Huma Finance is a PayFi (Payment Financing) network dedicated to delivering the ultimate on-chain liquidity solution to finance global payments.

Since its launch in 2022, Huma Finance has achieved remarkable milestones, including $2 billion in cumulative transaction volume and $1 billion in loans, all while maintaining operational stability with a default rate of 0%.

Huma recently completed its chain expansion to Solana, a blockchain emerging as a core player in the current crypto market. This expansion is expected to significantly enhance on-chain activity and service engagement. Furthermore, partnerships with global payment networks like Stellar open opportunities to extend its influence into underserved regions.

Finally, Huma’s token launch is anticipated to not only drive protocol growth but also create new use cases across its ecosystem, delivering broader value.

The advent of Bitcoin as a peer-to-peer network enabling asset transfers without intermediaries has ushered in a new era of finance, spurring the rapid development of diverse infrastructures and use cases. Today, the crypto market hosts a wide array of services, with certain sectors—namely stablecoins, Defi, and payments—achieving maturity and establishing a definitive product-market fit.

As of November 2024, the total issuance of stablecoins has surpassed $180 billion, with daily transaction volumes reaching $103 billion, underscoring their significance. The entry of traditional payment giants like PayPal and Stripe into the crypto space further validates the role of stablecoins. Similarly, the crypto lending market, led by platforms such as Aave, Morpho, and Spark, has grown into a multi-billion-dollar annual industry. The tokenization of RWAs, aimed at bringing tangible assets on-chain, has also emerged as a major trend in global finance. For instance, BlackRock’s RWA fund BUIDL recently exceeded $500 million, and JPMorgan, in collaboration with Apollo, has been exploring the industrialization of asset tokenization through Project Guardian.

As the convergence of traditional finance and crypto accelerates, the financial industry is undergoing rapid transformation. At the intersection of these changes, a project has emerged with the ambition to create a next-generation PayFi (Payment Financing) network, potentially more powerful than Visa. Enter Huma Finance.

Huma Finance is a PayFi (Payment Financing) network dedicated to delivering the ultimate on-chain liquidity solution to finance global payments. Since its launch in 2022, the platform has achieved remarkable growth, recording a cumulative transaction volume of $2 billion and a lending volume of $1 billion within just two years. Huma continues to sustain this rapid growth trajectory, bolstered by partnerships with key players such as Circle and its recent expansion to the Solana blockchain.

As of 2022, the global payment market processed 3.4 trillion transactions annually, managing payment volumes amounting to $1.8 quadrillion and generating $2.2 trillion in revenue. Key credit card networks, including Visa, UnionPay, and Mastercard, collectively handled $19.6 trillion in commercial payments, while the cross-border payment market reached a staggering $190 trillion. Globally, one in six households depends on international remittances, highlighting their critical importance for individuals and small businesses.

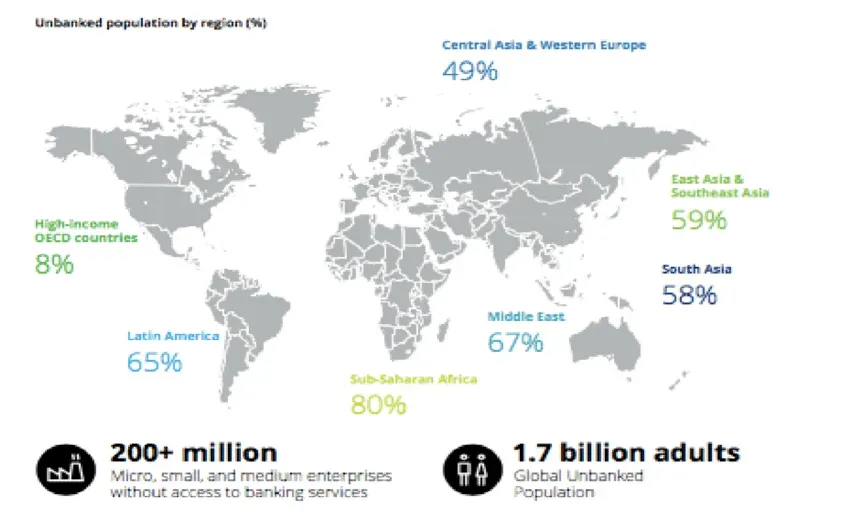

Despite its size, the global payment market is plagued by structural inefficiencies. Cross-border payments, for instance, involve complex processes that require multiple intermediary banks, often resulting in settlement times of 3–5 business days. The average global remittance fee stands at a substantial 6.35%, with higher fees imposed on developing countries and emerging markets, creating significant financial burdens for local businesses and individuals. Additionally, the World Bank reports that 1.7 billion adults worldwide remain unbanked, unable to access financial services. Finally, the reliance on the SWIFT network necessitates pre-funded accounts, tying up approximately $4 trillion in liquidity, exacerbating the problem of capital inefficiency.

