Expansion of Non-Trading Revenue and Accelerated M&A Among CEX: The key growth indicator for exchanges is shifting from trading volume, which depends on retail sentiment, to non-trading revenue. Coinbase has restructured its income mix through staking, USDC revenue, and subscription memberships, and as of 2025 its non-trading lines account for nearly 40% of total revenue.

Strengthening non-trading revenue lines is a preparatory phase for exchanges as they expand into full financial service providers. To meet the horizontally expanded set of business requirements, exchanges are expected to pursue mergers, acquisitions, and strategic partnerships even more aggressively in 2026.

In-App DeFi and Exotic Yield: Neobanks must always maintain sufficient liquidity buffers to meet withdrawal and payment needs, and mainstream users are far less willing than DeFi farmers to tolerate high levels of risk. As a result, liability-driven asset management needs to become increasingly sophisticated, and securing highly stable and sustainable yield sources becomes a primary challenge.

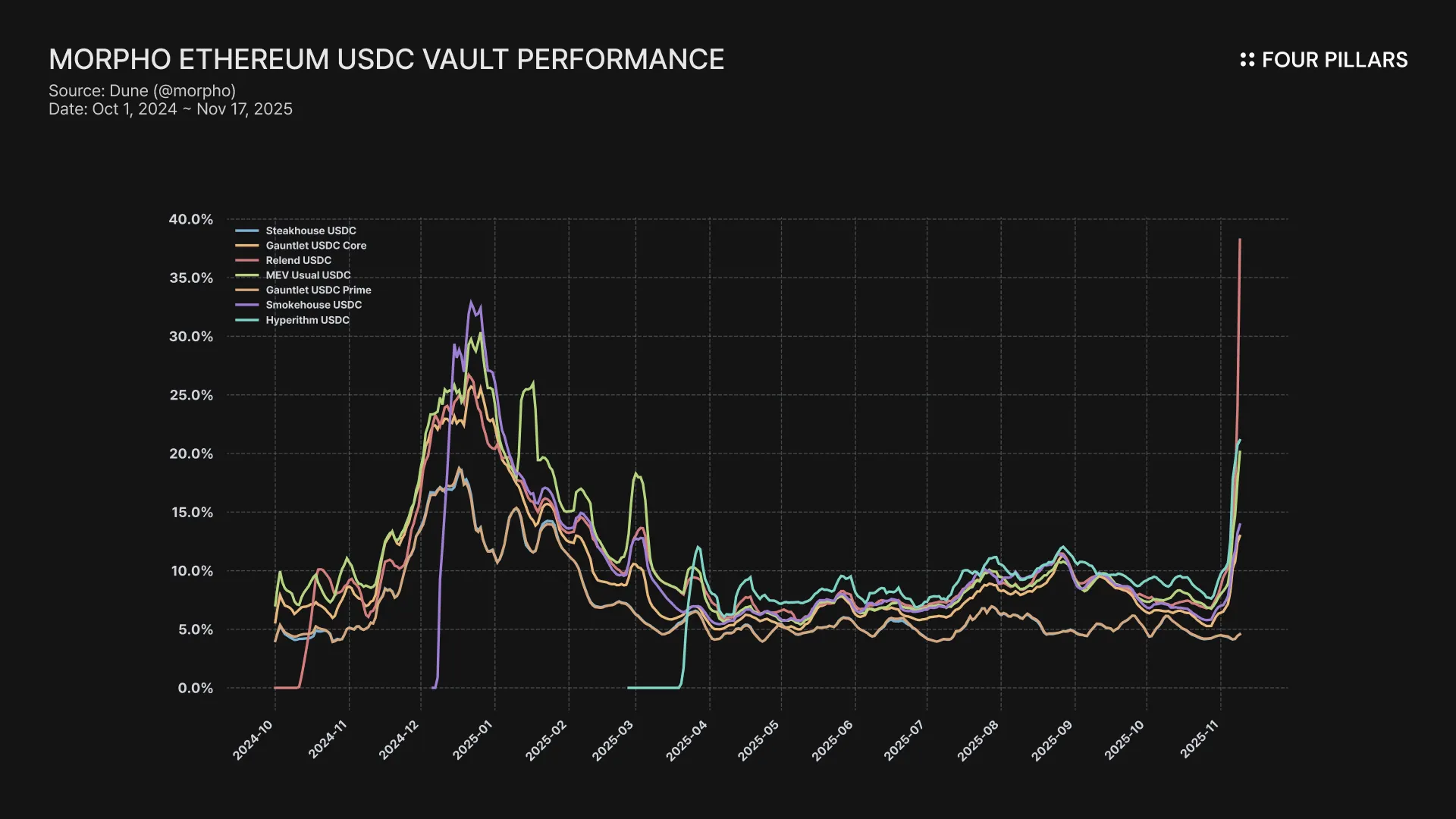

The stable yield band of existing DeFi income sources has compressed into the 4% to 8% range, and APYs are highly volatile because they depend on trading activity and borrowing demand in crypto markets based on onchain money markets. Within this environment, real cash flow based exotic yield-bearing assets are expected to gradually secure product-market fit.

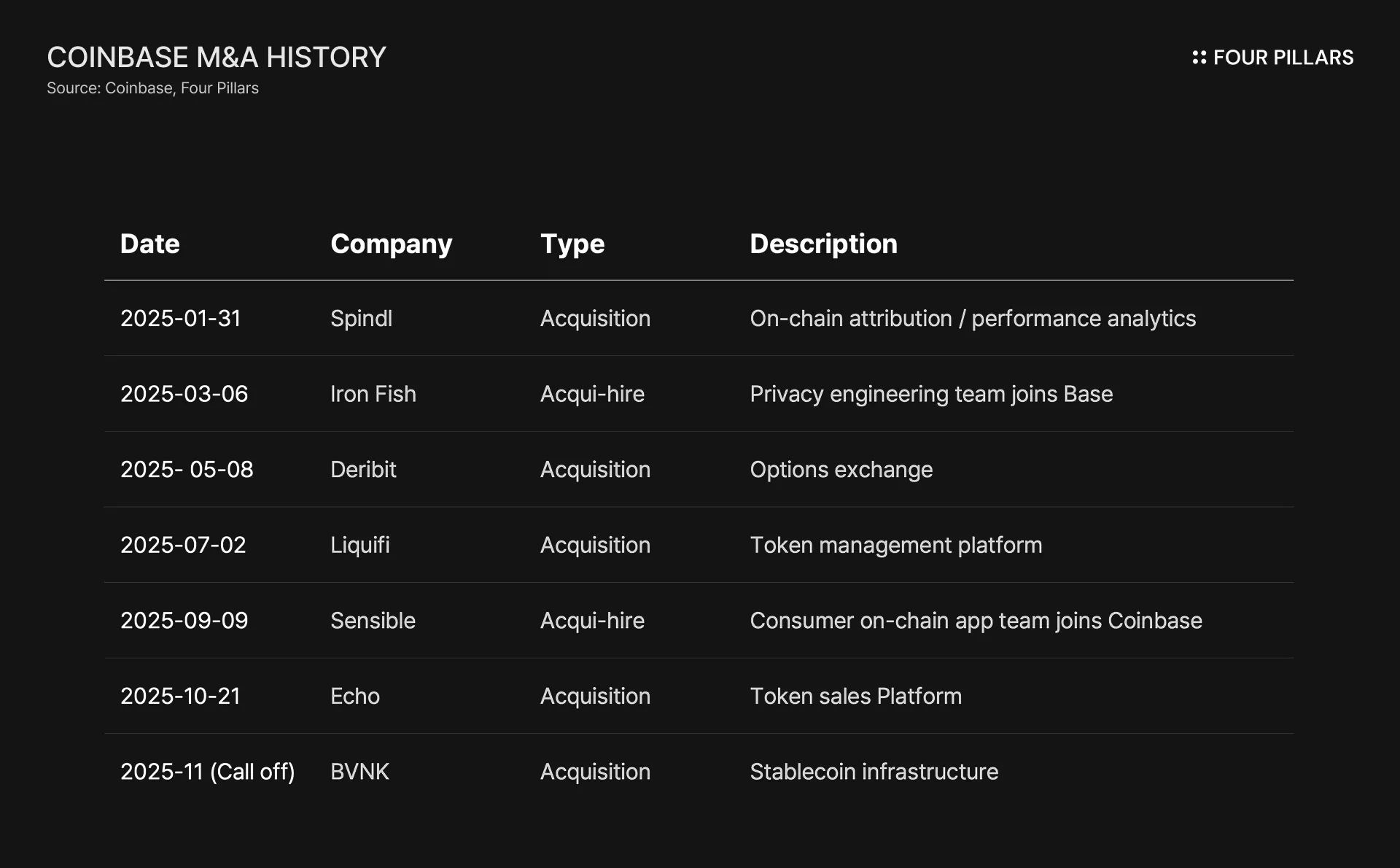

As stablecoins, tokenized securities, and neo-bank begin to replace traditional financial rails, CEX are positioned to become the core crypto-financial hubs in this transition. Coinbase’s acquisitions this year of Echo (ICO platform), Deribit (options exchange), and Liquifi (token management solution) illustrate how exchanges are pushing into new business domains at an accelerated pace. Through continued mergers and acquisitions, DeFi vault integrations, subscription-based memberships, and payment services, major CEXs are expected to broaden their product surface through next year.

At the core, these initiatives are all non-trading revenue lines. Spot and derivatives trading reached maturity long ago. They remain profitable but offer limited upside for future expansion. This makes non-trading revenue the most important indicator for measuring the growth trajectory of exchanges.

Efforts to replace traditional financial infrastructure are also taking place across crypto-native ecosystems. Even so, the player best positioned to drive this structural shift at scale remains the CEX.

Institutional capital onboarding: Major CEXs hold licenses that closely approximate traditional financial institutions. Coinbase maintains BitLicense, a Trust Charter, and MiCA-based CASP authorization, and it serves as custodian for Bitcoin and Ethereum ETFs issued by Fidelity and BlackRock. This demonstrates that CEXs meet institutional requirements for security and compliance and that they are the most reliable legacy platforms to absorb institutional inflows.

