The wallet and account layer is emerging as crypto's new frontier for value capture. Positioned at the user interface level yet functioning as sophisticated middleware, this layer is becoming the critical infrastructure that shapes user experience while seamlessly connecting multiple blockchain networks.

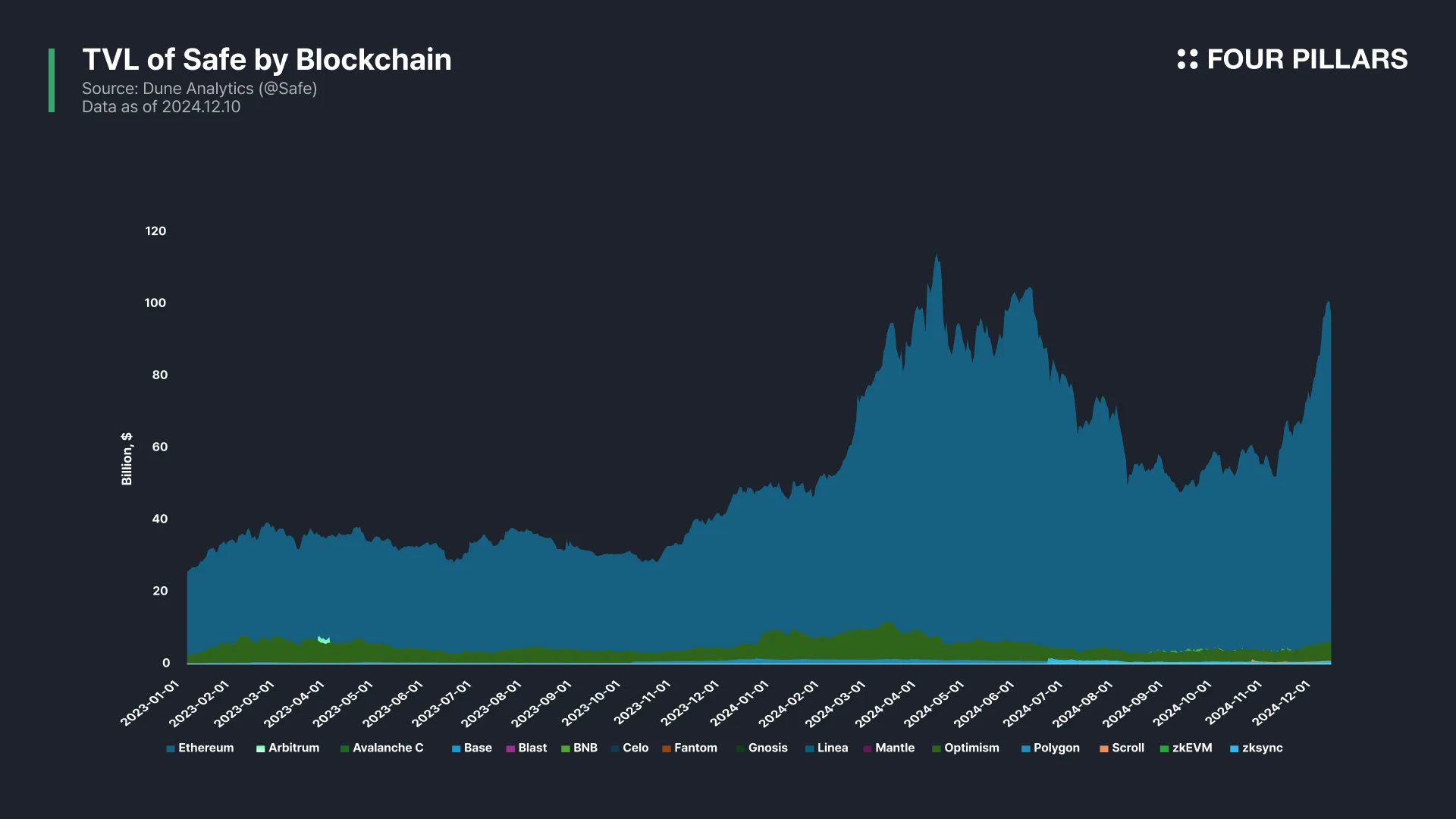

Safe has evolved from a simple multisig wallet in 2017 to the most trusted smart account infrastructure in crypto. With $70 billion in assets under management and 11 million smart accounts deployed, it stands as the backbone of Ethereum's institutional and retail custody solutions.

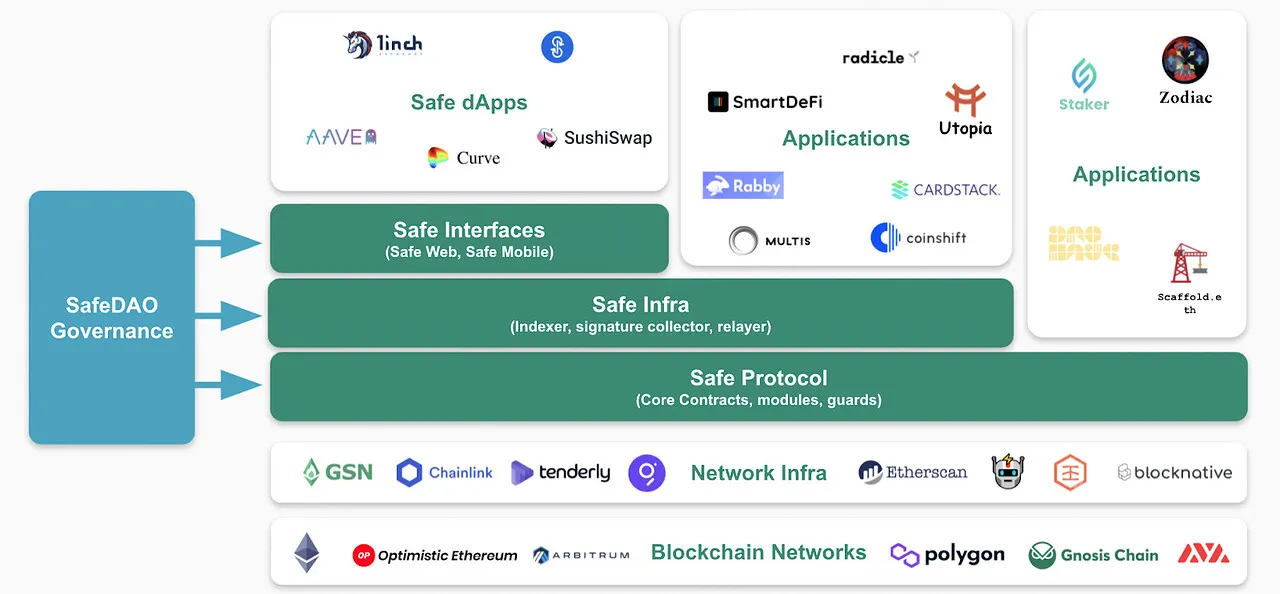

The Safe{Core} Protocol is establishing the industry standard for smart account integration, with its SDKs and APIs powering over 200 projects including major platforms like Polymarket and Worldcoin. Through Safe{Wallet}, it offers users direct access to these applications via an integrated app store.

Safe's modular architecture excels through clear separation of concerns: transaction execution, security validation, and protocol support. This design enables critical Web3 features like transaction simulation and social recovery, while ensuring users maintain sovereignty over their assets.

Safenet introduces a paradigm shift in cross-chain transactions through its decentralized network of processors, validators, and liquidity providers. By separating execution from settlement - similar to Visa's model - it achieves sub-500ms transaction speeds while maintaining security.

As blockchain infrastructure commoditizes, Safe's ability to abstract complexity while preserving security and interoperability positions it at the forefront of crypto's evolution. Through solutions for account abstraction and cross-chain settlement, Safe is defining the future of digital asset ownership.

The "Fat Protocol" thesis, introduced by USV's Joel Monegro in 2016, has been a foundational principle in crypto market. The thesis presents a compelling argument: blockchain networks fundamentally differ from traditional internet by acting as platforms that host both protocols and applications. This architectural distinction leads to a unique value distribution where the protocol layer captures the majority of value, contrasting sharply with traditional internet models. This framework has profoundly influenced market understanding and strategic decisions.

The thesis gained widespread acceptance across the market. For instance, even if Uniswap were dissatisfied with Ethereum's fees or policies, migrating to another chain would be challenging. Such a move would require abandoning their existing user base and losing interoperability with other DeFi protocols built on Ethereum. Consequently, Uniswap remains tethered to chains where their protocol operates, whether Ethereum or its L2s, creating a network effect that continues to draw users to these chains.

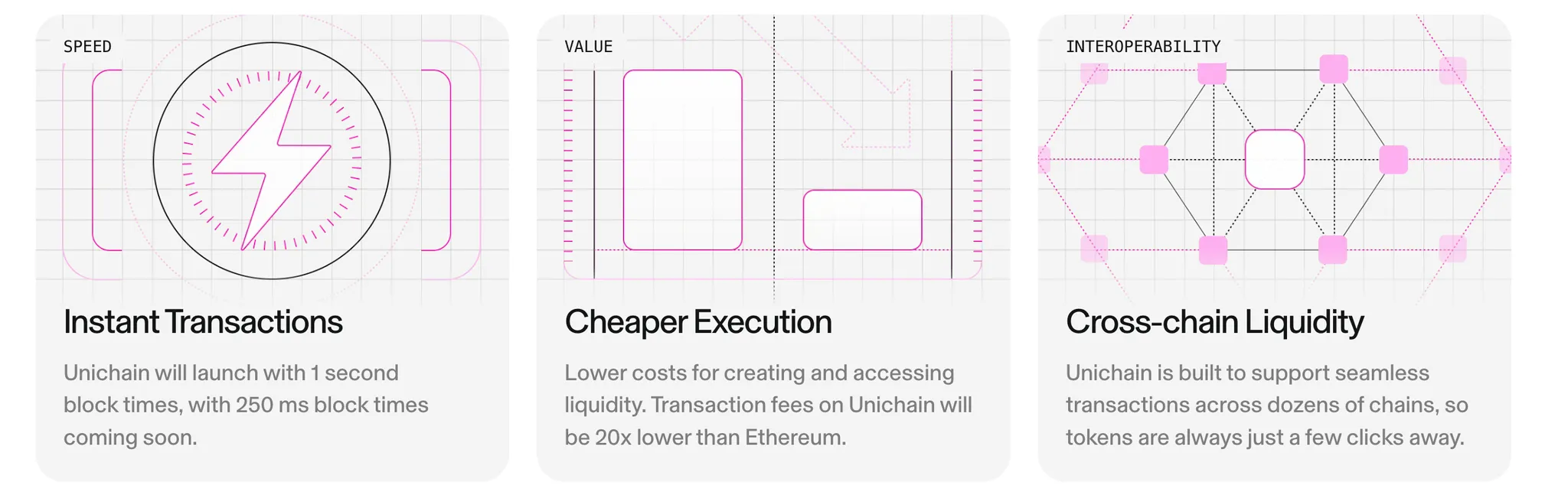

Source: Unichain

However, recent technological developments and evolving market dynamics are challenging this established paradigm. The launch of Unichain, Uniswap's new L2 initiative, represents a significant shift in this relationship. Historically, Uniswap has handed over transaction fees and MEV to external parties (primarily Ethereum's block builders or validators). With reduced barriers to chain development and improved cross-chain user experiences, Uniswap now aims to internalize value that previously leaked to external parties by launching its own chain, potentially improving both performance and economic security.

Uniswap isn't alone in this trend. Major protocols previously operating on Ethereum or its rollups - including Frax, Swell, Ethena, and Worldcoin - have announced plans to launch its own chains. This phenomenon is not restricted to Ethereum's ecosysten. Projects like Grass, Helium, and Code on Solana have similarly evolved from applications into independent chains or L2 sequencers.

