By 2030, people around the world no longer open their banking apps. Instead, they send money, invest, and earn yield—all from the Telegram app they use every day. With a single tap, they can deposit crypto and access returns from bonds, lending, DeFi, and more. No financial expertise or intermediaries are needed. It’s a new era of global wealth management that’s transparent and trustless. At the center of this shift is Affluent.

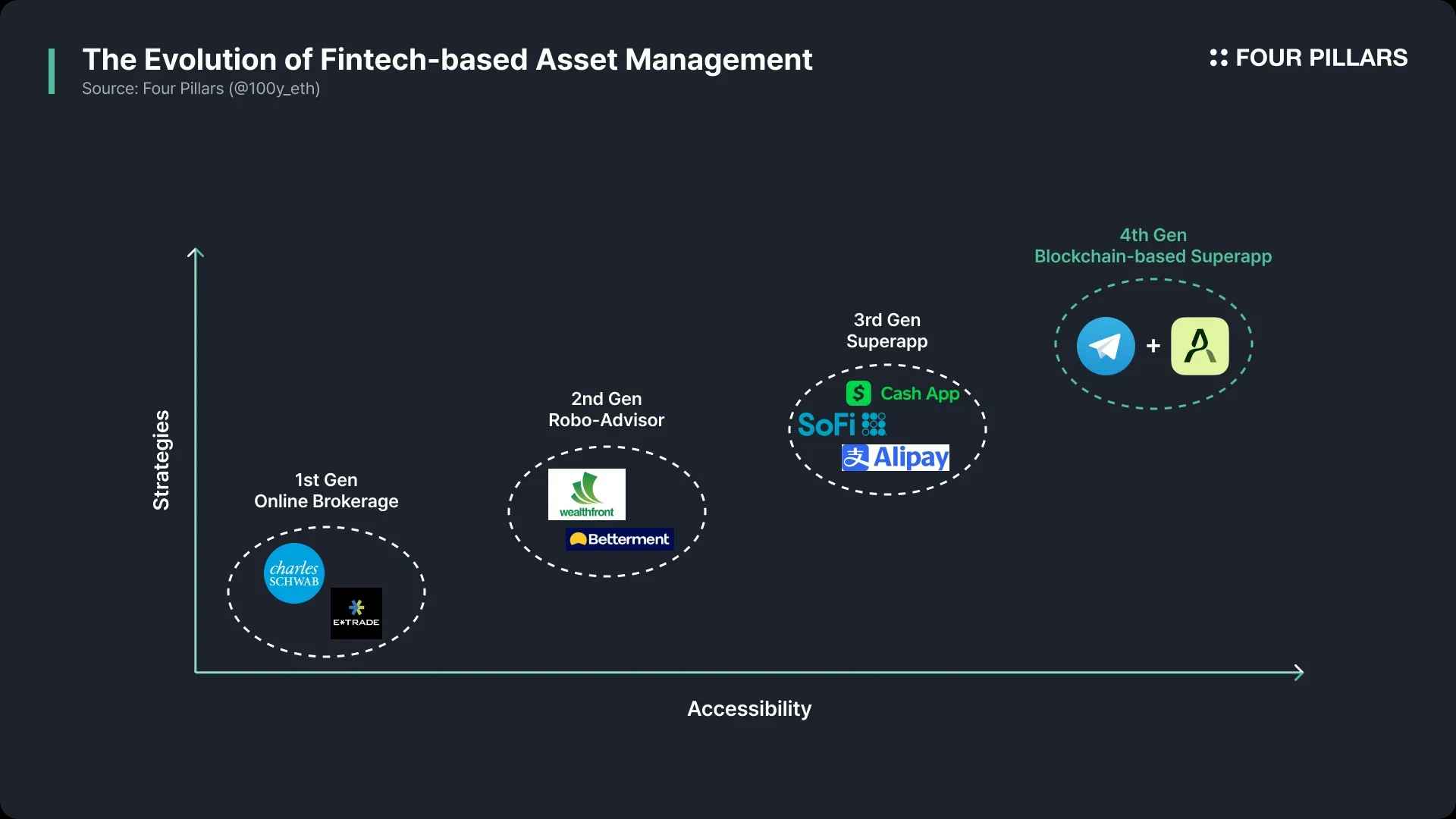

Fintech has evolved through three distinct phases: the first wave brought online brokerages and digital payments, the second introduced robo-advisors and automated wealth management, and the third phase is defined by all-in-one super apps. But most of this innovation has been limited to the frontend—while the backend of the financial system remains outdated.

