Current DA layers (Celestia, Avail, EigenDA) will divide the market in different directions long-term, similar to the Three Kingdoms of ancient China, with each focusing on different strengths.

All three DA layers are currently competing to improve throughput in the short term, and the outcome of this performance battle will likely determine which project dominates the DA market in the long run.

In this article, we discuss how the three major data availability layers are evolving differently despite their technical similarities.

Celestia, Avail, and EigenDA share many aspects in the business domain. Starting with Celestia, followed by Avail and EigenDA, they emerged during a similar period, and their current target markets are nearly identical. Moreover, shortly after the emergence of the DA sector, Ethereum's Dencun upgrade introduced blobspace, a very inexpensive data space, which somewhat diminished the thesis of DA.

Currently, Celestia, Avail, and EigenDA appear to be sharing the market in various overlapping areas, which has led to many technical comparisons on which one to choose.

https://blog.availproject.org/a-guide-to-selecting-the-right-data-availability-layer/

https://sunriselayer.medium.com/data-availability-layers-a-comparison-5188da1a97b8

While many researchers have well explained the technical status quo of these projects, these three projects will take different directions in the long term. As a result, each is expected to find a solution that matches its characteristics, and each DA will divide their territories like Wei, Shu, and Wu in the Three Kingdoms.

In this article, let's explore what goals these three DA layers have been developing towards and how they are taking different directions going forward.

Source: https://x.com/portport255/status/1900681749375373773

There might have been too many explanations about data availability itself, which could seem repetitive to readers who already understand the concept. However, as Porter from zkSync mentioned in the tweet above, there are likely many readers who haven't yet grasped the concept of data availability. Since it's essential for understanding this article, I'll try to explain it as simply as possible.

Data availability is proving that certain data exists in a network. Why is this necessary?

In the consensus process of blockchains, a leader typically propagates a new block to peers, and peers need to verify whether the block delivered by the leader is the same as what was actually submitted to the network. Without separate verification, consensus could proceed with malicious transactions hidden by the leader.

The same applies to L2s, where visibility of data is ensured by the sequencer propagating data to full nodes. In this case, a process is needed to verify that the block received matches the block actually submitted to the network.

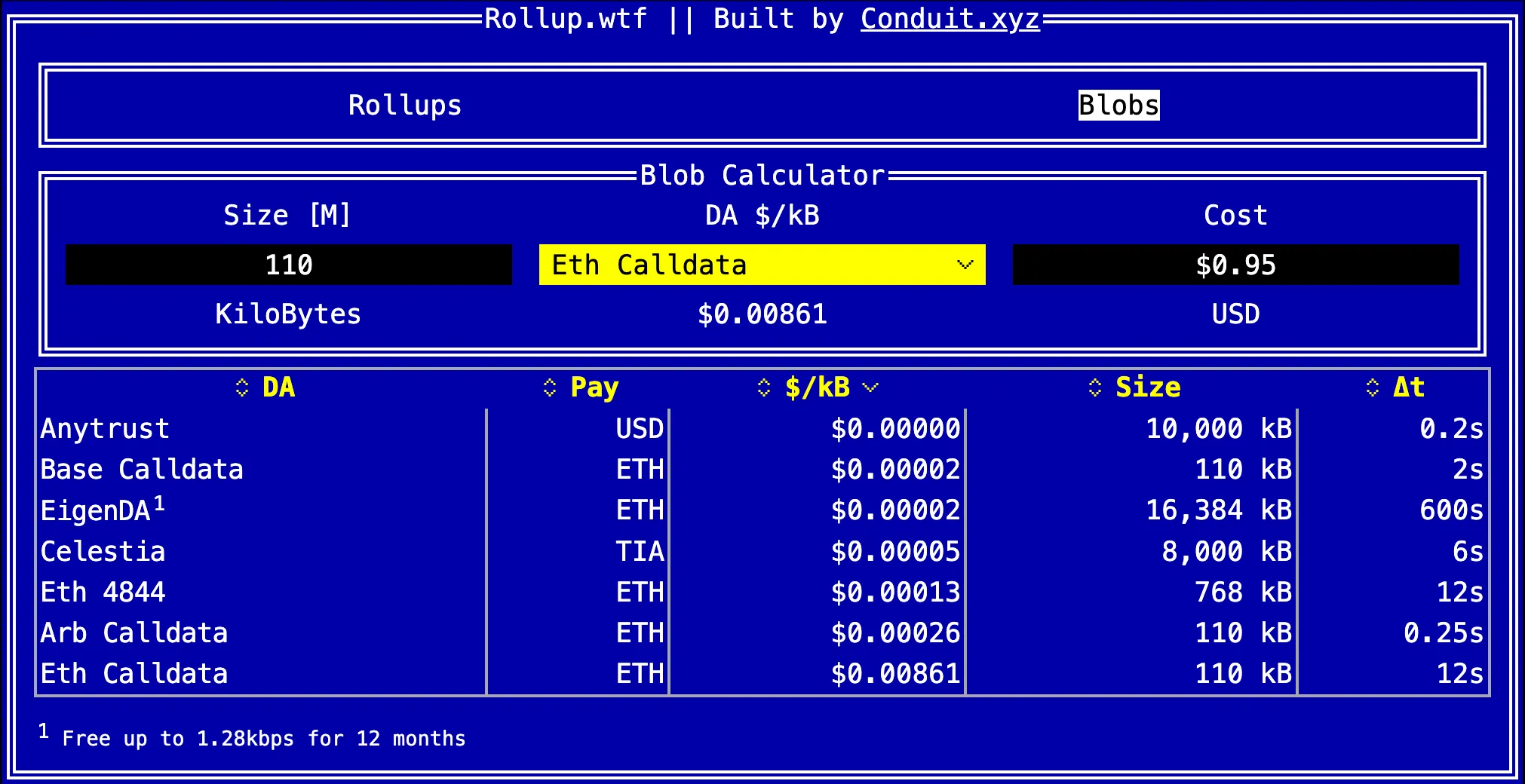

Source: rollup.wtf

The easiest way to verify this is to directly look up the chain's state. However, as shown in the figure above, submitting data to networks like Ethereum is highly inefficient in terms of cost and speed. The DA layer emerged from the idea of making this more efficient.

