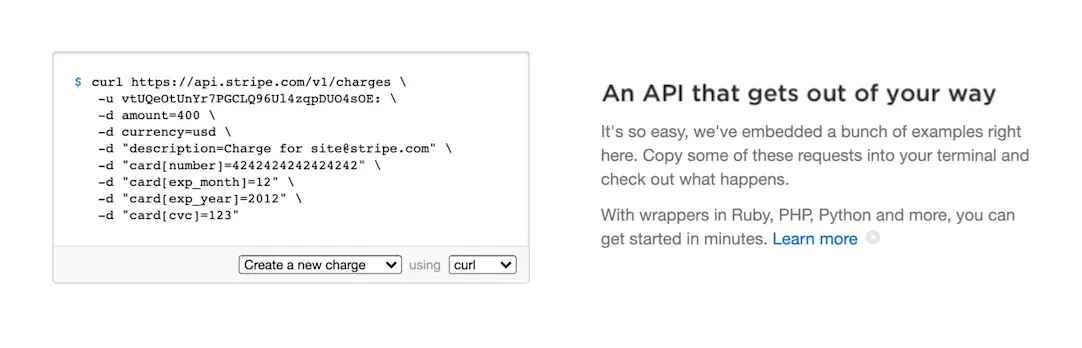

The seven lines of code symbolize Stripe’s core identity. By enabling businesses to integrate online payments with just a few lines of code, Stripe revolutionized the online payments market.

Recently, Stripe has been aggressively expanding its presence in the stablecoin space through strategic acquisitions and new product integrations. Most notably, its Tempo network, developed in partnership with Paradigm, surprised the industry by securing $500 million in funding.

Stripe’s stablecoin-focused strategy could redefine the payments paradigm. In the legacy financial system, Stripe played only a secondary role as a PSP, but in the stablecoin payments market, it can take on all key roles such as issuing bank, card network, and acquiring bank.

While we all engage in financial activities, most people have no idea what ACH, SEPA, SWIFT, VisaNet, or RTGS are. Stripe has the potential to drive mass adoption of blockchain-based stablecoin payments through Tempo, and if a world arrives where stablecoin payments become mainstream, Stripe will be at its center.

Source: Stripe, Wayback Machine

The screenshot above shows an example code snippet from Stripe’s website in 2011. Excluding a few optional lines of code, developers could integrate Stripe’s payment API into their product with just seven lines of code. (Today, Stripe supports even shorter API calls across various languages for basic integrations.)

Before Stripe’s arrival, online payment infrastructure came with numerous limitations and inconveniences. To accept credit card payments online, businesses had to apply for a merchant bank account, a process that could take several weeks or even months. While PayPal existed before Stripe, Stripe offered a far more developer-friendly environment, reinventing the very experience of enabling businesses to easily receive payments online.

Those seven lines of code turned Stripe into one of the most successful online payment infrastructure companies in the world. In 2024, Stripe processed $1.4 trillion in total payment volume (TPV), representing about 1.3% of global GDP. In early 2024, Stripe was valued at approximately $65 billion, and by early 2025, its valuation had risen sharply to about $91.5 billion, making it one of the largest fintech companies in the world. For reference, PayPal’s market capitalization is around $64 billion.

