Category: Infrastructure, L1, Algorithmic Stablecoin

ATH Price and Market Cap: $119.18 (2022. 04. 05), $139.11B (2022. 05. 12)

Current Price and Market Cap: $0.0001037 (2025. 01. 10) [-99.9999%], $571.19M (2025. 01. 10) [-99.6%]

Key Features: A blockchain platform aimed at building a decentralized financial ecosystem and providing a stable stablecoin through its algorithm-based stablecoin UST and its supporting native token, LUNA.

The "Missing Crypto Projects Series" is a series that highlights projects that were once at the center of attention and in the spotlight but, for some reason, have now faded into the shadows and no longer enjoy the same level of popularity as before.

1.1.1 Originally, Terra Was a Stablecoin for Payments

Source: CHAI

One of the facts that many people have forgotten or don't know is that Terra's original vision was to create an "algorithm-based stablecoin and blockchain for payments." As such, Terra created algorithm-based stablecoins pegged to the values of various national currencies and worked closely with the simple payment service CHAI to allow users to charge KRT (Terra Won) and directly use it in the real economy (though there were limits to how much KRT could be used to charge Korean Won, it was enough not to cause inconvenience in daily payments). However, this utility alone was not enough to bring Terra’s use case to a global level. The demand for stablecoins, even as of the time I am writing this, primarily comes from being used as quote currencies on centralized or decentralized exchanges. While payment was a promising sector, it was still small, and in 2021, when Terra was gaining attention in the market, it was even smaller. This is why they couldn't stick solely to payments. (Of course, this is a hindsight analysis, but if Terra had focused only on payments without considering aggressive growth, perhaps the de-pegging incident might not have occurred.)