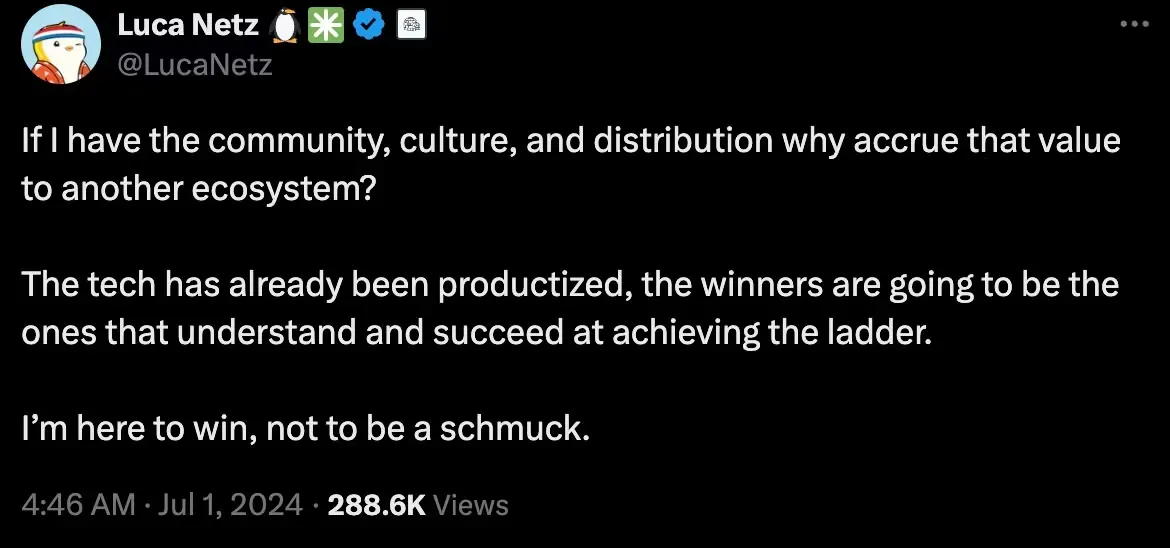

Applications are inherently motivated to seek greater economic value and control through ownership of block space and sequencing. As demonstrated by Unichain, applications can deliver enhanced user value through protocol-level optimizations that generate additional revenue or reduce costs. Alternatively, other specialized chains can offer tailored features such as native account abstraction or KYC/KYB integration that align with specific use cases and user experiences.

Source: X(@LucaNetz)

This trend toward application-specific chains is likely to accelerate. The evolution of rollups and modular frameworks has significantly lowered the barriers to chain development, and these barriers will continue to decrease. Particularly for applications that have achieved strong PMF or brand value, there's little incentive to surrender their generated value to uderlying layers.

As the established "Fat Protocol" thesis becomes less definitive, a crucial question emerges: what will emerge as the new primary layer for value accrual?

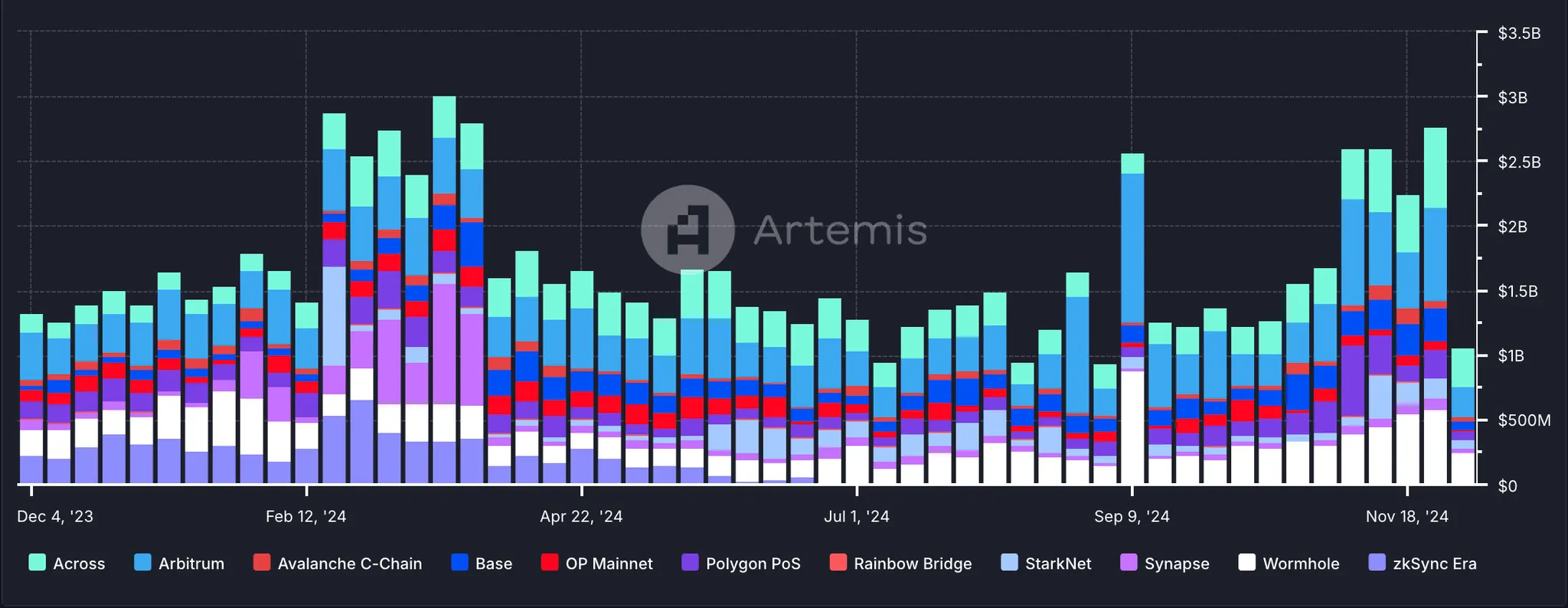

Source: Artemis

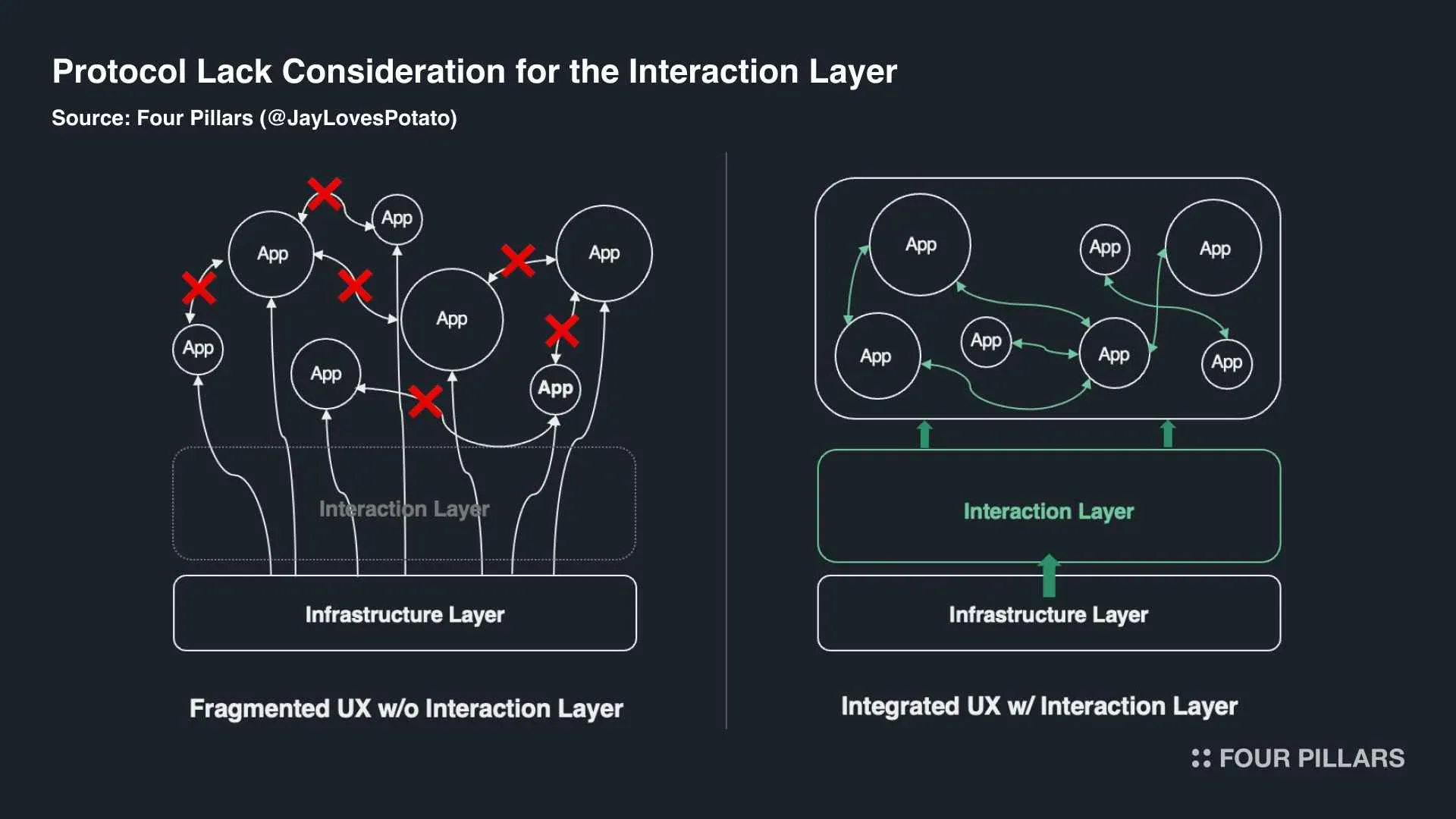

As blockchain networks continue to proliferate, the complexity of managing assets across dozens of chains has become increasingly challenging for users. While this multi-chain future holds promise, it presents fundamental challenges that must be addressed for widespread adoption.

Fragmentation across blockchain ecosystems creates significant barriers to entry. Users must navigate multiple chain-specific complexities: managing assets, using different tools, and handling various gas payment systems. This technical overhead proves particularly challenging for mainstream users accustomed to the seamless experiences of Web2 applications.

Protocol developers face similar challenges, particularly in the initial growth phase. Unlike Web2's established distribution channels such as the Apple App Store, the cryptocurrency ecosystem lacks effective discovery mechanisms. Even mature networks like Ethereum and Solana struggle to provide comprehensive application discovery beyond social channels, making it difficult for new protocols to attract and retain users.

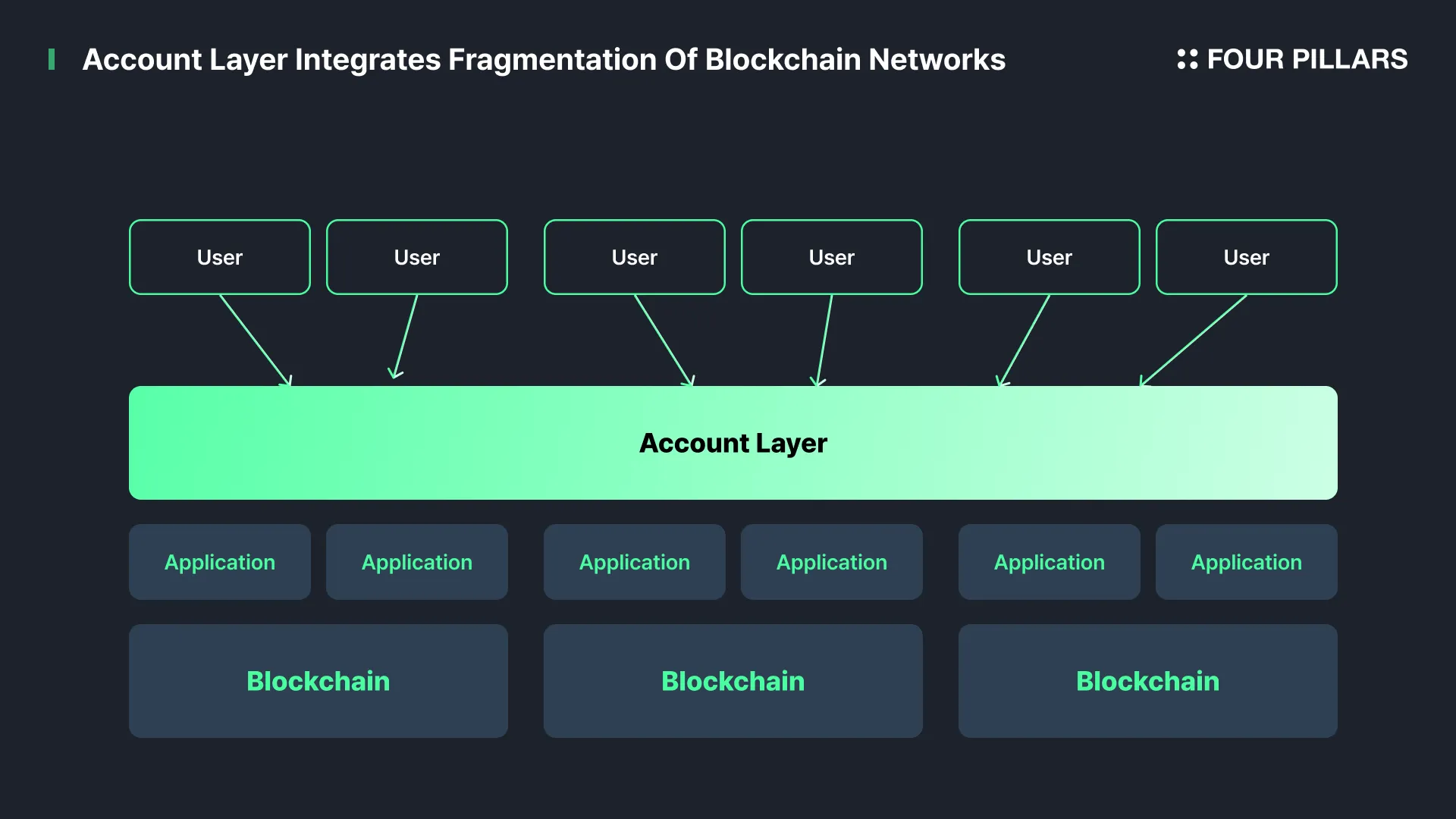

These challenges represent structural issues that technical improvements to individual chains alone cannot resolve. The success of a multi-chain ecosystem requires a new integration layer that can unify these fragmented experiences while providing consistent user interfaces.

