Considering the history of financial innovation and the overall trajectory of crypto, the emergence of a crypto super app is inevitable. In particular, as a growing number of USDT specialized infrastructure has emerged, and because the user groups that benefit from USDT and from a super app overlap, the year 2026 is the optimal moment for the rise of a USDT based super app.

As the institutional foundations for stablecoins are being established across the world, the appearance of many types of stablecoins and the fragmentation of liquidity are unavoidable. The time has come for infrastructure that enables one to one clearing and settlement.

After fiat currency and treasuries, the asset class with the greatest potential for tokenization is equities. Tokenized equitiy has been difficult because equities are more complex than other assets, but a variety of new attempts are now underway, and the equity tokenization sector is expected to grow rapidly in 2026.

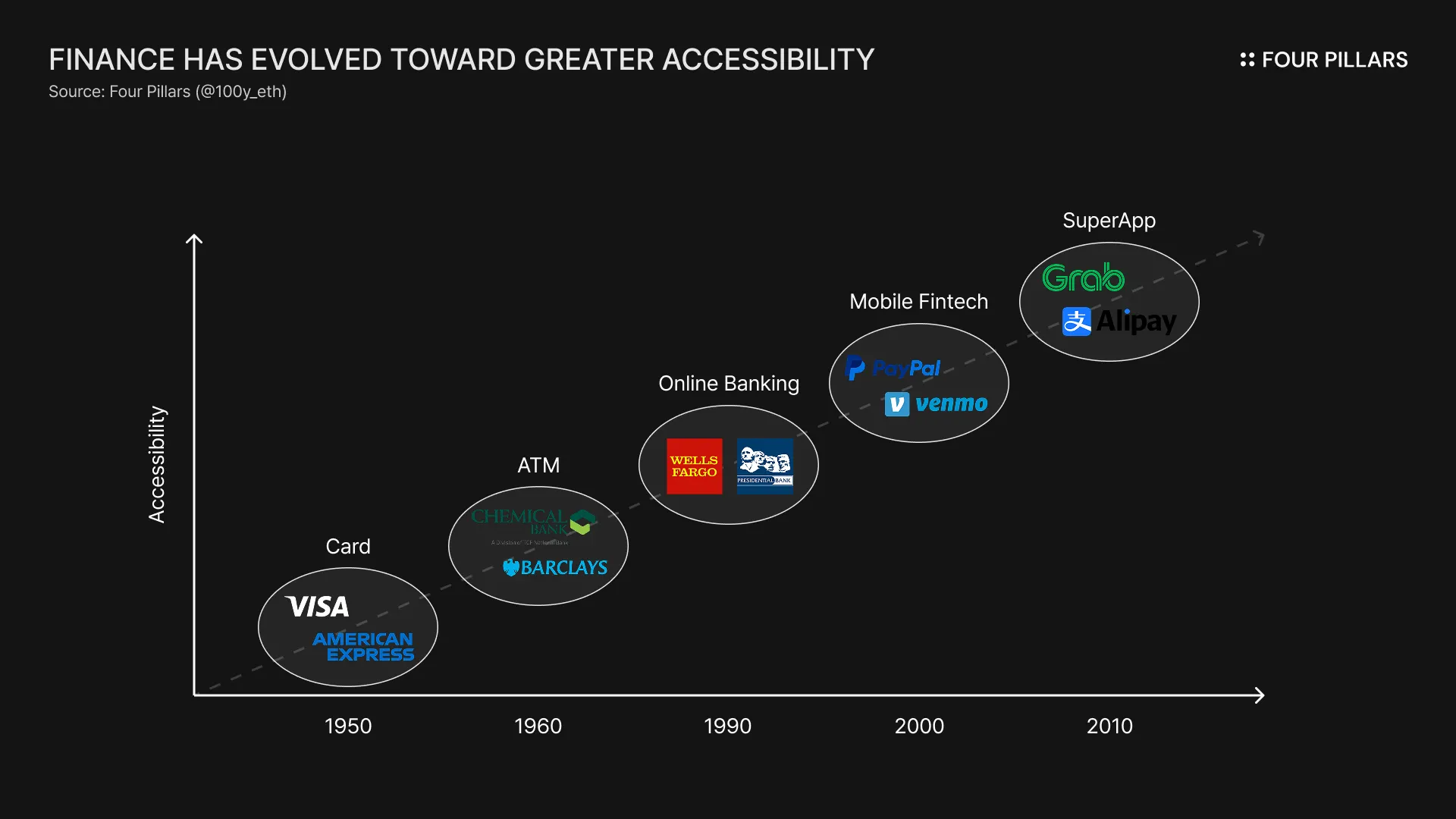

The development of finance can be summarized in one word: “improvement of accessibility.” From the era of cash only, to cards, ATMs, online banking, mobile fintech, and neobanks, leading up to today’s super app era, people have been able to access an increasingly wide range of assets and financial activities.

Today, people can access countless activities through super apps. A super app is a platform that provides multiple services within a single mobile or web app, allowing users to engage in not only real-life activities such as social networking, shopping, and booking, but also financial activities such as payments, remittances, savings, stock trading, and loans. Representative examples of super apps include WeChat, Alipay, and Grab.

So what exactly did super apps innovate? They improved the front-end and user experience (UI/UX) by obtaining the necessary licenses for various financial services. Today, users can easily access multiple financial activities because fintech companies have individually secured these financial service licenses and significantly enhanced their front-end interfaces to deliver seamless user experiences.

However, in traditional finance, back-end processes for different types of transactions are still fragmented across countries and transaction types. This fragmentation continues to create inefficiencies in terms of settlement time, fees, and accessibility. Blockchain can solve these inefficiencies.

“Every stock, every bond, every fund—every asset—can be tokenized. If they are, it will revolutionize investing.”

— Larry Fink (Blackrock CEO)

"We must allow for super app trading platform innovation that increases choices for market participants. Platforms should be able to offer trading, lending, and staking under a single regulatory umbrella."

— Paul Atkins (SEC Chair)

If super apps achieved financial unification at the front-end level, blockchain can achieve financial unification at the back-end level. Because blockchain operates freely across borders and enables instant settlement, it has the potential to process all assets and financial activities from all countries within a single back-end infrastructure.

These blockchain characteristics align closely with the goals of super apps, inevitably leading to the rise of crypto super apps. Many major Web2 and Web3 companies are converging toward this same north star of becoming a crypto super app:

Robinhood: Beyond traditional stock trading, it now offers crypto trading and, through collaboration with Arbitrum, provides tokenized stock and ETF trading services.

Coinbase: Beyond simple crypto trading, it offers a wide range of financial products such as DeFi-linked lending and earn products, staking, cards, and perpetual futures trading, with plans to expand into stock trading via tokenization.

PayPal: Has expanded from traditional remittance and payments to include crypto transfers, payments, and stablecoin-related products, integrating various crypto financial services.

In addition, companies like Lemon Cash, Rappi, and Mercado Pago in Latin America, and PalmPay in Africa, are supporting crypto services and growing rapidly.