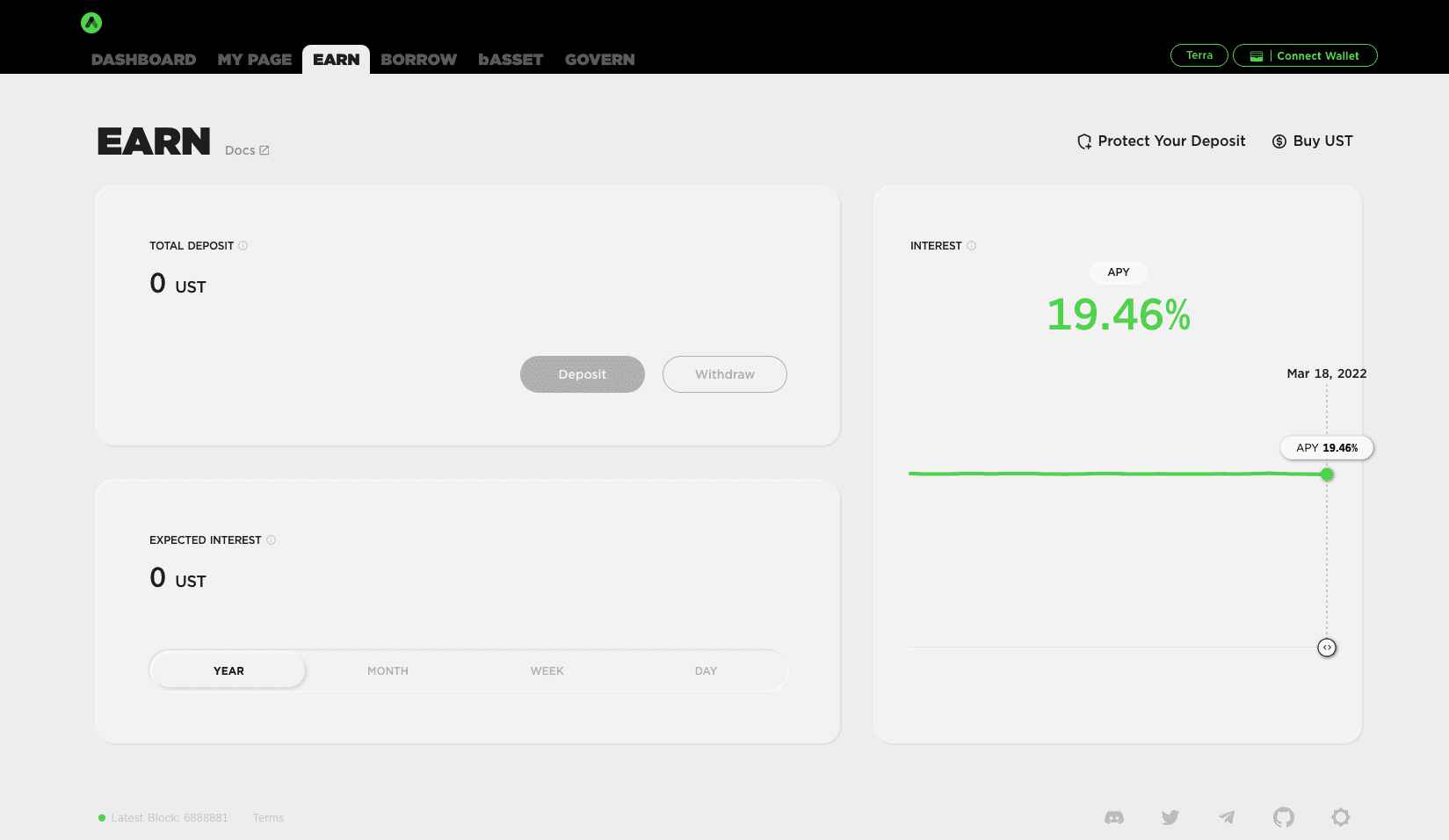

1.1.2 Deposit Terra and get 20%! The Black Hole of the Terra Crisis: Anchor Protocol

Source: Anchor Protocol

As will be discussed further, Terra and Luna's structure meant that demand for Terra (the stablecoin) had to increase for Luna's value to rise, so their goal was to drastically increase demand for Terra. So, how could they increase demand for Terra? Terraform Labs (the developer of the Terra blockchain) found the answer in "stable and high interest on safe assets." The problem with stablecoins was that while they have very little volatility, there was no way to earn high profits from them. So, Terraform Labs introduced a product that claimed to offer a consistent 20% interest rate, and this was the Anchor Protocol.

The way the Anchor Protocol works is simple. It is a step further than the Liquid Staking Protocol that exists on all chains. At the time, staking Luna yielded an annual staking reward of 10%, and using this Luna as collateral, with a collateralization ratio (LTV) of 50%, you could borrow stablecoins. The person who lent the stablecoins would receive the entire staking reward as interest, meaning that the stablecoin provider would earn an annual 20% interest on their deposit. To help explain with an example: if person A staked $100 worth of Luna and used it as collateral to borrow $50 worth of stablecoins, the person who deposited the $50 in stablecoins would receive the 10% staking interest from the $100 worth of Luna, which amounts to a 20% interest on the $50.

The 20% interest was enough to generate significant demand for Terra. Especially for crypto users who were familiar with DeFi but tired of unsustainable liquidity farming, the "seemingly sustainable 20%" interest rate from Terra seemed stable. Even people unfamiliar with DeFi likely saw the 20% as a "risk-minimized" way to earn returns. Perhaps that is why, after the introduction of Anchor Protocol, Terra gained significant momentum and became the third-largest stablecoin project after USDT and USDC.

1.1.3 The Fundamental Issues of Anchor Protocol and Terra's De-Pegging

However, the problem ultimately arose from the 20% interest. While the Anchor Protocol seemed theoretically perfect, there were several chronic issues: To maintain this structure, 1) Luna’s staking interest had to always exceed 10%, 2) the value of the staked Luna collateral had to remain stable or increase, and 3) the total amount of staked Luna collateral had to maintain a consistent ratio with the amount of stablecoins deposited. Only if all of these conditions were met could the 20% interest rate be maintained. If any of these conditions were violated, they would have to adjust the interest rate or set limits on the deposit amount to maintain an appropriate ratio between collateral assets and stablecoin deposits.

But Terraform Labs took no action to protect Anchor, and instead, they focused on artificially "injecting" money into Anchor to maintain the 20% interest rate. Naturally, this vicious cycle was not good for Terra, and eventually, large amounts of Terra were sold into the market from Anchor, leading to de-pegging (the state where a stablecoin loses its original value).

1.1.4 However, Anchor Was Not Operated Opaquely

Source: Anchor Protocol

One of the reasons why many media and politicians labeled Terra and Anchor as "Ponzi schemes" was because they continued to promote and promise 20% interest even though they couldn’t sustain it, misleading users. However, strictly speaking, Terra and Anchor never hid the "source" of the 20% interest. The image above is an example: at the time, when you entered Anchor, there was a section on the dashboard called "Yield Reserve," which showed how much money was in the fund from which interest was paid to users. This allowed users to roughly estimate whether the interest could continue and, if so, for how long. So, just because someone didn’t notice this does not mean they hid the source of the interest. I wanted to make this point clear.

