2025 was the year when regulations became clearer and Ethereum was recognized as a “digital commodity,” leading institutional investors to begin accumulating Ethereum in earnest and introducing it into traditional finance. Institutions are rapidly expanding so-called “active money” strategies, in which they not only hold Ethereum but also directly participate in a strengthened DeFi ecosystem that meets security and KYC·AML standards to seek additional yield.

The Ethereum network and major protocols are building an environment that allows large-scale capital to circulate stably within the ecosystem through scalability upgrades and the development of institution-focused infrastructure. With the continued inflow of large, long-term capital, such as pension funds, and stronger institutional support like 401(k) plans, institutional investment in the Ethereum ecosystem is expected to keep increasing in 2026.

Today, ZK technology is entering a transition period in which it is evolving beyond a simple blockchain scalability solution into an independent industrial ecosystem equipped with infrastructure and market structure. Thanks to the rapid advancement of the industrial foundation known as the “zkVM,” development barriers have significantly lowered, and competition to achieve real-time proofs is accelerating.

In addition, the emergence of “prover networks,” which efficiently buy and sell high-performance computing power, and “verifier networks,” aimed at reducing costs, is beginning to form an economic market structure. As demand surges across various sectors, including AI and finance, the ZKP market is expected to grow as large as the PoS staking market and ultimately establish itself as a core trust layer of the digital ecosystem, much like HTTPS.

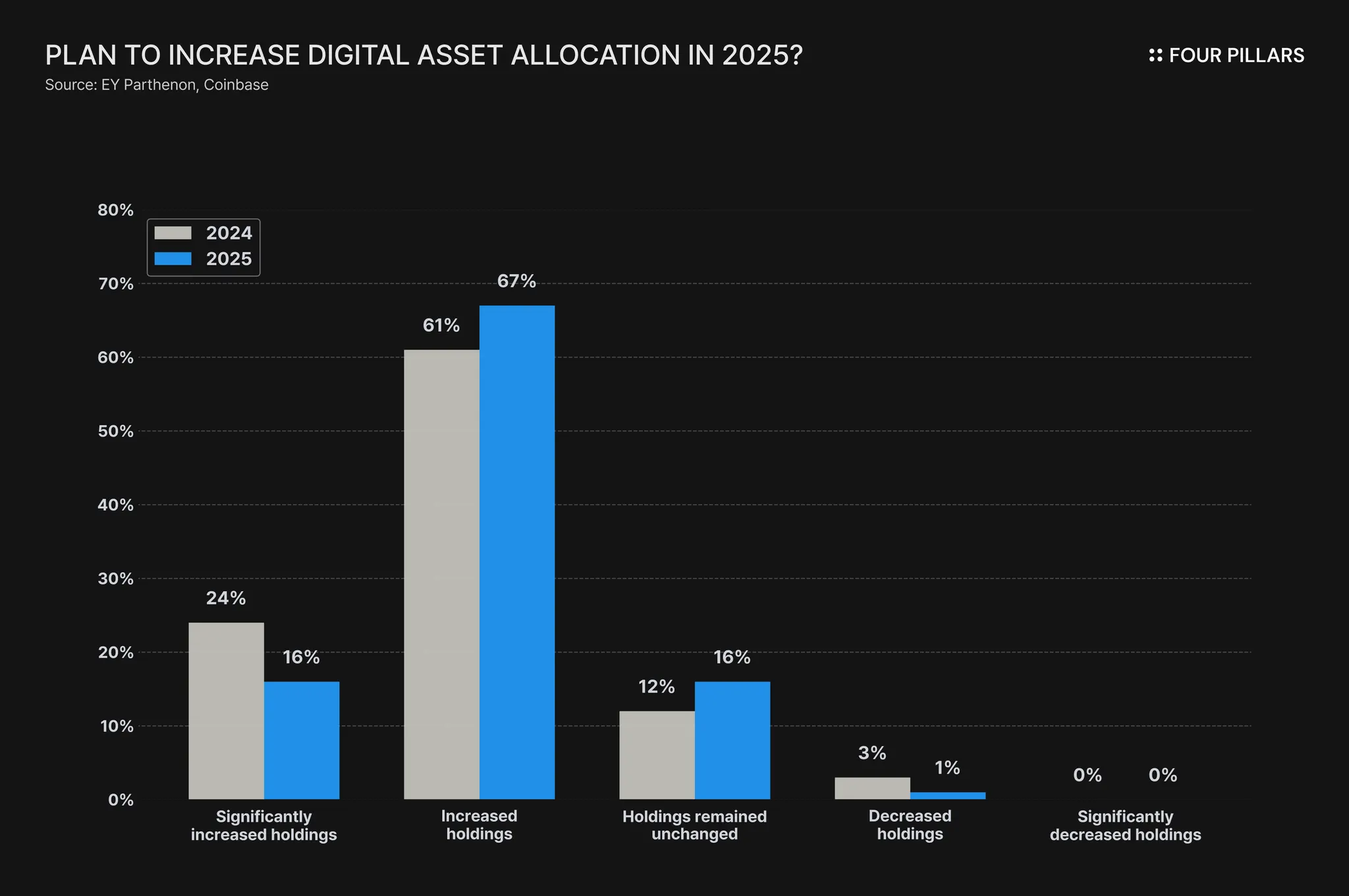

2025 was the year institutional investors began entering the cryptocurrency market in earnest. As regulations became clearer and the market matured, institutions started viewing crypto assets as strategic holdings due to their high return potential and portfolio diversification benefits. According to EY’s 2025 survey, 83% of global institutional investors responded that they planned to increase their digital asset allocation within 2025.

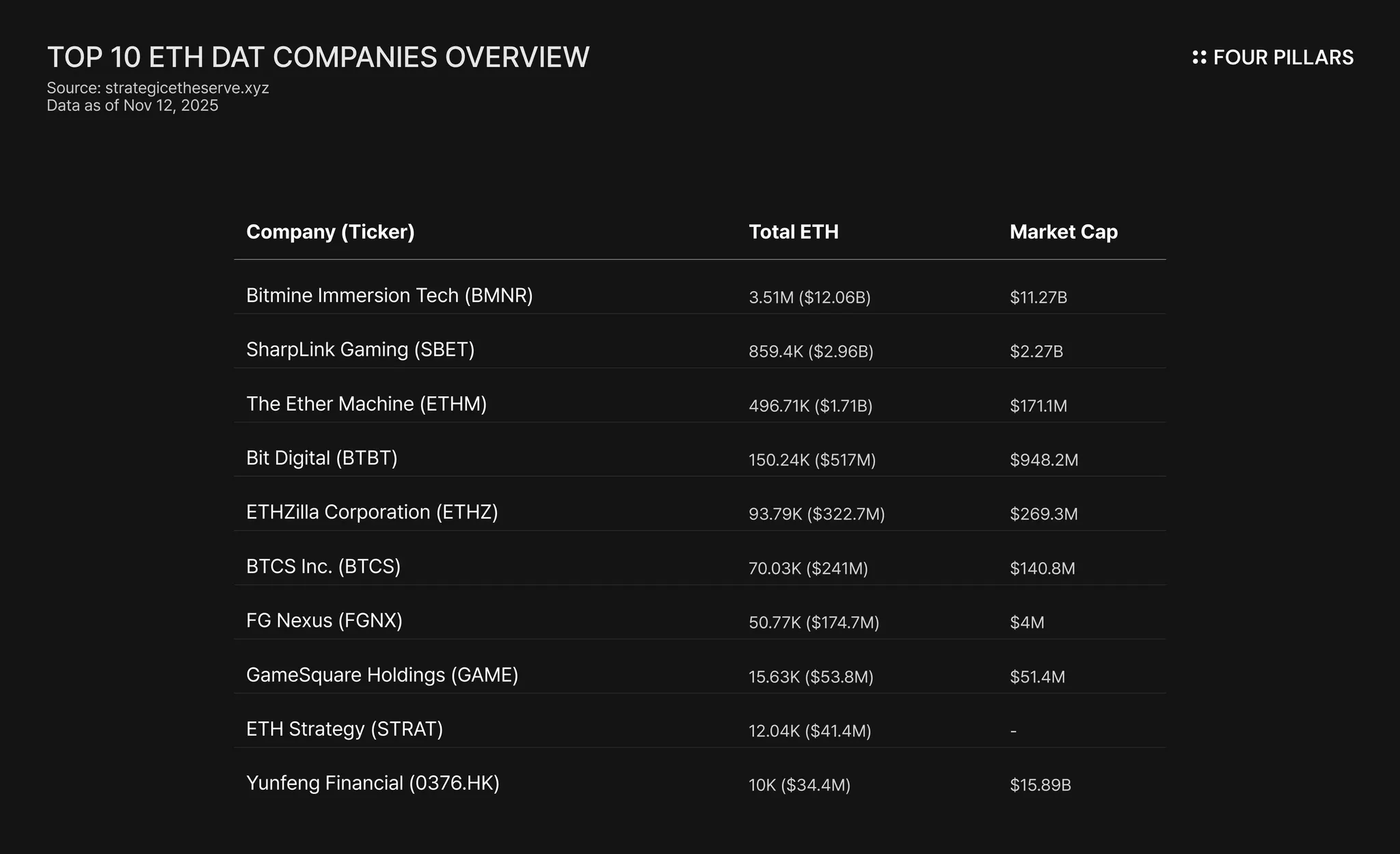

Among these assets, Bitcoin and Ethereum attracted the most attention. In particular, Ethereum saw noticeable, sustained buying from DATs(Digital Asset Treasury). Bitmine, the most representative Ethereum DAT, purchased roughly 3M ETH in 2025 alone, ending the year with more than 3.5M ETH, which accounts for about 2.8% of Ethereum’s total supply. The reason behind this institutional accumulation is that Ethereum is increasingly regarded as a well-established asset within the traditional financial system, second only to Bitcoin.

