AI trading agents already possess structural advantages such as operating 24/7 without FOMO or panic selling. The proliferation of projects and anxiety from DeFi incidents are actually increasing demand for verifiable and controllable automated asset management. By 2026, "manageable" DeFAI agents are expected to emerge, where users can set risk profiles and verify on-chain whether the AI adheres to them.

Monad and MegaETH have performance comparable to Solana and Base, while also possessing asymmetric weapons that existing chains cannot easily replicate: strong communities and novel incentive structures. Their core strategy is to dominate the consumer app ecosystem while Solana and Base shift toward institutional focus. If these two chains form a united front rather than competing against each other, it could become the most threatening scenario for incumbent chains.

Tokenizing trading cards provides clear value through instant ownership transfer, inheritance of grading records, and possibilities for fractional investment and derivatives. While 2025 exposed the limitations of projects relying on gacha mechanics and token expectations, the market outlook for 2026 is promising. Coinciding with Pokemon's 30th anniversary, marketplaces that focus on fundamentals could absorb the potential of the Web2 collectibles market.

Source: N of 1

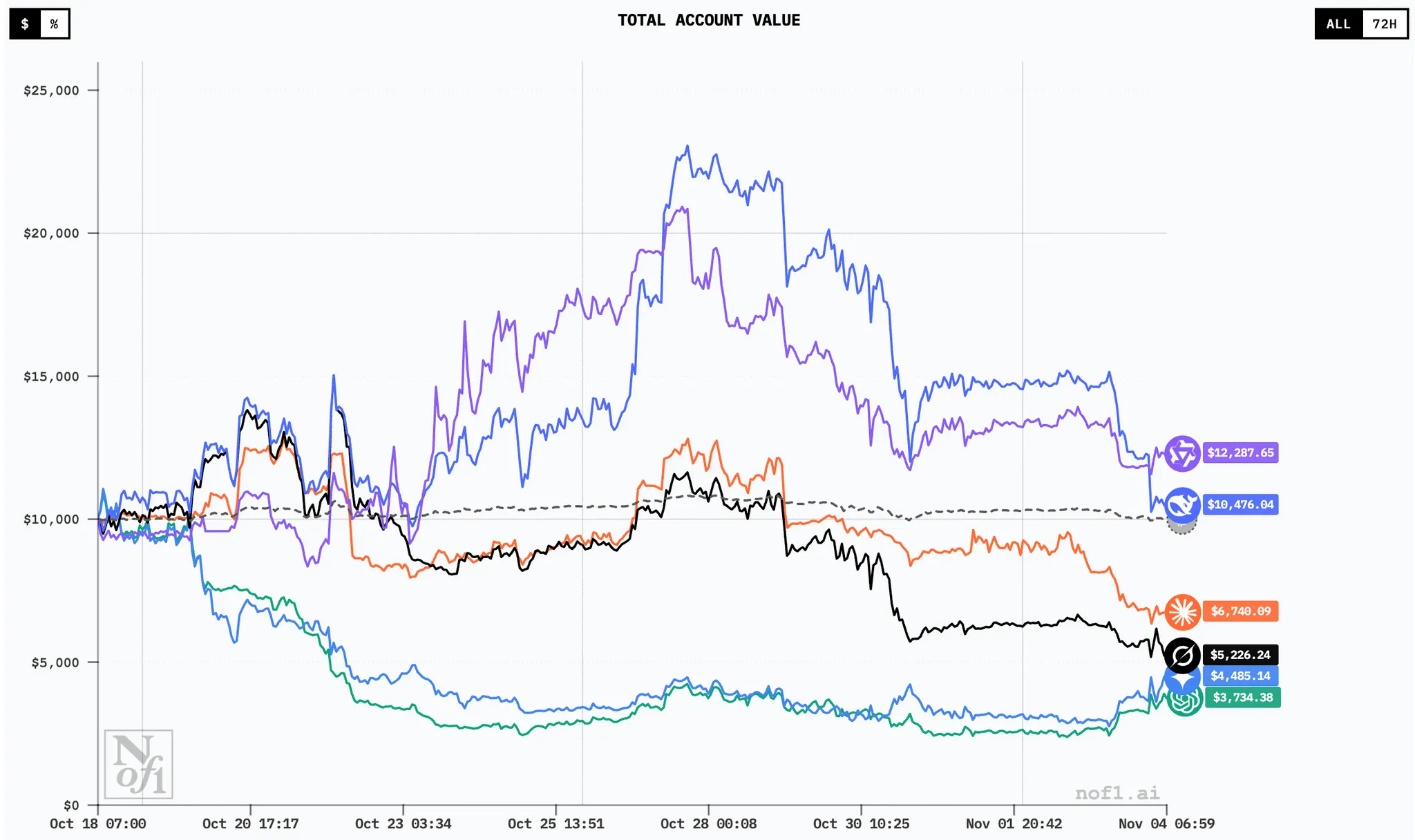

Recently, there have been continuous attempts to test the crypto trading performance of AI models. N of 1 held a competition last October comparing the trading performance of 6 LLMs on Hyperliquid using only chart data. Despite the short two-week period, the competition left significant insights. Open-source models DeepSeek and QWEN showed better performance than Bitcoin, while OpenAI, the most commonly used model, showed the poorest performance. The public commented, "AI doesn't seem to have much edge in trading yet."

However, looking at the results of the trading competition held at Synthetix during the same period would change this assessment. Despite 98 participants consisting of traders and CT influencers who are generally considered above average, only 25 made profits over three weeks. While direct performance comparison between the two competitions is difficult due to different durations and conditions, the important point is that AI models showed performance exceeding humans despite lacking additional training and being blocked from external information like web searches. AI already has structural advantages in being free from human traders' chronic problems like FOMO and panic selling, and being able to monitor markets 24/7.

Meanwhile, the current situation in the Web3 ecosystem is creating an environment conducive to retail's dependency on AI agents, which can be divided into two main reasons.

First is the difficulty in investment decisions due to excessively increased projects.

