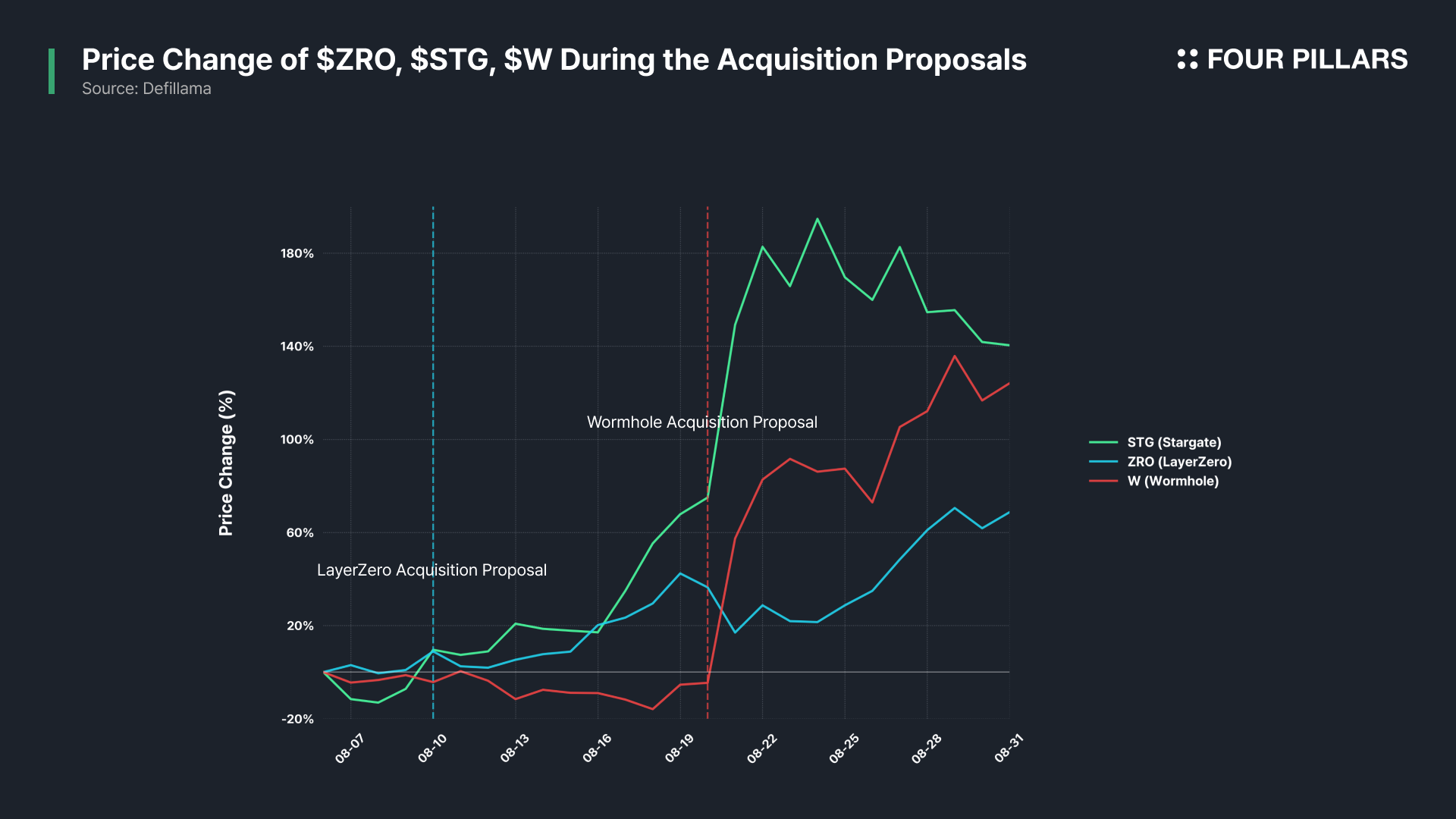

On August 10, 2025, the LayerZero Foundation announced an acquisition proposal worth approximately $110M(as the price went up, the value reached 160M), offering to exchange all STG for 0.08634 ZRO per token. However, veSTG holders, whose tokens are subject to long-term lockups, voiced dissatisfaction since they could not directly benefit. To address this, LayerZero proposed an adjustment: 50% of Stargate revenues generated over the next six months would be distributed to veSTG holders.