Source: Beacon Venture Capital

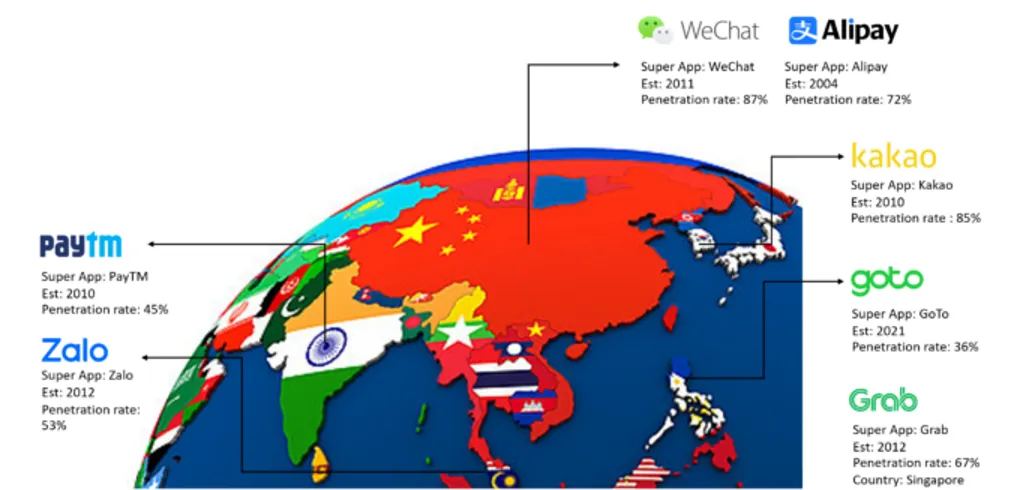

One interesting characteristic of super apps is that they became established faster in Asia and Latin America than in the United States. In the U.S., platforms for each vertical grew independently over a long period, while in Asia and Latin America, there was less time for such development and mobile-first environments were rapidly built. This allowed super apps such as Alipay, WeChat, and Grab to grow quickly.

Source: Chainalysis

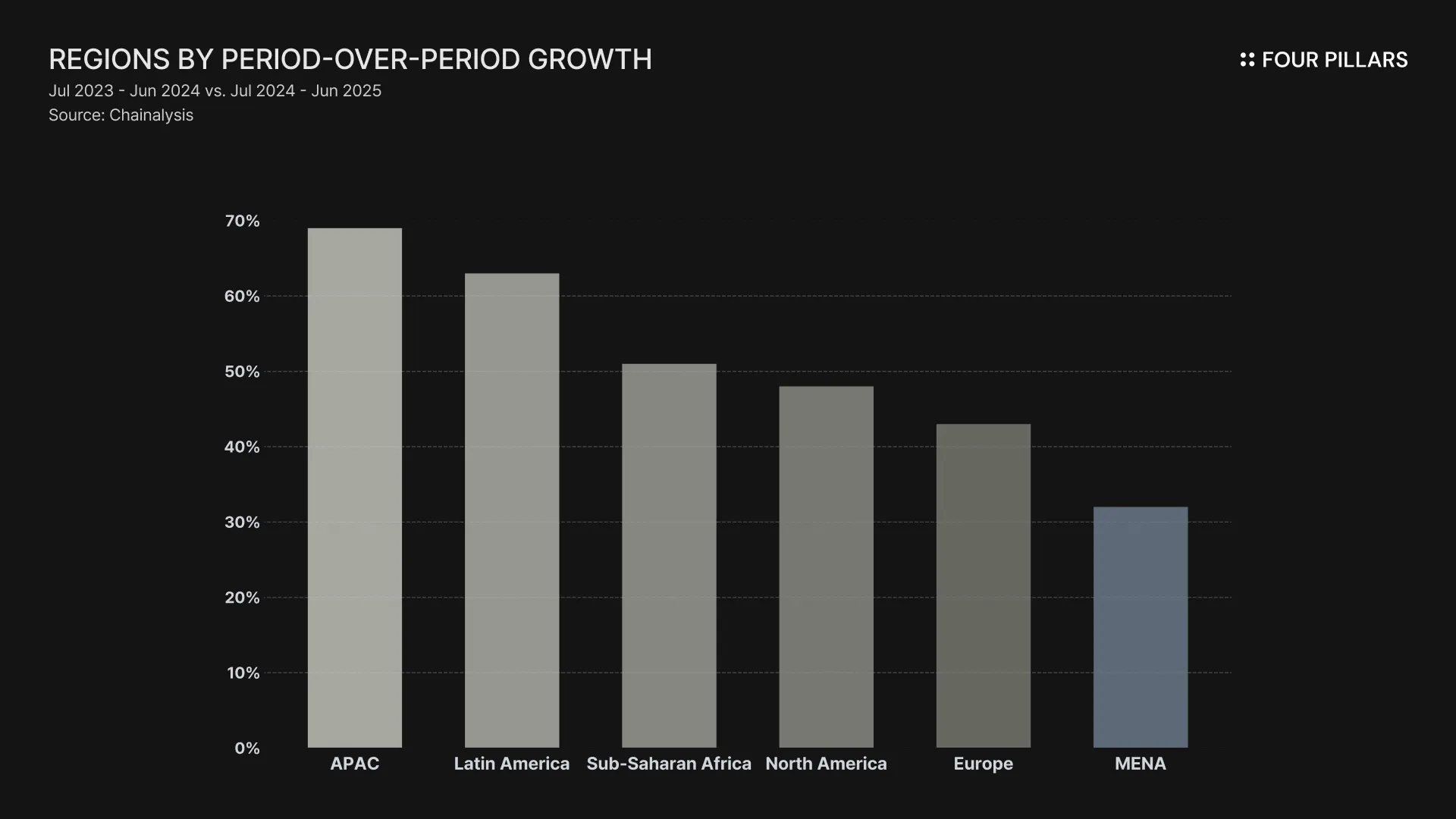

Similar to super apps, crypto provides greater utility in countries where access to legacy financial systems is relatively limited. According to recent research by Chainalysis, the crypto market growth rate in 2025 is projected to be higher in APAC, Latin America, and Sub-Saharan Africa compared to North America and Europe. This suggests a strong synergy between crypto and super apps and implies that the emergence and growth of crypto super apps are inevitable.