Interoperability: A frequently overlooked fact is that CEXs already function as hubs across most major networks including Ethereum-based chains, Solana, and Sui. Exchanges are the fastest to support new chains and new tokens and they continuously monitor token flows. The centralized, custodial key-management model can be criticized as a structural limitation. Yet compared to phishing attacks that compromise self-custody wallets or bridge failures that freeze funds, CEXs remain the most practical large-scale onboarding solution.

The boundary between onchain and offchain is also becoming less distinct. Exchanges are adopting interoperability infrastructure to improve operational efficiency. A notable example is Nodeit, a development arm under Dunamu, joining the LayerZero DVN. For OFT-based assets such as USDT0, which support movement across more than thirty chains, CEX participation in DVN verification allows them to roll out new networks at speed without altering existing infrastructure.

A single channel: Platforms such as Mantle’s UR and Coinbase’s Base App show how user experience is consolidating into unified interfaces where all financial activities can be executed in one place. Deep liquidity across hundreds of assets, KYC accounts, DeFi products, and payments can all be delivered through a single channel. At present, only CEXs possess the infrastructure to provide this full stack. As a result, they maintain clear advantages in user acquisition, psychological onboarding cost, and distribution compared to purely onchain products.

In summary, CEXs hold structural advantages in attracting users and institutional capital and in providing the infrastructure required for financial integration. The distinction between permissionless onchain systems and centralized offchain systems is becoming outdated. The chains, applications, and DeFi products operated by exchanges are evolving into tightly integrated environments where the boundaries have become harder to distinguish.

“In the next five or ten years, I think revenue from subscription and services could be 50% or more of our business. Things like staking, earning yield, debit cards, and institutional custody. these could become a much bigger portion of our revenue.”

— Brian Armstrong, Coinbase CEO, CNBC Interview (2021)

A clear indicator of where exchanges are heading, and one that will only matter more over time, is the rising share of non-trading revenue. The increase in non-trading income signals a move away from dependence on trading fees and demonstrates that exchanges are securing a stable and repeatable revenue base as full financial service providers. This trend mirrors what fintech firms such as Robinhood are pursuing as they add deposit products, subscription services, and prediction markets in order to diversify away from pure trading income.

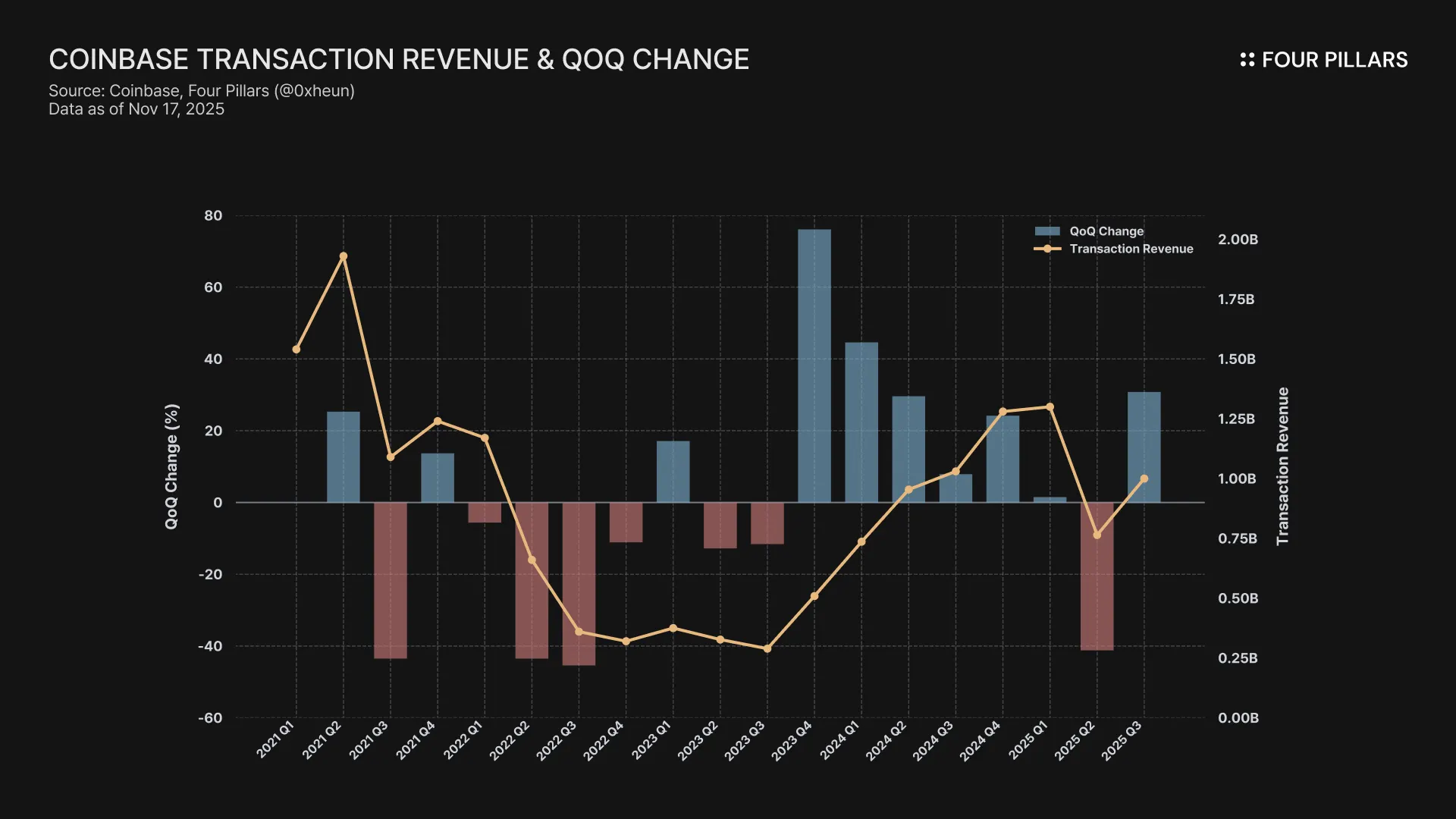

Historically, the high-margin engine of exchanges was retail trading fees. Retail trading volume is highly cyclical, and revenue deteriorates quickly in market downturns. The average QoQ change in trading revenue is approximately 27%, reflecting significant volatility that is largely driven by retail sentiment and market momentum. Reducing reliance on this unstable revenue source is an essential priority for exchanges.

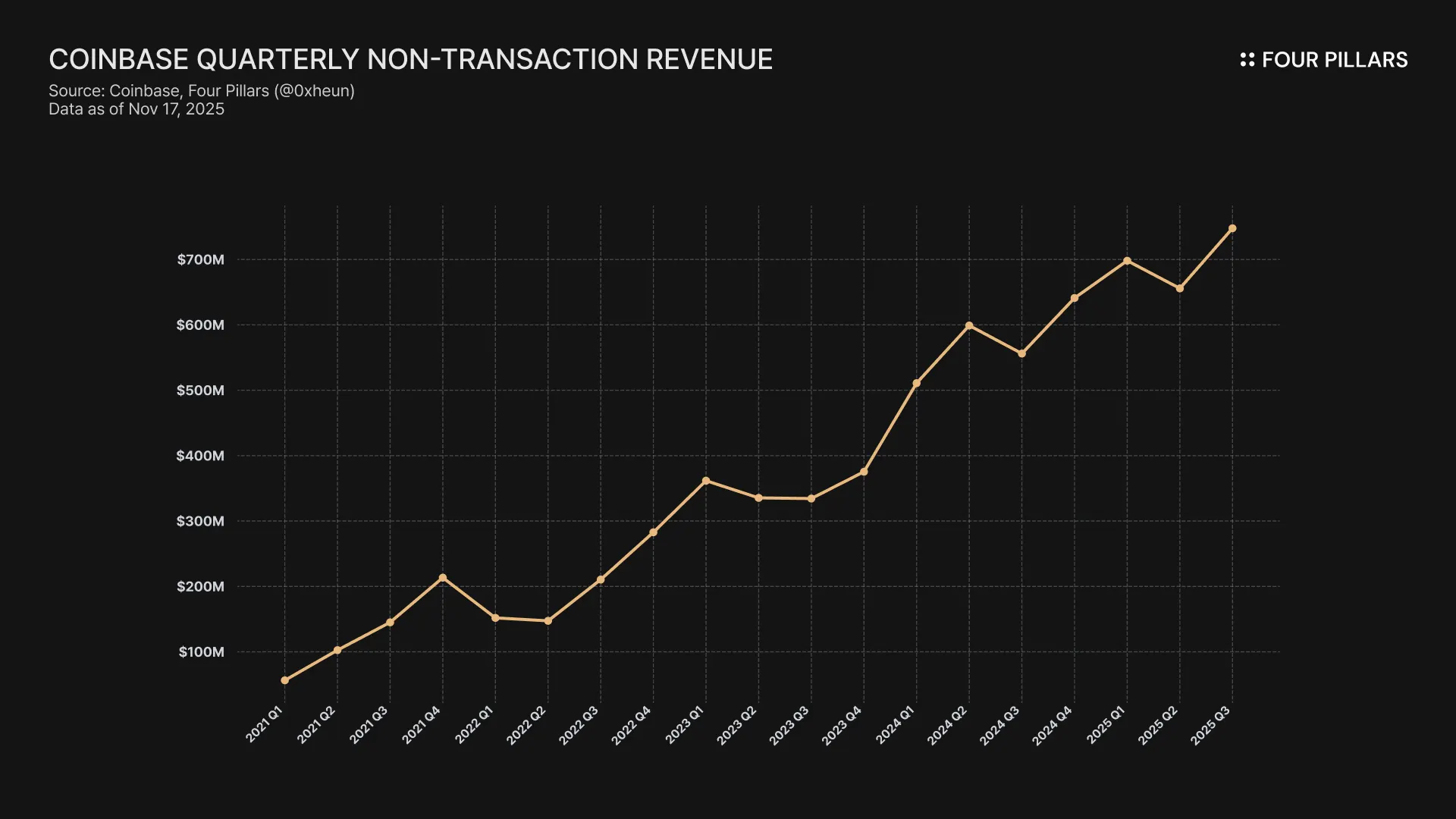

Over the past five years, Coinbase’s non-trading revenue has grown nearly thirteen-fold compared to Q1 2021, with a compound annual growth rate of roughly 77%. This performance reflects a deliberate strategy to move beyond a trading-centric model by securing reward program, scaling staking revenue, operating subscription services, etc.