In fact, Terra’s de-pegging was more due to Anchor's transparency in showing the source of interest. Those who deposited Terra in Anchor could see on the dashboard that the interest rate was not sustainable, so they began withdrawing their Terra deposits and selling them on the market. This became one of the catalysts for the de-pegging event, and it's ironic when you consider this.

“As you know, madness is like gravity... all it takes is a little push.”

— Joker

No matter which stablecoin it is, the most significant factor influencing depegging is the psychological state of the people holding the stablecoin. Considering that even asset-backed stablecoins like USDT and USDC, rather than algorithmic stablecoins, have experienced depegging multiple times, it's evident that depegging is not solely an issue tied to algorithmic stablecoins. The root cause of stablecoin depegging lies in the fear that “I may not be able to exchange my stablecoin for an asset of equivalent value.”

This fear, however, tends to affect algorithmic stablecoins more profoundly than asset-backed stablecoins. Anonymous whales who deliberately attacked Terra exploited this psychological vulnerability. To understand how these whales leveraged such fears, let’s provide some context: at the time, Terraform Labs had established the Luna Foundation Guard (LFG) to maintain Terra's peg by purchasing Terra when its price dropped. LFG acquired Bitcoin to defend Terra’s peg and also provided liquidity on Curve Finance via a stable pool containing USDT, USDC, and UST (known as the 3pool) to enable 1:1 swaps.

The issue arose when Terra moved liquidity from the 3pool to a new pool (4pool) that included FRAX for better stability. During the transition, liquidity in the 3pool dried up. Seizing this opportunity, whales sold a large amount of UST, breaking the peg.

What’s more critical is what followed. These whales simultaneously spread news about UST losing its peg and rumors about the inherent difficulty of algorithmic stablecoins in recovering their peg. As mentioned earlier, asset-backed stablecoins like USDT or USDC have accountable entities (Tether or Circle, respectively) that ensure redemption for physical assets. Terra, on the other hand, lacked such guarantees, which triggered fear among UST holders. To make matters worse, the Anchor protocol, which was offering unsustainably high yields, was running out of funds (Do Kwon had been injecting billions to maintain the 20% yield, but Anchor's reserves were frequently depleted). This combination of fear surrounding algorithmic stablecoins and doubts about Anchor's sustainability sent Terra spiraling out of control.

In hindsight, the whale who initiated UST’s depegging may have toppled it with minimal capital. Perhaps all they needed was to nudge Terra's price slightly downward. What followed was the collective fear of those who liked Terra but harbored doubts deep down about its potential to depeg, ultimately causing its collapse. Was Terra a Ponzi scheme? It had Ponzi-like aspects, sure. But was it outright fraud? That’s debatable. Do Kwon likely wanted to scale Terra further, surpass Ethereum’s market cap, and validate his ego and ambition. There was no reason for him to deliberately destroy Terra. Yet, Terra became one of the most significant failures in blockchain history, a failure stemming from Do Kwon's aggressive strategies and arrogance about himself and his project. While some compare Terra to FTX, I believe they are fundamentally different. The former represents a failure in product design, hubris, and overconfidence; the latter was intentional fraud.

Nevertheless, Terra left behind valuable lessons and a record of how we have evolved and grown from this experience. So, what lessons can we take away from the Terra-Luna incident?

Algorithmic stablecoins were an innovative approach that aimed to maintain value using internally designed economic algorithms and the "invisible hand" of the market, without relying on centralized collateral. However, these models inherently carried significant risks, which the Terra project starkly highlighted, raising global awareness about the vulnerabilities of algorithmic stablecoins.

Terra's UST attempted to maintain its value through economic algorithms and its interaction with LUNA. The crypto market bull run starting in 2021 facilitated these interactions positively, making the system appear stable. As LUNA's price surged, the profits generated through UST issuance also increased, driving the expansion of the Terra ecosystem and the growth of UST's circulation. However, this mechanism was inherently reliant on new capital inflows, embedding an extreme risk of destabilization into Terra's framework—though this risk was not immediately apparent.