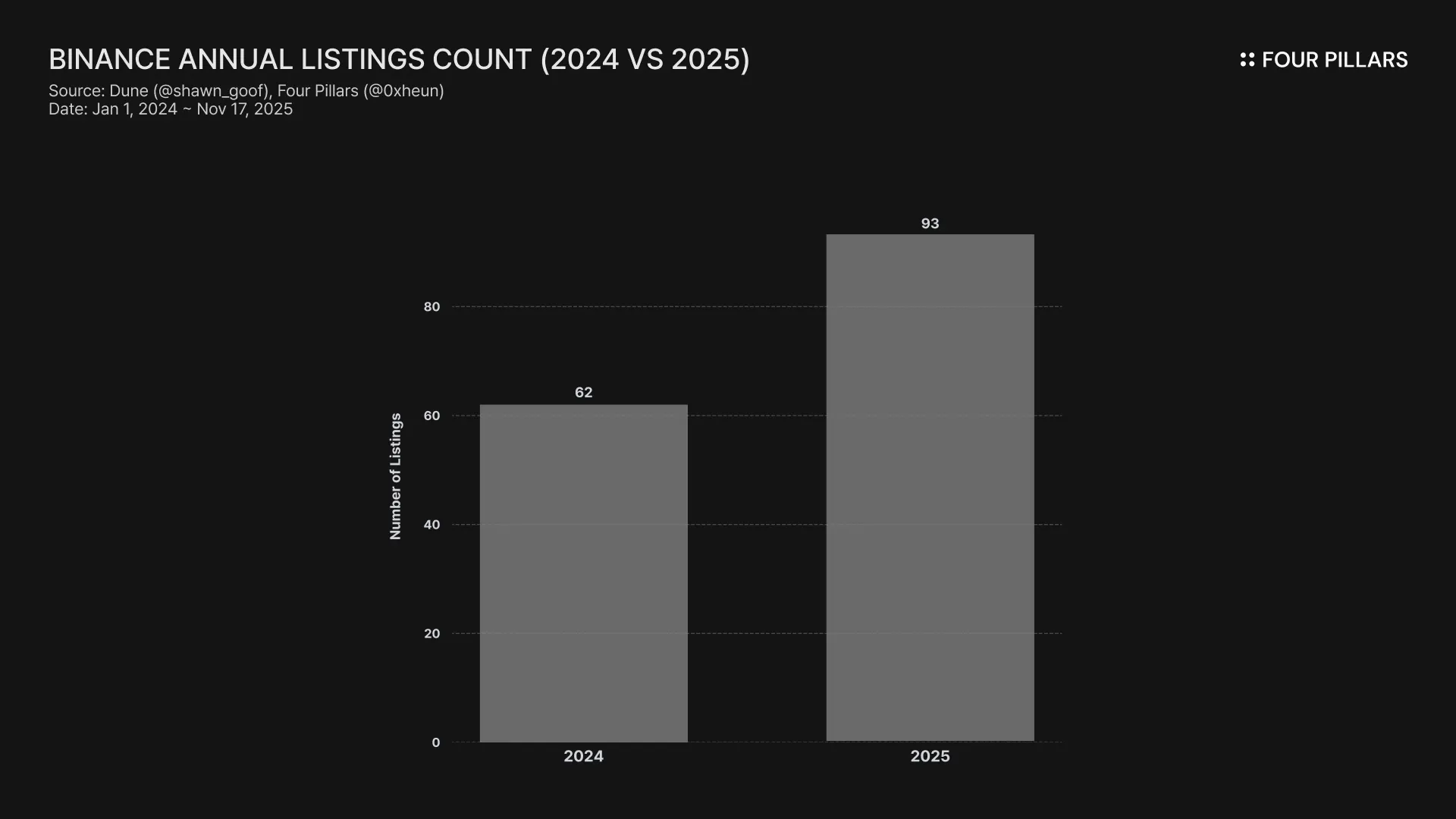

If 2024 was the year of memecoins, 2025 was the year VC-backed projects achieved listing rallies. Due to TGE events of numerous concept projects, retail has found it extremely difficult to value individual projects. In fact, the average daily number of new token listings in 2025 increased by more than 1.5 times compared to the previous year (Binance: 62 in 2024 → 93 in 2025), and with the flood of already-listed tokens, it has become virtually impossible for individuals to follow all projects.

This situation has greatly increased AI dependency for retail-level research, and AI crypto research services like Surf are now being used not only for simple project introductions but also for evaluating investment decisions and fair value. This trend suggests that the likelihood of retail gradually handing over control of their capital to AI is increasing beyond simply using AI for investment decisions.

Second is the demand for controllability due to increased fear of DeFi.

Public anxiety has intensified due to various incidents in the DeFi ecosystem, including the recent Stream Finance incident that caused approximately $285M in losses including indirect damages. While this can be resolved long-term through improved operational transparency as these were accidents caused by lack of asset management transparency and management complexity, general investors who have been investing based on yields without deep DeFi knowledge are turning away from DeFi to simple spot investments on exchanges or very passive portfolios due to strong fear. This anxiety may potentially transform into needs for automated asset management that users can control or verify.

So far, several DeFAI projects have existed where users delegate portfolio management to agents, but these have provided relatively low levels of controllability and verifiability. Successful DeFAI platform implementation requires user-configurable risk profiles and mechanisms to verify compliance with them.

In line with this trend, several Web3 projects have implemented mechanisms that can provide verifiability and controllability to AI trading agents.

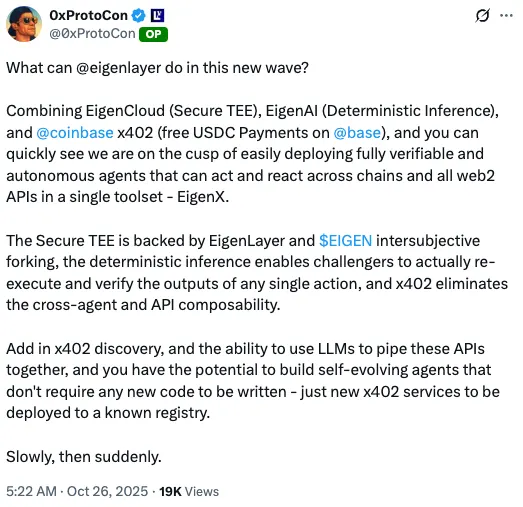

Source: @0xProtoCon

Notably, EigenCloud's EigenAI provides a mechanism that forces deterministic execution by controlling AI agents' computation processes down to the bit level. It provides maximum verifiability for AI agents through the combination of EigenCompute, which provides integrity verification through remote attestation by ensuring agents execute within TEE, and EigenLayer, which performs optimistic verification through economic incentive mechanisms.