Source: Stripe

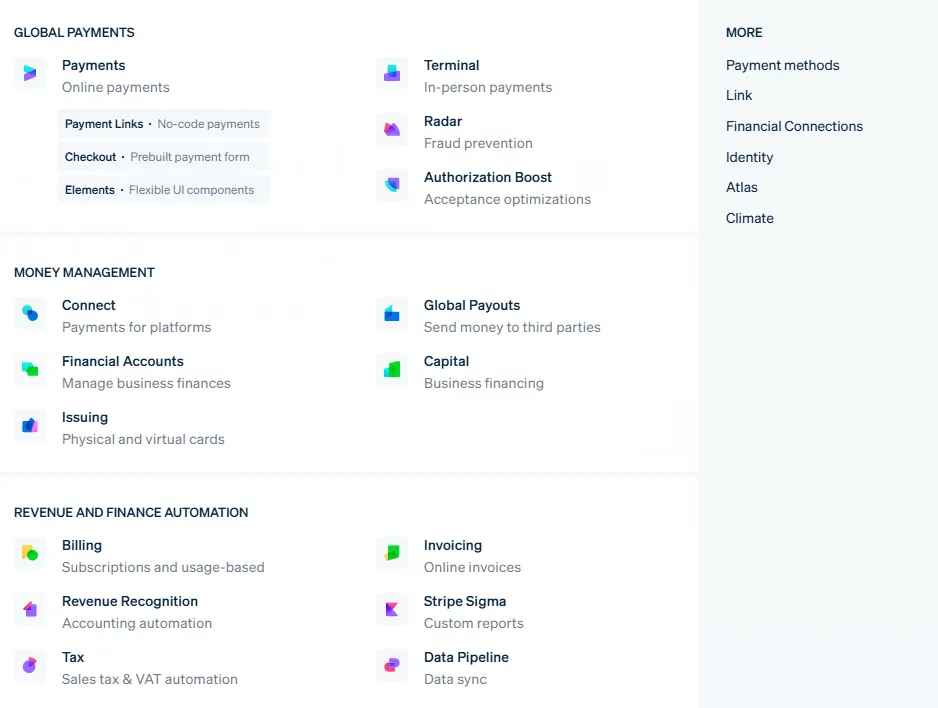

Just like early Stripe, the core of today’s Stripe still revolves around developer-friendly APIs that make it easy to adopt various payment methods online. However, Stripe has evolved into a company that innovates across the entire financial infrastructure stack, offering a wide range of products.

Stripe’s products can be broadly categorized into three groups: 1) Global Payments, 2) Money Management, and 3) Revenue and Finance Automation.

1.2.1 Global Payments

Payments: Stripe’s core functionality allows developers to integrate payment services into their products through a single API while supporting diverse global payment methods. “Payments” not only provides a simple payment interface but also includes features like “Payment Links,” “Checkout,” and “Elements” to optimize UI/UX, as well as tools like “Radar” and “Authorization Boost” that leverage AI.

Terminal: Enables merchants to manage both online and offline payments within a single system, supporting not only Stripe’s own hardware but also third-party card readers.

Radar: An AI-powered fraud detection solution that uses Stripe’s global payment data to identify and prevent suspicious transactions in real time.

Authorization Boost: An AI-based solution that detects false declines and retries transactions to increase payment approval rates.

1.2.2 Money Management

Connect: A B2B solution for platforms and marketplaces that enables them to build their own payment and payout systems. Leading platforms like Shopify and DoorDash use “Stripe Connect” to power their payment infrastructure. Businesses can onboard numerous merchants and customers without worrying about taxes, global payment methods, reporting, or compliance complexities.

Global Payouts: A solution that allows businesses to send money to anyone (customers, sellers, or third parties) in their local currencies.

Financial Accounts: Stripe-provided financial accounts for platform operators and businesses, enabling a wide range of financial activities such as payments, transfers, FX, lending, and stablecoin usage within a single dashboard.

Capital: A lending solution that allows businesses to easily receive financing from Stripe, with automatic repayments made as a portion of daily sales.

Issuing: A card program that enables companies and platforms to issue both virtual and physical cards under their own brand.

1.2.3 Revenue and Finance Automation

Billing: Supports and automates various recurring payment models, including subscription and usage-based pricing.

Invoicing: A solution for creating and sending invoices via email and collecting payments through multiple payment methods.

Revenue Recognition: Handles the complex accounting of recurring revenues (such as subscriptions) automatically, in compliance with standards like ASC 606 and IFRS 15.

Stripe Sigma: A reporting tool that lets businesses analyze their payment and subscription data within Stripe using SQL or natural language queries, enabling real-time financial insights.

Tax: Automatically calculates, collects, and reports taxes such as sales tax, VAT, and GST for payments processed through Stripe, including support for global tax rules.

