1.1.1 Project Han River: Bank of Korea's wCBDC and Deposit Token Experiment

The Bank of Korea (BOK) established a digital currency research team in 2020 and initiated simulations from 2021 to assess the technical feasibility and viability of a central bank digital currency (CBDC). Initially, these experiments were based on a retail CBDC structure. Phase 1 focused on verifying basic functionalities such as issuance, circulation, and redemption, while Phase 2 concentrated on technical completeness for smart contracts, offline payments, and digital asset linkage. The experimental process primarily aimed to examine core elements of digital currency, including wallet functionality, transaction tracking, and double-spending prevention.

Subsequently, considering changes in global settlement systems and linkages with domestic financial infrastructure, the BOK shifted its experimental focus to wholesale CBDC (wCBDC). Accordingly, in 2023, it launched 'Project Han River' in collaboration with the Financial Services Commission (FSC), Financial Supervisory Service (FSS), and BIS Innovation Hub Asia. This project experiments with a structure where the Bank of Korea issues wCBDC, commercial banks receive it, issue deposit tokens based on it, and general consumers use these tokens for payments in real life.

Project Han River: Bank of Korea Digital Currency Test Promotional Materials

Source: The Bank of Korea

The experiment is being conducted for approximately three months, from April to June 2025, with direct participation from up to 100,000 citizens. Participants can receive deposit tokens through the apps of major commercial banks, including Shinhan Bank, Hana Bank, Woori Bank, NH Nonghyup Bank, Industrial Bank of Korea (IBK), and Kookmin Bank. These tokens can be used for payments at offline merchants like 7-Eleven, EDIYA COFFEE, and Kyobo Book Centre, as well as on online platforms such as Hyundai Home Shopping, Danggyeo-yo, and Modhaus. The experiment also verifies usability and policy applicability through various scenarios, including remittances, voucher receipts, and post-settlement.

This experiment is regarded as a policy attempt to concretize the use of digital KRW within the institutional framework, extending beyond mere technical verification and aiming to link with private payment networks, consumer touchpoints, and settlement infrastructure. In a 2023 survey, the BIS classified Korea as a country that has entered the CBDC application experimentation phase, and the Bank of Korea is also participating in international collaborative research, such as the BIS Project Agora. Project Han River is the first domestic case to simulate how digital KRW would be used in real-life commercial environments. It can serve as a crucial policy reference for designing future digital settlement infrastructure, expanding private application models, and establishing institutional linkage strategies.

1.1.2 Technical and Institutional Limitations of Korean CBDC

The Korean CBDC experiment is simulating real-life payments using deposit tokens based on wCBDC. While significant in examining how digital KRW can operate within the institutional financial infrastructure, there are several technical and institutional limitations in its structural aspects.

Firstly, the network infrastructure is composed of a permissioned private blockchain, meaning only a limited number of entities, such as participating banks, have node access rights. This design did not consider technical interoperability with public blockchain-based digital asset ecosystems or smart contract-based systems, making it difficult to ensure interoperability with global digital currency networks. Consequently, the possibility of combining with decentralized application services or Web3 technologies is inherently limited.

The issuing entity of deposit tokens is commercial banks, and all token issuance, balance management, and remittances for users are processed within the banks' own systems. Users are designed to receive and use deposit tokens directly through bank apps without needing a separate wallet, providing a user experience similar to existing account-based simple payment services. However, this structure is far from an open design, as custody, collateral management, and settlement functions are all dependent on the banks' internal operations.

From the perspective of institutional interpretation and regulatory alignment, clear standards are still lacking. If deposit tokens are interpreted as a digital representation of existing deposits, the Depositor Protection Act may apply. Depending on various legal classifications, such as electronic money, digital payment instruments, or securities under the Capital Markets Act, the applicable laws and supervisory framework would differ. In particular, issues such as the applicability of depositor protection, the possibility of interest payments, compliance with reserve requirements, and accounting classification criteria for assets could become key issues in future institutionalization discussions.

The most fundamental limitation is the structural exclusion of private technology entities and various payment service providers. The issuance and circulation of deposit tokens are exclusively carried out by the banking sector, and non-bank fintech companies, Web3 wallet providers, and global stablecoin payment networks are not included in the experimental structure. This demonstrates that while the digital currency distribution infrastructure has been digitized, the openness of the ecosystem and technological innovation have not been sufficiently considered.

In summary, the current CBDC experimental structure focuses on verifying institutional feasibility as a digital settlement instrument. However, challenges such as network closedness, lack of user scalability, unclear regulatory alignment, and structural exclusion of private participation are identified as issues that must be addressed in future institutional design processes.

1.1.3 Technical and Institutional Limitations of Korean CBDC

The Bank of Korea's wCBDC and deposit token experiment is a policy attempt to implement digital settlement instruments within the institutional financial network. It holds significant meaning as a comprehensive experiment that includes various application scenarios beyond mere technical verification. Project Han River, in fact, deepened the scope of the policy experiment by incorporating consumer touchpoints such as remittances, voucher payments, and real-life payments.

However, the current experimental structure is based on a closed network centered around existing financial institutions, with limited participating entities and circulation scope. The issuance and use of deposit tokens are primarily conducted within bank apps and affiliated merchants, and open circulation or linkage with the private technology ecosystem has not been considered. While this is partly due to the initial experimental design conditions, policy consideration is needed as similar limitations could recur during future institutionalization.

Such structural constraints are common challenges faced by major countries overseas. The European Union is pursuing the MiCA (Markets in Crypto-Assets) regulation for stablecoins in parallel with digital euro development, while Japan has established a legal framework that permits the issuance of trust-based private stablecoins, separate from its digital yen development. Singapore has also prepared a clear regulatory framework for single-currency stablecoins (SCS) based on the parallel operation of wholesale CBDC and private stablecoins.

As such, major countries are approaching digital currency policy not by converging into a single form, but by adopting a parallel structure where public and private sectors share roles. Central banks focus on wholesale settlement networks that are easier to control, while the private sector handles technology-based distribution networks and consumer payment touchpoints. This approach aims to balance the speed of technological development with policy control and ensure the scalability of the entire digital currency ecosystem.

Korea also needs such a parallel structure design. While the current wCBDC experiment sufficiently demonstrates technical alignment and operational feasibility as a settlement infrastructure, structural limitations exist in extending it to the distribution and payment domains. Especially in areas where consumer utilization is concentrated, a separate structure that ensures private sector participation and technological flexibility is necessary. While wCBDC should be maintained as a wholesale settlement network, a parallel structure where private sector-led stablecoins function as a means of circulation and payment should be considered.

In summary, the current wCBDC experiment provides important policy implications. However, for the substantial expansion of digital KRW's practical use, a dual-structure design where settlement and distribution functions operate in parallel is essential. This is considered the most realistic policy direction for flexibly responding to technological changes and private demand.

1.2.1 Overview and Background of Discussion

Policy discussions on KRW stablecoins began to pick up pace in mid-2024. Prior to this, the focus of digital currency discussions was mainly on Central Bank Digital Currencies (CBDC). However, recently, arguments for separately institutionalizing KRW stablecoins have rapidly spread, primarily within political circles and industries. Notably, ahead of the 2025 presidential election, as major parties and candidates reviewed related pledges, interest in technical feasibility and policy design direction increased.

Against this backdrop, the 'bank-centric issuance model' is gaining attention as a scenario with high institutional acceptance. This model involves commercial banks issuing stablecoins collateralized by customer deposits and circulating them using their existing payment infrastructure. Since both issuance and settlement occur within the bank's internal system, it offers high alignment with existing financial infrastructure and consumer protection frameworks, and is considered a viable alternative due to its relatively high acceptance by regulatory authorities.

Similar structures are emerging overseas. A representative example is JPM Coin by JP Morgan Chase, where institutional clients deposit funds with the bank, and an equivalent amount of digital tokens are issued and traded only on Onyx, JP Morgan's private blockchain. Issuance, circulation, and redemption are all conducted in a closed manner within the bank's internal system, with general user access restricted. SG-Forge's EURCV in France was designed to comply with the EU's MiCA regulation, authorized by the French financial authorities (ACPR), and is used for limited purposes as an institutional euro-backed stablecoin.

Thus, the bank-centric issuance model holds significance as a policy experiment to build a digital asset distribution mechanism within the institutional financial system. This is because it can function as a structure that gradually responds to the digital financial environment while minimizing institutional risks. However, a more detailed analysis of the technical structure and institutional issues associated with this model will be presented in the next section.