Source: EthCC (Vitalik Buterin)

In this context, the account layer has emerged as a promising solution for integration. By acting as middleware between protocols, applications, and users, it offers unique potential to bridge these elements while abstracting away underlying complexities. Furthermore, the rapid pace of innovation in this space is particularly promising. Development at the account level continues to accelerate, suggesting we're still in the early stages of realizing its full potential.

While account abstraction and related technologies have been subjects of research and discussion for years, practical limitations—including technical constraints and high gas fees—previously hindered widespread adoption. However, the technology has now progressed beyond the research phase into active implementation across numerous services. The introduction of EIP-4844 earlier this year has substantially reduced gas fees to negligible levels, removing a significant barrier to adoption. In consumer applications, we're increasingly seeing account creation through Passkeys and social login mechanisms become the default option. In many cases, the wallet integration has become so seamless that users may not even recognize its presence unless they specifically look for it.

Its positioning at the user interface level provides strategic advantages. As protocols become increasingly commoditized, successful user acquisition and product-market fit have become crucial differentiators. Recent advances in account abstraction now enable experiences that parallel the simplicity of Web2 applications, eliminating traditional barriers like seed phrase management and complex transaction signing.

The evolution of wallet functionality demonstrates integrating layer's potential. Modern wallets extend far beyond basic asset management, offering yield generation, application interfaces, and value capture through transaction sequencing.

Moreover, being able to interact directly with users, wallet and account layer creates significant switching cost and brand value. This establishes stronger network effect that make account layer particularly suitable for value capture in this multi-layered ecosystem.

Perhaps most importantly, the account layer's ability to integrate multiple blockchain networks represents a crucial advantage handling fragmentation. Chain abstraction allow users to interact with applications through a unified interface, eliminating the need to understand or even know about underlying blockchains. This enables seamless exploration of multiple ecosystems without complex cross-chain navigation.

These benefits extend to applications as well. Historically, applications have been constrained by chain-specific user bases when choosing their operating environment. Chain abstraction liberates applications from these constraints, allowing them to select chains based on technical requirements rather than user accessibility. This enables services to optimize for their specific needs while minimizing limitations related to user base access or asset bridging.

As discussed in the previous chapter, the wallet and account layer is emerging as a key value capture layer in cryptocurrency. In this landscape, Safe stands out as one of the most promising projects through its effective PMF and industry-wide recognition. The protocol has established itself as the leading smart contract account solution, with over 11 million deployed accounts and about $70 billion in managed assets. In the past 12 months alone, Safe has processed transactions worth $150 billion. With the recent launch of Safenet, their cross-chain account abstraction solution, Safe is positioning itself as an integration layer for the multi-chain era. This chapter examines the Safe protocol and its wallet infrastructure.

Safe has a rich history that began as an internal project at Gnosis before evolving into an independent ecosystem. This journey, along with its battle-tested technology and products, demonstrates Safe's potential as an account layer capable of supporting multiple blockchains and protocols.

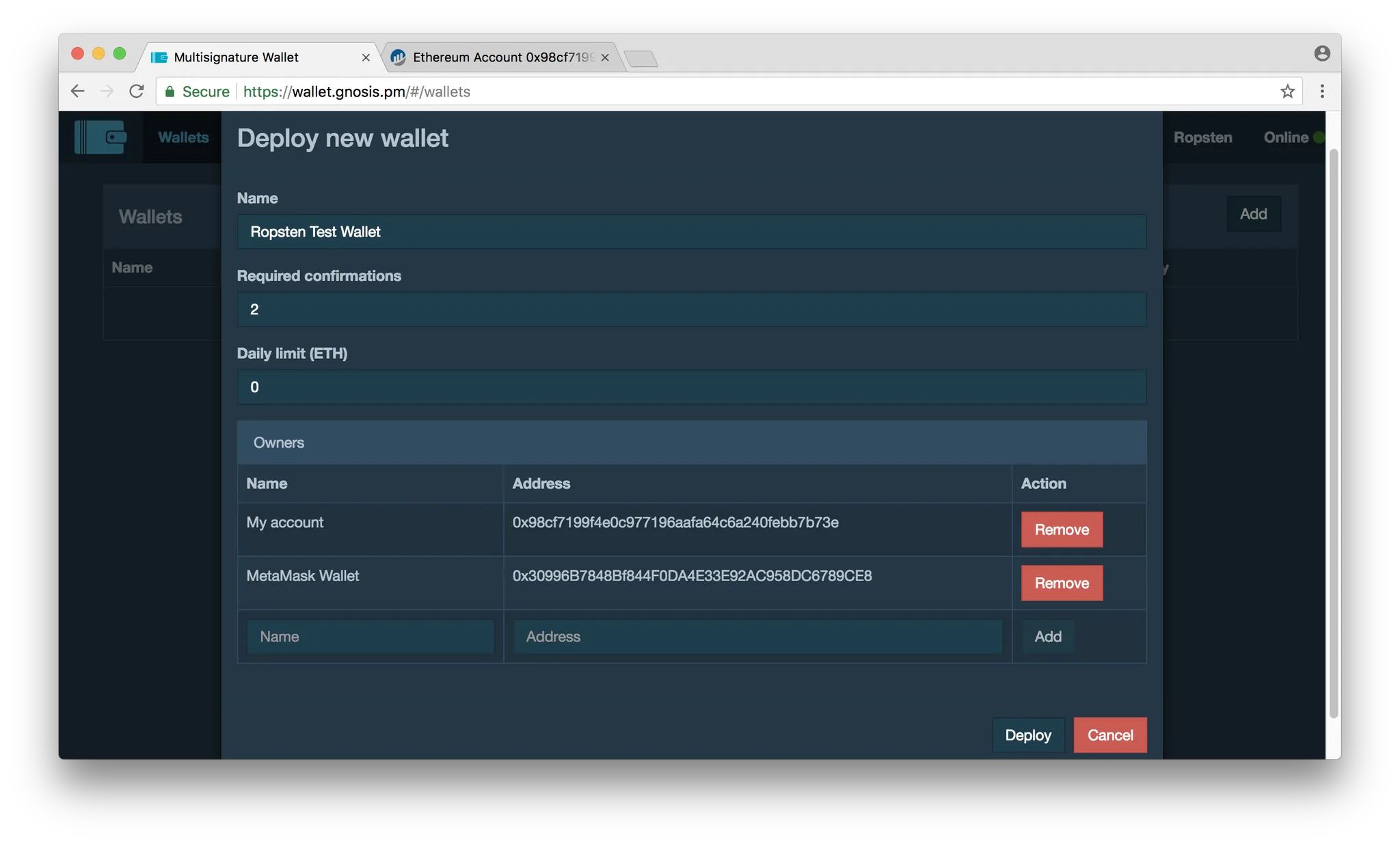

The story of Safe dates back to Gnosis's ICO in early 2017. At the time, the team needed a secure solution to manage their ICO funds, but no mature options existed for this purpose at then. Memeber of Gnosis responded by creating a PoC for a multi-sig wallet, which was later open-sourced as the Gnosis MultiSig Wallet.

Source: History of Safe

As the ICO boom took off, hundreds of projects followed suit, and the Gnosis MultiSig Wallet quickly became the de facto standard for multi-signature solutions. Within just a few years, it was securing over $1 billion in assets. As the unique capabilities of smart contract-based wallets became increasingly apparent, Gnosis assembled a team to develop a next-generation solution. This led to the birth of Gnosis Safe in 2018, designed as a universal smart account solution.

Initially, Safe focused on users who could benefit most from its enhanced security and modularity, such as crypto projects and DAOs. As the product matured and became more accessible and trustworthy, it naturally attracted a broader user base, including market makers, VCs, whales, and NFT communities. The adoption of Safe gained further momentum through market cycles, with its value as a custody solution becoming particularly evident during events like the FTX collapse, which highlighted the risks of centralized service providers.

Source: GIP-29: Spin-off safeDAO and Launch SAFE Token

By 2022, it became clear that Gnosis Safe had evolved beyond a simple project into a platform requiring tailored solutions for various user groups. This realization led the GnosisDAO community to spin off the Safe project. The team established a new mission: to grow an ecosystem centered around Safe smart accounts and ultimately enable all Ethereum user groups to benefit from smart account features. After successful fundraising from strategic investors and the establishment of the Safe Ecosystem Foundation, SafeDAO was formed in late 2022.

Source: Areta

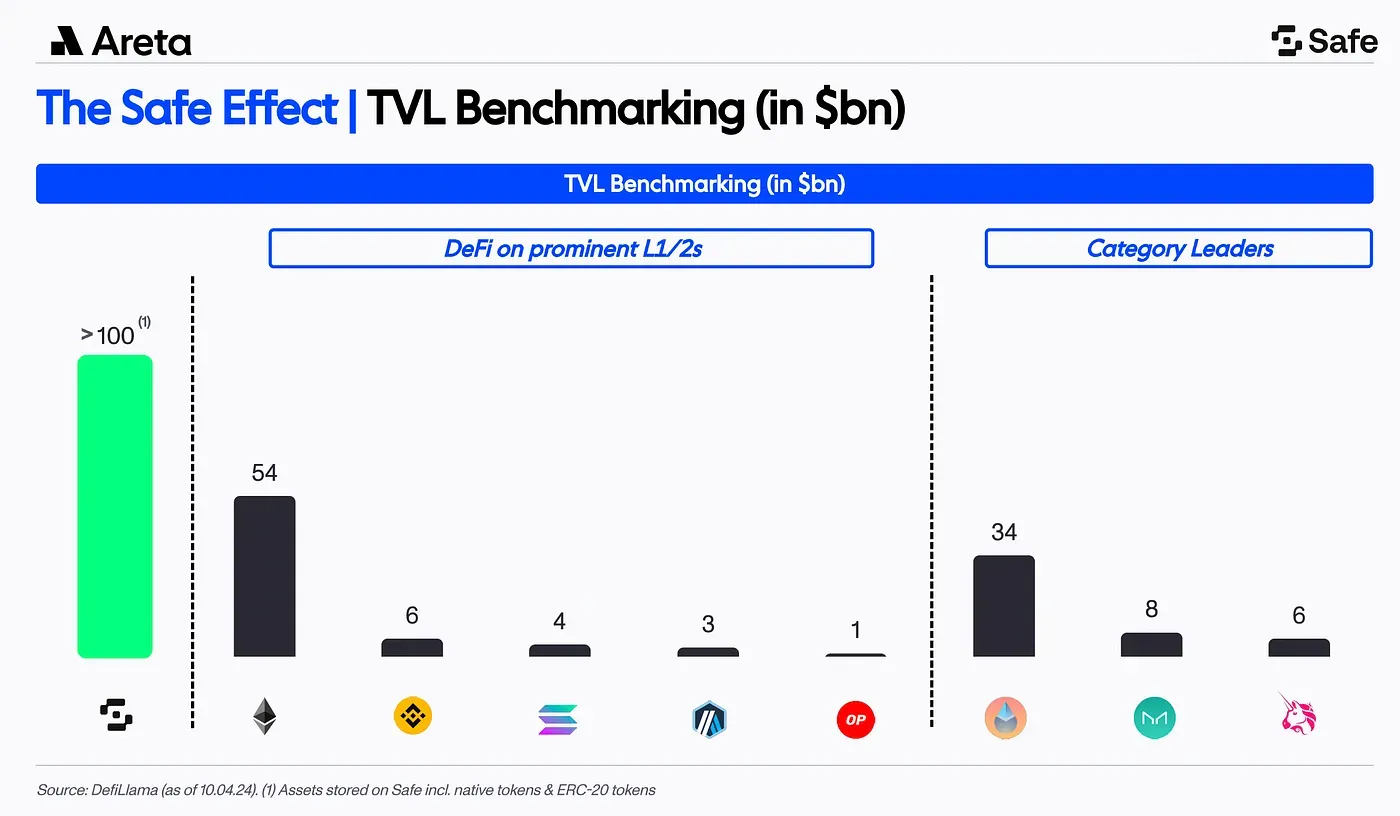

As of 2024, Safe has grown into the second-largest smart contract by assets under custody after Ethereum's staking deposit contract, securing around $100 billion in assets. This figure not only dwarfs other DeFi protocols but also matches or exceeds the deposits of most centralized exchanges except Binance. Furthermore, Safe wallets hold 6% of the total USDC supply and 9% of all CryptoPunks NFTs, underlining its high trustworthiness and broad user base.