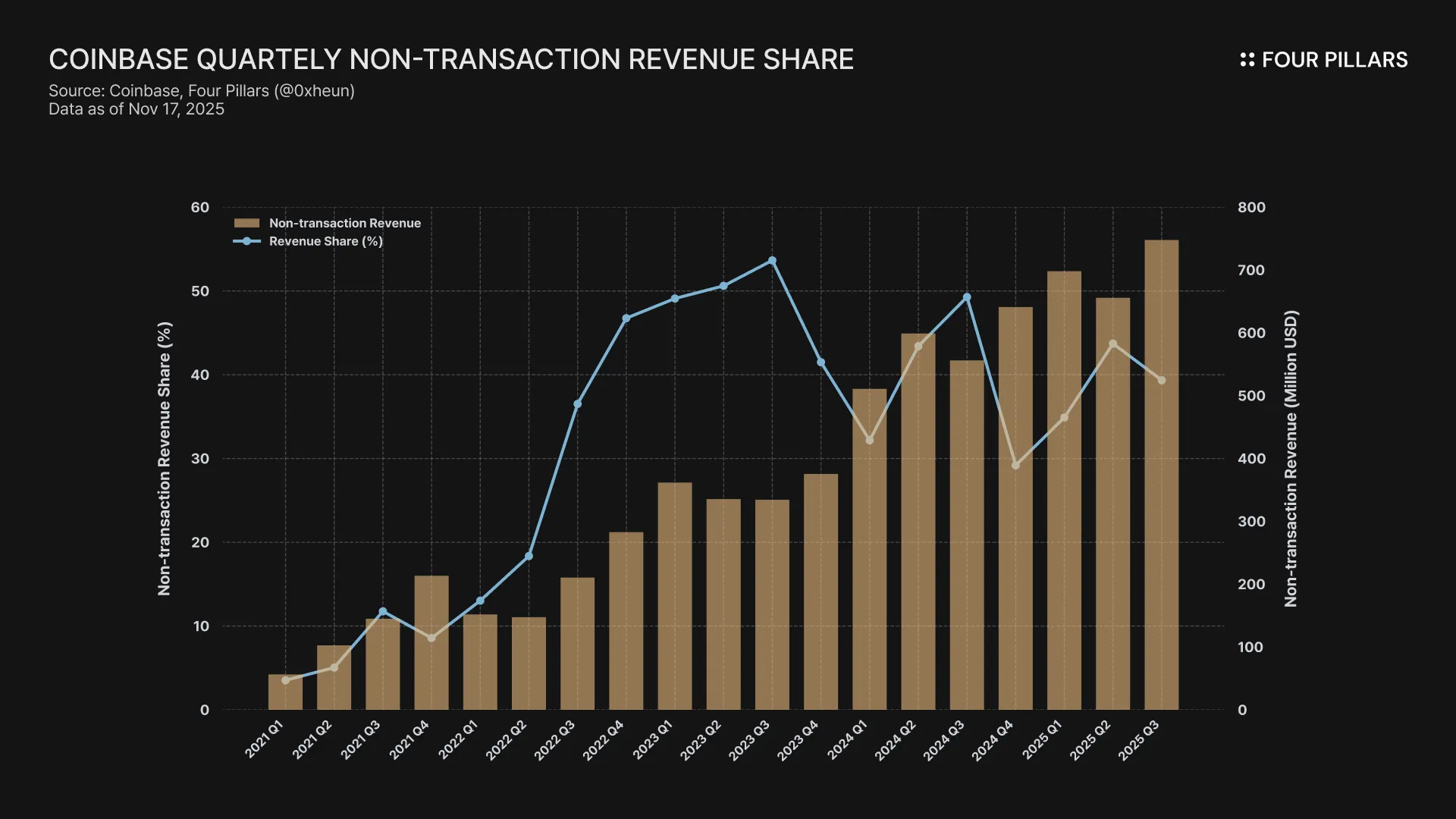

As a result, the share of non-trading revenue increased from 3% in 2021 to 39% in Q3 2025. Since the second half of 2022, non-trading revenue has consistently reached nearly half of total revenue, signaling a structural shift from a trading-led model to one anchored in financial services. As these lines mature, overall revenue volatility is expected to decline while recurring income from staking, custody fees, and USDC revenue becomes a more stable foundation for the business.

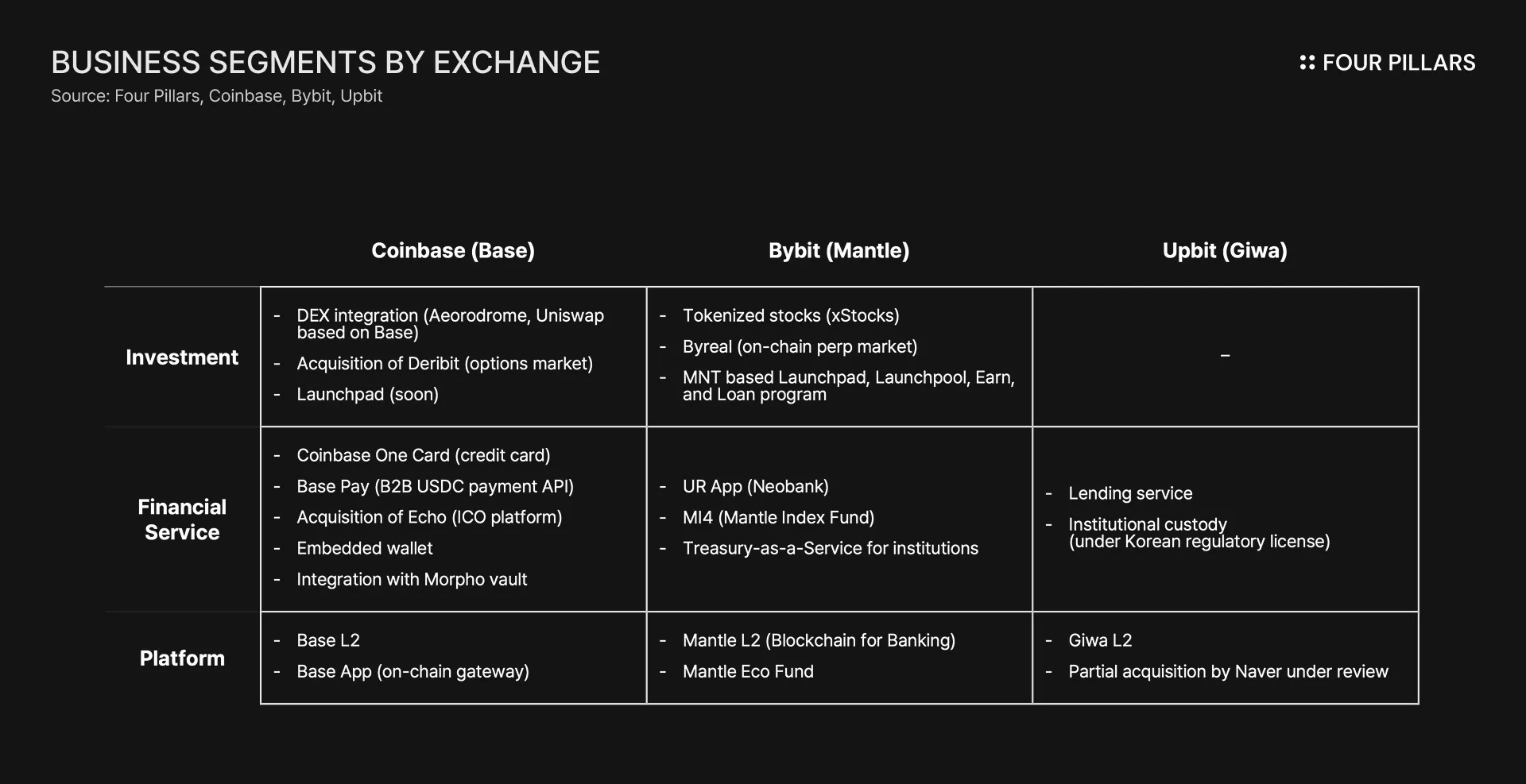

How are exchanges strengthening their non-trading revenue lines in practice? A closer look at three representative exchanges provides perspective. Coinbase leads the industry with institutional positioning and diversified financial services. Bybit has built a strong global presence as a borderless exchange. Upbit reflects the dynamics of a locally dominant player navigating the specific regulatory landscape of South Korea.