Source: Researchgate

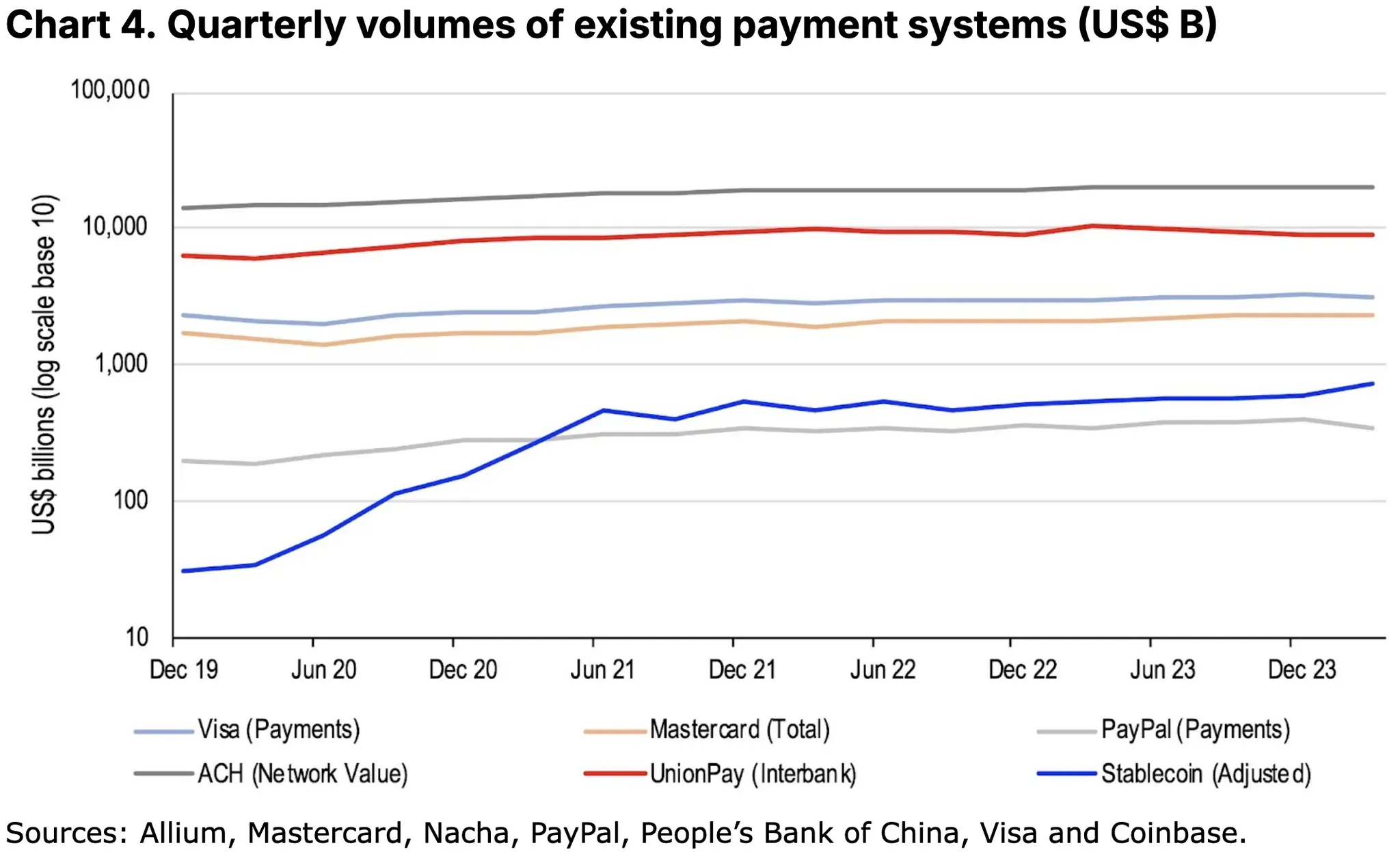

To address these challenges, Huma Finance leverages blockchain as a core technology. Blockchain facilitates fast, low-cost global transactions without the need for intermediary banks. By utilizing low-fee networks, the cost of remittances can be reduced to near zero. This capability is one reason stablecoins have already surpassed traditional payment networks like PayPal and Visa in transaction volumes.

Source: Huma Finance

Huma V1 was designed to connect individuals and businesses with global investors through on-chain financial solutions, incorporating traditional financial models like revolving credit lines and receivables factoring into the blockchain. Its income-based credit evaluation system enhanced risk management capabilities, creating a robust framework for secure lending. This differentiated approach has been met with positive reception, earning accolades at ETHDenver 2023 and cementing Huma’s position as a noteworthy project within the Ethereum developer community.

Huma Finance’s innovative vision has successfully captured the attention of investors. In February 2023, Huma raised $8.3 million in seed funding led by Distributed Global, with participation from Parafi, Folius Ventures, Circle Ventures, Robot Ventures, and Anagram Ventures. Following this, in April of the same year, Huma merged with Arf, a cross-border payment platform, to support the tokenization of real-world assets (RWAs). This partnership enabled USDC-based liquidity solutions without the need for pre-funded accounts. Under this operational structure, Arf manages lending and interest collection while Huma oversees user deposits.

Source: Startupticker.ch

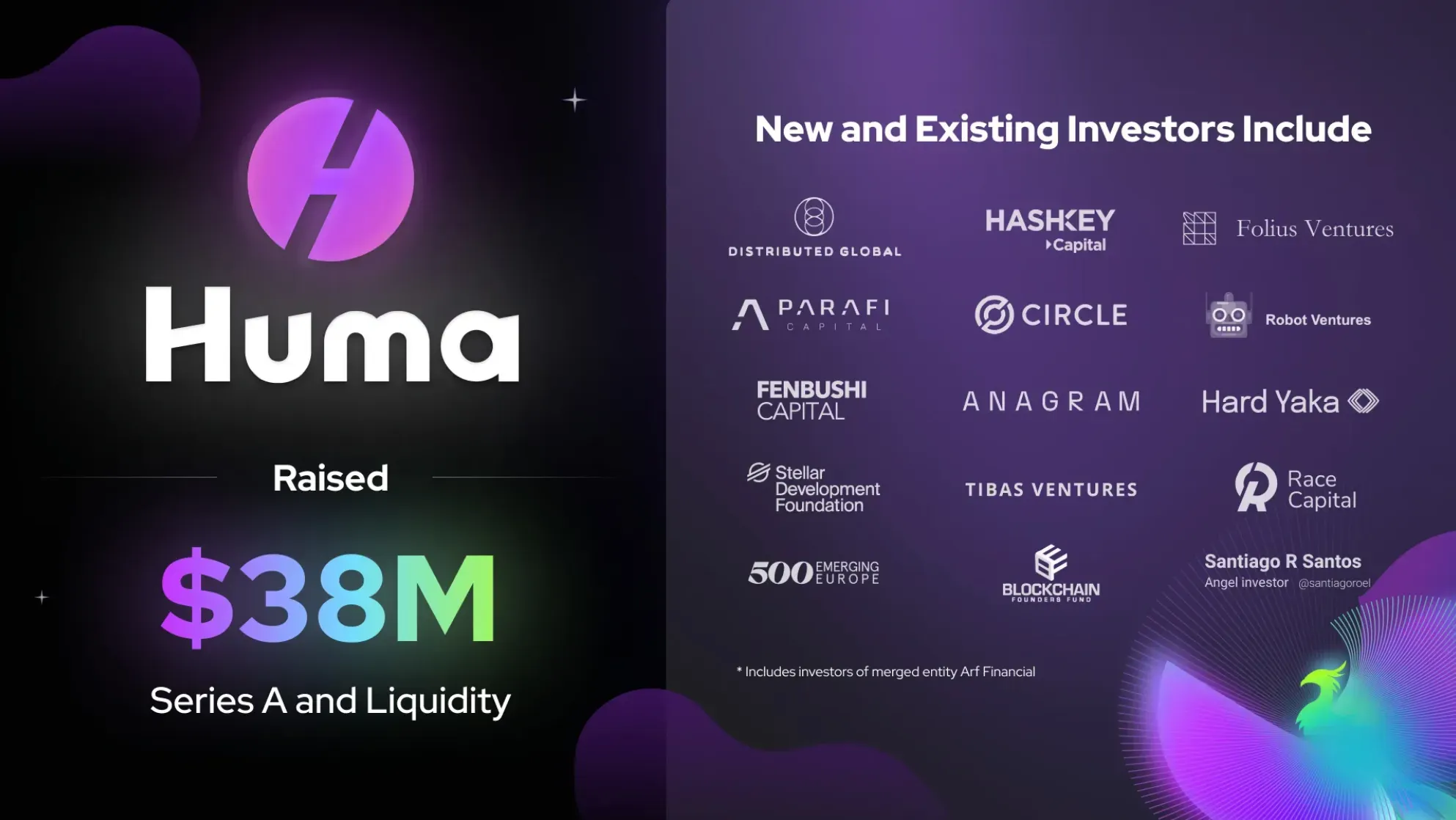

In September 2024, Huma Finance accelerated its growth trajectory by securing $38 million in a funding round once again led by Distributed Global. Of this amount, $10 million was equity funding, while $28 million was structured as RWA-backed loans. Key participants in this round included Hashkey Capital, Folius Ventures, the Stellar Development Foundation, and TIBAS Ventures, the corporate venture capital arm of İşbank, Türkiye’s largest private bank.