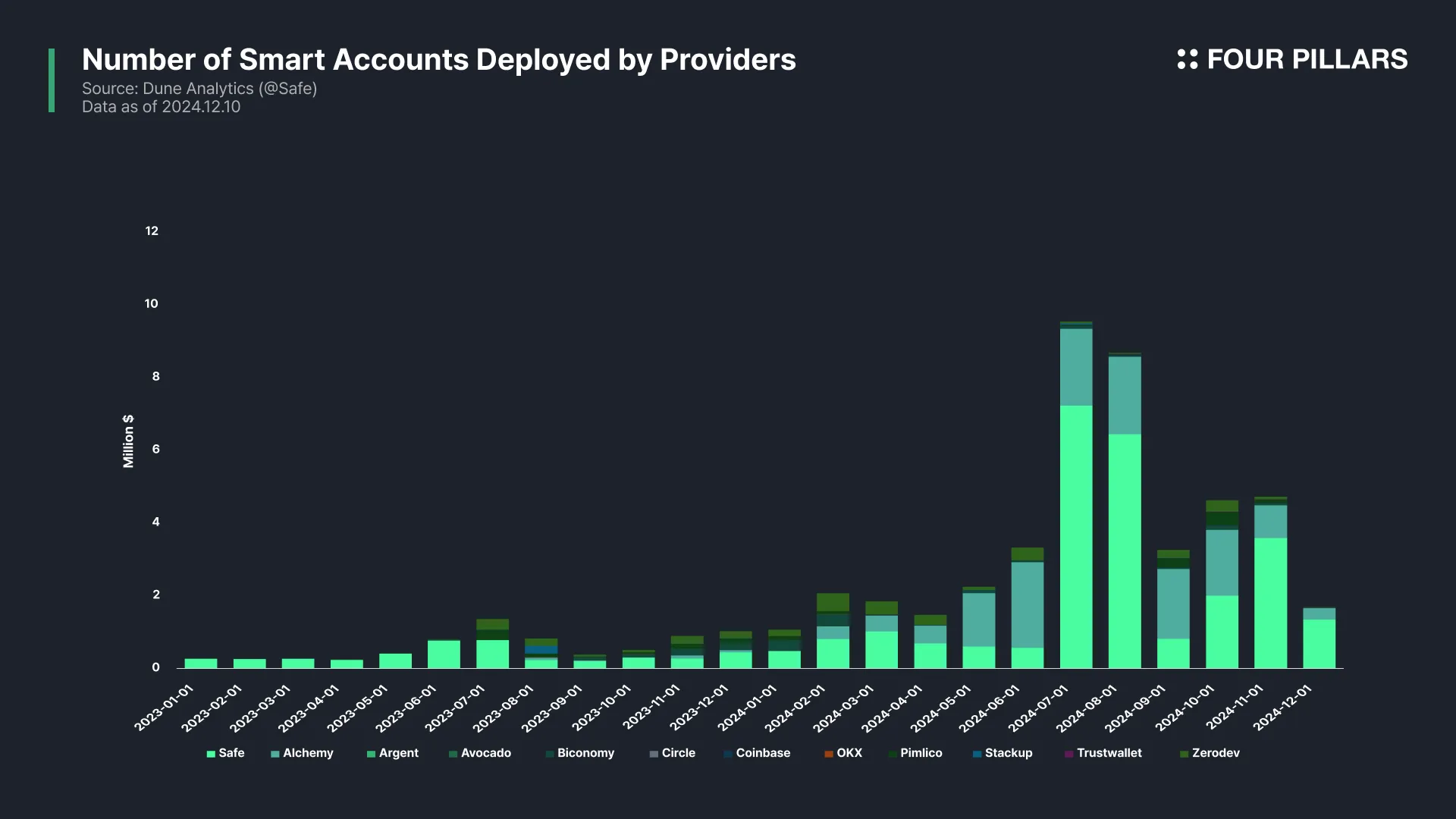

The adoption of smart accounts through Safe{Core} has also seen remarkable growth. Safe has deployed over 11 million smart accounts, making it the largest smart account provider. Through integrations with services like Gnosis Pay and BasedApp, users can now make payments at any Visa-accepting merchant using assets stored in Safe. Moreover, Safe's smart accounts power the custody stack for Worldcoin, which serves millions of users globally. With over 200 projects across most L1/L2 chains, including Polymarket, Dracula, and World App, integrating Safe's smart accounts, it's clear that Safe has evolved from a simple wallet into a core infrastructure component of the crypto ecosystem.

Source: npm trends

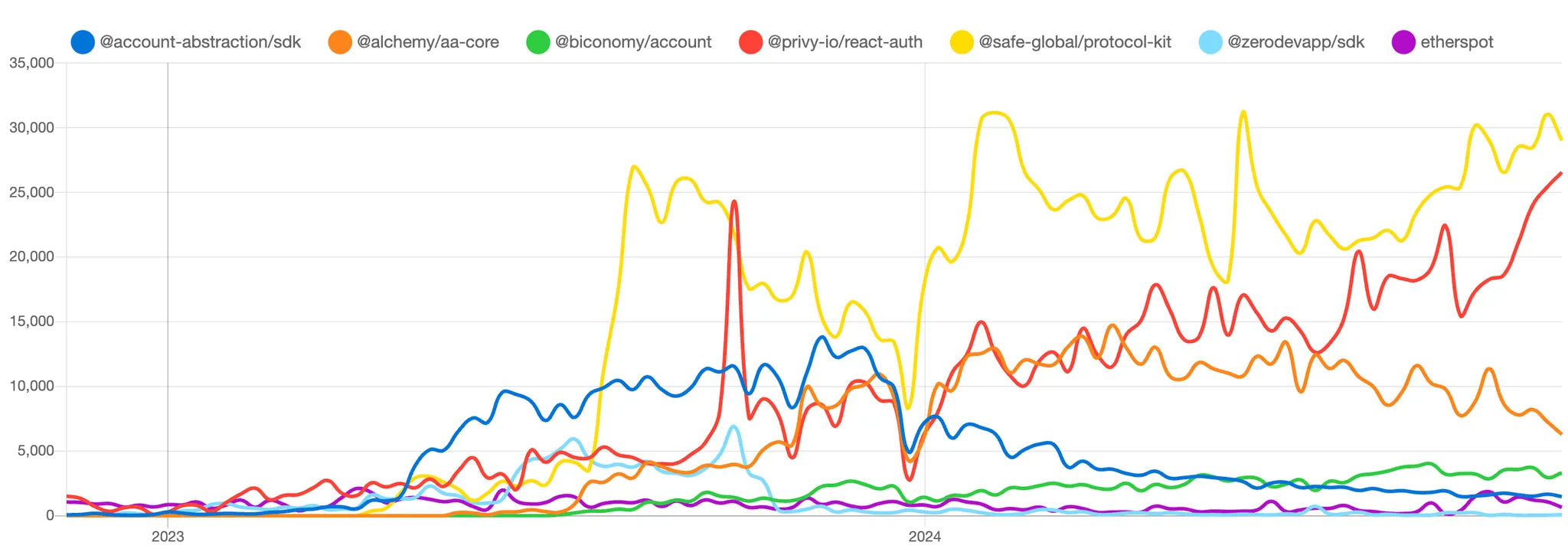

Safe's dominance in the developer ecosystem continues to expand. While the adoption of account abstraction development kits is generally trending upward, this growth is primarily driven by two packages: Safe and Privy. Notably, Safe's SDK maintains the highest market share among competitors, and this lead continues to widen. This success can be attributed to Safe's unwavering commitment to the highest security standards, proven track record, and ability to provide developers with production-ready tools that they can trust. The platform's maturity enables developers to build production-level applications with confidence, further cementing Safe's position as the go-to solution in the space.

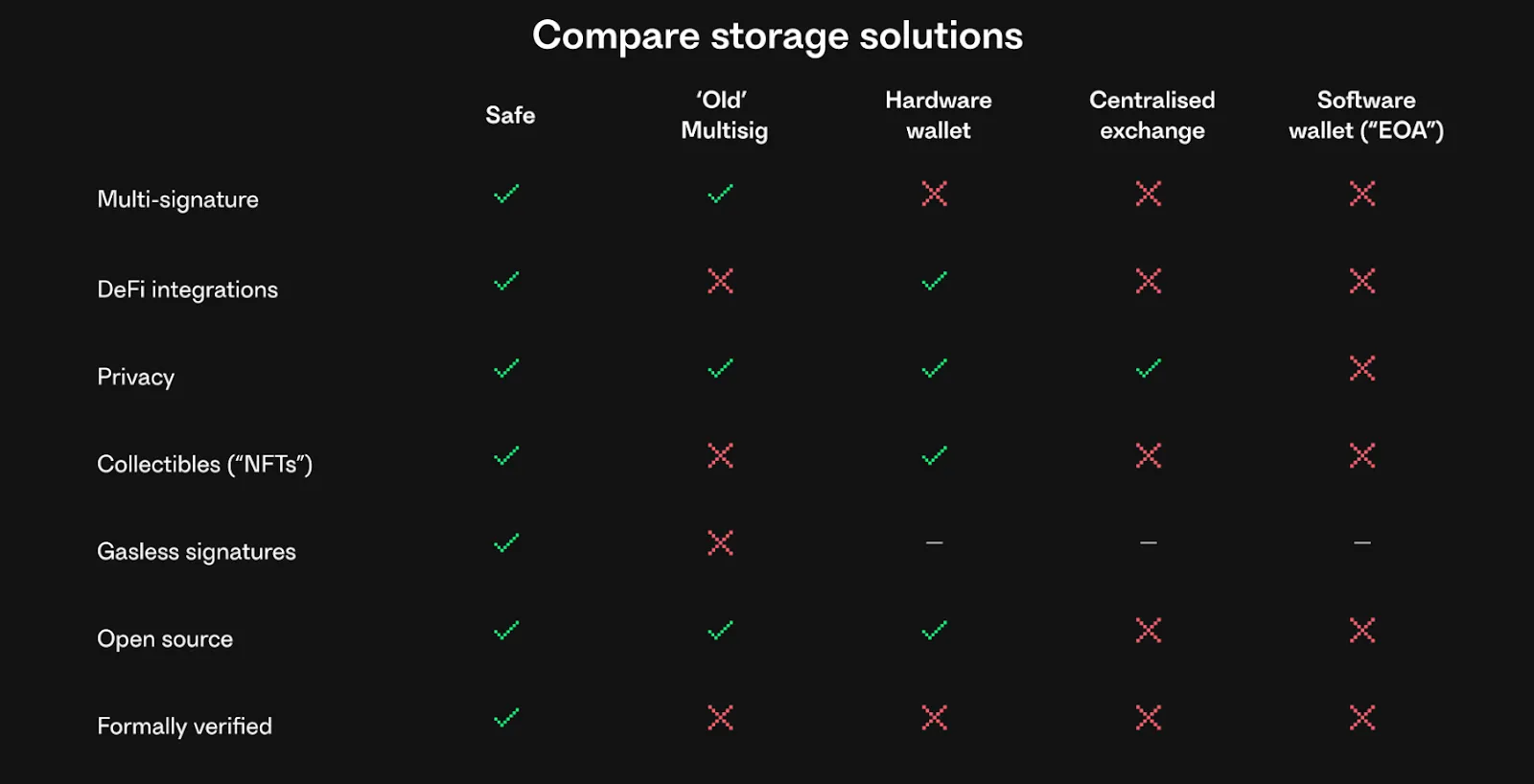

Currently, most interactions on Ethereum occur through Externally Owned Accounts (EOAs). While EOAs serve as the basic form of accounts authenticated through private keys, they have limitations: they lack complex functionality and require users to understand technical aspects like private key management and gas payments. For digital asset ownership to achieve broader adoption, we need more flexible and powerful account structures.