On August 21, 2025, Wormhole countered LayerZero’s proposal, claiming Stargate was undervalued and offering a $120M cash acquisition in USDC. Yet, Wormhole’s long-term strategic and technical synergies with Stargate remained unclear.

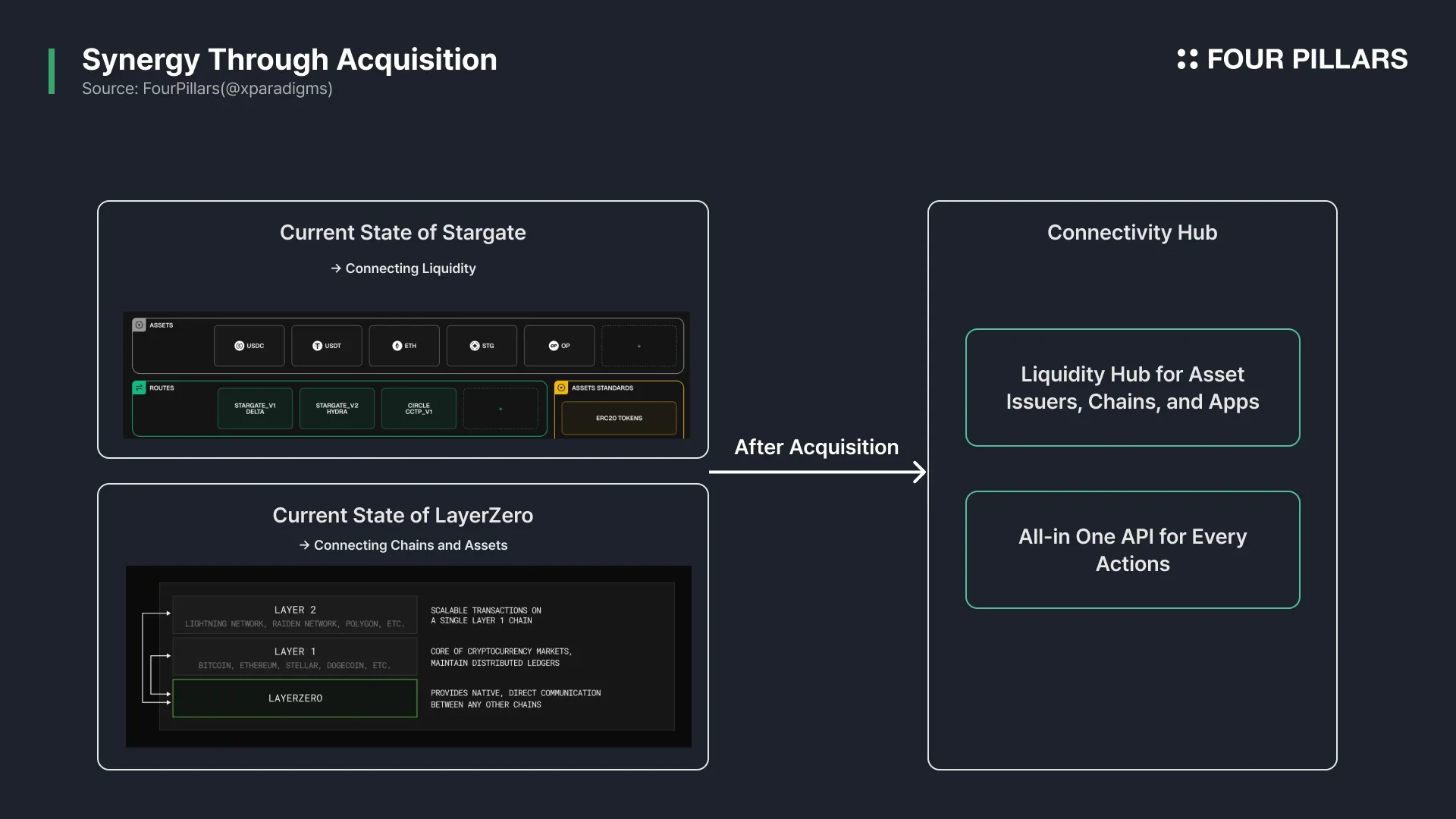

For LayerZero, acquiring Stargate is a natural expansion strategy aimed at expanding vertically from a cross-chain infrastructure provider into a platform that unifies all liquidity, value and services.

