Ethena is the yield layer for the dollar economy — a generational franchise in the making in crypto's fastest-growing product category. The stablecoin supply doubled to $320B in eighteen months, yet less than 10% earns any yield. USDe crossed $1B faster than any dollar product in crypto history, became the largest yield-bearing stablecoin within a year of launch, and has embedded itself into DeFi's lending infrastructure in a way non-DeFi competitors cannot replicate. $5.1B in idle capital is about to be redeployed, transforming USDe into the highest-yielding dollar in DeFi.

Ethena is the only protocol that converts perpetual futures funding into stablecoin yield, and both markets it straddles are accelerating at megatrend speed. Stablecoins are marching toward $500B+. Perps are breaking out of their crypto-native ceiling. HIP-3 equity perps on Hyperliquid scaled from $525M to $30.7B in weekly volume in a single quarter. More stablecoin demand means more capital flowing into USDe. Deeper perp markets mean more capacity to generate competitive yields without compressing returns. The two legs reinforce each other, and no other protocol occupies this intersection.

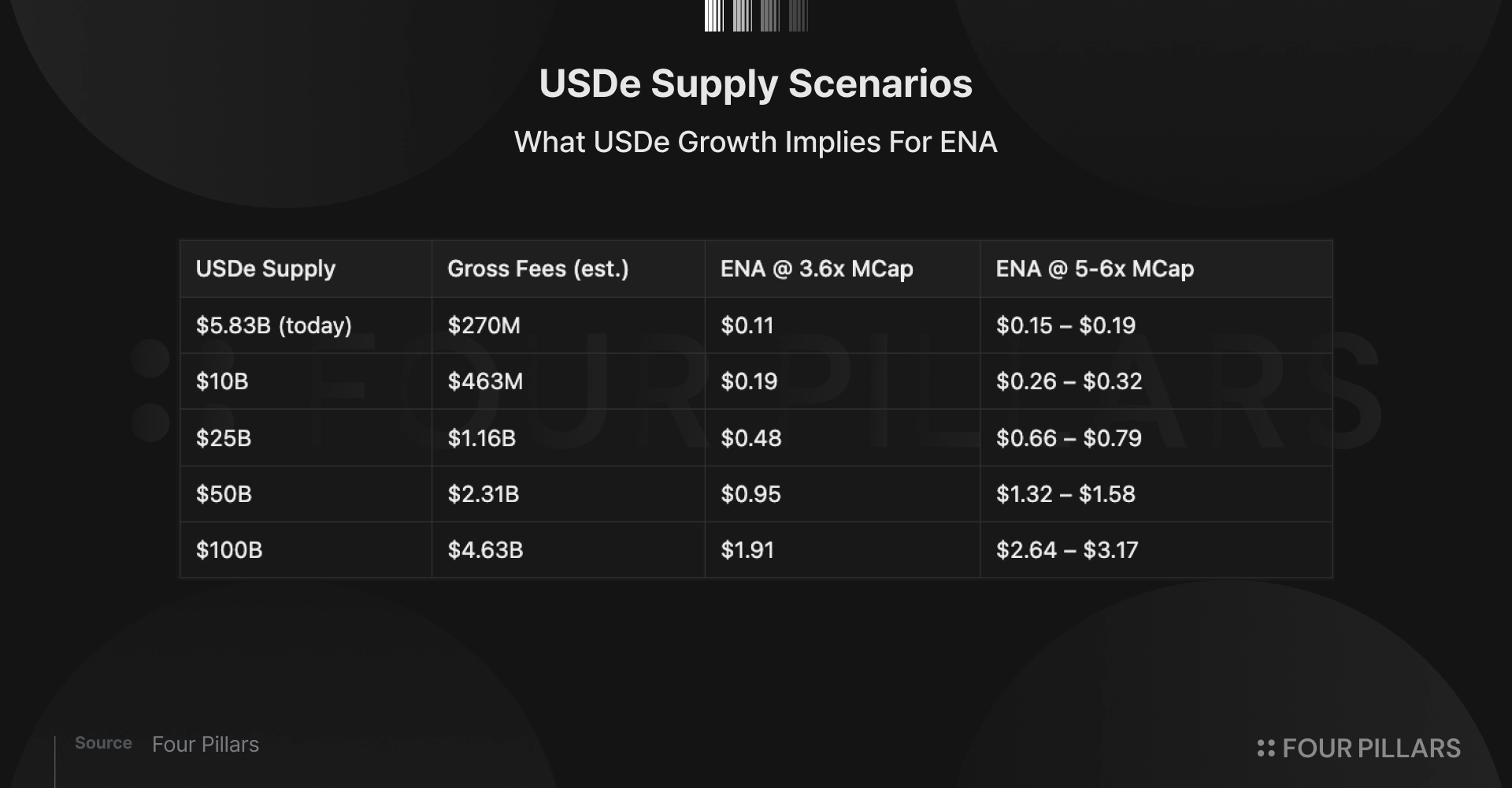

At $0.11, ENA trades at 3.6x gross fees with zero value accrual. Guy Young's stated target is $100B. Even at $25B, or 5% of a $500B stablecoin market, ENA is worth $0.48-$0.79 before any fee switch. The fee switch debate is really a scale debate: self-defeating at current AUM, trivially absorbed at $25B+ with diversified backing. The problem solves itself as USDe grows. Dilution of ~14.6% annualized is the carrying cost, and at this multiple, the scenarios absorb it several times over.

Stablecoins are crypto's most important product category. Full stop.

Supply crossed $320B earlier this year, doubling from $150B in eighteen months. Transaction volume hit $33T in 2025, surpassing the US Automated Clearing House network in adjusted throughput. B2B stablecoin payments grew from under $100M per month in 2023 to $6B per month in 2025. Every category that touches dollars is migrating on-chain, and it is happening faster than even bullish forecasts from two years ago suggested possible.

And yet less than 10% of that $320B earns any yield natively. USDT and USDC holders receive nothing directly from the issuer, while Tether and Circle collected over $7B in interest revenue last year. The closest exception (Circle routing 50% of its reserve interest to Coinbase, Coinbase handing a slice back to Coinbase One subscribers ($4.99/month) at 3.5% APY) actually sharpens the case for USDe. Yield exists in the stablecoin economy, but only after passing through an issuer, a distribution partner, a custody relationship, and a paywall.

