or Electronic Financial Transactions Act:Introduce a crypto transfer declaration system for cross-border stablecoin flows, requiring notification or approval when amounts exceed specific limits. This would align with existing capital movement rules.

Enhanced Financial Reporting Disclosures: Revise Korea’s corporate accounting standards (K-IFRS) to mandate footnote disclosures for digital asset transfers abroad. Corporations could be required to report cross-border stablecoin activity either through tax adjustments or financial statement annotations. KASB has already amended K-IFRS 1001 to establish disclosure rules for crypto holdings.

Technology-Driven Monitoring (Smart Reporting): Encourage stablecoin issuers like Circle or Tether to integrate API-based metadata tagging and geographic identifiers into DeFi modules. This would allow automated reporting of transaction information, including user profiles and jurisdictions.

Regulatory safeguards are essential to mitigate systemic risks posed by digital assets. However, overly burdensome controls could stifle innovation and adoption. Korean policymakers must carefully balance compliance requirements with the need to support responsible use of stablecoins in cross-border commerce.

3.6.1 Blockchain-Integrated ERP Systems

To support stablecoin adoption in the corporate sector, enterprise systems such as ERPs must evolve to accommodate blockchain-based transactions. In traditional banking environments, corporate ERP systems are tightly integrated with firm banking APIs, enabling seamless B2B payments, fund transfers, and collections. Vendor details are typically stored in master databases, allowing automated transactions and real-time reconciliation. Payment approvals are linked with electronic workflows embedded in the ERP. For stablecoins to be operationally viable at a similar level, blockchain-native ERP solutions must be developed. These systems should include: Multi-party computation (MPC) or custody wallets,APIs connected to exchanges or custodians (VASPs), Address mapping engines to match recipient wallet addresses,On-chain transaction logging for audit trails, KRW conversion logic for accounting, Internal key management and access logs.

Without these capabilities, stablecoin-based payments will remain isolated from core finance systems, reducing scalability and compliance readiness.

3.6.2 External Audit and Assurance

Stablecoins present various challenges in financial audits, such as a lack of accounting standards, the inherent uncertainty regarding the substance of assets due to the unique characteristics of virtual assets, and the importance of control testing. In particular, it is difficult to test for existence and sole ownership, as described in section 3.1, during an audit, and there are challenges in key audit areas such as valuation, measurement, and appropriateness of disclosures. Therefore, there is a need for institutional enhancements, including clarifying and standardizing accounting and disclosure standards for holding and using stablecoins, establishing standardized internal control procedures, and developing auditing standards

Stablecoins offer promising solutions for efficient corporate treasury management, cross-border payments, and broader digital transformation in the global economy. However, in Korea, the current regulatory, accounting, and tax frameworks lack the clarity and infrastructure needed to support widespread adoption by businesses.

As this report has outlined, companies face substantial uncertainty in areas such as civil ownership rights, accounting classification, volatility risk, foreign exchange treatment, tax obligations, and international reporting (CARF). Without legal recognition and administrative guidance, firms cannot confidently issue, hold, or use stablecoins for business purposes.

To unlock the benefits of stablecoins while minimizing systemic risk, Korean regulators must establish a holistic and forward-looking framework.

Dive into 'Narratives' that will be important in the next year