Blockchain technology has the potential to replace this legacy backend. The rapid growth of the stablecoin industry and Telegram’s expanding Web3 initiatives suggest that Telegram could emerge as the next-generation fintech super app built on blockchain.

Affluent is an asset management platform built on the TON network. Any Telegram user can deposit assets through a native Web3 wallet and earn yield from lending, RWA, DeFi, and other sources. To make this possible, Affluent uses a trustless and transparent strategy vault system that abstracts away the complexity of yield-generating strategies.

The essence of Web2.5 fintech is combining the user experience proven in Web2 with the open, trustless infrastructure and global accessibility of Web3. Affluent is targeting this exact intersection—connecting Telegram’s global reach with blockchain-based yield infrastructure to build a wealth management solution no existing service has ever offered.

1.1.1 1st generation: the rise of online brokerages and digital finance

Source: BBC

In the mid 1990s, the rise and spread of the internet brought about a major transformation in the financial industry. Individual investors were able to trade stocks and assets online, thanks to the emergence of services like E*Trade and Charles Schwab. During this period, not only stock trading but also banking and payment systems rapidly digitized. In 1998, PayPal launched and opened up a new industry of online payments, and in 2004, Alipay launched in China, marking the beginning of the era of electronic payments and digital financial services.

One key characteristic of first generation fintech was that investors could engage in financial activities without calling a representative or visiting a branch, significantly reducing transaction fees and entry barriers. Online brokerages did not just support stock trading and payments, but also offered a wide range of fund products, enabling ordinary investors to access financial services that were previously reserved for high-net-worth individuals. This democratization of investment services through first generation fintech is seen as the beginning of widespread participation in securities investment.

1.1.2 2nd generation: smarter asset management powered by robo advisors and algorithms

Source: Vanguard

Whereas early online asset management was mostly limited to deposits and funds, from the late 2000s a new type of tech-driven asset management began to emerge. At the heart of second generation fintech is algorithm-based management services, represented by robo advisors. Enabled by AI algorithms, big data analysis, and the proliferation of smartphones, robo advisors could perform asset allocation and rebalancing faster and more consistently than humans.

Leading examples include Betterment and Wealthfront, which were founded shortly after the 2008 financial crisis. In response to this trend, traditional financial institutions like Vanguard and Charles Schwab also launched their own robo advisor services and joined the market.

While first generation fintech helped popularize basic asset management such as deposits and funds, second generation fintech popularized more sophisticated wealth management services. These types of services were traditionally reserved for wealthy clients with access to personal advisors, but robo advisors opened the door for small retail investors to receive professional investment guidance.

1.1.3 3rd generation: integrated wealth management through super apps

Source: The Rookie VC

By the 2020s, smartphones had become central to everyday life, and in fintech, the concept of super apps began to take hold. Third generation fintech wealth management services are characterized by offering a full range of financial services—payments, investing, lending, wealth management, insurance—through a single integrated app. Examples of such super apps include PayPal, Cash App, SoFi, Alipay, and WeChat Pay.

The defining feature of super app-based fintech is its dramatically superior UX and accessibility compared to first and second generation fintech. Many super apps are integrated with messaging and social media, which means that anyone with a smartphone can engage with financial services anytime, anywhere.

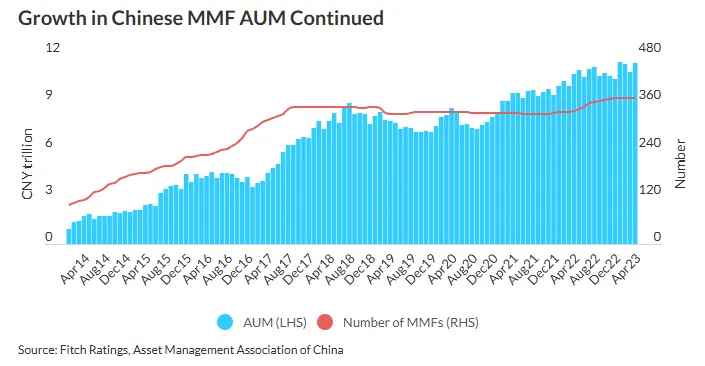

A key global case of third generation fintech is China’s MMF-linked wealth management via super apps. Representative examples include Yu’e Bao by Alipay and Li Cai Tong by WeChat. Users could invest their leftover wallet balance into MMF funds with one click and earn interest easily. In 2017, Yu’e Bao’s AUM surpassed the MMFs of JPMorgan and Fidelity to become the largest in the world. This case shows the powerful impact UX innovation can have on financial adoption.