Techniques are also emerging that set guardrails limiting the scope of model actions before execution through zero-knowledge proofs. This involves setting constraints on agent behaviors such as maximum transaction size limits, trading within approved token lists, and daily transaction limits through zero-knowledge proofs, then verifying compliance before transaction execution.

Of course, we must acknowledge that entrusting complex DeFi operations to AI agents is still challenging. While current AI models can adequately perform roles like constructing token portfolios when fundamental-based investment and quick access to narratives are possible, I believe they still lack the technical maturity to autonomously perform complex DeFi strategies like looping and cross-chain yield farming.

The fact that agent task complexity limits absolutely bottleneck model performance is a major problem currently. Errors are still possible in multi-step reasoning or complex mathematical calculations, which can lead to fatal results in the sensitive area of asset management. The ability to respond to crypto market's extreme volatility and unpredictable black swan events is also an area where trained human traders still have an advantage.

However, completely wrong decisions like calculation errors can be addressed through the aforementioned verification/control methods, and as reasoning model performance has been increasing dramatically recently, I expect agents capable of achieving meaningful results for DeFi strategy products will be developed in the near future.

I expect that in 2026, "manageable" DeFAI agents that general users can sufficiently rely on will be introduced. These next-generation DeFAI systems will allow users to finely set their risk preferences, investment goals, and constraints, while AI will adjust portfolios in real-time while strictly adhering to these parameters. Whether all decisions comply with user-set profiles will be verifiable in real-time through on-chain mechanisms. This also applies to defensive mechanisms like automatic stop-losses during emergencies. All transaction history and decision-making processes will be transparently recorded on-chain, enabling real-time performance analysis and benchmark comparisons, and an ecosystem will be built where successful strategies are shared and evaluated by the community.

Ultimately, DeFAI will position AI not as a replacement for human traders but as a tool that complements and enhances them. DeFAI systems with appropriate control mechanisms and transparency will lower entry barriers for general users who have abstract/mathematical understanding of DeFi but lack technical access capabilities to easily participate in the DeFi ecosystem, which I expect will ultimately lead to the growth and popularization of the entire Web3 ecosystem.

For me, the biggest expectations for 2026 are Monad and MegaETH. These have been developed long-term to build powerful infrastructure exceeding the performance of Solana and Base, the most user-intensive chains. But what's even more notable is that they've put greater effort into building loyal communities and ecosystem projects while delaying promotion of technical achievements. Monad and MegaETH will begin attacking gaps through community and ecosystem incentives, their most asymmetric advantages compared to existing chains.

2.1.1 Solana

In 2025, Solana announced a concrete roadmap for implementing Internet Capital Markets and focused entirely on infrastructure performance improvements, successfully achieving all the following short to medium-term goals this year:

DoubleZero Introduction: Resolving network congestion and spam issues, the biggest bottlenecks in the current consensus process, through introducing blockchain-dedicated networks using dark fiber

Jito BAM: Resolving the inability to implement separate sequencing logic per app due to Solana's unique transaction processing structure through TEE-based plugins

Alpenglow: Reducing end-to-end latency by improving fundamental consensus and block propagation structures, shortening block finalization time to 150ms. Mainnet deployment expected within the year.

This means Solana has moved much closer to its long-term goal of becoming an on-chain Nasdaq and has built an environment for accelerated institutional onboarding.

However, Solana is simultaneously the biggest playground for degens centered on memecoins, with almost all user interactions on Solana except DeFi coming from memecoin launchpads. The problem is that Solana's memecoin-related activity in 2025 has significantly decreased compared to 2024, as if reflecting Solana's recent direction. The number of Pump.fun graduation tokens, which exceeded 800 in January, now barely exceeds 70, and Solana chain's daily active users have maintained around 10M, an 80% decrease from January's 80M. Additionally, due to difficulties implementing CLOB due to its unique MEV environment, it hasn't shown notable activity in the recent meta centered on PerpDEX.

Meanwhile, the Solana ecosystem showed results in the privacy sector where other ecosystems struggled to find meaningful movement. Projects developed on Arcium, an MPC (multi-party computation) project, are receiving great attention, including Melee, a prediction market project providing private order flow, and Umbra, a protocol for private swaps and privacy application development.

Also, after Jito BAM presented the possibility of introducing app-specific sequencing through plugin mechanisms, projects attempting to implement PerpDEX in the form of network extensions similar to this, such as Bulk and Bullet, are emerging. The Solana ecosystem is expected to focus on developing applications centered on trading activities rather than consumer-oriented apps in line with future infrastructure development.

2.1.2 Base

In 2025, Base showed remarkable achievements in both infrastructure and consumer aspects. Base had been increasing chain performance by raising block gas limits by 20% monthly, but announced a major scalability improvement plan in October this year, declaring they would achieve more than double performance improvement within the year. Base shortened block time to 250ms through preconfirmation via Flashblocks introduction, and is upgrading sequencer, DB, and data availability aspects through close collaboration with OP Labs. Through blob scalability improvements via the Fusaka upgrade to Ethereum in December this year, Base plans to implement scalability of 150M gas per second and over 7100 TPS by year-end.

Ecosystem plays also responded to trends. Projects in popular sectors were launched timely and successfully attracted attention: perpdexes (Avantis), x402 & AI (Virtuals Protocol, Recall), prediction markets (Limitless, Football.fun). Currently showing concentrated attacks on SocialFi through support for Zora, linking Farcaster with the ecosystem, and launching socialization of the Coinbase app. Particularly, Base continuously hints at imminent token launch, and the incentive mechanisms created in the Base ecosystem after token launch will be a major measure in competition with emerging chains discussed later.

