Robinhood lists 200+ U.S. stocks and pre-IPOs as Arbitrum tokens, opening a regulated retail ramp on-chain.

Orbit-based Robinhood Chain will share 10% sequencer fees with Arbitrum DAO, but tokens remain whitelist-locked.

Spot-focused Robinhood and perp-focused Hyperliquid now race toward the same 24/7 all-asset exchange goal.

Legacy “5-day, 6.5-hour” equity hours look obsolete as border-free, always-on trading accelerates.

Robinhood has just thrown a major stone into the convergence pond, giving European users access to U.S stocks, ETFs, and even pre-IPO names such as OpenAI and SpaceX in the form of on-chain tokens that trade commission-free, 24 hours a day, 5 days a week on Arbitrum. A dedicated Robinhood L2, built with Arbitrum Orbit, is slated to follow. What began as a crypto-only mobile app for EU customers is now repositioned as a crypto-powered everything-broker.

Founded in 2013 to “democratize finance for all,” Robinhood weaponised zero-commission trading and an addictive mobile UX to attract a predominantly millennial customer base. The company’s promise of fee-free investing, fractional shares, and a SNS savvy brand translated into more than 25 million funded accounts and 221 billion dollars in assets under custody. By making Wall Street feel as approachable as a game, Robinhood effectively practised a Web3 like, user-first ethos before the term existed.

The results are tangible. Revenue climbed to 2.95 billion dollars in 2024, up 58% YoY, while net income reached 1.41 billion; a rarity among retail brokerages. Markets have rewarded that performance: HOOD has rallied roughly 140% YTD and recently printed all-time highs near 93 dollars on the heels of the tokenisation news.

At its recent “To Catch a Token” event, the firm unveiled its most ambitious experiment yet: tokenised equities. European clients can purchase on-chain representations of Apple, Nvidia, the S&P 500 ETF, or SpaceX around the clock, with dividends and corporate actions mirrored on-chain. Settlement occurs on Arbitrum for now, but Robinhood intends to migrate issuance to its own Orbit-based chain to unlock true 24/7 trading. The move transforms Robinhood Europe into a single application capable of handling crypto, stocks, leverage, and eventually staking, all under one roof.

Robinhood is also deploying classic growth hacks to seed this ecosystem. A 2% crypto deposit bonus (payable only if balances remain for twelve months) quickly hoovered up more than $500m in BTC, ETH, and SOL. While framed as generosity, the mechanic locks liquidity, generates trading and staking fees, and nudges customers toward the upcoming perpetual-futures platform. It is a textbook example of using incentives to create sticky behaviour, and it signals the firm’s willingness to spend aggressively to win crypto market share.

Choosing Arbitrum as the launch rail is an unequivocal victory for both the rollup and the wider modular Ethereum thesis. Robinhood’s bespoke chain will pay sequencer fees to Arbitrum, of which 10% flows automatically to the Arbitrum DAO. If tokenised-equity volumes scale as management hopes, that revenue share could become one of the DAO’s largest recurring income streams, aligning a highly regulated Web2 giant with a decentralised treasury.

The move also restores momentum to Arbitrum after a year in which Optimism’s Superchain, headlined by Coinbase’s Base, threatened to steal mindshare. Landing Robinhood reverses that momentum and validates Arbitrum’s open, permissionless approach to app-specific rollups. Two of America’s largest brokerages now build on Ethereum L2s, reinforcing the network’s claim as the default settlement layer for RWAs.