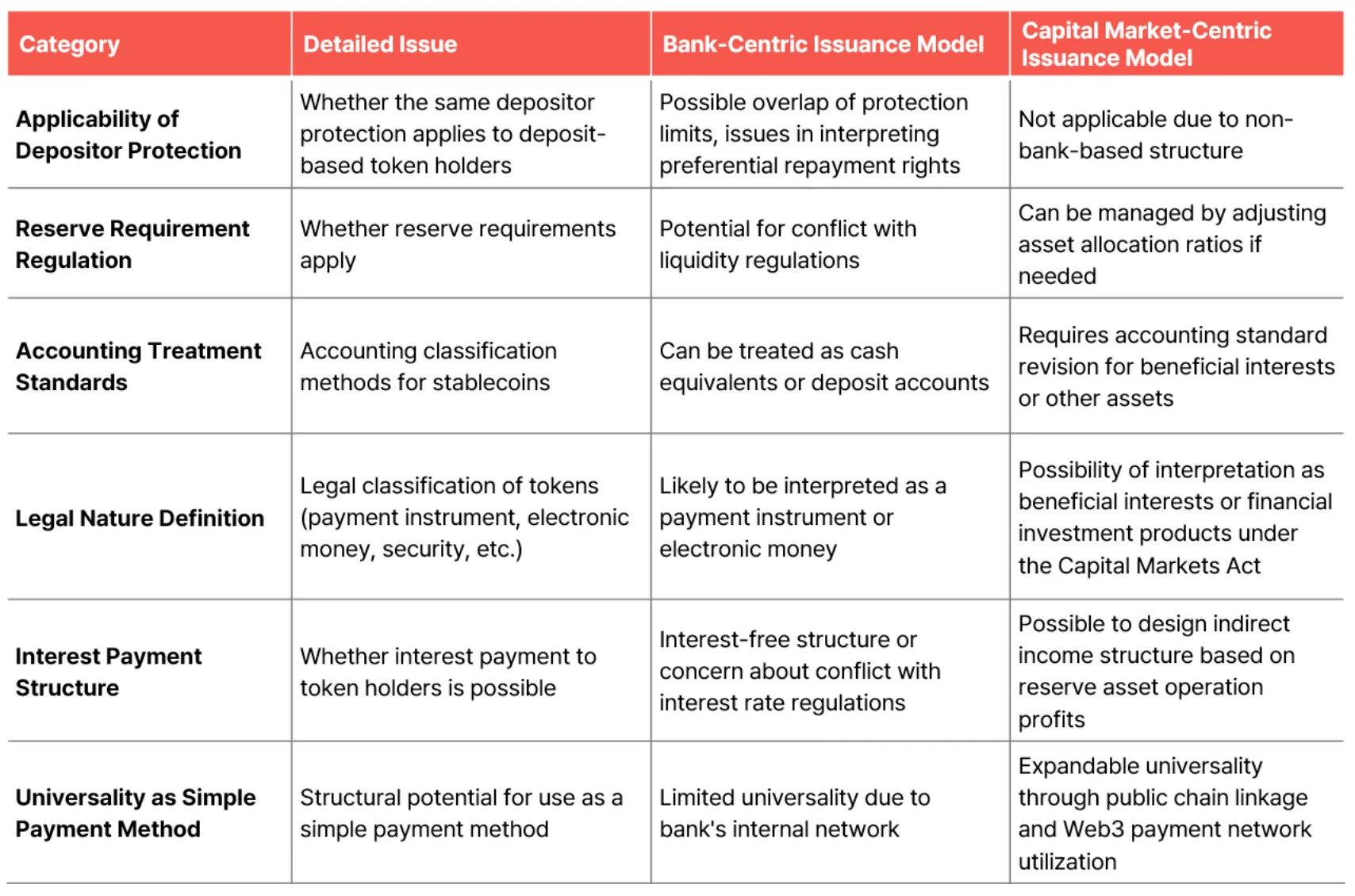

1.2.2 Legal Issues and Institutional Alignment

The bank-centric issuance model has high policy acceptance due to its ability to implement KRW stablecoins within the existing financial system. However, the actual institutionalization process involves several regulatory and legal issues. In particular, the unique structure of deposit-based digital tokens can lead to conflicts with existing financial laws, accounting standards, and consumer protection frameworks, requiring a precise alignment review.

Firstly, the applicability of depositor protection is a key issue. If stablecoins are considered digital representations of deposits, the question arises whether token holders are also covered by depositor protection. In this case, the issuance volume of stablecoins could overlap with the total bank deposits, potentially leading to legal inconsistencies in interpreting protection limits or preferential repayment rights.

Next is the relationship with reserve requirements and liquidity regulations. In a structure where stablecoins are issued against deposits, if these tokens are subject to reserve requirements, this could impose restrictions on fund operations and burdens related to maintaining liquidity ratios. Conversely, if stablecoins are classified as electronic money or securities, regulations other than the Banking Act would apply, fundamentally altering the issuing entity and supervisory framework.

Furthermore, accounting treatment standards and interest payment structures are also important considerations. If stablecoins are circulated as digital assets, it is unclear whether they can be accounted for as cash equivalents or if they should be classified as separate asset items. Moreover, if no interest is paid, consumer incentives may be weakened. If interest is paid, it could raise issues of competition with existing deposits and alignment with interest rate regulations.

The universality as a simple payment method could also be limited. The bank-centric model is likely to have its distribution confined to the bank's own payment network or affiliated networks, which may not satisfy the universality requirement for classification as a simple payment instrument under the Electronic Financial Transaction Act. Compared to simple payment services with similar functions, stablecoins may find it difficult to gain competitiveness.

Lastly, the legal nature of stablecoins itself is unclear. The applicable laws differ depending on whether deposit-based tokens fall under the legal categories of payment instruments, electronic money, or securities. Especially if smart contract-based functions are incorporated, the legal classification of the asset can become even more complex, potentially affecting investor protection measures or disclosure and reporting obligations.

In summary, while the bank-centric issuance model offers the policy advantage of establishing a digital distribution instrument within the institutional framework, its practical institutionalization requires multi-layered legal and institutional reforms, including depositor protection, liquidity regulation, accounting standards, and the definition of its legal nature. Without such a legal foundation, the model's scalability and effectiveness may be limited due to structural constraints.

1.2.3 Structural Limitations and Constraints on Private Diffusion

The bank-centric issuance model, being designed based on existing financial infrastructure, enjoys high policy acceptance. However, it possesses inherent limitations in terms of market scalability and technological openness. Particularly, if this model is adopted as the primary form of digital KRW implementation, the following constraining factors could simultaneously appear.

Firstly, limitations in technical scalability and practical usability. The bank-centric model is built around a permissioned private network, where issuance, circulation, and redemption all occur within the bank's internal system. Interoperability with public blockchains or smart contract-based on-chain ecosystems is structurally difficult. As a result, its competitiveness is limited in terms of digital asset linkage, automation functions, and global scalability. From a user's perspective, it is unclear how it differentiates from existing simple payment systems, making it difficult to encourage voluntary adoption.

Secondly, the fundamental exclusion of private technology providers and Web3-based companies. Since banks monopolize the entire process of issuance, settlement, and distribution, there is almost no room for collaboration with fintech companies, blockchain infrastructure providers, or Web3 wallet providers. This hinders ecosystem diversity and technological innovation, and in the long term, carries the risk of the entire digital asset ecosystem becoming entrenched in a closed structure centered around specific financial institutions.

Thirdly, it is difficult to achieve mass adoption. As seen in global stablecoin cases, key requirements for widespread circulation are openness, universality, and interoperability. However, the bank-centric model often has limited use cases and insufficient reward or incentive designs for consumers. Consequently, while a certain level of usage may be secured through policy initiatives in the initial distribution phase, natural user base expansion will be difficult in the long run, and it will be challenging to secure market competitiveness.

Fourthly, if policy discussions focus solely on the bank-centric structure, the overall direction of the ecosystem could become rigidly closed. In a trend where digital assets are circulated in a global public environment and combined with decentralized ecosystems, a bank-only model struggles to adapt to technological changes. Particularly, if alignment with international asset transactions, cross-border payments, and global on-chain interoperability is poor, the competitiveness of Korea's digital currency infrastructure itself could be weakened.

In summary, while the bank-centric issuance model can secure short-term policy acceptance through the digitization of institutional infrastructure, it inherently contains fundamental limitations in terms of key values of digital currency, such as technical openness, private participation potential, and mass adoption structure. To complement these structural limitations, a parallel design with a capital market-centric issuance model, premised on an open ecosystem based on private technology, is unavoidable.

1.3.1 Overview and Background of Discussion

While the bank-centric issuance model is considered a realistic alternative in terms of institutional acceptance and technical implementation, it has structural limitations regarding distribution scalability and technological openness. Accordingly, the capital market-centric issuance model is gaining attention as an alternative that responds to changes in the domestic and international digital asset policy environment and reflects the trend of digital transformation centered on capital markets.