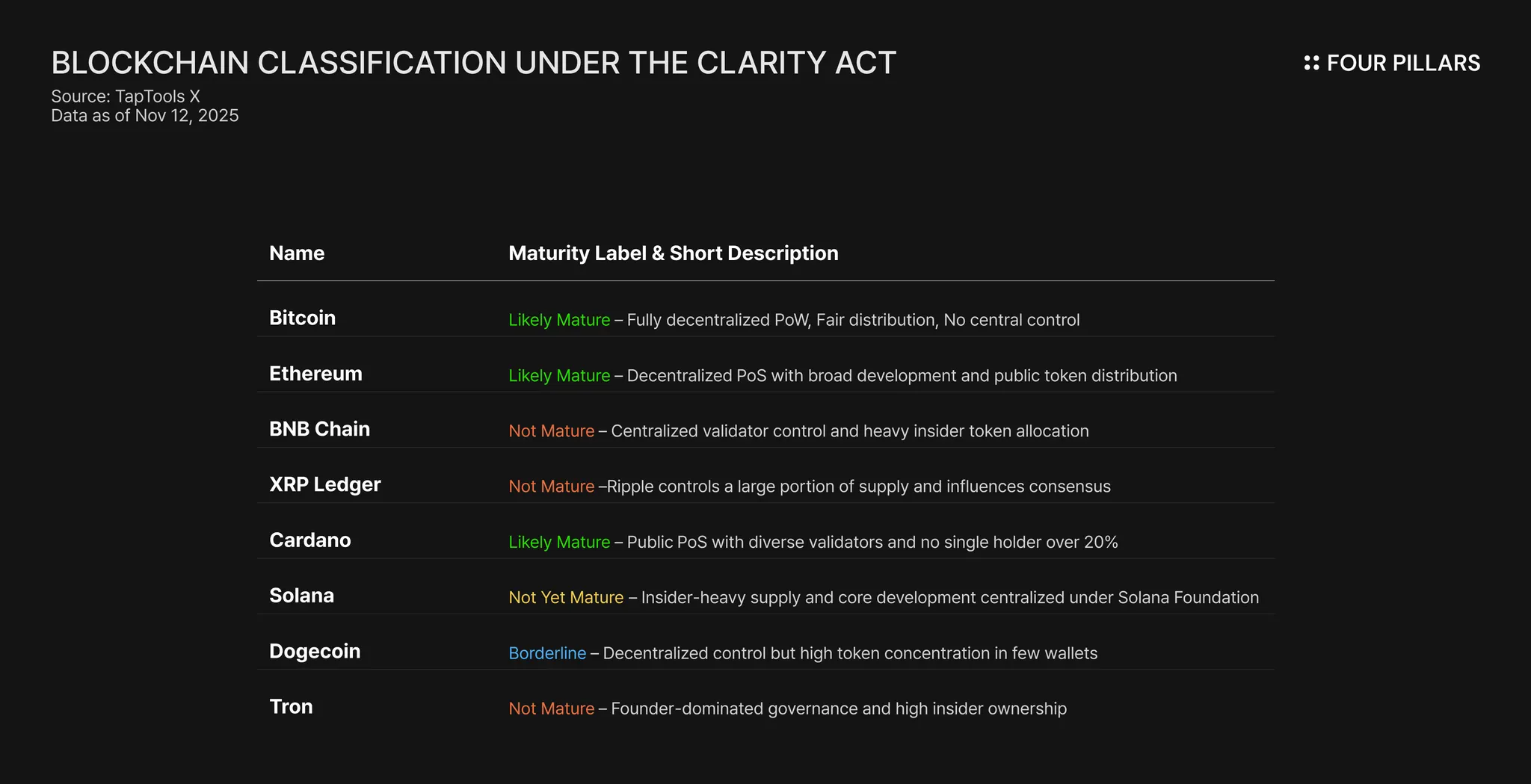

This perception strengthened in late 2024 when spot Ethereum ETFs were approved following Bitcoin, and even more so in Jul 2025 with the passage of the CLARITY Act. This act created the basis to classify cryptocurrencies such as Bitcoin, Ethereum, and Cardano as digital commodities. By recognizing these blockchains as ‘mature blockchains’, Ethereum escaped the risk of being classified as a security and secured its position as a commodity under the jurisdiction of the ‘Commodity Futures Trading Commission(CFTC)’.

This regulatory clarity reinforced the institutional infrastructure needed for traditional financial institutions to adopt Ethereum. BlackRock’s BUIDL fund and Deutsche Bank’s tokenization initiatives illustrate how major financial institutions have begun actively integrating Ethereum into actual business operations, extending the same trend.

However, institutions are not choosing Ethereum solely because of regulatory easing or because it has achieved parity with Bitcoin within the traditional financial system. Ethereum has actualized the concept of ‘programmable money’ through smart contracts, enabling institutional investors to go beyond simple ETH holding and directly participate in DeFi markets where liquidity and yield opportunities coexist. This functional utility has become a significant driver behind institutional preference for ETH.

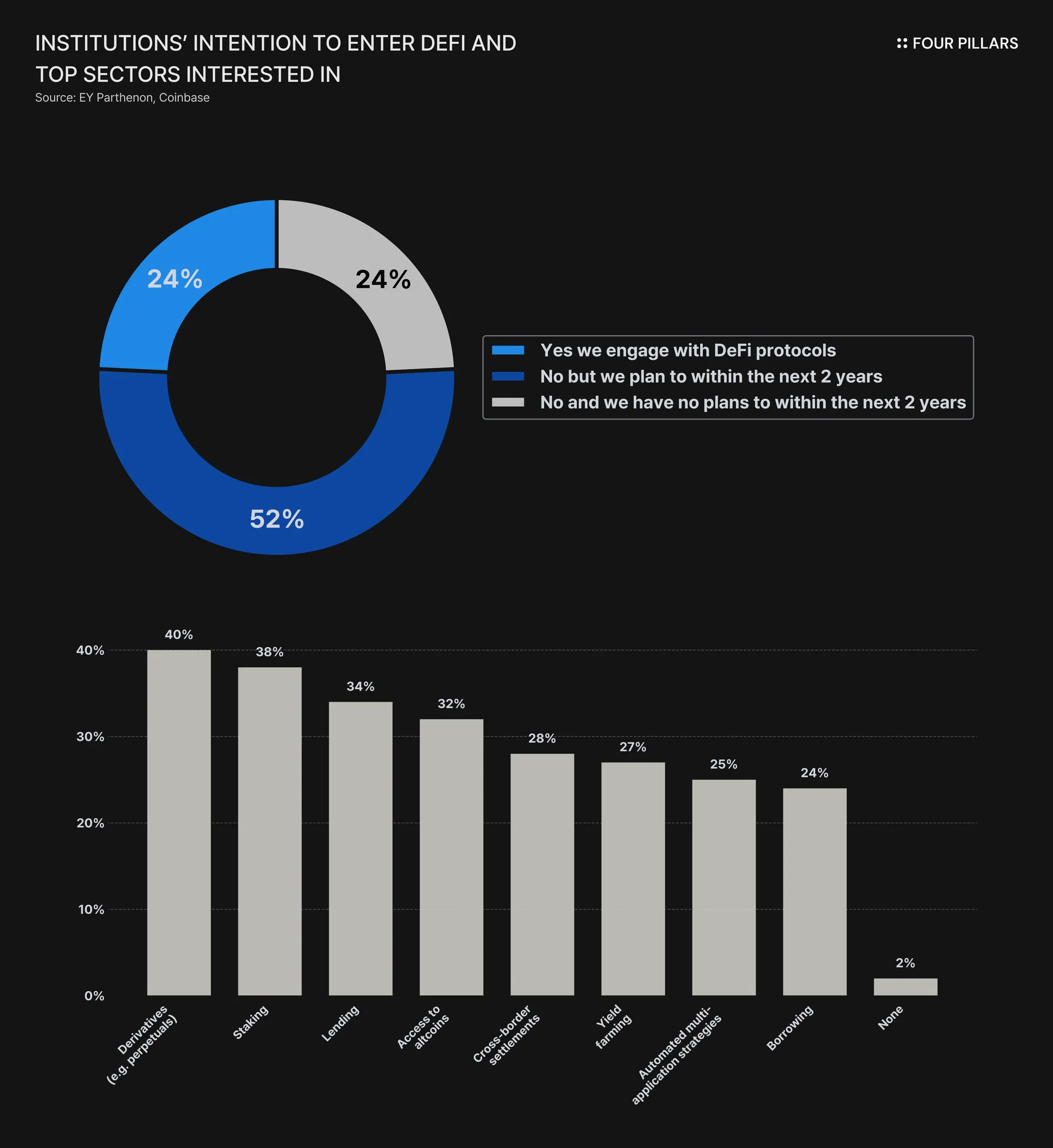

According to EY’s survey, 52% of institutional investors plan to participate directly in DeFi protocols within the next 2 years, and 24% are already using DeFi. Institutions displayed strong interest in Ethereum DeFi sectors such as staking(40%), derivatives(38%), and lending(34%).

Still, approximately 76% of institutions continue to hold Ethereum only in spot form due to regulatory requirements. Spot ETFs must comply with the SEC’s custody rules, which mandate that assets be held by qualified custodians, and DeFi’s non-custodial structure fails to meet this requirement. Although staking was initially prohibited at ETF approval due to concerns over slashing and centralization, by 2025 the SEC determined that liquid staking is not a security, creating momentum for staking options in some products, such as the Grayscale ETH ETF. Nevertheless, direct DeFi participation still presents risks of violating rules related to unregistered securities or KYC·AML obligations under the Bank Secrecy Act(BSA).

DAT firms have more operational flexibility than ETFs because they do not manage client assets directly, but as publicly listed companies they are subject to internal control and financial reporting requirements. Losses incurred through DeFi could trigger fiduciary duty litigation risks and expose these firms to additional registration demands from the SEC or CFTC, prompting many institutions to maintain conservative spot-based strategies.