2.2.1 Infrastructure Performance Advantage

First, let's examine their competitiveness from an infrastructure perspective. Monad is a project that started when Solana's MEV problems and instability issues were identified as maximum risks, as founder Keone mentioned in the past. It's noteworthy that Monad maintained Solana-level performance while minimizing node client workload to lower validator performance requirements to retail device levels.

Source: gmonads.com

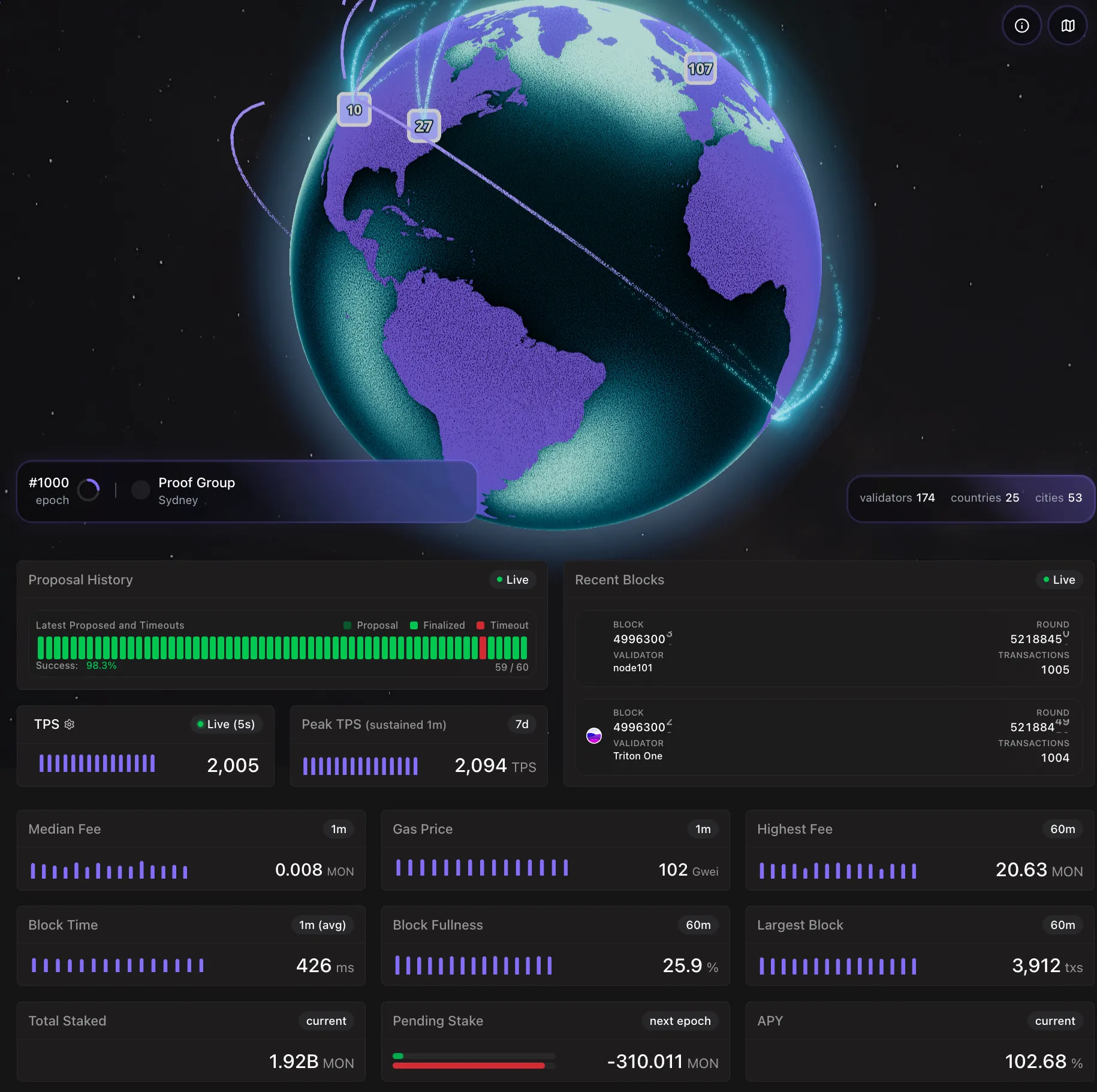

As of November 12 with mainnet launch imminent, Monad testnet is achieving real-time consensus with over 170 validators, showing performance comparable to Solana with 0.4-second block time and maximum 4K+ TPS. Also, delegation amounts for all validators except foundation-operated nodes are very even at 0.5%, and geographically distributed similarly to Solana.

MegaETH achieved technical advancement from a completely different angle. MegaETH achieved execution speed and implementation limits unseen in any existing chain through securing data availability via EigenDA, node specialization structure, and adopting dual chain-view structure of EVM blocks and mini blocks. MegaETH has stably maintained processing over 1,000 transactions per second with 10ms latency in testnet environments, and theoretically can process over 100,000 transactions + 1 giga gas per second. While MegaETH hasn't achieved the same level of decentralization as Monad, it has significance in achieving performance other L2s couldn't implement through various experimental structural designs.

Chain-level infrastructure cannot be easily reformed. Upgrading infrastructure of chains with deployed capital is like changing wheels on a moving car, requiring extreme attention to stability. Ethereum's Lean Ethereum roadmap is expected to take about 5 years to implement, and Solana is only now seeing substantial infrastructure-level improvements like Firedancer, Jito BAM, and Alpenglow ready for mainnet deployment, 4 years after MEV environment stability issues were raised. Therefore, initial infrastructure completeness for Monad and MegaETH is critical for competitiveness over the next 3-4 years, and the results of extreme stress tests immediately after launch and actual performance gaps between testnet and mainnet will greatly impact chains' long-term value assessment.

However, the reason for focusing on Monad and MegaETH as competitors to Solana and Base goes beyond performance. They are in asymmetric conditions to rebuild community and ecosystem from scratch.