What do projects considering DA protocols look for?

First is security. Since a DA layer adds another Trust Anchor, if the DA layer arbitrarily delays or fails to provide verification, Optimium without a separate data availability mechanism could experience Data Unavailability problems. To address this, DA layers go through separate consensus processes or introduce sampling technology called DAS, allowing users to verify integrity through light clients.

Additionally, DA must provide sufficient performance. With the addition of blobspace in Ethereum through the Dencun upgrade, Ethereum's own DA efficiency has significantly improved. Therefore, to provide merit to projects that want to use it, DA must offer much better performance than Ethereum in terms of cost and throughput.

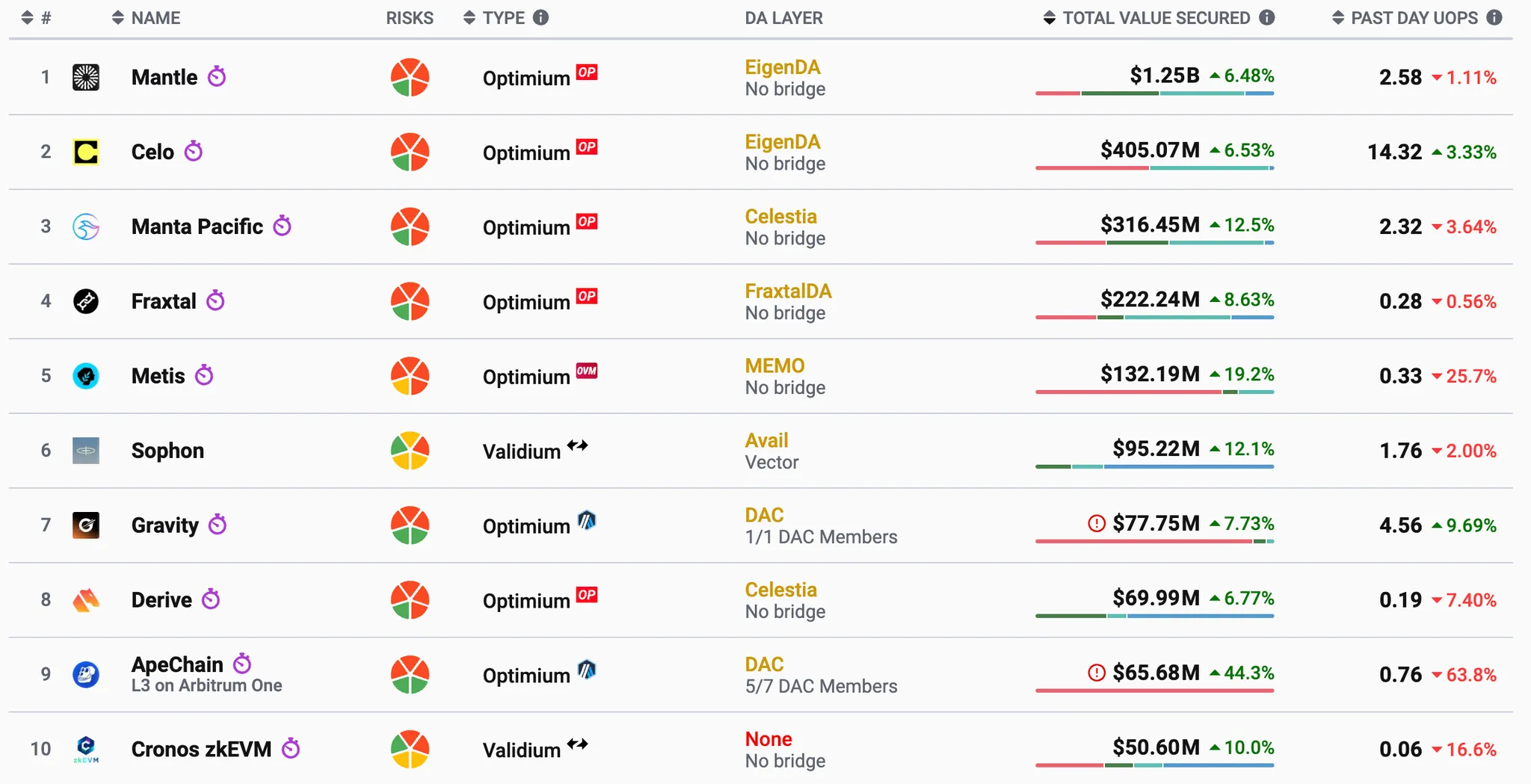

The prominent ones are Ethereum, Celestia, Avail, and EigenDA. Not all chains need to use external DA; according to L2BEAT, more than half of Optimium/Validium use their own DA based on multisig called DAC (Data availability committee). In such cases, data availability can be considered quite centralized.