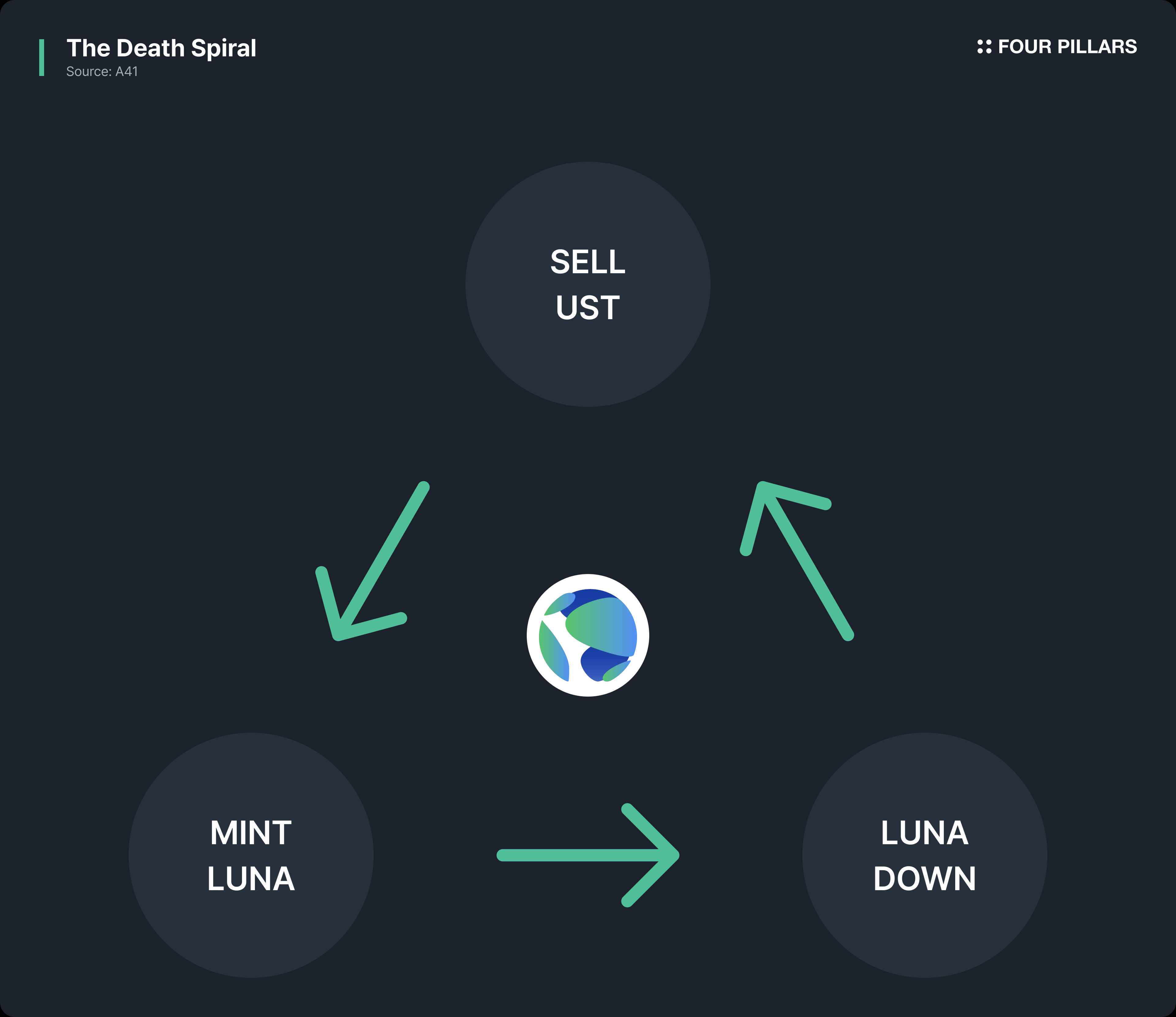

Eventually, as the price linkage between UST and the dollar broke and the economic algorithms tied to LUNA collapsed, the structural vulnerabilities of Terra were exposed. It became evident that the system could easily crumble under external shocks or a loss of investor confidence. This self-reinforcing collapse, known as the "death spiral," brought Terra—once the sixth-largest cryptocurrency by market cap—crashing down almost instantaneously. This incident underscored the need for more stable and robust alternatives in the economic design of algorithmic stablecoins.