1.2.1 The financial backend remains outdated

Looking back at the development of fintech so far, it can be summed up in one sentence. Improved UX has led to greater accessibility to a variety of financial strategies. But does that mean there is no more room for improvement in financial services? Not at all. While fintech companies have focused on innovating the frontend of financial systems, the backend remains stuck in legacy technology.

Today’s financial backends are complex and closed off. Each transaction often involves numerous intermediaries, leading to high fees, slow settlement times, and limited global accessibility. But there is a new infrastructure technology that can solve all these issues at once, and that is blockchain.

Blockchain is a decentralized network operated by servers across the globe, meaning it is inherently free from national borders. It can reduce the number of intermediaries, lowering fees, and it processes transactions in blocks, enabling real time settlement. On top of that, it allows automation of financial operations such as trading and asset management through smart contracts.

Thanks to these advantages, there has been a rapid increase in cases of traditional financial institutions and services adopting blockchain.

Payments and remittances: Visa, Mastercard, PayPal, Stripe, Worldpay, Cash App, …

Interbank settlement: JP Morgan, Brevan Howard, UBS, …

Fund tokenization: BlackRock, VanEck, Franklin Templeton, …

Fintech services in the asset management sector are no exception. If blockchain is applied here, the reduction of intermediaries would lower fees, and investors who currently lack access to banking services due to outdated infrastructure could easily tap into strategies like lending, liquidity provision, and RWA. This is the moment when innovation in fintech can truly take off. Now is the perfect time for blockchain based fourth generation fintech to emerge.

1.2.2 The rapid growth of stablecoins

Source: Ark Invest

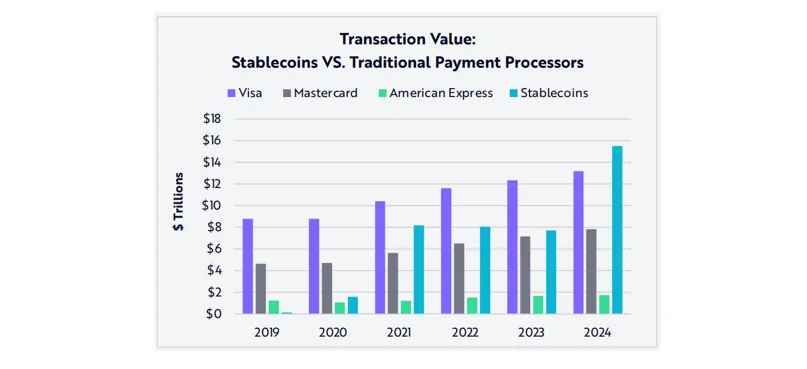

One of the biggest reasons why now is the ideal time for blockchain based super apps is the rapid growth of the stablecoin industry. Stablecoins are one of the few areas in blockchain that have already proven product market fit. According to Ark Invest, in 2024, despite a bear market in crypto, stablecoin transaction volume reached 15.6 trillion dollars, which is 119 percent and 200 percent of Visa and Mastercard’s respective volumes. Especially with the start of the Trump administration, the GENIUS Act, the first federal stablecoin regulatory framework, is being fast tracked. If this bill passes, the stablecoin industry is expected to grow rapidly, especially among American corporations and institutions.

Source: Tether

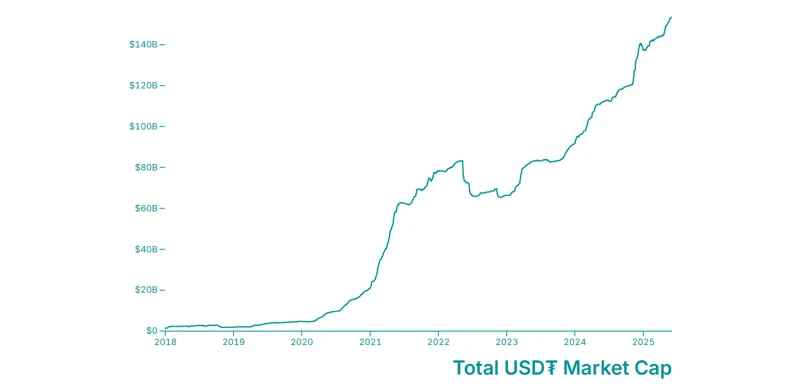

The most notable stablecoin is Tether’s USDT. The supply of USDT has nearly doubled in the last two years, currently reaching 153.9 billion dollars and holding the number one spot by a wide margin. Its user base is estimated at 433 million and its daily transaction volume reaches nearly 36 billion dollars, making it a massive market. While Tether does not currently comply with Europe’s MiCA or the US GENIUS Act, it is expected to expand into US and European markets through subsidiaries or other channels. Outside of that, it is being actively used in regions with low financial trust such as Africa, Latin America, and Asia.