Until now, LayerZero has played the role of an invisible backbone, a messaging layer connecting blockchains. With Stargate, however, LayerZero signals its ambition to move beyond merely being the “roads” that connect chains. By acquiring the “car” that drives on those roads which directs user-facing liquidity and applications, LayerZero seeks to elevate itself to the service layer. This positions the company to become a true hub of financial infrastructure, and ultimately to connect all value and its transfer.

Source: Message Passing Protocols

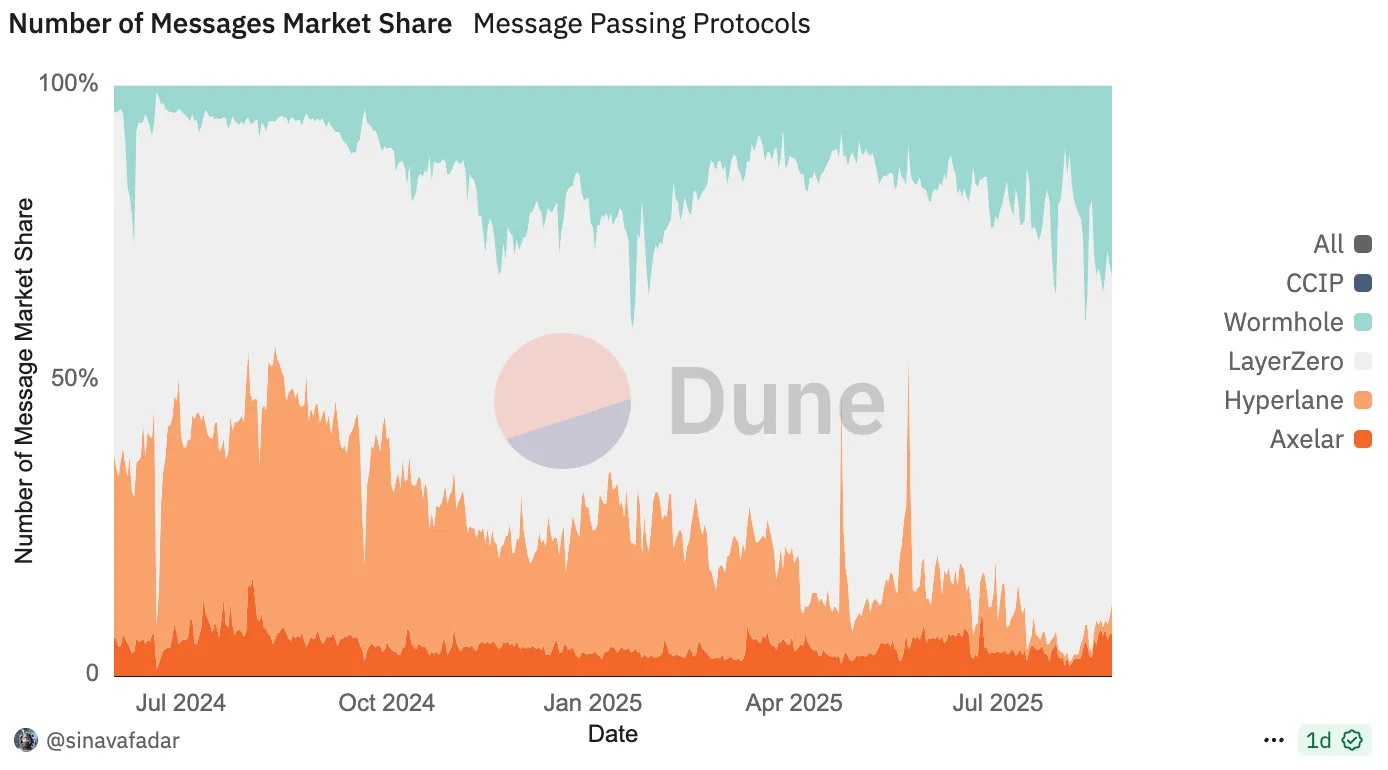

LayerZero, which holds a dominant position, with market share around 80% in the interoperability market, officially announced its plan to acquire Stargate. On August 10, 2025, the LayerZero Foundation announced its proposal: exchange all STG tokens for ZRO, dissolve the Stargate DAO, and redirect future revenues toward ZRO buybacks.

While LayerZero and Stargate are legally and operationally separate entities, they have collaborated closely since inception. Stargate was the first application to use LayerZero’s messaging infrastructure and remains its most active adopter. This acquisition proposal can be interpreted as a strategic move to internalize Stargate and maximize the synergies between the two projects.

LayerZero CEO Bryan Pellegrino showed this vision in his tweet “Bring the Bridge Home”, highlighting combining Stargate’s liquidity and user base with LayerZero’s messaging infrastructure could establish a unified cross-chain system, and also going beyond cross-chain to cross-system in web2. The acquisition vote was conducted through the Stargate DAO between August 17–24, 2025, and was approved.