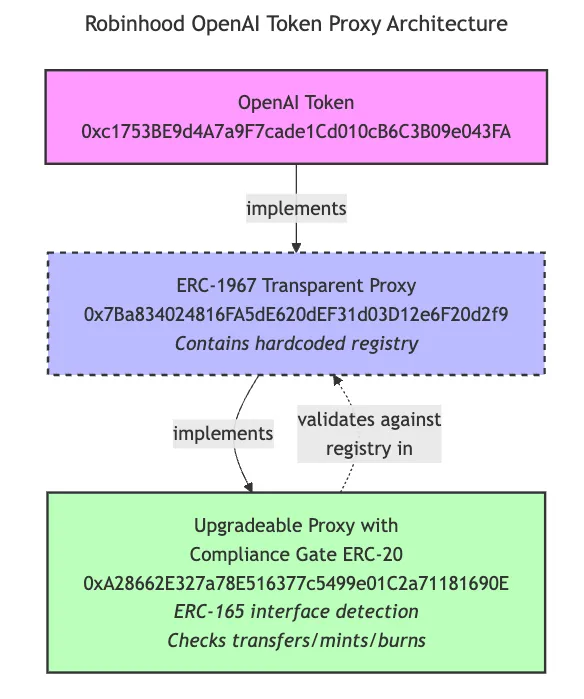

Yet composability is far from guaranteed. As @0xren_cf decompiled Robinhood’s equity-token contracts, he found every transfer gated by a registry of approved (KYC/AML-verified) wallets. If your address is not on that list, the transfer reverts, effectively isolating the tokens from open DeFi.

This contradicts to Bankless co-founder David Hoffman optimistic view that Robinhood’s tokens will slot neatly into Arbitrum’s existing DeFi stack once transfer restrictions loosen. Unless Robinhood relaxes the registry (or launches a parallel, freely transferable wrapper) true on-chain composability remains theoretical.

source: X (@0xen_cf)

Additional structural frictions emerge once you zoom in on the issuance model. Dragonfly GP @HadickM notes that Robinhood’s product, like existing xStocks, should rely on a Jersey-based SPV regulated in Liechtenstein. Minting or redeeming requires KYC with a partner exchange; holders gain only a right to off-chain cash settlement (minus a 25 bps redemption fee), not voting rights.

Because the SPV can acquire shares only during market hours, after-hours or weekend trading forces market-makers to warehouse price risk they can’t fully hedge, driving wider spreads exactly when retail hopes to trade. In short, near-term liquidity and UX may disappoint even as the long-term vision remains sound.

Robinhood’s pivot puts it on a collision course with Hyperliquid, the crypto-native venue that already captures roughly 70% of on-chain perpetual swap volume via a custom high-throughput L1, sub-second finality, and a cult like degen user base. Hyperliquid’s roadmap targets tokenised RWAs too, betting that traders will gravitate to a trust-minimised order book offering everything from Bitcoin to Berkshire.

Here the product scopes diverge: Robinhood leads with spot tokenised equities, whereas Hyperliquid is preparing perpetual futures on stocks. Robinhood just stole a march by bringing 200 equities on-chain overnight, an asset universe Hyperliquid cannot list spot without brokerage plumbing. Conversely, Hyperliquid can list equity perps the moment oracle infrastructure is ready, sidestepping custody and corporate-action headaches that hobble Robinhood.

Hyperliquid still owns distinct advantages: non-custodial, non-KYC access; extreme leverage on meme assets; and extremely low latency. The culture difference is also stark: Robinhood optimises for regulatory alignment, while Hyperliquid caters to users who prize speed and censorship resistance. That asymmetry sets up a classic pincer. Robinhood will push inward from the mainstream, wielding polished UX and fiat rails; Hyperliquid will push outward from crypto’s core, adding fiat on-ramps and RWA indices. Each now targets the other’s weak flank, forcing faster iteration and deeper liquidity across the sector.

In any case, the big winner in this clash may ultimately be the end-user. Whether you’re a crypto degen chasing double digit perp leverage or a stock-market newbie hunting 24/7 Apple exposure, competition will drive sharper pricing, broader asset menus, and UX that fuses DeFi’s openness with TradFi’s polish. The race for the House of Finance is on, and with Coinbase chasing its own deFi stack with Base, three very different origin stories are converging on the same end-goal: a borderless, always-on, all-asset exchange layer.

Robinhood’s tokenised-equity launch ultimately serves as a strategic wedge that

Injects a retail juggernaut into on-chain liquidity; even if its tokens start life in a KYC walled garden;

Confirms Ethereum rollups as the rails of choice for regulated institutions; and

Triggers an arms race: Hyperliquid perfecting on-chain equity perps, Coinbase scaling Base, and Robinhood refining custodial access for millions of normies.

The after-hours gap that closes Wall Street four-fifths of each week looks archaic. A permissionless perp powerhouse, a crypto native CEX turned L2 operator, and a FinTech brokerage, all sprinting toward the same destination, are set to abolish it. Finance, once gated by time zones and clearing cycles, is being rewired for an always-on, borderless future.

Dive into 'Narratives' that will be important in the next year