Security risks also discourage institutional entry into DeFi. The Balancer hack in Nov 2025 exploited an imprecise rounding mechanism within the batchSwap function of the smart contract. Using this vulnerability, the attacker repeatedly executed transactions across multiple chains, including Ethereum, Polygon, and Base, accumulating small token differentials generated during swaps. While each transaction yielded negligible gains, their accumulation exceeded $100M. This incident demonstrated that even minor smart contract flaws can produce substantial losses, reinforcing institutional awareness of DeFi-related risks.

The Ethereum DeFi ecosystem is responding rapidly to these challenges. Major protocols such as Aave, EtherFi, mETH Protocol, and EigenCloud are concentrating on security and regulatory alignment to support the inflow of institutional capital.

Security: Since 2025, Aave has engaged Certora and Enigma Dark for verification, EtherFi and EigenCloud have utilized Certora, and mETH Protocol has undergone audits by MixBytes and Blocksec, with the aim of preventing vulnerabilities in advance.

Regulatory alignment: On the regulatory front, Aave has introduced institution-focused real-time transaction monitoring and AI-driven KYC systems that comply with FATF AML guidelines. EtherFi has partnered with ETH Strategy, a DAT, to offer KYC-compliant restaking solutions that allow institutions to meet internal control requirements while participating in DeFi.

These security and compliance enhancements are elevating the Ethereum DeFi ecosystem toward an institutional-grade financial infrastructure. As a result, institutional investors have begun to move beyond spot ETH holdings and explore new yield opportunities enabled by Ethereum’s programmability.

As the foundation for institutional investors to enter the DeFi ecosystem is being established, Ethereum and DeFi projects recognize that institutional capital will become a driver of future growth. Accordingly, they are moving beyond simply attracting capital and toward maximizing the retention and circulation(flow) of capital that enters the Ethereum ecosystem.

L1/L2 scalability upgrades

In Mar 2024, the Dencun upgrade introduced proto-danksharding(EIP-4844) and applied a blob-based data structure, which significantly reduced data availability costs. The subsequent Pectra upgrade doubled blob capacity, further reinforcing L2 fee-reduction effects.

The Fusaka upgrade, scheduled for Dec 2025, plans to apply PeerDAS(Peer-to-Peer Data Availability Sampling) to increase the efficiency of data sampling and further reduce rollup costs. This series of scalability improvements aims to equip the Ethereum network with global-level throughput and build a foundation for institution-grade DeFi platforms to operate reliably.

Source: institutions.ethereum.org

Ethereum for institutions

To promote institutional adoption, the Ethereum Foundation has begun organizing dedicated strategies and creating specialized channels to execute them:

Launch of an institutional gateway: At the end of Jan 2025, the Ethereum Foundation opened an official website for institutional investors that provides comprehensive guidance on security architecture, privacy technologies, L2 scalability, and use cases for RWA, stablecoins, and DeFi. It particularly highlights examples from BlackRock, Visa, and Coinbase, helping institutions understand Ethereum as an on-chain financial infrastructure.

The Trillion-Dollar Security Initiative: A plan to achieve a level of security capable of supporting assets worth trillions of dollars, focusing not only on technical robustness at the protocol level but also on improving wallet usability and security. This is intended to strengthen the trust foundation required by institutional capital.

Etherealize: An organization that works closely with the Ethereum Foundation and oversees institutional products and marketing functions. Drawing on TradFi experience, it serves as a bridge between Wall Street and Ethereum. It develops institution-tailored technical solutions such as tokenization and privacy infrastructure, and conducts research and business development activities that redefine Ethereum as a cash-flow-generating asset, thereby facilitating institutional capital inflow.

Aave

Through its V4 upgrade in Q4 2025, Aave introduced a hub-and-spoke liquidity model and integrated Chainlink’s Automated Compliance Engine (ACE), while also forming a partnership with Maple Finance to connect institutional assets to the $40B DeFi lending market. This model enables efficient allocation of institutional capital and promotes long-term capital onboarding through RWA expansion.

Additionally, Aave launched the Horizon platform, which allows institutions or qualified users to borrow stablecoins using tokenized RWAs as collateral. Horizon is designed to meet regulatory requirements such as KYC, AML, and reporting obligations imposed by agencies like the SEC, making it a bridge that enables ETFs or DATs to utilize DeFi while minimizing legal risk.

EtherFi

With a Q3 2025 upgrade, EtherFi strengthened institution-grade ETH staking and approved a $50M ETH buyback program. Its integration with FalconX allows it to act as a bridge between DeFi and traditional finance. This supports stable institutional inflows and accelerates yield generation through liquid staking and restaking.

EtherFi is also partnering with Linea, EigenCloud, and Anchorage Digital to deploy $200M of institutional ETH from SharpLink, positioning EtherFi as a key staking solution for SharpLink’s ETH.

mETH Protocol

Through its partnership with Republic Technologies, mETH Protocol established itself as the first liquid staking platform selected by a publicly traded corporation’s treasury. CopperHQ’s custody support enables institutions to safely capture native mETH yields, and integration with the major exchange Bybit improves institutional access and convenience. With its cmETH product, which provides additional restaking yield, institutions can maximize capital efficiency and returns within mETH Protocol’s institution-oriented DeFi services.

EigenCloud

EigenCloud leverages restaking mechanisms to strengthen Ethereum’s security while offering institutions additional yield opportunities, taking an active role in attracting institutional capital. As noted earlier, it secured the $200M ETH deployment from SharpLink, establishing itself as a central hub for institutional ETH capital.

In Nov 2025, EigenCloud also formed a data partnership with Token Terminal, providing standardized metrics to institutional investors and improving transparency. Its integration with Linea, incorporating EigenDA and enhancing scalability, further reinforces the stability expected of institution-grade infrastructure.

As institution-focused capital pipelines start operating in earnest and institutional funds begin to flow in, Ethereum, the DeFi ecosystem, and existing retail investors are all likely to experience structural changes in multiple dimensions.

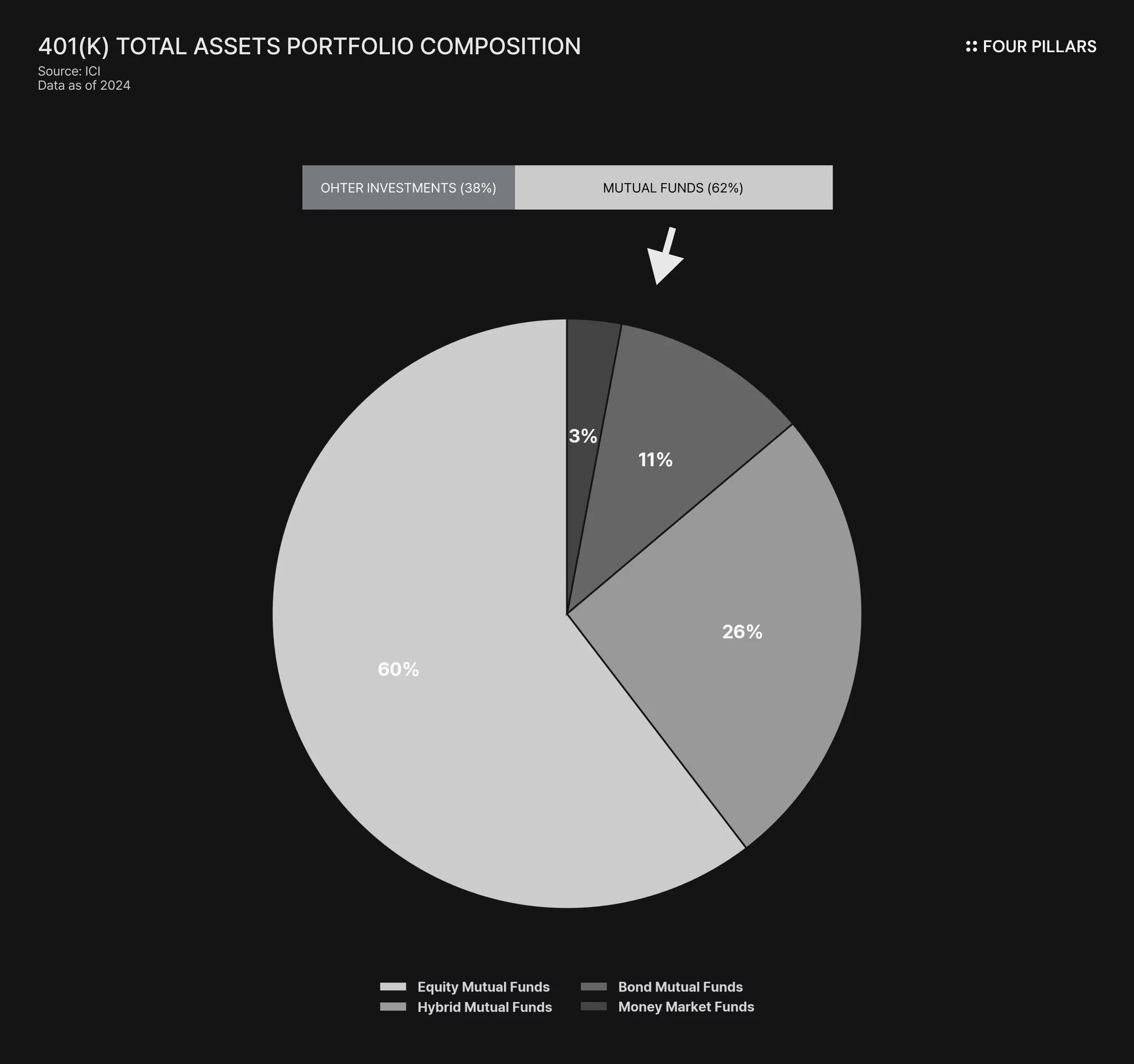

The 2025 executive order(EO) by the Trump administration that allowed approximately $9.3T in 401(k) plan assets to be used for cryptocurrency investment served as a starting gun for large-scale institutional inflows that are on a completely different level from retail capital. In particular, the DCA(dollar-cost averaging) structure, in which a portion of salaries is regularly invested, implies long-term and stable capital inflows into the crypto market and creates a strong virtuous cycle for the Ethereum ecosystem.