The arbitrage between what stablecoin capital could earn and what it actually earns remains one of the largest unserved opportunities in crypto, and it persists because the incumbents are structurally prevented from closing it. The GENIUS Act prohibits stablecoin issuers from paying yield directly to token holders. US money transmitter licenses and banking relationships do not permit native pass-through. Tether and Circle are prisoners of their own regulatory posture, and every intermediary that extracts a spread between the reserve and the holder is a toll USDe does not pay.

For the global yield-seeking side of this gap, USDe is the product built to close it natively. A synthetic dollar backed by delta-neutral positions (long spot crypto, short equivalent perps) that earns the funding rate differential and passes it through to sUSDe holders. The mechanism is not novel (the basis trade has existed for decades in both TradFi and crypto). Ethena's innovation lies in the packaging: tokenize the trade, institutionalize the custody, embed it into DeFi, and let the product become its own distribution channel.

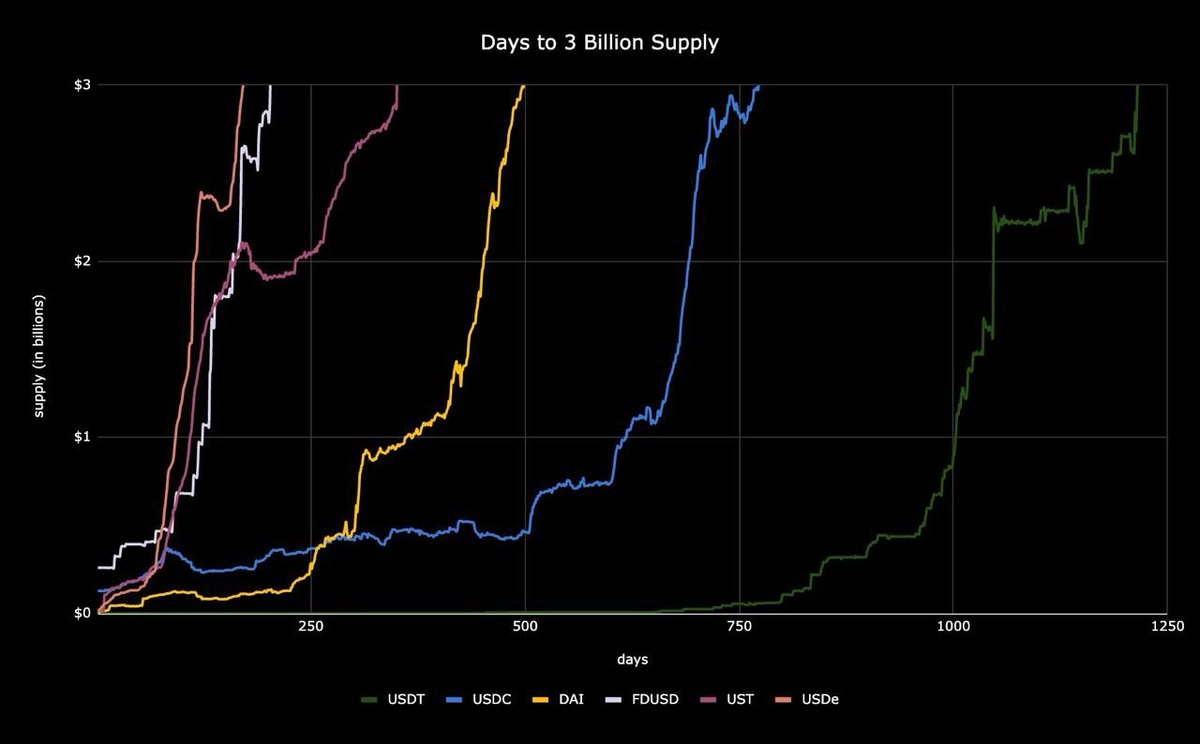

USDe reached $1B in supply within three to four weeks of launch. USDT took over three years to reach the same milestone. USDC took twenty-one months. USDe hit $2B in seven weeks and $6B in ten months. No dollar-denominated product in crypto has ever demonstrated this kind of demand velocity, and the trajectory suggests the market for yield-bearing stablecoins was underserved to a degree few appreciated before USDe existed.

Source: X (@gdog97_)

Below we share our thesis.

Ethena's story begins with Guy Young. Before he founded Ethena, Young spent his career at Cerberus Capital Management, a $55B distressed credit firm that specializes in the kind of decisions where the wrong answer costs you the fund. Distressed credit is an unglamorous apprenticeship. You spend your twenties staring at capital structures, haircuts, loan covenants, and liquidation waterfalls. You learn that most problems in finance are solvency problems dressed up as liquidity problems. That background shows up everywhere in how Ethena has been operated.

When the Bybit incident exposed Ethena to $30M in stuck collateral, Young resolved it through Copper's Clearloop infrastructure without breaking USDe's peg. After Oct 10/10, USDe's supply contracted from $15B to $6.3B in an orderly, mechanical way. No depeg. No panic. No structural failure. The product did what it was designed to do: shrink when yield compressed, preserve the mechanism, wait out the cycle. When Converge failed to deliver as an L1 experiment, Young killed it rather than sink more resources into a struggling product. When the market screamed for a fee switch as a short-term price catalyst, he declined to activate it prematurely.

These are costly signals. Each one could have gone the other way. Each one demonstrates a founder who has internalized the Howard Marks maxim that "you can't predict, but you can prepare", and who appears to care more about whether the business still exists in five years than whether the token pumps next quarter. Young has stated publicly that USDe "has the ability to be a $100B product," and has framed Ethena as "the yield version of Tether." If Tether sits at $186B today with zero yield to holders, the question becomes: “how large can USDe become as the version that pays you?”