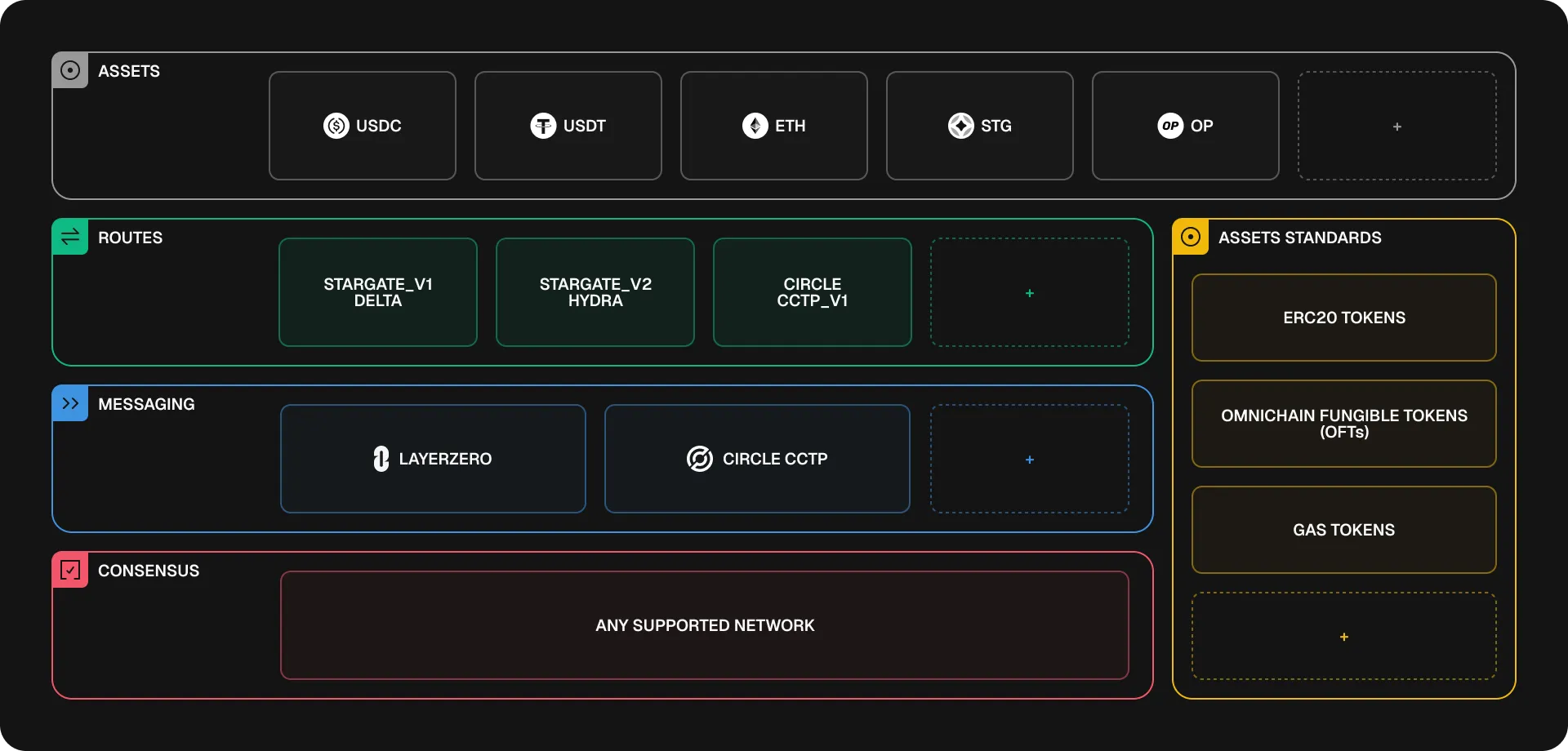

*To clear up common misconceptions: Stargate and LayerZero are separate protocols. While Stargate leverages LayerZero’s endpoints and messaging infrastructure, its liquidity pools and assets are managed independently by the Stargate DAO. LayerZero endpoints are designed to be immutable, and message verification is handled by multiple DVNs (Decentralized Verification Networks) - including LayerZero Labs DVN, Stargate DVN, Nethermind DVN, PayPal DVN, Deutsche Telekom DVN, and Axelar DVN, etc depending on token type and route. Additionally, USDC transfers rely on Circle’s CCTP, not LayerZero. This architecture prevents reliance on a single entity by distributing verification across multiple infrastructures.