To stabilize the value of UST, Terra relied on the Luna Foundation Guard (LFG) to purchase Bitcoin, using it as a single reserve pool. The idea was that if the value of 1 UST dropped below $1, LFG would sell its Bitcoin reserves to restore the peg. While this approach could be effective for short-term market stabilization, it carried significant risks. If UST or LUNA lost market confidence and Bitcoin’s value simultaneously declined, the situation could spiral out of control, making recovery nearly impossible.

This very scenario unfolded when UST lost its peg to the dollar, triggering a bank run that overwhelmed LFG’s ability to respond to the sell-off. The reliance on a single reserve asset—Bitcoin—became a critical weakness as Bitcoin’s price also began to drop, further undermining the intended safety mechanism.

In the end, Terra’s strategic reliance on a single collateral system failed. What if Terra had diversified its reserves beyond Bitcoin to include assets such as Ethereum, fiat currencies, gold, or bonds? While the outcome cannot be guaranteed, a diversified collateral system might have mitigated the risks associated with the volatility of a single asset and provided a more robust defense against sudden market shocks. By blending various stable assets, Terra could have been better positioned to handle such crises.

Ultimately, the Terra incident highlighted the importance of not only having robust risk management mechanisms to respond to stablecoin depegging but also implementing diversified collateral systems to ensure those mechanisms can be effectively executed.

From the early stages of its launch, Terra recognized the critical role of community and invested heavily in its growth. Terra attracted holders by offering high APY DeFi services and hosting various airdrop events that provided lucrative earning opportunities. Additionally, the community played a central role in regularly burning LUNA tokens to reduce its supply, helping to maintain or increase its value.

These events and announcements were actively promoted through platforms like Twitter, Telegram, and Discord, earning enthusiastic support from holders and paving the way for broader community engagement. Do Kwon, the founder of Terra, positioned himself as a leading voice for LUNA holders, engaging in heated debates and exerting significant influence on social media.

This led to the creation of a loyal and fervent Terra support base, which contributed significantly to the project’s growth and the initial establishment of trust. These passionate supporters boosted Terra and LUNA's exposure through their active online presence, driving up LUNA’s value and reinforcing the stability of UST. This strong backing further solidified UST’s price peg to the dollar, a core element of the Terra ecosystem.

Source: Kyle Samani X

However, too much of anything can become detrimental. Like the pitfalls of political extremism, Terra’s overly insular and dogmatic community, driven by blind optimism, led to the suppression of issues and a decline in the project’s ability to respond effectively to problems.

Do Kwon’s leadership during this period exacerbated these tendencies. His provocative and aggressive responses to critics of Terra, though celebrated by the core community, alienated neutral observers. This made it challenging for Terra to foster broader public support and connect with individuals outside its community.

As a result, the excessive insularity of the community led to missed opportunities to identify and address critical issues early on. Ultimately, it also contributed to Terra’s reputation deteriorating among the general public, culminating in its collapse. This highlights the importance of balancing community passion with openness to criticism and broader engagement to ensure sustainable growth and resilience.

Building on the lessons from Terra’s failure, a new wave of flexible collateral-based stablecoins is emerging, aiming to address the weaknesses of both algorithmic and collateralized stablecoins while combining their strengths.