Data Pipeline: An infrastructure tool that automatically syncs Stripe data with external data warehouses such as Snowflake and Redshift.

1.2.4 Others

Financial Connections: Allows quick linking and verification of customers’ bank accounts and financial data, reducing issues like failed payments and verification delays.

Identity: An online KYC/AML solution that reduces fraud risk and supports compliance during customer onboarding flows.

Atlas: Helps startups easily incorporate a Delaware-based U.S. entity and start accepting payments through Stripe.

Climate: Enables businesses to automatically contribute a portion of their revenue to climate change mitigation projects.

Today, many people can easily access online and offline payments, but that convenience exists only because fintech companies like Stripe have revolutionized the financial front end. The financial back end, however, remains outdated and inefficient, leading to the following problems:

Inefficient Cross-Border Payments: Although Stripe supports global payments with multiple currencies and payment options, the settlement back end still involves numerous intermediary banks, the SWIFT network, and national payment systems, resulting in significant inefficiencies.

AI Agent Payment Support: AI agents do not possess legal identities, which means they cannot access legitimate online payment methods such as bank accounts or cards.

Micropayments: When micropayments are processed through traditional card networks or payment systems, transaction fees become disproportionately high relative to the transaction size, making practical micropayment support impossible.

Fragmented Financial Systems: Current financial back ends, including card networks, remittance systems, and securities networks, are all fragmented by purpose and lack interoperability.

The technology that can solve all these problems is blockchain. Blockchain functions as a universal ledger, enabling all financial activities to be processed in one place regardless of borders. It can also enable previously impossible features such as AI agent payments and micropayments.

Among fintech companies, Stripe was one of the first to recognize the potential of blockchain and cryptocurrencies and to integrate them into its products. In 2014, Stripe became the first payment company to support Bitcoin payments, though it ended Bitcoin payment support in 2018. The main reason for discontinuing Bitcoin payments was that Bitcoin had come to be viewed more as a store of value than as a medium of exchange.

However, Bitcoin is not the only way to innovate payments using blockchain technology. Stablecoins, in particular, can serve this role. A stablecoin is a token on the blockchain pegged to the value of fiat currency, offering the potential to revolutionize the back end of Web2 payments using blockchain infrastructure.

Stripe has not missed the opportunity presented by stablecoins and has recently been among the most aggressive companies in this space. Starting with the acquisition of the stablecoin infrastructure company Bridge, Stripe went on to acquire Privy, a Web3 wallet infrastructure firm, and has since integrated stablecoin-related features into its products, rapidly expanding into stablecoin payments.

Examples of Stripe products that now support stablecoin-related services include:

Payments: Businesses can accept payments for online services and products in stablecoins.

Payouts: Enables faster global transfers to customers, sellers, and creators using stablecoins instead of traditional banks.

Crypto Onramp: Allows customers to purchase cryptocurrencies through various payment methods and use them within a platform.

Issuing: A service that helps businesses easily issue compliant stablecoin debit cards to their customers.

Financial Accounts: Businesses can manage both fiat currencies and stablecoins within the same financial account service. The platform connects to both traditional networks like ACH and SEPA as well as eight blockchain networks, allowing seamless management of fiat and crypto assets.

Open Issuance: A platform that enables businesses to issue and manage their own branded stablecoins in compliance with regulations.

Tempo: A high-performance EVM Layer 1 network currently being developed by Stripe for stablecoin payments and applications.

In summary, Stripe enables businesses to use stablecoins for faster and more cost-efficient payments and remittances, manage them seamlessly alongside fiat currencies, and even issue their own stablecoins. In essence, Stripe is becoming a powerful stablecoin infrastructure company that supports every stage of the stablecoin value chain—from issuance to utilization.

Many Web2 fintech companies are now introducing blockchain and stablecoin features. In this environment, what makes Stripe truly different?