In other words, Tether has already found product market fit in countries with unstable currency values, and dollarization led by Tether is expected to accelerate in those regions. In this context, if a next generation blockchain based asset management fintech service integrates USDT, it would be accessible to people in many countries around the world, creating a major market opportunity.

1.2.3 Telegram’s Web3 initiatives

Source: effectivesoft

As explained earlier, blockchain is a technology that transforms the backend of financial systems. But in order for users to engage with fintech services, a frontend with excellent UX is still essential. In this regard, Telegram is a prime candidate to serve as the frontend for next generation blockchain based super apps.

Telegram is a messenger app launched in 2013 by Pavel and Nikolai Durov. Unlike other messenger apps, it is built on core values of privacy, anti censorship, and independence. This sets it apart from the centralized approach of traditional Web2 social media platforms. From the start, Telegram has been built on principles aligned with decentralization.

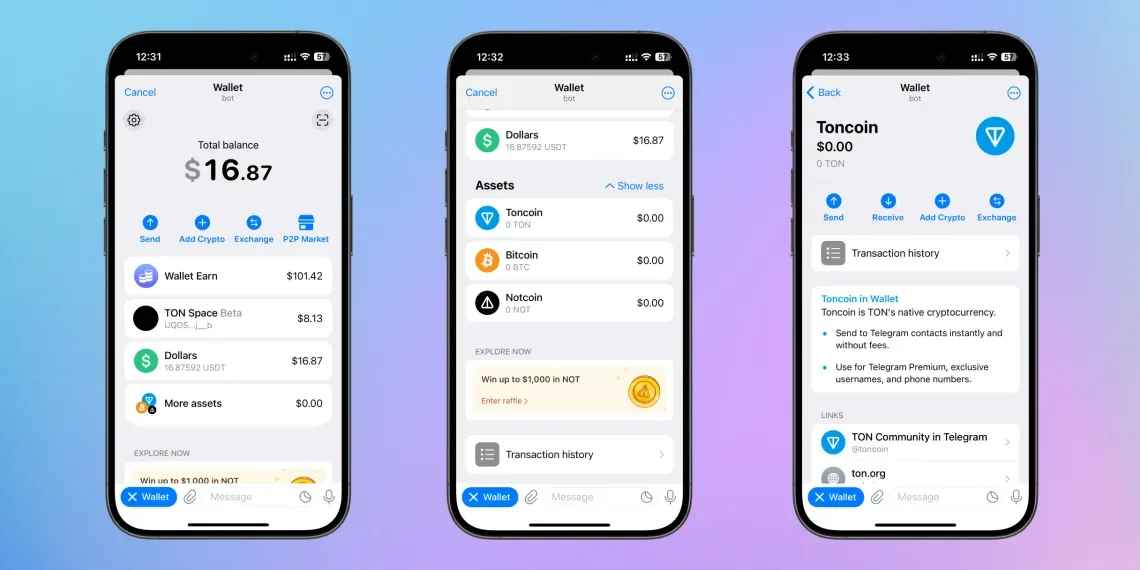

This is consistent with Telegram’s recent Web3 initiatives. Telegram is integrating various services around the TON (The Open Network) blockchain. The platform now features a native wallet embedded directly into the messenger app and is enabling various mini apps to connect and offer services. Users can easily top up their Telegram Web3 wallets via on ramp services, and use a range of DeFi and mini app functionalities. In short, Telegram is evolving from a simple messenger into a Web3 based super app.