1.3.1 Coinbase: Becoming the Best Place to Use USDC

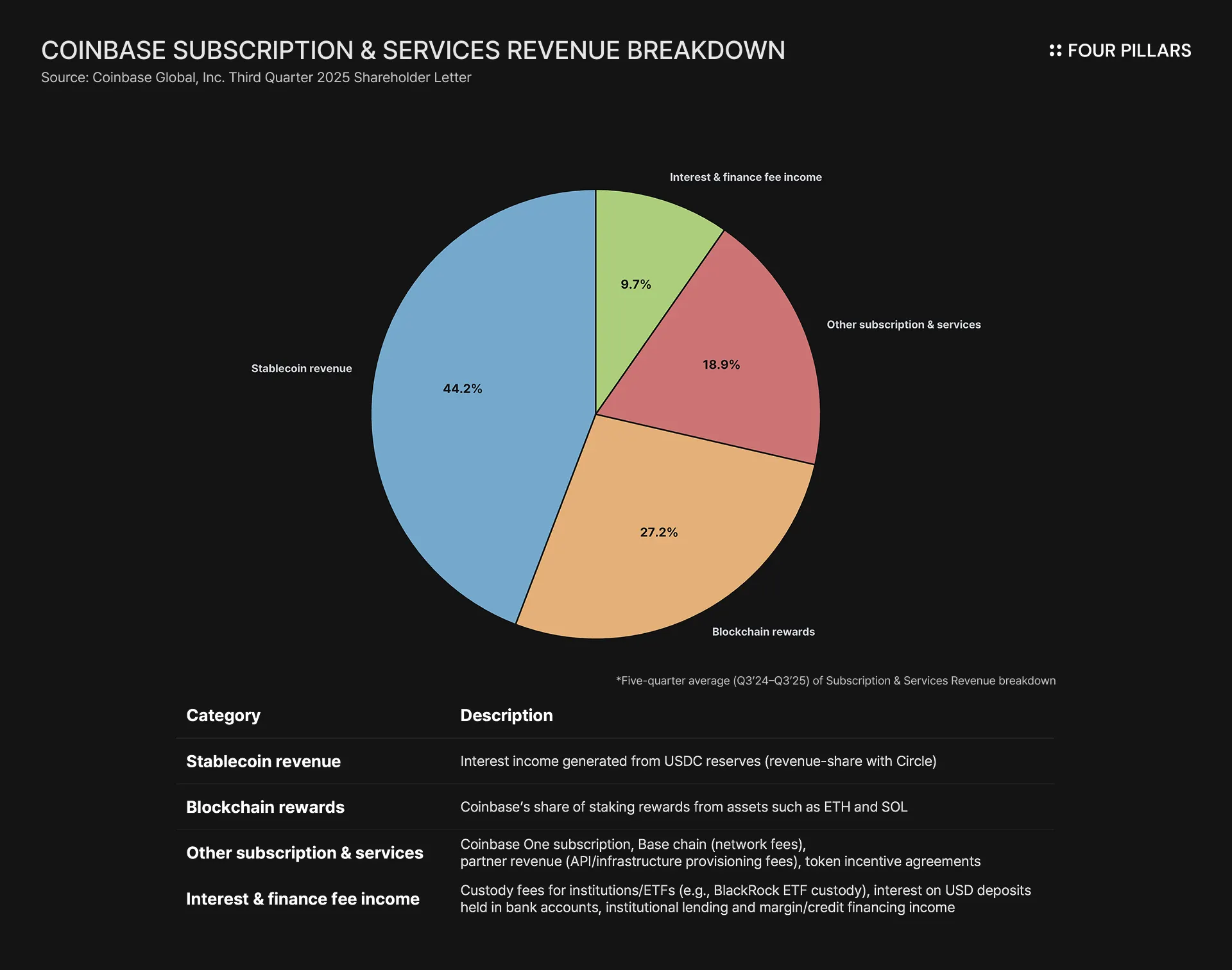

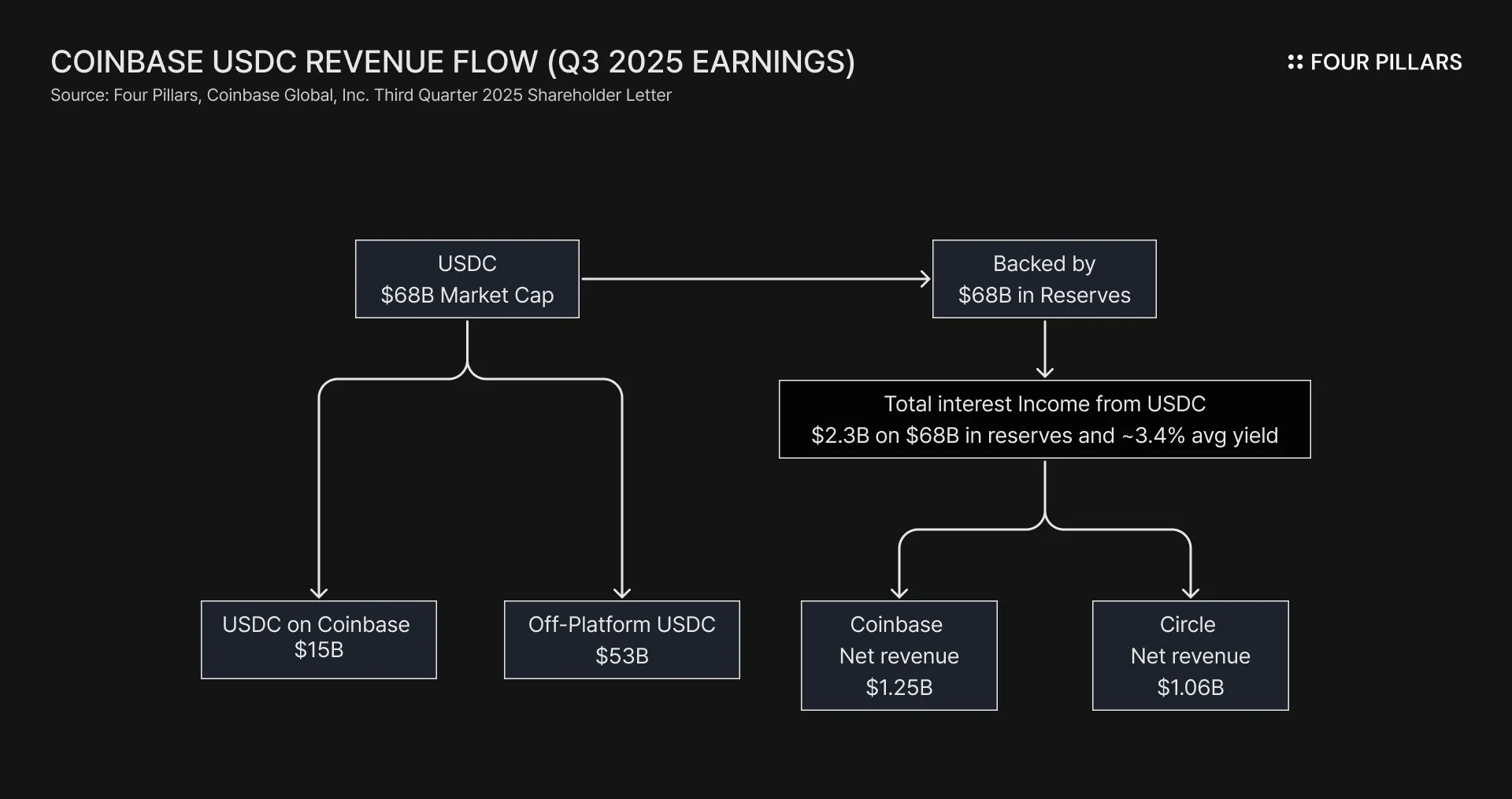

Recent quarterly data shows that stablecoin revenue represents the largest share of Coinbase’s non-trading income at an average of 44%. Blockchain rewards (Staking revenue) contribute 27%, subscription and service revenue contribute 19%, and interest and finance fees contribute 10%.

Coinbase’s structural advantage lies in its revenue-sharing arrangement with Circle for USDC. The exchange has a clear strategy to expand USDC usage across the Coinbase platform and the Base network. The USDC rewards program supports this strategy by applying rewards not only to retail users but also to institutions, accelerating USDC adoption.

Approximately $15B of USDC is held in Coinbase products as of Q3 2025, and an additional $4.3B circulates on Base. Combined, this accounts for roughly 26% of total USDC supply of $75B being used within the Coinbase ecosystem.

Coinbase Pay serves as an integrated payment channel that increases USDC stickiness inside the platform. Coinbase One drives predictable cash flow through subscription-based membership. Institutional custody fees, institutional lending, and staking revenue further contribute to stable non-trading income, smoothing the volatility of total revenue.