2.2.2 Strong Community

Technology alone cannot guarantee chain success. The reason Ethereum still maintains its throne despite numerous technical limitations, and why Solana could resurrect despite multiple network outages, is all due to strong communities. The biggest factor in Monad and MegaETH receiving high valuations before launch is also that they've built strong community foundations to support token prices, separate from technical contributions.

Monad has formed a very unique and strong community culture over the past three years. The Monad community has grown beyond a simple investor group into an organism that has developed its own culture, memes, and internal terminology. Monad community identity is so deeply formed that outsiders entering for the first time find it difficult to immediately understand their culture. This is more valuable as it formed organically rather than through calculated marketing.

This strong community foundation is likely to transform into explosive memecoin and NFT ecosystem activity immediately upon mainnet launch. With Solana's memecoin ecosystem entering maturity and decreasing volatility, Monad is expected to become an alternative outlet for new speculative demand. Considering that memecoins and NFTs are barometers measuring chain community cohesion and activity beyond simple speculative assets, Monad has a unique advantage from the starting line.

MegaETH took the opposite approach from Monad. While building a relatively small community of 5,000 over about a year, these consist of core personnel carefully selected based on on-chain activity and social influence. This community centered on Plirple SBT collection holders shows very high levels in density and loyalty despite small scale.

Even in the recent $50 million token presale process, MegaETH consistently maintained this philosophy. Instead of large public sales, they selected influential minorities to participate and granted them exclusive access to future incentive programs. Particularly, MegaETH allocated 53% of total token supply to staking rewards and introduced a KPI staking system where vesting unlocks upon achieving specific goals. KPI achievement conditions include MegaETH ecosystem growth goals, infrastructure technical breakthroughs, and Ethereum decentralization.

This strategy completely aligns ecosystem participants' incentives with chain success, a differentiating approach difficult for existing chains with established ecosystems and communities to attempt.

2.2.3 The Issue is Ecosystem Maturity

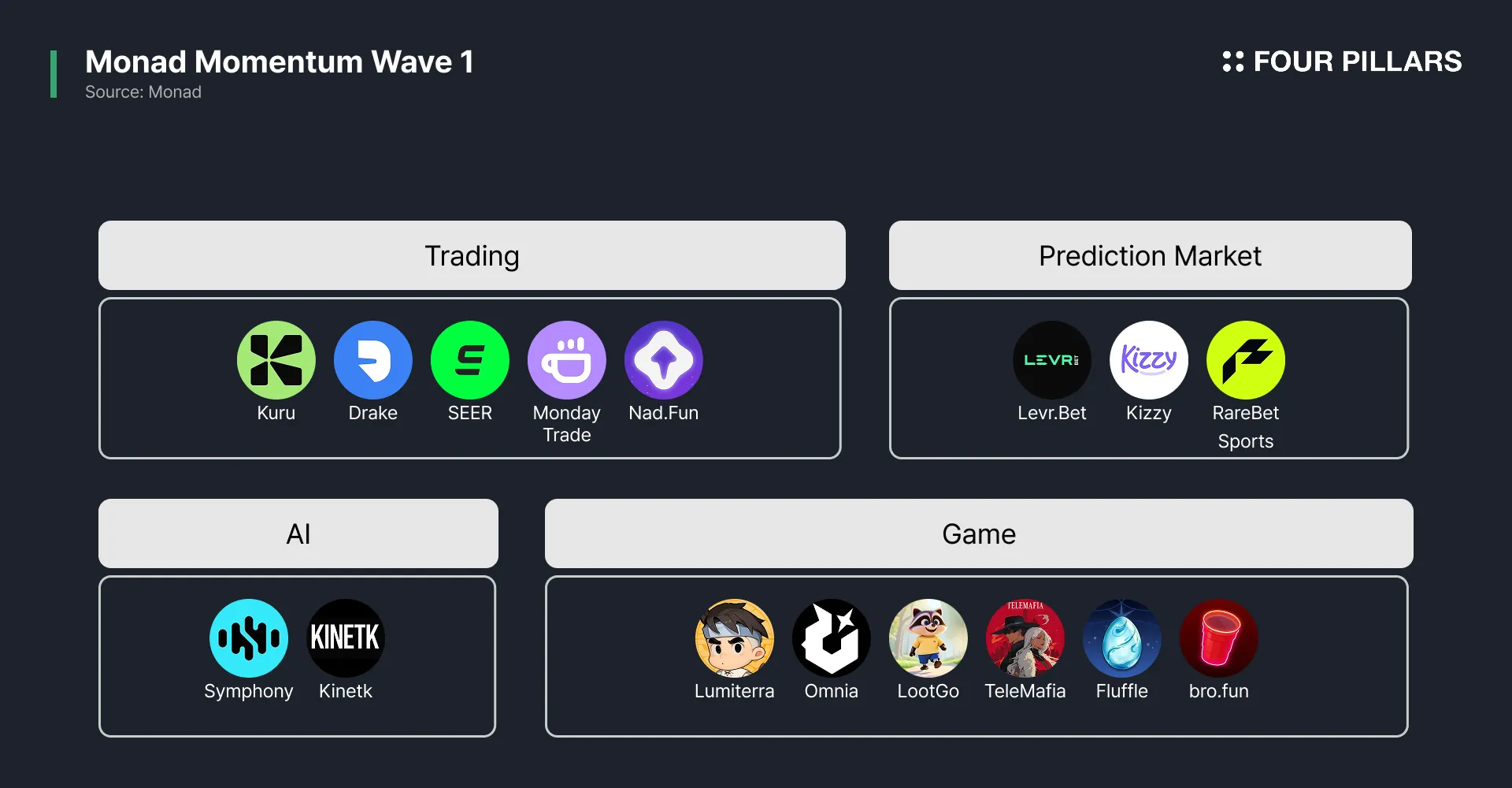

Monad and MegaETH show contrasting strategies in ecosystem plays. Monad is visibly building a broad vertical ecosystem aiming for a general-purpose blockchain. Projects from almost all sectors including liquid staking, perpdexes, games, prediction markets, AI, memecoins, NFTs, and SocialFi will onboard simultaneously with mainnet launch, and Monad chose a strategy of initially boosting selected projects through its own "Monad Momentum" incentive program.