Market stability and improved credibility: Large-scale ETH purchases and long-term holdings by institutions reduce market volatility and turn Ethereum into a more mature asset. This boosts retail investors’ confidence in holding Ethereum long term, while the expansion of products such as ETFs increases regulatory clarity and strengthens overall market trust.

Stronger Ethereum security and more efficient DeFi: Institutional participation in staking enhances the security of the Ethereum network, and large-scale liquidity provision to DeFi protocols reduces trading slippage, thereby offering lower trading costs and higher liquidity to retail users.

Increased accessibility: Institutional participation in DeFi elevates Ethereum to the level of a mainstream financial asset and provides retail investors with indirect exposure opportunities. Access via ETFs or institution-focused platforms has an educational benefit for novice DeFi investors, and institutional participation in the market brings higher-quality data and research materials to the space.

That said, several challenges remain to be addressed:

Declining yields: As institutional capital flows in, yields across DeFi are gradually falling. As a result, the risk-adjusted return profile may become less attractive, and continued efforts will be needed to connect real-world assets(RWA) on-chain to compensate for this.

Centralization risk: Concerns about centralization are growing as staked ETH becomes concentrated on large platforms such as Lido. Vitalik Buterin has also pointed out this issue, and if large institutional capital concentrates on specific platforms for reasons of stability, Ethereum’s decentralization could be weakened. To mitigate this, it will be necessary to design incentives that encourage diversification among staking platforms and to intentionally distribute DeFi market share so that institutional investors are guided toward building diversified staking portfolios.

Even so, institutional love for Ethereum is unlikely to fade easily. This is because the US Department of Labor(DOL) is recognizing crypto as a neutral asset and is expanding access for various types of institutional capital, including not only 401(k) but also pension funds and university endowments.

For example, the Michigan state pension system(MSRS), which manages around $100B, increased its direct Ethereum exposure by holding 460K shares(about $9.6M) of the Grayscale ETH Trust(ETHE) in early 2025. In addition, the Wisconsin State Investment Board(WSIB), which manages about $150B, realized roughly $200M in profit from crypto fund investments in 2024, and on the back of SEC approval of liquid staking, announced plans to allocate around 5% of its fund to RWA and DeFi by 2026.

If this kind of regulatory alignment with traditional finance and further technological trust-building continues, institutional love calls for Ethereum will likely persist into 2026. Institutions will no longer treat the Ethereum they previously held only in spot form as ‘Dead Money’, but will instead use it as ‘Active Money’ that generates continuous derivative returns. This shift will translate into stronger security for the Ethereum network and improved capital efficiency across DeFi. As a result, retail investors will benefit from a better environment in terms of Ethereum’s value stability and the transactional efficiency of DeFi.

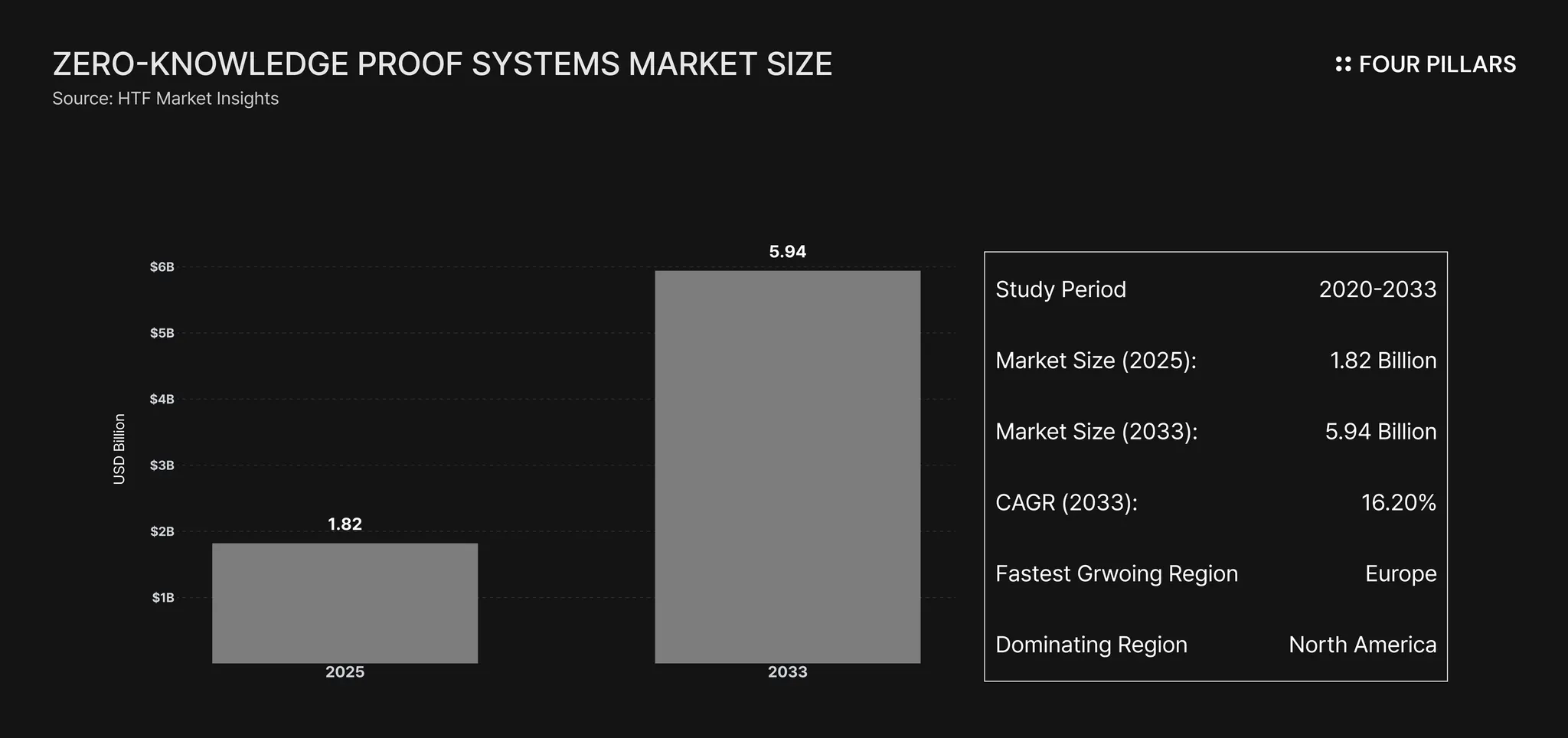

Currently, zero-knowledge (ZK) technology is still in a pre-industrial phase before establishing itself as an independent ecosystem, and it remains in a transitional period where it is heavily dependent on blockchain. The market size is estimated at about $1.8B as of 2025, which is less than 1% of the global IT infrastructure market.

Up to now, demand has been almost entirely concentrated in ZK-rollups for scaling Ethereum L2. In contrast, the share of ZK usage in application or infrastructure domains is so low that it is statistically insignificant. This shows that ZK technology is still used primarily as an auxiliary tool to improve blockchain performance rather than as a standalone industry.

However, outside of blockchain, several experimental attempts are emerging. Digital identity (DID), privacy-preserving financial use cases, and AI model verification (zkML) demonstrate that the data privacy and verification capabilities of ZKPs can be applied beyond blockchain. Still, several challenges remain before these attempts can evolve into broader industrial adoption.

Source: American Experiment

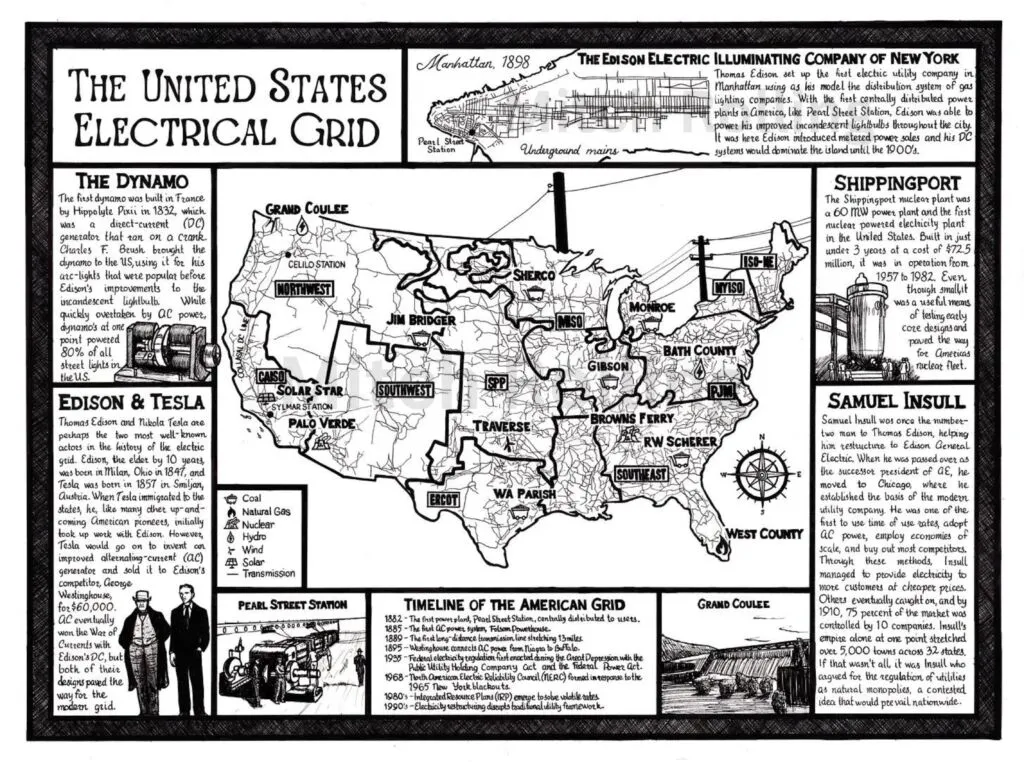

In the early 19th century, electricity was a technology that had not yet left the laboratory. Two stages were required for Michael Faraday’s discovery to become an industry.

