Institutional investors appear to be shifting their crypto strategies from Bitcoin to Ethereum. In this trend, “The Ether Machine” is formulating a strategy that goes beyond simply holding ETH—aiming to generate returns as an “active ETH-generating enterprise.”

While MicroStrategy focused on holding Bitcoin, The Ether Machine is building a leveraged operation model based on ETH. This not only introduces a new revenue model but also brings overlapping financial, technical, and regulatory risks, creating structural vulnerabilities that could impact the entire system.

If successful, The Ether Machine could establish itself as a “post-MicroStrategy” model. However, failure might lead institutional investors to retreat from on-chain strategies. Their direction will be revealed through disclosures, regulatory developments, performance metrics, and ecosystem responses.

Source: Strategy X

In the summer of 2020, MicroStrategy kicked off a wave of corporate treasury-style crypto investments by adopting Bitcoin as a corporate reserve asset. Now, five years later, that institutional focus appears to be shifting toward Ethereum. At the center of this trend is growing competition among publicly traded companies seeking to claim leadership in Ethereum dominance. Just as MicroStrategy successfully positioned Bitcoin as “digital gold” and an “inflation hedge,” these companies aim to redefine Ethereum as “productive digital oil” or “yield-generating internet bonds.”

Leading this movement are SharpLink Gaming (SBET) and BitMine Immersion Technologies (BMNR). SharpLink briefly became the largest ETH-holding company, acquiring 280,706 ETH and staking nearly all of it using funds raised via an at-the-market (ATM) offering. The company introduced a proprietary metric—the “$ETH Concentration Indicator,” representing ETH held per 1,000 diluted shares—to emphasize transparency and help investors intuitively assess asset value. BitMine later overtook SharpLink by securing 300,657 ETH, worth roughly $1 billion, and set a goal of acquiring and staking 5% of total ETH supply. Other companies such as Bit Digital and Ether Capital have also joined this emerging race.

Within this landscape, “The Ether Machine” has entered the fray. The company is aiming for a NASDAQ listing via a SPAC merger and has set ambitious targets of raising over $1.5 billion in initial capital and securing more than 400,000 ETH. If achieved, this would make it the world’s largest public ETH holder by disclosed reserves.

Source: Cointelegraph X

The Ether Machine recently drew fresh market attention after securing investment from Pantera Capital, a leading venture capital firm in the blockchain space. This wasn’t just a funding event—it signaled mainstream institutional validation of The Ether Machine’s model as an “active ETH-generating enterprise” with long-term strategic potential. Pantera reportedly appreciated the company’s plan to go beyond merely holding ETH, actively engaging in staking and restaking to contribute to the Ethereum network and generate revenue. This endorsement could serve as a strong trust signal to attract further institutional capital and fuel future business expansion.

What truly distinguishes The Ether Machine, however, is not its ETH holdings but its operating philosophy. The company doesn’t view itself as a passive ETH holder or Ethereum ETF proxy. Instead, it positions itself as an “Active ETH Generation Company,” seeking to transform ETH from a static asset into a productive one—one that actively yields returns through staking, DeFi participation, and infrastructure contribution.