Source: BIS

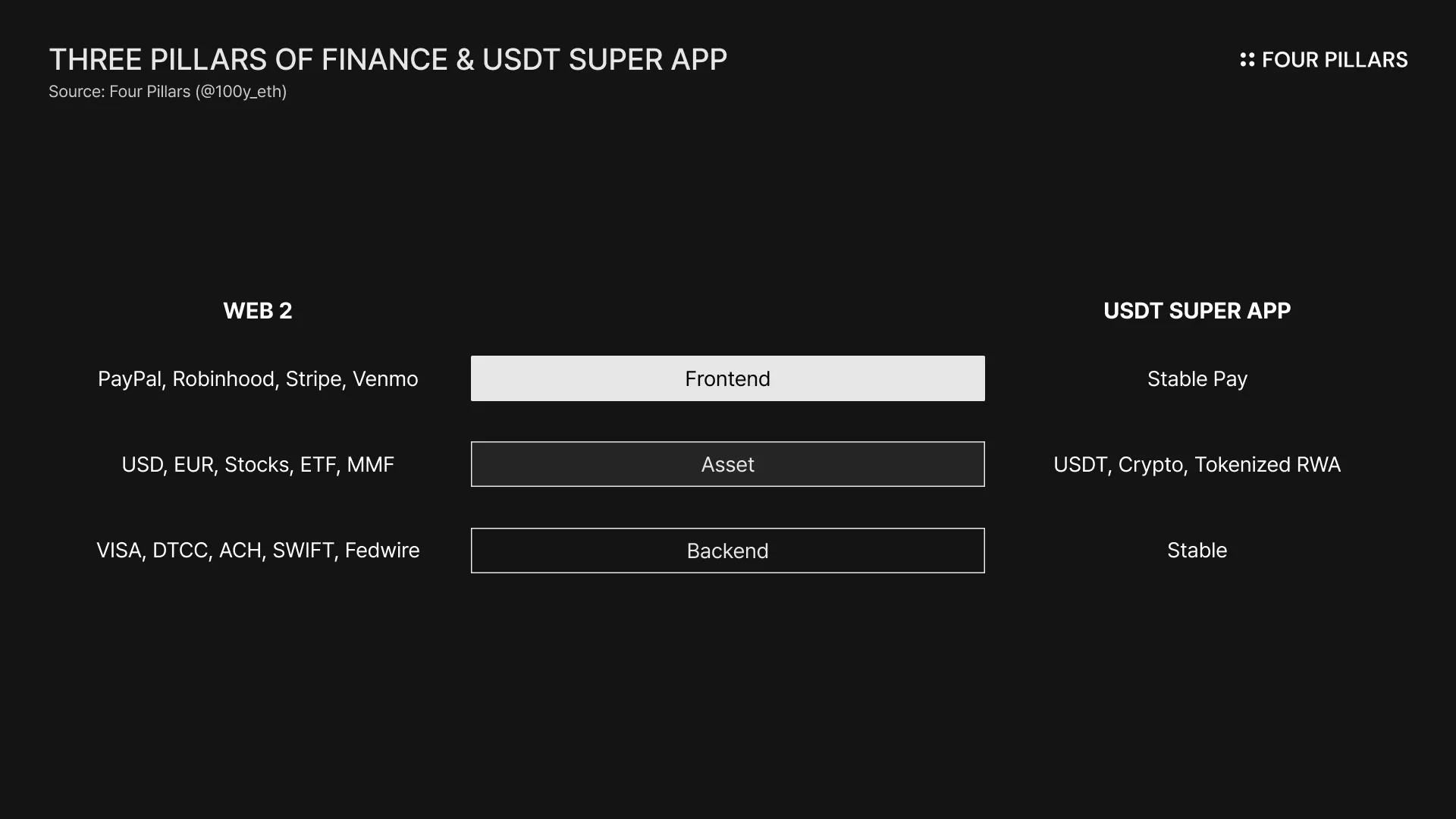

Among the many cryptocurrencies, the asset most compatible with a crypto super app is undoubtedly USDT. Although USDT is a stablecoin pegged to the U.S. dollar, it remains in a regulatory gray area in many countries outside the United States and Europe. This has allowed users in developing countries to easily gain exposure to the dollar. In other words, because the user base where USDT and super apps create value overlaps significantly, the USDT SuperApp is clearly the next paradigm.

From the perspective of the three elements of finance—assets, front-end, and back-end—the year 2026 presents the perfect conditions for the emergence of the USDT SuperApp. First, USDT’s role as an asset is overwhelming. USDT’s scale reaches $183B, with 506M users worldwide and an average daily transaction volume of $59B. According to the MV=PQ equation used to calculate a country's GDP, USDT has immense potential to drive onchain GDP growth due to its massive scale in both money supply (M) and velocity of circulation (V).

Second, on the back-end side, new blockchain networks specialized for USDT have begun to emerge. In the past, most USDT transactions took place on networks such as Tron or Ethereum, which caused significant inefficiencies in USDT transfers. To solve these inefficiencies, USDT-specialized blockchains such as Stable and Plasma have been launched. They serve as optimized back-end infrastructures by providing various USDT-oriented features such as zero-fee USDT transfers and USDT-based gas fees.

With both the asset and back-end in place, the next step is the emergence of the front-end. However, as of now, there is no dedicated front-end for USDT—that is, no USDT SuperApp exists in the market yet. The emergence of the USDT SuperApp is inevitable, and in fact, Stable is currently developing the Stable App. Through the Stable App, users can manage their USDT in a non-custodial manner and use it for instant, free transfers and payments.

The potential of the USDT SuperApp is limitless. Beyond simple USDT management, transfer, and payments, it can incorporate fundamental functions such as DEX and lending, and further introduce advanced features to enhance financial accessibility—such as earn products offering returns from DeFi yields or real-world assets like government bonds, on/off-ramps for fiat swaps, and FX engines enabling currency exchange between multiple countries.

Born in 2014, USDT will find new strength in 2025 and reach its full realization in 2026 as the “USDT SuperApp.”

In July 2025, the GENIUS Act, the first federal stablecoin legislation in the United States, was passed. This brought regulatory clarity to the U.S. stablecoin industry, and now not only existing issuers like Circle and Paxos, but also a wide variety of companies are showing interest in issuing stablecoins:

Banks: Major financial institutions such as Citigroup, Bank of America, Goldman Sachs, and Deutsche Bank have mentioned the potential for issuing stablecoins and have entered the exploratory phase.

E-commerce and retail companies: Companies like Amazon and Walmart have long been interested in issuing their own stablecoins to reduce payment processing fees and improve settlement speeds.

IT companies: Internet infrastructure company Cloudflare unveiled the NET Dollar, a stablecoin designed for AI agent payments.

Web3 companies: Many Web3 firms are preparing stablecoins that comply with the GENIUS Act, including Tether’s USAT, XRPL’s RLUSD, Ethena’s USDtb, and Frax’s frxUSD.