These funds enabled Huma Finance to launch Huma V2, signaling a transformative shift from a simple income-based lending protocol to a global PayFi network. This evolution, which will be explored further in Section 3, positions Huma at the forefront of innovation in on-chain financial services.

Source: Huma Finance

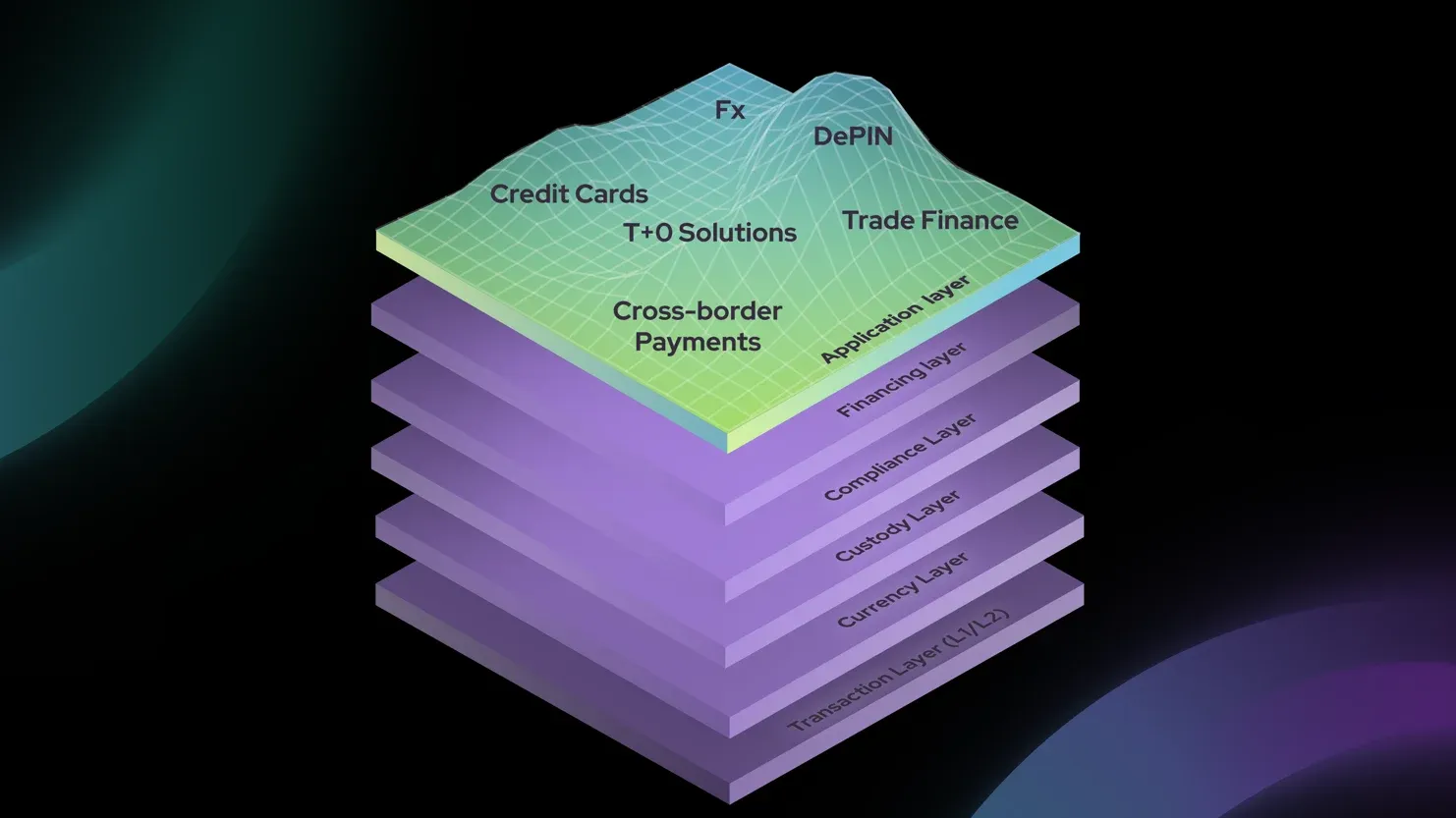

Before analyzing the technical architecture and unique features of Huma Finance, it is essential to first understand the structure of the PayFi stack that underpins the on-chain payment market and the specific role that Huma Finance plays within this ecosystem.

The PayFi stack, a framework proposed by Huma Finance, is composed of six key layers that define the on-chain payment finance ecosystem: Transaction, Currency, Custody, Financing, Compliance, and Application. Each layer forms the foundational structure of the payment ecosystem and continues to evolve in tandem with industry advancements. The roles and features of each layer are as follows.

At its core, the Transaction Layer serves as the backbone, composed of L1 and L2 blockchains designed to support payment systems. Given the demands of the payment industry, this layer prioritizes high throughput and low transaction costs to enable seamless and efficient services. Solana, which Huma recently expanded to, is regarded as an optimal blockchain for this layer due to its fast transaction speeds, low costs, and active ecosystem.

The Currency Layer is home to stablecoins such as USDT, USDC, DAI, and USDe. Among these, USDC and PYUSD stand out for their compliance with regulatory standards and their goal of achieving widespread adoption, making them particularly significant for traditional institutions and everyday payment use cases. National stablecoin initiatives designed to enhance regional liquidity may also fall within this layer.

The Custody Layer includes institutional-grade custody providers such as Fireblocks, Coinbase Custody, Cobo, and Copper, which meet the high-security standards demanded by financial institutions. These solutions incorporate features like MPC (multi-party computation) wallets, multi-party control mechanisms, and security agents to ensure the security and reliability of assets under management.

The Financing layer is the backbone of payment finance, encompassing infrastructure for risk management, credit scoring, underwriting, and oracle services. Huma Finance plays a central role in this layer by providing innovative solutions tailored to the payment financing sector, which will be examined in detail later in this report.