This model is based on a role-separated structure where non-deposit-taking financial institutions such as trust companies, securities firms, and asset management companies store reserve assets or participate as issuing entities, and blockchain technology providers offer distribution infrastructure. Since the issuance function and technical infrastructure are separated, open designs such as public blockchains, smart contracts, and Web3 interfaces are possible, and private participation based on domestic licensing systems can be more flexibly configured.

Similar structures are rapidly being institutionalized overseas. In the United States, PayPal's issued PYUSD relies on Paxos for asset custody and management, with token issuance implemented using an Ethereum-based ERC-20 structure. This separated structure of issuance, custody, and technical operation offers advantages such as risk diversification, increased regulatory acceptance, and the inducement of participation from various private entities in the market.

Japan, through the amendment of its Payment Services Act in 2023, allowed trust companies and electronic payment service providers to hold stablecoin reserve assets, and separate entities to issue tokens. This structure is regarded as a policy experiment designed to expand the role of private financial institutions while simultaneously avoiding debates about stablecoins being classified as securities.

In Korea, too, there is increasing demand for a digital distribution structure involving asset management companies, securities firms, custody providers, and blockchain technology companies. Especially with the expansion of asset-linked digital products such as security tokens (STO), digital MMFs, and real asset-backed tokens, the need for KRW-based stablecoin infrastructure for settlement, clearing, and distribution has been raised.

Above all, the capital market-centric issuance model aligns with the structure of stablecoins already practically used in global commerce and platform payments. Designed to enhance usability as an everyday payment method and function as infrastructure for real-asset transactions based on digital assets, this model is considered the most effective alternative in terms of both institutional alignment and technological scalability.

1.3.2 Legal Issues and Institutional Alignment

The capital market-centric issuance model, where private financial institutions manage reserve assets and stablecoins are issued and circulated on public blockchains, involves different legal issues and institutional alignments compared to the existing bank-based model. In particular, the separation of issuing entities and asset custodians, collateral structures based on financial investment products, and the use of decentralized distribution infrastructure are areas where existing financial regulatory frameworks need to be redefined.

Firstly, legal grounds for the operation and custody structure of reserve assets need to be established. In capital market-type stablecoins, the structure often involves asset management companies, securities firms, and trust companies operating deposited funds in short-term government bonds, MMFs, etc., and issuing corresponding stablecoins. In this case, since the underlying assets are not simply cash deposits but income-generating assets, there is a possibility that such stablecoins could be interpreted as beneficial interests or other financial investment products under the Capital Markets Act. This implies that the issuing entity must be an institution licensed for financial investment business, and capital market regulations such as investor protection requirements and operational reporting obligations could apply.

Secondly, a supervisory system for the separation of issuing entities and custodians is required. For instance, similar to the cases of USDC and PYUSD in the US, it is common to have a structure with a division of labor where reserve assets are held by banks or trust companies, and issuance is performed by a separate technology provider or affiliated legal entity. If Korea were to adopt a similar structure, a supervisory system would be needed to determine whether the issuer requires registration as an electronic financial business operator or payment service provider, and whether the custodian meets the trust regulations for beneficial interests under the Capital Markets Act. Additionally, regulatory alignment for intermediaries involved in the distribution infrastructure, such as custody, wallets, and order books, must also be reviewed.

Thirdly, the acceptability of a public blockchain-based distribution structure is institutionally unclear. Capital market-type stablecoins are inherently issued and circulated on decentralized networks, and users directly perform transfers, payments, and settlements through their own wallets. In this case, compliance with various regulatory elements is necessary, including KYC/AML requirements, transaction traceability, and the ability to control smart contracts. In particular, clear standards are required regarding whether all transactions occurring on a public chain are subject to regulation, or if supervision is limited to the scope controllable by the issuing entity.

Fourthly, establishing criteria for judging the legal nature of stablecoins is essential. If the reserve assets consist of real financial assets such as government bonds and MMFs, and the income generated from these assets indirectly accrues to users, this could be regarded as a structure similar to beneficial interests or collective investment schemes under the Capital Markets Act. Consequently, the application of relevant regulations, such as disclosure obligations, subscription requirements, prospectus submission, and investor protection measures, could be unavoidable.

However, these issues are not merely regulatory barriers but can also function as opportunities for market acceptance and institutional experimentation. The US, Japan, and Singapore, for instance, are simultaneously establishing the institutionalization of capital market-type stablecoins as a premise, along with guidelines for the separation of issuing and custodial entities, registration as electronic money or financial investment products, and technical guidelines for public chain utilization. Korea also needs to progressively build a stablecoin-specific regulatory framework that comprehensively considers the Capital Markets Act, the Electronic Financial Transaction Act, and the Act on Reporting and Using Specified Financial Transaction Information. Especially, since regulatory uncertainty can hinder technological development, an approach that encourages diverse private issuance experiments through pilot projects and regulatory sandboxes would be effective.

In summary, the capital market-centric issuance model structurally presupposes the cross-application of various laws. Detailed institutional design regarding reserve asset management structures, issuer-custodian separation systems, and public chain utilization scope must precede. In particular, clarifying whether stablecoins constitute beneficial interests and establishing a system for role division among supervisory authorities are key elements to simultaneously secure policy effectiveness and private acceptance. If Korea aims to realize private-sector stablecoins within the institutional framework, clear classification standards centered on the Capital Markets Act and flexible institutional operating policies must be adopted in parallel.

Accordingly, the capital market-centric issuance model and the bank-centric issuance model show structural differences in key institutional design items, and the applicable legal interpretations, accounting standards, and distribution structures also vary depending on each model. The following table compares the key issues between the two models:

Key Issues: Bank-Centric vs. Capital Market-Centric Stablecoin Issuance Models

1.3.3 Scalability and Policy Significance

The capital market-centric issuance model, with its structure allowing various private entities to share roles based on public blockchain, is evaluated as an alternative that can simultaneously ensure technical scalability and policy flexibility. Particularly, given that most major global stablecoins adopt a similar structure, Korea should benchmark this approach.

Firstly, it offers high scalability in terms of technical openness and interoperability. Stablecoins based on public chains like Ethereum, Solana, and Avalanche are easily linkable with the global digital asset ecosystem. They can also design various functions through smart contracts, such as automated settlement, conditional payments, and reward linkages. This provides a foundation for simultaneously ensuring settlement efficiency and programmable functions.

Secondly, it enables collaboration between private technology companies and institutional financial institutions. Asset management companies, securities firms, and trust companies can handle collateral management and custody functions. Blockchain technology providers and custodians can operate issuance infrastructure and user wallets, dividing responsibilities. A structure like Circle's USDC, where banks and trust institutions hold reserve assets while technology companies handle issuance and operations on public chains, prevents single-operator monopolies and contributes to ecosystem stability and transparency.

Thirdly, it allows for a parallel division of roles between public and private sectors. While wCBDC is designed for the central bank to control the settlement network, stablecoins can function as private-led distribution and payment instruments. The European Union, Japan, and Singapore are institutionalizing such parallel structures, and Korea should also consider policy design reflecting this.

Fourthly, it has significant economic effectiveness and potential for user base expansion. Capital market-type stablecoins can be used as a consumer payment method linked to points and rewards, beyond just remittances and settlements. Especially in commerce and platform-based services, they can simultaneously improve settlement efficiency and user experience, leading to anticipated voluntary diffusion.

Finally, it can be a means to secure the global competitiveness of the Korean digital asset ecosystem. Global stablecoins like USDC and PYUSD already operate as universal payment instruments linked to cross-chain infrastructure, global custody, and decentralized exchanges. If Korea institutionalizes capital market-type stablecoins and links them to the global digital financial network, the international scalability and usability of KRW-based digital assets could significantly increase in the future.

In summary, the capital market-centric issuance model is a realistic alternative with balanced scalability and effectiveness across technological, policy, and industrial aspects. As a design that can be pursued in parallel with wCBDC, it can be an important pillar of Korea's digital KRW strategy, requiring prioritized institutionalization and pilot experiments.

2.1.1 Consortium Formation of Issuing Entities: Financial Institutions and Technology Providers

The issuance structure of capital market-type KRW stablecoins is premised on a consortium model where financial institutions and technology providers divide functions. This design overcomes the limitations of closedness and scalability inherent in a bank-only issuance structure and simultaneously secures regulatory acceptance and technical flexibility. This consortium would include asset management companies, securities firms, banks, trust companies, custodians, accounting firms, and fintech and blockchain technology companies, each participating based on their licenses and specialized capabilities.