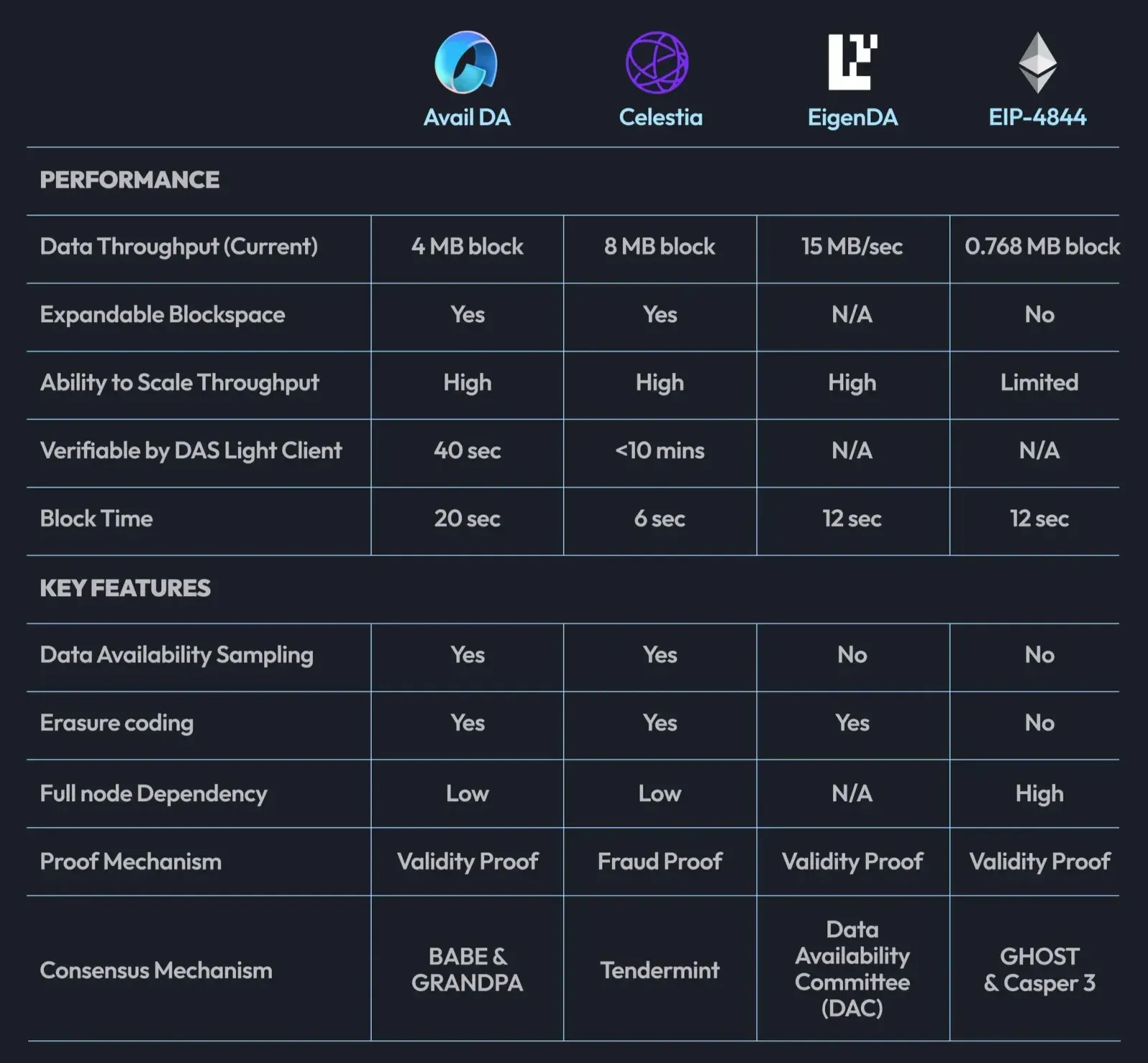

Source: Avail Blog

Here’s a comparison from Avail's "A Guide to Selecting the Right Data Availability Layer." A simple comparison of Avail/Celestia/EigenDA is as follows:

EigenDA: Has the highest throughput. However, it has been criticized for the critical drawback that economic security has not been operating so far. Very recently, it began providing economic security through a slashing update. Additionally, it offers a lower level of security compared to other consensus-based DA protocols by choosing a DAC structure rather than a separate network.

Avail: Has the slowest block time at 20 seconds, but its finalization is quite fast at 40 seconds. In addition to supporting about 1,000 validators, it supports client verification through DAS. Given that the network itself supports validity proof, Avail has the most secure feature in overall so far.

Celestia: Provides a short block time of 6 seconds and high throughput. It guarantees single-slot finality, making compatibility between rollups using Celestia very good, but there's a drawback that it takes about 10 minutes of challenges to guarantee finality for rollups that don't. It currently supports about 100 validators, one-tenth of Avail's number.

In conclusion, EigenDA offers very high throughput, Avail provides a higher level of decentralization compared to other DAs, and Celestia offers high scalability for rollups within its ecosystem as differentiators from Ethereum.

Since the DA market is expected be divided into sectors in the future, so observing onboarded projects is more appropriate for understanding the current state of the DA market than looking at token prices.

Source: EigenDA Website

What stands out most when looking at EigenDA's ecosystem partners is that it has been chosen by most RaaS (Rollup-as-a-Service) projects such as AltLayer, Caldera, Conduit, and Gelato. This shows that projects that outsource rollup operations may have deliberately chosen a DA that is cheap for data submission and doesn't require separate light client operation, as they have largely given up on decentralization.

Besides these, hyper-performant chains like Fluent, SOON, and MegaETH are notable. For hyper-performant chains, the amount of data that needs to be submitted in real-time is overwhelmingly larger than other chains, and since they want to extract maximum efficiency performance-wise, it makes sense that they have chosen EigenDA, which currently has the best throughput. According to L2BEAT, Mantle and Celo, which have the highest TVL among Validium/Optimium, are using EigenDA, and these two alone account for about 40% of the total TVL (about $3.06B). Considering the launch of promising chains like SOON and MegaETH, this proportion could increase even more.