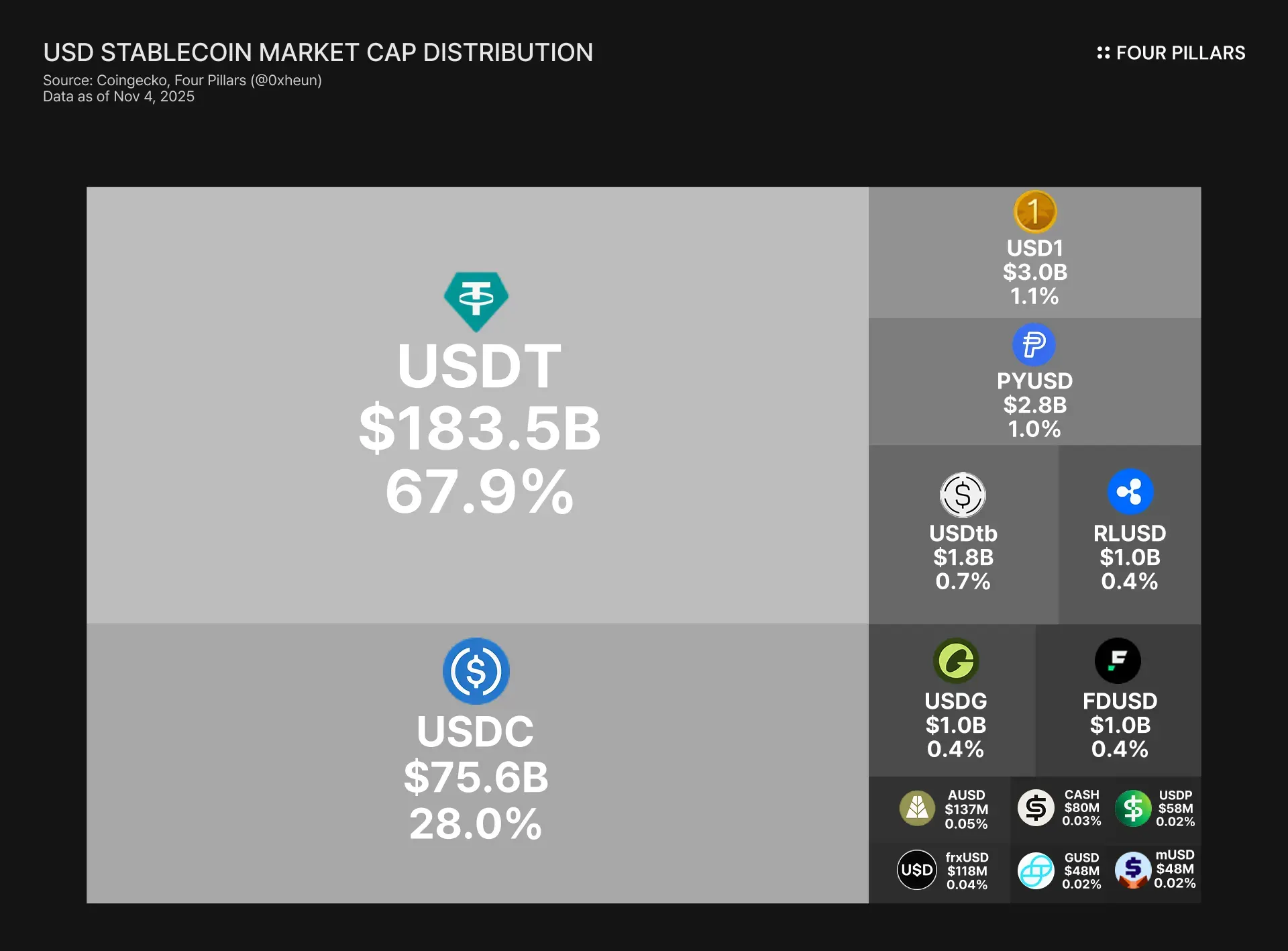

With numerous dollar stablecoins like USDT, USDC, and PYUSD already in existence, the full implementation of the GENIUS Act will likely lead to an explosion of new stablecoins. Some predict that most of these coins will fail due to lack of demand, except for the top few, but I disagree. Many banks and commerce companies already have massive user bases, so even after issuing their own stablecoins, they will be able to sustain meaningful circulation and usage volumes.

The biggest foreseeable issue here is liquidity fragmentation among stablecoins. If different platforms support different stablecoins, users will be forced to exchange them in order to use various services, which will inevitably cause friction.

If stablecoin swaps pegged to the same currency continue to occur only through AMMs or order book exchanges, perfect 1:1 exchange ratios cannot be guaranteed. Even on Binance, one of the deepest exchanges, the USDT/USDC pair shows notable volatility. While small trades can tolerate this level of slippage and fluctuation, in a future where stablecoins achieve mass adoption, an entity that guarantees 1:1 exchange between stablecoins will be essential.

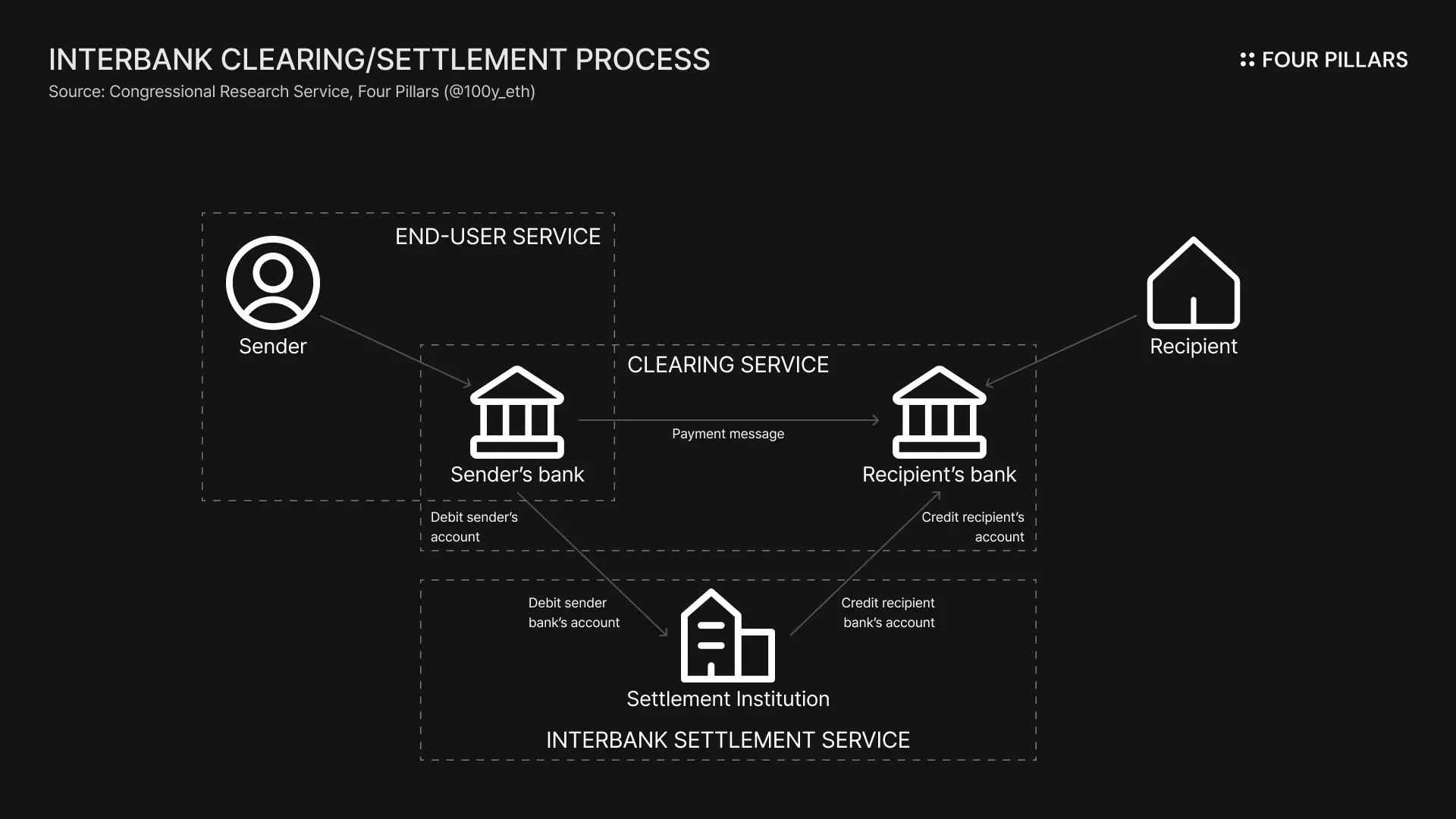

But wait, how do bank transfers between different banks in traditional finance achieve a 1:1 ratio today? For example, suppose you transfer 100 dollars from your JPMorgan Chase account to a Bank of America account. In other words, 100 jpmUSD is being converted into 100 boaUSD. How is this 1:1 exchange guaranteed?