Each entity would divide functions as follows:

Asset management companies would manage highly liquid KRW assets, such as short-term government bonds and MMFs, serving as the actual collateral assets for stablecoins.

Securities firms provide the trading infrastructure necessary for purchasing government bonds and MMFs and support practical execution, such as opening operating accounts and settlement.

Banks or trust companies hold collateral assets in dedicated accounts, ensuring legal separation and stability through a trust account-based custody structure.

Fintech and blockchain technology companies provide technical infrastructure, including building issuance systems, designing smart contracts, automating on-chain triggers, and linking with external payment networks via APIs.

Custodians hold and control administrator keys and emergency stop triggers for smart contracts, ensuring security and neutrality.

Accounting firms issue Proof of Reserve (PoR) reports verifying the alignment between reserve assets and circulating supply.

This functional division structure can maximize synergy, especially when combined with a financial group-level promotion strategy. For instance, Shinhan Financial Group, KB Financial Group, Hana Financial Group, and Woori Financial Group possess multiple affiliates, including banks, securities firms, asset management companies, and credit card companies, allowing for the internal formation of a functionally separated consortium. If big tech-based payment service providers like Kakao Pay, Naver Pay, and Toss participate, they can implement a strategy of issuing branded stablecoins at the group level and circulating them across online and offline channels. This structure not only facilitates technical implementation but also enables diverse applications such as group-specific marketing strategies, user reward programs, and the integration of proprietary payment networks, thereby serving as a practical incentive mechanism to encourage the voluntary adoption of stablecoins.

In summary, the issuance of capital market-type KRW stablecoins should be designed as a collaborative structure involving specialized entities by function, rather than a single operator. When combined with financial group-level promotion and the participation of private technology companies, it can become a realistic model that satisfies institutional acceptance, technical scalability, and user-friendliness.

2.1.2. Collateral Asset Management Structure and Issuance System Design

The core of the capital market-centric KRW stablecoin design lies in ensuring the safety and liquidity of collateral assets and maintaining real-time consistency with the on-chain issuance system. Collateral assets are not merely deposit targets but real assets that back the redeemability of issued stablecoins, while the on-chain system technologically verifies and links them.

Reserve assets typically consist of highly stable KRW assets such as short-term government bonds, Money Market Funds (MMFs), and demand deposits. Short-term government bonds, primarily those with maturities of less than one year, have low credit risk and price volatility. MMFs offer the advantages of daily redemption, liquidity, and diversified investment. Demand deposits, as bank-issued deposit assets, have high immediate cash convertibility and function as cash reserves for large-scale redemption requests.

In the global case of Circle (USDC), approximately 90% of its total reserve assets consist of short-term government bonds and MMFs, with the remaining approximately 10% in cash equivalents. KRW stablecoins could also refer to this, structuring 80-90% in short-term government bonds and MMFs, and 10-20% in demand deposit form. This asset composition is managed in real-time through a linkage structure among asset management companies, securities firms, and fintech companies. The asset management company establishes the overall portfolio composition and strategy, while the securities firm executes management directives as a trading window for purchasing government bonds and MMFs. Management strategies are adjusted according to liquidity coverage, deposit ratios, and risk diversification standards, and this must be maintained in constant synchronization with the issuance system.

The issuance system is designed as a smart contract-based on-chain structure. User KRW deposits or redemption requests automatically trigger issuance or burning, and the smart contract performs functions such as verifying settlement details, managing issuance limits, and checking collateral status. This system is linked with backend accounting systems, external payment networks, and user wallets, ensuring that the total collateral assets and the total circulating stablecoins always maintain a 1:1 ratio. Smart contracts are designed to allow issuance only when pre-set conditions (e.g., sufficient reserve assets, liquidity standards, AML/KYC verification) are met, and upon redemption requests, automatic burning is linked with asset liquidation. This structure acts as a safeguard to prevent risks such as over-issuance, accounting discrepancies, and liquidity crises.

In summary, the collateral asset management and issuance system of capital market-type KRW stablecoins should be structured through a real-time linkage between financial institutions and technology providers. While referencing global standards, it needs to be adjusted to suit Korea's institutional and accounting environment. This will simultaneously satisfy three core objectives: redemption guarantee, accounting transparency, and policy responsiveness.

2.1.3 Licensing System and Regulatory Applicability

For the institutionalization of capital market-type KRW stablecoins, it is essential to first clearly define the licensing framework under which each participating entity will operate. Since there is currently no stablecoin-specific licensing system in Korea, different regulations may apply based on existing laws such as the Electronic Financial Transaction Act, the Act on Reporting and Using Specified Financial Transaction Information (Virtual Asset Service Provider reporting system), and the Capital Markets Act, depending on the structure. Therefore, each consortium member must jointly review their legal status and regulatory applicability by role from the initial design stage.

The stablecoin issuance structure can technologically choose both public blockchain or private blockchain bases. For example, if tokens are issued through a public blockchain in a publicly accessible manner, allowing general users to directly purchase or redeem them, the issuing entity is highly likely to be subject to Virtual Asset Service Provider (VASP) registration under the Act on Reporting and Using Specified Financial Transaction Information. Particularly, if free transfer between wallets is possible via smart contracts and the issuing entity performs actual circulation management, it may be deemed to bear circulation responsibility.

Conversely, for institutional demonstration purposes, registration as an electronic financial business or utilization of innovative financial service special exemptions is possible. If certain requirements are met, such as 100% collateral deposit, no interest payment, and redemption guarantee, it can be interpreted as a payment-type electronic payment instrument or a prepaid electronic payment instrument, allowing for licensing under the Electronic Financial Transaction Act or designation as a regulatory sandbox. In fact, the Bank of Korea's deposit token experiment is also being pursued through the innovative financial services sandbox, and similar application could be considered for private stablecoins.

The licensing system by entity is summarized as follows:

Asset management companies: Can manage reserve assets through licenses under the Capital Markets Act.

Banks and trust companies: Can custody collateral assets based on the Trust Act and Banking Act.

Securities firms: Function as real trading windows for purchasing government bonds and MMFs and for settlement.

Custodians and technology providers: VASP registration under the Act on Reporting and Using Specified Financial Transaction Information is a key issue.

Accounting firms: Perform PoR report preparation and verify collateral-issuance alignment.

Especially, if the issuance system operator or custodian holds control rights over smart contracts (e.g., issuance/burning triggers, administrator keys, circulation control rights), that entity may be considered the de facto issuer. In such cases, it may need to satisfy electronic financial business licensing or VASP registration requirements. Therefore, it is advisable for the issuing consortium to design a structure that distributes authority by function and clearly distinguishes responsible entities based on licensed institutions.

In summary, the institutionalization of capital market-type KRW stablecoins cannot adopt a single licensing approach. Instead, it will inevitably be designed as a complex structure where functional regulations apply in parallel. Therefore, from the initial consortium design stage, it is necessary to analyze which licensing system can be applied based on the technical structure and service scope. A system that allocates responsibilities and roles to each entity based on licensed institutions must be established. This is a key condition for simultaneously securing institutional acceptance and market viability.

2.2.1 Collateral Asset Custody and Payment Guarantee Role

In the structure of capital market-type KRW stablecoins, the practical custody of collateral assets and the assurance of payment stability are core functions and fundamental to institutional design. This is not merely a question of where to deposit assets, but rather structurally clarifying who holds the legal ownership of the assets and which entity bears payment responsibility at the time of redemption.

Collateral assets are generally managed by asset management companies and consist of KRW-based highly stable assets such as government bonds, MMFs, and demand deposits. These assets are legally transferred to a trust account or a separate deposit account of a bank or trust company during the actual custody phase. This structure is clearly separated from the asset management company's proprietary assets or the securities firm's accounts used as trading channels. It is managed as an independent account for stablecoin holders.

Such a custody structure is similar to the legal and accounting standards used in existing MMFs and bond funds. The principles of asset segregation, fiduciary duty, and trustee liability under the Trust Act or Banking Act apply. In particular, trust accounts are independently protected regardless of the bankruptcy of the issuance system operator or custodian. This provides an institutional foundation in three aspects: accounting asset segregation, clear legal ownership, and user protection.

Similar principles apply in global cases. Circle distributes USDC's reserve assets across multiple third-party institutions like BNY Mellon and BlackRock MMFs, maintaining an accounting system separate from its own assets. Tether also holds assets in the form of government bonds and deposits across multiple bank accounts, verifying the alignment between circulating supply and custodial balances through a real-time PoR (Proof of Reserve) system. Korean KRW stablecoins can also adopt this structure, with custodial assets managed as low-risk KRW assets conforming to domestic financial institution standards.