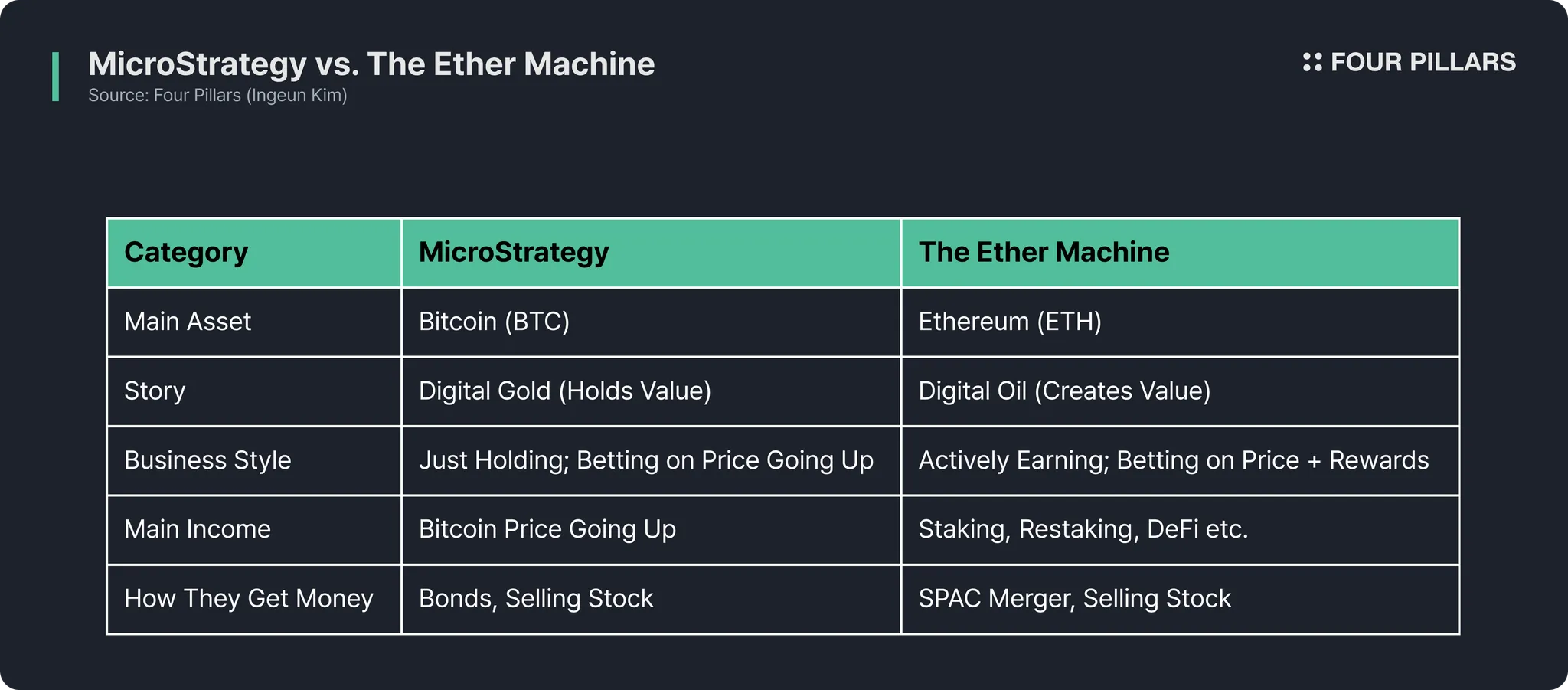

To fully understand The Ether Machine’s strategy, it must be compared with its archetype—MicroStrategy. While both companies center their models around crypto assets, they diverge fundamentally in the nature of the underlying asset, funding mechanisms, and business models.

Source: Medium | Modern Techno

MicroStrategy’s strategy revolves around Bitcoin’s scarcity and store-of-value properties. Bitcoin is a non-productive asset—it doesn’t generate yield by itself—but its strictly limited supply and the “digital gold” narrative support a long-term appreciation thesis. MicroStrategy’s conviction is rooted entirely in that narrative.

In contrast, The Ether Machine focuses on Ethereum’s productivity. ETH powers decentralized applications (such as DeFi), is widely used as collateral, and generates steady yields through proof-of-stake (PoS) staking. Rather than being passively held, Ethereum becomes a “productive asset” through active participation in the network. The Ether Machine’s strategy is directly linked to this productive utility.

Both companies deploy leverage to acquire crypto assets, but each utilizes sophisticated financial engineering. MicroStrategy pioneered the use of convertible senior notes, issuing debt at low interest rates in exchange for giving investors an option to convert the debt into equity. Investors accept lower interest in exchange for this optionality—if the stock price rises (typically correlated with Bitcoin’s price), they can convert their debt into shares and profit from capital gains. The high volatility of MicroStrategy’s stock, driven by Bitcoin exposure, increases the value of this option, allowing the company to raise capital at minimal cost.

This creates a powerful feedback loop: debt issuance leads to Bitcoin purchases → Bitcoin price increases → MicroStrategy’s stock rises → more favorable debt issuance conditions → more Bitcoin purchases.

The Ether Machine is expected to adopt a similar playbook post-SPAC merger, using a mix of debt and equity issuance to finance ETH accumulation.

The most fundamental difference between the two lies in their business models. MicroStrategy is essentially a leveraged Bitcoin holding company. Its legacy software business has become secondary; the firm’s fate now depends almost entirely on Bitcoin appreciating faster than the cost of its debt.

The Ether Machine, by contrast, positions itself as a leveraged Ethereum operating company. Rather than passively holding ETH, it seeks to actively generate “alpha” through staking, restaking, and deploying assets into vetted, secure DeFi protocols. This model not only captures ETH price appreciation but also grows the ETH balance itself—creating a dual-revenue structure. Furthermore, its plan to build infrastructure solutions for other institutions introduces a potential B2B service revenue stream, giving the company a much more dynamic operating profile.