First, ‘Infrastructure’ had to be built. Before Edison, Tesla, and Westinghouse constructed the electrical grid connecting power plants, transmission lines, and transformers, factories operated their own generators, and electricity remained inefficient. Once the grid was established, anyone could access electricity simply by plugging into an outlet, and electricity became a broadly useful resource that significantly boosted productivity.

Second was the formation of an ‘Economic Structure’. With the introduction of electric meters on top of the grid, producers and consumers became distinct entities, and a utility market emerged in which users paid based on consumption. This structure enabled factories to abandon self-generation and choose efficient centralized power.

Today, ZK technology is at a point similar to the transition from the era of self-generation to the era of the electrical grid. The universal infrastructure that allows anyone to execute complex cryptographic circuits easily, the ZK virtual machine (zkVM), is advancing rapidly, and an economic structure for buying and selling proving and verification computation is beginning to form on top of it.

Just as the electrical grid turned electricity into a general-purpose energy resource, zkVMs expanded ZK technology from a domain reserved for specialists into a general-purpose computing environment. Previously, each application needed to design its own dedicated ‘circuit’, but thanks to zkVMs, developers can now write code in general-purpose programming languages such as Rust or C++, and the zkVM automatically converts it into a proof-friendly form. This can be viewed as the emergence of standard infrastructure that significantly lowers the barrier to entry.

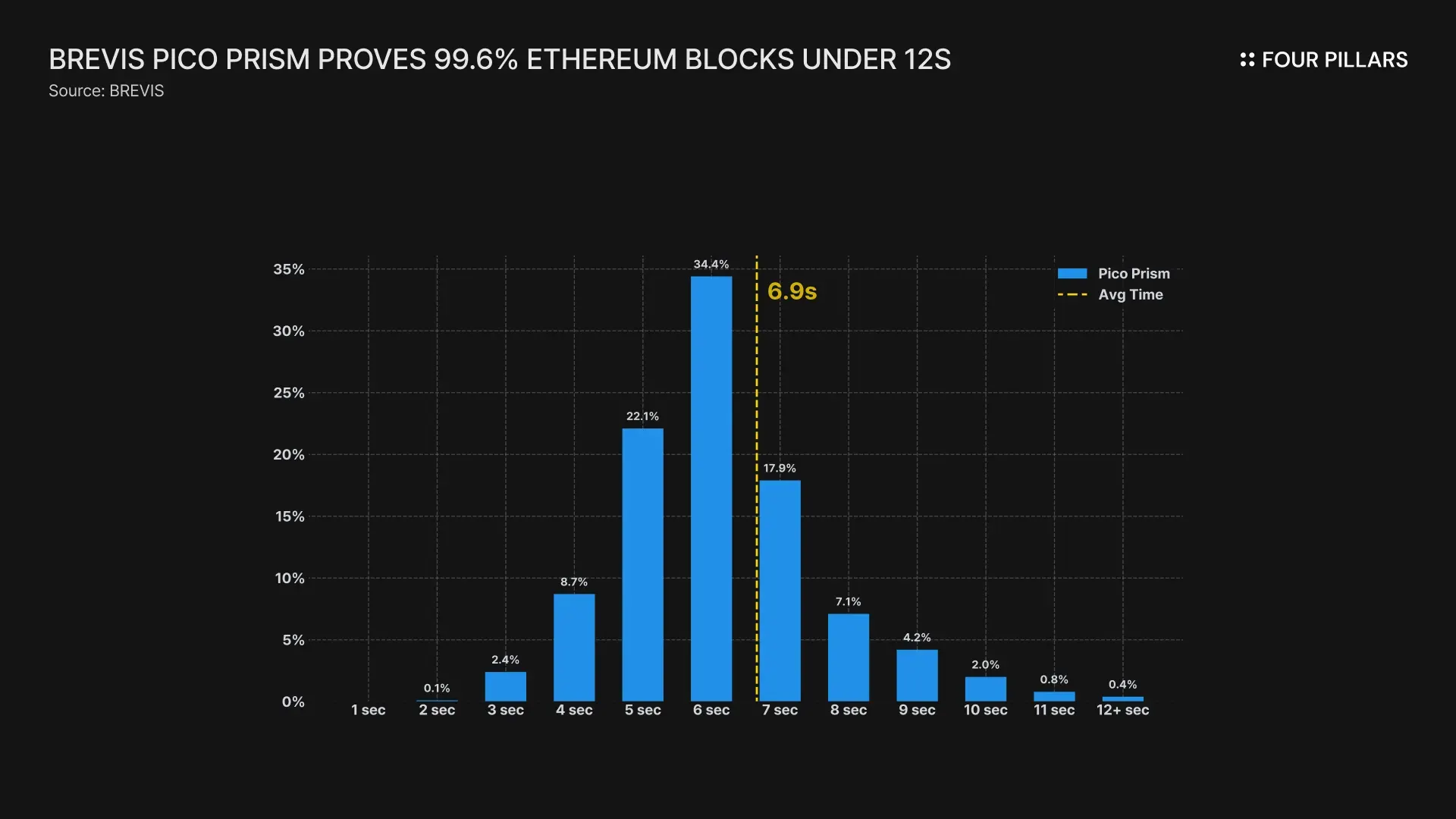

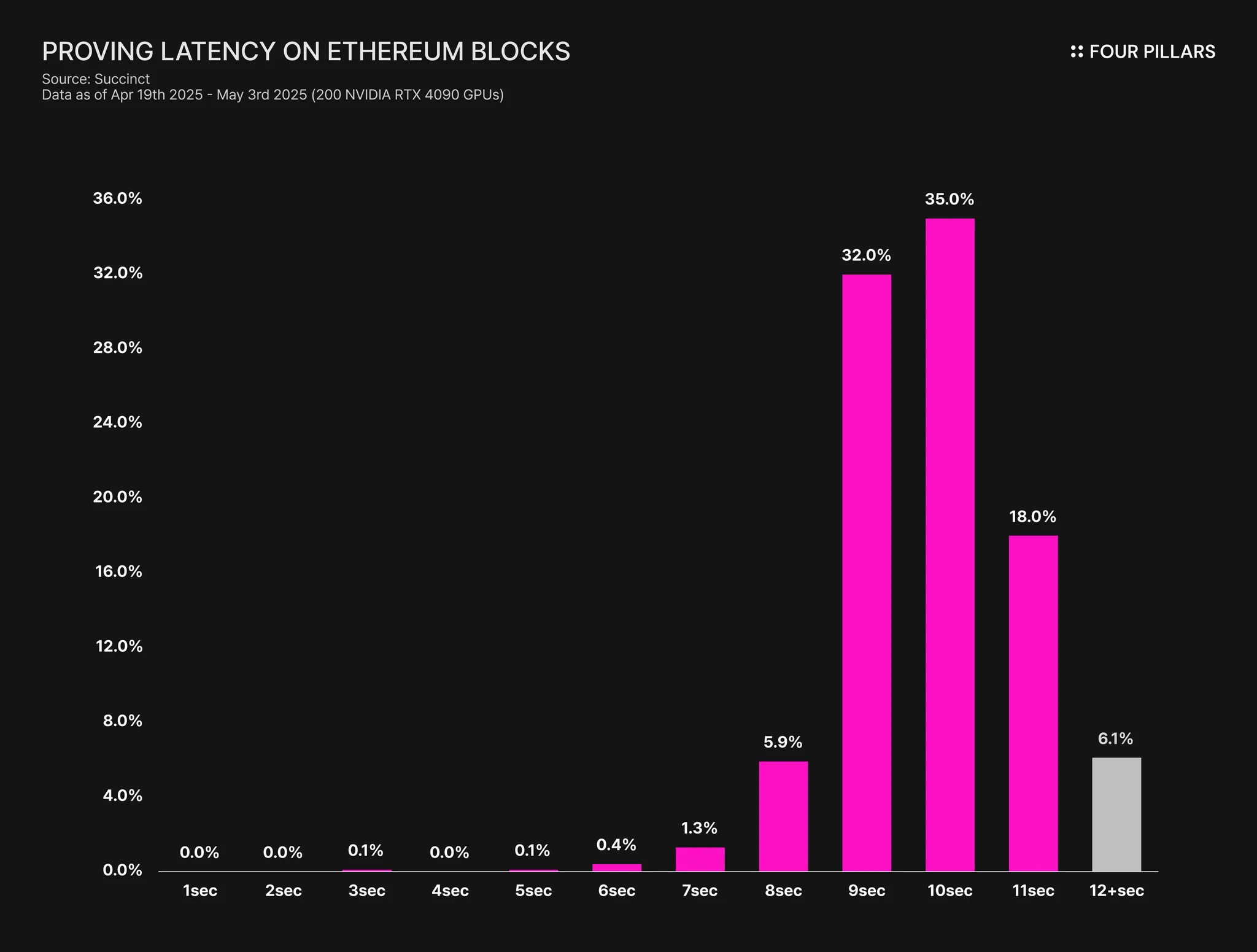

In addition, technology tends to advance faster when competition intensifies. What accelerated this trend was the release of the Ethereum Foundation’s Real-Time Proving (RTP) benchmark in July 2025. The Foundation presented six concrete guidelines, including “prove an Ethereum block in under 10 secs for more than 99% of blocks” and “total cost must remain under $100K.” This benchmark became a key indicator for assessing whether zkVMs can keep pace with actual blockchain network throughput, pushing major zkVM projects into a race to meet these criteria.