Meanwhile, considering the possibility of the custodian playing a structural payment guarantee role under certain conditions, beyond simple safekeeping, is also an option. For example, if a bank holds some reserves and conditionally responds to redemption requests using them, this effectively performs a partial payment guarantee function. However, such a structure requires a prior review of alignment with the Banking Act's depositor protection framework, payment guarantee limits, and credit risk avoidance mechanisms, making it difficult to introduce without clear institutional grounds.

In summary, the collateral asset custody structure for capital market-type KRW stablecoins must satisfy the following three elements:

In summary, the collateral asset custody structure for capital market-type KRW stablecoins must satisfy the following three elements:

Legal protection framework: Explicitly state legal ownership and user protection based on the Trust Act or Banking Act.

Assurance of redemption stability: Verify the accounting transparency and payment capacity of the custody structure.

This structure can simultaneously secure asset accounting transparency and user trust. During the institutionalization process, legal standards must also be established, including specifying trust accounts, setting the scope of trustee responsibility, and reviewing payment guarantee potential.

2.2.2 Key Management, Smart Contract Security, and PoR Audit

To ensure the reliability and technical stability of capital market-type KRW stablecoins, key management, smart contract security, and a PoR (Proof of Reserve) based audit system, which are core infrastructures of the issuance system, must be organically designed. Particularly in a consortium structure where multiple private entities collaborate, avoiding centralized authority and separating functional responsibilities and controls is a prerequisite for institutionalization.

(1) Private Key Management: The Starting Point of Security and Control

Administrator keys for stablecoin issuance contracts, smart contract modification rights, and emergency stop triggers are prime targets for hacking, insider threats, and operational errors, thus making a robust security system essential. Global projects secure their keys by utilizing Hardware Security Modules (HSM), Multi-Party Computation (MPC), multi-signature (Multisig), or by entrusting key custody to specialized custodians like Fireblocks or Anchorage. These methods are directly applicable in the Korean context. Especially, appointing a separate custodian to entrust key custody and smart contract access rights, and forming a joint control structure with the technology provider, is the most realistic approach. This helps prevent abuse of authority and system malfunctions, and establishes a rapid response system in case of security incidents.

(2) Smart Contract Security: Functional Control and Risk Response

Smart contracts are not merely code but also a means of policy execution. Major global stablecoins embed functions like blacklists, conditional transfer restrictions, and emergency stop capabilities to allow for immediate action in response to abnormal transactions or law enforcement requests. Capital market-type KRW stablecoins also need to embed issuance limits, issuance/burning triggers, and AML/KYC verification conditions within the contract. Operational authority should be managed in a distributed manner between the custodian and the technology provider. Dual-signature structures or conditional approval methods can simultaneously secure operational transparency and legal responsiveness.

(3) PoR Audit System: Ensuring Accounting Transparency and User Trust

The core of stablecoins is the alignment between collateral assets and circulating supply. To verify this, a Proof of Reserve (PoR) system must be essentially introduced, and real-time linkage between the technical system and the accounting system must be possible. In global cases, Circle operates a real-time dashboard in addition to monthly accounting firm reports. Tether also periodically discloses its reserve asset composition. Domestic stablecoins also need to establish a PoR reporting system through accounting firms in a similar manner and transparently disclose circulating supply and reserve asset details via a blockchain dashboard. Furthermore, the PoR system must go beyond simple audit reporting to meet structural requirements for standardizing reports based on accounting standards, real-time disclosure in case of risk situations, and ensuring the independence of the auditing entity. In this process, the establishment of stablecoin audit standards should also be pursued in consultation with the Korea Accounting Standards Board, financial authorities, and other relevant entities.

In summary, the core operating infrastructure for capital market-type KRW stablecoins must fulfill the following three functions:

Security assurance: Entrusting and distributing key management functions and implementing technical safeguards (HSM, MPC, etc.).

Operational control: Policy execution and crisis response system based on smart contract functions.

Accounting transparency: Standardization of PoR-based real-time audits and disclosure systems.

These elements serve as the foundation not only for technical safety but also for policy acceptance and user trust, and are crucial starting points for functional separation within the consortium and third-party verification systems.

2.2.3 Accounting and Disclosure Infrastructure and Industry Expansion Opportunities

For capital market-type KRW stablecoins to be institutionalized, the establishment of accounting treatment standards for reserve assets, the construction of a PoR (Proof of Reserve) audit system, and the design of real-time disclosure infrastructure must be pursued in parallel. This accounting and disclosure infrastructure goes beyond simply ensuring transparency and can lead to the advancement of related industries and the creation of demand for new specialized services.

(1) Establishing Accounting Standards: Clarifying Legal Ownership and Attributing Entities

For reserve assets operated by asset management companies and custodied by banks or trust companies, it must be clearly defined who holds legal ownership and to which entity they are attributed for accounting purposes. This goes beyond mere asset segregation and is a core element that determines the standards for investor protection, financial statement disclosure, and reporting to supervisory authorities. To achieve this, a separate account system for stablecoin holders, explicit provisions on the scope of the custodian's responsibility, and accounting treatment standards agreed upon with the Korea Accounting Standards Board are required. In particular, aspects such as changes in the value of reserve assets, criteria for redemption timing, and reflection of liquidity ratios also need to be regulated.

(2) PoR-based Audit System: Regular Verification and Reporting

The trustworthiness of stablecoins stems from a system where an independent third party regularly verifies that circulating tokens and reserve assets consistently maintain a 1:1 correspondence. To this end, accounting firms must receive asset details and issuance volume data from the issuing entity and publish monthly PoR reports based on the accounting standards. This process can be advanced beyond simple external auditing to include real-time linkage of accounting information, periodic sampling reviews, and the introduction of automated monitoring systems. Such audit demand provides new business opportunities not only for accounting firms but also for data analytics companies, RegTech solution providers, and back-office system operators.

(3) On-chain Disclosure Infrastructure: Building User Trust

While reserve assets exist off-chain, the circulating supply can be tracked in real-time on the blockchain. This makes the establishment of an on-chain disclosure system a core foundation for stablecoin institutionalization. A representative example, Circle (USDC), constantly discloses collateral composition, circulating supply, and issuance details via a dashboard, designed to even track cross-chain transfer status. Domestic stablecoins also need to secure user trust by building a blockchain-based dashboard, linking it with monthly PoR reports, and implementing an immediate notification system for abnormal transactions. Such systems can serve as technical entry opportunities for Web3-specific SaaS companies, blockchain data analytics companies, and financial security companies.

In summary, the accounting and disclosure infrastructure must satisfy the following three functions:

Establishing accounting standards: Creating accounting standards that clearly define asset attributing entities and custodial responsibilities.

Building an audit system: Implementing a PoR-based regular audit and third-party verification system by accounting firms.

Designing a disclosure system: Ensuring real-time transparency by integrating blockchain and off-chain data.

This will serve as the foundation for stablecoin institutionalization and allow the accounting, auditing, and blockchain infrastructure industries to grow together.

2.3.1 Asset Linkage Structure and On-chain Distribution Strategy

To expand the distribution of capital market-type KRW stablecoins, it is necessary to design an asset linkage structure and build on-chain distribution infrastructure in a way that complements the structural limitations of the current KRW (Korean Won) markets on domestic virtual asset exchanges. In particular, KRW markets operate as closed systems based on exchange accounts, making it structurally impossible to directly transfer KRW externally or freely utilize it on-chain.

For example, if a user wants to transfer KRW from their virtual asset exchange account to an external wallet, they cannot directly transfer KRW. They must first purchase dollar stablecoins (e.g., USDT, USDC) or other virtual assets and then withdraw them. However, until now, the domestic KRW market has been a closed account-based structure within exchanges, so there was no structural 'demand itself' for transferring KRW to external wallets. Without linkage to on-chain global payments or asset management, there was no market reason to use KRW on the blockchain.

However, the situation can change when capital market-type digital asset infrastructure fully materializes. If a structure where asset management-based financial products like tokenized MMFs and short-term government bonds are circulated on the blockchain is realized, users will need a means of transfer to directly store, utilize, and exchange KRW-based assets in external wallets. This is not merely a matter of technological innovation but can be interpreted as a turning point that opens up entirely new distribution and settlement structures that have not existed before.

KRW stablecoins are an on-chain based extension that can realize such structural changes. Upon issuance, they comply with existing financial regulatory requirements through bank account linkage. After circulation, they can be freely transferred, stored, and used for payments on public blockchains. They are particularly suitable for designing automated settlement structures with tokenized capital market products and can function as a core element of capital market-type digital asset infrastructure.

Furthermore, the introduction of KRW stablecoins can provide an opportunity to incorporate a payment method based on institutional infrastructure into the distribution structure, unlike non-institutional virtual assets handled by existing virtual asset exchanges. If financial authorities design the issuance and distribution channels of stablecoins within a controllable scope, a more regulated distribution structure can be established in terms of user protection and AML/KYC.