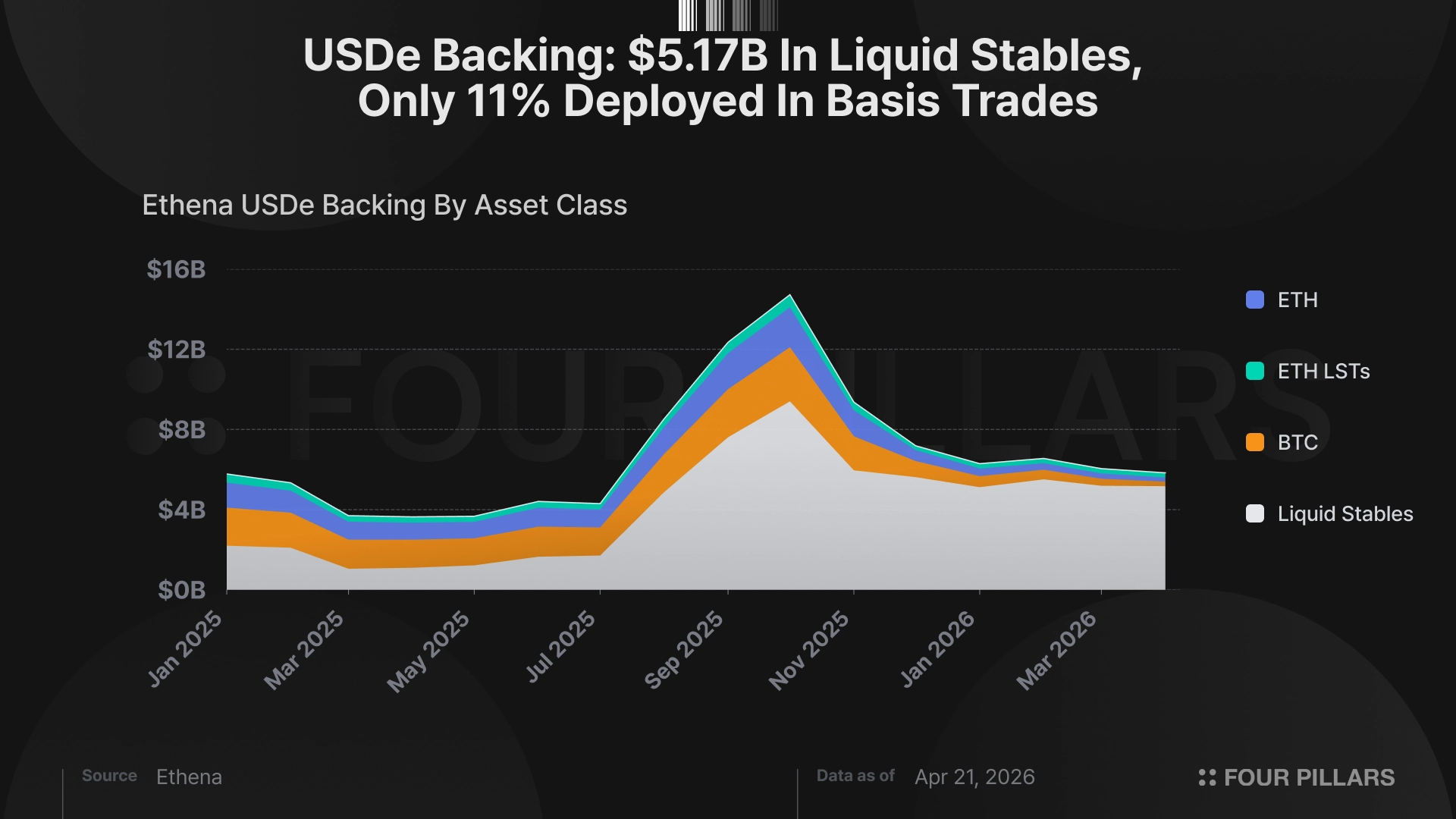

USDe today sits at $5.83B in supply. Of that, 89% ($5.19B) is held in liquid stablecoins at regulated custodians (Copper, Ceffu, Cobo) with regular attestations. Only 11% ($223M BTC, $423M ETH) is currently in delta-neutral perp positions actively generating basis yield. Roughly half the supply is staked (48.6%), with sUSDe paying 3.75%.

A few things fall out of those numbers. First, Ethena produces $270M in annualized gross fees with only 11% of AUM deployed into the yield-generating strategy. This is a top-tier DeFi revenue protocol running at a fraction of installed capacity. Second, the idle 89% is dry powder. On April 6, Ethena announced a plan to redeploy $5.1B of it into yield-generating strategies: institutional lending through Anchorage Digital (OCC-chartered), Maple Institutional, and Coinbase Asset Management; structured credit; and HyENA's equity and commodity basis trades on Hyperliquid. USDtb ($937M backed by BlackRock BUIDL) is already live. The rest is announced but not yet executed.

If the $5.1B deploys at a blended 4-5%, sUSDe yield rises from 3.75% to an estimated 8-10% at the current staking ratio. This is USDe becoming the highest-yielding stablecoin product in DeFi, using capital that currently generates nothing.

To understand why Ethena specifically wins this category, you have to understand the demand layer it is embedded in.