Regulatory compliance is one of the greatest challenges in utilizing stablecoins for real-world payments, particularly regarding AML (Anti-Money Laundering) requirements. The ease with which assets can be transferred between wallets and across chains without authorization complicates the tracking of illicit activity. The Compliance layer includes firms like Chainalysis, Elliptic, and TRMLabs, which specialize in security and compliance.

Finally, the Application Layer encompasses the various platforms that execute payment processes. Examples include Arf, which facilitates cross-border payments; Zeebu, which specializes in telecom roaming payments; Raincard and Reap, which focus on credit card-based payment solutions; BSOS, which addresses supply chain financing; and Zoth, which supports trade finance initiatives. These applications represent the practical deployment of the PayFi stack, demonstrating its real-world utility across diverse industries.

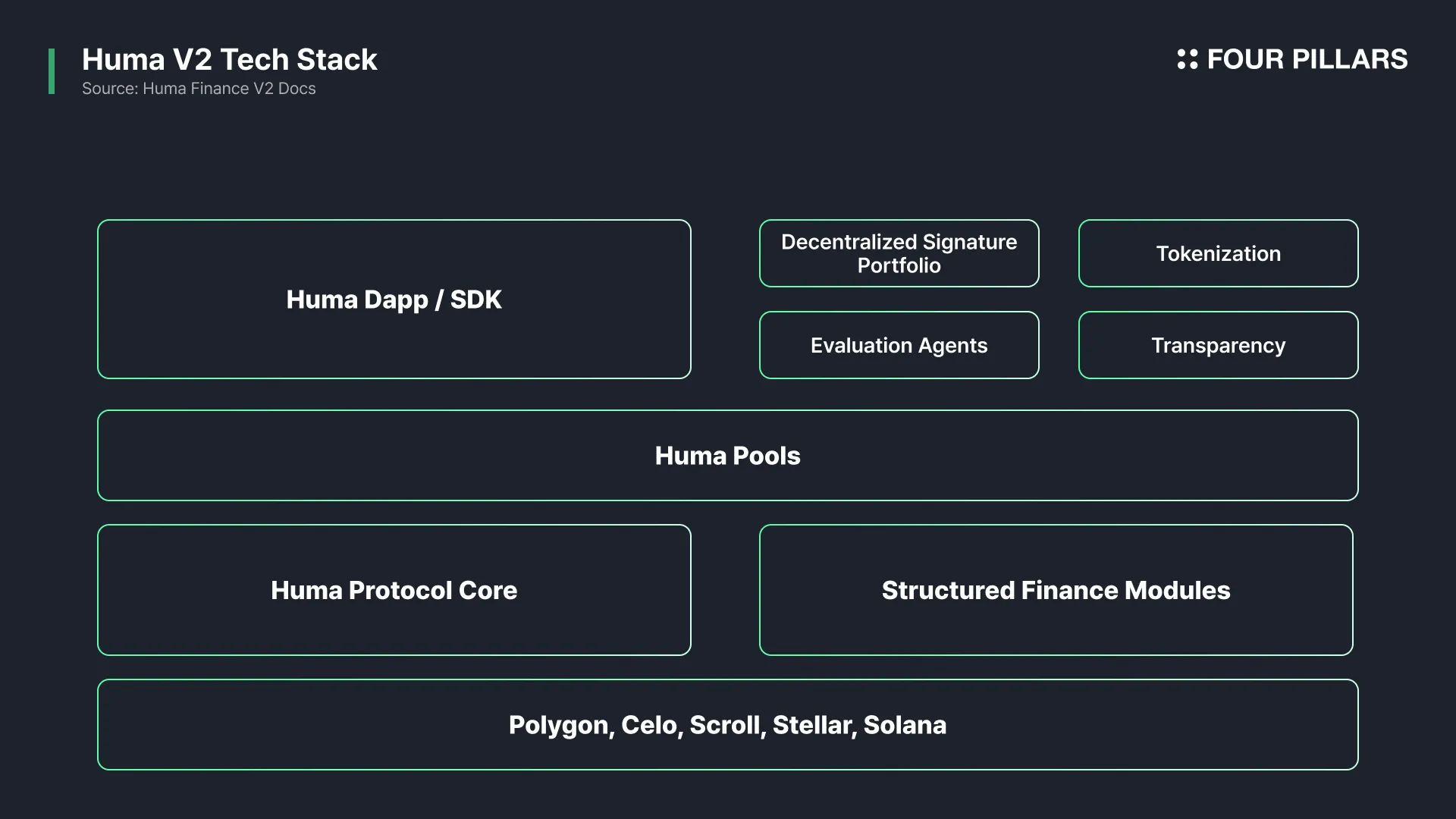

As outlined earlier, the Financing Layer in the PayFi stack encompasses not only payment finance protocols but also critical infrastructure for risk management, credit evaluation, underwriting, and oracle solutions. Huma Finance plays a leading role in this layer, offering institutional-grade, short-term financing solutions tailored for cross-border liquidity needs. Below is an overview of Huma’s technical stack and its structural features.

Huma Finance currently operates across Polygon, Celo, Scroll, Stellar Soroban, and more importantly, Solana, a blockchain known for its high throughput, low transaction fees, and a robust ecosystem. Solana’s optimization for payment finance is further strengthened by Circle’s native USDC and PayPal’s PYUSD support, alongside features like Solana Pay. These factors position Solana as a cornerstone blockchain in the PayFi network, aligning with Huma’s goal of driving the growth of on-chain payment systems.