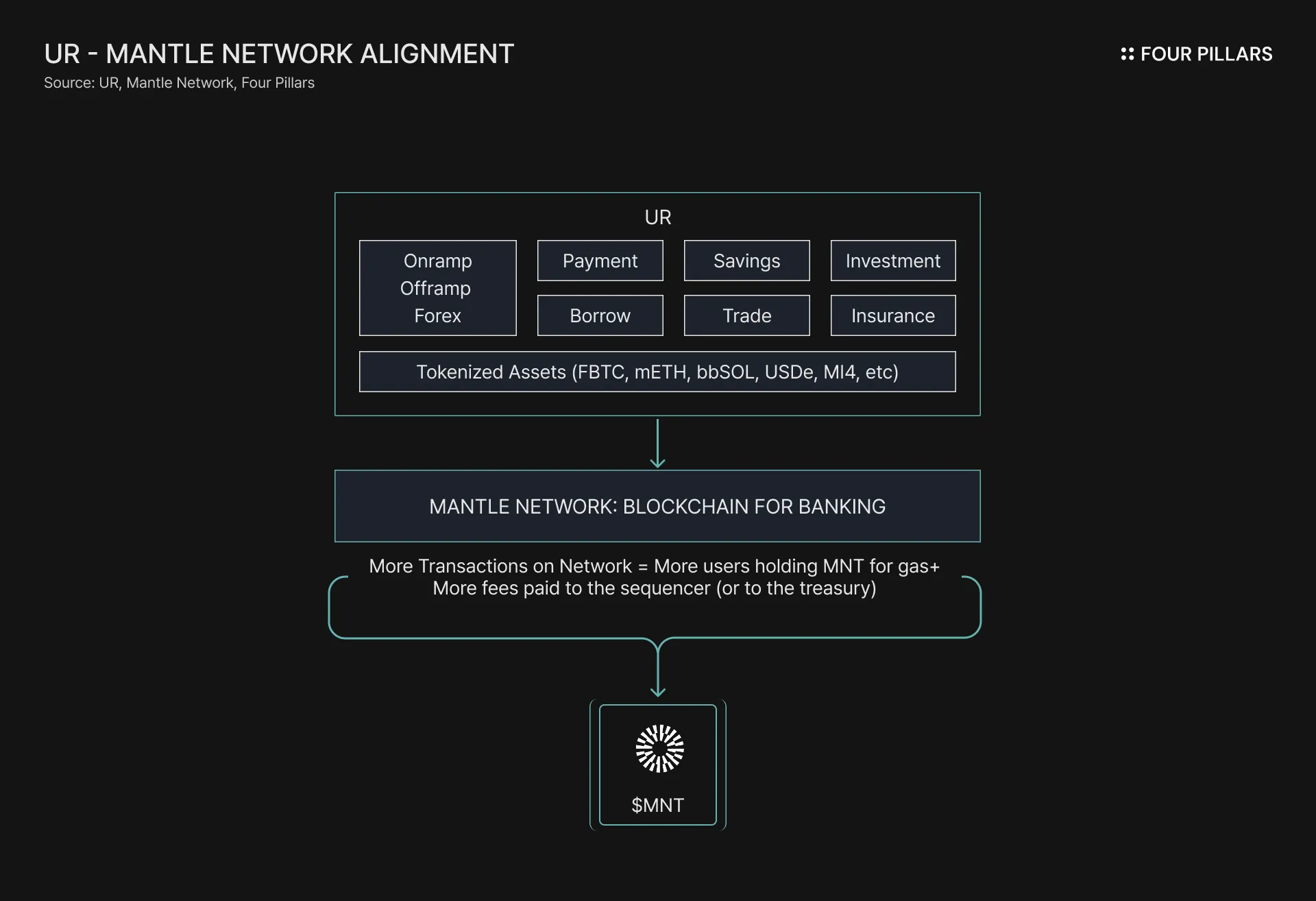

1.3.2 Bybit: A Chain Built for Banking and Value Accrual Through $MNT

Bybit is building out its non-trading revenue lines through the institutional index fund MI4 and the neobanking service UR. Both operate natively on the Mantle Network, which aims to function as a chain designed for banking infrastructure. As usage scales, more value flows into the network and ultimately accrues to $MNT.

UR: A Swiss international bank account based neobank supporting foreign exchange, on and off-ramps, yield products such as USDe, MI4, and mETH, DeFi connectivity, and Mastercard debit spending.

MI4: An institutional crypto index fund generating approximately 5 to 6% annual yield from assets such as BTC, mETH, bbSOL, and sUSDe.

A core principle in Bybit and Mantle’s strategy is the consolidation of value around $MNT. Coinbase’s non-trading revenue is anchored by USDC because Coinbase directly captures value from the reserves underlying USDC. Mantle follows a different model. It captures value through increased usage of Mantle-based financial products, which strengthens $MNT.

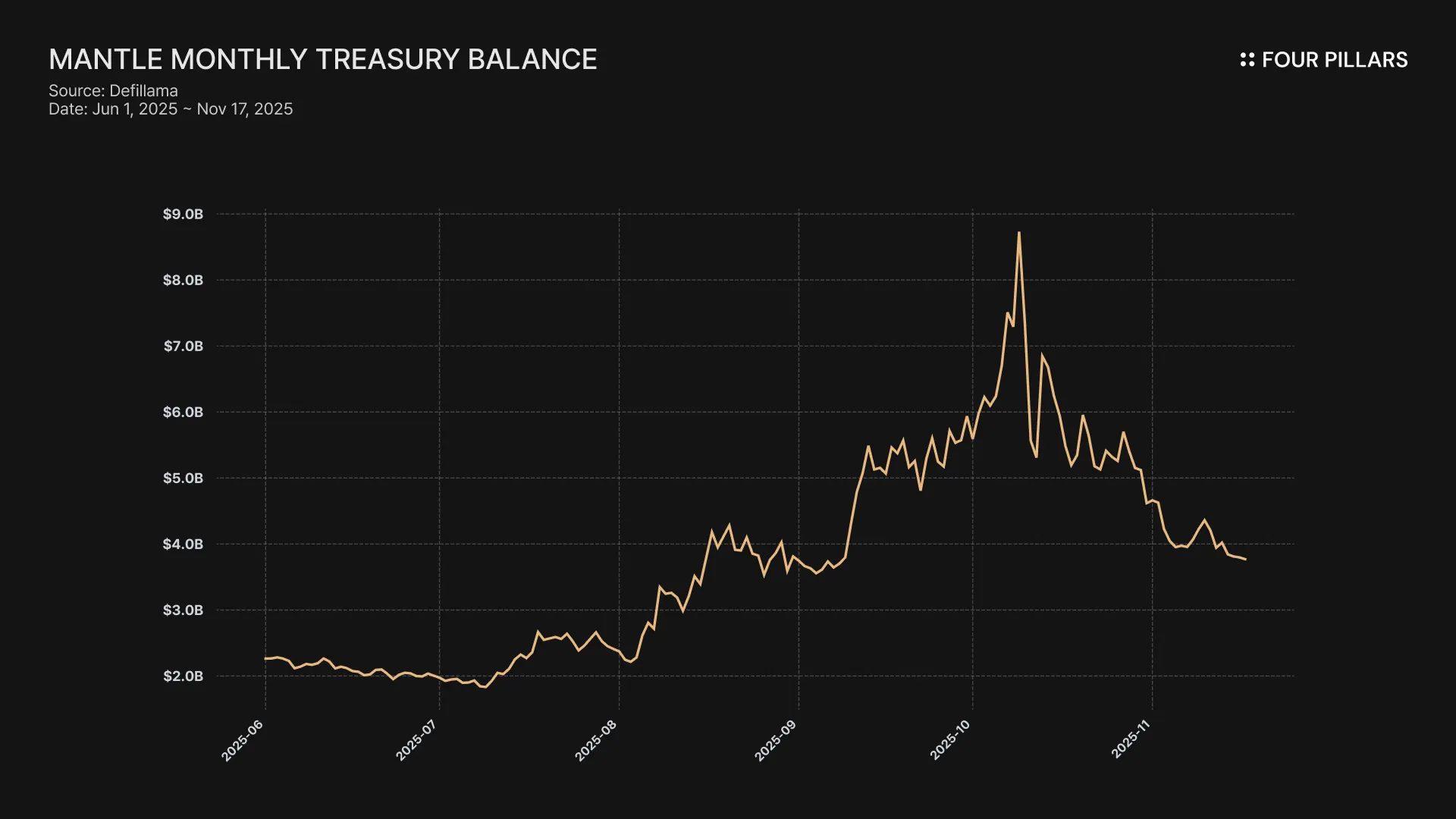

This model is supported by Mantle’s treasury structure. The Mantle Treasury currently holds approximately $4B in $MNT. As the value of $MNT appreciates, the treasury grows, placing Mantle among the largest treasuries in the ecosystem. These funds recycle into the Mantle EcoFund and are reinvested into the broader ecosystem, creating a flywheel that accelerates growth on the network.

1.3.3 Upbit: Strategic Integration with a Major Tech Company

Upbit dominates the South Korean retail trading market. However, competition is increasing as global exchanges move into the region. Binance recently announced its intent to acquire Gopax, which signals renewed efforts by global exchanges to enter the Korean market. At the same time, the Korean Financial Services Commission has highlighted deficiencies in listing oversight and announced plans to transition listing standards to formal government regulation. In this environment, additional upside in pure trading revenue is likely to be constrained.

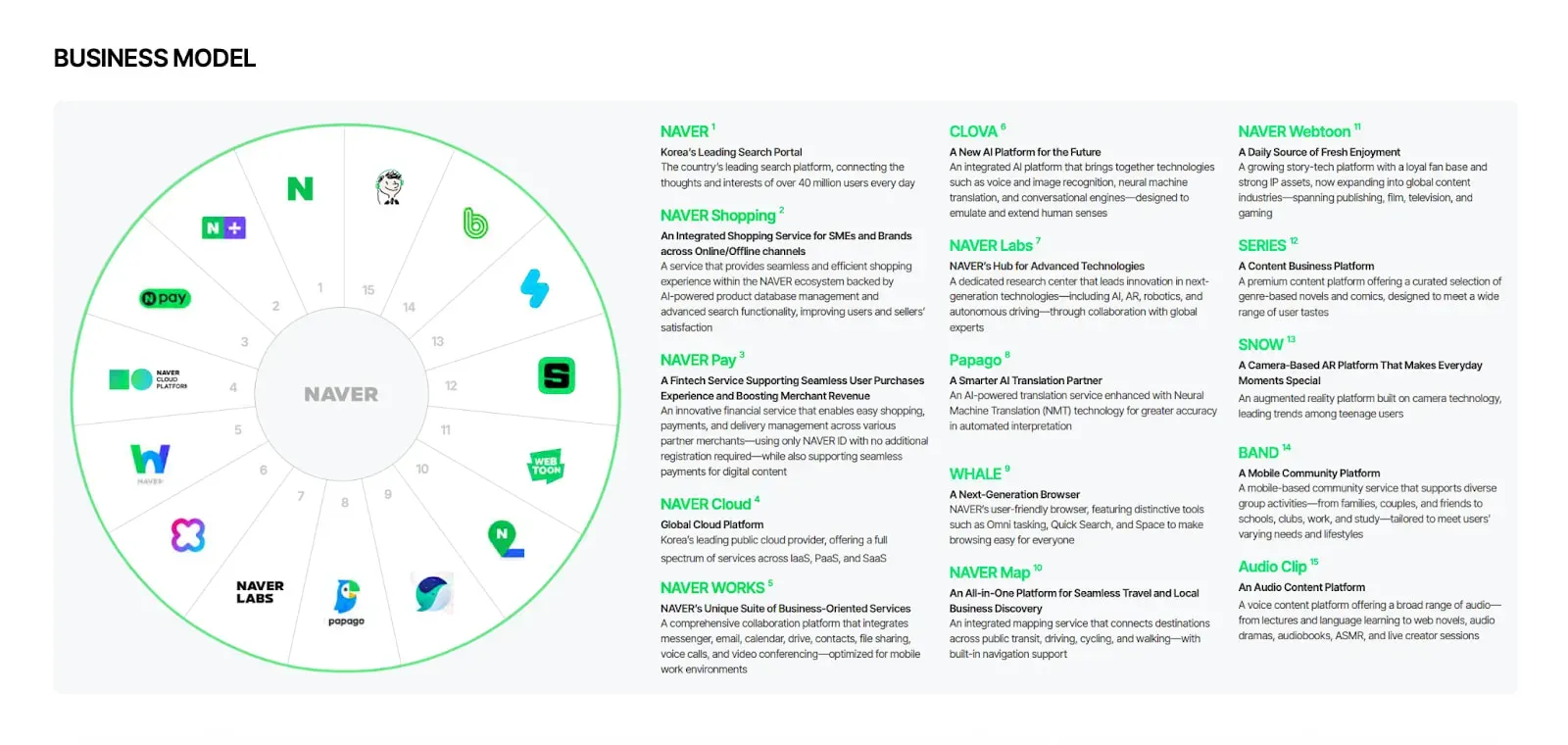

Source: Naver Integrated Report 2024

Dunamu, Upbit’s parent company, is therefore shifting toward non-trading expansion. It recently confirmed that it is reviewing a proposal for a partial acquisition by Naver. Naver is one of Korea’s largest technology companies with businesses spanning search, commerce, content, cloud, and payments. The proposed deal is widely interpreted as a strategic integration to connect Dunamu’s stablecoin-centered business with Naver Financial’s fintech offerings.