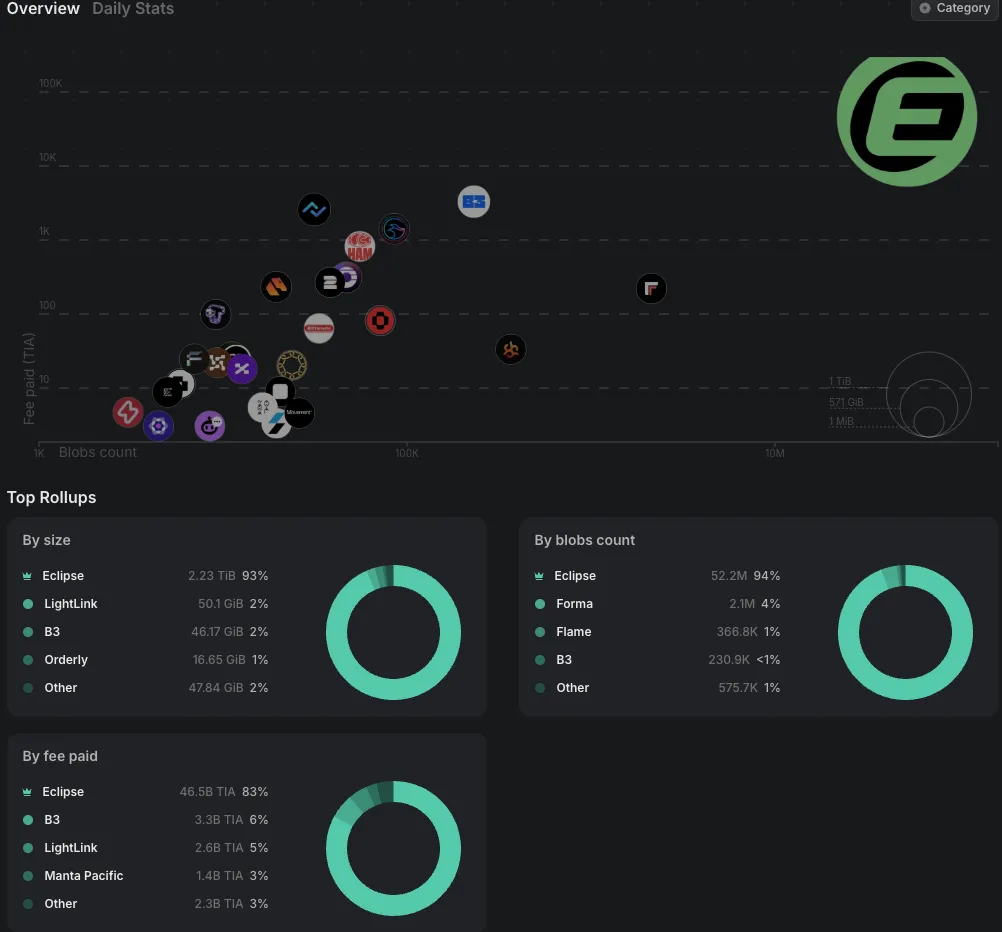

Source: celenium.io

Eclipse currently accounts for more than 90% of Celestia's data usage. This is likely because Eclipse, which is aiming to achieve hyper-performance through GigaCompute, not only has a larger size of data to upload compared to other chains, but also has very high on-chain activity ahead of its TGE.

However, checking celenium.io/rollup, we can see that the Celestia ecosystem has onboarded various rollups. Except for the general L2 Manta, almost all of them appear to be purpose-specific rollups (or appchains). This seems to be due to the trust assumption about finality mentioned earlier, as rollups within the Celestia ecosystem can overcome the relatively long 10-minute DA finality requirement time at the SSF level compared to Avail. For this reason, it seems to have some merit in the appchain ecosystem by achieving both decentralization and performance. This also implies why the Initia ecosystem chose to use Celestia.

Source: X (@celestia)