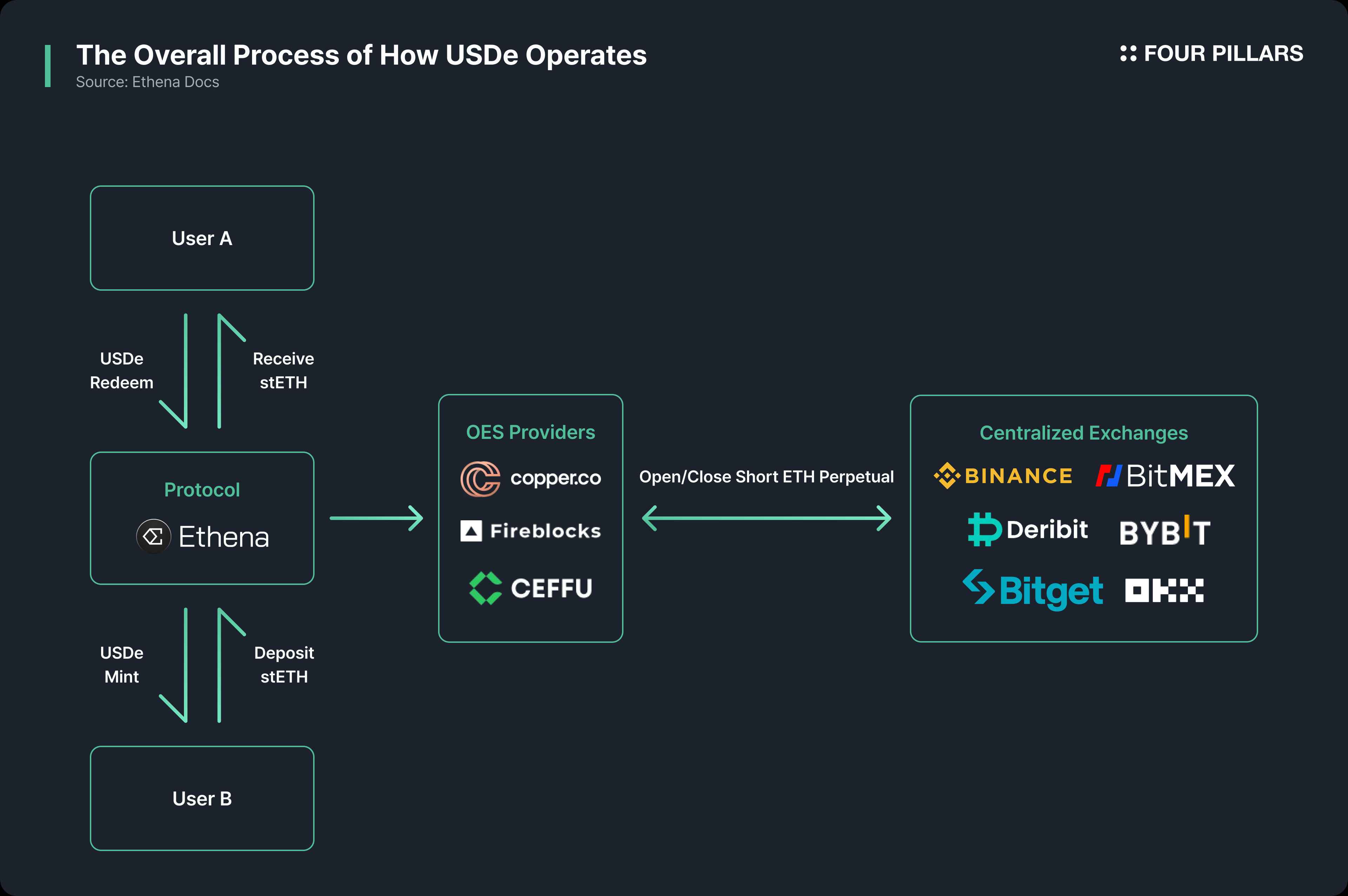

For example, Ethena is a collateralized stablecoin protocol that uses a delta-neutral hedging strategy to maintain the stability of its stablecoin, USDe. This approach involves holding short positions equivalent to the value of the assets backing USDe, effectively insulating USDe’s baseline value from the volatility of the underlying collateral. Through this strategy, Ethena enables a stablecoin mechanism that, unlike Terra, remains stable without requiring over-collateralization or reliance on assets closely tied to traditional financial systems.

Similarly, USDY, developed by Ondo Finance, is a stablecoin backed by U.S. short-term Treasury bonds and bank demand deposits. USDY has several notable features, such as minimizing individual losses even if the issuing company faces insolvency, generating yield automatically from its collateral, and providing legal protections for users.

As these examples demonstrate, modern stablecoins are increasingly adopting flexible collateral strategies to mitigate the risks and shortcomings associated with previous stablecoin models. They aim to provide users with greater benefits, convenience, and stability, while reducing the vulnerabilities that plagued earlier designs. This shift reflects an evolution in stablecoin mechanics, prioritizing resilience and user trust.

Stablecoin projects have recognized that relying on a single type of collateral introduces excessive risk and limits their ability to respond effectively in emergencies. To address this, many projects have moved toward diversifying their collateral systems.

USDC, a collateral-backed stablecoin pegged 1:1 to the U.S. dollar, is issued and managed by Circle and Coinbase. USDC maintains its stability by backing its value with U.S. bank deposits and short-term Treasury bonds. Additionally, it undergoes monthly accounting audits to ensure transparency. These processes, combined with strict adherence to U.S. financial regulations, have established USDC as a highly trusted and widely used stablecoin.