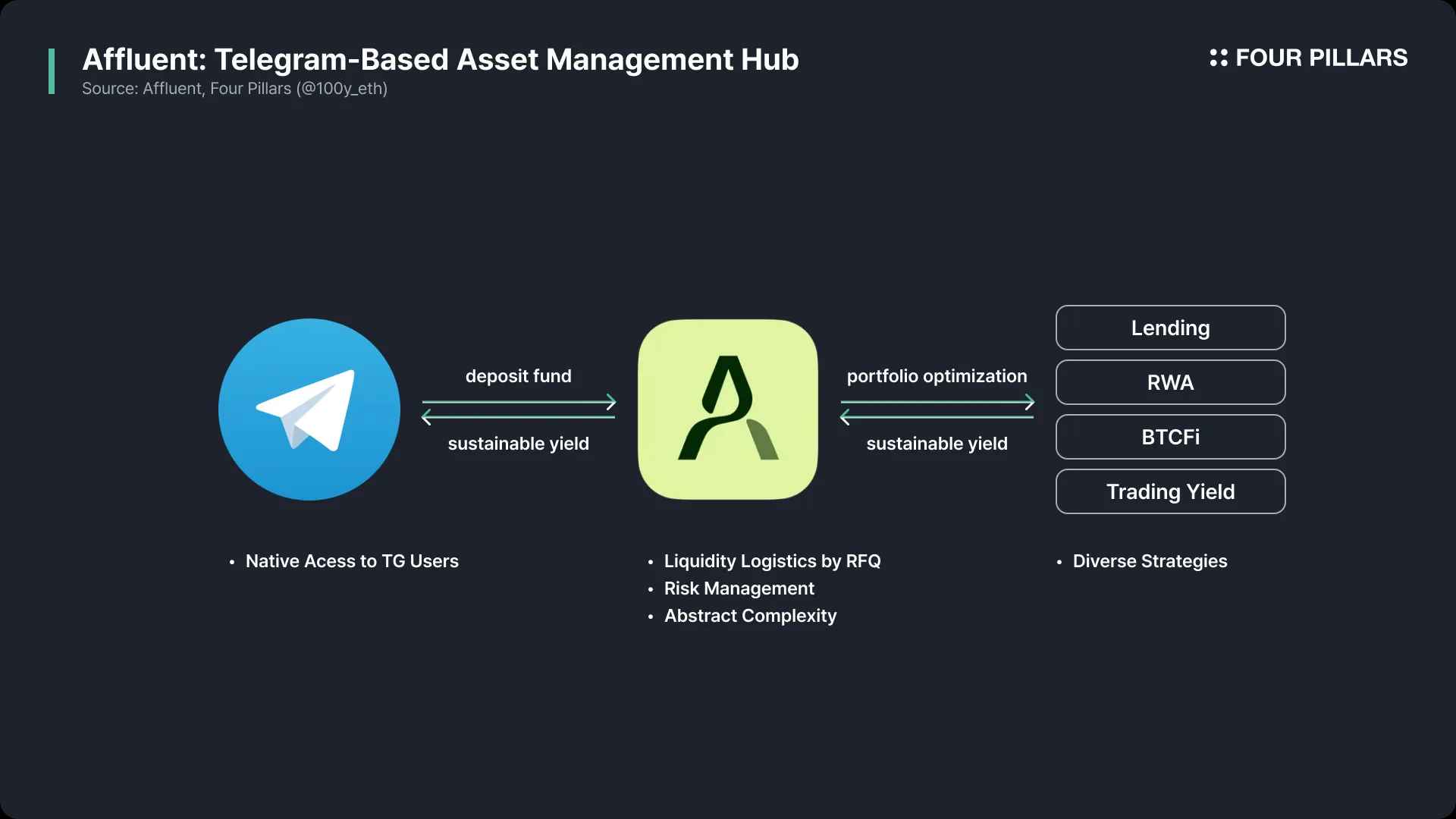

What would it look like if a Web2 product that has already found product market fit like Telegram is integrated with a Web3 product with proven product market fit like USDT? The answer can be found in Affluent, a blockchain based next generation asset management fintech service.

Affluent has a clear goal. To deliver a Web2.5 fintech experience to global users. To achieve this, Affluent abstracts complex blockchain based investment strategies and makes them accessible through a familiar and user friendly frontend like Telegram.