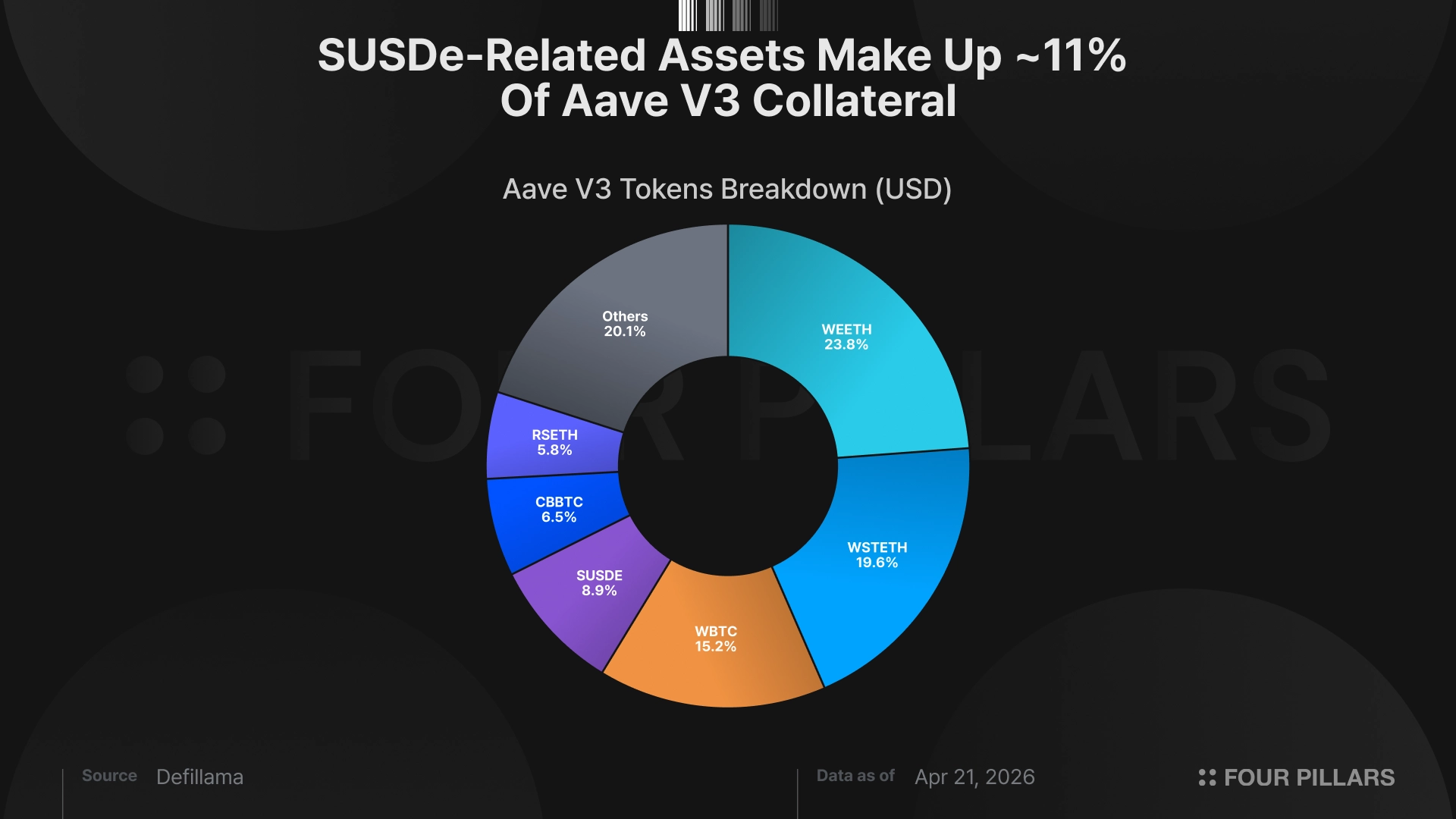

DeFi composability creates demand that alternatives cannot replicate. USDe-related exposure is spread across the DeFi stack in a way no other yield-bearing dollar has achieved. Roughly $2.9B sits on Aave (about 50% of total supply) as leveraged-loop collateral, ~$750M sits in Pendle's fixed-rate markets, and ~$250M sits in Morpho vaults as of April 19, 2026.

You deposit sUSDe, borrow USDC against it, buy more USDe, stake, and repeat, or fix the yield via Pendle PT and then re-collateralize. Each dollar of USDe in a loop creates 2-3x in effective protocol demand. This is multiplicative demand that exists because sUSDe has been accepted as blue-chip collateral on Aave, tokenized into principal and yield components on Pendle, supported in Morpho's isolated vaults, and sanctioned by Sky. Non-DeFi yield-bearing stablecoins can match USDe's stated yield. They cannot match the yield amplification that composability provides.

And these integrations took two years to build. Listing sUSDe on Aave required risk committee approvals, oracle design, liquidation parameter calibration, and real on-chain battle-testing through multiple volatility events. Pendle had to build dedicated PT markets with sufficient liquidity to support the re-collateralization loop. Morpho's isolated-vault architecture had to be risk-parameterized for sUSDe specifically. A competitor cannot clone this in a quarter. Switching costs are asymmetric. If Aave were to remove sUSDe, it would cascade into Aave's own balance sheet. At peak, Ethena-related exposure on Aave reached $6.6B. That level of infrastructural entanglement is co-dependency.

The composability is also self-reinforcing. More sUSDe accepted as collateral → more loops possible → more USDe demand → deeper liquidity → more protocols willing to accept sUSDe as collateral → repeat. The majority of supply being in loops today is evidence the flywheel is already spinning.

One subtle but important point on cyclicality — which has been the largest bear argument on Ethena since inception. The critique is that Ethena's yield depends on perp funding, funding depends on speculative leverage, leverage comes and goes with cycles, therefore USDe is a cyclical trade, therefore it will never be a permanent allocation, therefore USDe has a structural cap.