I believe the answer lies in Tempo. Whereas Stripe once played an auxiliary role in the payment process as a PSP (Payment Service Provider), with Tempo and stablecoin integration, Stripe is transforming into a full-stack payment platform that can handle every stage of the payment lifecycle.

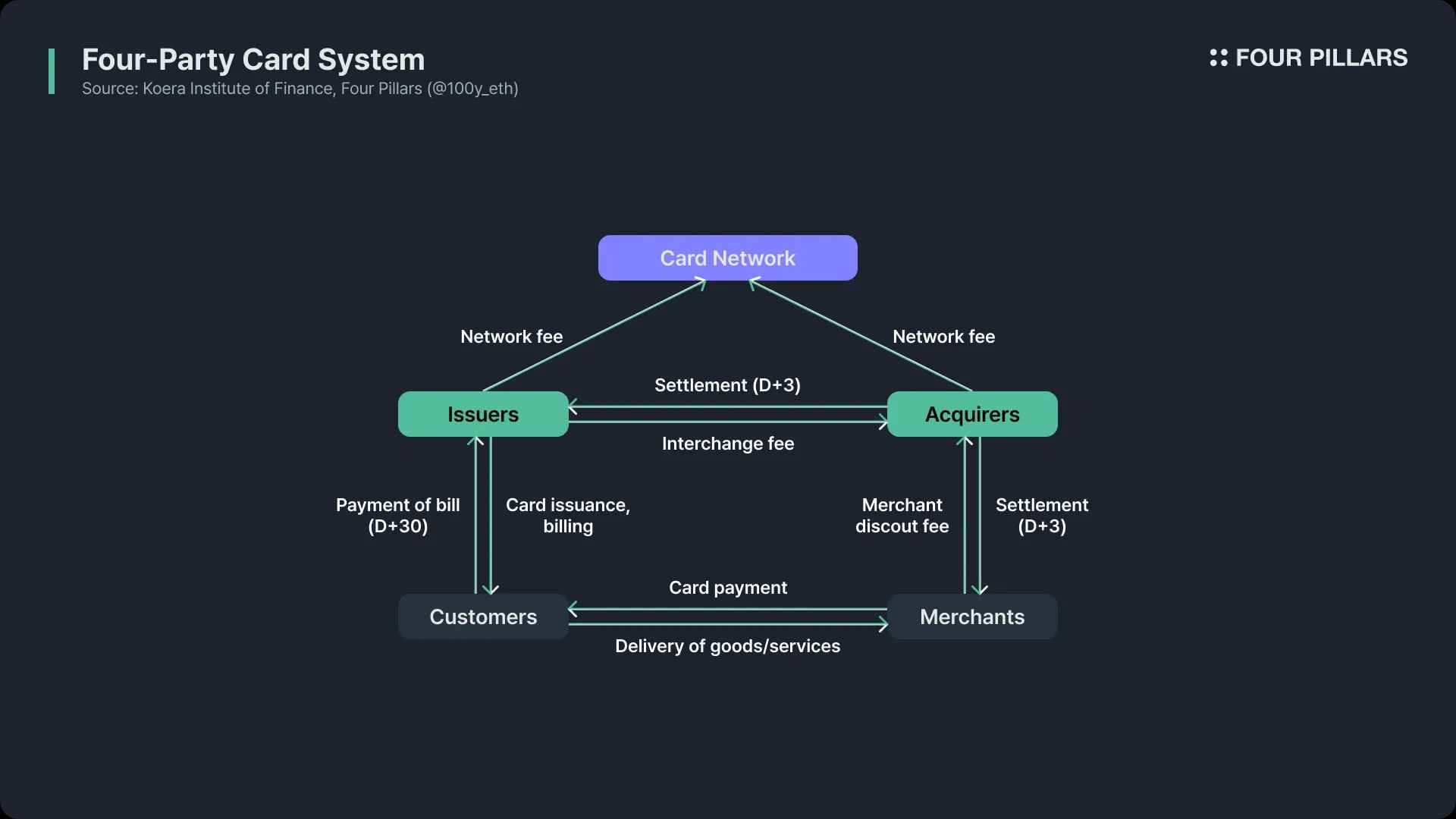

In the traditional card payment infrastructure, the key entities involved in processing payments are:

Issuing banks, which issue cards and manage customer funds,

Acquiring banks, which handle settlements for merchants, and

Card networks, which connect issuing and acquiring banks.