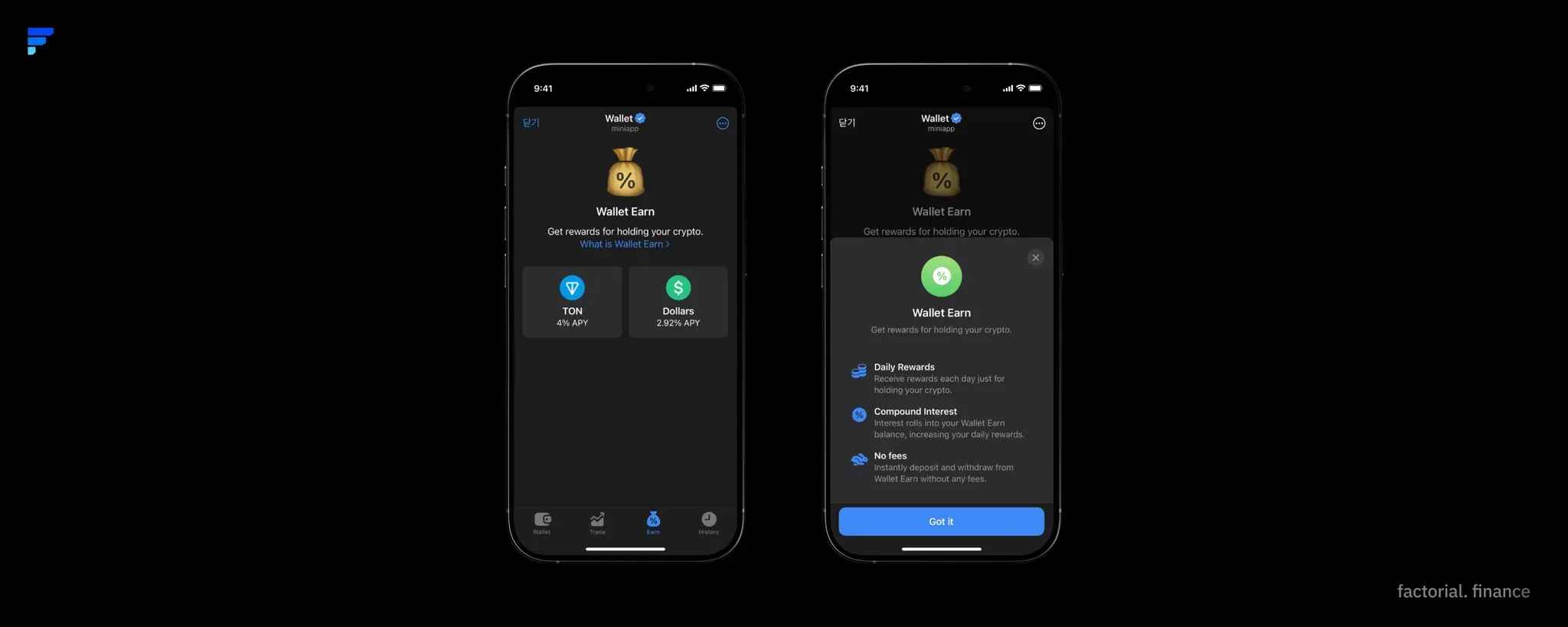

Source: Affluent (prev. Factorial Finance)

Telegram’s native wallet includes an Earn section, and the Affluent service will soon be integrated into it. Telegram users will be able to easily manage and invest their crypto holdings through Affluent. While traditional financial services depend on trust in intermediaries, blockchain based Affluent removes that need. Users maintain full ownership and control over their assets, enabling real financial sovereignty. This greatly reduces intermediary costs and expands financial inclusion to regions and user groups previously underserved by the financial system.

Affluent’s product direction aligns with the team’s core philosophy:

Mass adoption: Build a Web2.5 fintech experience with seamless UX distributed via Telegram

Open design: Through modular architecture, any Affluent participant can create and customize unique financial activities

Diversity: Provide a variety of yield generating strategies through strategy vaults

UX abstraction: Use offchain processes in a trustless manner to deliver a simple experience to end users

Trustless: Every component of Affluent’s architecture is built on trustless interactions between participants

Before diving deeper into Affluent, let’s briefly look at its history.