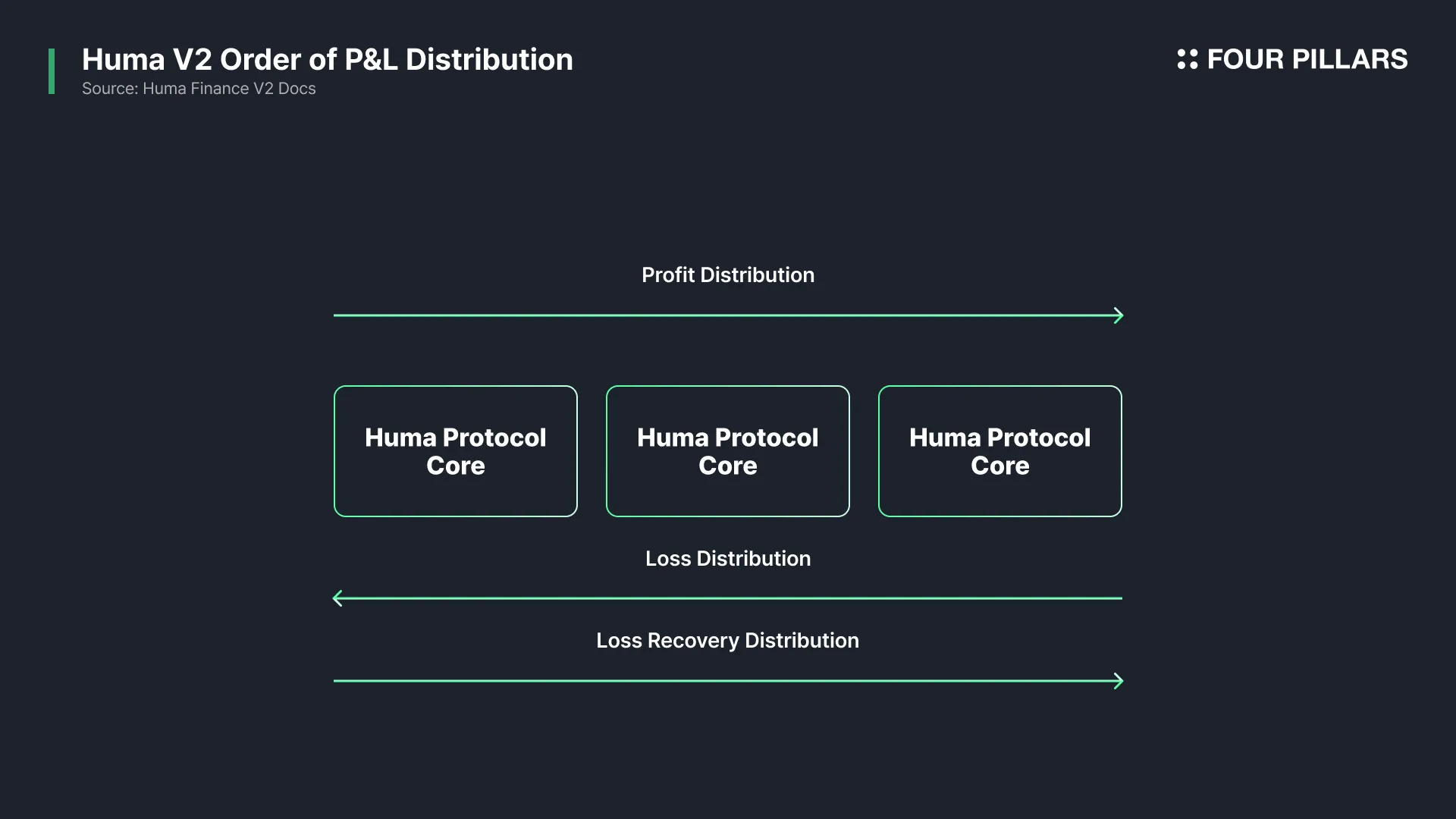

Huma’s Structured Finance Modules are designed to cater to diverse user needs, featuring components such as Tranches, First Loss Coverage, the 30/360 Calendar, and a Yield Manager. Tranches are divided into Senior and Junior levels, allowing investors to choose based on their risk tolerance. Senior tranches provide stable returns with lower risk and are prioritized during repayment in case of defaults. Conversely, junior tranches offer higher yields at greater risk, with repayment ranking below senior tranches.

The First Loss Coverage structure adds another layer of risk management by pooling resources from borrowers, insurers, and investors. Up to 16 layers of first-loss coverage can be implemented within a single pool, offering flexibility and security to all stakeholders. The Yield Manager Module supports a variety of revenue models, including pre-paid or post-paid structures and subscription-based fees, accommodating a wide range of financial products. Additionally, the calendar module supports the standard 30/360 calendar used in traditional finance while also enabling Defi’s flexible, second-level yield calculations.

Huma Pools, one of Huma Finance’s cornerstone modules, was developed during Huma V1 to support diverse financial scenarios such as credit-based loans, invoice-backed loans, and factoring. These smart contract modules incorporate customizable tranche policies, fee management systems, and payout structures, allowing flexibility to meet various use cases. This enables both investors and borrowers to choose financial products and structures best suited to their needs.

Risk management is another key strength of Huma Finance. Evaluation Agents handle critical tasks such as credit scoring, underwriting, and loan lifecycle management. They record approved credit terms on pool contracts, declare defaults, and adjust credit limits or rates as necessary. This system enhances transparency and reliability by leveraging on-chain data, which reassures investors while maintaining operational integrity.

The Tokenization Module allows RWA assets to be tokenized through SPV (Special Purpose Vehicle) structures. For invoice-backed loans and factoring, evaluation agents assess the tokenized invoices to make underwriting decisions. These tokenized invoices can also be represented as NFTs, enabling borrowers to maximize the utility of their assets.

Lastly, the Huma DApp/SDK serves as the primary interface for borrowers and lenders to interact with the Huma protocol. Borrowers can manage loan disbursements and repayments with ease, while lenders can efficiently deposit and withdraw funds. Most enterprise clients are expected to integrate with Huma’s services via the SDK, which will play a pivotal role in expanding the PayFi network and broadening its user base.