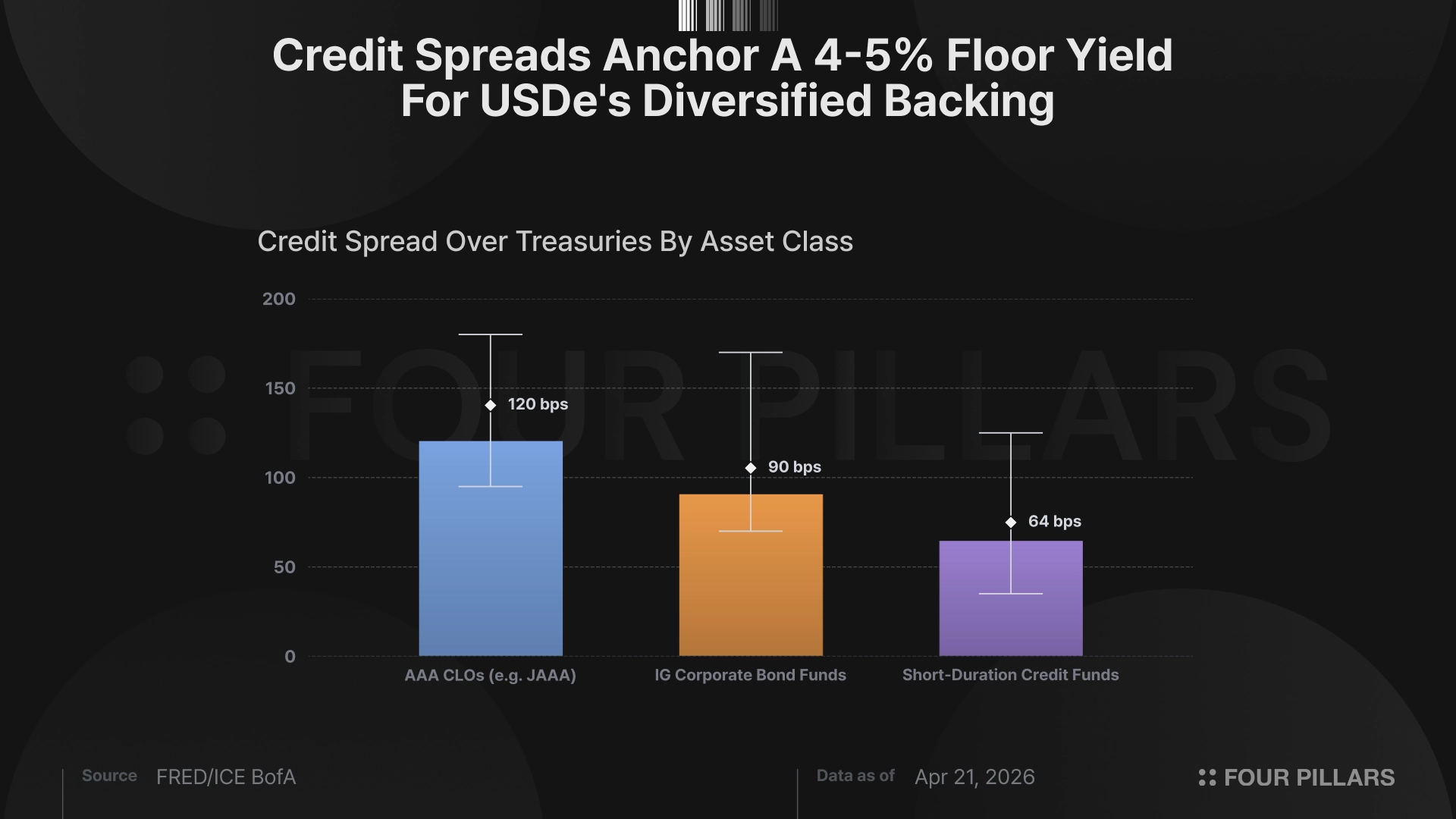

The diversification plan dissolves this critique. With $5.1B redeployed into institutional lending, Ethena adds a 4-5% floor yield from credit exposure that performs when rates are high — i.e., exactly when the basis trade compresses. High rates favor the diversified lending portfolio. Low rates favor the basis trade (falling rates drive speculation, which drives leverage demand, which drives perp funding). The two yield sources are counter-cyclical to each other.

The practical result is that USDe produces competitive yields in both rate environments. This is what transforms USDe from a cyclical product that capital rotates through into a permanent allocation that capital rotates into. Permanent allocations compound. Cyclical trades don't. That distinction is the difference between USDe capped at $5-6B forever and USDe reaching $25B+.

Ethena's structural position in the market is unique. It is the only protocol that connects the stablecoin economy and the perpetual futures economy through a single mechanism, converting perp funding into stablecoin yield. Both markets are accelerating, and both growth vectors expand Ethena's addressable market simultaneously.

The stablecoin side is already covered — $320B and growing, less than 10% earning yield, massive unserved demand. The GENIUS Act is the more complicated piece. Under the Act's 1:1 HQLA reserve requirement, USDe doesn't qualify as a permitted payment stablecoin and is effectively illegal to issue in the U.S. USDe is already not offered there, and inflows come primarily from outside the jurisdiction.

Ethena's answer was USDtb, a GENIUS-compliant payment stablecoin issued through Anchorage Digital's OCC-chartered infrastructure, built specifically to operate inside the Act for the U.S. institutional payments segment the law legitimizes. This is the operationally important move. Young built a second product that would be compliant by construction, capturing the demand the Act creates for regulated onshore dollars, while preserving USDe's offshore-first architecture for the yield-seeking capital the Act cannot touch.

The result is a two-track system: USDtb for U.S.-regulated payments, USDe for global yield. Neither product is what the Act's clean tailwind narrative suggests. Both reflect a founder who watched the regulatory boundary being drawn and built specifically to operate on both sides of it.