Source: Avail Blog

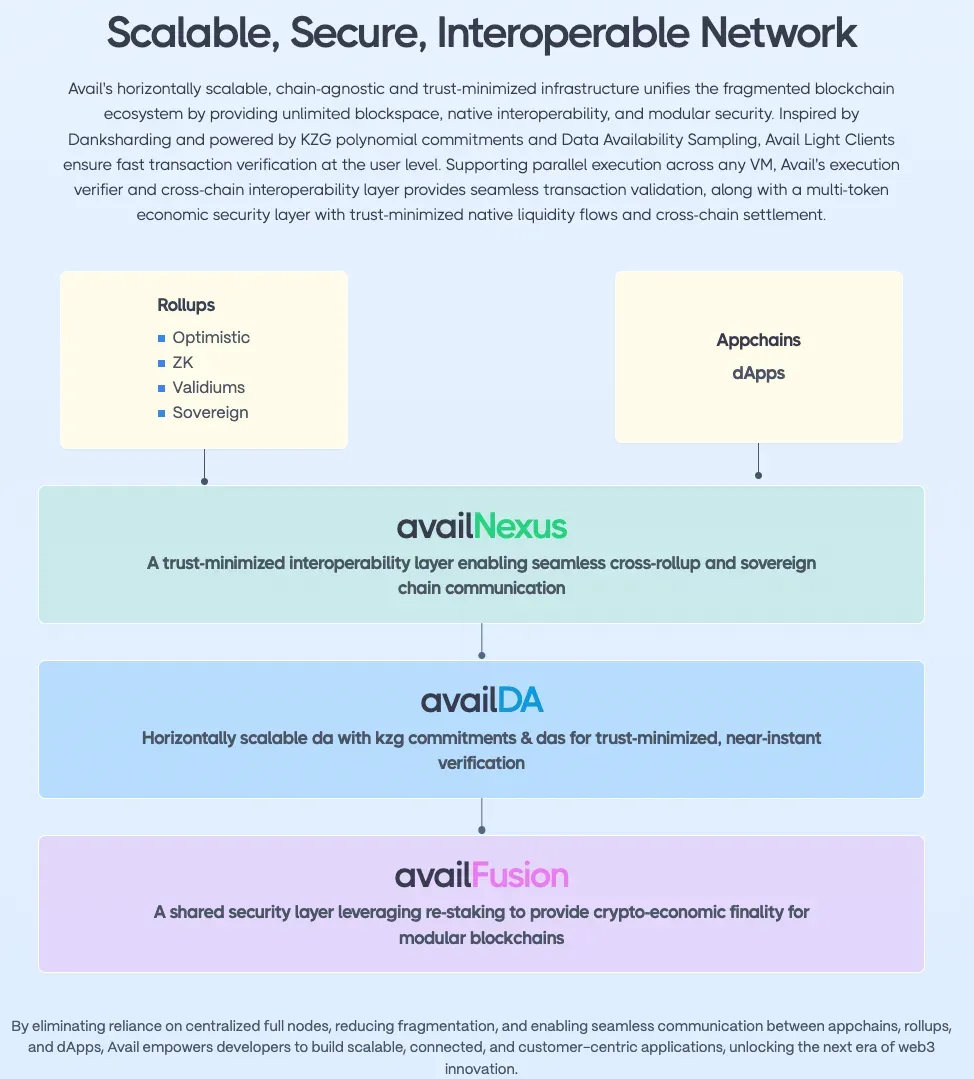

Avail operates various stacks including Nexus, an Interoperability stack, and Fusion, which supports Multi-asset consensus, in addition to DA, so it has many partner projects. Looking only at DA partners:

Appchain: Fuse, Ternoa, Arcana, OpenLayer, Darwinia, Neova, Stackr

Bitcoin Ecosystem: Yala, Zulu, BVM, (Starkware)

Ethereum L2: Sophon, Lens

Restaking: Symbiotic

Like Celestia, Avail also has appchains as its main ecosystem partners rather than High performance L2s. However, what's unique is that Avail is trying to create various synergies with ecosystem projects by utilizing its own stacks, Fusion and Nexus, along with DA. Fusion and Nexus are relatively less known compared to AvailDA. Nexus is an interoperability layer that integrates and verifies the states of all chains onboarded to the ecosystem through ZK proof aggregation, and Fusion is a security layer that provides Economic security by supporting staking of ETH/BTC/SOL and all ERC20 tokens. Both are layers focused on compatibility and unity among ecosystem projects, suggesting an intention to make onboarded projects dependent on Avail.

It appears that Avail has quickly captured the Bitcoin L2 ecosystem, thanks to its ability to provide Multi-asset consensus including BTC and its structurally highest level of security. Recently, it also introduced a Restaking-based framework through collaboration with Symbiotic, using Avail DA + Fusion. From this, we can glimpse that Avail's ultimate direction is quite different from other DAs.

Source: EigenLayer X

EigenLayer conducted a slashing update on April 18, addressing the chronic criticism of the absence of economic security. It is expected that many new projects that have been hesitant to adopt EigenDA due to the absence of slashing will now onboard.

EigenDA has been criticized for the absence of DAS and delays in introducing slashing, and in response, the team has promised to achieve decentralization in the long term. However, the upcoming upgrades in the short term clearly show EigenDA's direction, which is explicitly represented by the upcoming Blazar (EigenDA V2) upgrade.

Blazar Upgrade

There isn't much publicly available information about the Blazar upgrade beyond what's in the Docs, but EigenDA aims to improve Latency and Throughput in V2, even changing the project's fundamental structure.