Pico Prism made by Brevis

Brevis’s Pico Prism currently stands out the most in terms of speed and efficiency. Using 64 RTX 5090 GPUs, it proves 99.6% of a 45M gas Ethereum block in an average of 6.9 secs, delivering the closest performance to the Ethereum Foundation’s RTP benchmark. Pico Prism aims for a new era of home proving in which individuals can generate proofs at home by improving cost efficiency, and its modular architecture targets verifiable AI and intelligent DeFi applications.

SP1 Hypercube made by Succinct

Succinct’s SP1 Hypercube is a new model that enhances the internal performance of the SP1 framework already officially adopted by major rollups such as Arbitrum and Mantle. It proves about 93% of Ethereum blocks within 12 secs and approaches the RTP benchmark. Through collaboration with Nethermind Security, it has also completed ‘formal verification’, securing a level of reliability suitable for financial-grade infrastructure.

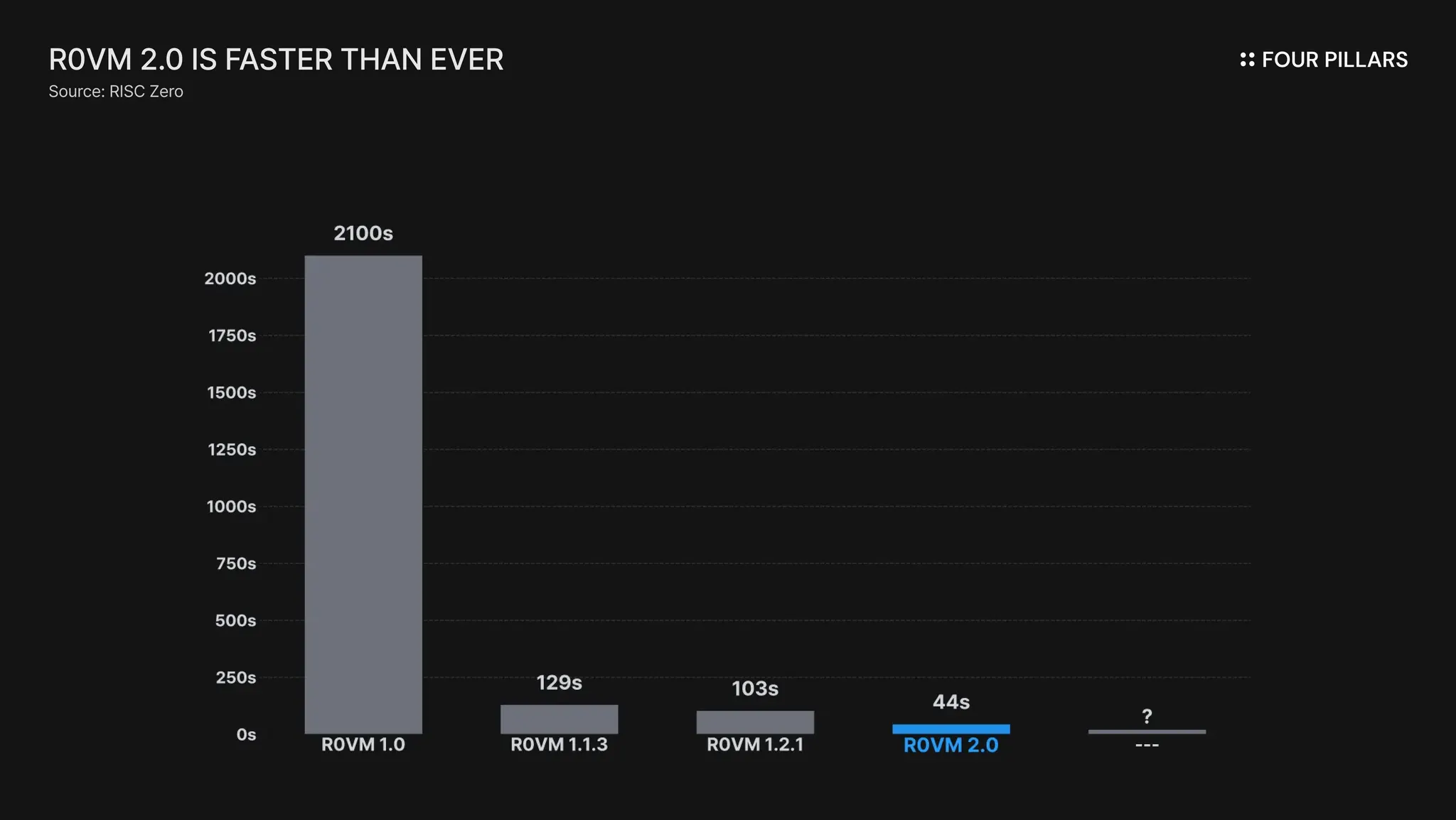

R0VM 2.0 made by RISC Zero

RISC Zero, an early pioneer of zkVMs, strengthened efficiency and scalability in R0VM 2.0. It improved memory efficiency by a factor of fifteen and reduced proving costs by a factor of five compared to the previous version, enabling economical operation even in environments requiring large-scale computation. It also expanded the memory limit to 3GB, making it possible to prove complex programs that were previously infeasible.

As zkVM infrastructure begins to take shape, a proving and verification market is emerging to allocate computational resources efficiently. No matter how advanced the infrastructure is, it cannot industrialize without economic efficiency, so proving and verification are beginning to function as assets and units of exchange.

Prover Network

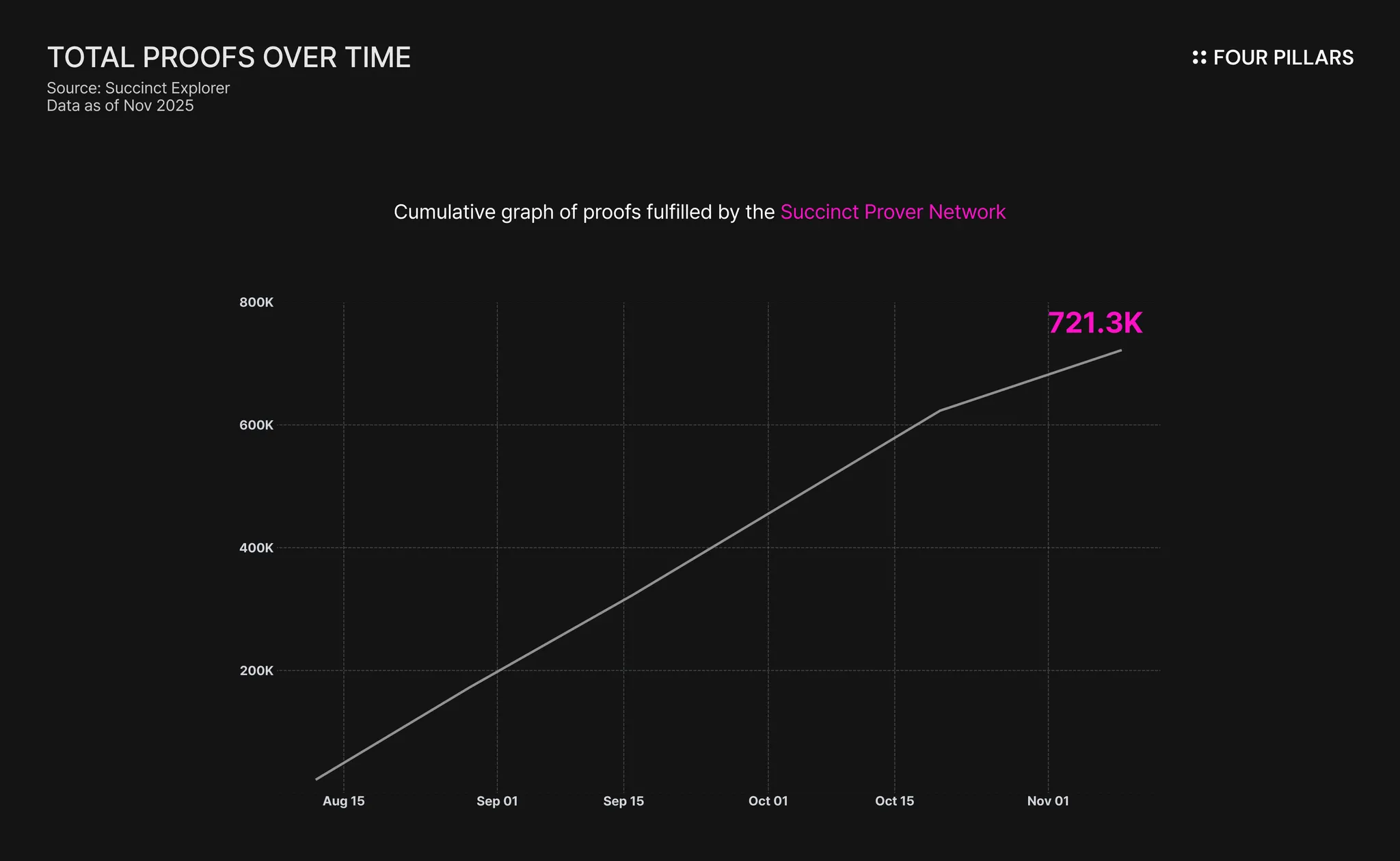

Proving requires high-performance GPUs, which entail substantial fixed costs. To resolve this cost burden, a two-sided market is growing in which external participants provide idle GPU resources and earn rewards without needing to own high-end hardware themselves. A proving cloud structure is forming in which users can borrow global GPU cluster capacity with just a few clicks. From the second half of 2025, this market began showing significant traction.

Succinct Prover Network: Based on the SP1 infrastructure, this network has grown rapidly since launching on mainnet in Aug 2025. Through a ‘proving contest’ mechanism, the prover offering the most efficient price and speed is selected for each task. As of Nov 2025, it has processed more than 720K proofs in total.