Technically, payments can be processed without PSPs like Stripe, but for businesses and merchants, integrating various cards and payment options individually is extremely inefficient. That is why many businesses and merchants rely on PSPs like Stripe to simplify payments. In other words, PSPs play a supplementary rather than a central role in the payment process.

However, if Stripe continues to aggressively adopt stablecoin functionalities and launches Tempo, its role in the payments market could change completely. Stripe could evolve from a supporting player into a central payment institution that manages every part of the process:

Acquiring: Stripe already plays a quasi-acquiring role by partnering with acquiring banks to provide settlement services to businesses and merchants. Recently, Stripe applied for and received approval from the Georgia Department of Banking and Finance for a MALPB license, signaling its intention to operate as an acquiring bank itself. If Stripe supports stablecoin-based settlement on the back end, it could synergize with its “Financial Accounts” product and effectively function as an acquiring bank.

Card Network: When card payments occur through Stripe, transactions are currently processed via external networks like Visa and Mastercard. Once Tempo is launched and stablecoin payments are processed on Tempo, it can effectively take on the role of a card network itself.

Issuing: Stripe already enables businesses to easily issue fiat and crypto-based cards through its “Issuing” feature. If Stripe further leverages Privy’s capabilities to let end users easily open wallets, the Stripe platform could effectively operate as an issuing bank.

Others: Tempo is a blockchain optimized for stablecoin use and emphasizes AI agent payments and micropayments as core features. In other words, Tempo has the potential to enable entirely new areas that the existing Web2 financial infrastructure cannot support.

Tempo’s emergence is not entirely new. Before its debut, networks like Stable (a USDT-focused chain) had already launched, and Circle, the issuer of USDC, also introduced Arc, a chain dedicated to USDC. All these stablecoin-focused chains share similar selling points, such as low and predictable fees, privacy features, and high scalability.

Tempo is often compared to Circle’s Arc because it is being developed by Stripe, a company that operates under U.S. regulatory compliance. However, its starting point is fundamentally different. Circle, as a stablecoin issuer, must newly onboard businesses and merchants to adopt Arc for real-world payments and financial use. In contrast, Stripe already has a powerful network effect built over more than a decade.

From the moment Tempo was announced, Stripe revealed partnerships with global companies and banks including Anthropic, Coupang, Deutsche Bank, Lead Bank, Nubank, OpenAI, Revolut, Shopify, Standard Chartered, and Visa. On the Web3 side, it is also incubated by Paradigm, one of the most highly regarded venture capital firms in the crypto industry. As a result, Stripe already has strong networks across both Web2 and Web3 ecosystems.

This extensive network is one of Tempo’s greatest differentiators compared to Arc, and it significantly increases the likelihood that Tempo will achieve real mass adoption upon launch.

In today’s payment industry, we live in the era of Visa and Mastercard. I would argue that in the future, when stablecoin payments become mainstream, everyone will end up using Stripe. The reasons are as follows:

In the legacy financial system, Stripe’s role was limited to that of a PSP, but in the stablecoin payments market, it can handle the entire payment process from start to finish.

Stripe’s developer-friendly DNA enables it to abstract complex stablecoin systems in a way that allows users to integrate blockchain functionality into services without even realizing they are using it.

Stripe’s powerful and expanding network will make mass adoption of stablecoin payments possible.

Today, we all use financial systems daily, yet most people have no idea what ACH, SEPA, SWIFT, VisaNet, or RTGS are. Stripe has the potential to lead the mass adoption of blockchain-based stablecoin payments through Tempo and beyond. If a world arrives where stablecoin payments become the norm, Stripe will undoubtedly be at its center.

Dive into 'Narratives' that will be important in the next year