Source: Architecture | Stargate Documentation

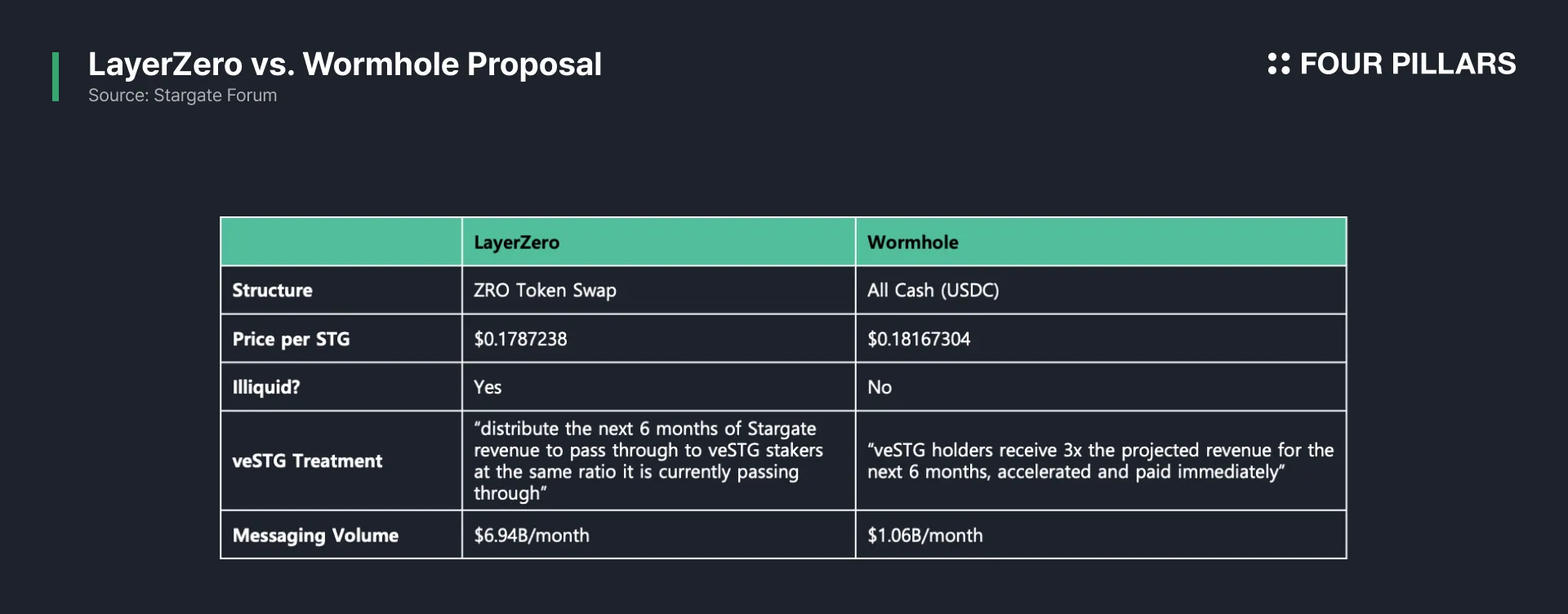

LayerZero proposed exchanging all circulating STG at a rate of 0.08634 ZRO per STG, reflecting roughly a 16% premium relative to Stargate’s treasury assets. At the time, STG was trading at less than 10% of ZRO’s fully diluted valuation (FDV), with about 24% of total STG locked in veSTG positions.

The market reacted positively: STG’s price soared over 20%, pushing the deal’s implied value to about $127M, while ZRO itself spiked between 3.96% and 26%. This reflected investor optimism that simplifying the multi-token structure and strengthening synergies between the two projects would drive long-term value.

Still, veSTG holders raised objections. Because their tokens are locked for extended periods, they could not realize immediate gains. To offset this, LayerZero pledged that 50% of Stargate’s revenues generated over the next six months would be distributed to veSTG holders (based on a snapshot at the time of announcement). The other half would go toward open-market ZRO buybacks. After six months, 100% of Stargate’s revenues will be used for ZRO buybacks, thereby simultaneously reducing supply and supporting price stability.

Currently, Stargate generates approximately $2M annually in protocol fees. Under the proposed plan, half of this revenue will initially go to veSTG holders for six months, while the remainder is directed to ZRO buybacks. Afterward, the entire revenue stream will reinforce ZRO demand, providing supply reduction.

Source: Stargate Forum

On August 21, 2025, the Wormhole Foundation announced a competing bid against LayerZero’s Stargate acquisition proposal. Wormhole criticized LayerZero’s $110M offer as undervaluing Stargate, pointing to Stargate’s $92M treasury, $4B bridge volume in July, and $354M TVL as evidence of stronger intrinsic value. Wormhole declared it was preparing an all-cash bid of at least $120M in USDC, emphasizing that this would provide immediate liquidity and certainty to STG holders, while avoiding the slippage risk of a ZRO token swap.

In the cross-chain messaging market, LayerZero dominates with 80% market share while Wormhole holds just 5%. Volume figures from July show Wormhole processed $905M compared to Stargate's $4B. While Wormhole's offer appeared financially advantageous in the short term, its long-term strategic vision and potential synergies with Stargate remained unclear.

Ultimately, the issue goes beyond raw numbers. It is about strategic synergies and long-term growth potential. So which would deliver stronger synergies?