The Ether Machine’s vision of the future presents massive upside potential—but with that opportunity comes a web of risks. Its success hinges on the ability to maximize the compounding effects of productive assets, while failure may stem from an inability to manage multilayered risks.

The Ether Machine’s core strength lies in its ETH-denominated compounding yield structure. Unlike the Bitcoin strategy that solely depends on price appreciation, The Ether Machine aims to increase the quantity of ETH held. Through consistent reinvestment of staking and restaking rewards, the ETH balance can grow exponentially via compounding, independently of dollar-based price volatility. This differentiates it from MicroStrategy’s passive holding model.

To maximize this compounding structure, The Ether Machine may construct a multilayered yield portfolio beyond basic ETH staking. Although still in its early phase, the following strategies may unfold:

Foundation Yield: Establishing a stable income base through liquid staking. Given the technical and liquidity constraints of running validator nodes directly at scale, institutional-grade platforms like Lido, Figment, or Kiln are likely choices. These allow ETH to become a yield-generating asset immediately while preserving liquidity.

Yield Amplification: On top of foundational yield, liquid restaking offers a way to boost returns. This strategy leverages ETH already staked via EigenLayer as collateral to earn additional rewards. Rather than taking on direct protocol risk, The Ether Machine can pursue a dual-income structure by utilizing Liquid Restaking Token (LRT) protocols such as EtherFi, mETH Protocol, and Renzo—capturing both staking and restaking yields simultaneously.

Active Alpha Generation: There’s also room for alpha-seeking strategies that exploit market inefficiencies. For example, constructing delta-neutral positions with ETH spot and perpetuals (as seen in Ethena’s model) to earn funding rates without directional exposure. Another is concentrating liquidity within a price band on Uniswap V3 to maximize fee income. These approaches require sophisticated asset management and risk controls.

Business Model Expansion:

Once performance is validated and operations mature, The Ether Machine can evolve into a Validator-as-a-Service provider—managing ETH on behalf of third parties in exchange for fees. This would shift the company from pure asset manager to infrastructure provider within the Ethereum ecosystem, aligning with a long-term vision to become a core institutional enabler.

Through this progression—from staking, to restaking, to DeFi deployment, and finally to infrastructure services—The Ether Machine could build a powerful ETH compounding flywheel:

ETH yield → reinvestment → asset growth → increased yield.

If this flywheel functions as intended, The Ether Machine may achieve a new model for sustained asset growth—less sensitive to market volatility, and rooted in productive on-chain capital efficiency.

3.2.1 Financial and Market Risk: The Dangers of Leverage

The Ether Machine employs leverage to acquire ETH. If ETH experiences a sharp price drop, the value of its liabilities could exceed its assets, potentially leading to insolvency. In such a scenario, the company's stock may be even more volatile than ETH itself. Complex instruments like convertible bonds also introduce dilution and default risks.

In short, while earnings can compound, losses are magnified by leverage. This structure enables rapid asset growth in bull markets but can become catastrophic during downturns.

3.2.2 Technical and Regulatory Risk: The Unknowns of Staking

The Ether Machine’s operational model is deeply embedded in regulatory gray zones like staking, restaking, and DeFi. While the SEC in May 2025 stated that some forms of staking are not securities, that statement lacks legal authority and made no mention of restaking or liquid staking. As such, the regulatory risk in the areas The Ether Machine is exploring could go beyond fines—potentially invalidating the entire business model. The ongoing delay in approval of BlackRock’s ETH ETF staking proposal is a strong signal of regulatory caution.

Technical risk is also significant. Slashing due to validator downtime, the added complexities of restaking structures, and smart contract vulnerabilities in DeFi can all result in total asset loss. Restaking, in particular, stacks risk vertically—meaning a failure in one system could cascade across the entire portfolio.

3.2.3 Governance and Centralization Risk: Ethereum's Unique Challenges

Ethereum’s governance model presents its own set of risks. While the Ethereum Foundation holds only a small amount of ETH, critics argue it still wields outsized influence through funding and development. Institutional investors like The Ether Machine are inherently exposed to this “social risk.” Meanwhile, the rise of large staking entities like Lido post-PoS transition has raised concerns about centralization. The Ether Machine’s entry into the ecosystem could worsen these dynamics, drawing criticism from the community and scrutiny from regulators.