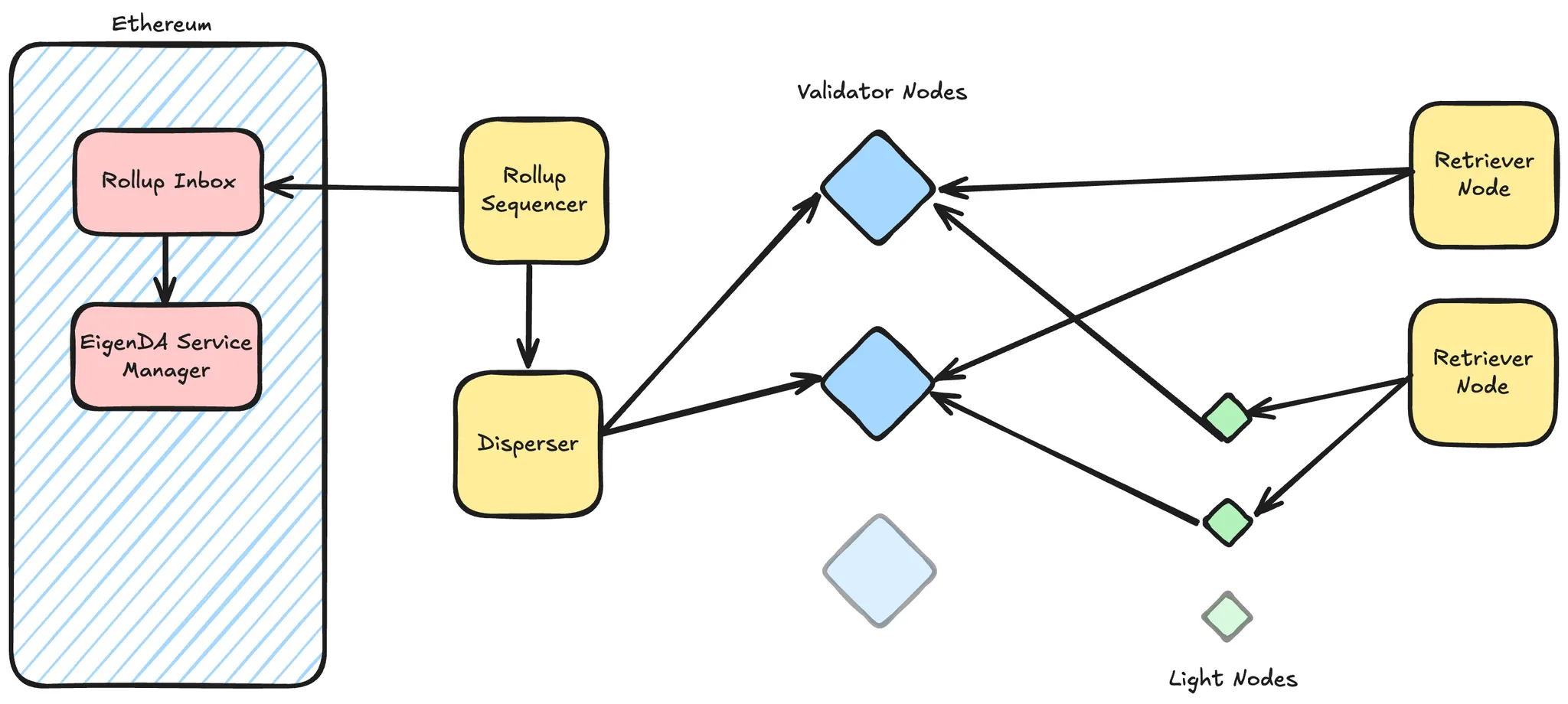

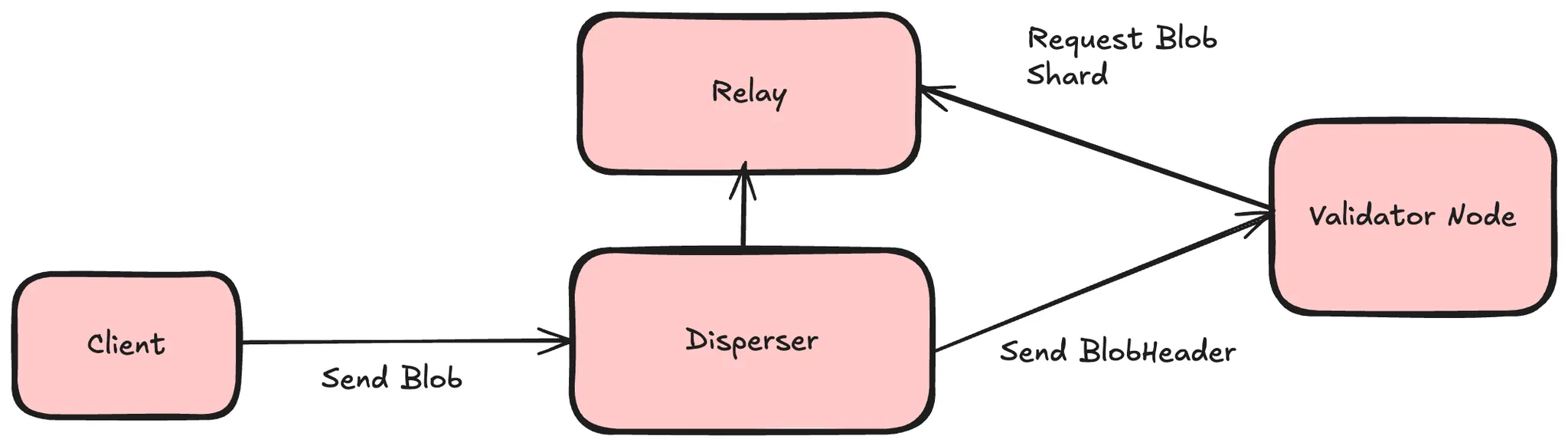

Source: EigenDA Docs

Source: EigenDA Docs

The figures above represent the structures of EigenDA V1 and V2 respectively.

The main update in EigenDA V2 is the addition of a new component called Relay. Relay is dedicated to storing blob chunks or distributing them at high speed, aiming to significantly improve data transmission speed and download performance of DA nodes.

In V1, a component called Disperser sent blob headers and data chunks together to DA nodes, creating a heavy network load. In V2, the transmission of blob headers and data chunks is separated, adopting a structure where DA nodes observe blob headers and selectively request data. This not only increases data transmission efficiency but is also expected to minimize DDoS risk by reducing data transmission load.

Additionally, by removing Batch bridging and internalizing blob confirmation in rollup logic, it aims to reduce rollup confirmation delay from minutes to seconds.

While numerous updates will be introduced through V2, what can be clearly understood from the Blazar upgrade is that EigenDA's mid-term roadmap is focused on improving data transmission speed. Even though it already provides an impressive throughput of 15MB/sec, it appears to intend to dominate the market in terms of performance through even more improved performance.

Source: Celestia Blog

Celestia's roadmap, as disclosed in the September 2024 blog update, is shown in the figure above.

Celestia's goals can be simply expressed as follows:

Scaling block size to GB levels to support all chains

Optimizing light node performance to enable DA verification on all devices

As can be seen from the roadmap, Celestia is conducting several development tracks in parallel. Their direction is not focused on any one area, but aims to expand in all directions: Throughput, Verifiability, and Interoperability. This may slow down the completion of the roadmap, but it suggests the ambitious long-term goal of building a "complete DA" to onboard all chains.

Celestia shares its project progress relatively transparently, conducting Live dev calls every two weeks and regularly updating development progress on GitHub. Through this, we can indirectly confirm Celestia's development roadmap and priorities.

So far, the mainnet has undergone two upgrades, Lemongrass and Ginger. The Lemongrass upgrade included updates to improve compatibility within the IBC ecosystem, such as Interchain Account and Packet Forward Module, while the Ginger upgrade focused on scalability, reducing block Finality to 6 seconds and doubling throughput. They recently finalized the third network upgrade, Lotus, which is an update related to token inflation and staking rewards, not a major technical upgrade.

A notable point is the Mamo-1 testnet launched on 4/14, which aims for a radical performance improvement by increasing block size to 128MB, enhancing throughput to 21.33MB/s, more than 16 times the existing level. This is made possible by Vacuum!, a new data transmission protocol that reduces the amount of data propagation by transmitting data on-demand during the consensus process. Celestia has hinted at a major update on 5/16 through a tweet, and it's possible that they will announce the mainnet introduction of Mamo-1 at that time.

Source: Celestia X

As such, Celestia has consistently shared its development status, making it easy to confirm that they are conducting upgrades in various aspects in parallel. However, with the recent emergence of numerous Hyper-performant L2s, it seems they are setting a short-term development direction aimed at radical performance improvement, as DA Throughput has become more important.