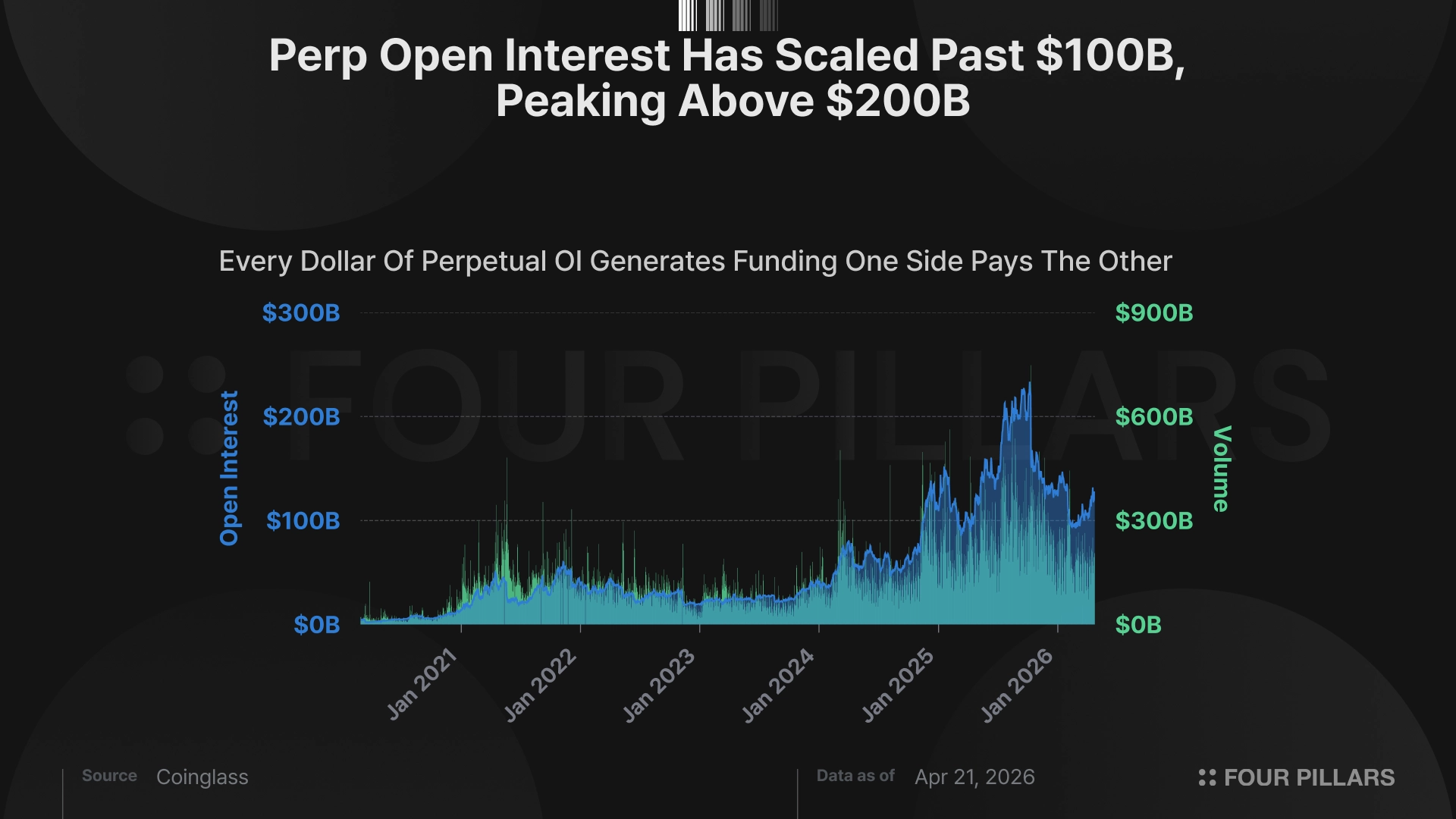

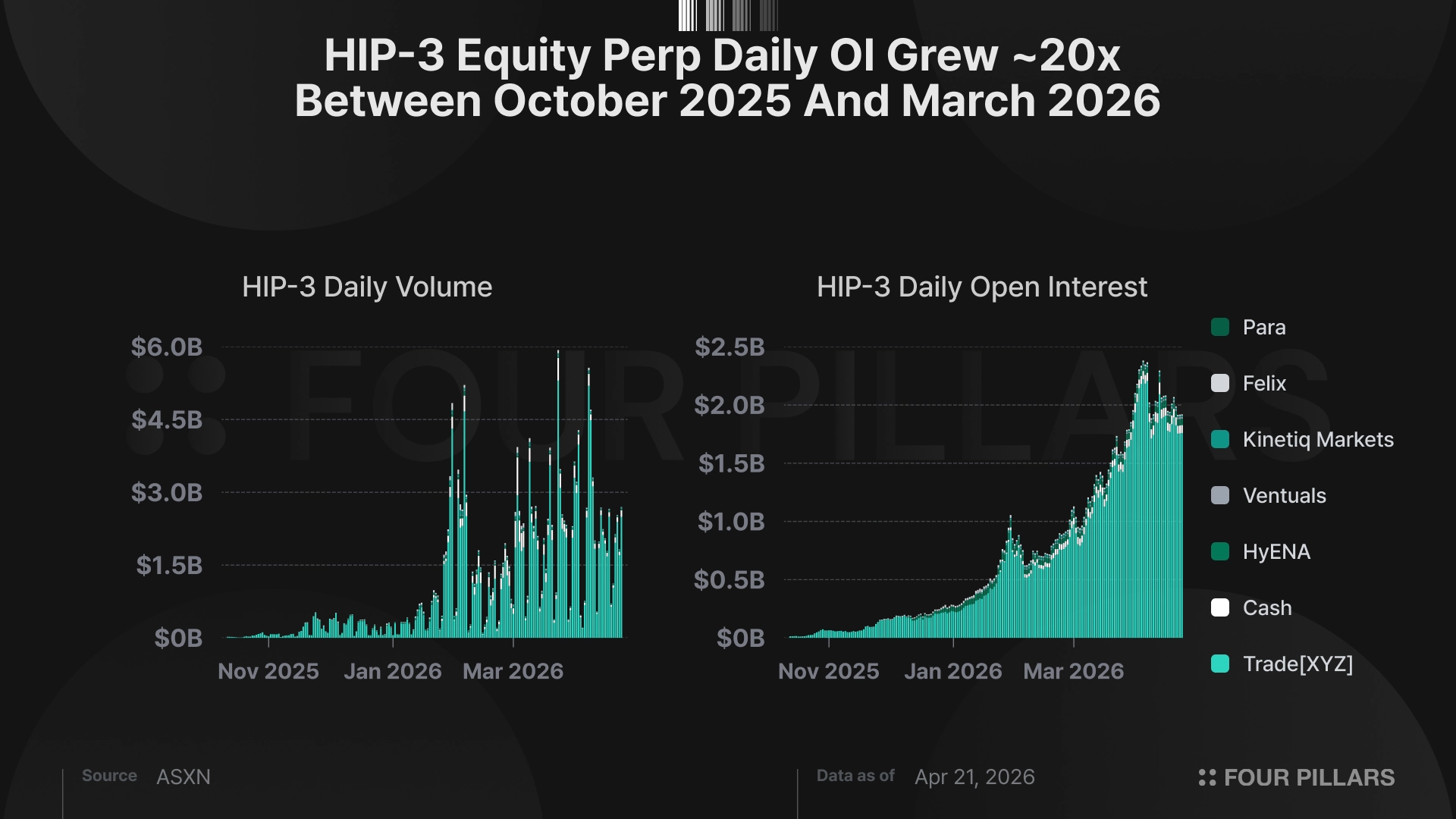

The perp side is where the acceleration has been most dramatic. DEX perp volume hit $7.7T in 2025, up 346% year-over-year. Then equity perps arrived. Binance launched Tesla perps in January 2026. Coinbase followed with stock perps in March. S&P Dow Jones Indices licensed the S&P 500 to TradeXYZ on Hyperliquid. HIP-3 equity perps on Hyperliquid went from $525M per week to $30.7B per week in Q1 — a 5,757% increase in a single quarter, growing from 21.5% to 45% (peak) of all Hyperliquid activity. A new asset class was effectively invented last quarter.