The answer lies in interbank clearing and settlement. Clearing is the process of verifying the details of a transaction after it occurs but before the actual transfer of assets. It determines how much each financial institution owes or is owed. Settlement is the subsequent step where the actual transfer of assets occurs and the transaction is finalized. When transfers happen between different banks, they are cleared and settled through ACH or FedNow operated by the Federal Reserve, or through RTP (Real-Time Payments) operated by The Clearing House. This ensures the 1:1 transfer of funds.

However, the stablecoin ecosystem still lacks robust clearing and settlement infrastructure. For smooth mass adoption of stablecoins, we need an entity that guarantees 1:1 exchange among stablecoins pegged to the same currency. In other words, we now need a stablecoin clearing house.

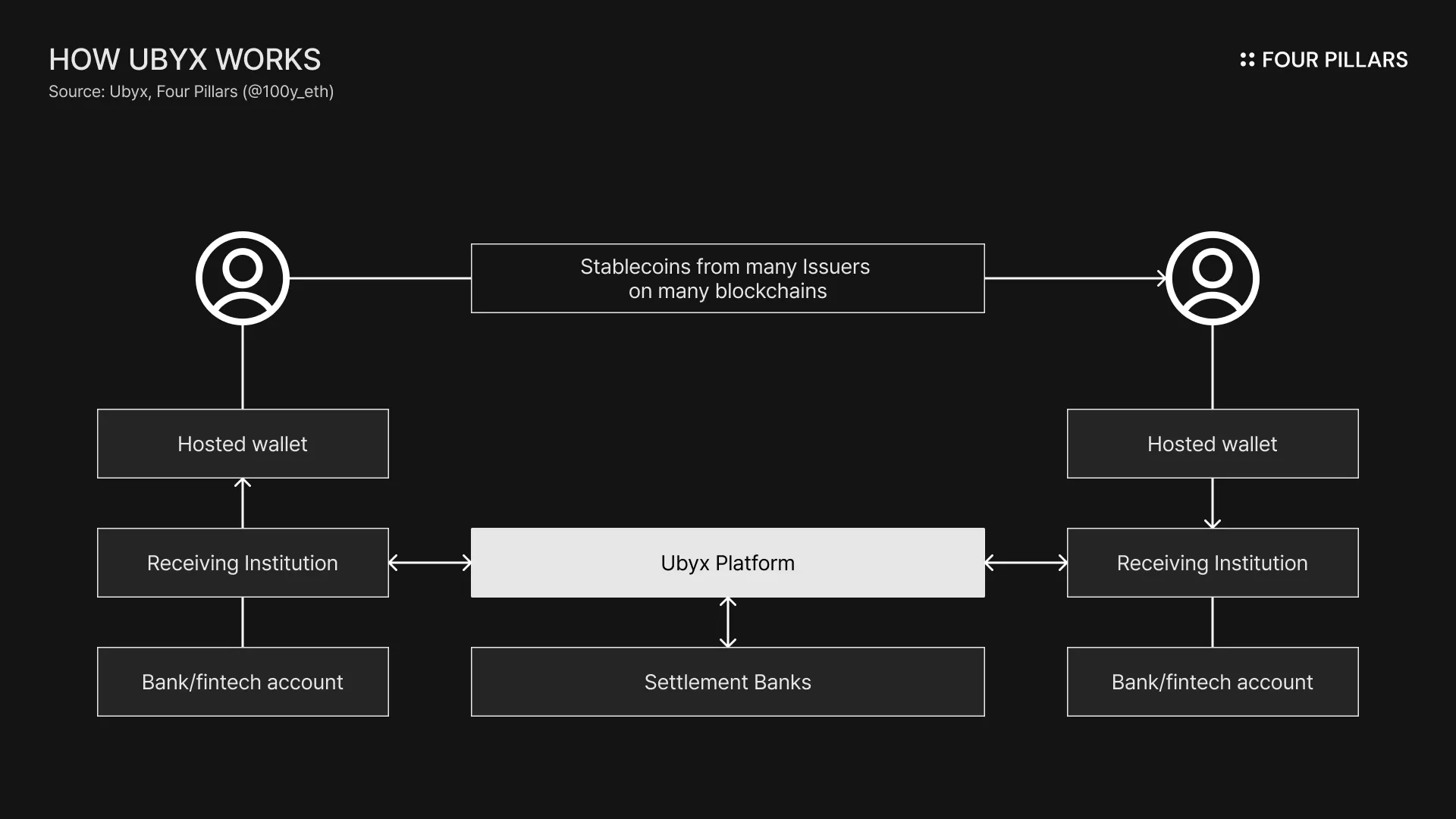

Unfortunately, the current market is still focused on stablecoin issuance and distribution. There is no entity that guarantees 1:1 exchange between different types of stablecoins. Recently, however, a startup called Ubyx has emerged to address a similar problem.

Previously, each issuer had to establish separate one-to-one contracts with individual financial institutions to enable full redemption. Ubyx changes this model into a many-to-many connection, allowing users to seamlessly exchange stablecoins for cash in bank accounts regardless of the issuer. This is similar to how the Visa card network connects a vast number of consumers and merchants. While Ubyx primarily guarantees 1:1 redemption rather than 1:1 exchange among stablecoins, it can indirectly serve as a stablecoin clearing system.

Then, how can we build a stablecoin clearing house that not only ensures 1:1 redemption but also enables 1:1 exchange? There are two possible approaches:

First, a central bank-led model. Today, 1:1 exchange between deposits at different banks is mediated and guaranteed by the central bank. Stablecoins could adopt a similar approach, but legal questions remain as to whether stablecoins can be treated as money, and since their collateral structures vary, it would be difficult to implement in the short term.

Second, an inventory-based model. Financial institutions with large capital reserves could hold various types of stablecoins as inventory. This would allow them to guarantee 1:1 exchanges to customers without directly interacting with each issuer for minting or redemption. While this approach is straightforward, it suffers from low liquidity efficiency since it requires holding a wide variety and large volume of stablecoins in inventory.

Beyond these, there are many considerations for building a stablecoin clearing house. For instance, even if two stablecoins are both pegged to the dollar, USDC complies with the GENIUS Act while USDG follows Singapore’s MAS framework. We must carefully consider how to guarantee 1:1 exchange between stablecoins under different regulatory jurisdictions.

Stablecoins are the future of money, and for them to become true money, we need the singleness of money. It is time to start discussing the stablecoin clearing house.