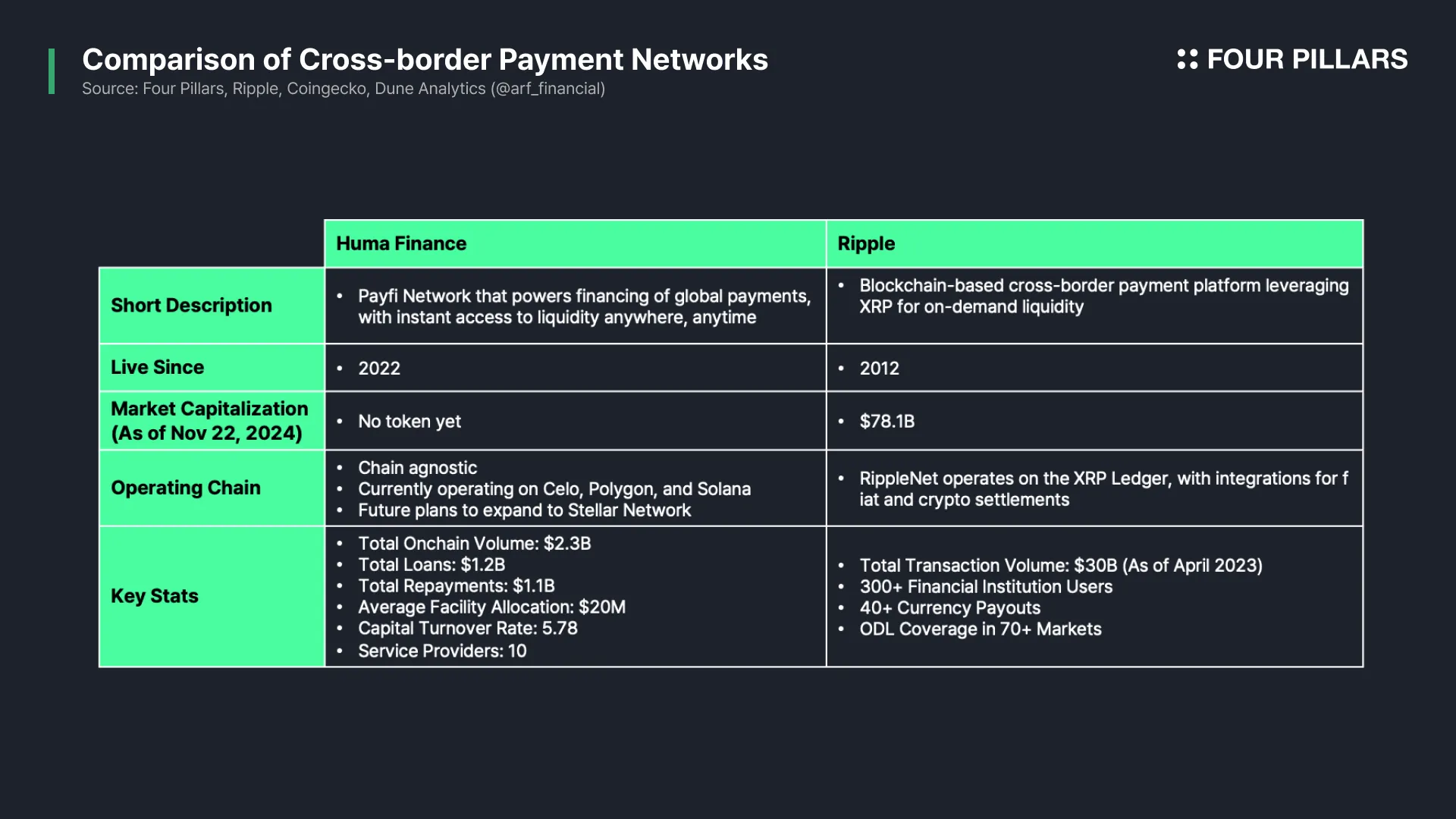

In the competitive Payment Financing (PayFi) sector, Ripple stands out as one of the leading players. Ripple offers real-time cross-border payment solutions tailored for financial institutions. Its flagship service, RippleNet, connects banks, payment providers, and cryptocurrency exchanges through a decentralized network, utilizing XRP for On-Demand Liquidity (ODL) to process transactions without requiring pre-funded accounts.

Since its inception in 2012, Ripple has solidified its position as a leading player in cross-border payments. By Q4 2022, RippleNet had facilitated over 2 billion transactions worth approximately $30 billion in cumulative volume, with participation from over 300 financial institutions and payment providers worldwide. This extensive track record and global network firmly establish Ripple as a stalwart in the payment sector.

At first glance, Huma Finance might appear to be a smaller player in comparison. However, we believe Huma possesses the potential to challenge or even rival Ripple, thanks to its differentiated strategies and unique technological strengths, which are steadily enhancing its competitive edge.

One of Huma’s most significant differentiators lies in its chain-agnostic architecture. While Ripple operates on its own proprietary blockchain, Huma embraces a multi-chain approach, seamlessly integrating with various blockchain ecosystems. This strategy positions Huma as an “open-stack version of Ripple,” offering technological flexibility and fostering a broader user and developer base across multiple networks.

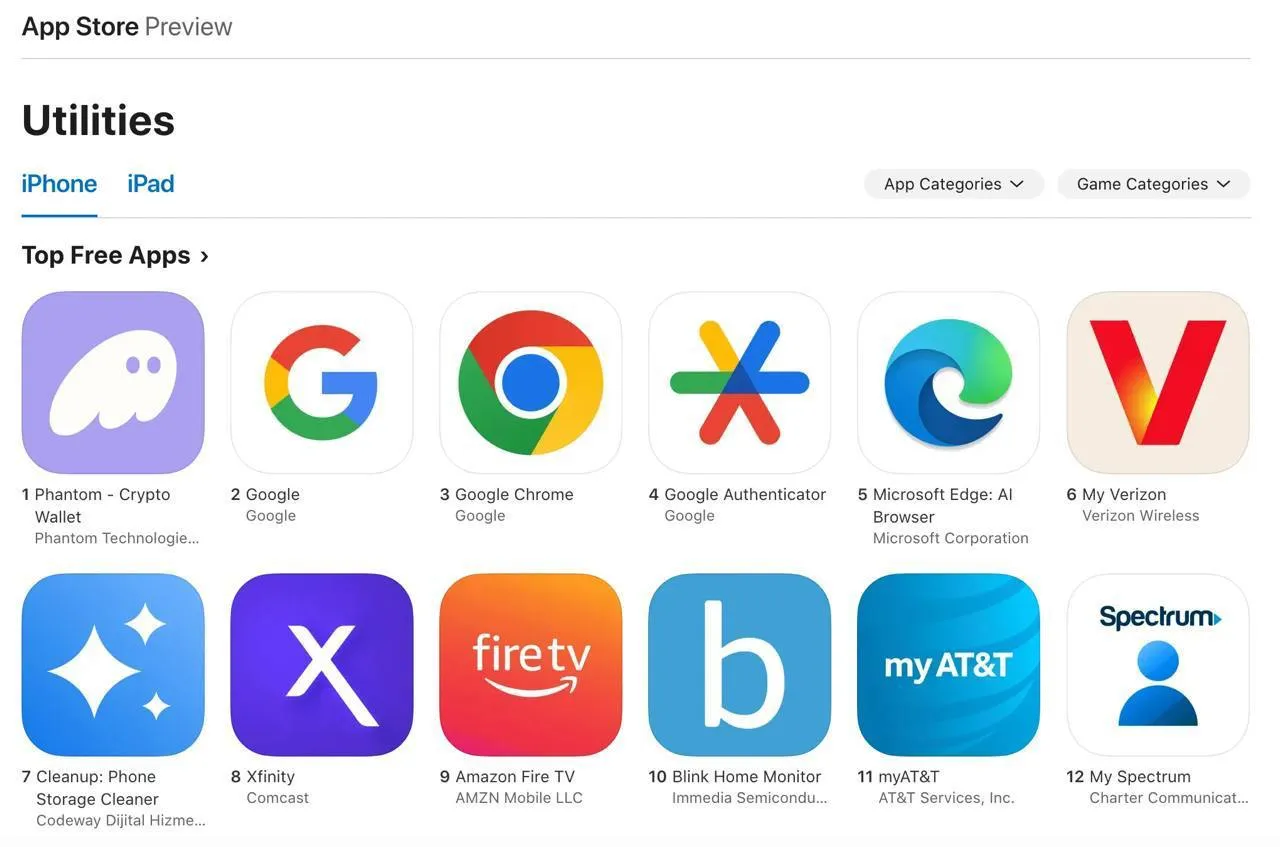

For instance, Huma recently expanded to Solana, one of the most active blockchain ecosystems as of November 2024. Solana outpaces Ethereum in DEX trading volume, achieving over $45.5 billion in weekly transaction volume—more than three times that of Ethereum. Furthermore, Phantom, a popular Solana wallet, ranked #1 in the Apple App Store’s utility category as of Nov 22, 2024, reflecting high user engagement. By integrating with such a vibrant ecosystem, Huma gains a substantial advantage in scalability and user acquisition.