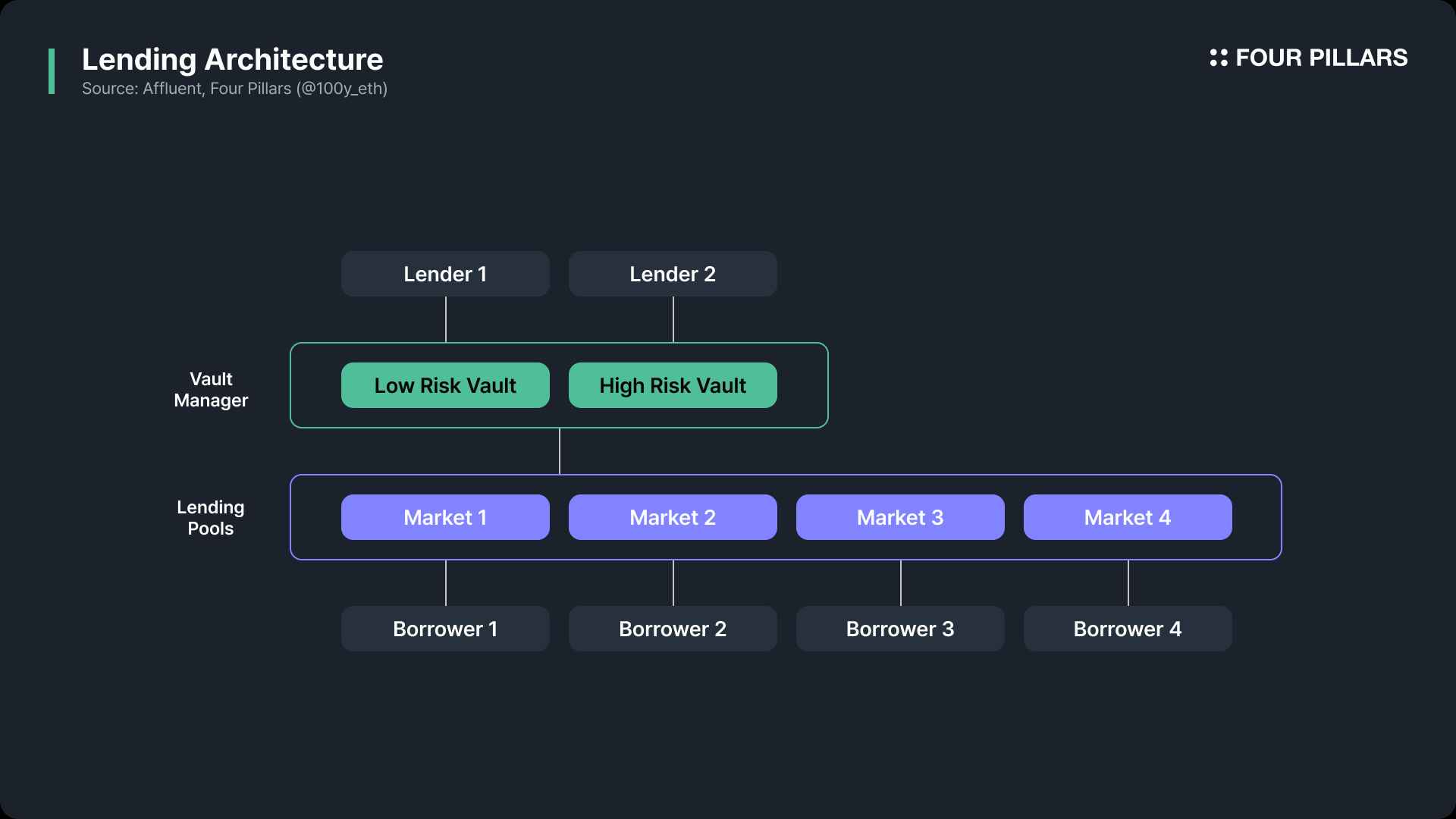

Before becoming a next generation fintech service, Affluent started as a modular lending protocol called Factorial Finance. The core model adopted a structure similar to Morpho Blue, one of the most prominent lending protocols in the Ethereum ecosystem.

Each lending pool operates as an isolated pool, meaning that if an incident occurs in one pool, the risk does not spill over to others. Factorial Finance offered a Pool Factory feature that allowed anyone to easily launch custom lending pools by choosing collateral types, loan assets, interest rate models, oracles, and risk frameworks.

Above these diverse lending pools is a vault layer. Each vault distributes liquidity across multiple pools based on a target risk or reward profile, rebalancing funds and optimizing yield to create a portfolio. This allows users to easily deposit without dealing with complexity.

Unlike money markets that use multiple assets as collateral and loan assets in one unified system, vaults built on isolated pools offer the following advantages:

Safety: Since liquidity between isolated pools is separated, issues in one asset do not affect other pools or assets

User convenience: Users can choose from a variety of vaults based on their preferred risk or reward profile, and deposit funds without worrying about rebalancing or optimization

Capital efficiency: Vault operators can dynamically allocate funds based on utilization ratios in isolated pools, improving the capital efficiency of the overall money market

Affluent’s lending platform offers more than just basic lending pools. It also includes advanced pools with higher risk and reward, leverage strategies through looping, and support for assets like SLP, the liquidity token of Storm, a perpetual DEX in the TON ecosystem. This gives depositors access to an even broader range of yield strategies.

2.3.1 Toward a Telegram based asset management hub

Let’s take another look from the user’s perspective. Users can easily deposit funds by choosing a vault with their preferred risk or reward profile among the many vaults offered by Affluent and earn interest from lending. But does yield generation need to be limited to lending? Wouldn’t users be exposed to a more attractive risk or reward profile if they could earn interest from more diverse sources?

Affluent is built on the TON network. This means it is in a strong position to leverage the network effects of Telegram as a massive platform. Telegram’s emphasis on censorship resistance and privacy, driven by the Durov brothers, also means its users tend to be more open and familiar with blockchain services compared to typical Web2 messenger users.