Source: https://www.availproject.org/

The image above is a diagram displayed on Avail's main page, which shows Avail's philosophy. Avail treats Security with higher importance compared to other DAs and, as mentioned in the previous section, aims for chains onboarded to the ecosystem to interact with high compatibility in a single stack through not only DA but also Nexus and Fusion.

However, in the short term, it seems they are prioritizing Throughput improvement to secure competitiveness with other DAs. Scalability-related roadmap updates were made in March and April consecutively this year. Let's briefly look at them.

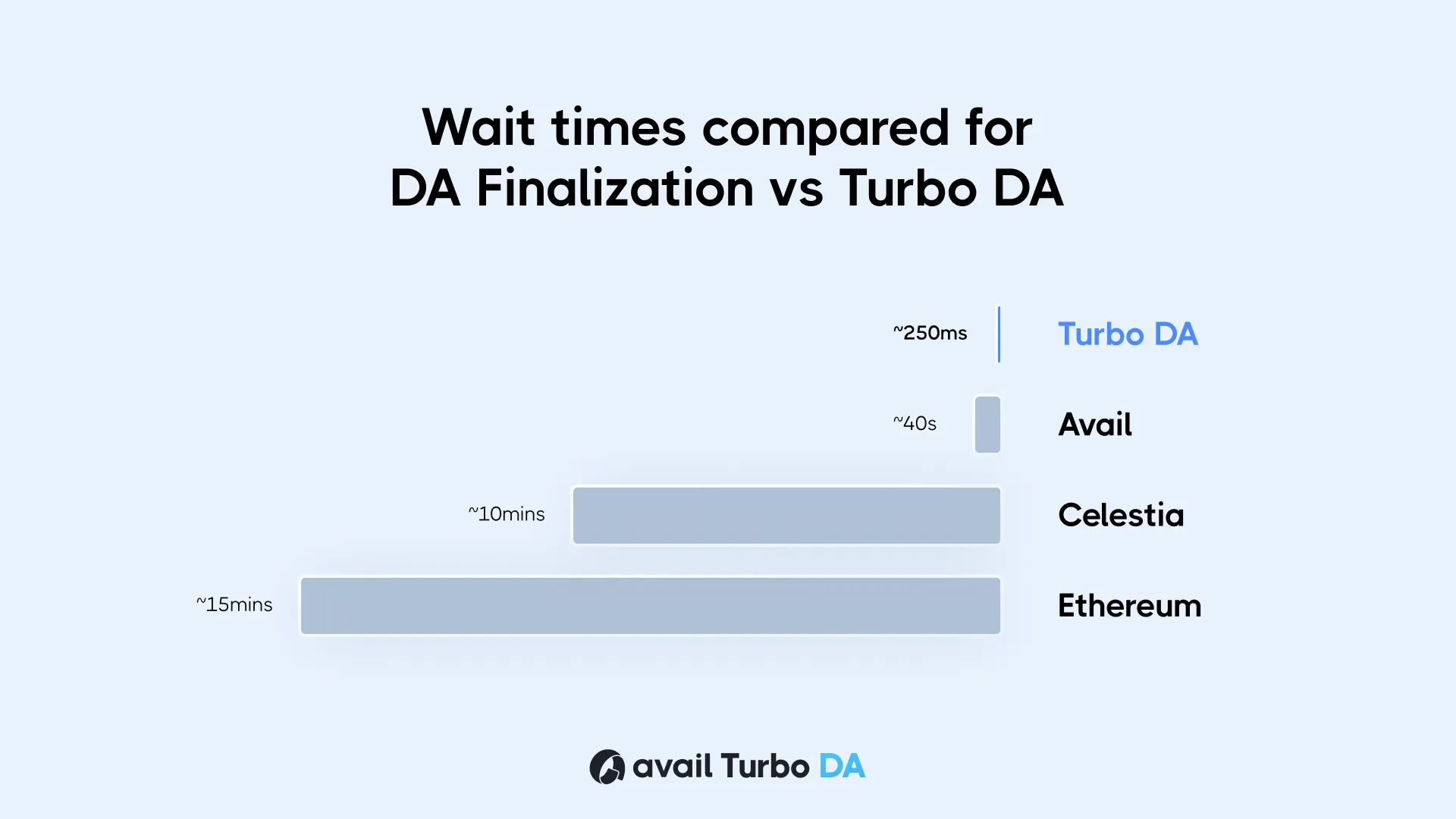

The first is TurboDA, disclosed in March, a protocol that drastically reduces DA Finalization to a level of 250ms. TurboDA is closer to layering than a direct upgrade to AvailDA. When data is submitted to TurboDA, it provides Preconfirmation for DA as existing rollups did, and then is finalized in AvailDA after 2 blocks. While this method may not be considered completely secure, it seems intended to provide interoperability at a similar speed as Celestia provides SSF-level interoperability among rollups within its ecosystem. (Note: Technical details of TurboDA could not be found.)

Source: Avail X

The second is the block size upgrade to 10GB level, disclosed in April. Avail aims to increase block size to a 10GB level, like Celestia, to maximize interoperability among rollups within the ecosystem, and to reduce block time from the current 20 seconds to 600ms.

Source: Avail Blog

To achieve this, AvailDA proposes to 1) optimize by shortening the process of generating data and commitments, 2) selectively perform block data transmission according to headers, and 3) separate from the DA verification process by verifying transactions unrelated to DA separately through ZK. This is fundamentally similar to the direction suggested by other DAs, which seems to be an unavoidable direction if one wants to extremely increase block size.

This might give an impression that Avail's direction has changed, as it’s known for prioritizing security and interoperability, continuously suggesting performance-related updates recently. However, the performance upgrade ultimately stems from the purpose of improving interoperability among rollups onboarded to the ecosystem, so it is interpreted that the fundamental direction has not changed.