Source: Apple App Store

Huma’s strategic decision to forego developing its own blockchain enables it to channel all resources into fine-tuning and scaling its services. Building and operating a proprietary blockchain entails considerable costs and resources, often resulting in a diluted focus and potential trade-offs in service quality. By leveraging existing infrastructure, Huma avoids these pitfalls and ensures its efforts remain fully concentrated on delivering world-class payment financing solutions.

The difference between Ripple and Huma’s approach to stablecoins further underscores this point. While Ripple launched its own stablecoin, RLUSD, in October 2024 as part of its strategy to build a standalone financial system, Huma distinguishes itself by partnering with globally compliant stablecoins such as USDC and PYUSD. This strategy enables Huma to efficiently leverage established on- and off-ramp networks, avoiding the need to construct foundational infrastructure from the ground up.

Ultimately, Huma’s open-stack approach underscores its strategic emphasis on collaboration with mature ecosystems, allowing it to concentrate resources on user experience and market growth. Compared to projects that attempt to build everything independently, Huma gains a distinct advantage in execution speed and scalability, showcasing a well-defined strategy for achieving a competitive edge in the market.

In terms of risk management, Huma’s innovative approach sets it apart from other on-chain financing platforms. For example, while Maple Finance employs a centralized model using delegates for risk management, Huma relies on decentralized signal processors and Evaluation Agents to analyze income and asset data, automating credit scoring and risk evaluation. This decentralized model enables precise risk assessment and provides on-chain transparency, earning trust from investors. Huma’s portfolio primarily comprises fiat-backed assets or short-duration assets maturing within days, reducing liquidity risk and allowing for faster capital rotation. Unlike Maple, Centrifuge, and Goldfinch, which have faced multiple defaults, Huma boasts a 0% default rate since its inception, underscoring its robust risk management framework.

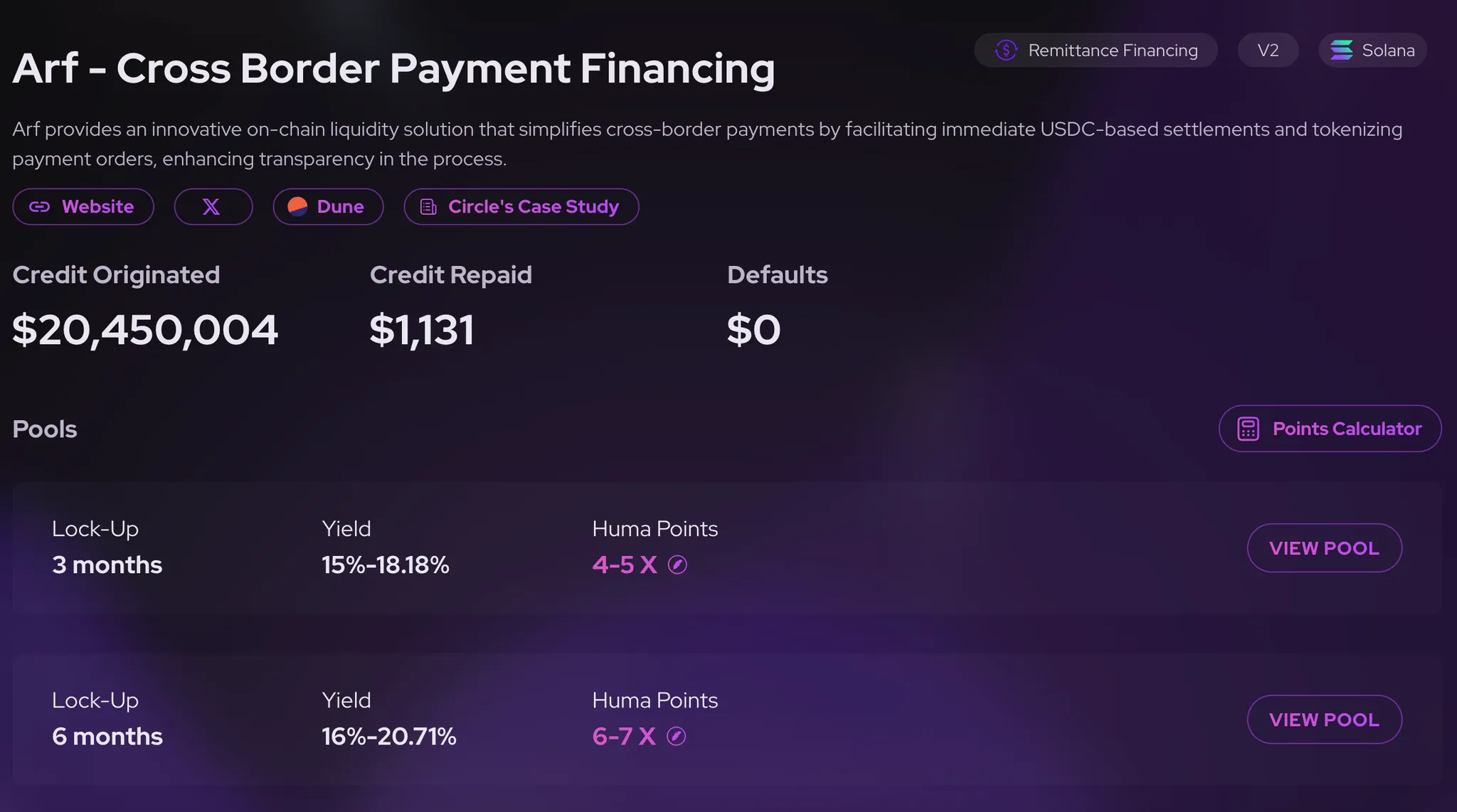

The April 2024 merger with Arf, a cross-border payment platform, further bolstered Huma’s competitive position. By eliminating the need for pre-funded accounts in the traditional SWIFT network, Huma freed approximately $4 trillion in liquidity, enabling transparent, low-cost, stablecoin-based payments. This system connects borrowers and investors more efficiently, laying the groundwork for an advanced PayFi network.

Lastly, Huma stands out by offering high real yields to its investors. For instance, in its current Solana-based campaign, Huma’s three-month lock-up pools offer annual yields (APY) of 15% for senior tranches and up to 24% for junior tranches. Six-month lock-up pools offer even higher rates, with senior tranches yielding 16% APY and junior tranches reaching up to 24.71% APY. These attractive yields are made possible by transaction fees of 8–10 basis points charged to institutional clients using Huma’s liquidity and cross-border payment services. Despite these relatively high fees, Huma’s services remain faster, cheaper, and more efficient than traditional SWIFT-based solutions, making them highly appealing to institutional clients.