Transforming every Web3 user's account into a smart contract has long been a dream of Ethereum ecosystem developers. Account Abstraction(AA) has been anticipated as a key solution to make Web3 more accessible and secure. Despite years of discussion, adoption has been slower than expected due to high gas fees and complex technical implementation requirements. However, the pace of adoption is expected to accelerate with Ethereum's Pectra upgrade next year and the increasing number of new rollups like Abstract that natively support AA.

Source: Why the Future of Ethereum is Smart Accounts

While Safe has become synonymous with multi-sig wallets, it also maintains the highest market share in the smart account market. What's particularly noteworthy is that Safe isn't just the most battle-tested solution with the longest history; it continues to drive innovation at the forefront of technological advancement.

Safe's wallet stack is built around two core product lines. The first is Safe{Wallet}, a smart account-based solution for secure digital asset custody, and the second is Safe{Core}, a toolkit enabling developers to easily integrate smart accounts into their applications. While Safe{Wallet} and Safe{Core} target different audiences - end users and developers respectively - they share a common foundation built on Safe's smart account architecture.

2.2.1 Safe{Core}

Safe{Core} is a development toolkit and protocol architecture designed to simplify the integration of smart accounts into onchain applications. In traditional EOA-based systems, developers had to implement numerous low-level operations manually, including private key management, transaction signing, and gas fee handling. Safe{Core} abstracts away these complexities, providing developers with packages that let them focus on business logic. It natively supports account abstraction standards like ERC-4337, making it easy to implement advanced features such as gasless transactions and batch transactions.

While various account abstraction solutions are emerging in the market, many either focus on narrow use cases or lack robust security measures. A particular concern is that different smart account implementations are being developed independently, leading to poor interoperability and creating vendor lock-in effects reminiscent of Web2. This not only contradicts the fundamental values of Web3 but could potentially impose even greater limitations than EOAs.

Source: Safe{Core} Protocol Whitepaper

To address these challenges, Safe{Core} focuses on three key principles:

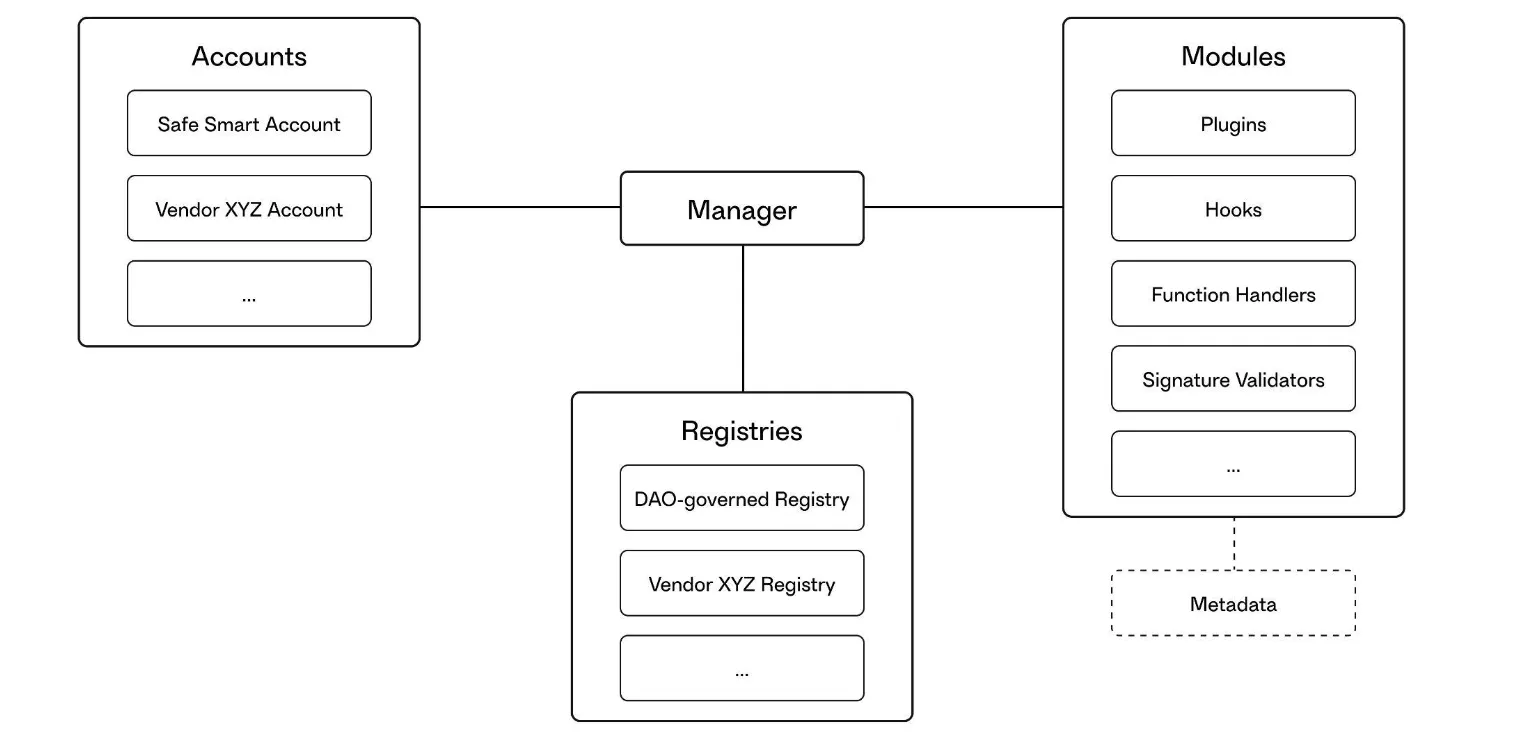

Modularity: Ensures interoperability between applications and SDKs through standardized modules including plugins, hooks, function handlers, and signature validators

Vendor Independence: Preserves account portability without vendor lock-in, giving application developers freedom of choice

Security: Minimizes smart contract risks and provides robust security through a comprehensive registry system

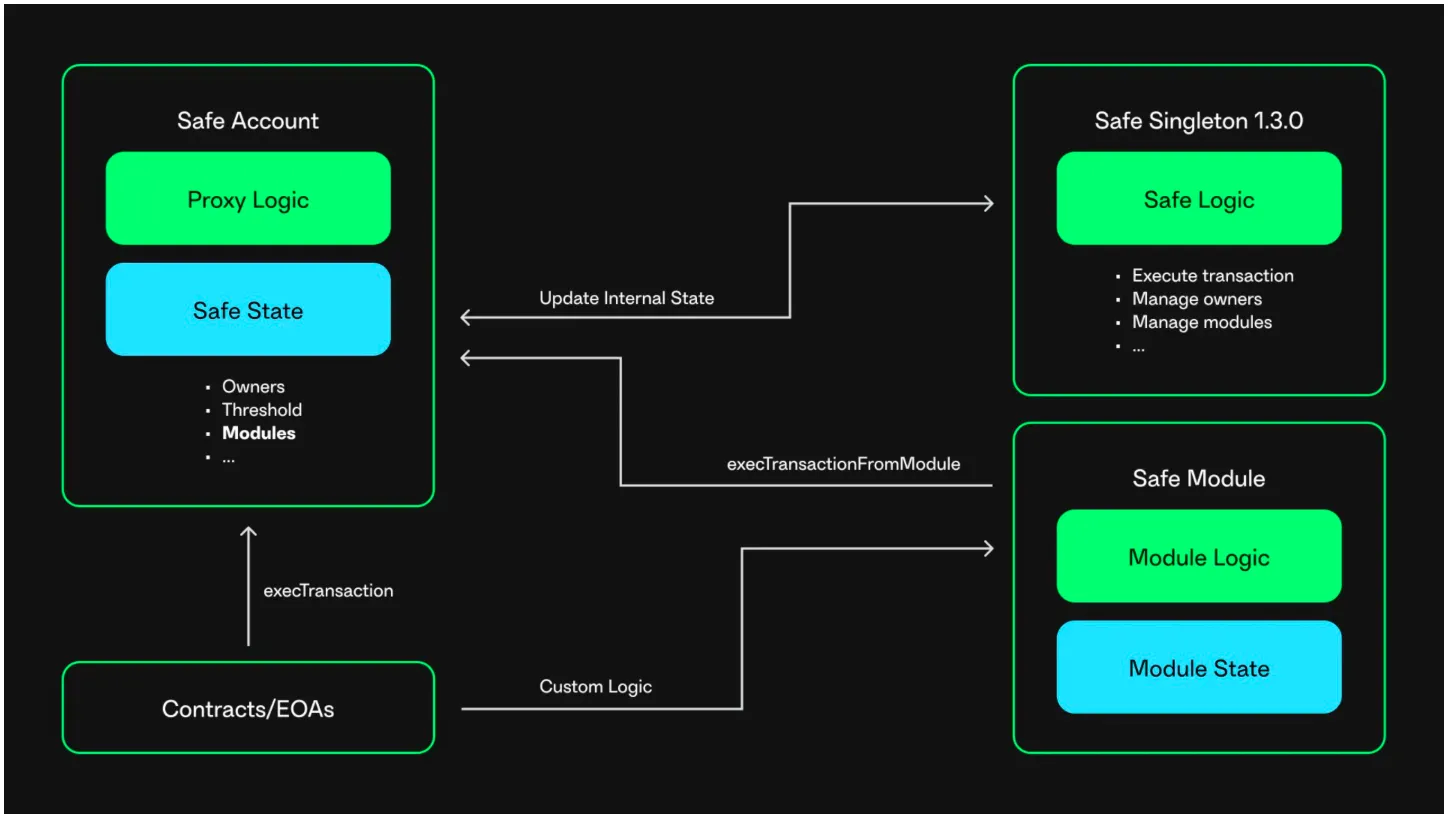

The Safe{Core} architecture consists of several independent components, centered around a manager that coordinates between accounts, registries, and modules. The Manager implements an abstraction layer to handle smart account modularity, allowing users to extend their account functionality by activating registries and their registered modules.

Within the Safe Core Protocol, accounts are user-owned smart accounts that participate in the protocol by activating the manager. Importantly, the protocol remains implementation-agnostic - any account supporting the manager's defined interfaces can utilize the protocol.

Modules serve to extend account functionality in various ways. For instance, plugins can add custom logic like recovery mechanisms, session keys, or automation features, while hooks enable additional logic execution at specific points in a transaction's lifecycle. (A more detailed explanation of Safe's modular structure follows in the next section)

Source: Safe{Core}

The technology stack of Safe{Core} is delivered through two main components: SDKs and APIs. The SDK provides a comprehensive library for smart account interactions, managing everything from new account deployment to transaction processing and account configuration. When implementing multisig functionality, for example, developers can utilize high-level interfaces provided by the SDK instead of writing low-level logic for signature collection and execution validation. The SDK's modular design allows developers to selectively use only the features they need, helping optimize application performance and security by minimizing unnecessary code and dependencies.

The Safe API provides endpoints for smart account interaction. Features like transaction indexing, offchain signature exchange, and event services can be costly or complex to implement directly onchain. Safe API provides the infrastructure to handle these operations efficiently. For multisig transactions specifically, the API can manage the entire process from collecting and verifying multiple signatures to executing the final transaction when conditions are met. The API currently offers four specialized packages with different levels of abstraction and functionality, ranging from Starter Kit to Protocol Kit and Relay Kit.