Every dollar of perpetual open interest generates funding that one side pays the other. That funding is the raw material for USDe's yield. The basis trade works on any asset with a futures curve in contango, not just BTC or ETH. As perps expand into equities, commodities, and (eventually) forex, Ethena's yield sources multiply and diversify. Crude oil did over $1B in weekend volume on Hyperliquid during the Iran tensions of 2025, when TradFi markets were closed. That is a yield source that did not exist twelve months ago.

The classical constraint on basis trade strategies is capacity. As you deploy more AUM into the trade, you compress the funding rate you are harvesting, and your yields fall. For a single-asset basis strategy, scale is self-defeating. Ethena's answer is to expand the number of markets it can deploy into. The factory gets bigger, and the production cost per unit of yield falls. Every new perpetual market (every equity, every commodity, every eventual forex pair) creates basis trade capacity that did not exist before. If equity perp OI reaches even 1% of S&P 500 futures OI (~$750B), that is $7.5B of new yield-generating capacity for Ethena alone.

Source: ASXN

Both legs growing at the same time is what makes this structural. Stablecoin demand grows, which pushes more yield-seeking capital into USDe. Perp market depth expands, which creates more capacity to generate competitive yields on that capital. The two reinforce each other. MakerDAO generates stablecoin yield through T-bill holdings. Hyperliquid facilitates perp trading. Neither converts one market into returns for the other. Ethena is the only protocol that does, and that positioning compounds as both markets scale.

ENA trades at $0.11 today. Against $270M in annualized gross fees, that is a 3.6x multiple on a top-tier DeFi revenue protocol with no active value accrual.

The vast majority of the fee flows to sUSDe holders through an ERC-4626 vault, with a portion allocated to a $62M reserve fund that absorbs negative-yield periods. The exact split is not publicly disclosed but the reserve fund is now overcapitalized at roughly nine times its conservative tail-risk requirement, and the governance subcommittee recommended in March 2026 that further interest be redirected to sUSDe holders.

Guy Young's stated target for USDe is $100B. The reference points that make this directionally plausible: Tether at $186B, USDC at $78B, and yield-bearing stablecoins today at less than 10% of total supply. If the yield-bearing share doubles to 20% of a $500B stablecoin market, a conservative assumption given the regulatory and rate tailwinds, the category is $100B, with Ethena as the largest and best-distributed protocol in it.

Below is the math at various supply levels, using current fee generation per dollar of AUM:

At $25B, 5% of a $500B stablecoin market, Ethena generates over $1B in annual gross fees and ENA is worth $0.48-$0.79 depending on the multiple. That is 4-7x from here with no fee switch required. The fee switch, which has consumed disproportionate analyst attention, is really a question of scale.

At $5.83B and 3.75% yield it is self-defeating. Competing yield products (e.g. Aave USDC deposits at roughly 3%, Sky's sDAI at ~3.75% already match sUSDe returns with simpler risk profiles. A 10% take rate on gross fees drops sUSDe from 3.75% to approximately 3.4%.

Capital is not sentimental. It migrates to the higher yield. USDe supply contracts. The fee base that funds the take rate shrinks with it. The mechanism designed to create value accrual instead destroys the product's competitiveness.

The trap breaks at larger scale, when yields are high enough to absorb a take rate without losing competitiveness. At $25B with diversified backing, 25-30% of AUM in basis trades generating 6-10% from perp funding, 55-60% in institutional lending at 4-5%, blended protocol yield lands around 4-5%, which at a ~50% staking ratio translates to roughly 8-10% sUSDe yield. That is the moderate estimate. Under more conservative assumptions (basis funding compressed to 5%, institutional lending at 4%), sUSDe still reaches approximately 7%, comfortably above T-bill alternatives and enough to absorb a modest take rate.

The Risk Committee's designed mechanism already solves the 'self-defeating at small scale' problem, it just needs scale to become material. The problem solves itself as USDe grows. The fee switch debate is a proxy for the AUM debate, and if you solve the AUM debate you solve the fee switch debate automatically.

Dilution runs at 14.6% annualized, roughly $30M per month at current prices. By December 2026, circulating supply reaches approximately 73% of fully diluted, up from 58.4% today. That is the carrying cost of this position, and it must be respected. At $0.11 against the scenarios above, the potential upside absorbs the dilution several times over. But dilution is also the reason this setup is asymmetric rather than infinite. You are paying a time premium of ~15% per year to be in this trade.

"Risk means more things can happen than will happen." — Elroy Dimson

Our thesis is not that Ethena will succeed. It is that the setup is asymmetric enough that it pays to bet. Surface level risks are already priced in. The risks worth discussing are the ones that sit inside Ethena's own mechanism.

DeFi contagion during a fragile period. The April 2026 sequence (Drift drained for $285M via DPRK social engineering, Kelp DAO's LayerZero bridge drained for $292M, $6.6B in Aave TVL exiting in 24 hours, $196M in Aave bad debt sitting against the Umbrella reserve) is not a passing storm. It is the composability flywheel running in reverse, and it is the specific risk the bull case on Thesis 1 flinches from. Ethena does not need to be hacked to take damage. USDe is whitelisted as collateral across Aave, Pendle, Morpho, and Sky; a failure in any adjacent asset or bridge can trigger cascading liquidations that compress sUSDe yield and unwind leveraged loops.