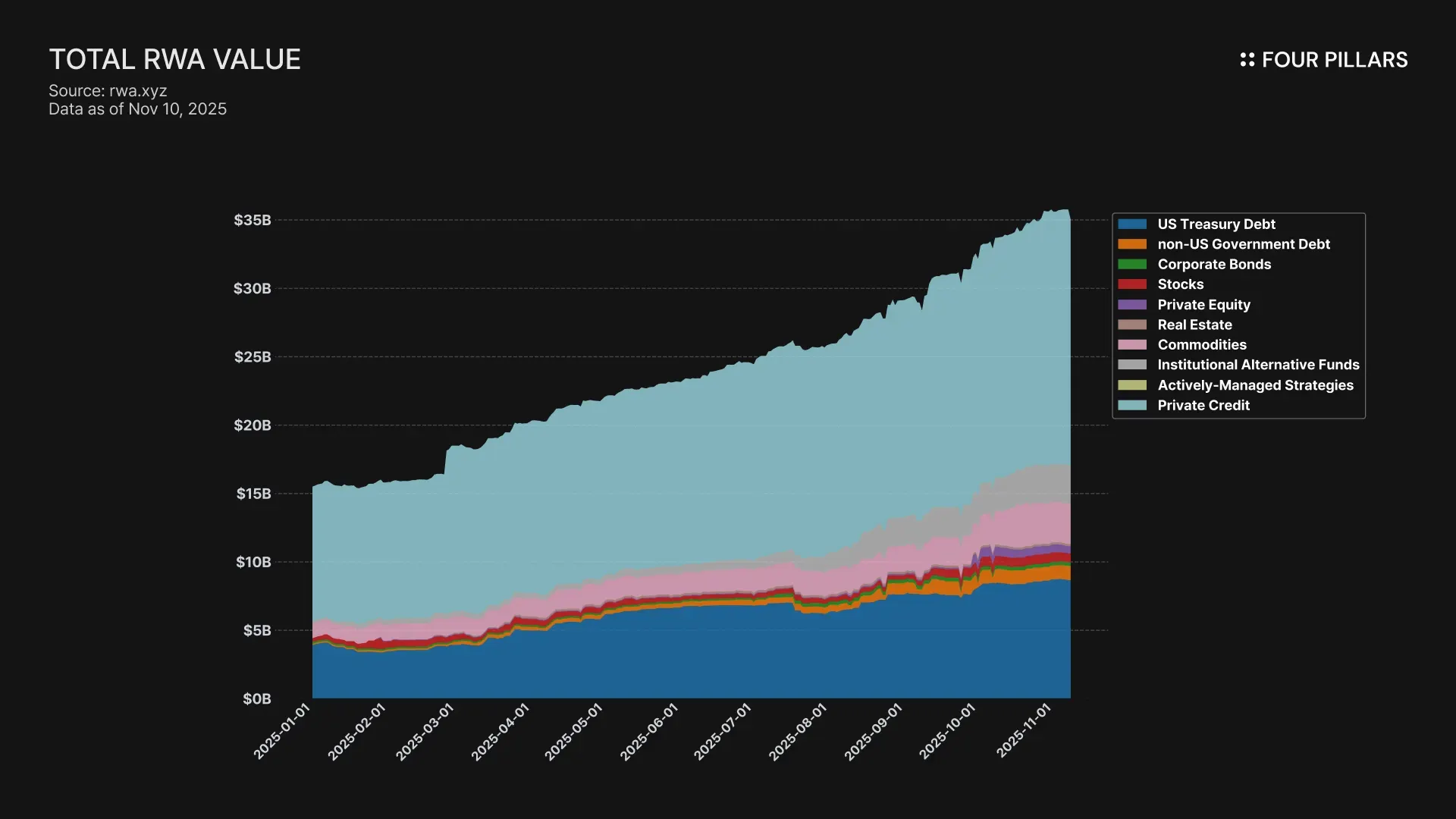

If I were to choose just one sector that grew the fastest in 2025, it would undoubtedly be RWA. While the total issuance of stablecoins increased by around 50% during the year, the RWA sector grew by an astonishing 133%. Compared to the approximately 300 billion dollar stablecoin market, RWA still sits around $35B, leaving tremendous room for growth.