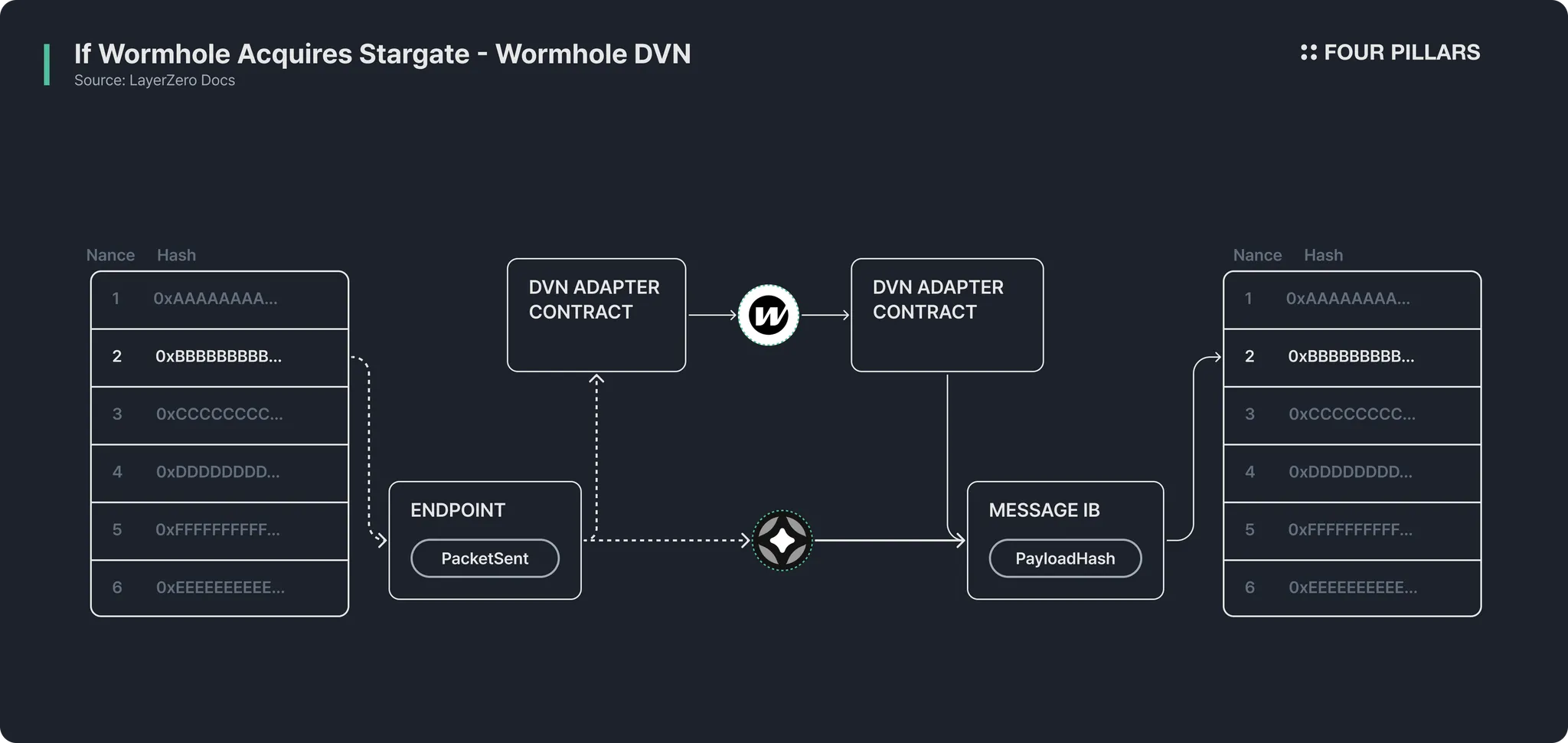

Wormhole's proposal was straightforward: acquire Stargate for approximately $120M in USDC cash. Several potential synergies exist in this deal. For instance, Stargate's Hydra program, which supports new chains, primarily relies on Stargate DVN and Nethermind DVN for messaging. Since Wormhole also provides messaging services, it could integrate as a DVN through an adapter to either supplement or replace the existing DVNs. This integration would enable Wormhole to capture a portion of Stargate's fee revenue while potentially securing a significant share of the cross-chain swap market when combined with Stargate.

However, questions remain over whether these potential synergies truly justify Wormhole’s $120M cash outlay. Wormhole currently has a market capitalization of about $381M, and the near-term and long-term benefits of acquiring Stargate is limited. Stargate’s infrastructure is built upon LayerZero messaging, so migrating it to Wormhole’s messaging layer would require significant development resources with very limited payoff.

Moreover, OFT transfers (e.g., USDT0, USDe) rely on LayerZero’s infrastructure, not Stargate, suggesting that even if Wormhole acquires Stargate, OFT traffic may bypass it entirely.

Wormhole’s acquisition attempt carries symbolic positioning value, but the cost-benefit tradeoff is not clear at all.

Source: Architecture | Stargate Documentation

Stargate has established itself as a token bridge that provides both infrastructure and the most efficient logic for cross-chain token transfers. Structurally, however, it is highly dependent on LayerZero. While Stargate can also facilitate transfers of USDC to other chains through mechanisms like Circle’s CCTP, at its core Stargate is built on LayerZero’s infrastructure. This dependency imposes limits on Stargate’s ability to expand independently.