Projects selected for Monad Momentum's first wave also show very diverse scope, confirming to some extent that the Monad team aims to build an ecosystem not biased toward specific sectors.

However, the concern is that apps' maturity doesn't yet appear high enough to have sufficient competitiveness when deployed on other chains, and liquidity fragmentation users will experience when dozens of apps are deployed simultaneously could lead to inconvenient usability, requiring careful ecosystem strategy.

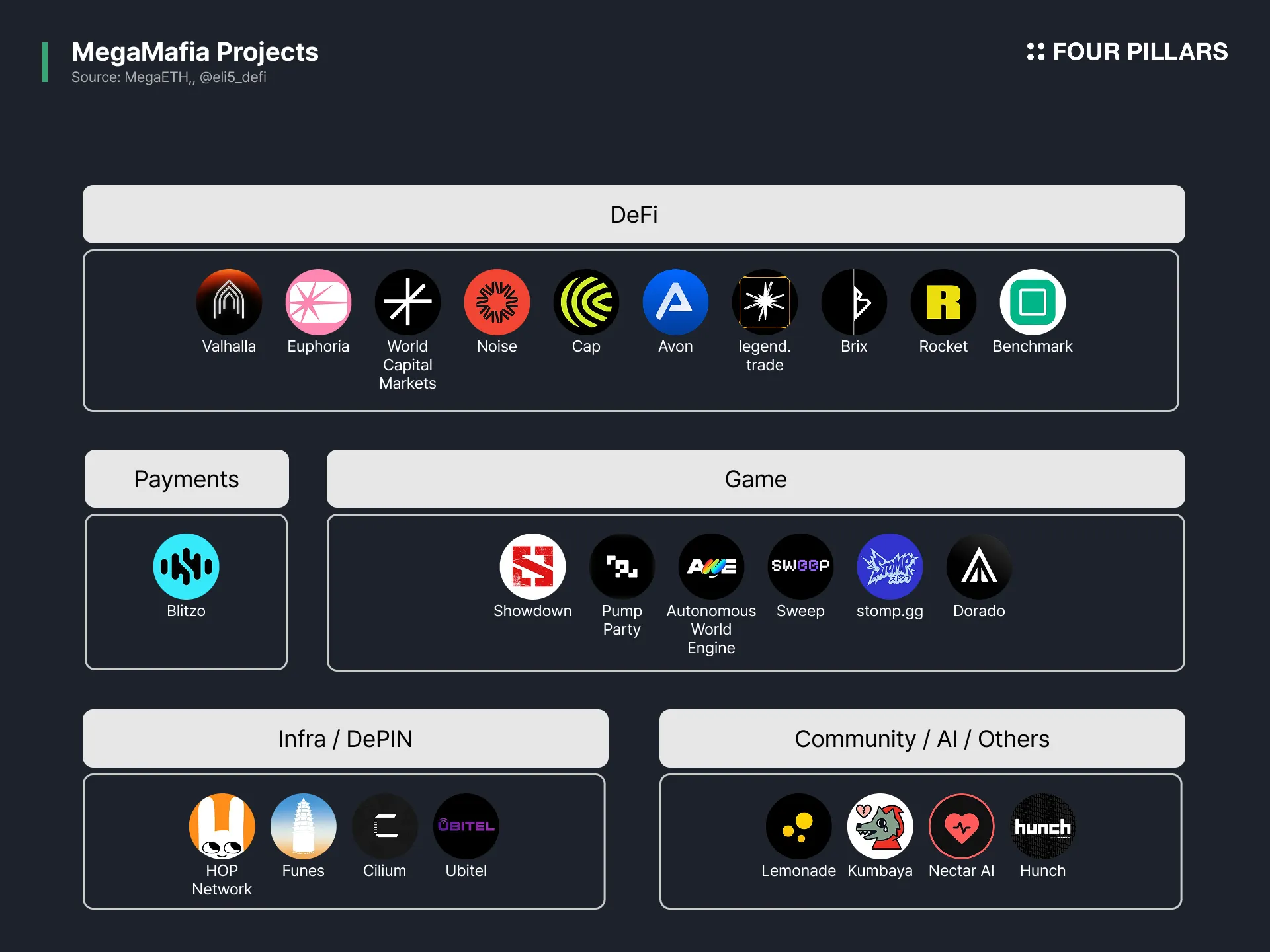

MegaETH adopted a method where the team directly selects and nurtures ecosystem projects through its own accelerator program called MegaMafia. Currently 25 MegaMafia projects are confirmed to be in development, also targeting various sectors. Notably, MegaMafia 1.0 projects alone have already achieved over $40M in total funding. Considering most MegaMafia projects deploy exclusively on MegaMafia, their potential was evaluated very highly. However, many MegaMafia projects, especially MegaMafia 2.0, have only been introduced with very brief descriptions like introduction 1, introduction 2, with services completely undisclosed, making information too limited to evaluate project value. Considering their development stage, realistically fewer than 10 MegaMafia projects are expected to be deployed at MegaETH mainnet launch, and they're expected to pursue an ecosystem strategy concentrating attention on a few apps.

Considering Solana and Base are gradually moving toward institutions based on trust and traditional finance partnerships built through operations so far, the fastest way for Monad and MegaETH to attract their users is building a strong consumer application ecosystem.

For Monad, the first task is attracting liquidity from Solana degens by creating strong volatility within the ecosystem centered on memecoin launchpads like Nad.fun. However, since the Monad community's self-developed cult is quite deep, this will be heavily reflected in the memecoin ecosystem, and if forms where minority communities absorb external capital through cabal plays continue, this remains a concern as a barrier to long-term liquidity inflow.