Thanks to these strategic advantages, Affluent aims to go beyond being a modular lending platform and evolve into a comprehensive crypto based asset management service that offers transparency and zero counterparty risk to Telegram’s massive user base. This marks a shift toward becoming the core asset management platform in Telegram’s evolution into a Web2.5 super app.

This also brings significant benefits for existing DeFi users. Traditional DeFi often requires users to manage wallets, select and transfer assets, and handle risk management on their own, making it less accessible. Affluent abstracts away these steps and dramatically improves UX so that users can invest easily without navigating complexity. In other words, users can access stable yield strategies through a single click in the familiar environment of Telegram without needing additional learning.

2.3.2 Diverse yield strategies

Telegram users will soon be able to access Affluent directly through the Earn section of the native Web3 wallet, deposit funds, and earn stable and sustainable returns. Behind the scenes, however, complex strategies are at work. Affluent’s role is to abstract away this complexity so users do not have to worry about it.

Affluent aims to generate returns through four types of strategy vaults, including lending:

Lending: Deposited assets are used for loans and generate interest in return. Vault managers can use dynamic lending positions within predefined leverage limits to increase capital efficiency. This includes leverage lending strategies using liquid staking tokens, allowing users to expect higher returns at relatively low risk.

Real World Assets (RWA): A sustainable and scalable yield source that can serve as the baseline return for the Affluent platform. The strategy vault system holds idle liquidity in yield generating RWAs or stablecoins and quickly moves that liquidity into lending pools when loan demand increases. When demand falls again, funds are reinvested into stable RWAs, dynamically optimizing deposit yield.

DeFi: Deposited assets are used for DEX LP provisioning or delta neutral positions in perpetual markets to earn funding fee income.

CeFi: Some strategy vault managers are allowed to deploy capital into strategies like CEX DEX arbitrage to generate returns.

Because many strategies are used, the liquidity needed is not limited to TON alone. Affluent is building an RFQ system so that strategy vault managers can access yield opportunities and liquidity across different networks beyond TON. In the future, Affluent also plans to launch a vault of vaults that sits above the strategy vault layer, enabling dynamic allocation of liquidity across strategies and further optimizing returns.

2.3.3 Growth strategy of Affluent

To support a variety of yield strategies, Affluent must integrate with a wide range of protocols and support many different assets. In addition to TON, USDT, stTON, tsTON, and SLP, the following assets are planned for support:

tgBond: In April 2025, Libre and the TON Foundation tokenized 500 million dollars worth of Telegram bonds on the TON blockchain. This represents a portion of Telegram’s total 2.35 billion dollar bond issuance.

tgBTC: tgBTC is a token issued through the TON Teleport BTC system. Users can send Bitcoin to a BTC address provided by TON Teleport and receive an equivalent amount of tgBTC on the TON network.

tsUSDe: In May 2025, the TON Foundation partnered with Ethena to onboard USDe into the TON ecosystem in the form of tsUSDe. USDe is a stablecoin that generates yield through delta neutral positions in perpetual markets via funding fees.

syrupUSDC: syrupUSDC is USDC deposited into Maple Finance, where the funds are lent to businesses and the interest is accumulated in syrupUSDC.

mTBILL: mTBILL is a token issued by Midas and is backed by ETFs like those from BlackRock that invest in US short term treasuries.

XAUT0: XAUT0 is a cross chain version of XAUT, which is a token backed by gold and tracks the price of gold.

This means Affluent users can gain exposure to a wide range of strategies using assets such as gold, Bitcoin, government bonds, corporate credit, and stablecoins that generate yield through lending or trading. Affluent also plans to support fixed interest markets through lending pools with maturity, enabling not only individuals but also institutions to access stable yield opportunities.

The world is ready for blockchain based fintech. At this point in time, I believe what we need is not Web3 native fintech but Web2.5 fintech. The essence of Web2.5 fintech lies in combining the user experience proven in Web2 with the open, trustless infrastructure and global accessibility of Web3. Affluent is a service aiming directly at this intersection, connecting Telegram as a global platform with blockchain based yield infrastructure to create a new kind of asset management solution no service has provided before.

This goes beyond simply using new technology. It is a redefinition of global financial accessibility. By removing borders and intermediaries through a blockchain backend, and providing an intuitive financial interface through the Telegram frontend, Affluent demonstrates the potential to become a true global asset management super app. It holds the potential to be used by anyone, including people in countries with low trust in currency or lacking financial infrastructure.

Ultimately, Web2.5 fintech is a new wave that drives the democratization and universalization of asset management. Just as the internet democratized access to information, blockchain can democratize access to finance, and at the forefront of that transformation stands Affluent.

Dive into 'Narratives' that will be important in the next year