The current main competitors in the DA sector, such as EigenDA, Celestia, and Avail, are pioneering the DA domain with clear goals. In the short term, all three DAs are expected to reach a satisfactory level in terms of performance and security through high throughput based on large blocks and DAS.

The DA market is also expected to expand rapidly. Hyper-performant L2s like MegaETH and Eclipse have started to emerge one by one, and the amount of data they need to process is overwhelmingly large compared to existing rollups. The amount of data these produce requires too high a cost to process through Ethereum blobs, so they have no choice but to use DA protocols with high throughput. New data availability markets are expected to continue to emerge, such as chains that require high data processing/storage volumes like projects that process AI computations at the chain level (e.g., 0G), and chains like Bitcoin L2 where the performance bottleneck of L1 is too large.

However, there are several hurdles that the current DA ecosystem needs to overcome to expand the market, so let's discuss them.

First, the emergence of projects building their own DAs. A representative example is 0G, which is building and using its own DA layer due to the performance limitations of Celestia and EigenDA and the specificity of AI computation. Not only 0G, but also Metis and Fraxtal, which have relatively high TVL, are also building and using their own solutions called MEMO and FraxtalDA respectively. This shows that a self-implemented, controllable DA can be more beneficial for projects in terms of price and compatibility. Also, the majority of current Validium/Optimium manage data through multisig-based off-chain storage (DAC), and the fact that they have not yet onboarded to the DA ecosystem means that they are not being provided with sufficient interoperability incentives or efficiency to attract them.

Source: https://l2beat.com/scaling/data-availability?tab=validiumsAndOptimiums

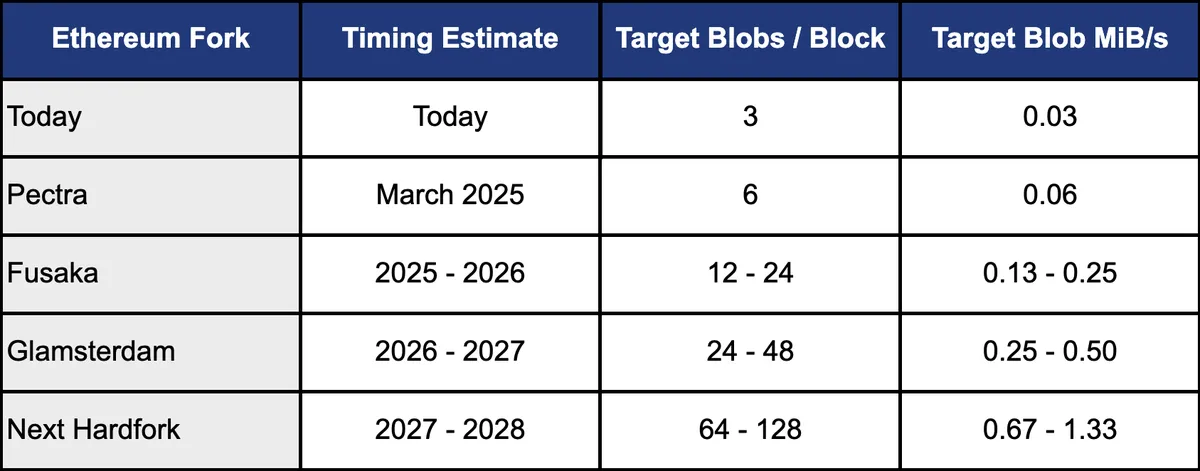

Second is the development of Ethereum DA. Ethereum aims to continuously improve the usability of blobs for network demand and Ethereum alignment of L2s. Pectra Upgrade doubled the number of Blobs, and the subsequent Fusaka Upgrade will increase it by even more. Also, in the long term, it will become closer to the level of performance currently supported by DA protocols through the introduction of Danksharding, DAS, reduction of Finality, and decrease in block time. Therefore, from the perspective of DA protocols, onboarding current Ethereum rollups will become increasingly difficult over time. They will be under pressure to stay ahead of Ethereum DA's development. This would be also why Celestia and Avail are focusing on their own rollup ecosystems, and future DA projects will need to provide not only simple DA throughput and cost benefits but also additional merits such as strong interoperability.

Source: https://x.com/jon_charb/status/1883912628952850935

Source: Rebellion Research

Coming back to the title, the expansion method of each DA layer resembles the Three Kingdoms.

EigenDA is similar to Wei, having dominated the performance-centered market with overwhelming throughput compared to other DAs, along with strong foundations of security through restaking. However, it has always experienced security concerns due to the DAC structure and the absence of Slashing, which has been its biggest challenge in the short term.

Celestia is similar to Wu, approaching appchains (or purpose-based rollups) with fragmented liquidity and interoperability based on rollup interoperability and the convenience of modular structure. Currently, it is emphasizing compatibility for rollups of various computational environments through the onboarding of Initia and Eclipse.

Avail can be compared to Shu, as it has a level of decentralization that can support 1,000 validators, the highest among DA projects, and a philosophy that values ecosystem synergy. What's unique is that it emphasizes building a DA ecosystem based on solid foundations like Nexus and Fusion, and it's capturing markets (like the Southern barbarians) that other DAs haven't pioneered, such as Bitcoin L2.

Thus, the three DAs exhibit different characteristics, but the updates coming in the short term suggest that a major clash could occur between them. This is because EigenDA, Celestia, and Avail are all aiming for improvement in Throughput, specifically a massive improvement based on block sizes at the 10GB level.

Just as the Battle of Red Cliff greatly divided the fate of the Three Kingdoms, the project that will occupy the DA market in the long term will be determined by how the performance battle between DAs proceeds in the short term. In the Three Kingdoms, the strategy of Zhuge Liang, the strategist of Shu, greatly changed the outcome of the war. In the competition of DA, what's noteworthy is who will play that role and what kind of unique points each DA will provide beyond just performance.

Dive into 'Narratives' that will be important in the next year