Source: MegaETH

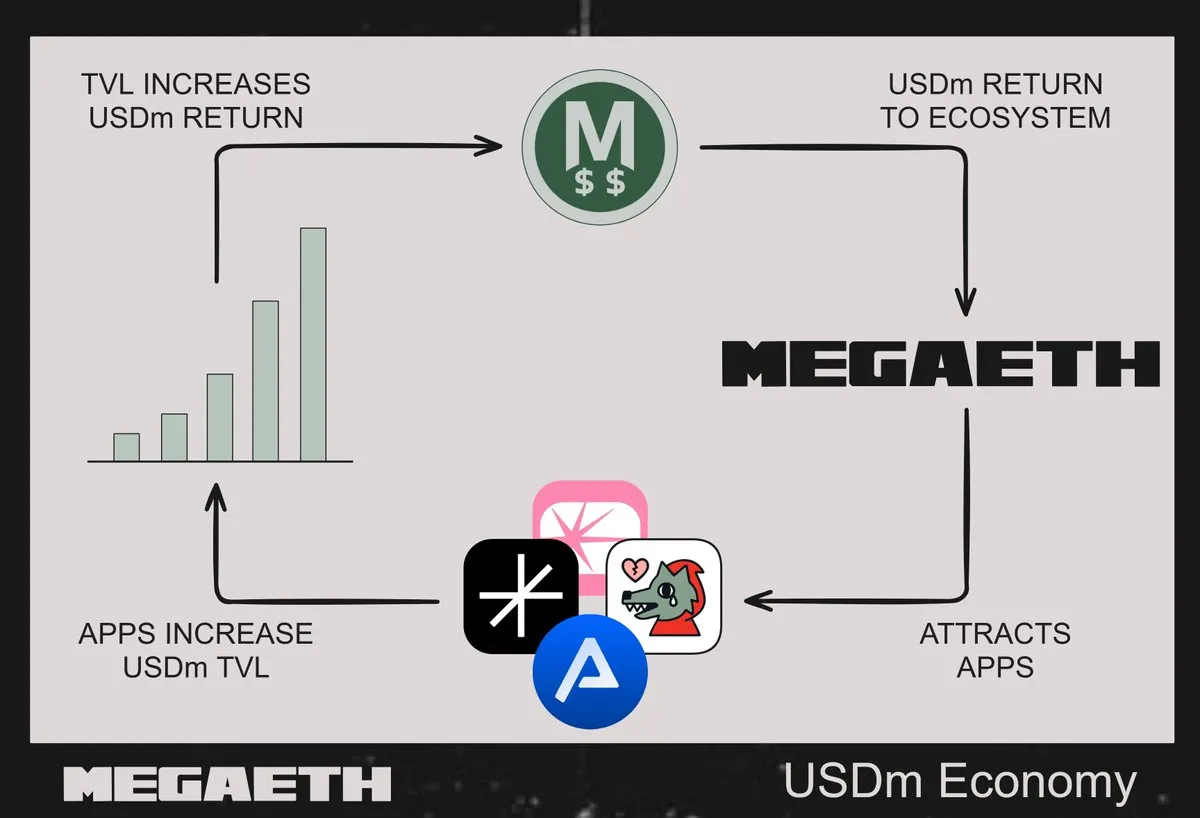

For MegaETH, while unclear if designed with this goal from the start, most MegaMafia-selected projects focus on improving or gamifying user experience of existing ecosystem applications, evaluated as having high novelty compared to recently emerging applications. Therefore, MegaETH ecosystem is advantageously designed to attract users themselves, but since these aren't mostly apps with large capital flows, whether they can attract liquidity appears to be the biggest challenge.

MegaETH appears to have planned launching its own stablecoin, USDM, to solve liquidity attraction problems within the chain. USDM is a stablecoin based on Ethena's USDtb, introduced as using yield generated from itself to maintain user sequencer fees at consistently low levels. However, since interest from USDM doesn't directly go to users, additional incentive design for USDM appears necessary for sufficient liquidity attraction, one being Benchmark Finance, a MegaMafia 2.0 project. Benchmark Finance is a USDM strategy vault built on Morpho, expected to attract significant liquidity in conjunction with MegaETH's limited reward program at mainnet launch. Of course, after the reward program ends, separate incentives to induce USDM deposits must be designed, but as Benchmark Finance is a MegaMafia project, we can expect the possibility of designing strategies with more favorable conditions than other stablecoins in the chain with team support.

For Monad and MegaETH to survive long-term, it will be important to escape the frame of seeing each other as competitors and form an allied front challenging the higher targets of Solana-Base. Actually, examining the two chains' strategies closely reveals more complementary elements than overlaps: Monad's broad community and MegaETH's curated ecosystem could create synergy together, and role division is possible where Monad lowers retail user entry barriers with memecoins and NFTs while MegaETH settles them with innovative on-chain applications. Above all, if these two chains together occupy the next-generation high-performance EVM category and establish themselves as clear alternatives to Solana/Base for builders, they could secure sustainable positioning beyond simple technical specs or temporary incentives. Perhaps the real winner of 2026 won't be either Monad or MegaETH but the new ecosystem alliance they create together, and this might be the scenario existing chains should be most wary of.