If South Korea enacts stablecoin legislation next year as expected, synergies across payments and commerce could deepen considerably. Dunamu is also developing its own blockchain, Giwa, signaling a potential longer-term move into onchain infrastructure.

Using Coinbase’s framework as a reference, exchanges today can categorize their crypto business across three domains.

Crypto as an investment: This includes spot and derivatives trading, which remain high-margin businesses, along with institutional custody and options markets. Mantle has recently widened its supported asset range by partnering with Backed Finance to list tokenized equities such as NVDAx, APPLx, and MSTRx directly on the Bybit exchange

Crypto as a financial service: This includes stablecoin payments, embedded DeFi, institutional lending, and participation in pre-sales. Coinbase already operates several of these services through the USDC rewards program, USDC payment features, and BTC collateralized lending via MoFro.

Crypto as a platform: This refers to exchanges building and expanding their own chain environments such as Base, Mantle, and BNB. The approach resembles that of existing L1 and L2 networks but has an advantage through direct integration with exchange infrastructure. This allows exchanges to create defensible moats in liquidity, user accessibility, and incentive structures such as launchpads and trading fee benefits.

Although all three domains will continue to develop in parallel, the second and third domains will become increasingly central to exchange revenue models as markets evolve and non-trading income becomes more important. Correspondingly, the primary performance indicators will shift from pure trading volume to metrics such as assets under management, user traffic, and transaction volume.

Trading Volume (Crypto as an investment) → AUM (Crypto as a financial service) → User Traffic and Transaction Volume (Crypto as a platform)

Earlier phases of exchange business models required only the addition of new assets or chains on top of custody infrastructure, order books, and deposit or withdrawal systems. In the next phase, the resource requirements spread horizontally. Legal licensing, technical infrastructure, human capital, security capabilities, and market entry strategies all become necessary components for growth. As partially observed this year, strategic acquisitions and partnerships are expected to accelerate in 2026.

Recent acquisitions show strong synergy across distributed verticals. In Coinbase’s acquisition of Echo, the recent Monad public sale sold out all 7.5B MON tokens and reached its maximum raise. The sale alone facilitated the distribution of at least $270M worth of USDC, involving 85,000 participants.

The sale also provided higher bidding limits for Coinbase One subscribers and used an allocation mechanism that prioritized lower bid prices. This structure encouraged broad participation from smaller buyers and concurrently incentivized subscription adoption. Both outcomes align with Coinbase’s strategy to expand the user base across its ecosystem.

The crypto market entered an inflection period this year driven by developments such as stablecoin regulation, onchain payments, crypto ETFs, and asset tokenization. New retail and institutional entrants require reliable legacy players in the crypto market, and exchanges now recognize that this is a key moment to move beyond narrow revenue models. The alignment of these needs is likely to continue from this year into next year. This period will serve as the foundation that determines the position of exchanges in the next stage of the crypto market.

Looking ahead to next year, onchain financial services such as neobanks are expected to move into full commercialization, which will accelerate in-app DeFi. Within this trend, yield-bearing assets based on real cash flows and exogenous yield are likely to find growing product-market fit.

Crypto is evolving at a rapid pace as a production-grade financial infrastructure. Stablecoin-based debit cards are a clear example. Paying for coffee at Starbucks directly from onchain assets without a traditional checking account is no longer a novel experience. More recently, Visa announced that it is testing a system that pays gig workers around the world in stablecoins. These developments reinforce the rise of onchain neobanks and suggest that onchain rails can become a default financial infrastructure.