Meanwhile, LayerZero’s Omnichain Fungible Token (OFT) has gained significant traction through partnerships with major players such as Tether (USDT), PayPal’s PYUSD, and Wyoming’s WYST. Yet, these tokens’ cross-chain transfers do not necessarily rely on Stargate. Issuers can build their own frontends and interfaces to provide transfer functionality directly. If users bypass Stargate, the protocol earns no fee revenue.

In other words, Stargate is tied to LayerZero’s broader success but faces structural constraints on scaling its own revenue.

The most successful scenario for Stargate would be to establish itself as the default hub for cross-chain liquidity exchange, but also potentially for all value transfer within the whole financial infra. If users and applications naturally route through Stargate, the protocol could expand into revenue models beyond simple transfer fees. Here, Stargate has the dependence with LayerZero in terms of OFTs. This could be a big opportunity for Stargate, but they can’t capture the whole value capture from issuance.

On the other hand, LayerZero remains fundamentally an infrastructure-level solution. Its messaging layer is available for any application to freely use, and individual projects can run their own DVNs (Decentralized Verification Networks) or adopt custom security measures. In this sense, LayerZero provides a decentralized messaging layer, and the business logic and services can be customized by the applications themselves. LayerZero has become the Layer“Zero” connecting all L1s and L2s.

This is where the synergy between Stargate and LayerZero becomes clear. Stargate is an application that can grow directly at the user level through liquidity, while LayerZero grows at the infrastructure level through connectivity. As Stargate and LayerZero combined, accounts for most of the market share of the cross-chain value transfer, there could be a big synergy.

By deciding to fully acquire Stargate, LayerZero signals a bold move to extend beyond technical collaboration into the service layer, breaking its own limitations as a pure infrastructure provider. In contrast, Wormhole’s proposal lacks the same clarity in terms of both technological and strategic synergy with Stargate.

Up until now, LayerZero has served as the “invisible backbone” of cross-chain messaging. LayerZero enables to connect not just EVM L1, L2 but also to non-EVM chains, and also private blockchains. It now conencts over 140 blockchains, powers 550 apps including Stargate, EtherFi, GMX, etc, and powers stablecoin issues like Tether, Paypal, Ethena, Ondo, Wyoming Stablecoin, etc

But with the Stargate acquisition, it reveals a new ambition: not just to be the “roads” connecting blockchains, but to acquire the “car” that drives on those roads, that would directly engage with users and generate revenue at the service layer. This move enables LayerZero to pursue vertical expansion in addition to horizontal connectivity, laying the foundation to become the true hub of financial infrastructure.

The first and most significant opportunity Stargate brings to LayerZero is direct access to enterprise clients and token issuers. Today, some OFT projects have already built their own frontends for token transfers, independent of Stargate’s API. But if LayerZero enhances the Stargate API and establishes it as the standard for OFT transfers, issuers will no longer need to build separate infrastructure.

Instead, they can immediately tap into multi-chain liquidity for asset exchanges across ecosystems. OFT API allows tokens to exist and be transferred on any blockchain as simply as if it was moving on a single chain. This would reposition LayerZero from a passive infrastructure provider into an active value-transfer partner, enabling enterprises to expand across chains and potentially to offchain.

The next stage naturally involves connecting the DeFi ecosystem like Lego blocks. With Stargate handling liquidity and LayerZero handling connectivity, users could hold assets on one chain while easily accessing lending, swaps, deposits, and other services on another. If integrated with payment rails such as card services, users could even conduct everyday spending based on assets deposited across chains.

This could mark a fundamental shift in the user experience but also developer experience in the multi-chain future.

LayerZero’s acquisition of Stargate is therefore more than a consolidation. It is a launchpad for LayerZero to evolve from a cross-chain infrastructure provider into a platform spanning all liquidity and services. By doing so, LayerZero positions itself for both horizontal integration and vertical expansion, paving the way to become the core hub of global financial infrastructure.

That’s why we need to pay attention to the next move by LayerZero.

Dive into 'Narratives' that will be important in the next year