Boundless: Built on the RISC Zero zkVM, Boundless launched its mainnet on the Base chain in Sep 2025. It adopted ‘PoVW (Proof of Verifiable Work)’, which performs useful proof computation instead of meaningless hash work. Within two months of launch, more than 2,700 provers participated and over 1.56M requests were processed. This indicates the establishment of an open market where even small and mid-sized provers can contribute to the ecosystem through $ZKC incentives.

Verifier Network

Specialized layers are also appearing that bundle large numbers of proofs to reduce verification costs when verifying on relatively slow or expensive blockchains such as Ethereum mainnet.

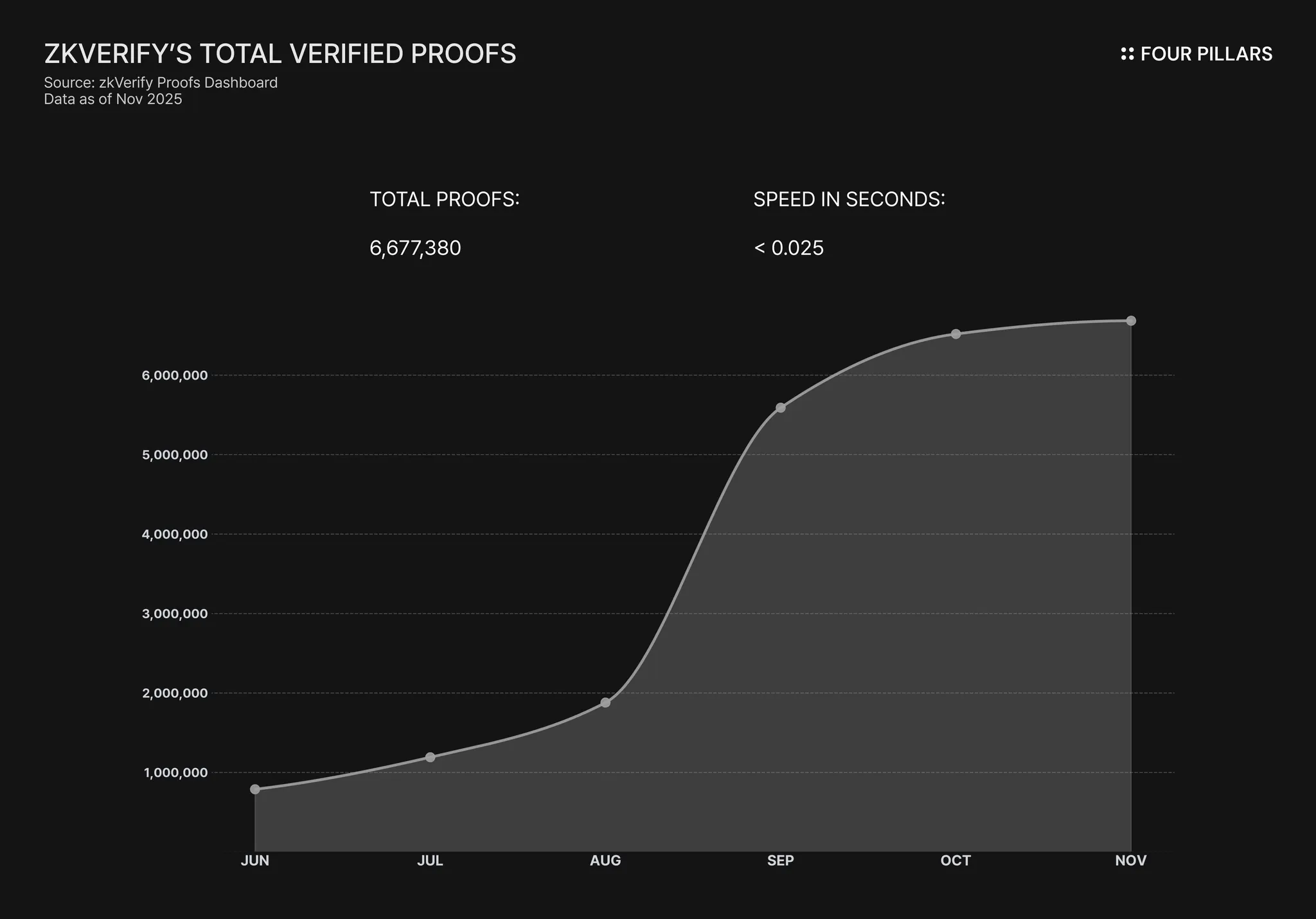

zkVerify: A L1 blockchain specialized for ZKP verification. It aggregates thousands of individual proofs into a single aggregated proof and submits it to Ethereum, reducing gas costs by more than 90% compared with conventional methods and providing sub-second verification latency. After completing more than 6M verifications on testnet, it launched mainnet in Sep 2025 and is currently expanding as a general-purpose verification layer with partnerships involving more than forty networks.

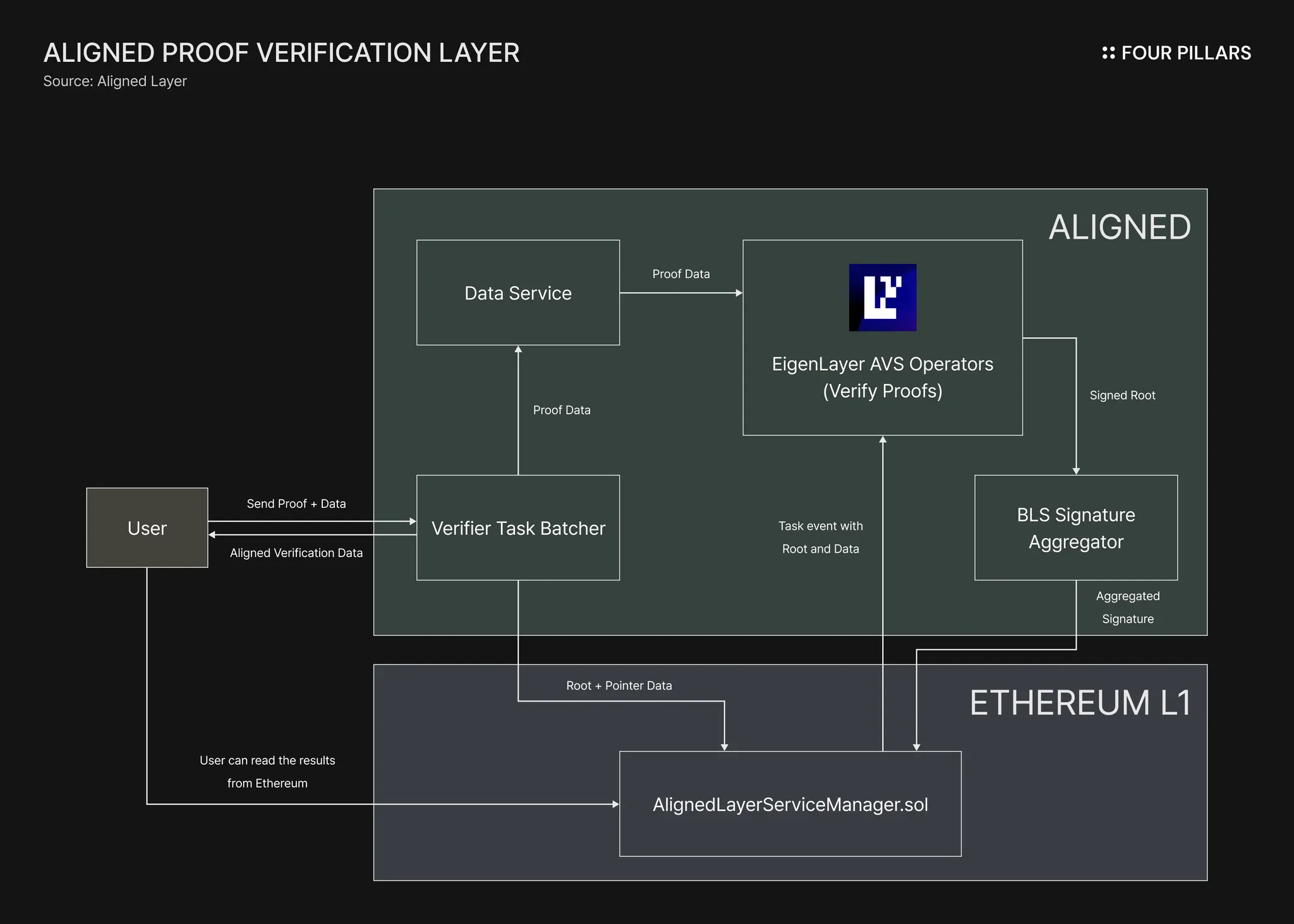

Aligned Layer: A ZKP verification layer running as an EigenLayer AVS, aiming to process ZKPs on Ethereum mainnet quickly and cheaply at around 250K gas. By using proof aggregation services to process thousands of proofs at once, it mitigates gas-limit constraints. Supporting multiple ZK systems (SP1, RISC Zero, Groth16, etc.), it is growing quickly with more than forty partners based on general-purpose compatibility and a decentralized security model.