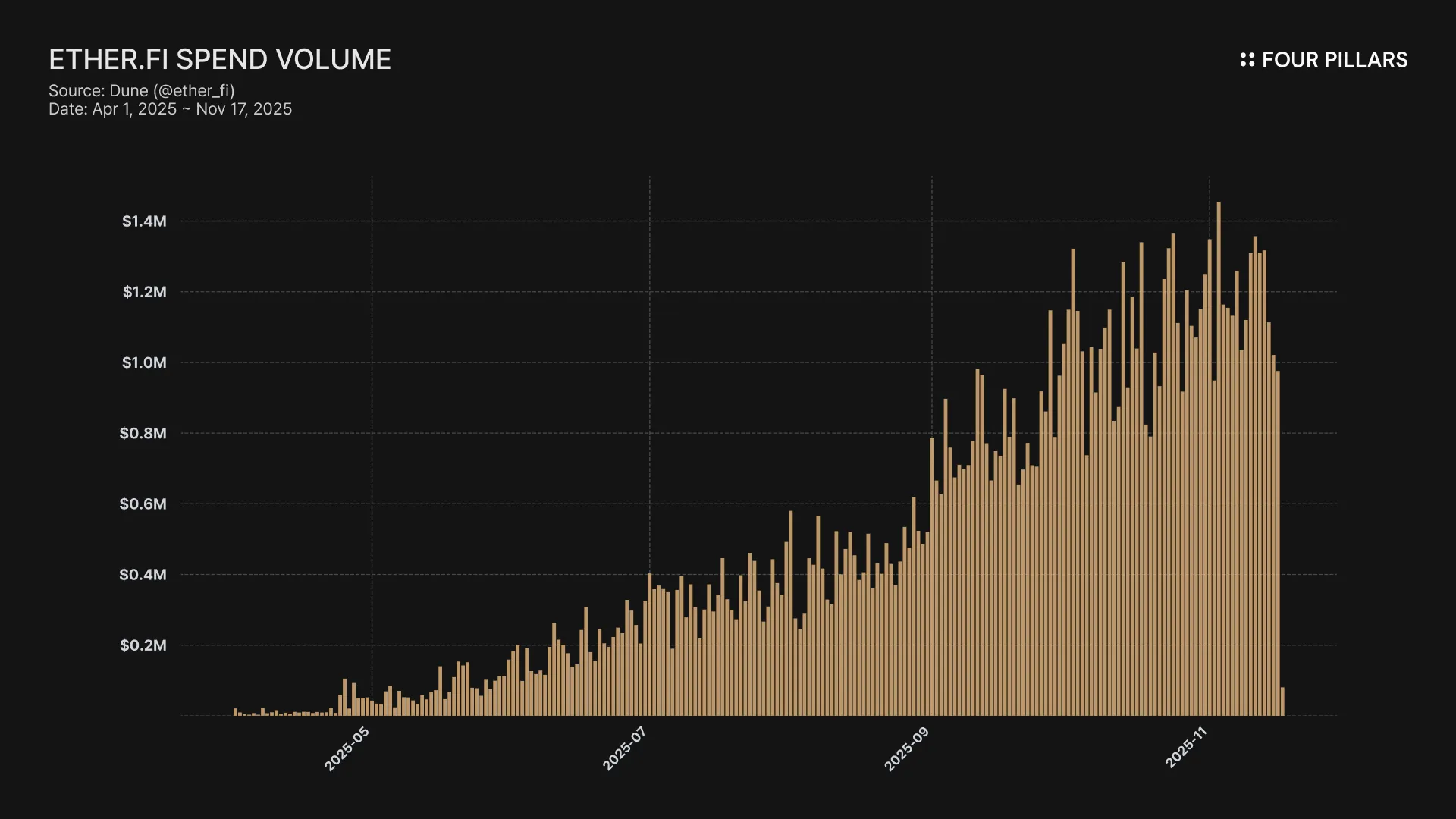

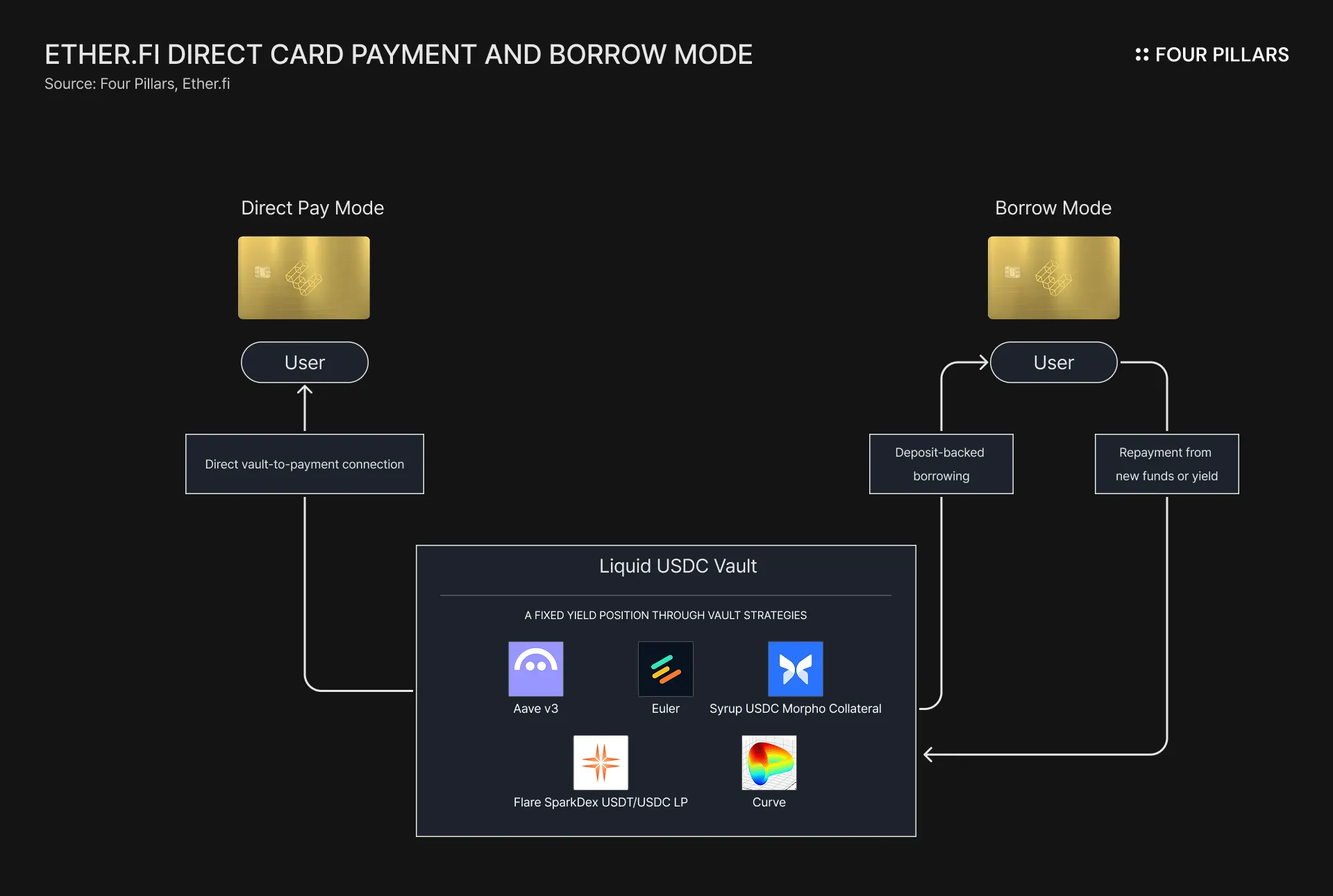

One of the core value propositions driving neobank adoption is that, by leveraging DeFi composability, they can offer higher deposit yields and more flexible asset management than traditional banks. For instance, Ether.fi uses its Liquid USDC vault to deploy assets into DeFi strategies to generate yield, and directly connects the vault’s deposits to payment rails so that users can spend via debit card. When users opt into Borrow Mode, they can borrow against their vault deposits and spend the borrowed funds, which allows them to keep DeFi exposure while maintaining spending flexibility.

This in-app DeFi model is spreading across a broader landscape. Neobanks, fintech apps, exchanges, and wallets are increasingly integrating DeFi yield sources. This is a meaningful shift in how DeFi is used. Users no longer access DeFi solely through dedicated frontends where they manually select individual vaults. Instead, they become default participants in DeFi markets while pursuing their original intent such as payments or remittances.

For service providers, it becomes more important to curate yield sources with sound underlying cash flows and strong repayment capacity rather than pursuing high-risk strategies for TVL competition. The emphasis shifts from maximizing nominal APY to building robust, liability-aware yield portfolios.

The primary factor that will determine user adoption for onchain neobanks will narrow down to the DeFi-linked yields they can provide. Users ultimately migrate toward platforms that offer higher passive income. From a business model perspective, neobanks generate revenue by allocating customer deposits into portfolios of interest-bearing assets, integrating directly with capital allocators such as Ether.fi, Spark, and Veda, or connecting with structured vaults. The intermediation margin created through these allocations becomes a primary source of income.

However, as the path by which yield is delivered changes, the way that yield is sourced must also evolve. Neobanks must maintain sufficient liquidity buffers to meet withdrawal and payment needs at all times, and typical users are far less willing than crypto-native DeFi farmers to bear high levels of risk. This makes liability-driven asset management even more important and raises the bar for building highly stable and sustainable yield sources.

At the same time, users who leave the safety of traditional banks and accept long-tail risks such as smart contract bugs, exploits, and oracle failures expect yields that are meaningfully higher than bank deposit rates. Once user risk profiles and yield expectations are taken into account, portfolio construction becomes considerably more complex.

Under current conditions, if we restrict ourselves to fully collateralized approaches that avoid beta exposure to volatile assets and still source yield in a crypto-native environment, the options can be summarized as follows:

Lending pool liquidity provision: Yield is paid by borrowers as interest. Blue-chip BTC and ETH pools tend to be relatively safe given deep liquidation and repayment liquidity, but yields depend heavily on onchain liquidity demand and therefore fluctuate with market conditions.

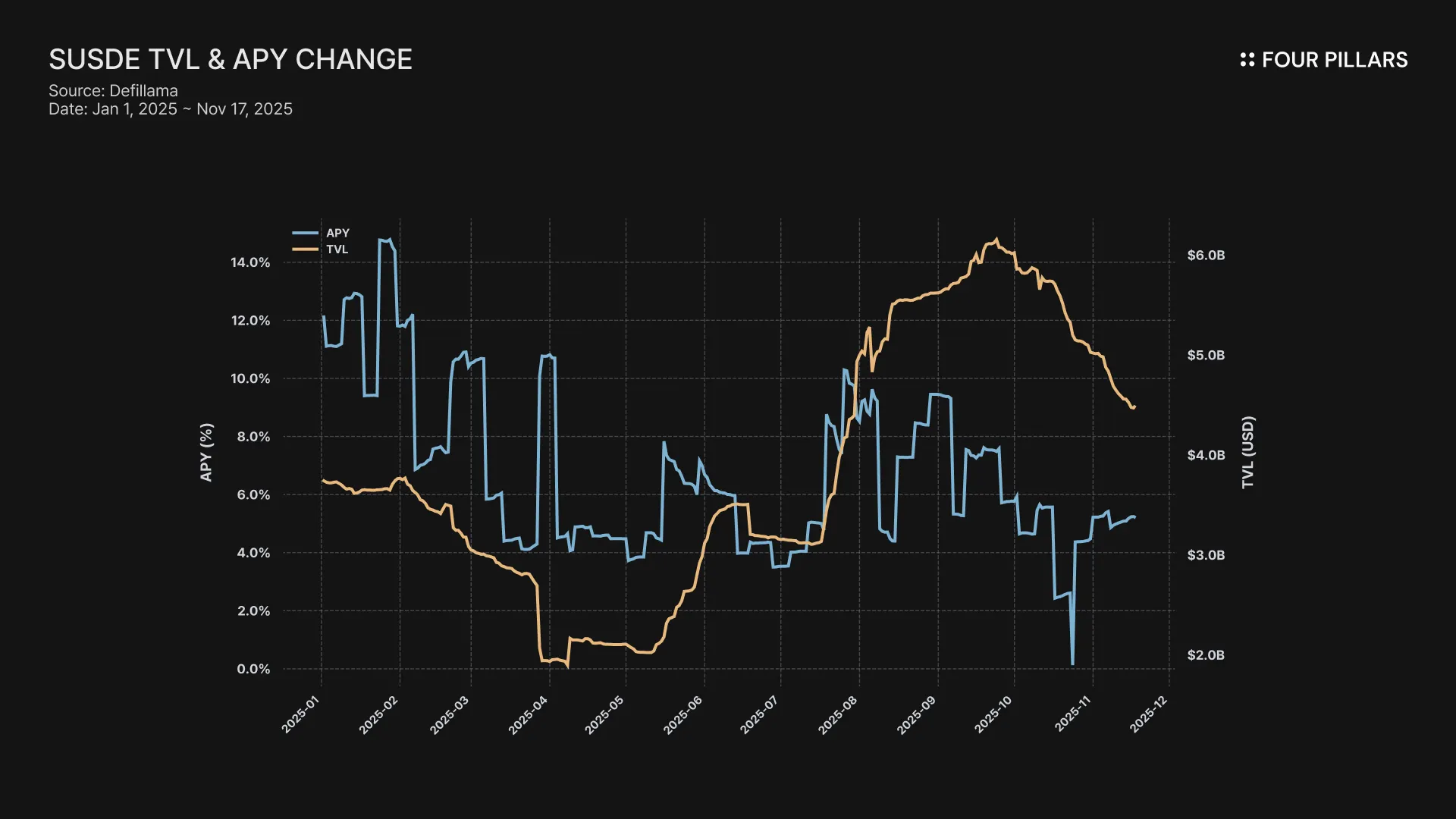

T-bill-backed tokenized fund yield: Since the fund is fully backed by short-term U.S. Treasuries, default risk is minimal. As a result, yields closely follow short-term Treasury rates and generally sit around the 4% range

Delta-neutral basis strategies: Use spot and perpetual futures together to neutralize price exposure and earn the funding rate spread. If funding turns negative for prolonged periods, collateral can be eroded and yields become volatile as they depend on leverage demand.

Across these sources, the stable yield band has compressed into roughly the 4 to 8% range, and yields are highly sensitive to trading activity and borrowing demand in crypto markets. To push returns higher, strategies must layer in leveraged lending or rely on incentive programs, but these approaches introduce significant structural risk or lack sustainability. As a result, they are poorly suited to the user segments described above.

Lending strategies and T-bill-based yields will continue to play an important role as relatively stable components that support portfolio resilience. However, there is still a shortage of complementary assets that can enhance yield competitiveness. In practice, assets that can deliver reasonable returns while minimizing stacked DeFi model risk remain largely unfilled in the market. There is a clear open slot for yield-bearing assets that sit in the mid-risk, mid-yield segment.

One candidate set to fill this gap is exogenous, so-called “exotic” yield-bearing assets that generate returns from real cash flows under disciplined risk management. Examples include OTC premia and institutional lending.