Ensuring cross-chain distribution alignment is also important. As seen in Circle's Cross-Chain Transfer Protocol (CCTP) case, mechanisms that maintain asset alignment across chains serve as a core foundation for on-chain auditing, accounting transparency, and risk control. KRW stablecoins can also secure cross-chain settlement consistency and policy responsiveness through such structures.

In summary, capital market-type KRW stablecoins, rather than completely replacing existing virtual asset exchange KRW markets, can function as a practical alternative that complements their limitations and enables external distribution and global utilization as 'on-chain KRW'. By balancing challenges of fund mobility, international interoperability, and technological scalability, it can be evaluated as an infrastructure that satisfies both policy effectiveness and market demand.

2.3.2. Distribution Structure Design and VASP Registration Review

The distribution structure of capital market-type KRW stablecoins has no precedent for institutionalization or commercialization yet. However, by referencing major global stablecoin designs, a public blockchain-based distribution infrastructure is highly likely to be the core axis. In this case, it includes direct user-to-user transfers and smart contract-based settlement functions, and depending on the role of each functional operating entity, a Virtual Asset Service Provider (VASP) registration obligation under the "Act on Reporting and Using Specified Financial Transaction Information" may arise. Therefore, the distribution method and functional separation must be carefully considered at the initial design stage.

Under current law, anyone performing virtual asset-related activities such as trading, exchanging, custody, or brokerage must register as a VASP with the FIU, and in practice, most VASPs operate as single-function specialized entities. This is similar to traditional financial systems that presuppose industry separation, where exchanges, custody, and brokerage are handled by different entities.

Considering this structural context, a clear division of roles by function is also desirable for the design of KRW stablecoin distribution. For example:

Issuance functions can secure an institutional foundation through electronic financial business registration or innovative financial service special exemptions.

Distribution functions may be subject to VASP registration.

Custody functions are ideally handled through an asset custody structure via banks or trust companies.

Particularly, an entity that technologically operates and manages user stablecoin transfers on a public blockchain, smart contract-based automated settlement functions, etc., is highly likely to be considered a de facto distribution responsible entity and thus subject to VASP registration. For example, a platform that provides decentralized wallet interfaces or has technical control over distribution channels may be subject to registration requirements depending on its control authority.

Overseas examples also show a similar direction. The EU's MiCA and Japan's Payment Services Act generally permit public blockchain distribution but apply differentiated licensing frameworks based on functional separation and clarified roles between issuers and distributors. Domestic institutional design also needs to adopt a similar approach.

In summary, the distribution structure of capital market-type KRW stablecoins should be designed on a public blockchain to ensure scalability and flexibility. However, VASP registration may vary depending on the location of technical operational authority, the scope of distribution function control, and the user interface structure. Therefore, by clearly establishing the principle of functional separation from the initial design stage and designing a structure that can satisfy the licensing requirements for each function, both policy acceptance and business sustainability can be secured.

2.3.3. Domestic and International Distribution Ecosystem and Collaboration Opportunities

For the distribution infrastructure of capital market-type KRW stablecoins to function effectively, strategic linkage with domestic and international digital asset ecosystems is essential. While previous discussions on distribution primarily focused on issuance and redemption structures, this section focuses on collaboration strategies to ensure widespread adoption and usability in the actual use phase.

Firstly, from a domestic perspective, virtual asset exchanges are currently the only platforms capable of KRW-based trading, but most operate on a closed account-based structure within the exchanges. To convert KRW stablecoins into a form that can be circulated on-chain, the following technical and institutional redesigns are required:

On-chain transfer system linkable with public blockchains.

Stablecoin-based order book structure and trading API.

AML/KYC linkage, accounting information integration, and other settlement and regulatory compliance infrastructure.

Especially, to link stablecoin distribution organically with an exchange's trading system, settlement system, and user authentication system, rather than just listing, deep technical collaboration and institutional alignment review must be pursued in parallel.

Meanwhile, a brand-centric issuance strategy at the financial group level can be a practical catalyst for expanding distribution channels. For example, if a specific financial group issues stablecoins and links them with its credit card company, fintech affiliates, payment service providers, etc., for use across online and offline distribution channels, it can form a self-contained distribution ecosystem within a single brand. Such a structure not only secures an initial diffusion base but also acts as a reliable asset for long-term expansion of external affiliation networks. Competition between stablecoins of different brands can stimulate user incentives and drive innovation in the distribution ecosystem. Especially when combined with customer rewards, membership benefits, and payment mileage, it can become an important distribution strategy that broadens consumer choice.

In terms of international cooperation, linkage with decentralized exchanges (DEX), Web3 payment infrastructure, and cross-chain bridges is key. Circle's USDC is circulated on various chains like Ethereum, Solana, and Avalanche, and it employs Cross-Chain Transfer Protocol (CCTP) to ensure asset alignment across chains. KRW stablecoins also need to consider multi-chain compatibility and cross-chain settlement consistency in the future. A likely practical collaboration structure for this is a tripartite cooperation model among financial institutions, technology providers, and global partners. Financial institutions handle asset custody and regulatory compliance (AML/KYC), technology providers build on-chain issuance and distribution management infrastructure, and global partners support securing distribution channels and payment linkages.

This collaborative structure can lead to the following phased expansion strategy:

Phase 1: Secure initial distribution through domestic exchange listings.

Phase 2: Linkage with Web3 wallets and on-chain payment systems.

Phase 3: Integration with global DEXs, bridges, and overseas payment platforms.

For such expansion, a technical and policy framework, including API standardization, regulatory alignment, and chain selection strategy, must be established from the initial design stage.

In summary, the distribution structure of capital market-type KRW stablecoins should be designed based on connectivity with domestic and international digital ecosystems. If combined with financial group-centric brand strategies and global distribution partnerships, it can simultaneously secure practical market expansion and institutional acceptance.

2.4 Payment: Structure, Regulatory Issues, and Beneficiary Industries

2.4.1 PG/VAN Linkage and Real-World Payment Expansion Strategy

For capital market-type KRW stablecoins to function as a practical payment method in the real economy, linkage with existing domestic payment infrastructure, namely PG (Payment Gateway) and VAN (Value Added Network) systems, is essential. Unlike overseas, Korea adopts a card-centric tripartite payment structure, where PG companies mediate transaction approvals and settlements between merchants and card companies online, and VAN companies do so offline. Card companies are responsible for final payment approval and fund settlement, and there is no separate acquirer.