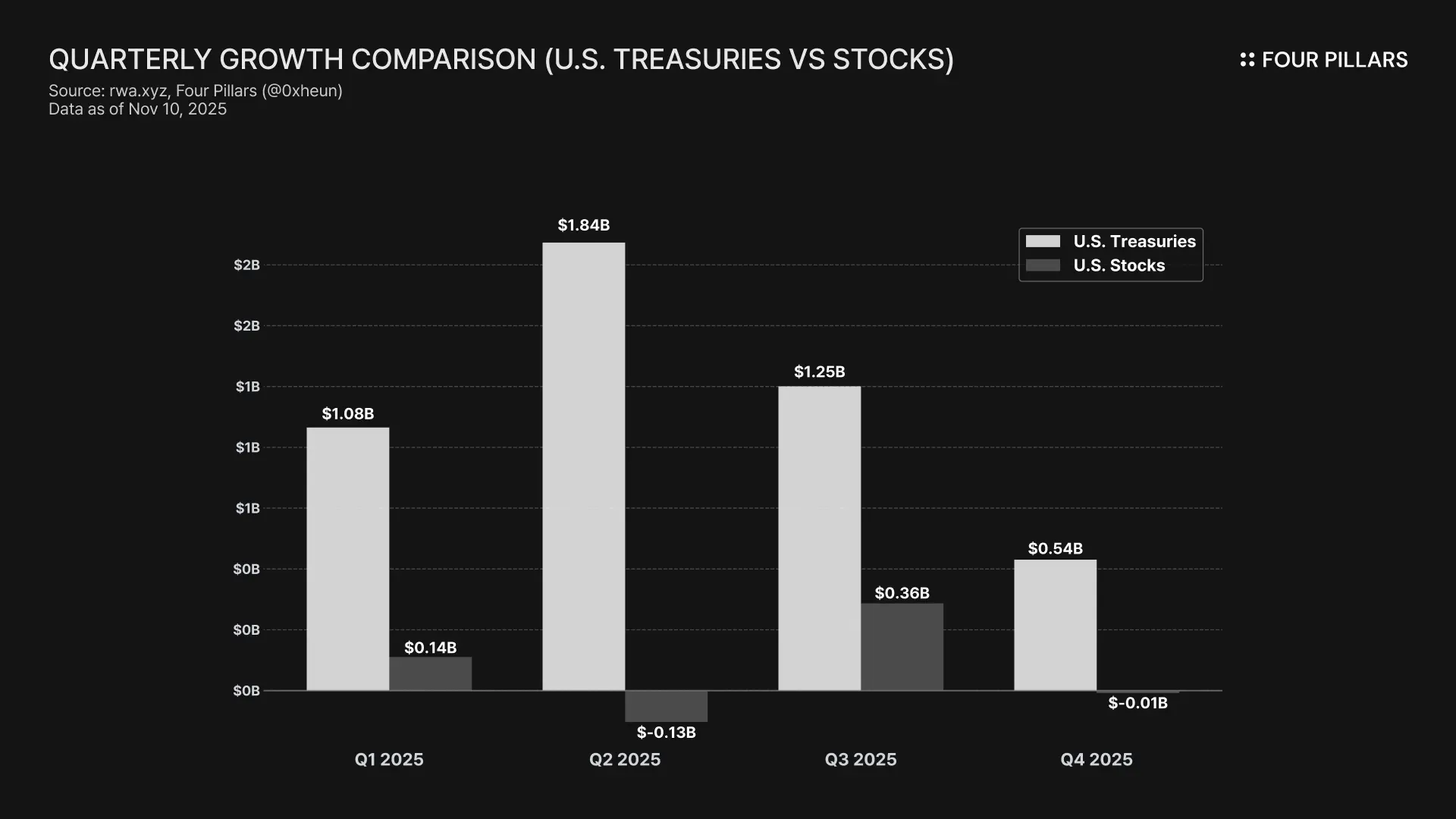

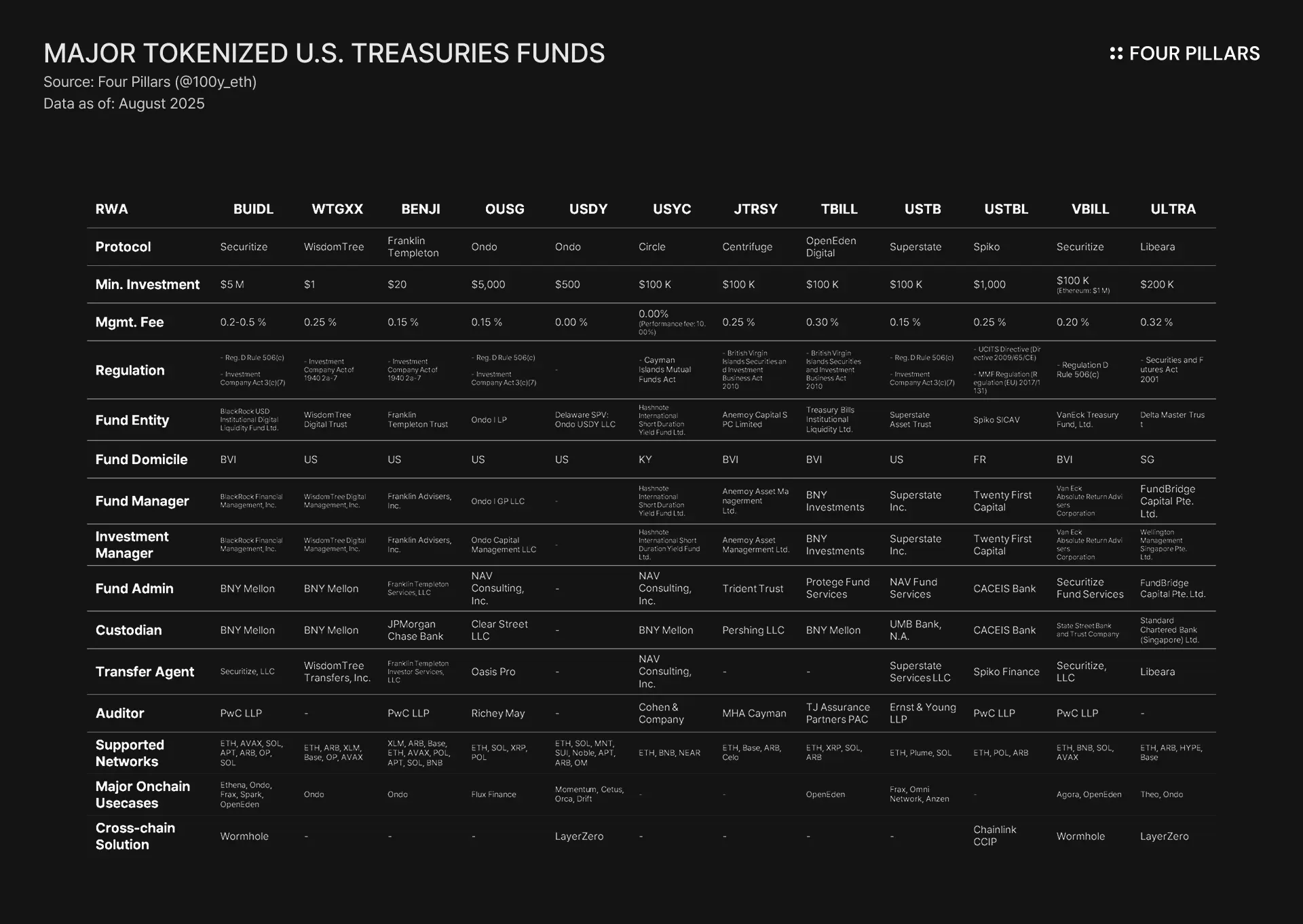

Among RWAs, the most rapidly growing asset class has been funds backed by U.S. short-term Treasury bills. The tokenized U.S. Treasury market, which was about $4B in January 2025, more than doubled to over $8B by the end of the year. Various asset managers and tokenization platforms have successfully tokenized U.S. short-term Treasury funds, including BlackRock’s BUIDL, Circle’s USYC, Franklin Templeton’s BENJI, Ondo’s OUSG, and WisdomTree’s WTGXX.

But wait, when we think of investments, stocks are just as prominent as bonds. So what about the stock tokenization market? Unfortunately, while the tokenized U.S. Treasury market is around $8.7B, the tokenized stock market remains at only about $700M. This gap results from several factors, including limited investor demand and the significant legal barriers associated with tokenization.

Tokenized U.S. short-term Treasury funds are straightforward in both demand and tokenization methodology. The bond market consists of various short-term maturities and repos, but money market funds (MMFs) that bundle these instruments into baskets are highly attractive because they provide stability and steady returns. This makes them particularly appealing to investors who previously lacked access to U.S. bonds and to onchain protocols managing large treasuries.

Moreover, the rights associated with U.S. short-term Treasury funds are primarily limited to profit claims, making their ownership structure simple and intuitive. As shown in the table above, the tokenization process for such funds is highly standardized. Depending on jurisdiction, a fund is established, and its share registry is recorded onchain by a transfer agent, enabling easy tokenization.

By contrast, what about stocks? Unlike bonds, the stock market consists of a vast number of individual companies, making it extremely difficult to maintain liquidity across all tokenized equities. In addition, stocks grant not only profit rights but also voting and governance rights, which are challenging to represent fully through tokens.

For these reasons, unlike the highly standardized Treasury tokenization market, the stock tokenization market remains small and fragmented. The few players that exist tokenize in different ways, leading to significant fragmentation in both regulation and process.