Source: Huma Finance

Building on these distinguishing features, Huma Finance has demonstrated remarkable growth, as evidenced by its standout on-chain metrics. Within approximately two years of its launch, the platform has surpassed $2.3 billion in cumulative on-chain transaction volume. This figure includes $1.2 billion in total loans issued and $1.1 billion in repayments, underscoring Huma’s operational stability, particularly given its impressive 0% default rate while maintaining a balance between loans and repayments.

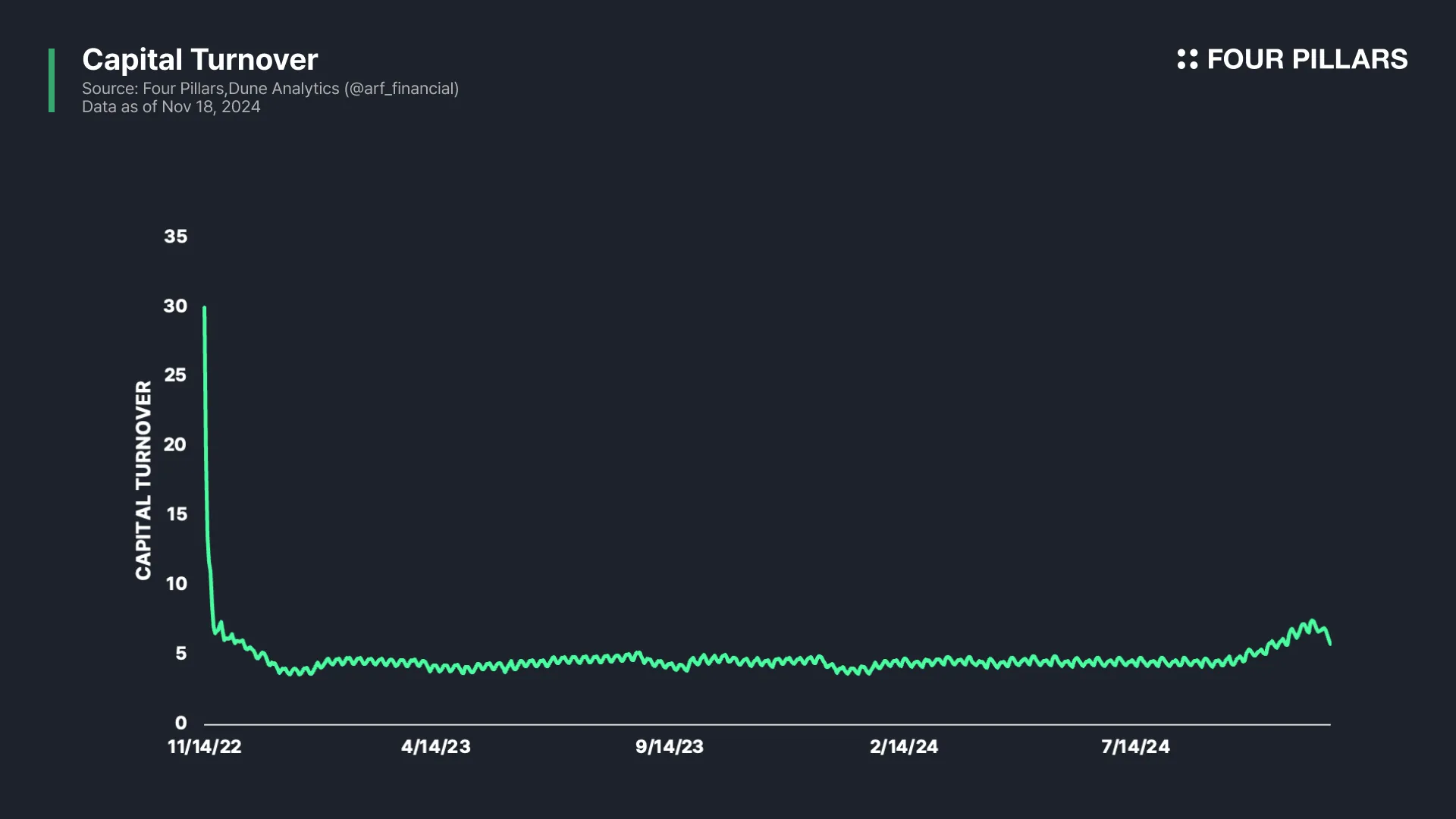

Huma Finance’s monthly capital turnover ratio stands at approximately 5.78 as of Nov 18, 2024, indicating that capital deployed for loans circulates through the platform an average of 5.78 times per month. In traditional financial analysis, capital turnover measures the efficiency with which deployed capital generates revenue. In Huma’s case, this metric emphasizes the velocity of loan capital circulation, reflecting the platform’s liquidity utilization efficiency.

This high capital turnover ratio highlights the platform’s competitive edge in two key aspects. First, from the perspective of liquidity providers (LPs), a high turnover ratio signals effective utilization of capital, offering reassurance about the stability of their investments. LPs favor platforms where capital does not remain idle but instead circulates consistently, generating returns. Second, for borrowers, rapid capital circulation demonstrates the platform’s capacity to promptly meet borrowing demands. This responsiveness enhances Huma’s appeal as a lending platform, helping to expand its user base in the highly competitive DeFi market.

In conclusion, Huma Finance’s on-chain performance is not merely a testament to its rapid growth but also to its operational stability and capital efficiency. These achievements reinforce the platform’s competitive position, demonstrating its ability to carve out a differentiated niche in the PayFi market.

Amid the frenzy surrounding memecoins, Huma Finance’s business model may initially appear understated. Yet, it is precisely such projects that highlight blockchain’s true potential—going beyond speculative trends to deliver substantial and meaningful transformation.

Building on its early successes, Huma now stands at a pivotal juncture, honing its services and expanding its ecosystem. On November 13, 2024, Huma completed its chain expansion to Solana, a blockchain rapidly establishing itself as a cornerstone of the crypto market. This milestone is expected to significantly enhance on-chain activity and drive broader adoption of its services. Furthermore, partnerships with global payment networks like Stellar hold the promise of extending Huma’s impact to financially underserved regions.

The anticipated token launch in 2025 is another major development on the horizon. More than just a growth driver for the protocol, the token is set to unlock innovative use cases across the ecosystem, generating significant value.

Huma Finance is emerging as more than a technological innovator—it is a force for tangible, sustainable change where it is most needed. As Huma continues to innovate and redefine the traditional financial landscape, its transformative journey is only just beginning.

Dive into 'Narratives' that will be important in the next year