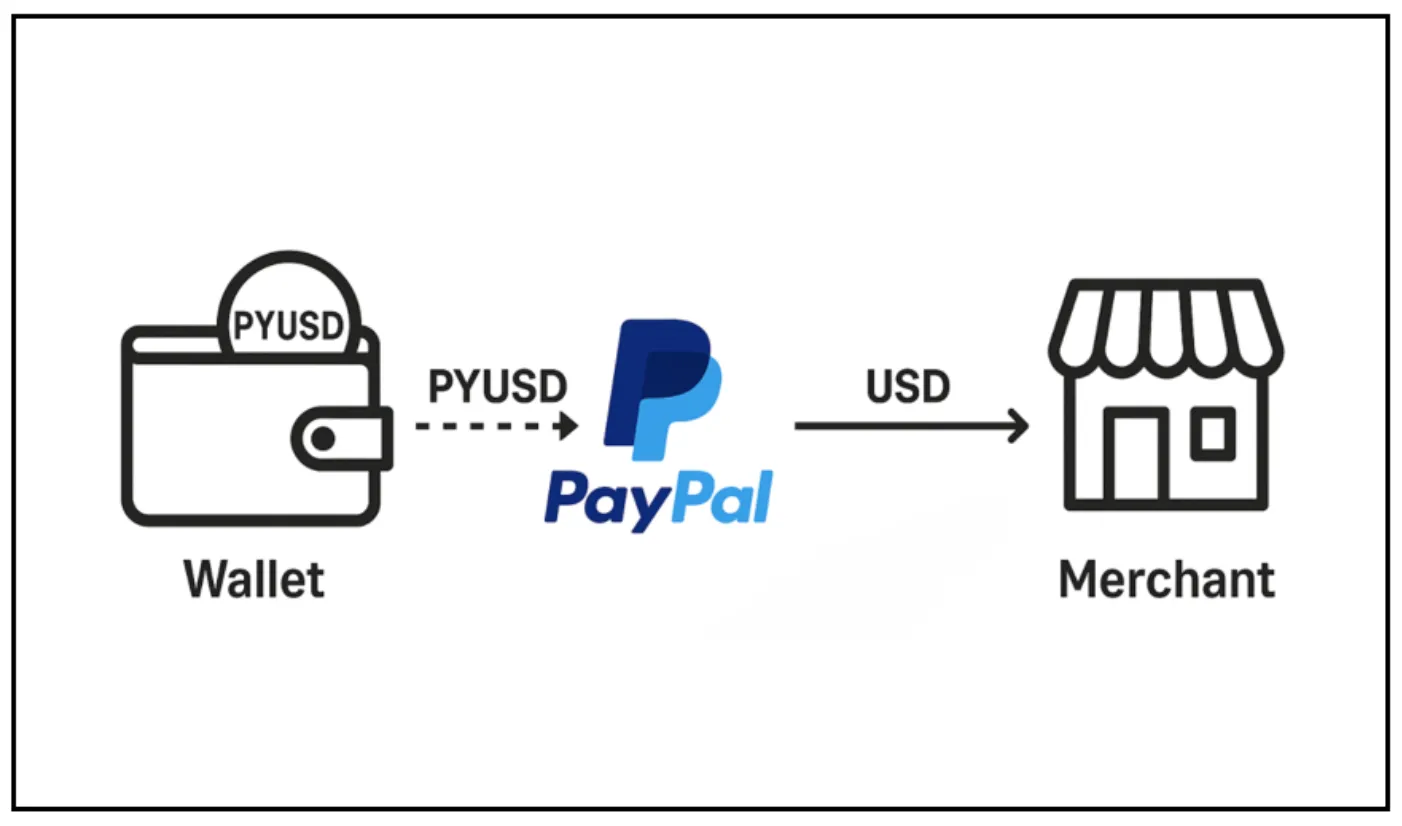

In this structure, for KRW stablecoins to be used as a payment method, a technical interface between blockchain-based transactions and the existing card payment network is required. However, most PG/VAN companies' technical infrastructures are optimized for the Web2 environment, making direct blockchain linkage difficult. Therefore, a realistic alternative is for fintech companies or electronic financial business operators to participate as intermediate technical intermediaries.

For example, when a user requests payment from a wallet holding stablecoins, the intermediary fintech operator verifies the transaction on the blockchain and transmits it to the PG or card company. Payment approval follows the existing card company process, but settlement is processed in a separate account based on stablecoins. During this process, AML/KYC, transaction tracking, and abnormal transaction detection functions can be automatically performed by smart contracts and backend systems.

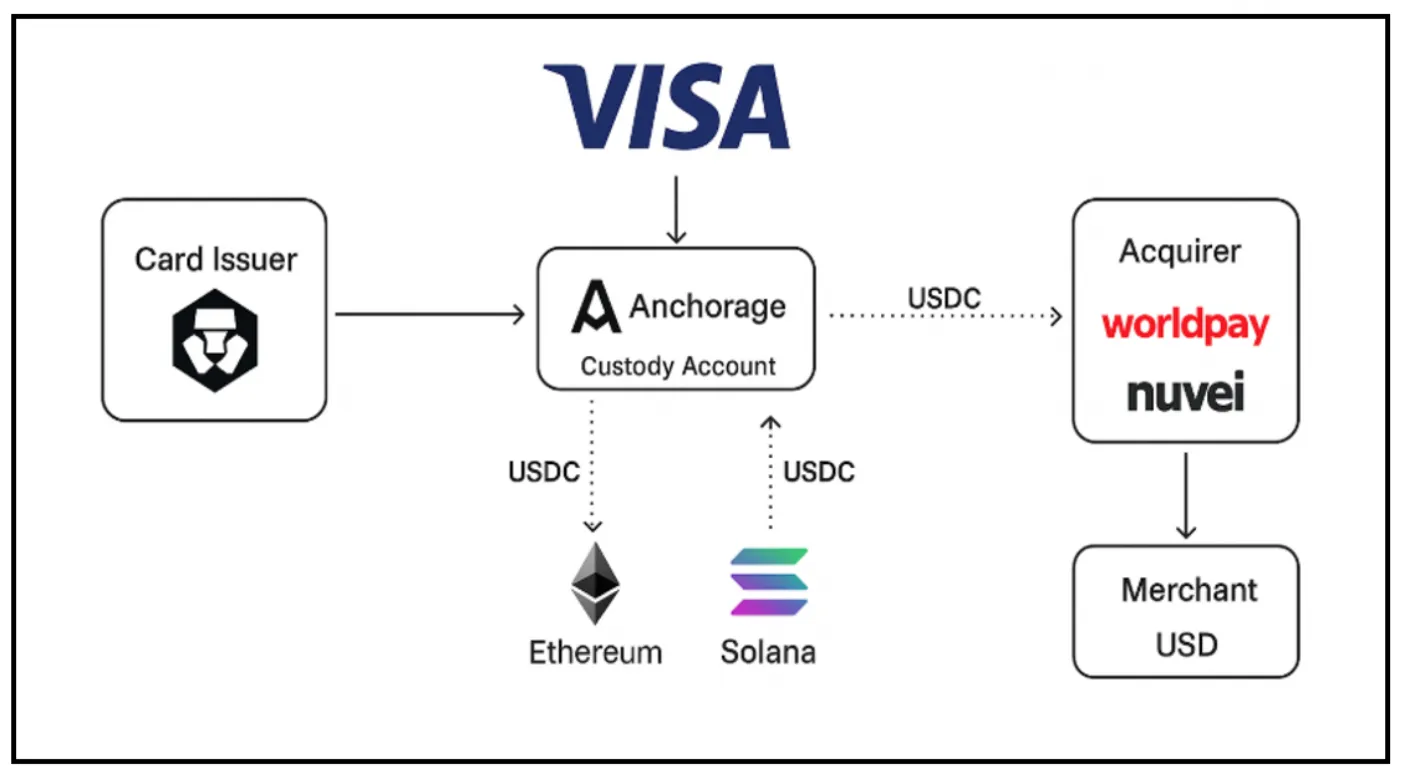

Similar structures are emerging in global cases. Visa is collaborating with Circle to integrate USDC-based payment settlement systems into its card network, while Checkout.com is experimenting with linking stablecoin payments to PSP systems through Fireblocks infrastructure. These are all considered hybrid settlement models that combine blockchain-based flexibility with existing payment networks.

To implement such linkage models in Korea, the following conditions must be met:

API linkage system between PG/VAN companies and intermediary fintechs.

Ensuring alignment between on-chain approval information and payment results.

Real-name verification, transaction monitoring, emergency stop functions, and other supervisory authority requirements must be reflected.

Securing fund flow stability through dedicated card company accounts or settlement channels.

Through such a structure, blockchain transactions can be integrated into the real economy's payment flows, and stablecoins can be used across various channels, including credit card payments, mobile payments, and QR-based payments. Especially, if cooperation with PG and card companies is achieved, it can serve as a decisive catalyst for initial merchant acquisition and distribution expansion.

In summary, for capital market-type KRW stablecoins to become a practical payment method, technical linkage with existing card-based payment infrastructure is essential, and the role of electronic financial business operators or fintech companies to mediate this is important. A hybrid payment model that combines the stability of Korea's tripartite payment structure with the flexibility of blockchain can be a starting point for substantially expanding the real-world usability of stablecoins.

2.4.2 Cross-border Remittance and Global Expansion Potential

To expand the policy utility of capital market-type KRW stablecoins, securing a linkage structure with global payment and remittance infrastructure, beyond simple domestic distribution, is a key challenge. In particular, the characteristics of blockchain-based stablecoins—real-time cross-border settlement, reduced intermediaries, and low-cost value transfer—are drawing attention as a practical alternative that can replace or complement the existing SWIFT-based foreign exchange infrastructure.

Currently, global remittance structures involve complex processes through numerous intermediary banks, leading to high fees and settlement delays. In contrast, remittances using stablecoins can maximize efficiency through direct transfer on blockchain networks, chain-based verification, and smart contract-based settlement. In fact, US-based stablecoins like USDC and USDT are already informally used for remittances to developing countries, immigrant communities, and black market currency exchange.

This structure is equally applicable to KRW stablecoins. In particular, there is potential for use in small-value remittances and current account settlements, especially in major Asian countries (e.g., Vietnam, the Philippines, and Thailand) that have close ties with Korea through trade, tourism, study abroad, and labor migration. For example, a model where foreign workers in Korea directly receive and exchange KRW stablecoins issued in Korea through their home country's on-chain or off-chain infrastructure is considered feasible.

Key requirements for realizing such global utilization are as follows:

Cross-chain infrastructure linkage: As seen in Circle's CCTP (Cross-Chain Transfer Protocol) case, technical design to maintain settlement alignment across multiple chains is essential. This forms the basis for ensuring the safety and consistency of conversions with foreign currency-based tokens, cross-chain swaps, and bridge transactions.