2.2.2 Safe{Wallet}

Source: Playing It Safe With a Safe Multisig

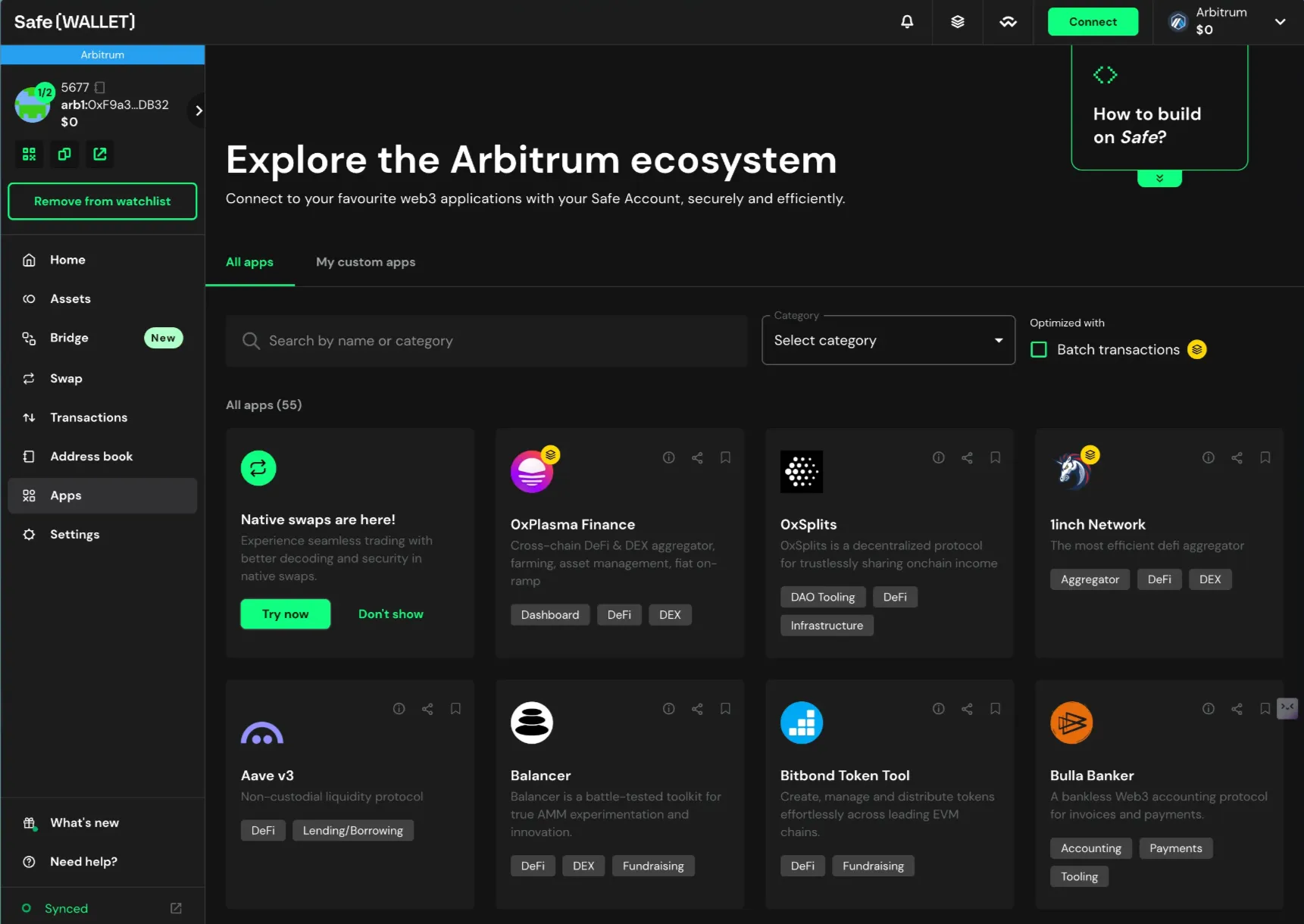

Safe{Wallet} represents one of Safe's flagship products, built on the foundation of the Safe{Core} protocol. The product initially found its market fit through its multi-signature functionality and has since grown to become the primary treasury management tool. However, Safe{Wallet} has evolved beyond being just a tool for businesses and DAOs – it's now positioned as a gateway for all users to access the benefits of smart accounts.

Safe{Wallet} continues to introduce innovative features to enhance security and user experience. For example, through counterfactual deployment of accounts, users can defer gas costs until they actually need to execute transactions. The platform also includes transaction simulation and risk assessment capabilities, allowing users to identify potential risks before executing transactions. Additionally, social recovery features provide users with secure access to their assets even in emergency situations like private key loss.

Source: Safe{Wallet}

A particularly noteworthy aspect is Safe{Wallet}'s integration with the DeFi ecosystem through its app store. The wallet's app store currently hosts over 200 applications, enabling users to directly access various services including DeFi protocols, NFT platforms, bridges, and governance tools through the wallet interface. This demonstrates how wallets can evolve beyond simple asset storage to become comprehensive entry points for Web3 services.

Safe{Wallet} combines battle-tested smart contracts with broad interoperability across protocols and applications, making it a cornerstone of the Safe ecosystem. Looking ahead, Safe{Wallet} is expected to maintain its position as one of crypto's most trusted solutions while continuing to innovate, creating an environment where users can manage their digital assets more safely and conveniently.

2.2.3 Modular Smart Account

One of Safe's core objectives is modularity and extensibility. These features are essential for fully realizing the potential of smart accounts and account abstraction. Safe's architecture allows for significant expansion of account functionality through the integration of complementary smart contracts.

Just as app stores revolutionized mobile devices by enabling unlimited functional expansion, Safe's modular accounts are opening new possibilities in Web3. Through its registry system, Safe ensures all modules meet specific security standards, creates a global marketplace for developers to offer specialized modules, and enables new revenue models through in-module payment systems.

The biggest challenge in implementing modular smart accounts is managing the risks associated with complex smart contract configurations. Safe addresses this through the principle of 'Separation of Concerns,' implemented through three types of plugins:

Source: Safe Smart Accounts & Diamond Proxies

The biggest challenge in implementing modular smart accounts is managing the risks associated with complex smart contract configurations. Safe addresses this through the principle of 'Separation of Concerns,' implemented through three types of plugins:

First, Modules are whitelisted addresses that can execute transactions on behalf of the Safe smart account. For example, the Allowance Module enables specific accounts to spend funds within preset limits without requiring additional user confirmation. Modules operate independently from the core contract and can only interact through defined methods like specific functions.

Source: Safe Smart Accounts & Diamond Proxies

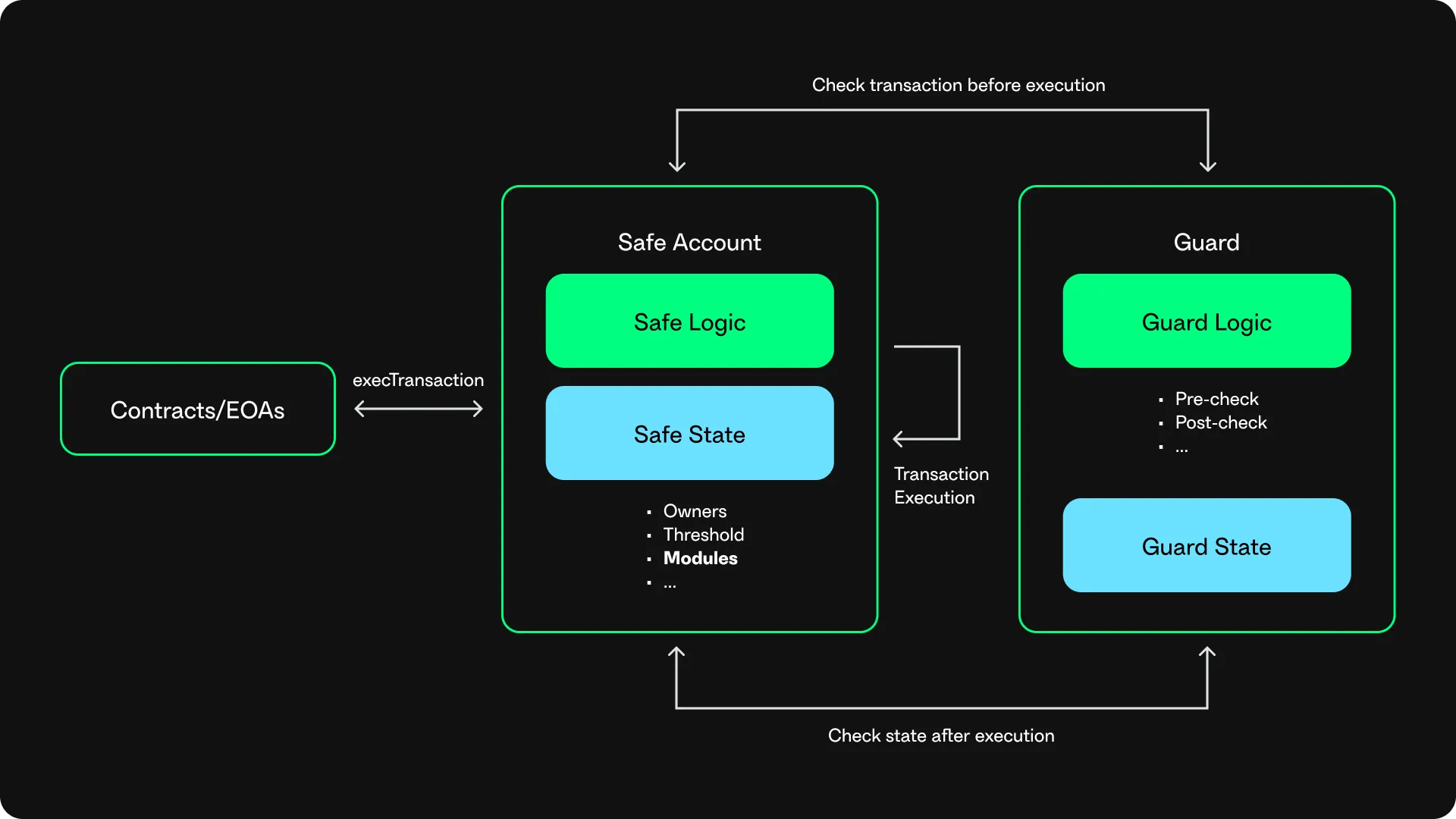

Second, Guards act as hook mechanisms that perform additional security checks on transactions. Before execution, Guards examine all transaction parameters and only allow execution if there are no issues. After completion, Guards are called again to verify the transaction's outcome. This enables features like restricting interactions with specific contracts or monitoring account state changes.