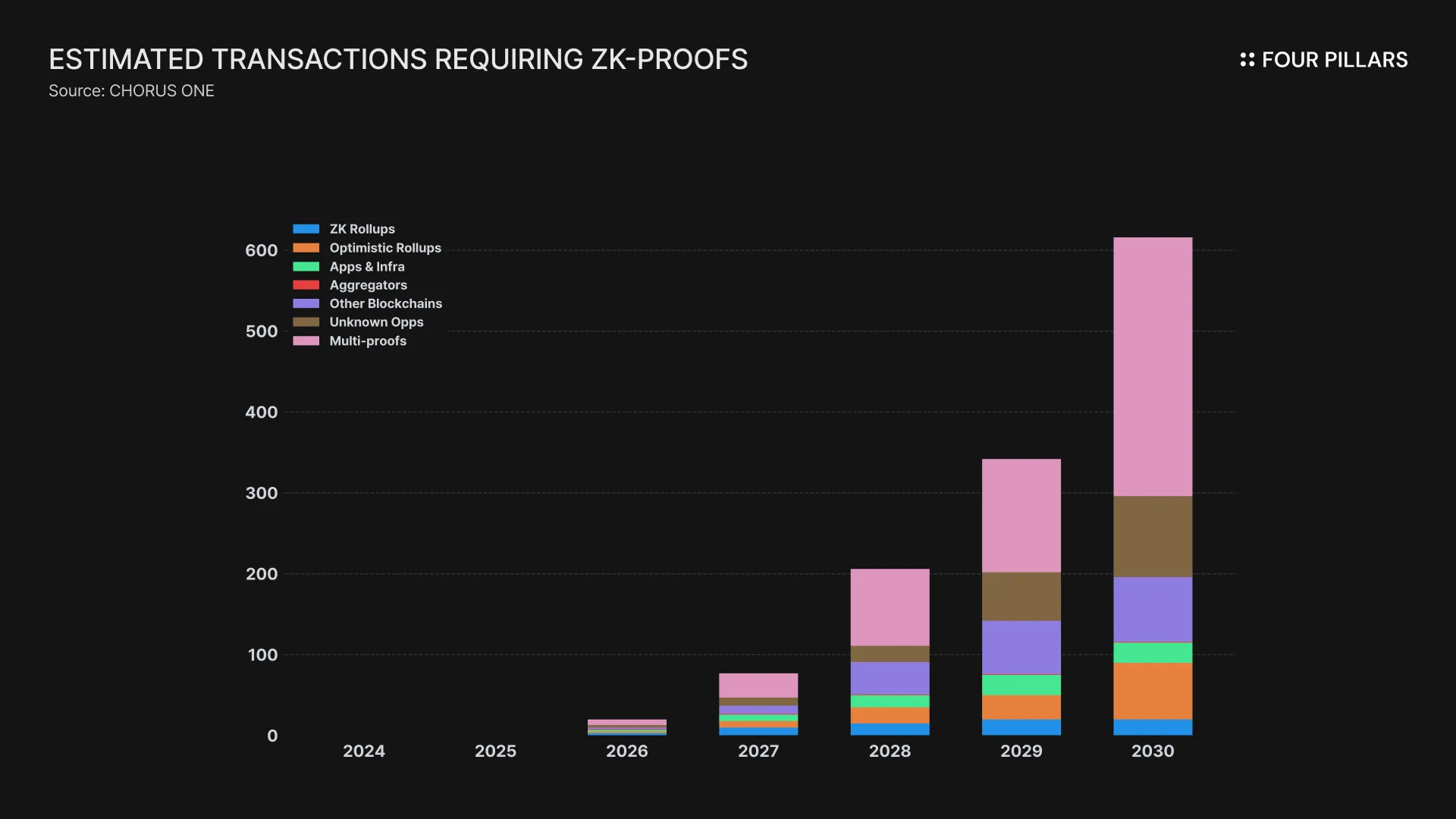

The growth potential of the ZK industry is not based on abstract expectations but on real and rapidly increasing demand. According to Chorus One, about 590M transactions requiring ZKPs occurred in 2024, and the number is projected to grow nearly 1,000 times to more than 600B by 2030.

This demand is not limited to blockchain. The ZK industry has high portability, meaning it can be applied in any sector where data reliability and privacy are important, including AI, traditional finance, and healthcare.

AI and ML: Recent zkML research is gaining momentum, highlighting ZK technology as a key tool for verifying that AI outputs have not been tampered with without revealing training data or model parameters.

Traditional finance: As illustrated by the EU’s EUDI Wallet and the Bank of Canada’s CBDC design report, ZKPs are being adopted as a privacy-preserving way to verify eligibility criteria without disclosing sensitive information such as account balances or credit scores.

Manufacturing and supply chain: As seen in the example of Teijin (Japan) and Circularise (Netherlands), ZKPs are used to verify carbon emissions and regulatory compliance for raw materials without disclosing proprietary corporate data.

This broad-based demand naturally connects to the advancement of ZK infrastructure (zkVMs) and economic structures (proving·verification markets). Handling hundreds of billions of proof and verification requests across diverse industries requires faster and cheaper general-purpose computing engines (zkVMs) and efficient markets for computational resources.

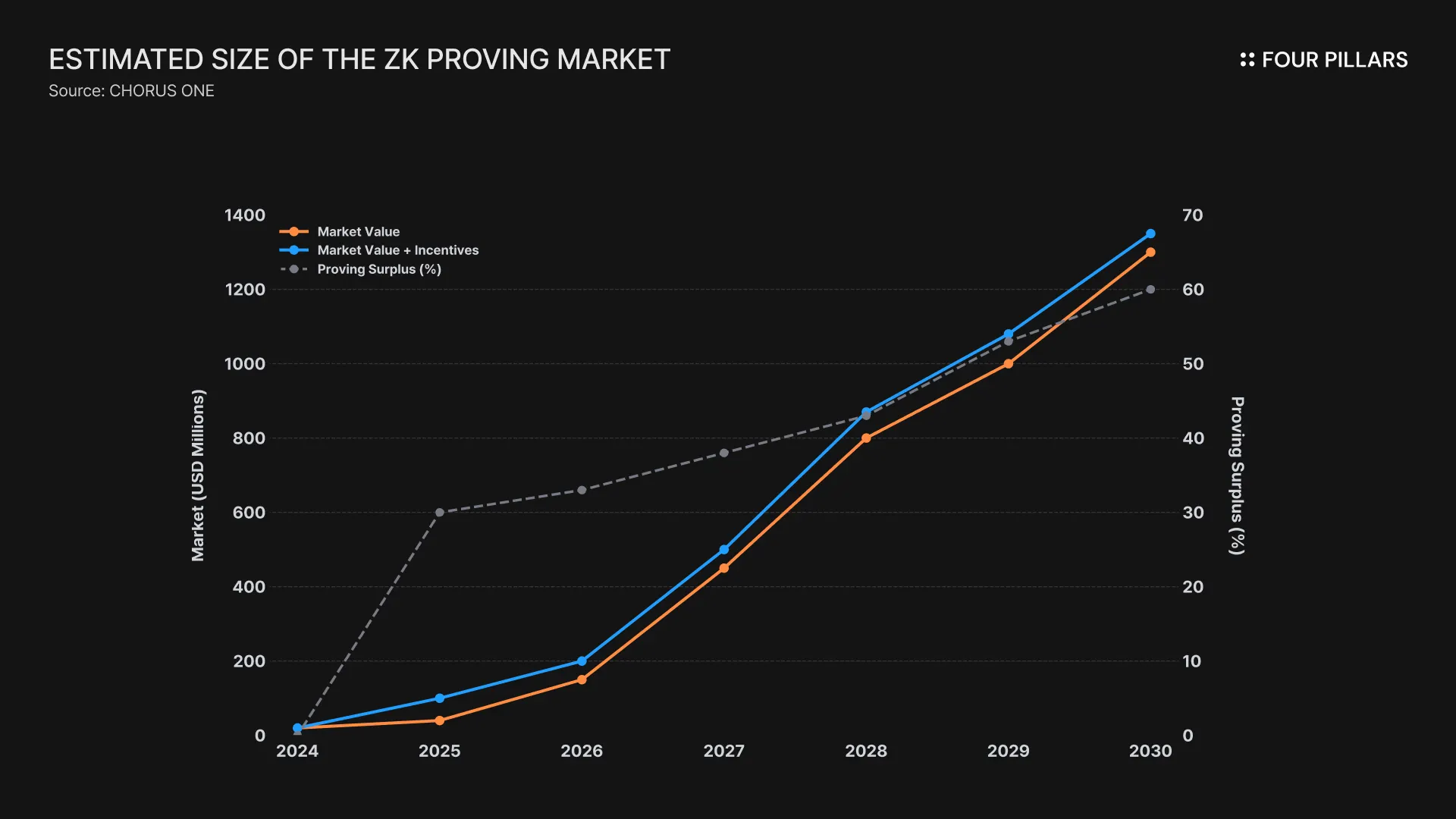

According to the Chorus One report, the proving and verification market is no longer a technical subcategory but is emerging as a new cryptoeconomic infrastructure alongside Bitcoin mining (PoW) and Ethereum staking (PoS). As of early 2025, annual staking rewards generated across major PoS chains are estimated at about $16.3B, and the fees captured by validators as infrastructure providers are roughly $800M.

In contrast, the ZK proving market is expected to grow from about $97M in 2025 to approximately $1.34B in 2030 at a compound annual growth rate of 68.6%. Compared with today’s PoS validation reward market, this is around 1.6 times larger. This implies that once ZK proving and verification infrastructure becomes firmly established, it may create earning opportunities similar to or greater than current PoS validation infrastructure, forming a third major pillar in cryptoeconomic systems.

As large-scale demand and capital enter the space, specialization will accelerate. To handle transaction volumes on the order of 600B per year, the proving market will inevitably consolidate around large-scale prover networks that provide high-performance GPU resources most efficiently. The verification market will likewise rely on specialized verification networks capable of processing vast numbers of proofs at low cost. Over the next 5 years, ZK technology is likely to evolve from mere software into a large-scale market for computational commodities.

The growth of zkVMs and proving and verification markets leads directly to stronger fundamentals across the entire ZK industry. An expanded proving market reduces infrastructure costs, and lower barriers to entry drive adoption in AI, finance, healthcare, and other sectors, creating strong positive feedback.

The OECD’s emphasis on the fusion of AI and privacy-enhancing technologies and the EU’s trend toward embedding ZK proofs as default components in digital ID design demonstrate that ZK technology is no longer optional. Once this positive feedback loop becomes fully established, ZK will transform from a tool used in specific industries into foundational infrastructure that supports all digital interactions. Just as HTTPS became the trust layer of the web, ZK technology will become the invisible backbone maintaining the integrity of all data.

Dive into 'Narratives' that will be important in the next year