Global custody, wallet, and DEX partnerships: Technical linkage with global services that can support foreign currency receipt and exchange is required. The overall user experience (UX) should be considered, extending beyond simple transfers to include payments, exchanges, and asset management.

KYC/AML and foreign exchange regulatory compliance: Review of alignment with exchange registration, foreign exchange business licensing, and foreign exchange reporting systems is essential for cross-border fund transfers. It should be noted that applicable regulations may differ between cases where KRW stablecoin issuance/redemption is limited to domestic transactions and where direct overseas transfer is possible.

Potential for use as a cross-border payment instrument based on digital securities: If capital market-type stablecoins are used as a payment method for overseas trading or profit settlement of digital securities, they can function as a settlement infrastructure for capital market exports, going beyond simple remittances. This can be a core foundation for digital securities projects considering global exchange listings.

Meanwhile, the functional separation structure of Korea's VASP system could act as a limiting factor for global expansion. For example, if global partners require a structure where custody, exchange, and distribution functions are integrated within a single infrastructure, it may conflict with the domestic requirement for functional separation of Korean entities. Therefore, the issuing consortium should design a separate legal entity or collaborative partner structure to handle global expansion functions, and a review of related licenses and regulatory alignment must be conducted in parallel.

In summary, the global expansion of capital market-type KRW stablecoins can be a strategic tool to extend the digital distribution path of KRW across borders, beyond simple remittances. If it satisfies three conditions—technical interoperability, foreign exchange regulatory alignment, and securing global partnerships—it can function as a core infrastructure for the digitalization of Korea's capital market and a foundation for expanding KRW distribution based on blockchain.

In Korea, discussions around stablecoins have primarily focused on the issuance of KRW-based stablecoins. While stablecoins are expected to become a key part of future payment and settlement infrastructure, there is currently no KRW-denominated stablecoin in active circulation. As a result, various players are actively seeking to gain a first-mover advantage in this emerging market.

The introduction of issuance and operation of stablecoins requires not only technological capability but also capital soundness and well-established distribution channels. From a regulatory perspective, there is a possibility that the role of issuance, distribution, and custody may be separated such that entities responsible for each role should operate in collaboration. In particular, we are seeing various discussions regarding consortia led by major commercial banks, partnerships between virtual asset exchanges and blockchain technology firms, or between exchanges and financial institutions in the Korea market. Also, fintech companies are also in play to build partnerships.

However, for a KRW-based stablecoin to be issued and used domestically, a regulatory framework must be established foremost. Although the enactment of the Digital Asset Fundamental Act (Phase 2 legislation for virtual assets) is currently under discussion in the National Assembly, it is expected to take considerable time before the bill actually passes into law. Accordingly, some market participants are hoping to be granted with pilot testing exemptions through the financial regulatory sandbox[1].

From the perspective of financial supervisory authorities, immediate full adoption of stablecoins, which could have unseen implications for financial stability, the payment system, and the foreign exchange market, would not be the preferred approach. Rather, it is considered more appropriate to gradually design the relevant systems by first operating pilot tests within the regulatory sandbox environment. Therefore, it is highly likely that small-scale issuance will initially be allowed under the regulatory sandbox regime, with full implementation to follow once a formal legal framework is in place.

The financial regulatory sandbox is a framework that allows innovative financial services to be tested within a controlled environment to evaluate the adequacy of existing regulations. Initial implementation through sandbox is recognized as an effective method for verifying the technological and institutional feasibility of new financial services before a full-fledged legal framework for a service is established.

This report assumes the establishment of a formal legal framework governing stablecoins and aims to explore how stablecoins will be used domestically, along with identifying the provisions that will be necessary to implement such use and the existing provisions that may require amendment.

The first stablecoin report by HOR proposed a high-level regulatory framework for KRW-based stablecoins. While the first report outlined a broad structure regarding the scope of regulation, issuer eligibility, issuer supervision, reserve asset requirements, regulatory measures in case of operational failure, and foreign exchange transaction regulations, this second report aims to provide a more detailed and precise plan for regulatory framework.

In regulating virtual assets, including stablecoins, the most important consideration is minimizing regulatory arbitrage with global markets. Unlike traditional financial markets, the virtual asset market is not a closed system confined to a single jurisdiction. Rather, it is an open market where the same virtual assets are traded across multiple jurisdictions and are mutually interchangeable. Therefore, any regulatory arbitrage directly affects market demand and, ultimately, the overall competitiveness of the market[2].

Accordingly, this report focuses on ensuring the competitiveness of the domestic virtual asset market by minimizing regulatory divergence from global standards in suggesting the plan for future regulatory framework. The primary benchmark for domestic regulatory framework will be the United States' stablecoin legislation, the Guiding and Establishing National Innovation in U.S. Stablecoins Act (GENIUS Act), while also referencing the regulatory directions of other major jurisdictions such as the EU and the UK where necessary.

The revised version of the GENIUS Act, proposed on May 1, significantly strengthened the regulatory framework compared to the initial draft. Regarding its scope of application, the Act prohibits anyone—including digital asset service providers—from offering or selling stablecoins to U.S. persons unless the stablecoin is issued by an issuer authorized under U.S. law. This effectively imposes strict compliance requirements on USD-based stablecoins issued abroad, mandating that they adhere to U.S. regulations in order to be accessible within the U.S. market[3] [4].

As an exception for foreign issuers, if they are subject to the regulation and supervision of a foreign regulatory authority whose regime is deemed equivalently strong to the regulatory and supervisory framework established under the GENIUS Act, they may offer or sell stablecoins through digital asset service providers under the following conditions:

(i) they must register with a U.S. accounting auditor; and

(ii) they must maintain sufficient reserve funds at U.S. financial institutions to meet the liquidity demands of U.S. customers.

The above regulation sets out the requirements that must be met for foreign-issued stablecoins to be distributed locally. Applying this to the domestic context would means that, for example, if a domestic exchange wishes to support trading of USDT, Tether must not only be subject to supervision by the regulatory authority of its home country—which must have a stablecoin regulatory regime comparable to that of Korea—but also be registered with the domestic supervisory authority and maintain reserve funds in a domestic bank. Considering the differences between the U.S. and Korean markets, such regulatory requirements may not be practically feasible.

In contrast, the UK Treasury has opted to regulate stablecoins not as electronic money but in a manner akin to financial securities, by imposing requirements such as disclosure obligations, minimum capital requirements, and reserve asset management standards. The UK government explicitly stated in a recently published policy note that this regulatory approach is based on the assessment that stablecoins are not yet widely used as a means of payment.

Under the UK framework, stablecoins issued overseas can be distributed in the UK without the issuer itself being required to obtain authorization locally, as long as the stablecoins are circulated through UK-authorized exchanges. However, this approach has drawn criticism for potentially disadvantaging pound-sterling-based stablecoins issued within the UK and creating an environment in which foreign-issued USD-based stablecoins could effectively dominate the UK market. This represents an important policy consideration that should be taken into account when designing regulations for foreign-issued stablecoins.

This report suggests that a list of foreign jurisdictions to which the principle of reciprocity may apply be made public. Also, through appropriate international cooperation procedures adopted by agreements, such as execution of MOUs amongst those countries, it should be possible to ensure effective priority repayment from reserve assets in the event of insolvency of foreign issuers.

For stablecoins that do not fall under this list but are nonetheless intended to be supported for trading, it would be necessary for exchanges or designated industry associations to enter into contractual arrangements with the issuing foundation that explicitly guarantee redemption rights for the exchange[5], and to establish practical means of securing those rights. The underlying reason for requiring reserves to be held domestically is to ensure the enforceability of redemption rights in the event of bankruptcy of the issuer. However, if the exchange, acting on behalf of users, formalize and execute a clear agreement with the issuing foundation, a clear method to exercise redemption rights can be secured in cases of potential future international disputes.

Stablecoins possess a dual nature: they function both as means of payment and as investment assets. Allowing the payment of interest would enhance the attractiveness of stablecoins as investment assets and is likely to increase demand for holding them, thereby accelerating their market penetration in a short period. However, it is undeniable that such a structure could potentially have negative implications for the stability of the financial system.

Those opposed to allowing interest payments on stablecoins argue that doing so could cause stablecoins to function as substitutes for traditional bank deposits. This, in turn, may undermine banks’ ability to extend credit, potentially raising corporate financing costs and weakening the overall credit intermediation role of the banking sector. It could also impair the effectiveness of monetary policy. Accordingly, they advocate for a ban on interest-bearing stablecoins to prevent their use as deposit alternatives and to ensure they are used solely as a means of payment.