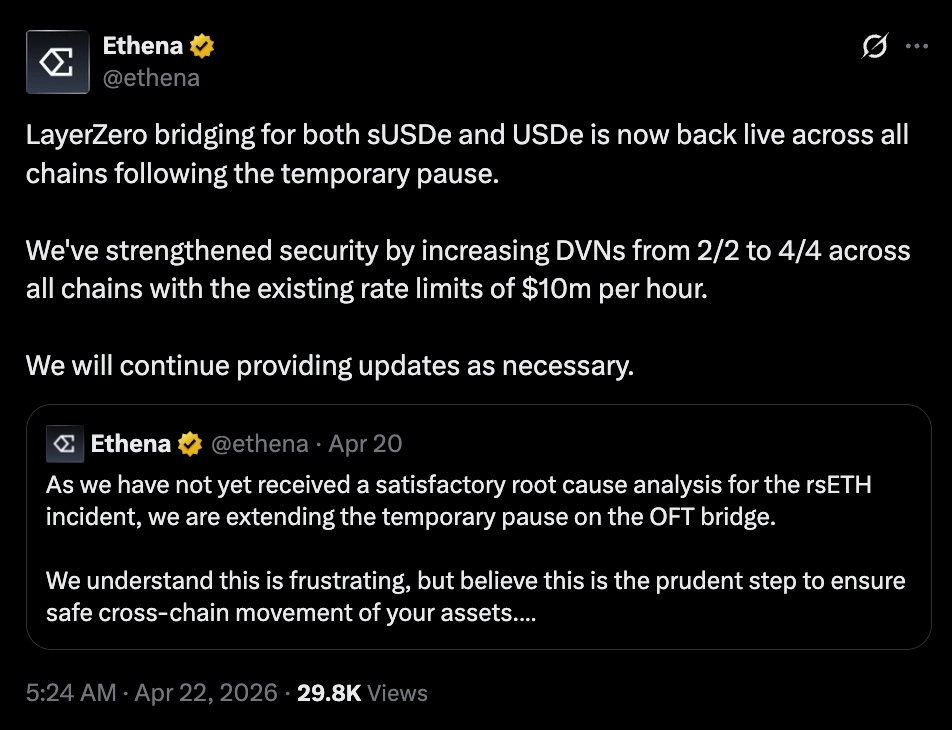

That said, Ethena's response to the Kelp event (LayerZero OFT bridges paused within hours, fresh proof of reserves published on-demand, zero rsETH exposure confirmed) was the correct operational behavior and exactly what credit-trained management does in a contagion event. By April 22, bridging was restored across all chains with DVNs doubled from 2/2 to 4/4 and rate limits held at $10M per hour, a textbook pause-verify-upgrade-resume sequence.

Source: X (@ethena)

Basis trade capacity is not fungible across markets the way the bull case assumes. The scaling argument rests on perp markets expanding into equities, commodities, and forex, with Ethena deploying into each new basis curve. In practice, most new perp markets do not trade in persistent contango. Equity perps specifically have a meaningfully different funding structure than crypto perps because the underlying trades during defined hours, has dividend curves, and has short-borrow costs that compete with funding as the clearing mechanism.

The diversification plan solves cyclicality by introducing a different risk — credit. The story that "high rates favor lending, low rates favor the basis trade, so USDe yields through the cycle" is elegant but quietly reclassifies Ethena from a market-neutral basis protocol into a credit-bearing balance sheet. Anchorage, Maple, and Coinbase Asset Management are intermediating real credit exposure. Institutional lending at 4-5% in 2026 is not riskless yield. It reflects someone's cost of capital, and somewhere downstream of that is borrower default risk that sUSDe holders are now implicitly underwriting.

sUSDe's "stickiness" is endogenous to leverage, not to allocation demand. The bull case reads $4.9B in Aave loops as evidence of deep demand and a composability moat. It is equally readable as evidence that the majority of USDe is held by leveraged yield farmers, not real money allocators. Leveraged positions are the most rate-sensitive holders in any market. If sUSDe APY drops below USDC borrow cost on Aave for even a few weeks, the loops unwind mechanically. The composability flywheel works in both directions.

The fee switch may not be the re-rating catalyst the market is pricing. The mechanism is already well-designed. The Risk Committee's activation criteria include a live competitiveness guardrail that keeps post-buyback sUSDe yield at ≥1.075× sUSDS, and OAK Research's March 2026 scenario analysis shows the preferred implementation (progressive brackets with a reserve) would preserve sUSDe competitiveness while running active 95% of the time. The problem is scale. Under current compressed-spread conditions, even the best-designed scenario generates only ~$26M annualized buyback against ENA's $74M daily trading volume and $300M+ of 2026 emissions.

OAK's own recommendation is to not activate the switch right now because dividends that are too small to matter creates more disappointment than no activation at all. The bull case implicitly prices in the fee switch as a near-term value-accrual catalyst. In practice it is probably a non-event until either USDe AUM scales materially (bigger numerator) or the emission schedule burns down (smaller denominator). Neither happens before late 2026 in any realistic scenario, which means the value accrual story the market has been waiting for is likely 12-18 months delayed from current expectations.

None of these is a reason not to take the position. They are the reasons to size carefully and watch the specific metrics that tell you whether the thesis is playing out or not (e.g. the spread between sUSDe APY and Aave USDC/USDT borrow, the composition of collateral backing USDe as diversification progresses, the funding profiles of new perp markets as they come online, and Ethena's own disclosures around credit structure).

Gradually, then suddenly.

The stablecoin category did not meaningfully exist in 2018. It was a curiosity at $2B in 2020. It crossed $150B in 2023 and $320B by the end of 2025. Few product categories in the history of finance have grown this quickly.

Ethena is the next layer. It is doing something that has never been packaged at scale before in finance, routing the speculative energy of one market into stable yield for another. Perp traders pay funding to go long. Stablecoin holders earn that funding as yield. Two markets, one mechanism, a single protocol sitting between them.

And both markets are compounding. Stablecoins are marching toward $500B+. Perpetual futures are breaking out of their crypto-native ceiling — equities came online in Q1, commodities are already trading, forex is inevitable. Every new perpetual market expands Ethena's yield-generating capacity. Every dollar of stablecoin demand expands the pool of capital that wants to sit in it. The two legs pull each other forward.

We view Ethena as the first synthetic dollar at scale, and the coronation of a category that until recently did not exist. USDe is not competing with Tether or Circle. Those are payment rails. USDe is capital infrastructure where on-chain dollars sit to earn. In that category, Ethena is already the largest, with two years of integration depth no competitor can clone in under a cycle.

Markets eventually reprice businesses as the business takes shape in front of them. Our job is to be positioned before that repricing, not after it, and sized appropriately to the asymmetry available.

At $0.11, the asymmetry is generous.

Dive into 'Narratives' that will be important in the next year