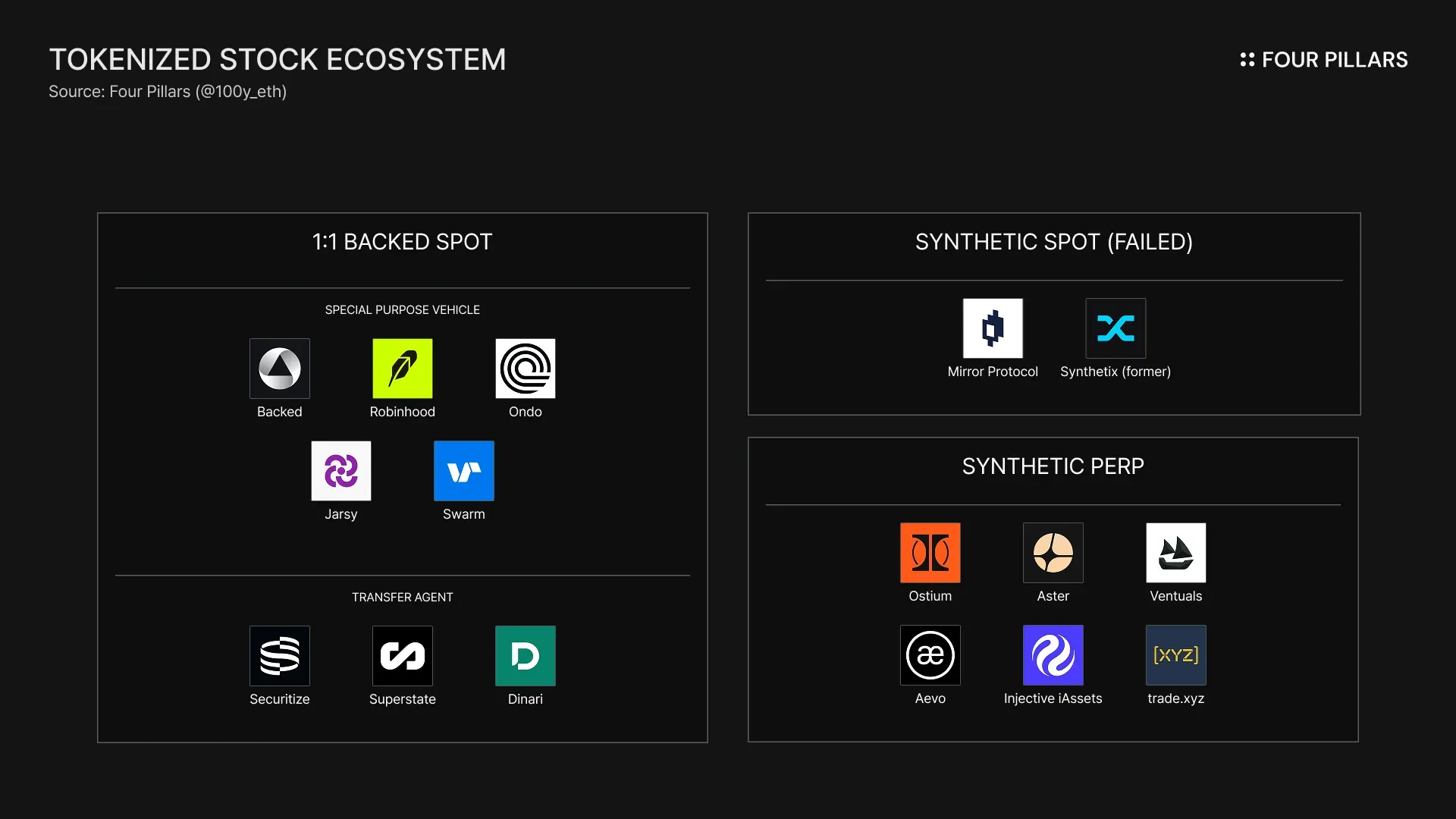

For these reasons, stock tokenization is currently being carried out in various ways. Depending on whether the underlying assets are backed, the regulatory framework, and the trading mechanism, the major approaches can be categorized as follows:

1:1 Backed Spot (SPV): An SPV holds the actual stocks and tokenizes the profit rights onchain. The advantage is that the tokens are fully backed 1:1 by real stocks, but the issuance and redemption process is inefficient, and rights other than profit claims are not tokenized.

1:1 Backed Spot (Transfer Agent): A transfer agent regulated by the SEC records and manages stock ownership directly onchain. This is very similar to how U.S. Treasury funds are tokenized. Unlike the SPV model, this approach allows for tokenization of all rights, including voting rights, but due to regulation, investors must meet specific eligibility requirements to trade such stock tokens.

Synthetic Spot: A synthetic asset collateralized by crypto that tracks the price of a particular stock. Although it is backed by collateral, this synthetic asset does not represent any of the original stock’s rights and lacks stability under market stress, which is why it is no longer in use.

Synthetic Perp: A perpetual futures market model that uses oracles and liquidity providers to allow trading of an index tracking the price of a specific stock. It provides the most straightforward way to gain stock exposure, but it does not involve actual stock ownership, dividends, or voting rights, and it is not legally viable in jurisdictions with well-established securities laws such as the United States or Europe.

There is still a long journey ahead. When people discuss the advantages of stock tokenization, they often mention features such as 24/7 trading, faster settlement, composability in onchain money legos, and global accessibility. However, these are idealized scenarios. If someone speaks this way, they are either working in stock tokenization or have not done enough research.

Stocks are fundamentally regulated under national securities laws, making it difficult to fully leverage blockchain’s benefits. Stock tokens face numerous obstacles:

Diverse rights associated with stocks: The rights inherited by token holders vary widely depending on the tokenization method. The most ideal approach today is for licensed transfer agent platforms like Securitize or Superstate to directly tokenize equities onchain, as this is the only way to fully inherit all shareholder rights.

Regulatory risk: Models such as SPV-based 1:1 backing or synthetic perpetuals do not comply with U.S. regulations, and therefore cannot legally serve U.S. investors.

Accessibility: In transfer agent-based tokenization, holding, transferring, and trading tokens require strict investor eligibility, which limits accessibility for global retail investors.

Counterparty risk: Although SPV structures isolate assets to protect investors, as seen in cases like FTX, the existence of intermediaries still introduces counterparty risk.

Price divergence: Outside regular stock market hours, there are no reference prices for underlying assets, making it impossible for market makers to hedge. As a result, spreads widen, discouraging investors, reducing onchain liquidity, and creating a vicious cycle.

Onchain user persona: In traditional finance, crypto ETFs and DAT companies have helped large institutional capital flow into the crypto market. However, considering the typical onchain user persona, stock tokens are less attractive due to regulation, KYC requirements, regional restrictions, and low liquidity.

Onchain integration: Integrating stock tokens into DeFi is not easy. Stock tokens compliant with U.S. securities law can only be used by qualified investors, while non-compliant tokens cannot legally serve U.S. users.

The reason there are multiple methods for tokenizing the same stock is that stock tokenization is still in a transitional phase. But seen differently, the fact that various companies and protocols are experimenting with their own approaches shows how much untapped potential exists in the stock tokenization sector.

The RWA tokenization market will continue to grow rapidly. As the tokenized U.S. Treasury market matures, it is now the stock token’s turn. Stock tokenization is not only an area of interest for Web3 protocols and fintech firms but also for traditional financial institutions such as Nasdaq and DTCC. Stock tokenization is an inevitable future.

If 2025 was the year that saw numerous experiments in stock tokenization, 2026 will be the year when stock tokenization becomes more mature and standardized.

Dive into 'Narratives' that will be important in the next year