Source: Safe Smart Accounts & Diamond Proxies

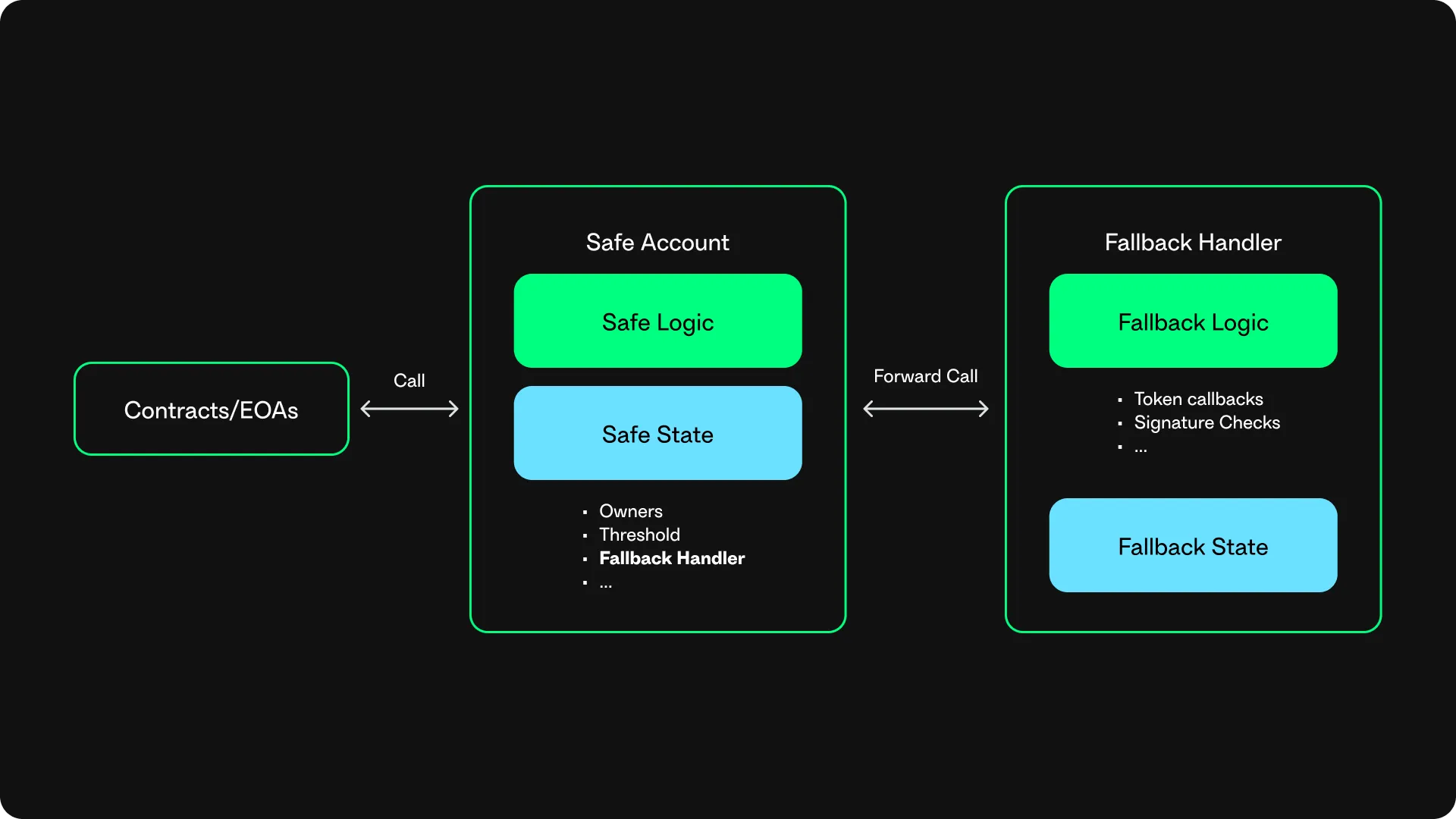

Finally, Fallback Handlers process incoming calls and implement callbacks for new standards or asset types. Common examples include contract signatures through EIP-1271 and support for various token standards like ERC-721, ERC-1155, and ERC-777.

Each of these three plugin types operates independently and maintains its own storage. Interactions occur only through predefined interfaces, enabling robust security guidelines and automated testing.

Blockchain has the potential to become a global settlement layer that transforms how society coordinates, trades, and brings the world closer together. To achieve this vision, the ultimate goal would be to bring the world's economic activities onchain. However, several fundamental challenges in the current crypto ecosystem need to be addressed first.

First, the rapid proliferation of L1/L2 solutions has paradoxically led to increased ecosystem fragmentation. Not only are chains isolated from each other with their own ecosystems, but they also lack sufficient integration with existing offchain financial networks. Cross-chain transactions through bridges involve significant time delays, limiting critical use cases like real-time payments. Additionally, complex technical requirements and security vulnerabilities create barriers to entry for mainstream users.

Source: Visa

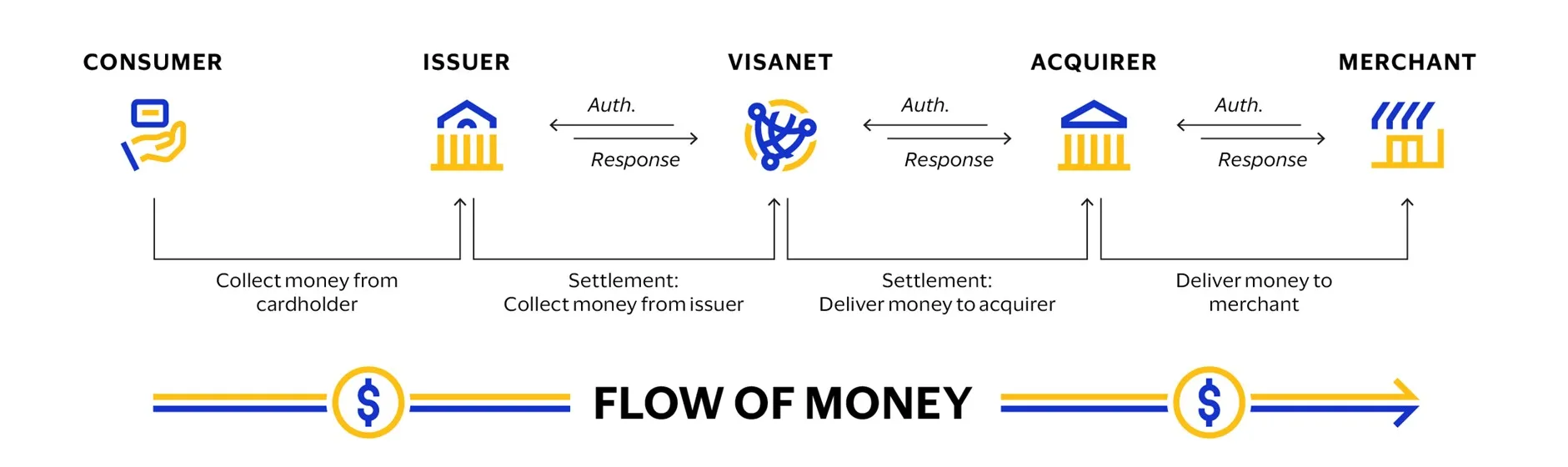

In simple terms, Safenet aims to become the onchain equivalent of the Visa network by separating execution and settlement on blockchain. When you pay with a card, VisaNet verifies the buyer's balance, reserves the necessary funds, and issues a payment execution guarantee to the merchant's bank. The actual fund transfer occurs 2-3 days later as part of settlement. Visa's key innovation lies in this separation of transaction execution guarantee and settlement. Safenet is introducing this proven model to the crypto ecosystem, aiming to bring the convenience and speed of centralized financial systems to blockchain.

Safenet presents an innovative approach to addressing the structural problems of fragmented onchain ecosystems. Rather than adding another blockchain or Layer 2, Safenet has built an optimistic validity proof transaction processing network based on the Ethereum mainnet. This network is compatible with all existing chains and can even connect to offchain systems like the Visa network and centralized exchanges, setting it apart from existing solutions.

Safenet's most notable innovation is the separation of transaction execution and settlement. While traditional crypto transactions required simultaneous execution and settlement, Safenet achieves dramatic performance improvements by separating these processes. This approach offers three key benefits:

Speed: Safenet guarantees execution speeds within 500ms, even for cross-chain transactions. This is hundreds of times faster than existing bridges and cross-chain solutions.

Security: Through optimistic validity proofs, all transactions are guaranteed to comply with predefined security policies. Users are protected from common risks like address spoofing and malicious contracts, and can even apply their own custom security policies.

Scalability: The system enables unified asset management across Ethereum, its Layer 2 networks, and non-EVM compatible chains like Solana. Furthermore, users can freely utilize onchain assets through offchain channels like physical card payments and centralized exchanges.

Source: Safenet Docs

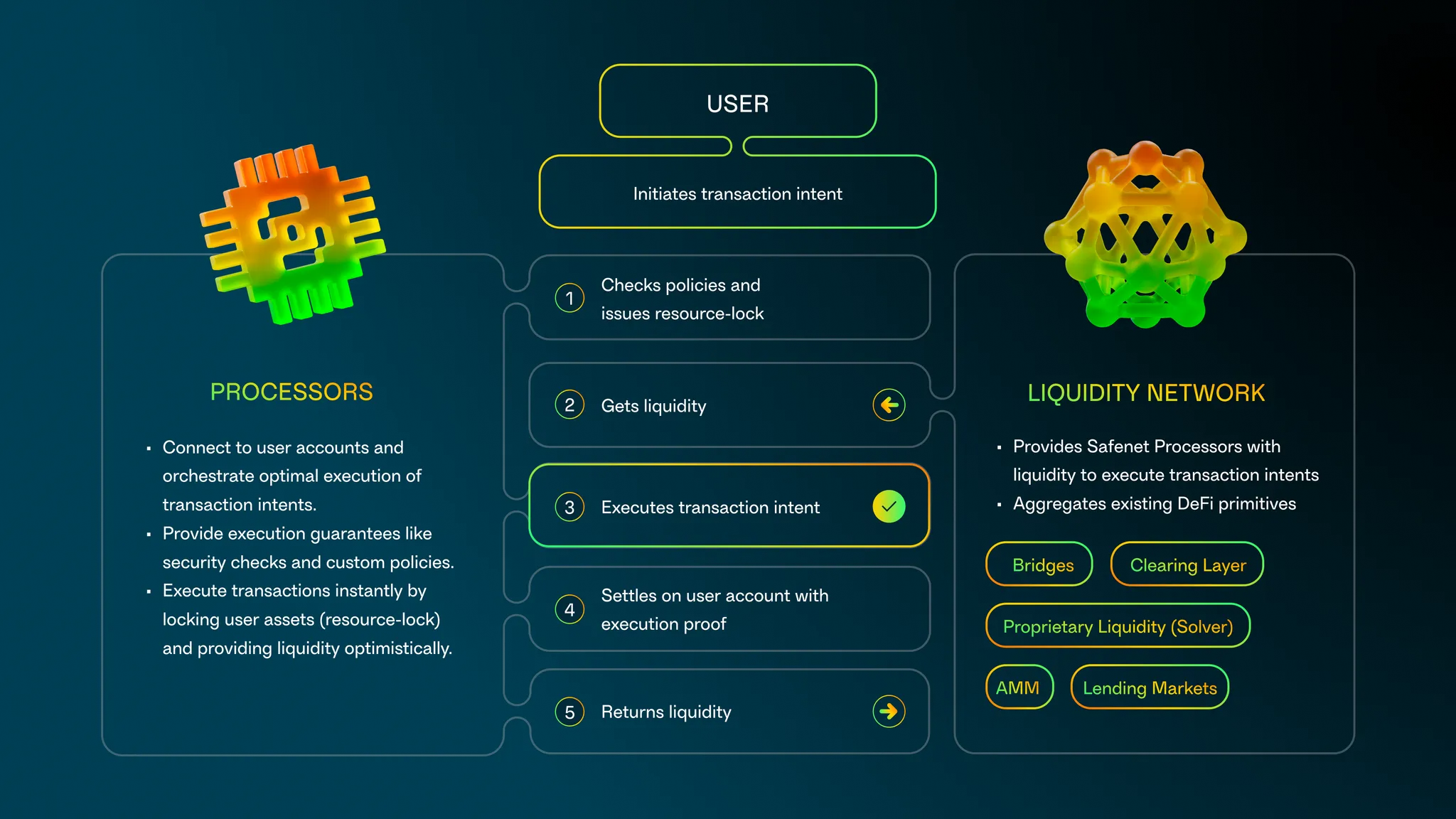

As explained earlier, Safenet's biggest innovation is separating transaction execution from settlement. The network consisting of processors, validators, and liquidity providers simplifies complex cross-chain interactions by taking responsibility for security and cross-chain bridging. This enables users to instantly use assets on any supported chain without traditional bridging. Behind the scenes, Safenet handles settlement by coordinating funds across various blockchains where users hold assets.