Source: CS Bastiat X

As Vitalik Buterin and the Bank for International Settlements (BIS) have pointed out, many DeFi and Layer 2 projects contain backdoor mechanisms like admin keys or centralized sequencers. These tools can override protocols or freeze funds, meaning what appears decentralized may, in practice, rely on centralized governance. When The Ether Machine allocates capital into such ecosystems, it isn’t just investing in code or decentralization—but in the judgment and ethics of a small group of operators. This makes it more vulnerable to regulatory intervention, insider manipulation, or security breaches.

3.2.4 The Ether Machine as a Source of Systemic Risk

The Ether Machine is not merely a crypto-holding company. It uses debt to acquire large volumes of ETH and reinvests this capital into DeFi, staking, restaking, and other yield strategies. This model blends financial leverage with protocol leverage—a structure where asset management and network participation are tightly coupled.

This double-leverage system amplifies gains during bull markets but may significantly expand systemic risk in downturns. For instance, if ETH price crashes or staked assets are slashed, The Ether Machine may be forced to liquidate large amounts of ETH to cover margin or debt obligations. This selling pressure could further depress ETH’s price and destabilize multiple protocols—especially those relying on Actively Validated Services (AVS) with high security dependencies (EigenLayer AVS guide).

In short, The Ether Machine is no longer a passive investor but a structural player capable of influencing Ethereum’s broader ecosystem. If successful, it could become a powerful engine of yield generation. If it fails, however, it could act as a catalyst for systemic contagion across Ethereum’s infrastructure.

Source: imgflip.com

The Ether Machine aims to merge MicroStrategy’s financial engineering with the complex on-chain operations of a DeFi power user. This is more than simply utilizing blockchain—it represents a new kind of public company that places blockchain infrastructure at the very center of its business model.

Could this become a “post-MicroStrategy” model? If successful, it would demonstrate that publicly traded companies can evolve from passive holders of crypto assets to active participants in the decentralized economy, capable of generating real on-chain value. Especially in the case of Ethereum—a productive asset—this would mark a significant shift in how institutional players view and manage crypto: not as speculative exposure, but as operational capital.

However, this ambition comes with inherent complexity and multi-layered risks. Technical, financial, and regulatory uncertainties could constrain success, and ironically, the sophistication of the model itself may become its biggest vulnerability. If The Ether Machine underperforms or faces external setbacks, institutional investors may retreat back toward simpler strategies like ETFs or passive holding.

To assess where The Ether Machine is headed, several key indicators warrant close attention:

SEC Filings & SPAC Merger Details: The Ether Machine is planning a backdoor listing through a SPAC merger with Dynamix Corporation (DYNX). The final S-4 filing submitted to the SEC will be crucial—not only disclosing merger details, but also offering a comprehensive overview of the company’s financial condition, governance structure, competitive outlook, and risk factors. Investors will be able to assess how The Ether Machine positions itself in the market and plans to grow.

Staking Regulatory Developments: Whether the SEC classifies restaking—especially across multiple protocols—as a securities activity will have a direct impact on The Ether Machine’s operating model. If such activity is deemed to involve securities, the company may face registration requirements, increased disclosures, and tighter compliance obligations. Future SEC guidelines or legal precedents could prove to be pivotal, not only for The Ether Machine but for the broader liquid staking and restaking ecosystem.

Initial Yield Performance and Operational Reporting: Early performance data from staking and DeFi operations will serve as a first litmus test of the business model’s revenue-generating capabilities. But raw yield numbers won’t be enough; transparent disclosure of associated risks—such as smart contract vulnerabilities, slashing exposure, and protocol-level risks—will be essential. If The Ether Machine can demonstrate reliable returns and disciplined risk management, it will strengthen institutional confidence and market legitimacy.

Ecosystem Response: The Ethereum community and institutional stakeholders may have mixed reactions to The Ether Machine’s influence. On one hand, its capital deployment and infrastructure building could be seen as a boon for the network. On the other, concerns around validator concentration and centralization could spark community backlash and regulatory scrutiny. Earning community trust will be critical—not just for reputation management, but for the long-term sustainability of the project.

Regardless of The Ether Machine’s ultimate outcome, its emergence signals a major inflection point. At the intersection of traditional finance and decentralized networks, it raises real-world questions:

How should risk be defined? How should regulation evolve? How can governance be reimagined?

Whether The Ether Machine succeeds or fails, it will likely become a key case study in institutional crypto adoption—and one that shapes the next chapter of blockchain-integrated corporate strategy.

Related Articles, News, Tweets etc. :

Dive into 'Narratives' that will be important in the next year