MakerDAO initially relied solely on Ethereum (ETH) as collateral but has since evolved into a Multi-Collateral DAI system. This system allows MakerDAO to issue its stablecoin, DAI, using a diverse range of assets as collateral, selected through governance votes. Currently, MakerDAO accepts assets such as Ethereum (ETH), Wrapped Bitcoin (WBTC), USDC, Basic Attention Token (BAT), and Chainlink (LINK) as collateral. By diversifying its collateral base, MakerDAO mitigates risks associated with price and liquidity fluctuations of individual assets, thereby increasing the stability of DAI.

These examples highlight the growing trend of collateral diversification as a key mechanism for enhancing the resilience and stability of stablecoins. This approach reduces reliance on any single asset, distributes risk, and fortifies the overall robustness of stablecoin ecosystems.

The importance of community—acting as the closest and most impactful extension of blockchain projects—has remained a focal point even after the Terra incident. Projects like Berachain, Monad, Hyperliquid, and Pudgy Penguins have taken lessons from Terra, striving to foster passionate yet open communities rather than insular and overly defensive ones.

Source: Smokey The Bera X

Berachain, for instance, began its community-building efforts with the launch of the Bong Bears NFT collection. The founder, SmokeyTheBera, introduced Bong Bears in August 2021 as the foundation for community development. Using a rebasing model, they conducted additional NFT airdrops for existing holders, fostering loyalty and encouraging organic community growth. Moreover, memes like "Ooga Booga," which emerged naturally within the community, helped strengthen internal bonds while also appealing to a broader audience, expanding Berachain’s reach.

Source: Pudgy Penguins X

Another notable example is Pudgy Penguins, which built its community around adorable penguin characters, leveraging them as its core intellectual property (IP). This strategy not only helped the NFT project gain significant traction but also provided a solid foundation for community-building. Pudgy Penguins expanded beyond NFTs by introducing physical merchandise, such as t-shirts, hats, and toys, to meet community demands. Furthermore, they issued the $PENGU token and conducted airdrops, maximizing community loyalty while encouraging user-generated content to enhance the project’s broader appeal.

Pudgy Penguins also demonstrated the positive impact of a strong community when it ousted its original founder, who was accused of mismanaging funds and attempting to sell the project. With the support of the #savethepenguins movement, the community managed to steer the project back on course, exemplifying how engaged supporters can safeguard and revitalize a project.

Both Berachain and Pudgy Penguins show that fostering an open and enthusiastic community, while avoiding insularity and promoting transparency, can lead to sustained growth, resilience, and greater public engagement.

Source: The Block

One thing is certain: during its heyday, Terra’s ecosystem boasted some of the brightest talents, more so than almost any other ecosystem. This abundance of talent allowed Terra to grow explosively in a short time. As mentioned earlier, the overwhelming loyalty toward Terra and Do Kwon served as a powerful incentive for talented builders to create excellent products within the ecosystem. However, Terra eventually collapsed, dispersing its talented builders into the broader market. For instance, Zon Mangalji, who was an intern at Terra, is now building a blockchain called Initia. Additionally, the SVM-based rollup project Eclipse, which is preparing to launch its mainnet soon, has drawn significant attention as it was created by former Terra developers. According to Electric Capital's developer report, five developers from Terra joined the Solana ecosystem, while eleven moved to Osmosis.

Undoubtedly, there are many more former Terra developers, unknown to us, who are now building exciting products in various ecosystems. The experiences these individuals gained at Terra likely became invaluable lessons and assets as they embarked on new journeys.

In this article, we’ve examined the causes of Terra’s failure, the lessons learned, and the resulting outcomes. One regret I have is that people tend to focus excessively on sensational keywords, often missing the essence of the situation. If the collapse of Terra was indeed a premeditated fraud, it deserves criticism and condemnation. However, the Terra story is far more complex than a simple black-and-white narrative. While it is true that Terra failed—and failures inevitably cause economic and psychological harm to many—I, too, am one of the victims. That said, not all failed projects cause harm intentionally, and when failures occur, we should focus less on sensationalism and more on understanding the causes of failure and sharing the lessons learned.

If we are not tolerant of failure and rush to oversimplify or stigmatize it, who in Korea—or the global crypto industry—would dare to take on new challenges? Our industry must develop the ability to discern what constitutes a failure and what constitutes fraud. Moreover, we should foster an environment where open debates on such topics are encouraged, allowing the industry to mature, learn more, and evolve in a constructive direction.

Related Articles, News, Tweets etc. :

Dive into 'Narratives' that will be important in the next year