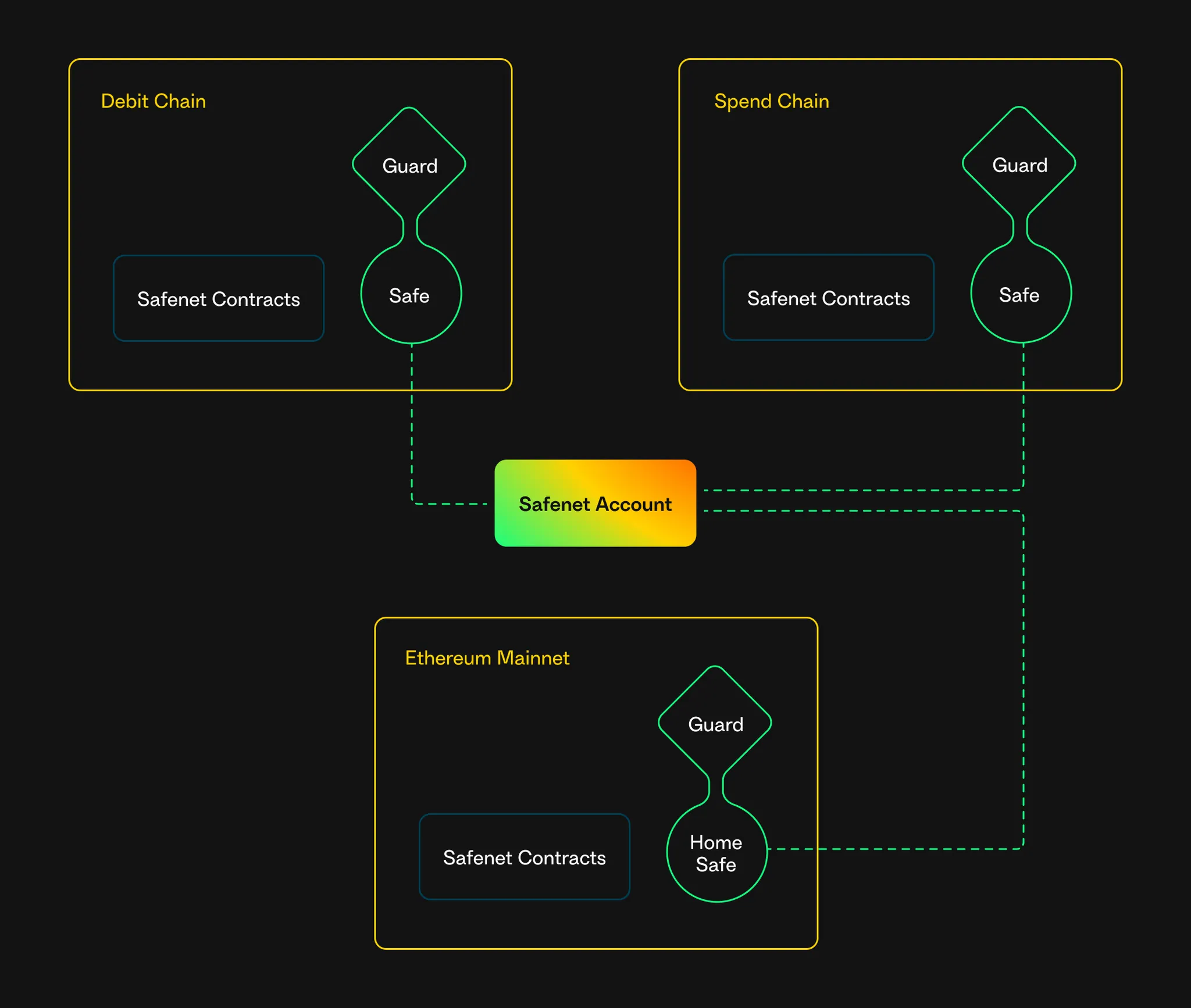

To separate transaction execution from settlement in a multi-chain environment, it's essential to clearly define the role of each chain. Safenet distinguishes between three types of chains:

Spend Chain: This is the chain where users actually execute transactions. For quick transaction processing, necessary funds must be readily available on this chain. Safenet ensures this through its processors and liquidity providers. Sometimes referred to as the 'target chain.'

Debit Chain: This is the chain where users hold the assets needed for execution. Since users' assets may be distributed across multiple chains, Safenet automatically identifies required funds across all connected chains and establishes optimized settlement routes. This means users don't need to manually specify debit chains. Also known as the 'source chain.'

Home Chain: This refers to the Ethereum mainnet, which serves as the trust foundation for the entire system. Safenet's security policies and user account configurations are recorded here, and it serves as the final arbitration standard in case of disputes. Ethereum mainnet's high security and decentralization level ensures the stability of the entire system.

For example, if a user wants to execute a transaction on Optimism but has the necessary funds on Base, Optimism becomes the spend chain and Base becomes the debit chain. If executing a transaction on the same chain where funds are held, the spend chain and debit chain are identical.

Source: Introducing Safenet

Safenet's architecture is operated by three key offchain participants. Each participant has specific responsibilities and works in close coordination to settle user payment requests:

First, Safe Smart Accounts implement a distributed account system across multiple blockchains. Each chain has a deployed smart account, and all accounts are connected to the home Safe smart account on Ethereum mainnet. This allows users to manage assets distributed across multiple chains while taking advantage of each chain's unique features and capabilities.

Second, Safenet smart contracts are deployed on all supported chains to handle actual transaction processing. These contracts are centered around Ethereum mainnet and coordinate cross-chain interactions while validating transaction validity.

Finally, the most crucial element in Safenet's mechanism is its decentralized offchain participants. They each have clear roles and responsibilities, with economic incentives ensuring stable system operation. The three offchain participants operating Safenet are:

Processors serve as Safenet's execution nodes, functioning similarly to sequencers in Ethereum Layer 2s. They verify user account assets, issue resource locks, and handle immediate transaction processing using external liquidity.

Validators monitor and verify processors' work. They can challenge settlement requests if they detect fraud or errors, requiring processors to prove transaction validity. This checks and balances mechanism enhances system stability and reliability.

Liquidity Providers are crucial participants enabling immediate execution of cross-chain transactions. They pre-fund necessary assets for a premium and receive repayment with additional fees during settlement. This structure enables cross-chain transactions without bridging delays.

Safenet is in active development, waiting to being applied to real-world problems. Starting with an alpha version featuring cross-chain account creation in Q1 2025, they plan to integrate Safe App SDK and decentralize the validator network in Q2. The second half of 2025 will focus on expanding the liquidity network and introducing third-party processors, aiming for broader ecosystem expansion.

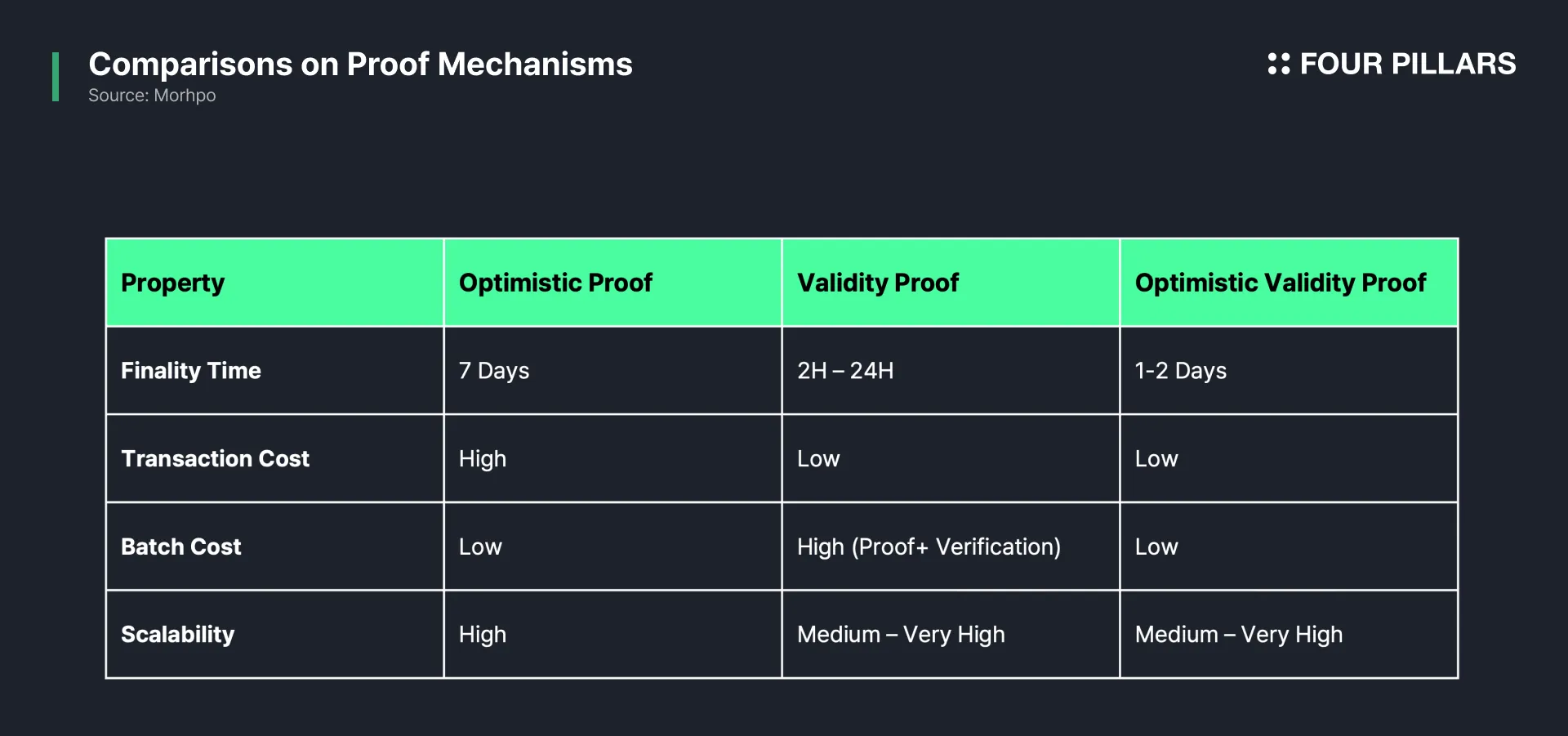

Safenet adopted optimistic validity proofs as its rollup proof mechanism to achieve both efficiency and security. This validation method combines the advantages of both optimistic rollups and ZK rollups. While traditional optimistic rollups using fraud proofs require multiple rounds of interaction and long challenge periods due to complex implementation, optimistic validity proofs adopt an approach where sequencers directly generate and verify ZK proofs. This significantly reduces challenge periods, enables transaction data compression, and simplifies validator roles. Additionally, this design makes it easier to transition to a full ZK rollup if needed.

This mechanism operates similarly to slashing in proof-of-stake networks, using participants' economic interests to ensure system security. Processors risk losing their stake or pre-funded assets if they process invalid transactions, while validators forfeit their collateral if they challenge valid transactions.

The impact of this mechanism on transaction speed and gas fees can be categorized into three phases:

Execution: During transaction execution, processing is always fast and gas-efficient. Neither processors nor liquidity providers have any incentive to provide users with funds they can't recover, and processors act cautiously to avoid losing their stake.

Settlement: During settlement, gas efficiency is maintained though speed is somewhat slower. This delay is necessary to allow validators time to challenge settlement requests. However, it remains gas-efficient since processors don't need to submit validity proofs upfront.

Challenge: Only challenged settlements incur high gas fees and slower processing times. When a validator challenges a settlement request, processors must submit proofs that need to be transferred from the spend chain to the debit chain through cross-chain bridges. This process inevitably involves higher costs and time.

Processors are motivated to process transactions correctly since they risk losing funds for incorrect processing. Their stake serves as collateral protecting liquidity providers' funds. Validators can earn fees by identifying and challenging incorrect transactions but lose funds if they challenge valid transactions, encouraging careful behavior.

The optimistic validity proof system thus enables fast and efficient processing in most cases while maintaining safety mechanisms for the resolution. It represents a balanced combination of achieving centralized system efficiency with decentralized system security.

The crypto ecosystem has undergone significant changes in recent years and is now entering a new phase. As blockchain's underlying infrastructure layer matures, user experience and accessibility have emerged as key priorities. In particular, there's a growing need for a new layer that can unify fragmented user experiences in a multi-chain environment and abstract away crypto's technical complexities.

In this context, Safe appears to be at the forefront of driving change. Over the past seven years, Safe has built a solid foundation by establishing itself as Ethereum's most trusted multi-sig wallet. Building on this foundation, Safe has introduced a new paradigm for smart accounts through account abstraction and modular architecture. More recently, it's opening new possibilities for cross-chain payments through Safenet.

Safenet presents an ambitious vision of becoming an integrated payment layer bridging both onchain and offchain systems. By separating transaction execution from settlement and building a network of decentralized participants, Safenet is creating a new paradigm that combines the efficiency of traditional financial systems with blockchain's trustlessness and transparency. This goes beyond simply improving connectivity within the crypto ecosystem – it demonstrates the potential for blockchain to evolve into a new foundational layer for global finance.

Dive into 'Narratives' that will be important in the next year