OTC premia (Neutrl), institutional credit (Cap), GPU rental (USDai), and solar power sales (DayFi) are representative cases where diverse yield sources are being connected to DeFi markets.

Source: Cap

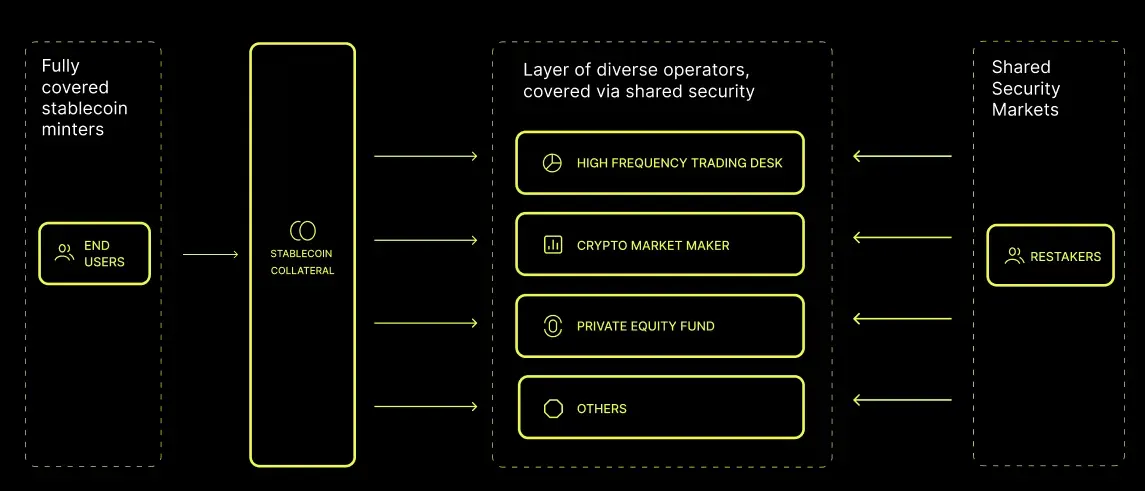

Cap: Cap allows operators such as HFT firms, banks, liquidity funds, and market makers to borrow USDC from vaults to run strategies like delta hedging, arbitrage, and market making. Operators do not post collateral directly. Instead, restakers’ ETH, committed via off-chain legal agreements, serves as the guarantee for the loans.

Users deposit USDC, mint cUSD, then stake it as stcUSD to receive a share of operators’ strategy profits. Operators pay interest on borrowed capital, and these interest revenues accrue to stcUSD holders. The structure targets double-digit yields and sits in the high-risk, high-return segment. It is nevertheless notable that operator default risk is designed to be absorbed by restaker collateral rather than depositors.

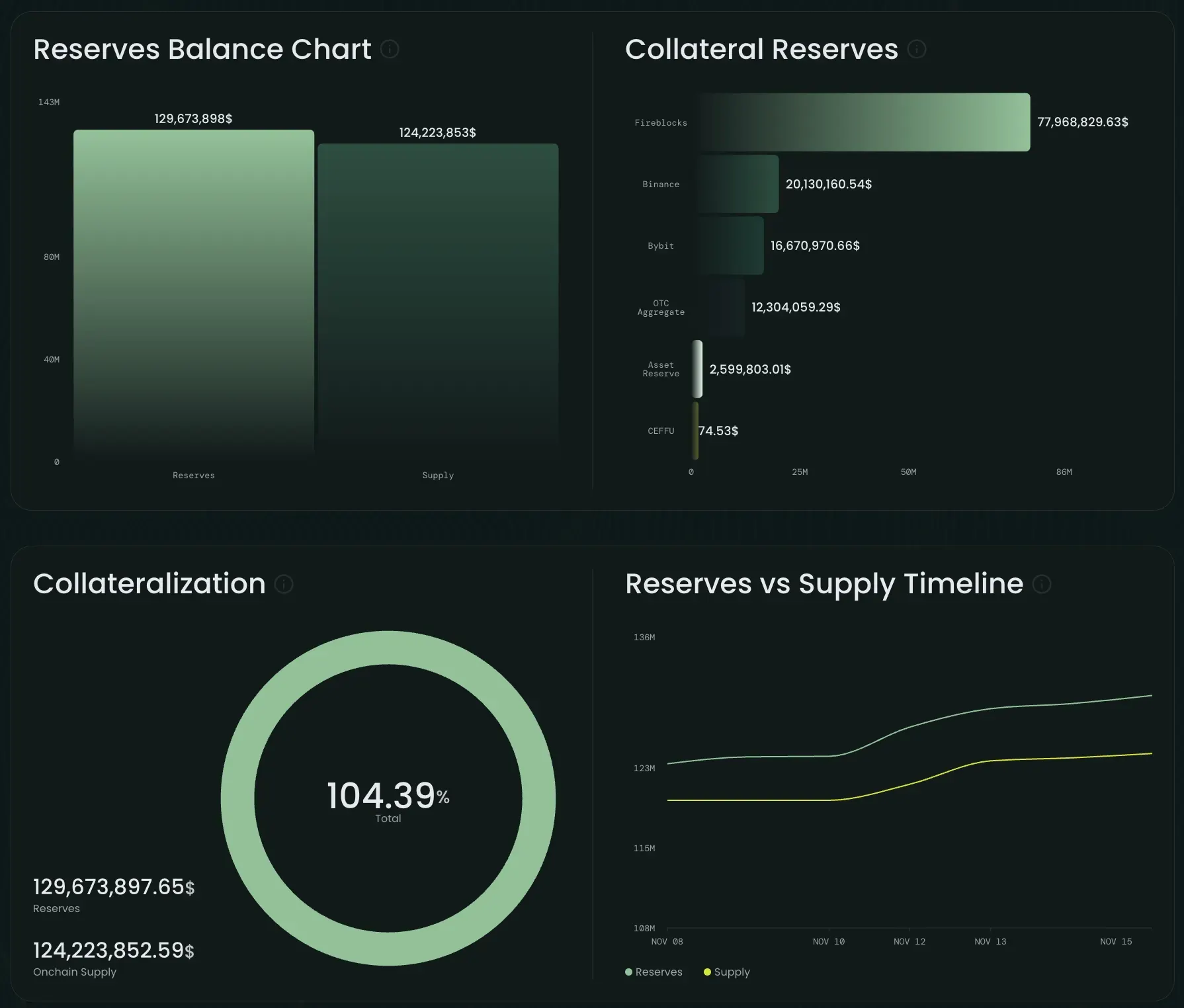

Neutrl: Neutrl is a fully collateralized synthetic dollar that combines three primary components. (1) It purchases locked tokens in OTC markets at sizable discounts to spot prices and opens short perpetual positions to hedge price exposure. (2) It captures basis yield and funding premia between spot and perpetual futures. (3) Where possible, it earns staking yield on the hedged collateral. In effect, Neutrl sources trading yield by buying top-100 tokens at wholesale prices in private markets and shorting perpetual futures to lock in funding and staking returns.

OTC allocations are structured as relatively short 3 to 6 month vesting schedules with designs that can be verified onchain. Leverage is kept conservative, and roughly 80% of the portfolio remains in liquid assets that can be rotated within 24 hours. Over the next two years, token unlocks for the top 100 assets are expected to reach about $55B, which suggests ample OTC supply.

Risk scenarios include OTC counterparty defaults, loss of access to custodial assets, and exchange failures or freezes. Products such as SAFTs and pre-TGE agreements that rely on off-chain contracts and introduce structural opacity are excluded by design.

These yield-bearing assets serve two sides of the market. On the one hand, they satisfy the funding needs of trading counterparties through OTC liquidity and institutional borrowing. On the other, they offer users access to alpha strategies that would be difficult to reach via open DeFi markets alone. By addressing this market inefficiency, structured exotic yield models are emerging as alternatives that are less dependent on market direction or leverage cycles, while still delivering attractive returns.

Recently, the DeFi market went through a painful episode due to the lax vault management practices at Stream Finance. This incident resurfaced concerns about weak risk management and led to renewed discussion around low-risk DeFi as a critical theme.

As institutional capital flows in and in-app DeFi continues to scale, risk management standards are likely to tighten further. In parallel, DeFi risk assessment infrastructure (Credora, exponential.fi, Chaos Labs) is expected to become more sophisticated.

Source: Accountable

Because many exotic yield strategies rely on off-chain transactions, a key prerequisite for their broader inclusion in portfolios is the ability to verify reserves and yields onchain.

Neutrl addresses this by working with Accountable to prove reserves using zero-knowledge cryptography. Accountable connects directly to Neutrl’s exchange accounts and custodial balances through read-only APIs and verifies balances, margin, hedge positions, OTC discounts, and adherence to position caps.

This design allows external observers to verify that discounts have been applied correctly, vesting schedules reflected, and position caps enforced, without revealing sensitive position-level information. The protocol can therefore demonstrate accurate reserve accounting and risk constraints while protecting itself from predatory behavior such as stop hunting.

Taken together, these shifts show that DeFi is moving away from a self-referential, closed ecosystem and integrating into the broader financial infrastructure. Some long-time participants say that the days of triple-digit APYs, ve(3,3), OM forks, and vampire attacks are long gone. They are not wrong. The bold, frontier-era experiments that once defined early DeFi are now difficult to find. The unique phenomena created by a blend of financial engineering and speculative demand have largely faded or been pushed to the margins.

DeFi is now progressing toward becoming a part of the entire financial system (and in some cases transitioning into it). It is increasingly used as an alternative to traditional institutions for low-cost liquidity sourcing and settlement. In this context, it has never been more important to distinguish whether yield comes from real economic activity or from leverage and printed money (tokens).

There is no other way. Within this transition, the players that matter most will be those that precisely align DeFi’s structural efficiency with the needs of traditional capital. They will be the ones to uncover new market opportunities and persistent inefficiencies before the rest of the market catches up.

Dive into 'Narratives' that will be important in the next year