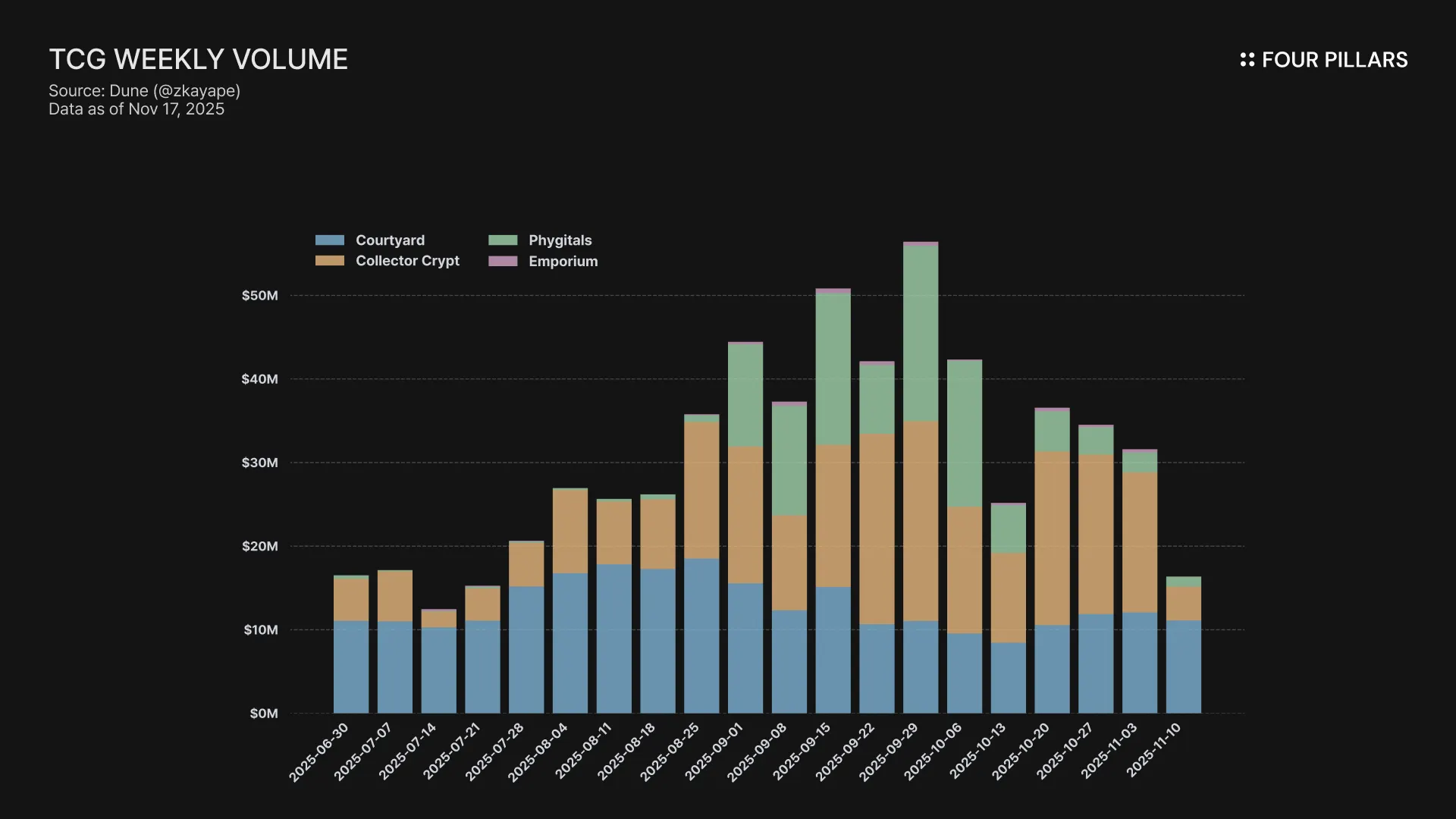

One area expected to grow significantly in 2026 is the physical collectibles marketplace centered on trading cards. The collectibles market has already gone through one rise and fall this year through Pokemon card gacha and marketplace projects, but this was rather an opportunity to clearly reveal what existing projects need to improve. On-chain trading card projects that stood out in 2025 include:

Courtyard: One of the oldest platforms launched in 2023. Pokemon card trading on Courtyard recorded only $242K in March 2024 but reached $28.9M in March 2025, over 100 times more transactions.

Collector Crypt: A Solana-based platform that achieved explosive trading volume through gacha systems and utility token $CARDS. Gacha machines generated over $89 million in total revenue and processed over $150 million in annual trading volume. Particularly notable is the amazing growth from $50K in January 2025 to $50 million in July, 100x growth in 18 months. The $CARDS token recorded over $600 million market cap within a week after launching on August 29, 2025.

Phygitals: Attracted attention with a unique revenue-sharing system providing 1% royalty whenever cards tokenized through the platform are resold. Tokenized over 60,000 cards, processed over 500,000 transactions, and recorded over $30 million in trading volume.

The problem is that except for Courtyard, which launched long ago, the common point of other platforms is they generated massive volume and revenue short-term through highly gambling-oriented gacha systems and expectations for token airdrops.

These projects targeted the difficulty of immediate trading card sales, inducing continuous gacha participation by offering options to immediately buyback gacha-obtained cards at 85-90% of actual trading prices. However, these buyback ratios are exploitative even compared to typical gambling projects, naturally unable to maintain existing user numbers.

Nevertheless, on-chain trading cards clearly have demand and value, which can be summarized in three main reasons:

Solving Liquidity Problems: While purchasing trading cards on eBay typically takes 5 days to receive, on-chain trading allows immediate ownership transfer. Also, since physical condition enormously impacts trading card prices, storage risk exists, but on-chain trading eliminates worries about loss or quality degradation as cards don't physically move from storage. Historically, single cards could only be sold about 60 times annually due to physical movement time, but card tokenization has the great advantage of completely removing transaction frequency limits.

Solving Verification Problems: Trading card value is determined by trusted grading institutions like PSA and CGC. PSA's bulk grading service costs $19.99 per card, and as of 2025 requires 15 business days processing time plus additional grading time. Storing initial grading records and receipts on-chain has the advantage that initial grading status can be inherited directly by secondary traders.

Potential for Derivative Development: In Web2, ownership division of physical cards requires very complex legal processes. And since price indices only occur from pure transaction history, volatility is very high and asset value prediction is opaque. When trading cards are traded through Web3, fractional investment through smart contracts becomes easy, and betting on rare card price fluctuations becomes easier. This fits well with the thesis of "tokenization of all assets" that current prediction market projects have. A representative example of such projects is Trove, which aims to build perpetual futures markets for collectibles on Hyperliquid based on HIP-3.

In 2026, I expect genuine products focused on the essence of trading card marketplaces - liquidity for rare cards, easy tracking and verification of authenticity, low transaction fees - to emerge and absorb some of the huge potential of the Web2 collectibles market. 2026 is particularly Pokemon's 30th anniversary, with various events expected to bring renewed attention to the Pokemon trading card ecosystem. If sustainable infrastructure is successfully built in the Web3 trading card marketplace market in line with this timing, I expect they can establish themselves as winners of the next-generation on-chain collectibles market.

Dive into 'Narratives' that will be important in the next year